Gastrointestinal Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 43.74 Billion |

| Market Size (2031) | USD 53.96 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

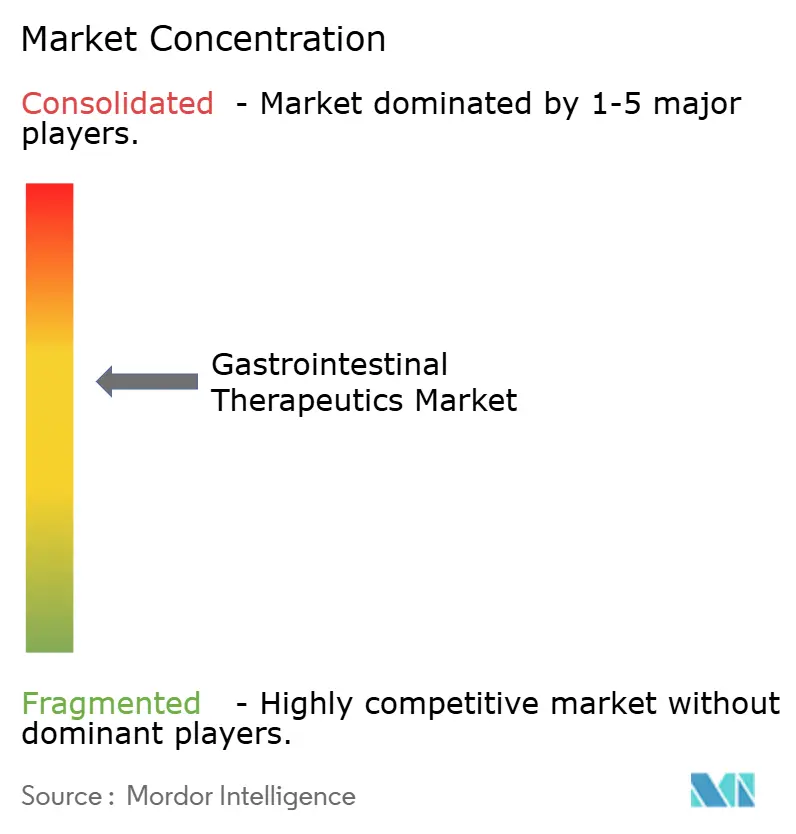

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastrointestinal Therapeutics Market Analysis by Mordor Intelligence

The Gastrointestinal Therapeutics Market size was valued at USD 41.94 billion in 2025 and is estimated to grow from USD 43.74 billion in 2026 to reach USD 53.96 billion by 2031, at a CAGR of 4.29% during the forecast period (2026-2031).

Growing prevalence of digestive disorders, rapid uptake of next-generation biologics, and the commercialization of live microbiome agents are expanding the gastrointestinal therapeutics market even as proton-pump-inhibitor (PPI) prescriptions flatten. Sensor-enabled delivery platforms are improving adherence and enabling value-based payment, while biosimilar competition is altering pricing dynamics in high-volume biologic classes. Regulatory agencies are fast-tracking precision oncology combinations and microbiome interventions, shortening time-to-market and sustaining mid-single-digit value growth. Meanwhile, regional manufacturing scale-ups in Asia-Pacific are deepening supply resilience and lowering treatment costs across the gastrointestinal therapeutics market.

Key Report Takeaways

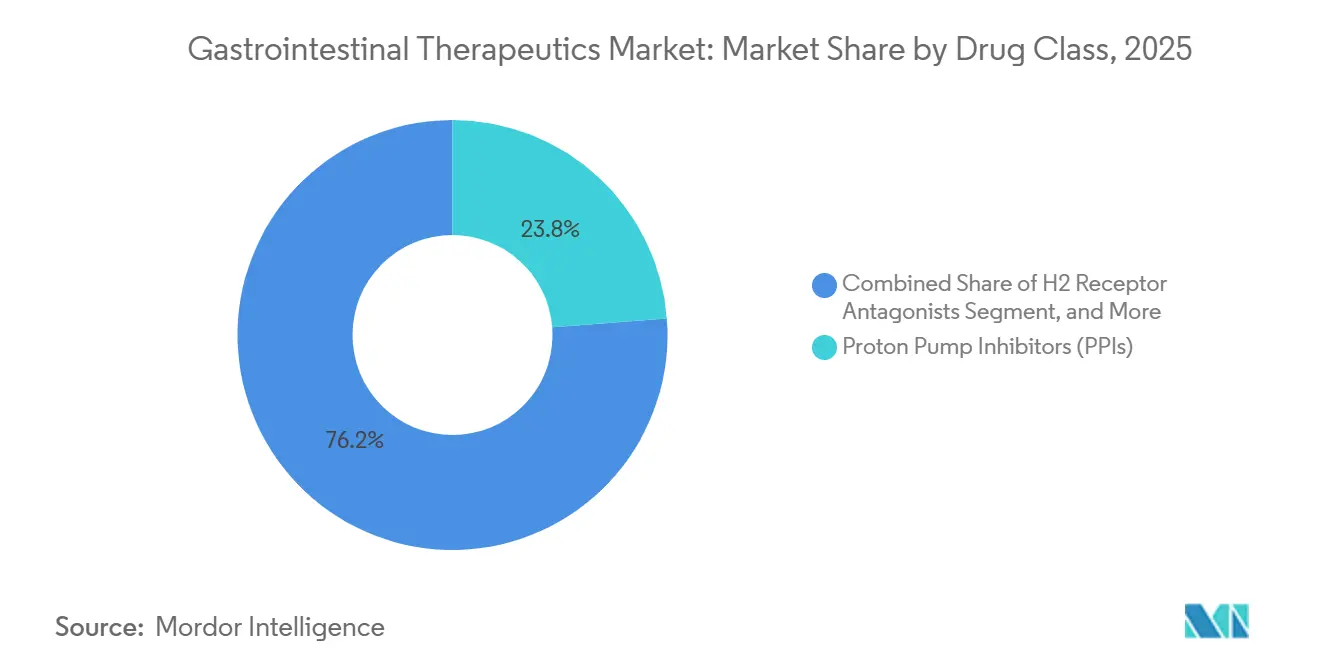

- By drug class, proton pump inhibitors led with 23.78% of the gastrointestinal therapeutics market share in 2025, while microbiome-based therapeutics are projected to expand at a 4.33% CAGR through 2031.

- By disease indication, inflammatory bowel disease accounted for 29.08% of the gastrointestinal therapeutics market size in 2025, whereas gastrointestinal cancer therapeutics are growing at a 4.86% CAGR over the same period.

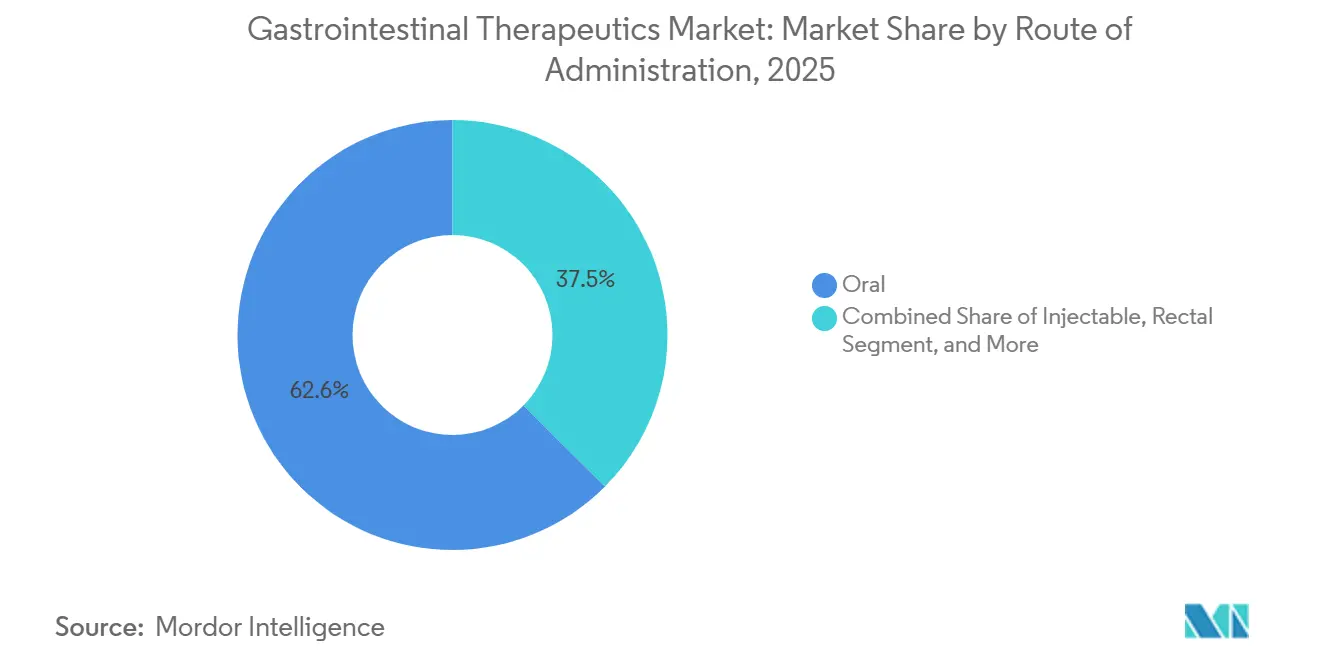

- By route of administration, oral formulations accounted for 62.55% of the gastrointestinal therapeutics market share in 2025, and injectable products are forecast to grow at a 4.65% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 45.21% of the gastrointestinal therapeutics market in 2025, while online pharmacies are projected to grow at a 4.44% CAGR through 2031.

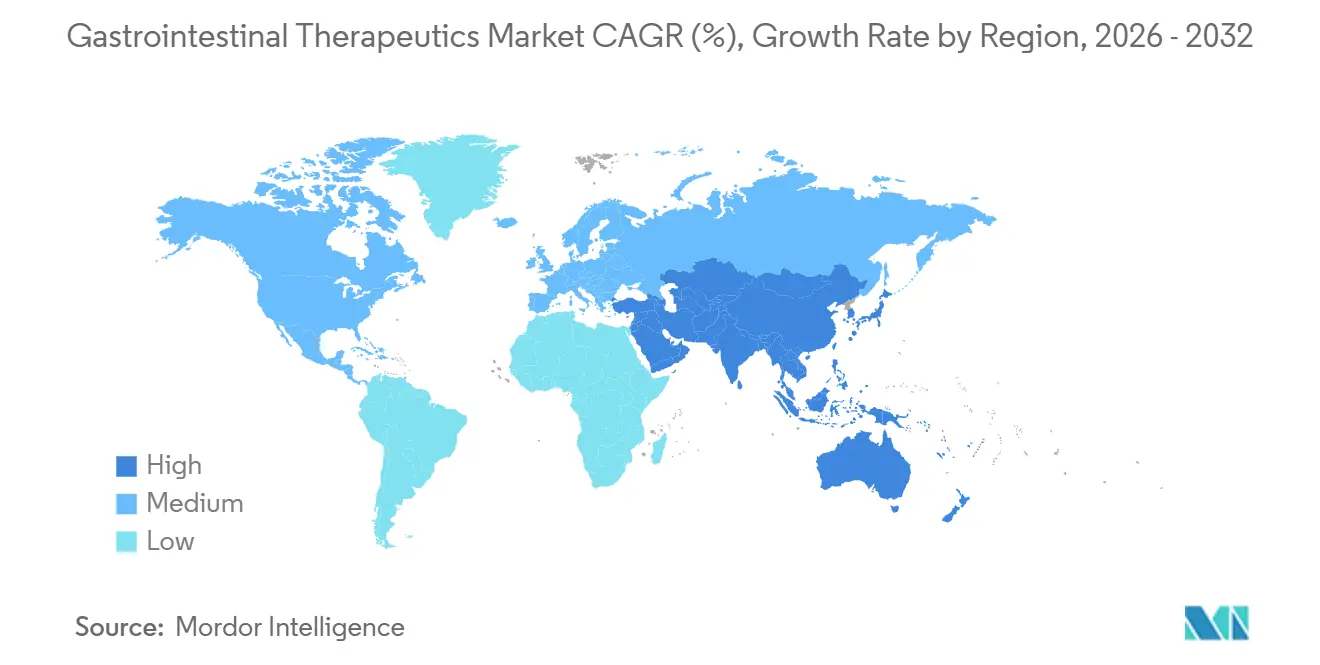

- By geography, North America led with a 38.61% revenue share in 2025; Asia-Pacific is the fastest-growing region, with a 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastrointestinal Therapeutics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of digestive disorders | +1.2% | Global, with higher impact in Asia-Pacific and aging Western populations | Medium term (2-4 years) |

| Uptake of next-gen biologics & biosimilars | +0.8% | North America, Europe, Japan, with spillover to urban Asia-Pacific | Long term (≥ 4 years) |

| Smart-pill & sensor delivery growth | +0.9% | Global, concentrated in developed markets with regulatory frameworks | Short term (≤ 2 years) |

| Commercialisation of live microbiome therapies | +0.4% | North America, Europe, with gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| AI-enabled drug-repurposing momentum | +0.6% | North America, Europe, early adoption in select Asia-Pacific markets | Long term (≥ 4 years) |

| VC shift to nutrition-pharma hybrids | +0.3% | Global, with concentration in research-intensive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Digestive Disorders

As countries increasingly adopt Western dietary patterns, the global incidence of inflammatory bowel disease (IBD) and functional bowel conditions is on the rise. On January 1, 2024, New Zealand reported an IBD prevalence of 671 cases per 100,000 residents.[1]The Lancet Editorial Team, “Global Burden of Digestive Diseases,” TheLancet.com Meanwhile, projections indicate that by 2050, India could see numbers soaring to 456,921 patients.[2]The Lancet Editorial Team, “Global Burden of Digestive Diseases,” TheLancet.com In sub-Saharan Africa, the limited specialist capacity, with fewer than 2 gastroenterologists per 100,000 people, hampers the uptake of biologics. In response, payers are experimenting with nurse-led infusion models, achieving a 40% reduction in per-patient costs without compromising safety. Consequently, while competition from biosimilars has moderated prices, the volume growth remains robust.

Uptake of Next-Generation Biologics & Biosimilars

By Q4 2025, biosimilars accounted for 45% of new biologic initiations in Europe, compared with 22% in the United States. Amgen’s adalimumab biosimilar achieved an 18% share of Humira’s U.S. market volume within 12 months of its 2023 launch. Originator companies are mitigating market erosion through differentiated assets, with AbbVie’s Skyrizi and Rinvoq collectively generating USD 13 billion in 2025, offsetting a 60% decline in Humira sales. Rapid escalation protocols now transition patients to advanced treatments within 18 months of diagnosis, halving the 2020 interval and improving hospitalization outcomes.

Smart-Pill & Sensor Delivery Growth

In August 2024, the FDA approved Medtronic’s PillSense, an ingestible sensor enabling real-time gastric pH tracking to optimize PPI dosing. Subsequently, the PillCam Genius, which utilizes AI for capsule endoscopy and delivers 94% lesion sensitivity, received approval in November 2024.[3]Medtronic, “PillCam Genius Press Release,” Medtronic.com To address the 40% non-compliance rate in ulcerative colitis, Japan introduced a fast-tracked digital mesalamine platform with integrated adherence sensors. With unit costs now below USD 50, these disposables have become economically viable for chronic monitoring.

Commercialization of Live Microbiome Therapies

The FDA-approved VOWST for Clostridioides difficile infection prevention validates live biotherapeutic modalities and attracted a USD 175 million acquisition by Nestlé Health Science. Phase 1b data for SER-155 point to broader applications in immunocompromised patients, and multiple academic consortia are mapping strain-specific gene clusters to optimize efficacy. Early commercial success spurs venture funding for start-ups developing targeted consortia therapies for ulcerative colitis and hepatic encephalopathy. In 2024, Rebyota and Vowst became the first FDA-approved live biotherapeutics for recurrent C. difficile, establishing a new regulatory pathway. Dedicated microbiome research centers are scaling up, with India’s AIG Hospitals launching a national hub in January 2026 to accelerate gut-based therapeutic development. Lower development costs and favorable safety profiles are attracting venture capital, expediting market entry.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High biologic costs | -0.7% | Global, with higher impact in emerging markets and cost-sensitive healthcare systems | Short term (≤ 2 years) |

| Patent cliffs 2026-29 | -0.5% | North America, Europe, with varying impact across payer systems | Medium term (2-4 years) |

| Specialist shortages in emerging markets | -0.6% | Global, concentrated in markets with established biosimilar frameworks | Short term (≤ 2 years) |

| Long-term PPI safety concerns | -0.4% | Asia-Pacific, Latin America, Africa, with rural area concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Biologic Costs

Annual biologic treatment can exceed USD 50,000, straining public and private payers that increasingly impose prior-authorization hurdles. Value-based contracts tie reimbursement to real-world outcomes, compelling manufacturers to fund post-marketing studies. Specialty pharmacies consolidate to negotiate steeper discounts, eroding gross margins yet expanding patient reach through copay-assistance programs. Emerging-market governments explore pooled procurement to lower unit prices, but constrained budgets delay the uptake of biologics compared with small-molecule alternatives. Although biosimilars promise relief, originators often counter with life-cycle management strategies, such as high-concentration formulations, thereby prolonging price rigidity.

Limited Specialist Availability in Emerging Nations

A projected shortfall of 1,630 gastroenterologists in the United States by 2025 mirrors shortages across Asia-Pacific and Latin America, where rural counties lack any GI specialists. Tele-endoscopy hubs and AI-assisted capsule-imaging interpretation mitigate access gaps but depend on broadband penetration and clinician training. Pharmaceutical firms partner with medical societies to expand fellowship slots, yet the pipeline lags behind the growth in demand. Private-equity-funded clinic chains are scaling endoscopy services in India and Brazil but face regulatory scrutiny over care quality. Persistent workforce deficits slow diagnosis and treatment initiation, tempering near-term sales potential for advanced therapies in underserved regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Microbiome Agents Outpace Mature Categories

Proton pump inhibitors remained the revenue anchor in 2025, holding 23.78% gastrointestinal therapeutics market share, underpinned by widespread management of gastroesophageal reflux disease and ulcer prophylaxis. Branded PPIs still command premiums in hospital formularies where rapid-acting IV formulations are required for acute bleeding, though generics dominate retail channels. The gastrointestinal therapeutics market size attributable to PPIs is expected to plateau as guideline revisions advocate step-down therapy to minimize long-term adverse effects. In parallel, the biologics segment captures incremental spend through anti-TNF agents, IL-12/23 inhibitors, and JAK inhibitors, but faces biosimilar erosion post-2025. Antibiotics, led by rifaximin, retain niche applications in hepatic encephalopathy and small-intestinal bacterial overgrowth, aided by label expansions.

Microbiome-based therapies comprise the fastest-growing drug class at a 4.33% CAGR, albeit from a low base, benefiting from VOWST’s commercial traction and promising pipelines like SER-155 for immunocompromised hosts. Live biotherapeutic product standardization and scalable anaerobic manufacturing processes cut production costs, narrowing the price gap with conventional biologics. Pharma-food cross-sector collaborations, as exemplified by Nestlé Health Science, infuse diet-adjacent capabilities such as prebiotic adjuncts that enhance colonization. Over the forecast period, the gastrointestinal therapeutics market size for microbiome products is expected to expand as payers accept real-world evidence of relapse reduction in recurrent C. difficile infection.

By Disease Indication: IBS Dominates, GI Cancer Accelerates

Inflammatory bowel disease accounted for 29.08% of the gastrointestinal therapeutics market in 2025, generating stable chronic-care revenues through treat-to-target protocols that emphasize mucosal healing. The approach increases biologic dosing frequency and supports the uptake of companion diagnostics, aligning with value-based care metrics. Biosimilar entry for Stelara and Humira suppresses average selling prices yet widens eligible-patient cohorts, softening unit-price erosion. Emerging small-molecule S1P modulators and oral JAK inhibitors may cannibalize anti-TNF share but overall elevate category sales through oral-route convenience.

Gastrointestinal cancer therapeutics advance at a 4.86% CAGR, driven by precision oncology regimens integrating checkpoint inhibitors with targeted small molecules. AI-enabled colonoscopy improves adenoma detection, facilitating earlier intervention that increases adjuvant-therapy cycles and overall prescriptions. Biomarker-guided therapy for gastric and pancreatic cancers widens patient stratification, and companion diagnostics enhance reimbursement prospects. Though volumes remain smaller than those for reflux or motility disorders, oncology’s premium pricing and continuous line-extension strategies are boosting its revenue trajectory in the gastrointestinal therapeutics market.

By Route of Administration: Injectables Gain as Oral Dominates

Oral formulations accounted for 62.55% of the gastrointestinal therapeutics market share in 2025, owing to patient convenience and well-established generics across the acid-suppression and motility segments. Yet adherence issues persist in chronic regimens, prompting digital pill-dispensing solutions that track ingestion events and alert caregivers. Oral biologic platforms leveraging permeation enhancers and nanocarriers are in early clinical testing, aiming to capture share from injectables without compromising efficacy.

Injectables are the fastest-growing route, projected to grow at a 4.65% CAGR through 2031, as large-volume subcutaneous devices enable self-administration previously limited to infusion centers. Hyaluronidase-based co-formulation permits 10-mL subcutaneous dosing, cutting infusion-chair time and hospital overhead. Smart-injector pens offer biometric-based lockout to prevent dosing errors and capture adherence analytics for payer reporting. Although rectal and transdermal routes serve niche populations such as maintenance therapy in distal ulcerative colitis, their market contribution remains marginal within the broader gastrointestinal therapeutics market.

By Distribution Channel: Online Pharmacies Disrupt Hospital Dominance

In 2025, hospital pharmacies accounted for 45.21% of distribution revenue, driven by biologics from infusion centers and complex inpatient protocols. Online pharmacies, expanding at a 4.44% CAGR, are utilizing cold-chain logistics and telehealth to deliver specialty drugs directly to patients.

Regulatory approvals for electronic verification of Risk Evaluation and Mitigation Strategy products have expanded the online market. Home nurse infusions are reducing per-dose costs by 30%, increasing price transparency, and challenging traditional hospital markups in the gastrointestinal therapeutics market.

Geography Analysis

North America delivered 38.61% of global revenue in 2025, propelled by high biologic penetration and supportive reimbursement environments despite pronounced specialist shortages across 69.3% of counties. Tele-gastroenterology networks and capsule endoscopy interpretation centers extend reach, but the backlog for elective colonoscopy still stretches clinician capacity. Biosimilar adoption accelerates after updated interchangeability rules, with payer formularies quickly prioritizing cost-saving options.

Asia-Pacific is the fastest-growing region at a 5.12% CAGR as aging demographics in China and India intersect with government insurance expansion. Urban dietary shifts drive ulcerative colitis and Crohn’s disease incidence, steering investment toward biologics manufacturing facilities in Singapore and South Korea. Meanwhile, Japan’s super-aged society sustains steady demand for PPIs and prokinetics, although strict HTA controls temper price inflation. Digital-health startups capitalize on smartphone penetration to deliver microbiome-tracking apps, integrating seamlessly with hospital EMR systems to guide personalized therapy.

Europe maintains a balanced outlook, with Germany, the United Kingdom, and France jointly accounting for more than half of regional sales. HTA bodies negotiate aggressive price caps, spurring rapid biosimilar uptake that broadens patient access yet compresses margins. Southern European countries are exploring outcome-based payment models for high-cost biologics, mirroring pilot programs in Scandinavia. In South America and the Middle East & Africa, Brazil and Saudi Arabia spearhead adoption of endoscopy capital equipment and biologics, leveraging public-private partnerships to upgrade hospital infrastructure. Nonetheless, payer fragmentation and import tariffs slow widespread uptake, keeping these regions at an earlier stage of the gastrointestinal therapeutics market development curve.

Competitive Landscape

Market concentration remains moderate. A consortium of AbbVie, Takeda, Janssen, Pfizer, and Amgen commands approximately 40% of global revenue, creating opportunities for microbiome specialists and regional biosimilar firms. These incumbents are strengthening their market share through line extensions and next-generation assets. AbbVie’s Skyrizi secured Crohn’s approval in June 2024, while Takeda is co-developing its vedolizumab biosimilar to mitigate competitive threats.

Technology is transforming the competitive landscape. Insilico Medicine has reduced discovery timelines to 18 months for an IBD candidate currently in Phase II, highlighting AI's ability to diminish Big Pharma’s traditional scale advantage. Additionally, digital health is emerging as a key differentiator: Medtronic’s smart-pill ecosystem integrates diagnostics with dosing algorithms, generating proprietary data that is difficult for competitors to replicate.

Distribution capabilities remain critical. The FDA's Risk Evaluation and Mitigation Strategy requirements restrict biosimilar access to certified channels, reinforcing the advantage of established players. However, new entrants in the live microbiome segment face fewer cold-chain complexities and can collaborate with consumer-health brands, introducing agility into the gastrointestinal therapeutics market.

Gastrointestinal Therapeutics Industry Leaders

Abbvie Inc.

Bausch Health Companies Inc. (Salix Pharmaceuticals Inc.)

Takeda Pharmaceutical Co.

Johnson & Johnson Services, Inc. (Janssen)

AstraZeneca plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The FDA granted orphan designation to Cellenkos’s CK0804, an allogeneic T-reg therapy that reduced spleen volume and symptom burden in heavily pre-treated myelofibrosis patients.

- January 2026: Braintree Laboratories submitted an NDA for tegoprazan, a potassium-competitive acid blocker, seeking simultaneous approvals in three GERD indications.

- January 2026: The FDA awarded Breakthrough Therapy Designation to Cogent Biosciences’ bezuclastinib plus sunitinib for gastrointestinal stromal tumors after imatinib failure.

Global Gastrointestinal Therapeutics Market Report Scope

As per the scope of the report, gastrointestinal disorders are medical conditions related to the digestive system that affect the colon, small and large intestine, and rectum. The disorders mainly include constipation, peptic ulcer diseases, and irritable bowel syndrome, characterized by various symptoms such as pain, bloating, diarrhea, nausea, and vomiting.

The gastrointestinal therapeutics market is segmented by drug type, dosage form, application, and geography. The drug type segment is further divided into biologics/ biosimilars, antacids, laxatives, antidiarrheal agents, antiemetics, antiulcer agents, and other drug types. The dosage form is further segmented into oral, parenteral, and other dosage forms. The application is further bifurcated into ulcerative colitis, irritable bowel syndrome, Crohn's disease, celiac disease, gastroenteritis, and other applications. The geography region is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for countries across major regions globally. The report offers the value (in USD) for the above segments.

| Proton Pump Inhibitors | |

| H2 Receptor Antagonists | |

| Antacids & Alginates | |

| Prokinetics | |

| Laxatives | Bulk-forming |

| Osmotic | |

| Stimulant | |

| Lubricant / Emollient | |

| Anti-emetics | 5-HT3 Antagonists |

| NK-1 Antagonists | |

| Dopamine Antagonists | |

| Antispasmodics | |

| Biologics & Biosimilars | Anti-TNF Agents |

| Anti-integrin Agents | |

| IL-12/23 Inhibitors | |

| JAK Inhibitors (Small-molecule) | |

| S1P Modulators | |

| Antibiotics (e.g., Rifaximin) | |

| GLP-2 & GLP-1 Analogues | |

| Microbiome-based Therapeutics | |

| Others (Bile-acid sequestrants, enzymes) |

| Gastro-esophageal Reflux Disease (GERD) |

| Peptic Ulcer Disease |

| Functional Dyspepsia |

| Irritable Bowel Syndrome (IBS) |

| Chronic Idiopathic Constipation (CIC) |

| Ulcerative Colitis |

| Crohn's Disease |

| Clostridioides difficile Infection |

| Short Bowel Syndrome |

| Gastrointestinal Cancer |

| GI Motility Disorders |

| Others (Eosinophilic Esophagitis, etc.) |

| Oral | Immediate-release |

| Delayed / Enteric-coated | |

| Extended-release | |

| Injectable | Intravenous |

| Subcutaneous | |

| Rectal | Suppositories |

| Foams / Enemas | |

| Parenteral Infusion Pumps | |

| Others (Transdermal, Intranasal) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Specialty Clinics / Infusion Centres |

| Others (Home-care Settings) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Proton Pump Inhibitors | |

| H2 Receptor Antagonists | ||

| Antacids & Alginates | ||

| Prokinetics | ||

| Laxatives | Bulk-forming | |

| Osmotic | ||

| Stimulant | ||

| Lubricant / Emollient | ||

| Anti-emetics | 5-HT3 Antagonists | |

| NK-1 Antagonists | ||

| Dopamine Antagonists | ||

| Antispasmodics | ||

| Biologics & Biosimilars | Anti-TNF Agents | |

| Anti-integrin Agents | ||

| IL-12/23 Inhibitors | ||

| JAK Inhibitors (Small-molecule) | ||

| S1P Modulators | ||

| Antibiotics (e.g., Rifaximin) | ||

| GLP-2 & GLP-1 Analogues | ||

| Microbiome-based Therapeutics | ||

| Others (Bile-acid sequestrants, enzymes) | ||

| By Disease Indication | Gastro-esophageal Reflux Disease (GERD) | |

| Peptic Ulcer Disease | ||

| Functional Dyspepsia | ||

| Irritable Bowel Syndrome (IBS) | ||

| Chronic Idiopathic Constipation (CIC) | ||

| Ulcerative Colitis | ||

| Crohn's Disease | ||

| Clostridioides difficile Infection | ||

| Short Bowel Syndrome | ||

| Gastrointestinal Cancer | ||

| GI Motility Disorders | ||

| Others (Eosinophilic Esophagitis, etc.) | ||

| By Route of Administration | Oral | Immediate-release |

| Delayed / Enteric-coated | ||

| Extended-release | ||

| Injectable | Intravenous | |

| Subcutaneous | ||

| Rectal | Suppositories | |

| Foams / Enemas | ||

| Parenteral Infusion Pumps | ||

| Others (Transdermal, Intranasal) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Specialty Clinics / Infusion Centres | ||

| Others (Home-care Settings) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value for gastrointestinal therapeutics market?

The gastrointestinal therapeutics market is 43.74 billion and grow at 4.29% CAGR through 2031.

Which drug class is growing fastest within gastrointestinal therapeutics?

Microbiome-based live biotherapeutics lead growth at a 4.33% CAGR due to successful commercialization of VOWST and a robust pipeline.

How significant is the specialist shortage for gastrointestinal care?

In 2025, 69.3% of U.S. counties lack a gastroenterologist, underscoring an access gap that boosts telemedicine and AI-driven diagnostic adoption.

Which region will post the highest CAGR to 2031?

Asia-Pacific is forecast to expand at 5.12% CAGR, fueled by aging populations, rising healthcare spending, and increased digestive-disease burden.

How will biosimilar entry affect market pricing?

Patent expiries such as Stelaras in 2025 invite biosimilars that lower average selling prices yet broaden patient access, sustaining revenue growth.

What is the outlook for injectable versus oral formulations?

Oral routes still dominate at 62.55% share but injectables are the fastest-growing at 4.65% CAGR, aided by large-volume subcutaneous delivery systems.

Page last updated on: