Nocturia Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

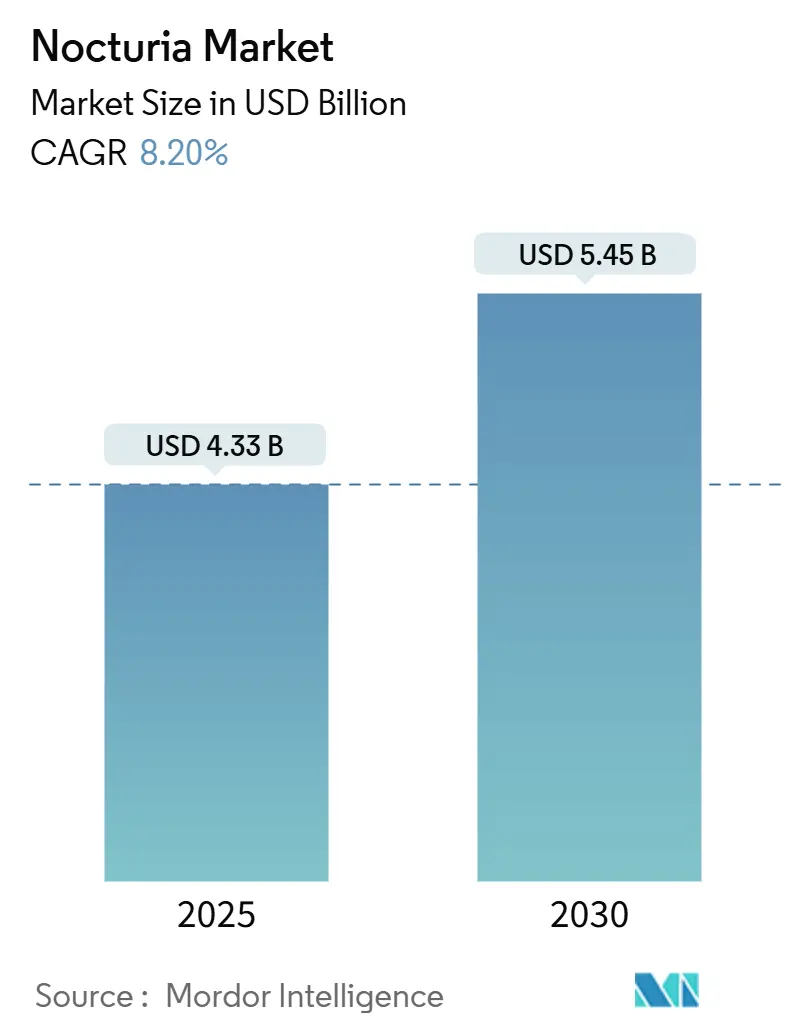

| Market Size (2025) | USD 4.33 Billion |

| Market Size (2030) | USD 5.45 Billion |

| Growth Rate (2025 - 2030) | 8.20% CAGR |

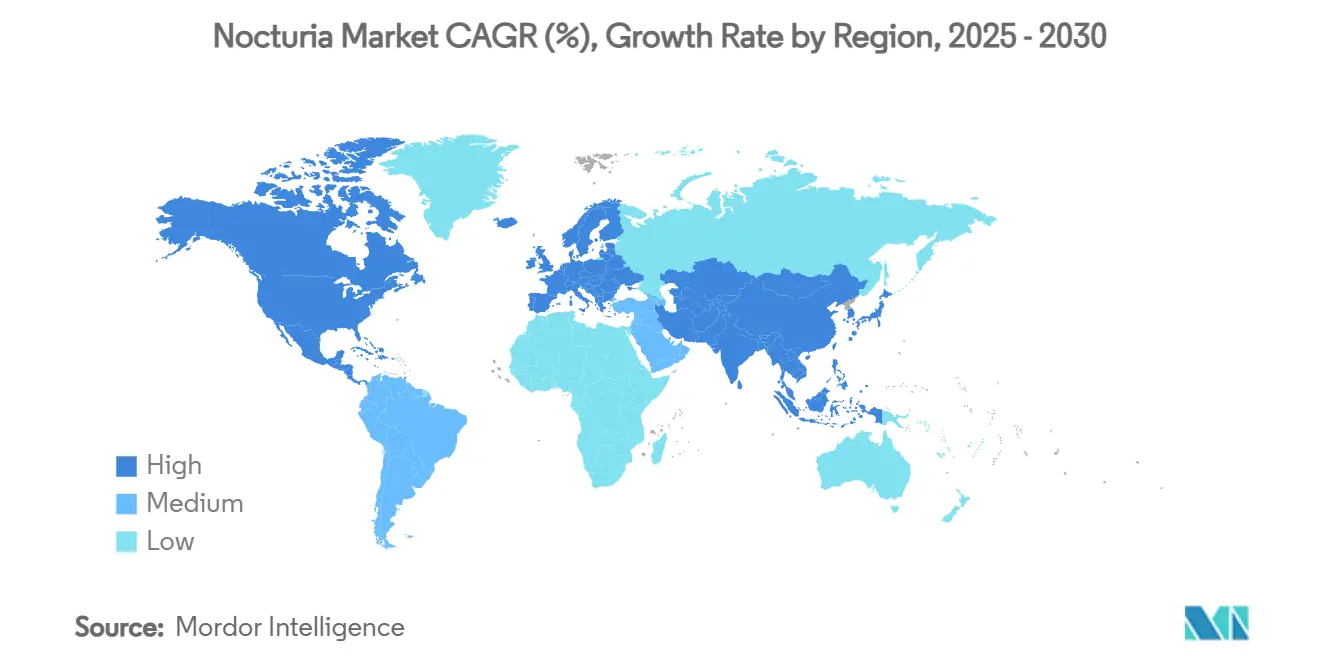

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nocturia Market Analysis by Mordor Intelligence

The Nocturia Market size is estimated at USD 4.33 billion in 2025, and is expected to reach USD 5.45 billion by 2030, at a CAGR of 8.20% during the forecast period (2025-2030).

Greater longevity, rising prevalence of metabolic diseases, and patient-centric drug delivery technologies collectively underpin this expansion trajectory. Sustained uptake of vasopressin analogues, particularly desmopressin ODT, anchors current revenue streams, while the superior tolerability of β-3 adrenergic agonists accelerates future growth momentum. The increasing recognition that circadian rhythm disruption contributes to the pathogenesis of nocturia is guiding both basic research and commercial pipelines toward mechanism-specific therapies. In parallel, the rapid adoption of digital health is expanding the reach of diagnosis and prescription, particularly in the Asia Pacific, thereby enhancing overall addressable demand.

Key Report Takeaways

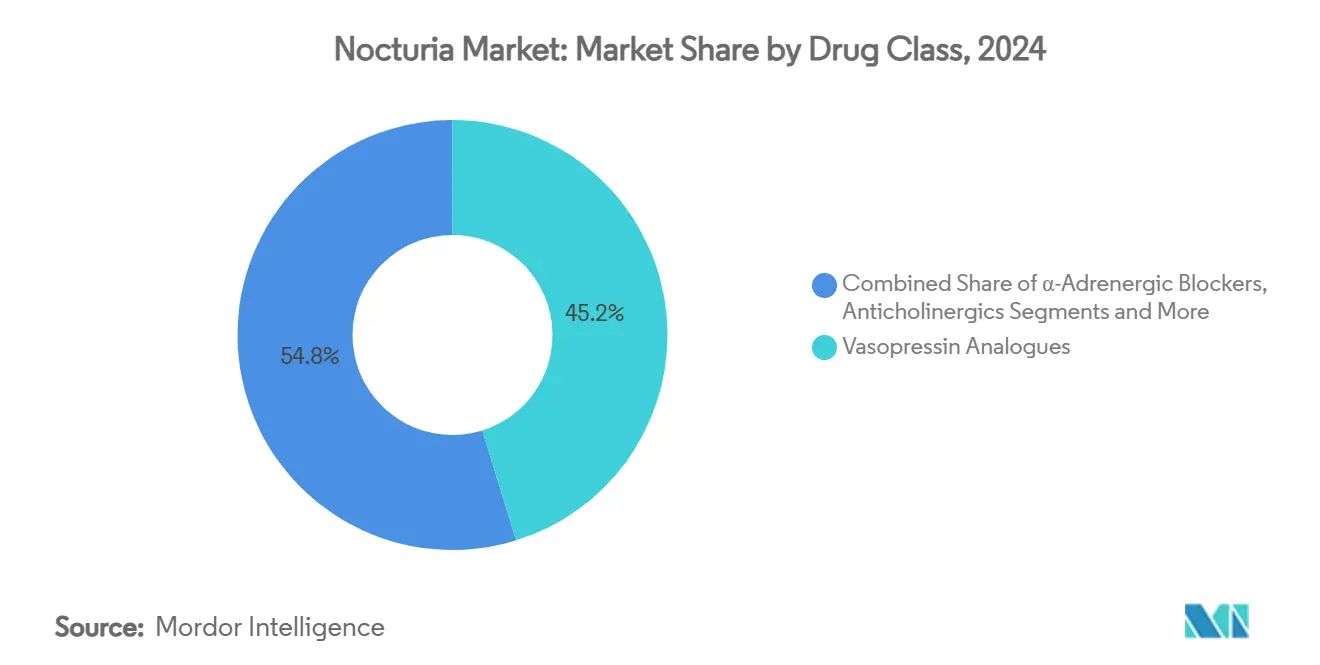

- By drug class, vasopressin analogues held 45.2% of the nocturia market share in 2024, whereas β-3 adrenergic agonists are projected to advance at a 14.8% CAGR through 2030.

- By disease type, nocturnal polyuria accounted for 39.1% of the nocturia market size in 2024, while mixed pathophysiology is projected to expand at a 9.9% CAGR through 2030.

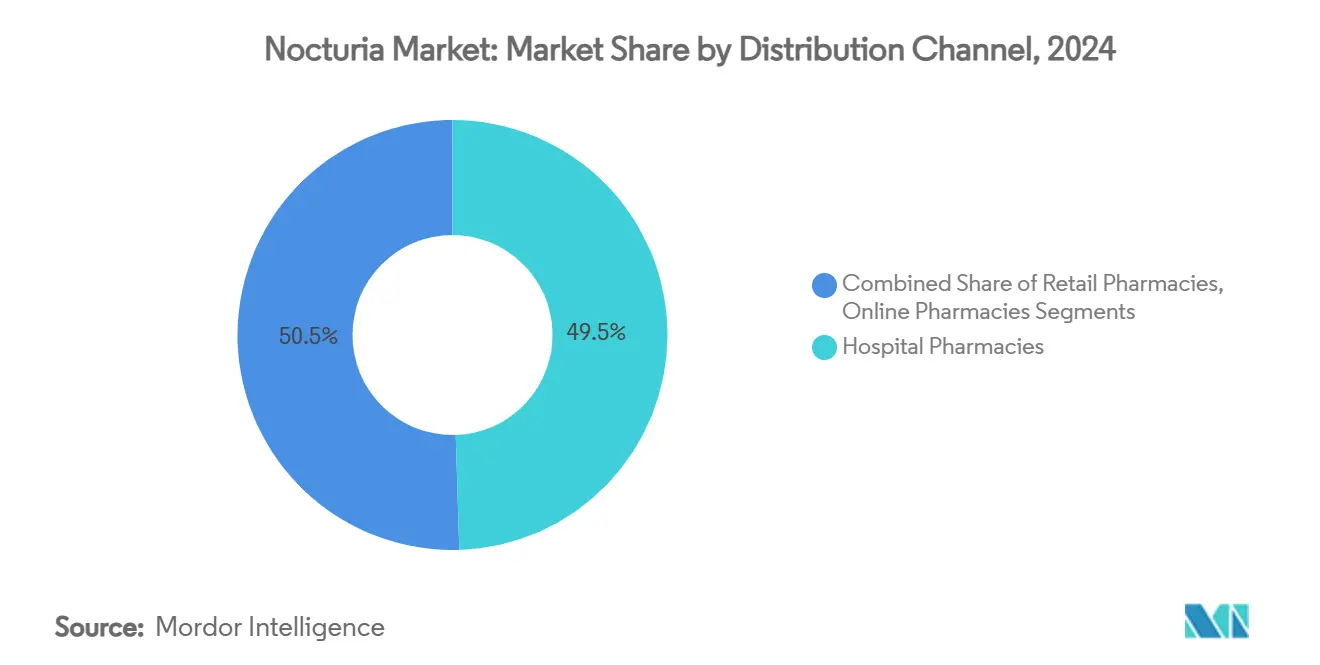

- By distribution channel, hospital pharmacies captured 49.5% of the nocturia market share in 2024, whereas online pharmacies are projected to grow at a 15.8% CAGR through 2030.

- Geographically, North America led with 38.4% revenue share in 2024; Asia Pacific is forecast to record a 9.2% CAGR between 2025 and 2030.

Global Nocturia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Elderly Population Base | +1.80% | Global, with highest impact in Japan, Germany, Italy | Long term (≥ 4 years) |

| Rising Prevalence Of Type-2 Diabetes & Obesity | +1.20% | Global, particularly North America and Middle East | Medium term (2-4 years) |

| Expanding Uptake Of Desmopressin ODT Formulations | +0.90% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Pipeline Launch Of Gene-Based Circadian Rhythm Modulators | +1.10% | Global, early adoption in US and EU | Long term (≥ 4 years) |

| AI-Enabled Symptom Tracking Apps Improving Diagnosis Rates | +1.50% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Employer-Paid Sleep-Health Programs Boosting Treatment Demand | +0.80% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Elderly Population Base

Global ageing is the strongest structural force behind the growth of the nocturia market. Japan already reports that 29% of residents are ≥65 years old, and nocturia prevalence exceeds 80% among those ≥80 years.[1]Marco Hafner et al., “How frequent night-time bathroom visits can negatively impact sleep, well-being and productivity,” RAND Corporation, rand.org Similar demographic shifts in Germany and Italy are widening the treated patient pool and driving payer focus on sleep-related quality-of-life outcomes. RAND analysis estimates that nocturia-linked productivity losses reach USD 79 billion annually across six major economies, elevating the disorder on policy agendas. Within emerging regions, rapid urbanization in China and India is coupled with longevity trends to amplify future demand. Collectively, these factors position the nocturia market as a defensive healthcare segment with steady long-term growth prospects.

Rising Prevalence of Type-2 Diabetes & Obesity

Metabolic disorders intensify the severity of nocturia, creating a disease-cluster effect that expands therapeutic demand beyond aging alone. Clinical evidence shows that patients with type 2 diabetes experience 2-3 times higher nocturia incidence than healthy cohorts.[2]Salim Mujais, “Efficacy and Safety of Vibegron… COURAGE Trial,” Journal of Urology, auajournals.org Obesity contributes to elevated intra-abdominal pressure, sleep apnea, and insulin resistance, making nocturia management inseparable from metabolic care in North America and the Middle East. Consequently, the nocturia market benefits when clinicians adopt integrated care pathways that address both urological and metabolic abnormalities.

Expanding Uptake of Desmopressin ODT Formulations

Orally disintegrating desmopressin eliminates the need for water co-administration and reduces the risk of hyponatremia, thereby boosting adherence among elderly patients with complex regimens. Ferring’s Nocdurna achieved a 47% responder rate in pivotal trials and gained regulatory clearances across Europe and the US.[3]FDA Center for Drug Evaluation and Research, “FDA approves first treatment for frequent urination at night due to overproduction of urine,” fda.gov As prescriber familiarity grows and generic nasal sprays face usage constraints, ODT formulations are capturing an incremental market share for nocturia. This illustrates how delivery-system innovation can reinvigorate established molecules.

Pipeline Launch of Gene-Based Circadian Rhythm Modulators

Roughly 20% of kidney-expressed genes operate on circadian cycles, and disruption of this axis has been linked to overactive bladder symptoms. Early-stage modulators aim to reset clock gene expression and may offer disease-modifying benefits beyond symptom control. Small trials of melatonin receptor agonists already signal potential efficacy, and larger late-stage studies are planned. First movers in this niche could redefine standard-of-care protocols by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Concerns Around Hyponatremia With Vasopressin Analogs | -0.70% | Global, particularly affecting elderly populations | Short term (≤ 2 years) |

| Low Awareness Among Primary-Care Physicians | -0.50% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Generic Erosion Of Antimuscarinic Drugs | -0.40% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) |

| Reimbursement Hurdles For Digital Therapeutics | -0.30% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns Around Hyponatremia

Mandatory serum sodium monitoring and age-specific dosing guidelines for desmopressin create operational burdens that deter some prescribers. Although the incidence is low, potential severity drives cautious utilisation, especially in nursing home populations. This safety shadow slows the uptake of vasopressin analogues in the nocturia market, stimulating interest in alternative classes, notably β-3 agonists.

Low Awareness Among Primary-Care Physicians

Surveys indicated that 72% of adults in the US believe nocturia is an inevitable part of ageing, and comparable misconceptions exist among physicians. Underdiagnosis delays care initiation and limits volume growth. Pharmaceutical and academic groups are responding with continuing-education modules and decision-support tools, but penetration remains uneven outside tertiary centres.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Vasopressin Analogues Lead Even as β-3 Agonists Surge

Vasopressin analogues retained 45.2% revenue share in 2024, anchoring the nocturia market despite safety monitoring requirements. β-3 adrenergic agonists, however, are forecast to grow at a 14.8% CAGR through 2030 as vibegron demonstrates strong persistence and tolerability in the COURAGE and COMPOSUR studies.

Hospital audit data indicate that β-3 agonists hold a 12% share in 2024, but early real-world adherence of 73.9% at six months suggests a robust trajectory toward wider adoption. Anticholinergics remain relevant for cost-sensitive segments, yet the risk of cognitive side effects and generic erosion continues to erode their value. Pipeline candidates such as sunobinop could further diversify the class portfolio by mid-decade, sustaining competitive churn within the nocturia market.

By Disease Type: Mixed Pathophysiology Gains Traction

Nocturnal polyuria accounted for 39.1% of 2024 revenue, driven by its high prevalence and clear diagnostic criteria. Although the mixed pathophysiology is smaller, it is rising at a 9.9% CAGR, as advanced voiding diaries and bladder scans reveal a multifactorial etiology.

Personalized regimens combining desmopressin, β-3 agonists, and lifestyle modifications are translating diagnostic granularity into clinical benefit. This evolution supports higher per-patient spend and encourages manufacturers to maintain broad portfolios capable of addressing blended pathologies within the nocturia market.

By Distribution Channel: Digital Acceleration Fuels Online Pharmacies

Hospital pharmacies accounted for 49.5% of global sales in 2024, thanks to specialist-driven prescribing and hyponatremia monitoring requirements. Yet online pharmacies are climbing at 15.8% CAGR, propelled by telemedicine integration and patient preference for discreet purchasing.

COVID-19 normalized digital refill workflows, and elderly patients increasingly use home delivery to mitigate mobility constraints. This behavioral shift is prompting manufacturers to partner with e-pharmacy platforms for targeted adherence programs, reinforcing digital’s rising influence over nocturia market dynamics.

Geography Analysis

North America generated 38.4% of 2024 revenue, supported by comprehensive insurance coverage, strong urology networks, and early product launches. Payer moves toward value-based models, however, are squeezing margins for antimuscarinics and accelerating the pivot to high-persistence β-3 agents.

Europe remains mature but steady, with Germany, France, and the United Kingdom prioritizing quality-of-life metrics in reimbursement dossiers. Southern Europe’s ageing demographic adds incremental volume, although budgetary constraints temper the uptake of premium prices.

The Asia Pacific is the fastest-growing region, with a 9.2% CAGR, driven by China’s healthcare reform, India’s rising middle class, and Japan’s rapidly aging population. Digital symptom-tracking pilots in South Korea and Singapore demonstrate the regional appetite for tech-enabled care pathways, thereby broadening the future addressable market for the nocturia market.

Middle East & Africa and South America are emerging yet under-penetrated. High diabetes prevalence in Gulf states and improving hospital infrastructure in Brazil provide future catalysts, but near-term growth is moderated by variable reimbursement and supply-chain challenges.

Competitive Landscape

The nocturia market is moderately fragmented. Ferring, Otsuka, and Astellas collectively controlled slightly more than 40% of the revenue in 2024, leveraging their long-standing physician relationships and diversified portfolios. Competitive strategy emphasizes lifecycle management—new formulations, dose optimization, and label extensions—rather than de-novo molecular classes.

β-3 agonist patents, such as Gemtesa protection until 2040, safeguard key revenue streams and justify ongoing investment in post-marketing studies and patient-support programs. Beyond pharmacology, leading firms invest in AI-driven adherence apps to fortify real-world outcomes, thereby strengthening payer value propositions.

Emerging biotech entrants target circadian clock genes and combination products that integrate metabolic and urological benefits. Strategic collaborations between digital therapeutics start-ups and drug manufacturers signal a convergence trend aimed at holistic nocturia management over the next decade.

Nocturia Industry Leaders

Ferring Pharmaceuticals

Otsuka Holdings Co.

Astellas Pharma Inc.

Kyowa Kirin Co.

Teva Pharmaceutical Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Phase 4 COMPOSUR interim data showed 73.9% vibegron persistence at six months, reinforcing its first-line potential.

- January 2025: Eisai received a prestigious Japanese award for lemborexant, underscoring mounting interest in sleep-wake modulation for nocturia management.

- January 2025: Imbrium Therapeutics reported positive Phase 1b findings for sunobinop, a novel β-3 pathway candidate.

- August 2024: Bayer filed an FDA submission for elinzanetant targeting menopause-linked vasomotor symptoms, a comorbidity frequently associated with nocturia.

Global Nocturia Market Report Scope

| Vasopressin Analogues |

| Anticholinergics / Antimuscarinics |

| ?-Adrenergic Blockers |

| ?-3 Adrenergic Agonists |

| Others |

| Nocturnal Polyuria |

| Global Polyuria |

| Reduced Nocturnal Bladder Capacity |

| Mixed Pathophysiology |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Vasopressin Analogues | |

| Anticholinergics / Antimuscarinics | ||

| ?-Adrenergic Blockers | ||

| ?-3 Adrenergic Agonists | ||

| Others | ||

| By Disease Type | Nocturnal Polyuria | |

| Global Polyuria | ||

| Reduced Nocturnal Bladder Capacity | ||

| Mixed Pathophysiology | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the nocturia market by 2030?

The market is forecast to reach USD 5.45 billion in 2030 based on an 8.20% CAGR between 2025 and 2030.

Which therapy class is expanding fastest?

Β-3 adrenergic agonists are growing at a 14.8% CAGR owing to vibegron’s strong tolerability and persistence.

Which geographic region will record the highest growth rate?

Asia Pacific is expected to advance at 9.2% CAGR through 2030 on the back of ageing demographics and broader healthcare access.

How are digital channels influencing nocturia prescriptions?

Online pharmacies are increasing at 15.8% CAGR as telemedicine normalises remote diagnosis and home delivery for nocturia medicines.

What safety issue limits vasopressin analogue use?

Hyponatremia risk necessitates serum sodium monitoring and age-adjusted dosing, dampening uptake among older patients.

Which emerging therapeutic approach targets root-cause biology?

Gene-based circadian rhythm modulators aim to reset disrupted clock genes that drive nocturia, potentially offering disease-modifying benefits.

Page last updated on: