Urinary Retention Therapeutics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

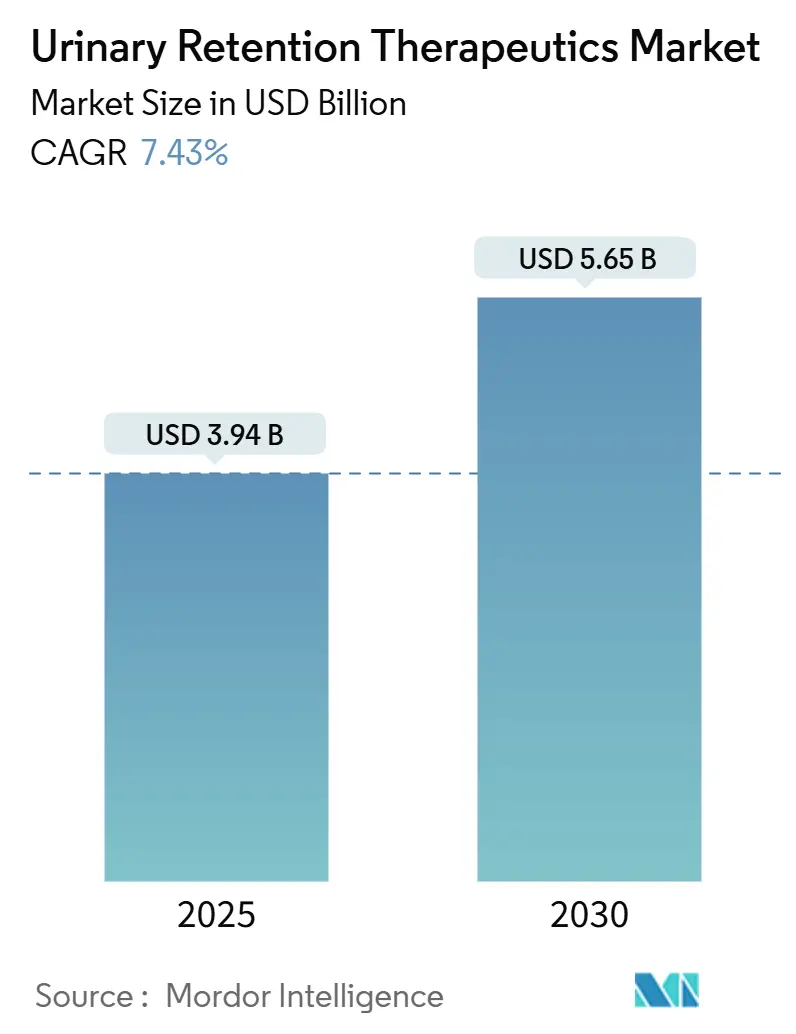

| Market Size (2025) | USD 3.94 Billion |

| Market Size (2030) | USD 5.65 Billion |

| Growth Rate (2025 - 2030) | 7.43% CAGR |

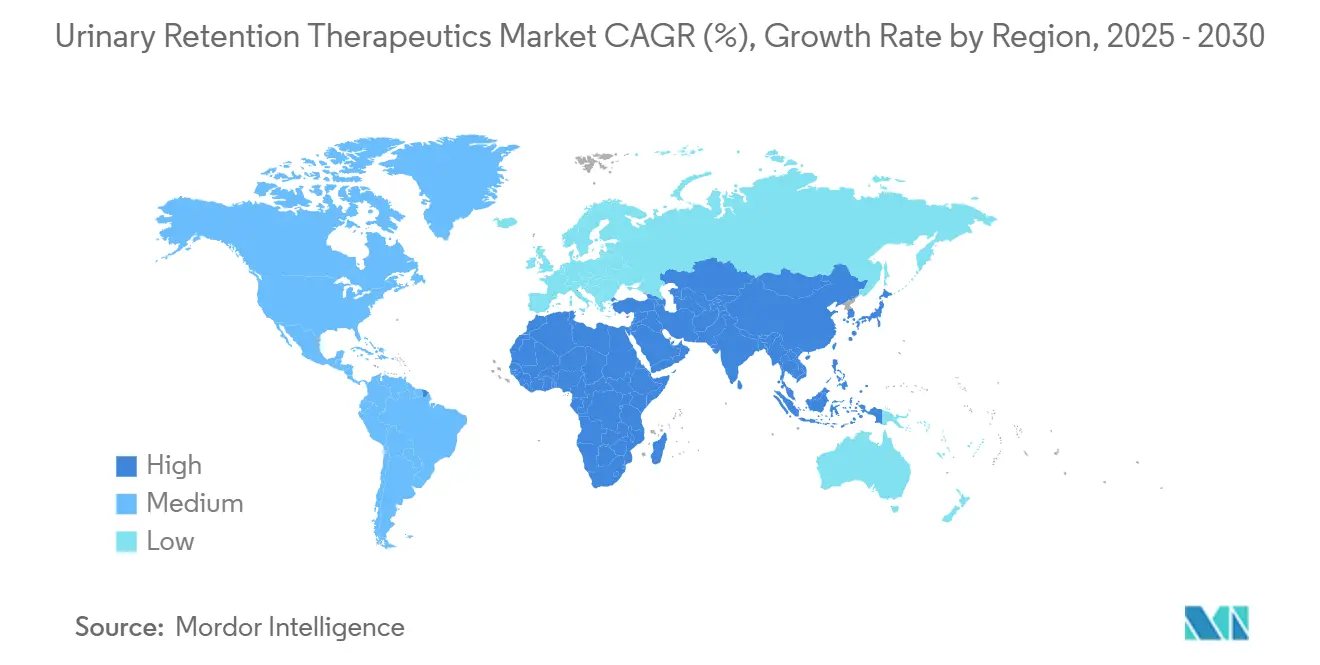

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urinary Retention Therapeutics Market Analysis by Mordor Intelligence

The urinary retention therapeutics market size reached USD 3.94 billion in 2025 and is projected to rise to USD 5.65 billion by 2030, advancing at a 7.43% CAGR. Aging populations, fast-track regulatory approvals, and artificial-intelligence-enabled diagnostics are jointly broadening clinical demand and shortening adoption cycles for both oral drugs and minimally invasive delivery systems. Early diagnosis through AI bladder-volume measurement is shifting clinical practice from crisis intervention to preventive care, prompting payers to re-evaluate reimbursement pathways for first-line pharmacotherapy. At the same time, supply-chain resiliency programs in Asia are lowering production costs and improving access to combination products that tackle urinary symptoms and erectile dysfunction in a single pill. Competitive intensity is therefore rising as innovators leverage expedited approval routes and digital distribution to offset generic erosion and device competition.

Key Report Takeaways

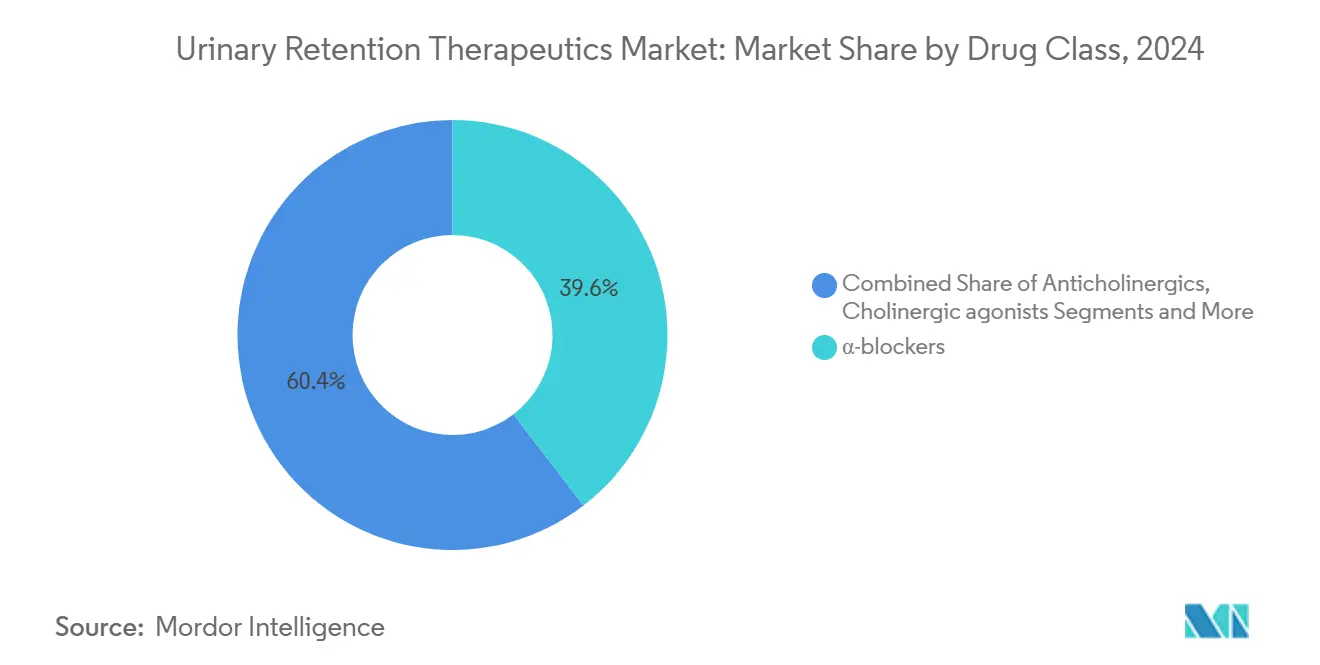

- By drug class, α-blockers led with 39.58% revenue share in 2024; β3-adrenergic agonists are forecast to expand at a 10.37% CAGR to 2030.

- By route of administration, oral formulations captured 77.48% share of the urinary retention therapeutics market size in 2024, while injectable and intravesical options are growing at a 10.79% CAGR.

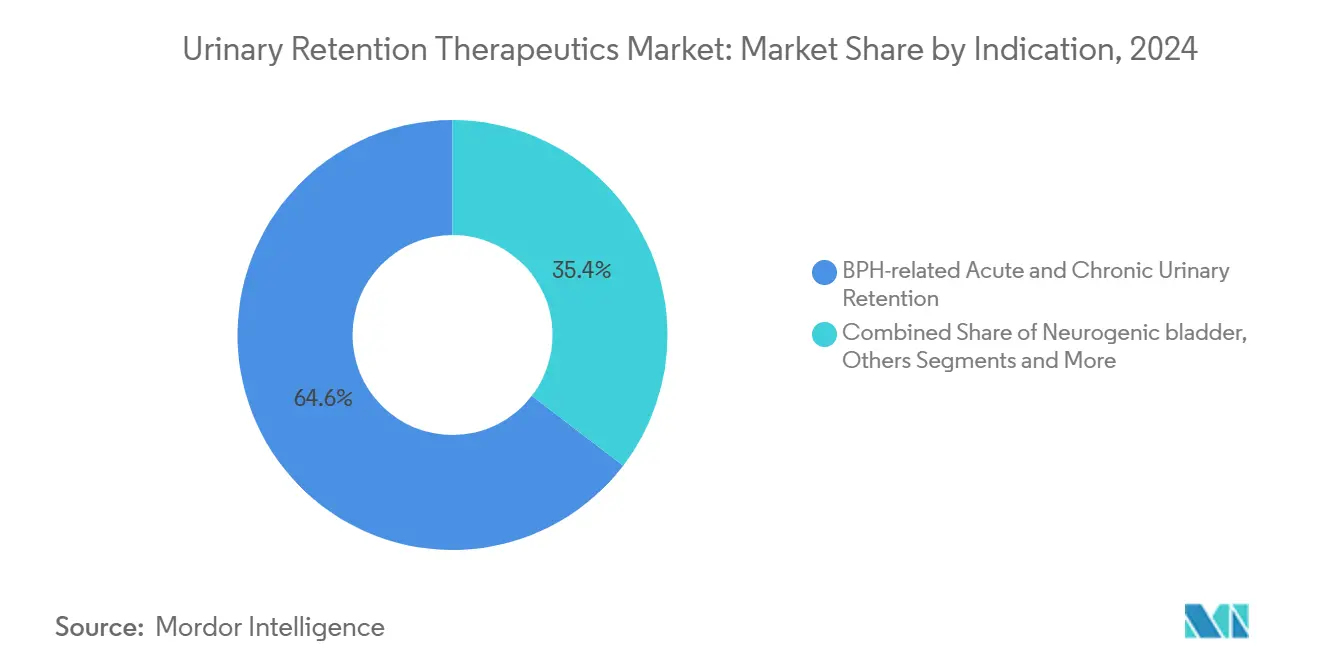

- By indication, BPH-related retention accounted for 64.59% of the urinary retention therapeutics market share in 2024, whereas neurogenic bladder is advancing at a 9.28% CAGR.

- By distribution channel, hospital pharmacies held 48.66% share in 2024; online pharmacies and tele-pharmacy platforms are expanding at an 11.44% CAGR.

- By region, North America commanded 36.23% share in 2024 and Asia-Pacific is pacing ahead with a 9.53% CAGR through 2030.

Global Urinary Retention Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging male population & rising BPH prevalence | +2.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| Growing preference for minimally invasive pharmacotherapy | +1.8% | High-income economies | Medium term (2-4 years) |

| Expanding healthcare access in emerging markets | +1.5% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Combination α-blocker + PDE5 inhibitors improve adherence | +1.2% | North America, Europe, rising in Asia-Pacific | Medium term (2-4 years) |

| AI-driven diagnostics enabling earlier intervention | +0.9% | North America, pilot sites in Europe & Asia-Pacific | Short term (≤ 2 years) |

| Regulatory fast-tracks for β3-agonists targeting female urinary retention | +0.7% | United States, European Economic Area | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Male Population & Rising BPH Prevalence

Benign prostatic hyperplasia affects up to 80% of men over 70 years, and earlier pharmacologic intervention can delay surgery by 3–5 years, keeping many patients on long-term prescriptions.[1]Amy Kichler, “Medical Management of Benign Prostatic Hyperplasia,” Cleveland Clinic Journal of Medicine, ccjm.orgOral α-blockers therefore remain first-line agents, and their convenience aligns with patient preference for non-surgical care. Payers in Japan and Western Europe now reimburse extended drug courses that historically required annual renewal, lengthening revenue cycles. Although minimally invasive devices such as UroLift are gaining ground, their uptake is still modest relative to the broad base of pharmacologic users. Consequently, demographic momentum continues to reinforce drug predominance across high-income health systems.

Growing Preference for Minimally Invasive Pharmacotherapy

Clinical data from 2024 showed that fixed-dose α-blocker + PDE5 inhibitor tablets delivered 76% patient satisfaction versus 49% for monotherapy, highlighting a strong shift toward single-pill solutions.[2]Medtronic PLC, “Bladder Control – Considering Our Therapies,” medtronic.com Industry pipelines now include transdermal patches and once-weekly intravesical gels designed to reduce systemic exposure while preserving efficacy. Younger cohorts—motivated by lifestyle and convenience—are accelerating demand for such formats, prompting formulators to invest in novel excipients that enable sustained release without injection. This behavior change is nudging clinicians to re-write treatment algorithms that once defaulted to daily oral tablets.

Expanding Healthcare Access in Emerging Markets

Government insurance schemes in India, China, and Indonesia now cover chronic urological conditions, adding millions of potential users to the urinary retention therapeutics market.[3]UroGen Pharma Ltd., “UroGen Announces FDA Acceptance of NDA for UGN-102,” urogen.com Local contract manufacturers are scaling production under WHO pre-qualification, lowering unit costs for α-blockers and β3-agonists. Telemedicine platforms distribute these medicines to rural regions, overcoming physician shortages and logistic barriers. Female patients, who once delayed care due to cultural constraints, are increasingly filling e-prescriptions from the privacy of home. The broader patient funnel raises baseline demand and stabilizes year-over-year volume growth for multinational and domestic producers alike.

Combination α-Blocker + PDE5 Inhibitors Improve Adherence

Clinical studies report 40% fewer discontinuations when urinary and erectile symptoms are managed with a single pill versus two separate prescriptions.[4]Richard Dmochowski et al., “Satisfaction and Persistence with Vibegron: COMPOSUR Interim Results,” BMC Urology, biomedcentral.com Retrograde ejaculation fell to 8% on combination therapy from 18% on tamsulosin alone, easing a key deterrent to adherence. Manufacturers are responding with once-daily tablets that blend optimized doses to minimize hypotension while sustaining symptom relief. Prescribers welcome the simplified regimen, and pharmacists note higher refill compliance among working-age men who value discretion and convenience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse sexual side-effects causing therapy discontinuation | -1.4% | Global, most visible in high-income markets | Medium term (2-4 years) |

| Generic erosion reducing branded revenues | -1.1% | Worldwide, amplified in price-sensitive regions | Short term (≤ 2 years) |

| Shift toward neuromodulation & device-based therapies | -0.8% | North America, Europe | Long term (≥ 4 years) |

| Cross-border telemedicine price competition via e-pharmacies | -0.6% | Global, regulation dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Sexual Side-Effects Causing Therapy Discontinuation

Up to 18% of men on tamsulosin report retrograde ejaculation, and 11% of alfuzosin users cite sexual dysfunction, prompting high dropout rates. These outcomes deter new starts and undermine long-term adherence, especially in sexually active patients under 65. Pipeline programs now focus on subtype-selective antagonists to minimize ejaculatory impact. Some firms are testing intravesical α-blocker gels that avoid systemic exposure, yet commercial timelines remain uncertain. Until safer profiles emerge, prescribers may prefer β3-agonists for patients with quality-of-life concerns.

Generic Erosion Reducing Branded Revenues

Within 18 months of patent expiry, tamsulosin generics captured 70% share in major markets, compressing average selling prices and pressuring originator margins. Innovators respond by fast-tracking life-cycle extensions such as sustained-release beads and once-weekly patches that restore some pricing power. Nonetheless, formulary committees in Asia and Latin America continue to prioritize low-cost copies. The revenue squeeze forces branded players to allocate more capital to R&D for novel mechanisms, raising overall development risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: β3-Agonists Challenge α-Blocker Dominance

In 2024 α-blockers retained 39.58% of category revenues, supported by decades of clinical familiarity and low manufacturing costs, yet their growth is slowing amid generic saturation and adherence issues. The urinary retention therapeutics market size for β3-agonists is forecast to surge at a 10.37% CAGR as vibegron gains multi-regional approvals and demonstrates 73.9% six-month persistence in the COMPOSUR trial. Physicians increasingly reserve β3-agonists for patients intolerant of α-blockers, and their favorable side-effect profile is expanding first-line use among women. Meanwhile, 5α-reductase inhibitors grow modestly as adjuncts rather than stand-alone fixes, and anticholinergics retreat due to cognitive safety warnings in older adults.

Combination tablets that merge α-blockers with PDE5 inhibitors exemplify the shift toward patient-centric therapy, and early uptake indicates willingness to pay a premium for improved adherence. Innovators are also engineering selective α1A antagonists to curb hypotension, but market entry may not occur until post-2030. Altogether, portfolio managers must balance erosion in the legacy core with accelerated gains in the flexible, fast-growing β3 category, an equilibrium that will define competitive positioning across the urinary retention therapeutics market.

By Route of Administration: Injectable Growth Accelerates

Oral dosage forms controlled 77.48% of revenue in 2024, benefiting from clinician comfort and mature reimbursement coding. Yet injectable and intravesical options are on a 10.79% CAGR trajectory, indicating that the urinary retention therapeutics market share mix is slowly tilting toward localized delivery. Intravesical installations such as UGN-102 illustrate how site-specific therapy can lower systemic adverse events while targeting bladder pathology directly. Sustained-release microspheres administered quarterly are under investigation to replace daily tablets.

Transdermal patches appeal to patients who experience gastrointestinal upset with oral agents, though manufacturing complexity inflates cost of goods. Looking ahead, bi-annual in-office injections could alleviate adherence burdens for neurogenic populations, but payers will demand real-world evidence before endorsing broad coverage. Formulation versatility is therefore emerging as a strategic differentiator across the urinary retention therapeutics industry.

By Indication: Neurogenic Bladder Gains Momentum

BPH-related retention represented 64.59% revenue in 2024, underscoring the condition’s prevalence in aging men and the entrenched role of α-blockers. Nonetheless neurogenic bladder is the fastest-growing niche at 9.28% CAGR, driven by better spinal cord injury survival and heightened diagnostic acuity through urodynamics. The urinary retention therapeutics market size for neurogenic patients is set to expand as hospitals adopt neuromodulation devices in tandem with pharmacologic regimens.

Rehabilitation centers now run multidisciplinary clinics that coordinate urologists, neurologists, and physiatrists, boosting prescription volumes for agents tailored to detrusor overactivity. Post-operative retention remains stable yet benefits from prophylactic drug protocols in hip and abdominal surgeries. Collectively, these patterns reinforce the need for indication-specific labeling and dosing guidance.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies held 48.66% share in 2024, reflecting their role in initial diagnosis and complex case management, but online pharmacies are rising at an 11.44% CAGR with aggressive customer-acquisition campaigns. The urinary retention therapeutics market is therefore decentralizing as tele-pharmacy services pair virtual consults with doorstep delivery, a model resonating in chronic disease cohorts. Retail chains are blending curbside pickup, mail order, and in-store counseling to stay competitive.

Regulators in the European Economic Area are drafting common e-prescription standards that could unlock wider cross-border fulfillment. As infrastructure matures, manufacturers gain direct-to-consumer channels for adherence programs, but must guard against grey-market leakage and counterfeit risk. Channel strategy thus becomes as critical as molecule innovation when capturing long-term value.

Geography Analysis

North America maintains pole position with 36.23% 2024 revenue on the back of robust payer coverage, high disease awareness, and early AI adoption in diagnostic suites. FDA fast-track pathways shortened approval cycles for β3-agonists, enabling rapid uptake among women historically underserved by α-blockers. Insurers are also experimenting with outcomes-based contracts that share financial risk when acute retention events decline. Integration of electronic medical records with predictive analytics means candidates begin therapy earlier, lengthening cumulative treatment time and reinforcing the urinary retention therapeutics market.

Europe follows with steady growth anchored in EMA accelerated assessment schemes and growing acceptance of combination tablets that target sexual comorbidities. National health systems in Germany and France now reimburse once-daily vibegron for women who failed anticholinergics, expanding the addressable pool. Brexit-related customs friction encourages multi-national firms to diversify packaging hubs, ensuring uninterrupted supply to both the United Kingdom and continental bloc. Parallel import rules simultaneously foster price convergence, pressuring branded margins yet broadening patient reach.

Asia-Pacific is the headline growth engine at 9.53% CAGR thanks to public insurance expansion in China and India. Community health apps link rural patients to urology specialists, while domestic generics manufacturers drive costs down enough to put β3-agonists within reach of middle-income households. Japan’s super-aging society provides a large, clinically sophisticated base for early use of combination α-blocker + PDE5 inhibitor products. Southeast Asian nations are piloting government-funded tele-pharmacy portals that ship medicines overnight, adding momentum to online channel share within the urinary retention therapeutics market.

Competitive Landscape

Strategic consolidation is reshaping the industry as innovators secure geographic rights to high-growth molecules while shoring up portfolios threatened by generic cliffs. Pierre Fabre’s 2024 acquisition of European rights to vibegron deepened its presence in β3-agonists and granted immediate entry to the fastest-growing drug class. Simultaneously, medical-device giants are moving upstream; Boston Scientific’s agreement to purchase Axonics positions it to cross-sell sacral-neuromodulation systems alongside drug managers seeking adjunctive solutions for refractory cases.

Lifecycle management dominates branded strategies: companies bundle adherence apps with starter kits, pursue combination patents that extend exclusivity, and engage in post-marketing studies to claim new indications. Digital therapeutics partnerships are multiplying as firms mine real-world data to refine dosing algorithms and personalize therapy. Despite these moves, competitive intensity rises each time a major molecule loses exclusivity, driving sponsors to accelerate phase-II assets into pivotal trials even at higher clinical-development risk.

White-space opportunities persist in female-specific formulations, pediatric neurogenic protocols, and AI-assisted diagnostic packages. Entrants capable of integrating molecule, device, and software into a seamless care pathway may secure outsized share of the urinary retention therapeutics market. The race is now as much about data ownership and patient engagement as it is about pharmacology, signaling a paradigm shift toward holistic disease-management franchises.

Urinary Retention Therapeutics Industry Leaders

AbbVie Inc.

Astellas Pharma Inc.

Merck & Co., Inc.

GlaxoSmithKline plc

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Eisai Thailand launched Beova Tablets (vibegron) for overactive bladder, marking the molecule’s first Southeast Asian entry.

- June 2025: UroGen Pharma received FDA approval for ZUSDURI, the inaugural therapy for recurrent low-grade intermediate-risk non-muscle invasive bladder cancer.

- December 2024: Sumitomo Pharma America secured FDA clearance for GEMTESA (vibegron) to treat men with overactive bladder symptoms concurrent with BPH therapy.

Global Urinary Retention Therapeutics Market Report Scope

| α-blockers |

| 5-α-reductase inhibitors |

| Anticholinergics |

| Cholinergic agonists |

| β3-adrenergic agonists |

| Combination therapies |

| Oral |

| Injectable/Intravesical |

| Transdermal |

| BPH-related acute & chronic urinary retention |

| Neurogenic bladder |

| Post-operative urinary retention |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies & Tele-pharmacy Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | α-blockers | |

| 5-α-reductase inhibitors | ||

| Anticholinergics | ||

| Cholinergic agonists | ||

| β3-adrenergic agonists | ||

| Combination therapies | ||

| By Route of Administration | Oral | |

| Injectable/Intravesical | ||

| Transdermal | ||

| By Indication | BPH-related acute & chronic urinary retention | |

| Neurogenic bladder | ||

| Post-operative urinary retention | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies & Tele-pharmacy Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the urinary retention therapeutics market by 2030?

The market is forecast to reach USD 5.65 billion by 2030, growing at a 7.43% CAGR.

Which drug class is expanding fastest?

Β3-adrenergic agonists, led by vibegron, are advancing at a 10.37% CAGR through 2030.

How significant is online pharmacy growth in urinary retention care?

Online pharmacies and tele-pharmacy platforms are growing at an 11.44% CAGR, eroding traditional channels.

Which geographic region offers the highest growth rate?

Asia-Pacific is pacing at a 9.53% CAGR due to expanding insurance coverage and digital health adoption.

Why are combination α-blocker + PDE5 inhibitor tablets gaining popularity?

They cut therapy discontinuations by 40% versus separate pills, improving adherence and patient quality of life.

How does AI improve urinary retention treatment outcomes?

AI‐enabled diagnostics identify at-risk patients earlier, reducing acute retention episodes by about 30%.

Page last updated on: