Anti-Acne Dermal Patch Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

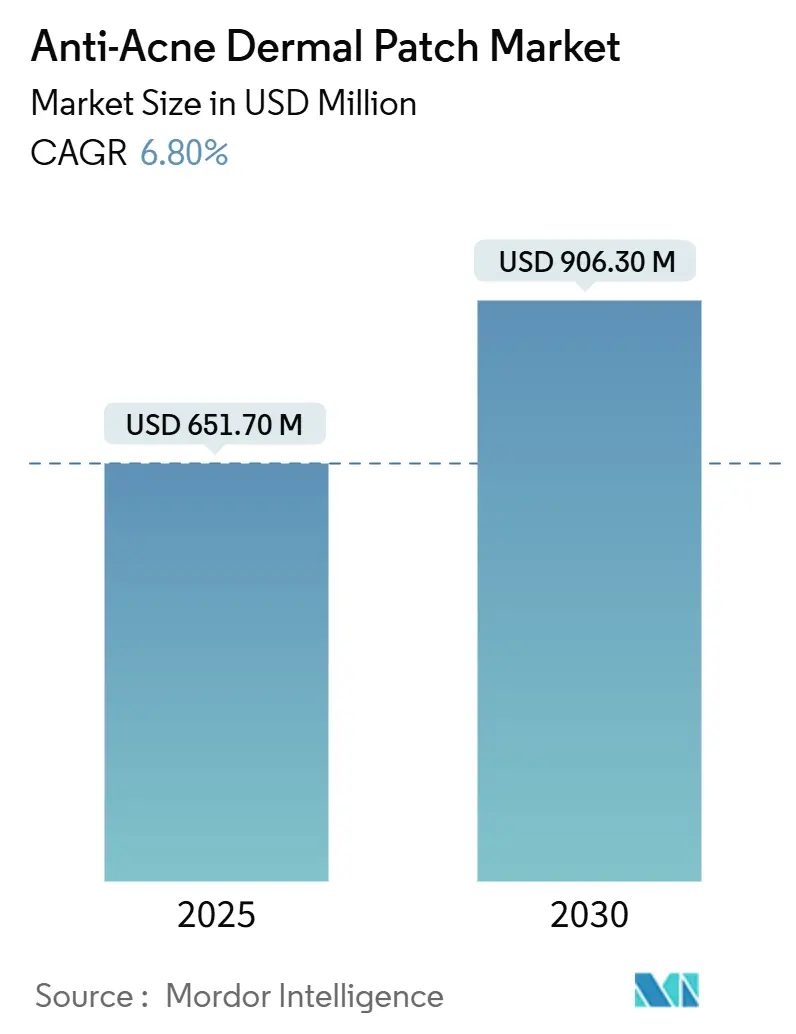

| Market Size (2025) | USD 651.70 Million |

| Market Size (2030) | USD 906.30 Million |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

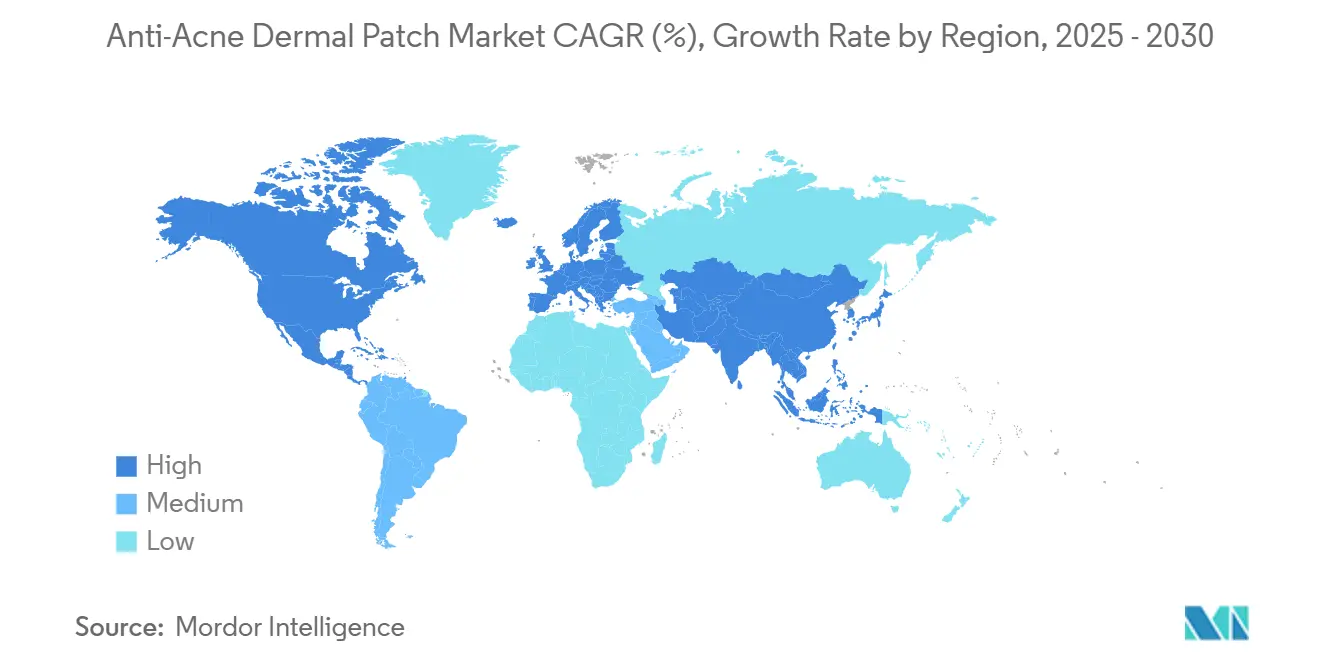

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Acne Dermal Patch Market Analysis by Mordor Intelligence

The anti-acne dermal patch market size stood at USD 651.7 million in 2025 and is projected to climb to USD 906.3 million by 2030, reflecting a 6.8% CAGR over the forecast window. A convergence of social-media visibility, hydrocolloid material innovation, and growing consumer appetite for non-invasive care is sustaining the growth trajectory. Patches have migrated from a discreet overnight remedy to an openly worn accessory, especially among Generation Z, turning skin-care compliance into a form of personal expression. Normalization of visible treatment has also widened the addressable audience, encouraging established consumer-goods companies to fast-track acquisitions and partnerships.

Key Report Takeaways

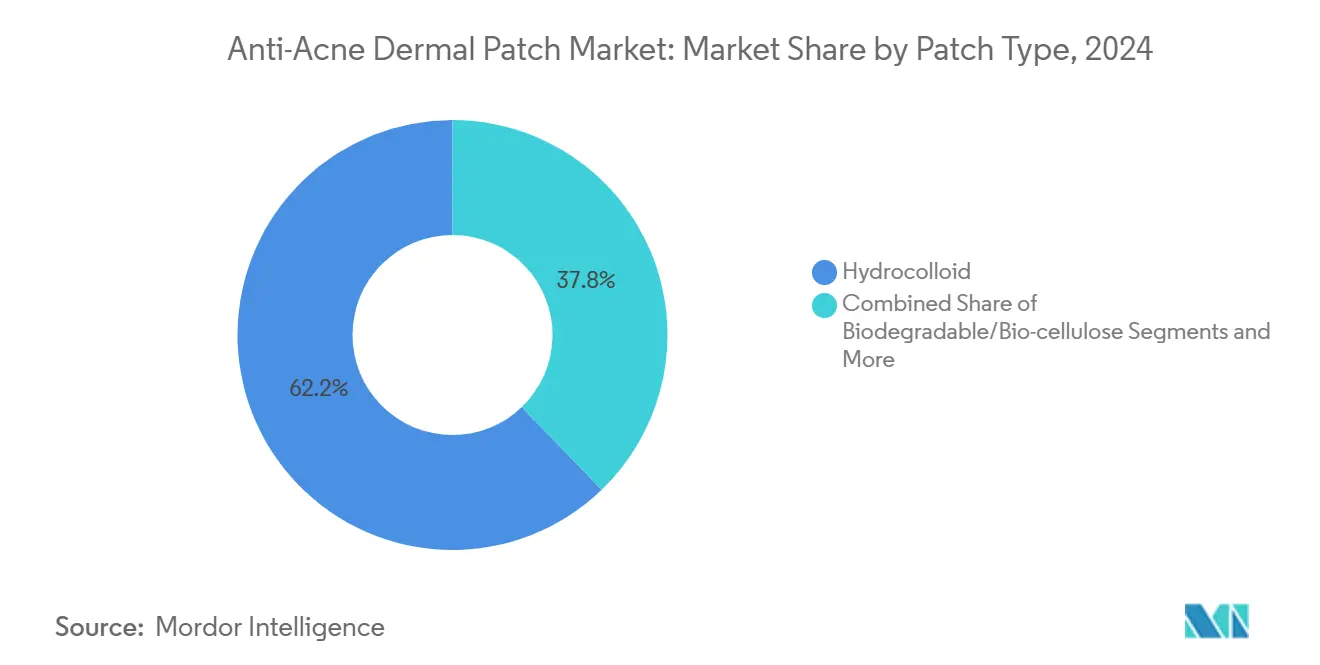

- By patch type, hydrocolloid captured 62.2% of anti-acne dermal patch market share in 2024; microneedle variants are forecast to advance at a 10.8% CAGR through 2030.

- By ingredient, salicylic acid held 48.6% of the anti-acne dermal patch market size in 2024, while herbal actives are positioned to expand at a 9.6% CAGR to 2030.

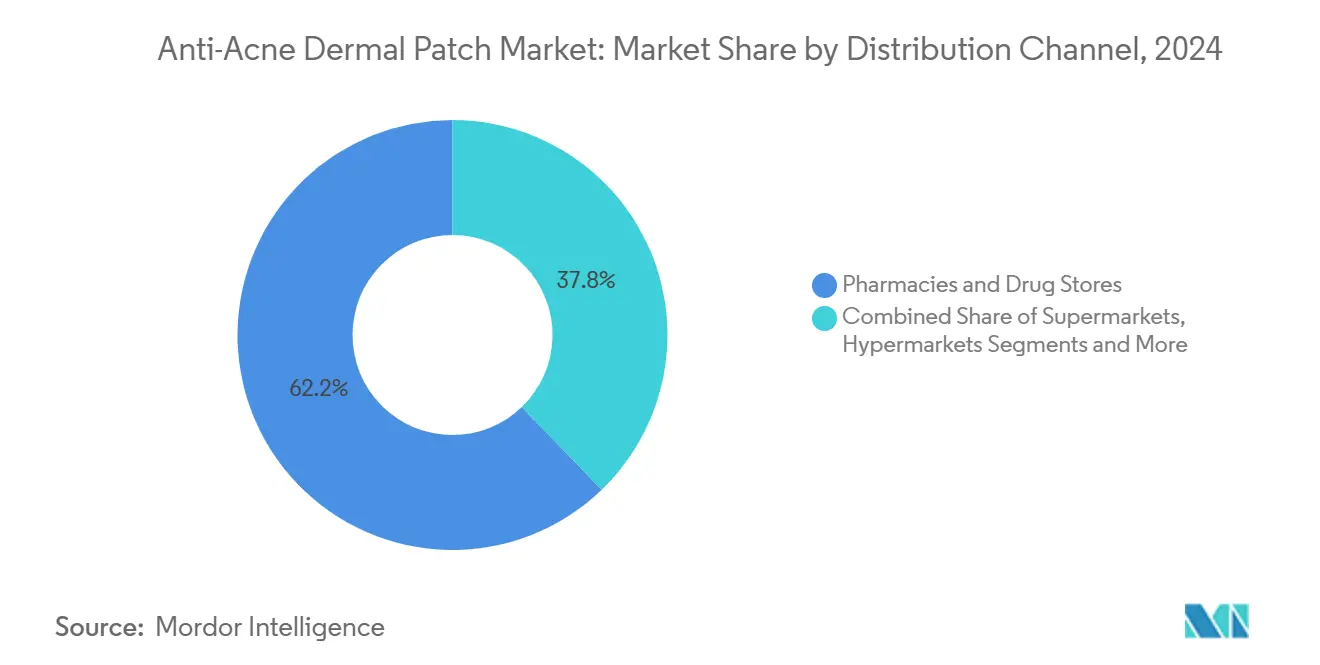

- By distribution channel, pharmacies retained 38.3% revenue share in 2024, whereas e-commerce is tracking an 11.5% CAGR to 2030.

- By geography, Asia Pacific accounted for 39.2% of the anti-acne dermal patch market share in 2024 and is on course for an 8.1% CAGR through 2030.

Global Anti-Acne Dermal Patch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social-media-led K-beauty adoption surge | +1.20% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| E-commerce penetration in dermo-cosmetics | +0.90% | Global, peak growth in Asia Pacific and North America | Medium term (2-4 years) |

| Hydrocolloid material cost decline | +0.70% | Asia Pacific manufacturing hubs, global distribution | Medium term (2-4 years) |

| Microneedle IP expiries | +0.60% | North America and European Union | Long term (≥ 4 years) |

| Growing male-grooming spend in Asia Pacific | +0.50% | Asia Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| AI-powered personalized subscription models | +0.40% | North America and European early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Social-Media-Led K-Beauty Adoption Surge

Korean beauty culture boosted patch visibility, shifting them from a nighttime fix to a daytime accessory. TikTok search volumes for K-skincare terms in the United States jumped over 180% during 2024, signaling mass cultural crossover. Brands leaned into eye-catching shapes and bright colors that transform treatment into self-expression, fostering positive skin conversations instead of concealment. COSRX’s daily global sales cadence—one patch pack sold every 25 seconds—illustrates commercial upside when solution messaging is paired with playful aesthetics.[1]Heta Chhabhaiya et al., “Navigating the Skincare Journey: Analysing the Effectiveness of COSRX’s Global Marketing Strategy,” Journal of Development Research, drj.ves.ac.in Continuous influencer engagement keeps the trend sticky, encouraging incumbents to refresh designs and maintain social relevance.

E-Commerce Penetration in Dermo-Cosmetics

Direct-to-consumer storefronts slash pharmacy mark-ups and collapse discovery barriers by offering ingredient explainers, usage videos, and peer reviews in a single scroll. Hero Cosmetics validated the model with an online-first roll-out that converted early adopters into repeat buyers before moving into brick-and-mortar. Mobile checkout now accounts for more than two-thirds of online beauty orders, demonstrating how one-click convenience and discreet delivery resonate with younger shoppers. Subscription bundles drive retention by predicting replenishment cycles and offering marginal savings without eroding premium positioning. As marketplaces refine search algorithms, visibility hinges on consumer-generated ratings and brand storytelling rather than shelf placement.

Hydrocolloid Material Cost Decline Due to Local Sourcing

Regionalizing hydrocolloid production trims transport outlays and buffers supply shocks. Chinese and Korean manufacturers quote ex-works prices below USD 0.10 per unit, widening private-label margins while letting premium brands invest in differentiated packaging. The broader pharmaceutical-grade hydrocolloids segment is tracking low-single-digit cost deflation, benefiting patch makers that lock in volume contracts. ISO 13485:2016 certification has become the de facto entry criterion for export-ready factories, aligning quality standards across borders. With raw-material volatility tempered, brand owners can redirect savings into marketing or R&D without raising shelf prices.

Microneedle IP Expiries Enabling Private-Label Entry

Several foundational microneedle patents are lapsing, unlocking options for new entrants to repurpose the delivery platform for over-the-counter acne care. FDA’s Class I device route accelerates market clearance versus drug pathways, and academic prototypes using carbon masters underscore scalable manufacturing. As tooling costs fall, retailers are lining up exclusive ranges that marry hydrocolloid bases with dissolving micro-darts to justify premium shelf sets. Brands must still demonstrate puncture safety and ingredient stability, but IP democratization is set to broaden consumer choice and drag down unit economics over the back half of the decade.[2]Seung-Kyung Kang, “Fully Biodegradable Electrochromic Display for Disposable Patch,” Nature, nature.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Grey Zone Between Cosmetic & OTC Drug In The EU | -0.80% | EU regulatory zones, spillover to aligned markets | Short term (≤ 2 years) |

| Patch Disposal & Micro-Plastic Concerns | -0.60% | Global, concentrated in environmentally conscious regions | Medium term (2-4 years) |

| Ingredient-Induced Contact Dermatitis Incidents | -0.50% | Global, higher impact in sensitive skin demographics | Short term (≤ 2 years) |

| Diminishing Novelty Factor In Mature Markets | -0.40% | North America & EU mature markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Grey Zone Between Cosmetic & OTC Drug in the EU

Acne patches containing active ingredients straddle EU definitions that separate cosmetics from over-the-counter drugs. Divergent labeling rules and dossier demands raise compliance costs, tilting the playing field toward multinational incumbents with in-house regulatory teams. U.S. FDA labeling rules under 21 CFR 333.350 further complicate harmonized packaging for trans-Atlantic launches.[3]U.S. Food and Drug Administration, “21 CFR 333.350 — Labeling of Acne Drug Products,” ecfr.govSmaller firms either limit formulas to hydrocolloid-only constructions or restrict sales to single jurisdictions, slowing innovation cycles and market entry velocity.

Patch Disposal & Micro-Plastic Concerns

Single-use formats contribute to the 120 billion cosmetic packaging units generated annually, triggering consumer pushback in regions with rising eco-regulation. Scientific reviews link non-degradable polymers to microplastic accumulation, elevating demand for bio-cellulose or chitin-based substrates that decompose within eight weeks. Early adopters accept moderate price premiums, yet mass market conversion hinges on narrowing cost gaps through material science breakthroughs and scale efficiencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Patch Type: Hydrocolloid Dominance Drives Innovation

Hydrocolloid patches commanded 62.2% of anti-acne dermal patch market share in 2024, underscoring their clinical heritage in moisture-balanced wound care. The segment represents the core of the anti-acne dermal patch market size and maintains steady mid-single-digit growth by bundling proven efficacy with playful designs. Microneedle formats, though starting from a low base, are set to post a 10.8% CAGR through 2030 as intellectual-property expiries cut barriers and retailers champion premium SKUs.

Hybrid architectures pairing hydrocolloid backings with micro-arrays promise faster ingredient infusion without forfeiting occlusion benefits. Waterproof hydrogel and reusable silicone options cater to sport and eco-minded niches, respectively. Research into fully biodegradable electrochromic displays hints at future convergence between treatment and wearable tech, allowing users to track active release visually. Regulatory clarity—Class I for hydrocolloid, more stringent dossiers for microneedles—will continue to shape brand portfolios.

By Ingredient Type: Salicylic Acid Leadership Faces Herbal Challenge

Salicylic acid held 48.6% of the anti-acne dermal patch market size in 2024, benefiting from a monograph status that simplifies label claims and reassures dermatologists. Its keratolytic action clears clogged pores without the bleaching risk tied to benzoyl peroxide, securing continued formulary preference. Herbal actives are pacing at a 9.6% CAGR, riding clean-beauty sentiment and consumer wariness of synthetic chemicals.

Tea-tree oil patches appeal to users seeking natural antimicrobial benefits, while hydrocolloid-only discs serve those prioritizing mechanical extraction. Regulatory ceilings remain: the FDA only sanctions five actives—salicylic acid, benzoyl peroxide, resorcinol, resorcinol monoacetate, and sulfur—for OTC acne applications. Brands respond by layering supportive botanicals under cosmetic claims rather than therapeutic ones, walking a tightrope between efficacy messaging and regulatory compliance.

By Distribution Channel: E-Commerce Disrupts Pharmacy Dominance

Pharmacies commanded 38.3% of the anti-acne dermal patch market share in 2024 thanks to pharmacist recommendations and immediate availability, yet their growth arc is lagging. E-commerce posted an 11.5% CAGR, eroding brick-and-mortar barriers and extending reach to consumers in regions with sparse retail infrastructure. The channel’s coupon stacking, same-day delivery, and auto-ship programs drive repeat purchases, while detailed ingredient filters empower informed decision-making.

Supermarkets and hypermarkets offer convenience for pantry restockers, whereas dermatology clinics endorse medical-grade SKUs, validating clinical efficacy claims. Specialty beauty outlets round out the mix by curating design-forward patches that double as statement accessories. An omnichannel future is emerging, with brands unifying inventory and pricing across touchpoints to ensure seamless shopping journeys.

Geography Analysis

Asia Pacific accounted for 39.2% of anti-acne dermal patch market share in 2024 and is forecast to post an 8.1% CAGR through 2030, fueled by K-beauty’s cultural pull and the region’s status as hydrocolloid manufacturing epicenter. Domestic champions in South Korea supply proprietary films at competitive rates, allowing rapid SKU turnover tailored to local trends. Rising male grooming spend further widens the revenue base, especially in urban China and Southeast Asia.

North America, although expanding more slowly, delivers the highest unit economics thanks to premium positioning and a consumer base accustomed to subscription models. Retailers lean on dermatologist endorsements and visible shelf space to maintain pricing power. Europe leans toward natural ingredients and biodegradable substrates, reflecting stringent eco-policy and consumer activism. Regulatory divergence inside the bloc continues to cloud labeling strategies, yet opportunity remains for brands that harmonize formulations without actives.

Latin America shows early promise, with Brazil’s aggressive dermatological culture and growing e-commerce infrastructure positioning it as a future growth pocket. The Middle East and Africa remain nascent but benefit from rising disposable incomes and social-media awareness, setting the stage for localized halal-certified or fragrance-free propositions. Across regions, effective market entry increasingly depends on tailoring ingredient stacks and marketing narratives to cultural expectations and regulatory prerequisites.

Competitive Landscape

The anti-acne dermal patch industry remains moderately fragmented, though consolidation is accelerating. Church & Dwight’s USD 630 million purchase of Hero Cosmetics in 2024 validated the segment’s strategic value within broader consumer-health portfolios. Hero remains a category pioneer, yet Korean producers such as T&L and COSRX command sizeable export volumes, enabling private-label programs across North American and European retailers.

Vertical integration between Asia Pacific manufacturers and Western brand owners streamlines supply chains while safeguarding intellectual capital in hydrocolloid engineering. Competition differentiates along three vectors: ingredient sophistication, aesthetic design, and sustainability credentials. Microneedle specialists retain pricing power through patented arrays, whereas hydrocolloid commoditization pressures force brand owners to invest in design-led packaging and influencer relationships.

White-space innovation centers on biodegradable substrates, male-specific SKUs, and AI-driven personalization. Incumbents with data ecosystems can bundle routine tracking with educational content, enhancing switching costs. Entry barriers, in turn, hinge less on manufacturing capacity than on brand equity and regulatory fluency across multi-jurisdiction portfolios.

Anti-Acne Dermal Patch Industry Leaders

3M

Hero Cosmetics

Peter Thomas Roth Labs

Starface

COSRX

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Church & Dwight closed a USD 630 million deal for Hero Cosmetics, the largest acquisition in patch history, giving the buyer a fast-growing hydrocolloid franchise and providing Hero with global distribution muscle.

- April 2025: Heyday acquired ZitSticka to embed patch technology within its service-led skincare model, furthering the sector’s consolidation wave.

- April 2025: Hero Cosmetics announced its first major international rollout into Canada, leveraging regulatory alignment with the United States to test global scalability.

Global Anti-Acne Dermal Patch Market Report Scope

| Hydrocolloid |

| Microneedle |

| Hydrogel |

| Silicone-based |

| Biodegradable/Bio-cellulose |

| Salicylic-acid |

| Tea-tree / Herbal actives |

| Hydrocolloid-only (non-medicated) |

| Charcoal / Absorptive blends |

| Other actives (Niacinamide, Retinoids, etc.) |

| Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets |

| Online / E-commerce |

| Dermatology Clinics |

| Specialty Beauty Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Patch Type | Hydrocolloid | |

| Microneedle | ||

| Hydrogel | ||

| Silicone-based | ||

| Biodegradable/Bio-cellulose | ||

| By Ingredient Type | Salicylic-acid | |

| Tea-tree / Herbal actives | ||

| Hydrocolloid-only (non-medicated) | ||

| Charcoal / Absorptive blends | ||

| Other actives (Niacinamide, Retinoids, etc.) | ||

| By Distribution Channel | Pharmacies & Drug Stores | |

| Supermarkets & Hypermarkets | ||

| Online / E-commerce | ||

| Dermatology Clinics | ||

| Specialty Beauty Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the anti-acne dermal patch market in 2030?

The market is expected to reach USD 906.3 million by 2030, reflecting a 6.8% CAGR from 2025.

Which patch type currently dominates sales?

Hydrocolloid variants lead with 62.2% of global revenue in 2024.

Why are microneedle patches gaining attention?

Patent expiries and easier Class I device clearance have opened the door for more affordable microneedle formats that deliver actives directly into blemish sites.

Which region presents the fastest growth outlook?

Asia Pacific is on pace for an 8.1% CAGR, supported by manufacturing scale and K-beauty cultural influence.

How are sustainability concerns being addressed?

Brands are experimenting with biodegradable bio-cellulose substrates and reusable silicone formats to curb single-use waste without sacrificing efficacy.

What recent M&A activity signals category consolidation?

Church & Dwights USD 630 million acquisition of Hero Cosmetics underscores growing interest from large consumer-health players.

Page last updated on: