North America Companion Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

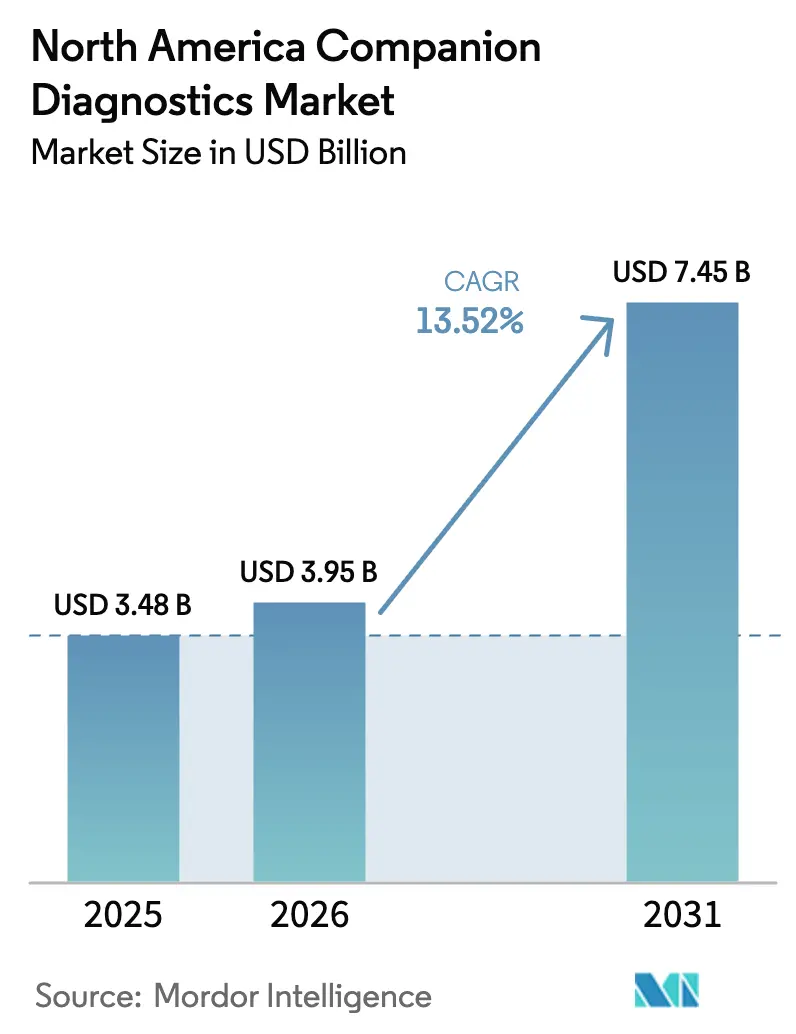

| Base Year Market Size (2025) | USD 3.48 Billion |

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 7.45 Billion |

| Growth Rate (2026 - 2031) | 13.52% CAGR |

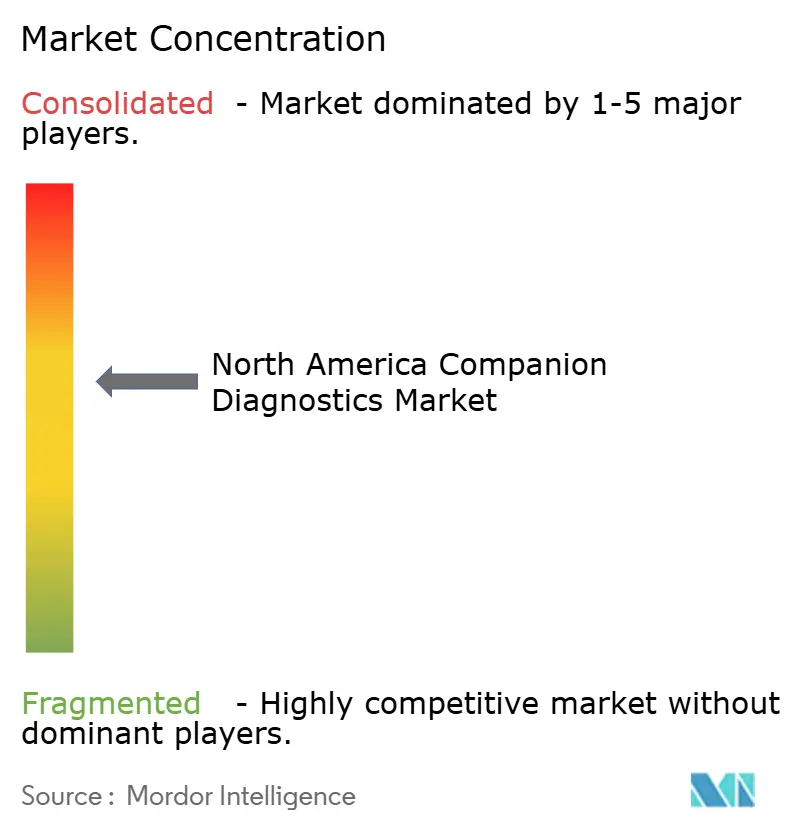

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Companion Diagnostics Market Analysis by Mordor Intelligence

The North America Companion Diagnostics Market size was valued at USD 3.48 billion in 2025 and is estimated to grow from USD 3.95 billion in 2026 to reach USD 7.45 billion by 2031, at a CAGR of 13.52% during the forecast period (2026-2031).

The surge traces directly to oncology drug developers integrating biomarkers into pivotal trials, state regulators mandating test reimbursement, and the FDA compressing parallel review timelines for assays and therapeutics. Fourteen molecular entities entered U.S. commercial channels with mandatory companion tests in 2024, and 72% of late-stage oncology assets now carry biomarker-linked labels, locking in steady assay demand across academic and community settings. Platform innovation also matters: rapid NGS instruments that deliver 50-gene results in under 24 hours shorten time-to-treatment and tilt purchasing toward vendors offering integrated hardware, software, and cloud-enabled analytics.

Key clinical-workflow frictions continue to resolve. The Real-Time Oncology Review pilot pared median FDA approval timelines for CDx-drug pairs to six months in 2025, enhancing forecast visibility for assay makers and biopharma partners. Medicare’s Molecular Diagnostic Services Program reimbursed 1.8 million NGS claims in 2024, anchoring revenue for laboratories that derive two-thirds of test volume from federal programs. Mexico is building capacity inside the Instituto Mexicano del Seguro Social, while Health Canada’s single-dossier alignment with the FDA trims filing cycles by six months, signaling a broader regional convergence that sustains the North America companion diagnostics devices market through the decade.

Key Report Takeaways

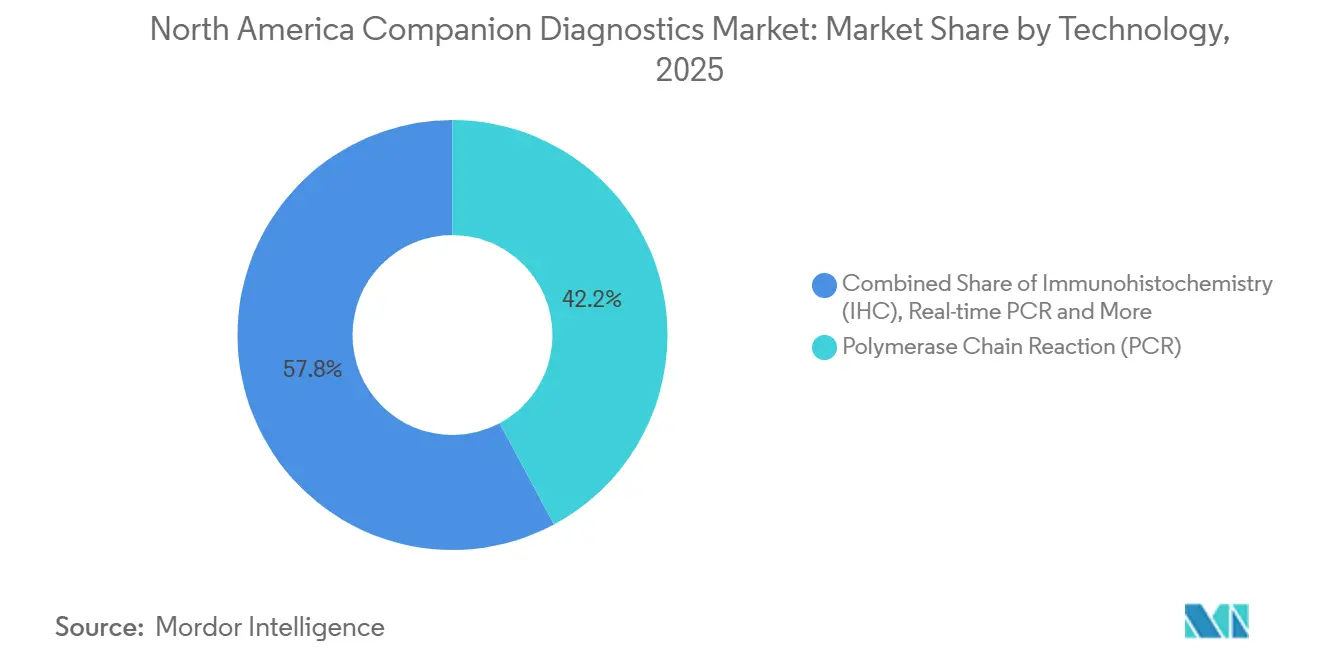

- By technology, polymerase chain reaction (PCR) platforms led with 42.18% of companion diagnostics devices market share in 2025. Next-generation sequencing is forecast to advance at a 14.22% CAGR to 2031, the highest among assay modalities.

- By indication, lung cancer accounted for 32.21% revenue in 2025, reflecting sustained EGFR, ALK, and KRAS testing volumes. Melanoma tests are projected to expand at a 15.65% CAGR between 2026-2031 as BRAF V600E/K assays move into adjuvant care.

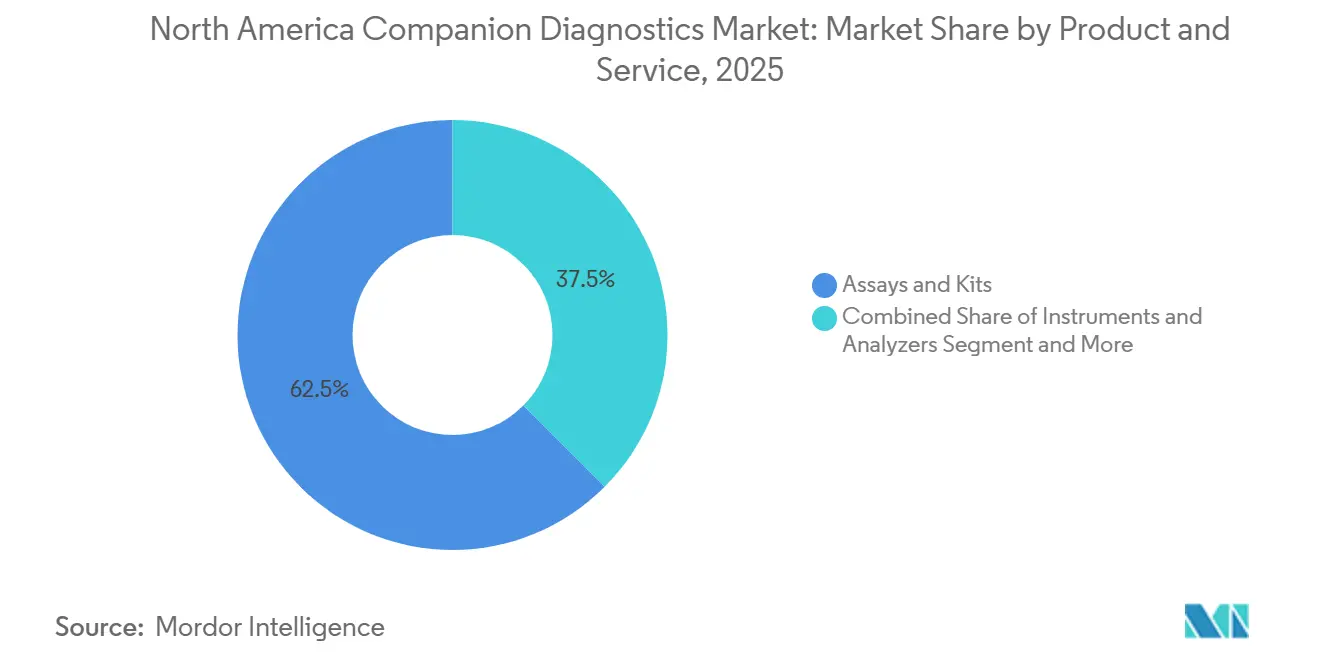

- By product category, assays and kits commanded 62.52% of 2025 revenue, whereas software and services show a 15.68% CAGR through 2031.

- By country, the United States contributed 68.25% of regional revenue in 2025, while Mexico is the fastest-growing geography at 13.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Companion Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oncology pipeline dominated by biomarker-linked drugs | +3.8% | Global, led by U.S. and Canada | Medium term (2-4 years) |

| FDA’s streamlined co-approval pathway | +2.9% | United States, spillover to Canada | Short term (≤ 2 years) |

| Rapid uptake of NGS-based multi-gene panels | +3.2% | North America, centered on academic systems | Medium term (2-4 years) |

| State biomarker-testing reimbursement mandates | +2.1% | United States | Long term (≥ 4 years) |

| 24-hour rapid NGS platforms | +1.4% | United States community oncology | Short term (≤ 2 years) |

| On-shoring of reagent manufacturing | +0.8% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oncology Pipeline Dominated by Biomarker-Linked Drugs

Seventy-two percent of the 57 novel oncology drugs the FDA cleared during 2024-2025 required a companion diagnostic, up from 58% in the prior five-year span[1]U.S. Food and Drug Administration, “Novel Drug Approvals 2024,” fda.gov. Sponsors embraced biomarker-enriched trials that trimmed enrollment by nearly one-third, lowered R&D expense, and realized a 6.2-month median review versus 10.1 months for biomarker-agnostic submissions. Lung cancer led with 18 biomarker-specified approvals, spotlighting EGFR exon 20 insertions, KRAS G12C, and MET exon 14 skipping, each defining distinct patient micro-segments that benefit from precise mutation detection. Breast cancer followed, driven by HER2-low labeling that now covers over half of HER2-negative tumors, expanding reach for antibody-drug conjugates. With 23 phase III agents already tied to CDx co-development agreements for 2026-2027, clinical evidence signals durable demand that underpins the North America companion diagnostics devices market.

FDA’s Streamlined Co-Approval Pathway for CDx & Drugs

The Real-Time Oncology Review program, extended to diagnostics in 2024, processed 11 co-dependent filings in 2025 with a six-month median timeline, shaving four months off traditional Premarket Approval reviews. Every month saved preserves an estimated USD 8 million in peak-sales value per therapy, aligning economic incentives between assay makers and drug sponsors. March 2025 draft guidance also let manufacturers file bridging studies to extend existing claims to new drug labels, a route Roche used three times in 2025 to widen cobas EGFR coverage without full re-validation. Joint CDRH-OCE reviews eliminated redundant data requests, and Health Canada’s parallel-submission pilot now accepts the same dossier, cutting filing redundancy by 200 staff hours. These gains flow directly into the operating leverage of companies active in the companion diagnostics devices market.

Rapid Uptake of NGS-Based Multi-Gene Panels

NGS panels interrogating 50-500 genes captured 28% of North American test volume in 2025, up nine points from 2023. Clinicians favor single-specimen, multi-mutation data that conserves tissue and reveals co-occurring resistance variants, such as TP53 loss in EGFR-mutant NSCLC, which alters treatment sequencing. However, the 3-5-day turnaround typical of legacy sequencers slows therapy initiation, especially outside academic hubs. FDA clearance of Element Biosciences’ 18-hour AVITI system in February 2025 allows same-week decisions for 80% of solid-tumor cases, catalyzing demand among community oncologists who handle most U.S. cancer care. Academic centers embed these platforms in CLIA-certified labs, further scaling volumes that anchor the North America companion diagnostics devices market.

State-Level Biomarker-Testing Reimbursement Mandates

Colorado’s SB 21-077 took effect in 2024 and lifted NGS testing rates from 61% to 94% of late-stage cancer patients by 2025. California followed with AB 2402, extending coverage to Medi-Cal’s 14 million members. New Jersey mandates liquid biopsy coverage when tissue is unavailable, addressing roughly one-fifth of advanced lung cases. New Mexico and Maryland added similar provisions, and together these states blanket 38% of commercially insured Americans. With out-of-pocket expenses averaging USD 1,200 per NGS test in 2023, mandates remove a price hurdle that previously dissuaded 28% of eligible patients. Although gene lists vary by payer, the volume lift sustains reagent pull-through across the companion diagnostics devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of CDx development & clinical validation | −1.9% | Global, acute for smaller developers | Medium term (2-4 years) |

| Lengthy FDA PMA Class III review timelines | −1.2% | United States | Short term (≤ 2 years) |

| Tightening state-level genomic-privacy legislation | −0.6% | United States (California, New York) | Long term (≥ 4 years) |

| Shortage of molecular pathologists & bioinformaticians | −0.9% | North America, severe in rural sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of CDx Development & Clinical Validation

Bringing a single companion diagnostic from assay design to FDA approval costs USD 15-25 million and can span three years. Guardant Health allocated 42% of its 2024 R&D spending to clinical validation, underscoring heavy cash needs even for public companies. Additional FDA requirements for fresh-tissue concordance, despite 95% liquid-biopsy sensitivity, tack on USD 3-5 million and up to one year per indication. Exact Sciences invested USD 180 million over five years to build evidence for Oncotype DX, a burden that would exceed the resources of most start-ups. Consequently, economies of scale accrue to diversified incumbents such as Roche, which spreads costs across 17 label extensions on its FoundationOne CDx platform.

Lengthy FDA PMA Class III Review Timelines

Despite the statutory 180-day clock, Class III PMA reviews averaged 10.2 months in 2024, largely because 68% generated major-deficiency letters that reopened analytical questions. Illumina’s HRD assay lost six commercial months and an estimated USD 12 million owing to algorithmic cutoff queries. Guardant360 TissueNext faced 14 months of review as the FDA demanded cross-platform concordance against FoundationOne CDx across eight tumors. Smaller firms lacking deep regulatory teams often cede first-mover advantage, concentrating power among companies with established PMA playbooks—a headwind that tempers growth in the North America companion diagnostics devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PCR Anchors Revenue, NGS Captures Growth

Polymerase chain reaction platforms generated 42.18% of 2025 revenue, buoyed by entrenched EGFR, KRAS, and BRAF single-gene workflows priced at USD 150-300 per test[2]Qiagen N.V., “Investor Relations Financial Reports,” qiagen.com. Their 24-48-hour turnaround fits community oncology, which treats 70% of U.S. patients and often lacks onsite sequencing labs. Roche’s cobas EGFR v2 alone processed 1.2 million samples worldwide in 2025. Yet NGS systems are scaling quickly: eight fresh FDA clearances in 2024-2025 plus payer policies that now favor comprehensive profiling drive a 14.22% CAGR for NGS through 2031 across the North America companion diagnostics devices market. Illumina’s TruSight Oncology 500 ctDNA merges mutational burden and microsatellite instability in a single run, meeting both targeted-therapy and immunotherapy requirements.

Immunohistochemistry (IHC) and in-situ hybridization still matter for protein biomarkers where cellular architecture guides interpretation. Agilent’s PD-L1 22C3 pharmDx processed 850,000 slides in 2025, with digital pathology cutting inter-observer variance by more than half. Liquid biopsy volumes reached a notable percentage of companion testing as clinicians adopted plasma assays for patients unable to undergo tissue biopsy. Bio-Rad’s droplet digital PCR offers 0.1% sensitivity, enabling early detection of resistance alleles. Together, these modalities ensure the North America companion diagnostics devices market retains technological diversification even as NGS leads growth.

By Indication: Lung Cancer Dominates, Melanoma Accelerates

Lung cancer generated 32.21% of 2025 revenues, underpinned by EGFR, ALK, ROS1, and KRAS coverage fed by six new FDA-approved NSCLC therapies between 2024-2025. Guardant360 CDx, cleared for first-line use in June 2024, recorded USD 320 million in its initial year by offering a non-invasive option that delivers results in seven days. Melanoma assays expand fastest at a 15.65% CAGR as adjuvant BRAF V600E/K testing moves upstream; dabrafenib-trametinib already cut recurrence risk by 44% in resected stage III disease. The companion diagnostics devices market size for melanoma could therefore more than double by 2031.

Breast cancer comprised a significant share of 2025 revenue, but HER2-low labeling resets IHC scoring requirements that AI pathology now automates with 96% concordance. Leukemia and a basket of gastric, ovarian, and prostate tumors account for the remainder, with PARP-inhibitor approvals in 2025 expected to lift BRCA testing rates in prostate cancer. Collectively, indication diversity protects revenue resilience within the North America companion diagnostics devices market.

By Product and Service: Kits Lead, Software Surges

Assays and reagent kits captured 62.52% of 2025 revenue, exemplified by Roche’s USD 5,800 FoundationOne CDx and Qiagen’s PCR kits spanning a dozen genes. Instruments and analyzers represented 22% as capital budgets stretched replacement cycles to seven years. Yet cloud analytics and decision-support software will grow 15.68% CAGR to 2031, outpacing physical goods. Tempus AI processed 95,000 integrated genomic reports in 2025 at USD 1,200 each, bolstering a fee-for-service engine unlinked to hardware refresh cycles. PathAI’s AISight cut PD-L1 scoring time by 60%, converting pathologist labor into software margins. With digital pathology startups raising USD 340 million in 2025, the companion diagnostics devices industry pivots toward subscription revenue that embeds algorithms directly into oncologist workflows.

Geography Analysis

The United States retained 68.25% revenue share in 2025, fueled by Medicare’s reimbursement of up to USD 3,000 per NGS panel and 11 new FDA platform clearances over two years. Biomarker-testing mandates in five populous states erased prior-authorization hurdles for 85,000 additional patients and nudged nationwide testing penetration to a fresh high. Forty-two NCI-designated cancer centers plus integrated networks like Kaiser Permanente standardize protocols across millions of covered lives, reinforcing economies of scale that keep the North America companion diagnostics devices market anchored in the U.S. Meanwhile, the FDA’s April 2024 laboratory-developed-test rule harmonized validation requirements for in-house assays, boosting confidence in hospital-run sequencing programs.

Mexico posts the region’s fastest trajectory at 13.88% CAGR to 2031. IMSS earmarked MXN 2.4 billion (USD 140 million) for lab infrastructure and workforce development that extends genomic testing to 60 million beneficiaries[3]Instituto Mexicano del Seguro Social, “Plan Estratégico 2025-2030,” imss.gob.mx. Eighteen private laboratories added NGS capacity in 2024-2025, targeting self-pay patients willing to fund USD 2,000-3,500 comprehensive panels. Yet public reimbursement still favors single-gene PCR, keeping access uneven across socioeconomic strata. A Pan American Health Organization partnership to train 500 molecular pathologists by 2028 addresses rural shortages that currently add 15-25 days to turnaround times.

Canada remains fragmented. Ontario conditionally funds FoundationOne CDx only for metastatic NSCLC, while Quebec reimburses a 50-gene panel at CAD 1,500 (USD 1,100) versus U.S. rates nearly triple that figure. BC Cancer’s centralized program processed 12,000 samples in 2025 but posted a 21-day median turnaround, double U.S. academic benchmarks. Health Canada’s FDA-aligned dossier reduced regulatory lag to 12 months; however, decentralized provincial funding still delays rollouts by up to two years. A 22% vacancy in molecular pathology roles forces 30% of specimens across provinces to U.S. reference labs, imposing extra costs and reinforcing U.S. dominance in the companion diagnostics devices market.

Regulatory Landscape

In the United States, companion diagnostics are regulated by the FDA as in vitro diagnostic devices, and they are typically reviewed alongside the associated therapeutics when the test is essential for safe and effective treatment selection. The region has also continued moving toward risk-based oversight for IVDs, including FDA signaling a transition path away from broad reliance on Class III pathways for many tests. The agency also maintains an active list of cleared or approved companion diagnostic devices, which shapes market access decisions for oncology sponsors and laboratories.

In Canada, Health Canada regulates companion diagnostics under the Medical Devices Regulations and applies a risk-based classification framework for in vitro diagnostic devices, with many CDx products commonly handled as higher-risk devices requiring premarket scientific assessment. Cross-border commercialization still involves separate filings and evidence packages, increasing operational burden for manufacturers launching the same drug-diagnostic pairing in both the United States and Canada. Even with dossier alignment initiatives and parallel-submission practices reducing administrative duplication for some programs, these requirements can still add lead time for product launches.

Competitive Landscape

The North America companion diagnostics devices market is moderately concentrated: top-five vendors—Roche, Illumina, Guardant Health, Thermo Fisher Scientific, and Qiagen—held a significant share in 2025. Guardant Health exemplifies the laboratory-services insurgency, processing 180,000 Guardant360 tests and capturing full Medicare reimbursement without selling sequencers. Illumina and Thermo Fisher defend installed bases through menu expansion and EHR integration, but the razor-and-blade economics weaken as laboratories opt for send-out models or negotiate reagent-rental discounts.

Speed differentiates newcomers. Element Biosciences’ AVITI posts 18-hour turnaround versus 3-5 days for mainstream platforms, granting same-week therapy decisions that drive physician preference. AI pathology further disrupts incumbents: Paige Prostate automates Gleason scoring at USD 150 per slide, undercutting manual pathology by 40% while securing the FDA’s first software-as-a-medical-device CDx status. Tempus AI embedded clinical outcomes data to recommend off-label therapies, processing 95,000 cases in 2025 after raising USD 410 million in an IPO. As revenue shifts toward informatics, strategic control may pivot from instrument giants to data-rich software platforms, intensifying competitive dynamics in the companion diagnostics devices market.

North America Companion Diagnostics Industry Leaders

F. Hoffmann-La Roche Ltd.

Illumina Inc.

Guardant Health Inc.

Thermo Fisher Scientific Inc.

Qiagen N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace in North America centers on scaling comprehensive profiling beyond tertiary cancer centers into community settings, where rapid turnaround and standardized reporting support therapy decisions. A concrete access catalyst emerged in January 2026, when CMS granted reimbursement for Illumina's FDA-approved TruSight Oncology Comprehensive test (effective January 1, 2026), strengthening the business case for wider NGS deployment and companion-diagnostic menu expansion tied to targeted therapies.

Partnership-led platform integration is also creating commercialization lanes that combine tissue and liquid biopsy with informatics, reducing friction for health systems that lack dedicated molecular teams. Examples include Illumina and Labcorp expanding collaboration in March 2026 to broaden access to precision oncology testing, and Guardant Health entering a multi-year collaboration with Merck in January 2026 to develop companion diagnostics and support clinical trial enrollment using Guardant's liquid biopsy platform. These moves point to opportunities for vendors able to package regulated CDx claims, high-throughput workflows, and decision support into solutions designed for distributed oncology networks across the United States, Canada, and Mexico.

Recent Industry Developments

- June 2026: Roche announced FDA approval of the VENTANA PTEN (SP218) RxDx Assay as an immunohistochemistry companion diagnostic to assess PTEN protein loss in prostate adenocarcinoma patients eligible for AstraZeneca's TRUQAP (capivasertib). The approval broadens the CDx mix beyond genomics into protein-loss biomarkers and reinforces the role of digital pathology-ready IHC workflows in precision oncology.

- April 2025: Roche secured FDA Breakthrough Device Designation for the VENTANA TROP2 (EPR20043) RxDx computational pathology companion diagnostic device. The designation indicates priority engagement with the FDA for an AI-enabled pathology CDx pathway and supports faster iteration on software-centric capabilities tied to oncology drug development programs.

- June 2024: Guardant Health received FDA clearance for Guardant360 CDx for first-line use, expanding the addressable liquid biopsy companion testing population for advanced cancer patients. Wider first-line positioning supports earlier biomarker identification when tissue is limited, reinforcing the shift toward blood-based testing in community oncology workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America companion diagnostics market covers regulated tests and enabling tools used to match patients to a specific therapy based on a biomarker result, and the value includes related assays, instruments, and supporting software and services across the region.

Scope exclusions: Research-only assays without a therapy-linked clinical claim, and general lab consumables not specific to companion diagnostics, are excluded.

Segmentation Overview

- By Technology

- Immunohistochemistry (IHC)

- Polymerase Chain Reaction (PCR)

- In-situ Hybridization (ISH)

- Real-time PCR (RT-PCR)

- Next-Generation Sequencing (NGS)

- Liquid Biopsy-based Assays

- Other Technologies

- By Indication

- Lung Cancer

- Breast Cancer

- Colorectal Cancer

- Leukemia

- Melanoma

- Other Indications

- By Product & Service

- Assays & Kits

- Instruments & Analyzers

- Software & Services

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market boundaries, understand approved companion diagnostic claims, and build the base demand logic by country. We referred to public sources such as FDA test and drug labeling information, CDC cancer statistics, SEER cancer incidence data, and OECD health data to anchor disease burden and testing context in a consistent way.

To translate this into a workable sizing model, we also used sources such as company annual reports and filings, investor presentations, clinical trial registries, and peer reviewed oncology and diagnostics journals to track how testing adoption follows targeted therapies. Select paid subscriptions for company financials and intelligence and for patent databases were used to validate product footprints and timing, and these were then checked against public disclosures. The desk sources listed above are illustrative, and we relied on additional public and paid sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the adoption rate of CDx linked testing, typical pricing bands by test type, and where software and services are actually billed as part of a CDx workflow. We spoke with lab decision makers, diagnostics commercial teams, and clinical stakeholders across the United States, Canada, and Mexico, so the assumptions reflect real ordering patterns and reimbursement realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | |

| Mid tier: 48% | Functional/Unit leaders: 41% | |

| Smaller Players: 20% | Managers: 43% |

Market-Sizing & Forecasting

Sizing starts with a top down demand pool built from biomarker relevant patient volumes and the practical testing pathway tied to targeted therapies, which is then translated into annual test volumes by major indications. Once those volumes are in place, average selling price ranges are applied by technology (such as IHC, PCR, ISH, RT-PCR, NGS, and liquid biopsy), then adjusted for country level mix across the United States, Canada, and Mexico.

To avoid relying only on theoretical totals, we corroborated outputs with selective bottom-up approximations, including sampled revenue benchmarks from public filings, channel feedback on instrument placements, and checks on the split between assays and kits versus instruments and software and services. Inputs that mattered most included FDA approval and label updates for CDx claims, oncology incidence trends by tumor type, the share of therapies requiring a biomarker test, laboratory throughput capacity signals, and observed price moves tied to technology shifts. For forecasting, scenario analysis is used around therapy pipeline intensity and testing penetration, and the final growth path is aligned with expert consensus collected during interviews. Where direct data is thinner for smaller countries or niche indications, we fill gaps using proportional allocation based on patient pools and validated adoption ratios, then re-check the combined output against known market constraints.

Data Validation & Update Cycle

Validation is done through multiple checks so the output stays consistent with real world signals. We compare country totals against independent indicators like labeled therapy volumes, testing utilization signals discussed by labs, and public financial disclosures, then review outliers before sign-off.

If a large variance shows up, assumptions are revisited and experts are re-contacted to confirm whether it reflects a temporary disruption or a real structural shift. The model and narrative are refreshed annually, and interim updates are made when material events occur, such as major CDx approvals, reimbursement changes, or sudden shifts in oncology testing practice. Before delivery, a final analyst pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's North America Companion Diagnostics Market Market Size Measured Against Other Published Estimates

Published market values for companion diagnostics in North America can differ because each publisher draws the line differently around what counts as a companion diagnostic and what does not. The biggest drivers are usually product scope, the year used for currency conversion and base sizing, and how much of software and services is counted as part of CDx spend.

The main gap comes from whether instruments and software and services are counted alongside assays and kits, where Mordor Intelligence includes these billed components when they are tied to CDx workflows rather than treating the market as tests only. Differences also come from how fast adoption is assumed for NGS and liquid biopsy, whether the model leans on aggressive therapy pipeline ramp assumptions, and how frequently the underlying approval and labeling signals are refreshed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.48 B (2025) | |

| Industry Publisher A | USD 2.71 B (2025) | Often closer to a test-centric definition, with less explicit inclusion of instruments plus software and services, which can compress the total value even when test volumes look similar. |

| Market Tracker B | USD 2.19 B (2024) | Uses an earlier base year and frames the scope as devices, which can shift the mix of what is priced and counted, and also creates a timing gap versus 2025 values. |

The table shows that most of the spread is explained by scope and timing rather than a completely different view of demand. By keeping the counted items tied to therapy-linked CDx workflows, and by aligning assumptions to observable approval and adoption signals, the estimate stays traceable to clear variables that can be reviewed and repeated.

Key Questions Answered in the Report

What value could North American companion diagnostics devices reach by 2031?

Revenue is projected to climb to USD 7.45 billion.

Which assay technology records the fastest growth over 2026-2031?

Next-generation sequencing posts the top trajectory at a 14.22% CAGR.

How do state biomarker-testing mandates influence clinical uptake?

They erase prior authorization and out-of-pocket costs, lifting NGS testing rates to 94% of eligible patients in Colorado.

At what pace are Mexican revenues expected to expand?

Mexico shows a 13.88% CAGR through 2031.

Which cancer indication currently yields the highest revenue share?

Lung cancer contributes 32.21% of 2025 revenue.

What operational advantage do rapid NGS systems such as AVITI deliver?

An 18-hour turnaround enables same-week therapy decisions in community oncology settings.

Page last updated on: