United States Veterinary Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

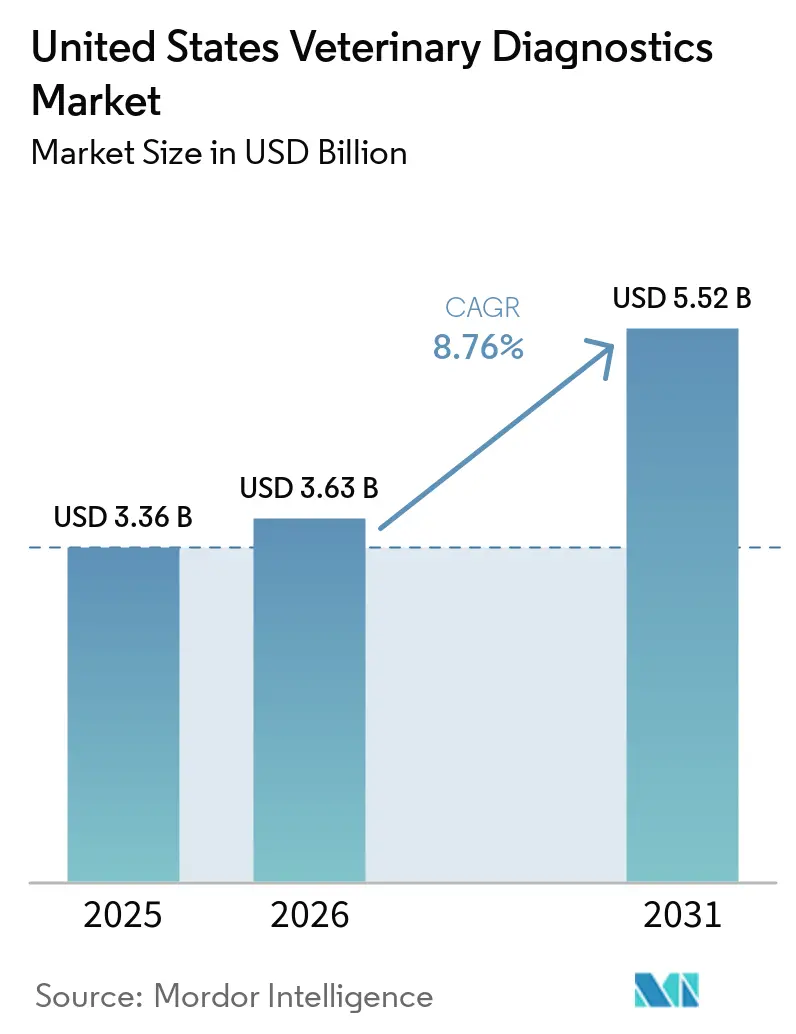

| Base Year Market Size (2025) | USD 3.36 Billion |

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 5.52 Billion |

| Growth Rate (2026 - 2031) | 8.76% CAGR |

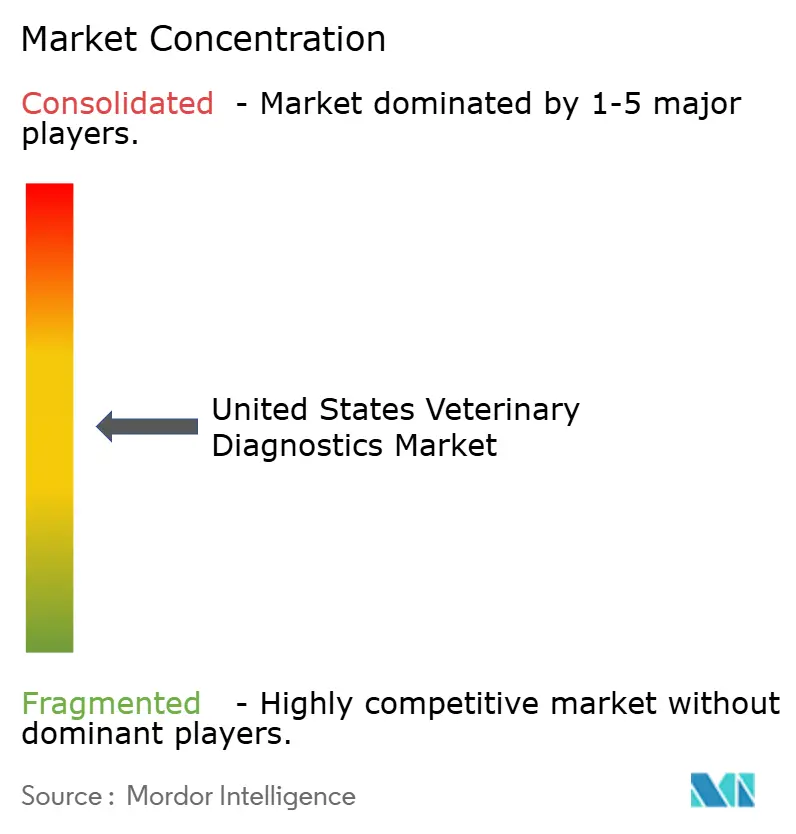

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Veterinary Diagnostics Market Analysis by Mordor Intelligence

The United States Veterinary Diagnostics Market size is projected to be USD 3.36 billion in 2025, USD 3.63 billion in 2026, and reach USD 5.52 billion by 2031, growing at a CAGR of 8.76% from 2026 to 2031.

Growth in the United States veterinary diagnostics market is being supported by a deeper use of bloodwork panels, imaging, and screening during routine appointments, which has lifted diagnostic revenue even when practice visit volumes have been under pressure. Companion animal care remains the main revenue base, supported by 95 million pet-owning U.S. households and USD 41.4 billion in veterinary care spending in 2025, while insurance expansion is making higher-value testing easier to accept at the point of care. The United States veterinary diagnostics market is also being strengthened by mandatory HPAI H5N1 raw-milk PCR surveillance, which has pushed molecular testing into a more durable role in livestock care. AI-based cytology, imaging, and blood-based oncology tools are shortening turnaround times and broadening the menu of tests that practices can use in regular workflows, while larger networks continue to favor integrated instrument, software, and reagent ecosystems from major suppliers.

Key Report Takeaways

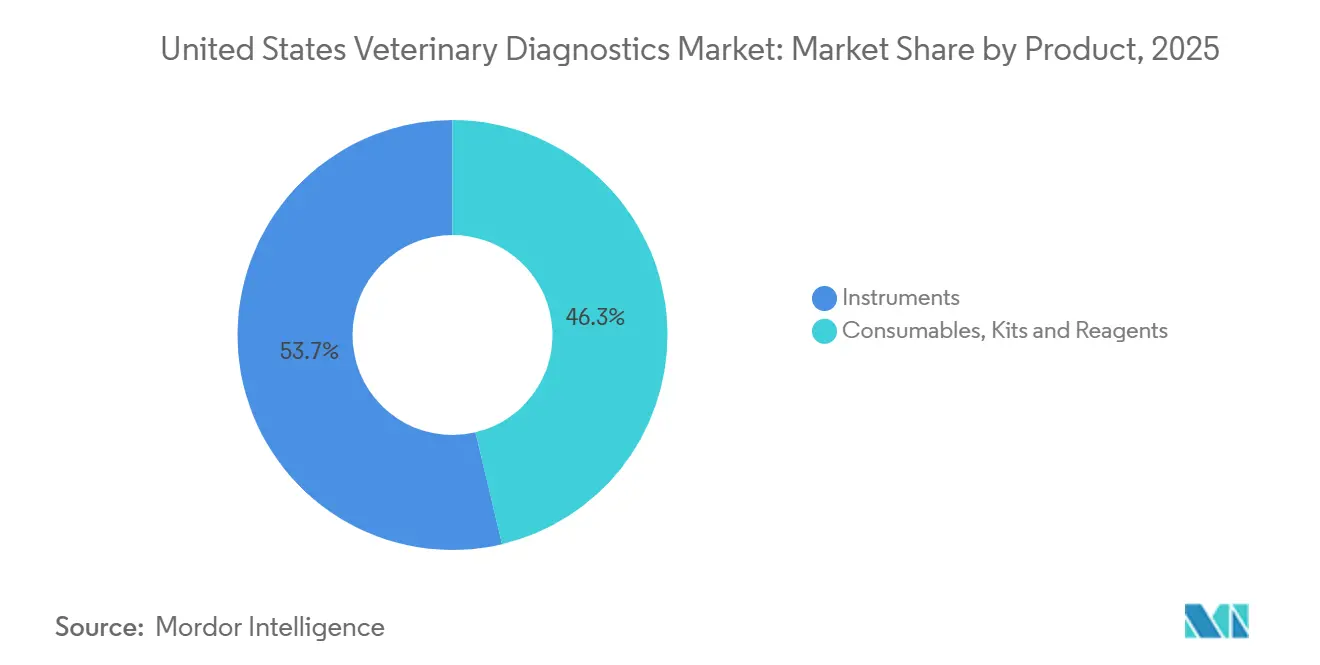

- By product, consumables, kits, and reagents held 46.27% revenue share in 2025, while instruments in the United States veterinary diagnostics market are forecast to expand at 9.08% CAGR through 2031.

- By technology, immunodiagnostics led with 35.79% of revenue in 2025, while molecular diagnostics in the United States veterinary diagnostics market are projected to grow at 8.38% CAGR through 2031.

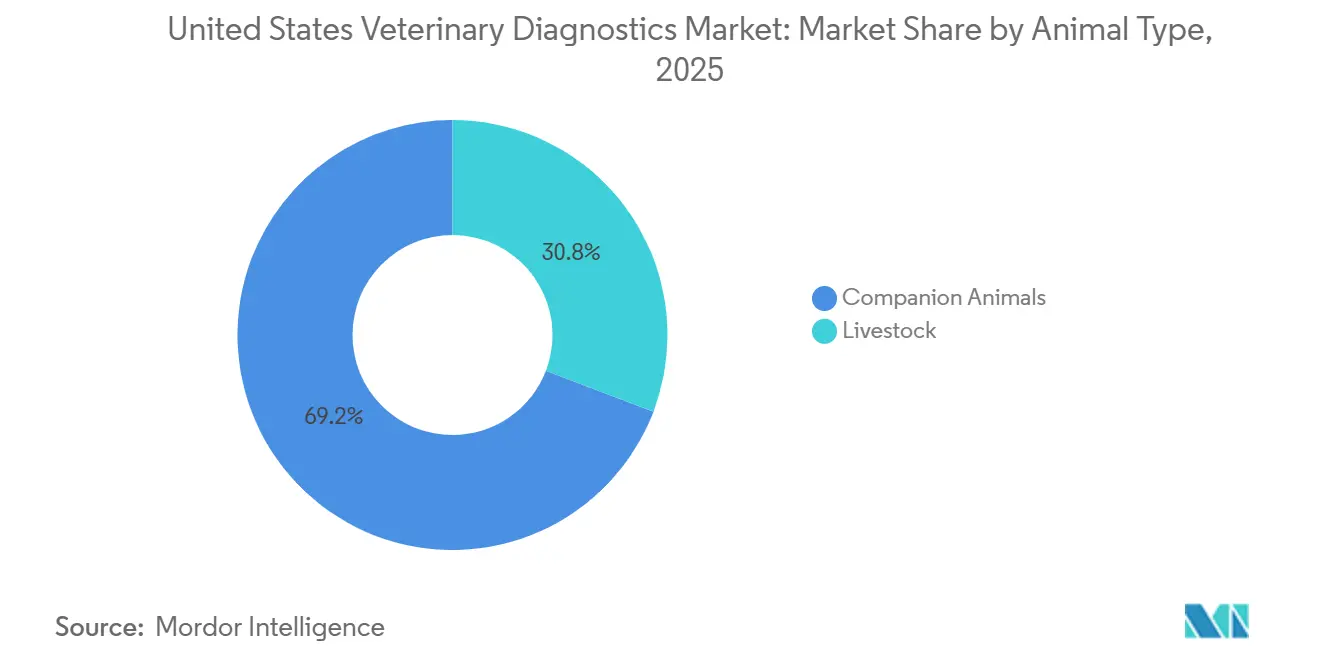

- By animal type, companion animals held 69.22% of revenue in 2025, while livestock is forecast to record the fastest growth at 9.96% CAGR through 2031.

- By application, infectious diseases accounted for 42.82% of revenue in 2025, while oncology is projected to advance at 10.49% CAGR through 2031.

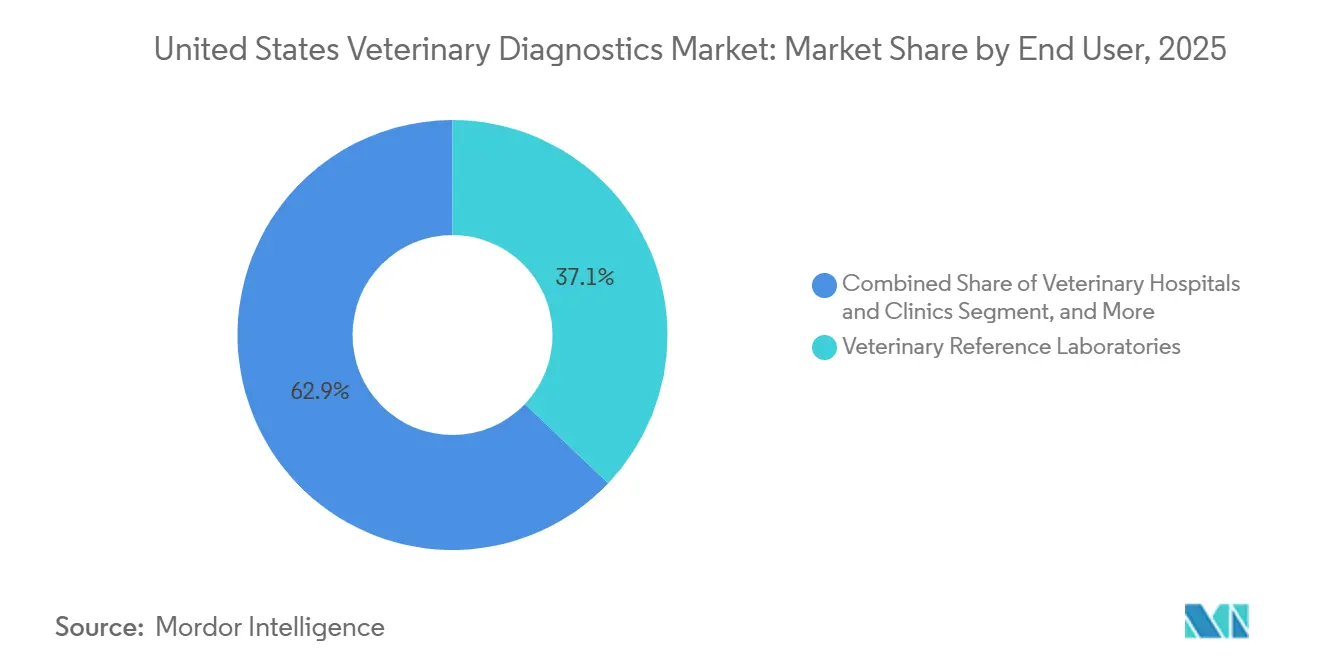

- By end user, veterinary reference laboratories held 37.12% of revenue in 2025, while point-of-care and in-house testing in the United States veterinary diagnostics market is forecast to grow at 10.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Veterinary Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Companion Animal Health Spend | +2.8% | National, with peak intensity in California, Texas, Florida, and New York | Medium term (2-4 years) |

| Expansion of In-Clinic and Point-of-Care Testing | +2.1% | National, with early adoption concentration in the urban Northeast and Pacific Coast | Short term (≤ 2 years) |

| AI-Enabled Interpretation of Images and Bloodwork | +1.5% | National, with faster uptake in corporate chain practices and specialist referral centers | Medium term (2-4 years) |

| Wider Use of Molecular and Rapid Assays in Routine Practice | +1.4% | National, with HPAI surveillance concentrated in Midwest and Southwest dairy and poultry belts | Medium term (2-4 years) |

| Corporate Chain Standardization and Bulk Reagent Buying | +0.9% | National, concentrated in suburban and metropolitan markets | Long term (≥ 4 years) |

| Under-Served Mobile and Ambulatory Veterinary Models | +0.4% | Rural Midwest, Appalachian South, and Mountain West states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Health Spend

Pet insurance penetration in the United States reached 3.9% of the total pet population in 2024, covering 6.4 million dogs and cats, while gross written premiums exceeded USD 4.74 billion and rose 21.4% year over year.[1]National Association of Insurance Commissioners, “Pet Insurance Model Act,” NAIC, content.naic.org That still leaves most pets outside formal reimbursement, which means the United States veterinary diagnostics market continues to face a meaningful out-of-pocket limit on premium panel adoption. At the same time, insured households are more able to accept deeper diagnostic workups because accident and illness plans commonly cover testing costs tied to clinical evaluation. State-level standard setting through the Pet Insurance Model Act supports broader policy consistency and should make insurance easier to scale through the forecast period. The result is a market where premium visits are becoming more diagnostics-intensive, while uninsured visits remain more price sensitive across the United States veterinary diagnostics market.

Expansion of In-Clinic and Point-of-Care Testing

The United States veterinary diagnostics market is seeing faster growth in in-clinic testing because compact analyzers now fit both standard hospitals and smaller ambulatory models. Zomedica’s TRUFORMA platform shows this shift clearly, as the system is built to deliver endocrine assays in a compact format that can work in practices with limited space and in mobile settings. As more practices place point-of-care systems, the revenue profile moves beyond one-time hardware sales and toward recurring consumable pull. This is important because point-of-care and in-house testing is the fastest-growing end-user channel, with forecast growth of 10.2% through 2031 in the United States veterinary diagnostics market. The broader effect is that faster in-house turnaround is becoming part of routine care expectations, especially where same-visit clinical decisions matter most.

AI-Enabled Interpretation of Images and Bloodwork

AI tools are becoming part of the normal diagnostic workflow rather than stand-alone pilot programs in the United States veterinary diagnostics market. Zoetis expanded Vetscan Imagyst to seven AI-powered microscopic testing capabilities and launched AI Masses in June 2025 for the cytologic classification of common lymph node and skin or subcutaneous lesions in minutes. IDEXX also broadened its oncology workflow, with inVue Dx moving into fine-needle aspirate cytology, and Cancer Dx already adopted by more than 6,000 practices in the United States and Canada before the mast cell tumor expansion announced in January 2026. A 2025 review in Frontiers in Veterinary Science noted that veterinary AI still depends on larger standardized training datasets and better image annotation across species, which means scale and data ownership matter as much as algorithm design. That gives early movers a durable advantage, especially when AI is tied to installed analyzers, connected software, and reference laboratory support across the United States veterinary diagnostics market.

Wider Use of Molecular and Rapid Assays in Routine Practice

Molecular testing is moving further into everyday care in the United States veterinary diagnostics market because both oncology screening and livestock surveillance now require more advanced assays. A 2024 study in the Journal of the American Veterinary Medical Association showed that a blood-based liquid biopsy test that combined cell-free DNA quantification with next-generation sequencing reached 71.3% sensitivity and 98.7% specificity across 7 canine cancer types.[2]S. Tsumoto et al., “High-Sensitivity Multicancer Detection of Stage 1 Cancer in Dogs,” American Journal of Veterinary Research, avmajournals.avma.org A second study published in the American Journal of Veterinary Research in June 2025 reported stage 1 multicancer detection sensitivities ranging from 68% to 98% across 5 canine cancer types using peptide microarrays. On the livestock side, USDA’s December 2024 Federal Order established nationwide raw-milk PCR testing under the National Milk Testing Strategy, which expanded laboratory demand and equipment needs across the National Animal Health Laboratory Network. This mix of companion-animal cancer screening and mandated herd surveillance gives molecular diagnostics one of the broadest demand bases in the United States veterinary diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Veterinarian and Laboratory Technician Shortages | -0.7% | National, acute in rural Midwest, Mountain West, and Southeast livestock regions | Medium term (2-4 years) |

| High Cost of Advanced Diagnostics for Price-Sensitive Owners | -0.4% | National, with disproportionate impact in lower-income and rural catchment areas | Long term (≥ 4 years) |

| Fragmented Workflow Integration Across Practice Software and Devices | -0.3% | National, more pronounced in independent practices operating mixed-vendor instrument fleets | Medium term (2-4 years) |

| Limited Reimbursement Visibility for Premium Diagnostics | -0.2% | National, with highest friction in states without mature pet insurance penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Veterinarian and Laboratory Technician Shortages

The United States veterinary diagnostics market continues to face a supply constraint because companion-animal veterinarian numbers rose over the past decade, while mixed-animal and agricultural veterinarian numbers moved lower, widening the service gap in food-animal care. Federal capacity also weakened in 2025 when USDA APHIS lost more than 1,300 staff members, including a reported 20% to 30% of personnel at a key animal disease testing laboratory. That leaves commercial laboratories carrying more of the response burden during outbreaks, even though the United States veterinary diagnostics market still depends on veterinarians to collect, interpret, and follow up on samples. Technician shortages add another bottleneck because cytology, histopathology, and specialized lab workflows cannot yet be fully automated at a commercial scale. The pressure is strongest in rural livestock territories, where test demand exists but local clinical capacity remains too thin to convert all of that demand into steady revenue.[3]USDA, “USDA Expands Efforts to Strengthen Rural Food Animal Veterinary Workforce and Protect America’s Food Supply,” USDA, usda.gov

High Cost of Advanced Diagnostics for Price-Sensitive Owners

Only 3.9% of the U.S. pet population carried insurance coverage at the end of 2024, which means most visits in the United States veterinary diagnostics market still rely on owner willingness to pay at the clinic. This matters because oncology liquid biopsy panels, multi-analyte endocrine testing, and sequencing-based workflows sit above the price points that many owners accept without reimbursement support. Practice behavior already reflects that tension, with smaller analytics-supported clinics in 2025 improving revenue partly by leaning away from premium diagnostics that clients were more likely to decline and toward mid-tier tests with better acceptance. IDEXX’s decision to price the Cancer Dx lymphoma panel from as low as USD 15 shows that major suppliers are actively trying to lower the consent barrier for early cancer testing. Until insurance coverage becomes broader, affordability will keep shaping the pace at which advanced tests move from specialist use into mainstream care across the United States veterinary diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Anchor Revenue as Instrument Investments Accelerate

Consumables, kits, and reagents held 46.27% of the United States veterinary diagnostics market share in 2025, making them the largest product category by revenue. This position reflects the recurring nature of assay cartridges, slides, reagents, and test kits that follow every successful analyzer placement in the United States veterinary diagnostics industry. Once a clinic commits to a platform such as IDEXX Catalyst or Zoetis Vetscan, repeat ordering becomes a stable part of operating spend rather than a discretionary purchase cycle. The United States veterinary diagnostics market also benefits here from stronger diagnostic intensity per visit, because higher test depth lifts reagent use even when visit growth is modest.

Instruments are forecast to grow at 9.08% CAGR through 2031, which makes them the fastest-growing product segment in the United States veterinary diagnostics market. The current investment cycle is being supported by hardware replacement, AI-enabled imaging upgrades, and demand for compact systems that fit smaller footprints. IDEXX’s January 2026 launch of the ImageVue DR50 Plus added an imaging option with AI support and up to 60% lower radiation exposure than competing veterinary systems, which shows how vendors are using differentiated hardware to justify new placements. Corporate groups can absorb this capital spending more easily because they buy across many sites, while independents face the same competitive pressure with less pricing leverage. Over time, each new placement expands the downstream consumables tail, which keeps product growth in the United States veterinary diagnostics industry tied to both equipment refresh and recurring test use.

By Technology: Immunodiagnostics Leads While Molecular Diagnostics Redefine Scope

Immunodiagnostics led with 35.79% of revenue in 2025, supported by high-frequency use in infectious disease panels, vector-borne disease testing, heartworm screening, and allergy diagnostics. These assays have long been part of standard wellness and disease management protocols, which gives them broad installed-base support in both clinics and reference laboratories. Clinical biochemistry and hematology remain central to routine internal medicine because they support liver, kidney, endocrine, and complete blood count evaluation across large patient volumes. That steady test mix keeps mature technologies relevant even as the United States veterinary diagnostics market adds newer methods at the margin.

Molecular diagnostics are projected to grow at 8.38% CAGR through 2031, which makes them the fastest-expanding technology segment. USDA’s National Milk Testing Strategy created a lasting role for PCR infrastructure in dairy herd surveillance after the December 2024 Federal Order. In companion animals, peer-reviewed validation has strengthened the case for liquid biopsy and related molecular tools in earlier cancer detection, including 98.7% specificity in a 2024 canine screening study. These parallel use cases matter because they reduce dependence on a single disease area or animal population. The technology mix is therefore widening the practical scope of the United States veterinary diagnostics market rather than replacing legacy formats outright.

By Animal Type: Companion Animals Lead Despite Faster Livestock Expansion

Companion animals accounted for 69.22% of revenue in 2025, giving them the clear lead in the United States veterinary diagnostics market size. The category benefits from the density of small-animal practices, higher spending per visit, and a clinical culture that already uses bloodwork, imaging, and specialized testing in a broad range of cases. Dogs contribute a large share of value because oncology, endocrinology, cardiology, and chronic disease monitoring often require repeated and multi-panel diagnostics. The segment is also supported by insurance growth and high owner engagement in preventive and follow-up care.

Livestock are forecast to grow at 9.96% CAGR through 2031, the fastest rate among animal types. That performance is tied to a heavier testing burden from outbreak surveillance and a wider commercial interest in precision herd health. California alone recorded 771 H5N1-positive dairy herds by September 2025, which shows how one disease front can drive major testing volumes in a short period. Cattle remain the largest livestock test base, followed by poultry and swine, because surveillance and disease management require repeated assay use across large populations. As crisis testing gradually blends into more routine herd monitoring, livestock should keep gaining weight in the United States veterinary diagnostics market.

By Application: Infectious Diseases Hold the Largest Base While Oncology Advances Fastest

Infectious diseases commanded 42.82% of revenue in 2025, which made them the largest application segment in the United States veterinary diagnostics market. The category spans companion and livestock care, covering routine wellness tests as well as outbreak response for diseases such as heartworm, Lyme disease, feline leukemia, HPAI H5N1, and bovine respiratory disease complex. This wide clinical scope gives infectious disease testing a repeat-use profile that few other applications can match. USDA livestock surveillance requirements have reinforced that volume-based since 2024, especially for dairy-related PCR workflows.

Oncology is projected to grow at 10.49% CAGR through 2031, making it the fastest-growing application in the United States veterinary diagnostics market. New blood-based assays are expanding the addressable pool beyond referral settings and into general practice workflows. The June 2025 AJVR study on peptide microarrays reported stage 1 detection sensitivities from 68% to 98% across 5 canine cancer types, while a 2026 Frontiers in Veterinary Science paper evaluated OncoCan for diagnosis and prognosis monitoring through plasma cfDNA. Endocrinology is also deepening at the point of care, as shown by IDEXX’s Catalyst Cortisol Test launch in June 2025. Even so, oncology is where the strongest mix of pricing power, innovation, and workflow change is now emerging across the United States veterinary diagnostics market.

By End User: Reference Laboratories Retain Scale While Point-of-Care Gains Speed

Veterinary reference laboratories held 37.12% of the United States veterinary diagnostics market share in 2025, which kept them ahead of other end-user groups by revenue. Their lead comes from the depth of the menu, because cytology, histopathology, genetic testing, and advanced chemistry panels still require capabilities that most clinics cannot match in-house at comparable cost. Mars, through Antech and its wider veterinary network, and IDEXX Reference Laboratories remain central to this part of the market because they combine testing capacity with software and installed instruments. That structure gives the United States veterinary diagnostics industry a strong send-out backbone even as faster in-clinic options expand.

Point-of-care and in-house testing is forecast to grow at 10.17% CAGR through 2031, making it the fastest-growing end-user segment. TRUFORMA illustrates why this channel is widening, since its endocrine testing platform was designed for fast turnaround and a small physical footprint suited to regular clinics and ambulatory practice. Hospitals and clinics remain the main sites of device placement, but research institutes and universities still play an important role because they generate validation data that later supports commercial adoption. This creates a split model in which reference laboratories keep scale and complexity, while point-of-care systems take a share in speed-sensitive workflows. That balance should remain a defining feature of the United States veterinary diagnostics market through 2031.

Geography Analysis

California sits at the center of demand in the United States veterinary diagnostics market because it combines a leading companion-animal base with one of the heaviest livestock surveillance burdens in the country. It represented 18.3% of all insured U.S. pets in 2024, which supports a stronger willingness to accept advanced testing in small-animal care. The state also recorded 771 H5N1-positive dairy herds by September 2025, which drove high PCR testing volumes and made outbreak surveillance a major revenue influence for commercial labs. Texas shows a similar two-sided structure because it combines large cattle, swine, and poultry populations with expanding urban companion-animal demand in Dallas-Fort Worth, Houston, and Austin. Florida and New York add to this high-value cluster, and together with California and Texas, they account for more than one-third of insured pets in the country, which supports above-average uptake of premium diagnostics.

The Midwest and Appalachian South show a different pattern, where unmet need is often limited by workforce capacity rather than by lack of clinical value. Rural counties have seen meaningful declines in mixed-animal service density, and shortage designations cover much of Oklahoma over a five-year period according to the Farm Journal Foundation. That weakens sample collection, interpretation, and follow-up, which keeps livestock testing revenue below its full potential in several states. USDA’s August 2025 rural veterinary workforce actions address that issue directly, but the benefit will take time to spread across the United States veterinary diagnostics market.

The Mountain West, Pacific Northwest, and Upper Midwest offer a third pattern that combines supply gaps with selective premium adoption. Colorado, Wyoming, and Montana have meaningful equine and cattle exposure, which creates room for compact diagnostic systems designed for ambulatory use. Washington and Oregon have also discussed workforce expansion support, which could improve the service side of testing access if those efforts move forward. In practice, the best regional opportunities in the United States veterinary diagnostics market sit where underserved geographies meet affordable in-house testing and better local clinical coverage.

Competitive Landscape

The United States veterinary diagnostics market is moderately concentrated in reference laboratories and installed consumables platforms, while remaining more fragmented in stand-alone hardware categories. IDEXX and Mars, through Antech and the wider veterinary care network around Banfield, VCA, and BluePearl, hold powerful positions because they combine laboratory services, software links, and recurring assay ecosystems. Those connected systems raise switching costs for practices and make platform depth as important as instrument price in competitive decisions. The same structure helps explain why the United States veterinary diagnostics market favors vendors that can sell hardware, assays, workflow software, and clinical interpretation together rather than as isolated products. Smaller challengers still have room to compete, but they usually gain traction first in specific niches such as mobile care, ambulatory settings, or single-application testing.

IDEXX has been reinforcing its installed base through product extensions rather than relying only on new hardware placements. In June 2026, the company integrated SDMA directly into standard Catalyst chemistry profiles, which added kidney evaluation to common point-of-care workflows without creating extra process steps for clinics. In January 2026, it launched the ImageVue DR50 Plus with AI-powered imaging and up to 60% lower radiation exposure than competing veterinary systems, while also expanding Cancer Dx to include canine mast cell tumor detection. These moves show a strategy built around menu expansion, workflow integration, and earlier disease detection inside the same customer base.

Zoetis is the clearest challenger among large animal health companies because it is building diagnostics around AI, imaging support, and data-linked interpretation. Its June 2025 launch of AI Masses on Vetscan Imagyst added rapid cytologic screening for common lesions, and its February 2026 agreement to acquire Neogen’s animal genomics business extended that push into precision animal health. bioMérieux also used targeted M&A when it acquired SpinChip Diagnostics in January 2025, adding rapid immunoassay capability that could support companion cardiology and adjacent testing needs. White space remains strongest in mobile practice, ambulatory livestock care, and newer molecular surveillance areas where large incumbents still do not control every workflow in the United States veterinary diagnostics market.

United States Veterinary Diagnostics Industry Leaders

Bio-Rad Laboratories, Inc.

bioMérieux SA

IDEXX Laboratories, Inc.

Neogen Corporation

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IDEXX Laboratories announced the integration of SDMA, a renal biomarker, directly into standard Catalyst CLIPs, making comprehensive kidney function evaluation part of the most common point-of-care chemistry profiles available to U.S. and Canadian veterinarians. This represents the fourth Catalyst menu expansion by IDEXX in under 2 years and deepens the consumable moat of its 75,000-unit global installed base.

- March 2026: Zoetis signed a definitive agreement to acquire Neogen Corporation's animal genomics business, a move that aligns Zoetis' livestock strategy with predictive and precision health capabilities. The transaction, expected to close in the second half of 2026, will add genomic data solutions and individualized care analytics across companion and livestock species.

- January 2026: IDEXX Laboratories launched the ImageVue DR50 Plus Digital Imaging System, its most advanced veterinary imaging solution, combining AI-powered imaging with up to 60% lower radiation versus competing veterinary systems. The product is currently available to U.S. and Canadian veterinary clinics, targeting practices with high imaging throughput.

- January 2026: IDEXX Laboratories announced the expansion of its Cancer Dx Panel to include canine mast cell tumor detection, mid-year 2026, North America, alongside the commercial rollout of FNA cytology on the inVue Dx Cellular Analyzer from Q4 2025. These innovations together address more than one-third of all canine cancer cases in a single platform.

United States Veterinary Diagnostics Market Report Scope

The United States veterinary diagnostics market refers to the commercial ecosystem of specialized tools, instruments, reagents, and laboratory services used to detect, monitor, and prevent health disorders, infectious diseases, and chronic conditions in both companion animals and livestock.

The United States Veterinary Diagnostics Market is segmented by product type, technology, animal type, application, and end user. By product type, the market includes consumables, kits and reagents and instruments. By technology, it spans immunodiagnostics, clinical biochemistry, molecular diagnostics, hematology, urinalysis, and other diagnostic technologies. By animal type, the market is divided into companion animals, including dogs, cats, and other pets, and livestock such as cattle, swine, poultry, and other farm animals. By application, diagnostics are used for infectious diseases, endocrinology, cardiology, oncology, and other clinical areas. Finally, by end user, adoption is seen across veterinary reference laboratories, veterinary hospitals and clinics, point‑of‑care and in‑house testing, and veterinary research institutes and universities.

| Consumables, Kits and Reagents |

| Instruments |

| Immunodiagnostics |

| Clinical Biochemistry |

| Molecular Diagnostics |

| Hematology |

| Urinalysis |

| Other Technologies |

| Companion Animals | Dogs |

| Cats | |

| Other Companion Animals | |

| Livestock | Cattle |

| Swine | |

| Poultry | |

| Other Livestock Animals |

| Infectious Diseases |

| Endocrinology |

| Cardiology |

| Oncology |

| Other Applications |

| Veterinary Reference Laboratories |

| Veterinary Hospitals and Clinics |

| Point-of-Care and In-House Testing |

| Veterinary Research Institutes and Universities |

| By Product | Consumables, Kits and Reagents | |

| Instruments | ||

| By Technology | Immunodiagnostics | |

| Clinical Biochemistry | ||

| Molecular Diagnostics | ||

| Hematology | ||

| Urinalysis | ||

| Other Technologies | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Other Companion Animals | ||

| Livestock | Cattle | |

| Swine | ||

| Poultry | ||

| Other Livestock Animals | ||

| By Application | Infectious Diseases | |

| Endocrinology | ||

| Cardiology | ||

| Oncology | ||

| Other Applications | ||

| By End User | Veterinary Reference Laboratories | |

| Veterinary Hospitals and Clinics | ||

| Point-of-Care and In-House Testing | ||

| Veterinary Research Institutes and Universities | ||

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for veterinary diagnostics in the United States?

The United States veterinary diagnostics market is projected to rise from USD 3.63 billion in 2026 to USD 5.52 billion by 2031 at an 8.76% CAGR.

Which animal group contributes the most revenue?

Companion animals led with 69.22% of revenue in 2025, supported by a large small-animal practice base, high owner engagement, and growing insurance support.

Which technology area is growing the fastest?

Molecular diagnostics is the fastest-growing technology segment, with 8.38% CAGR through 2031, supported by canine cancer screening advances and USDA-led raw-milk PCR surveillance.

Why is oncology becoming more important in veterinary testing?

Oncology is forecast to grow at 10.49% CAGR through 2031 because blood-based liquid biopsy and AI-supported cytology are helping move cancer detection closer to routine practice workflows.

Which end-user channel is expanding most quickly?

Point-of-care and in-house testing is the fastest-growing end-user segment at 10.17% CAGR through 2031, helped by compact analyzers that fit small clinics and ambulatory practice models.

Page last updated on: