Equine Diagnostic Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 314.20 Million |

| Market Size (2031) | USD 422.80 Million |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

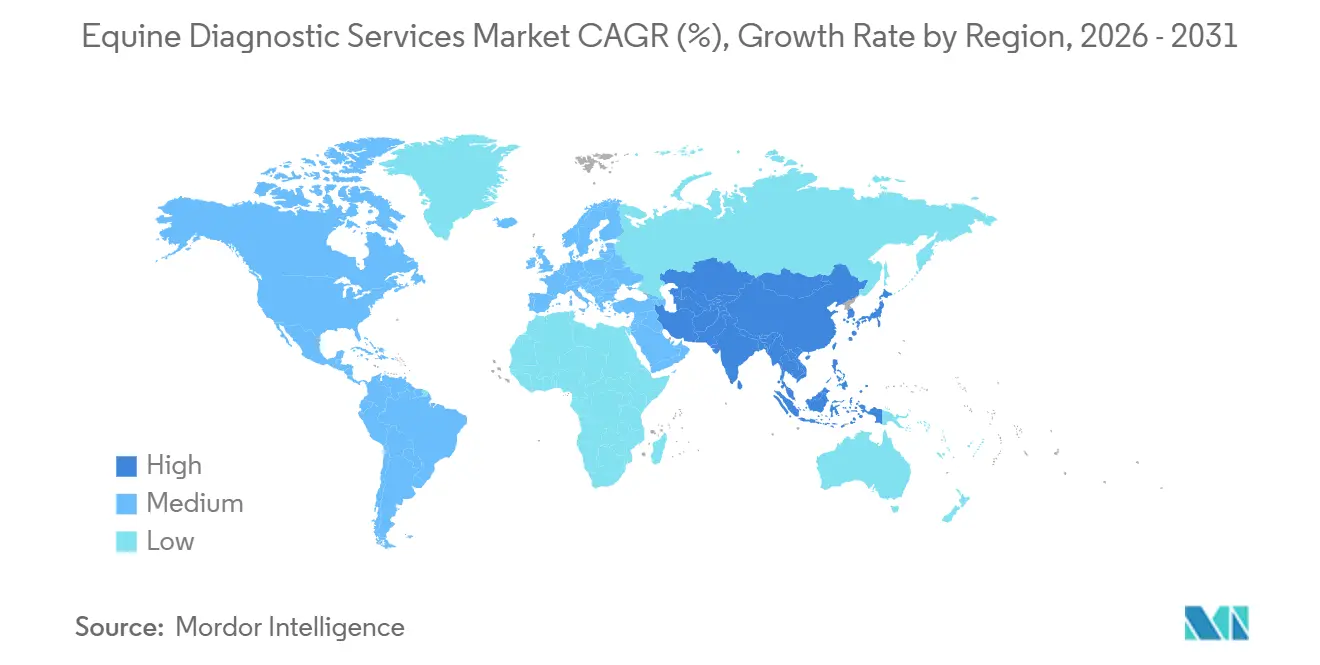

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

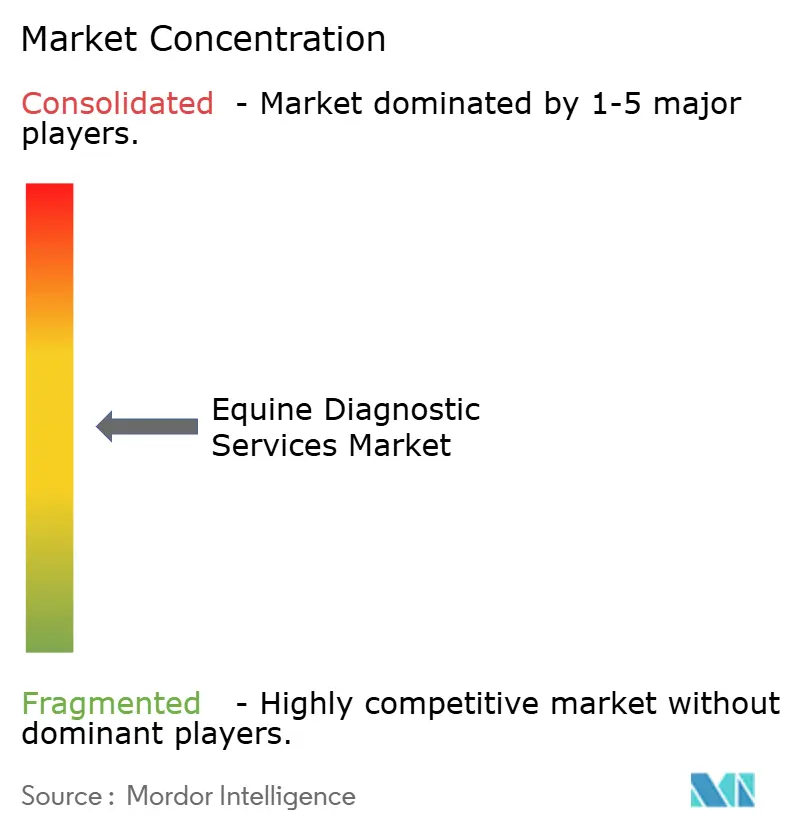

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Equine Diagnostic Services Market Analysis by Mordor Intelligence

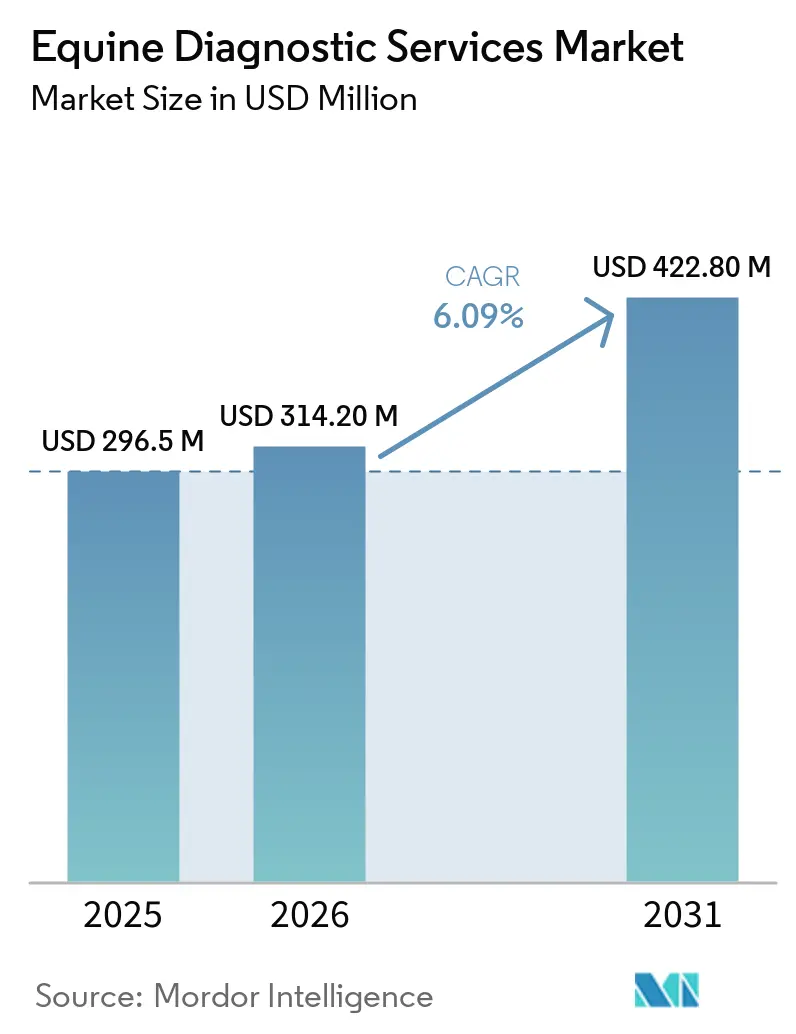

The Equine Diagnostic Services Market size was valued at USD 296.5 million in 2025 and is estimated to grow from USD 314.20 million in 2026 to reach USD 422.80 million by 2031, at a CAGR of 6.09% during the forecast period (2026-2031).

Regulatory biosecurity protocols in 2026 have turned molecular testing from a specialty option into a standard requirement across elite competition and cross-border movement, which has raised baseline volumes for reference labs and on-site event testing. Standing MRI and weight-bearing CT are scaling as default lameness workups in referral hubs because they shorten time to diagnosis and avoid general anesthesia risks, while subscription models reduce capital hurdles for mid-sized practices. Stall-side analyzers and handheld imaging now push diagnostics into the barn aisle, compressing turnaround times for time-critical calls such as colic triage and respiratory quarantines. Remote operations for advanced modalities are addressing technician scarcity by allowing centralized experts to run scanners in the field, which expands geographic access without adding on-site headcount. Objective gait analytics are tightening referral criteria by detecting subclinical asymmetries, which feed more targeted imaging workups and strengthen risk management in high-stakes racing and sport programs.

Key Report Takeaways

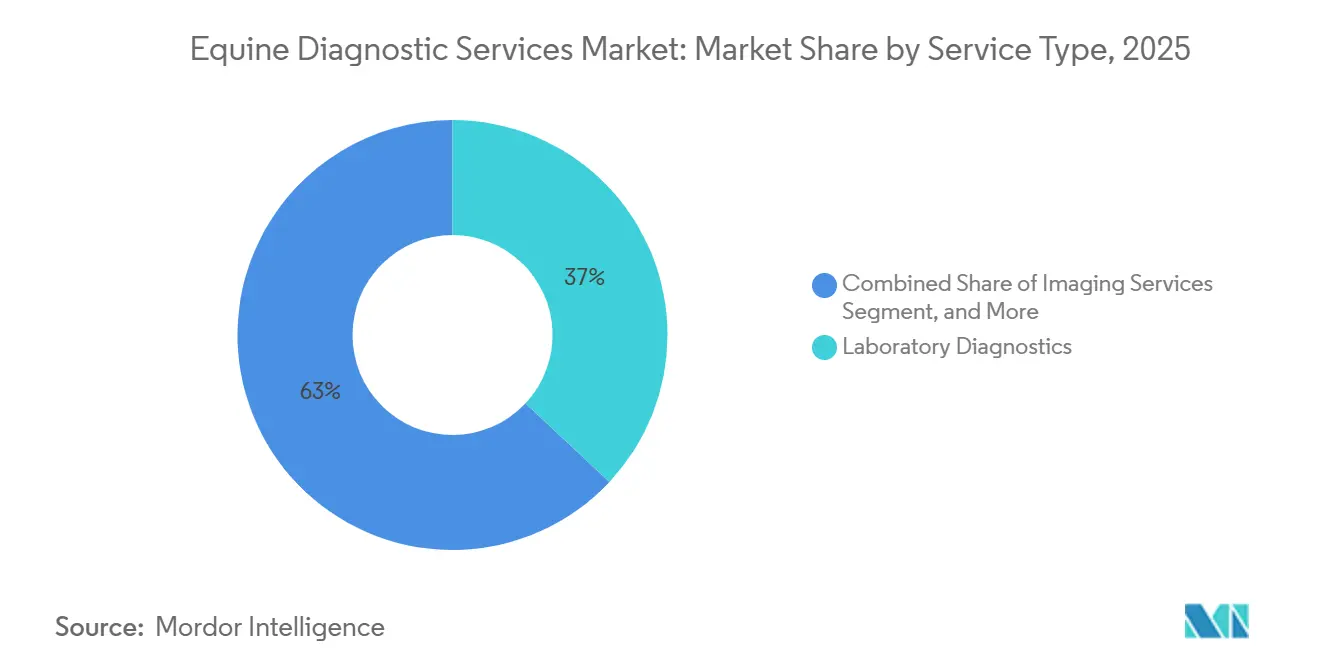

- By service type, laboratory diagnostics led with 36.98% revenue share in 2025, while point-of-care or field diagnostics is projected to grow at an 8.93% CAGR through 2031 in the equine diagnostic services market.

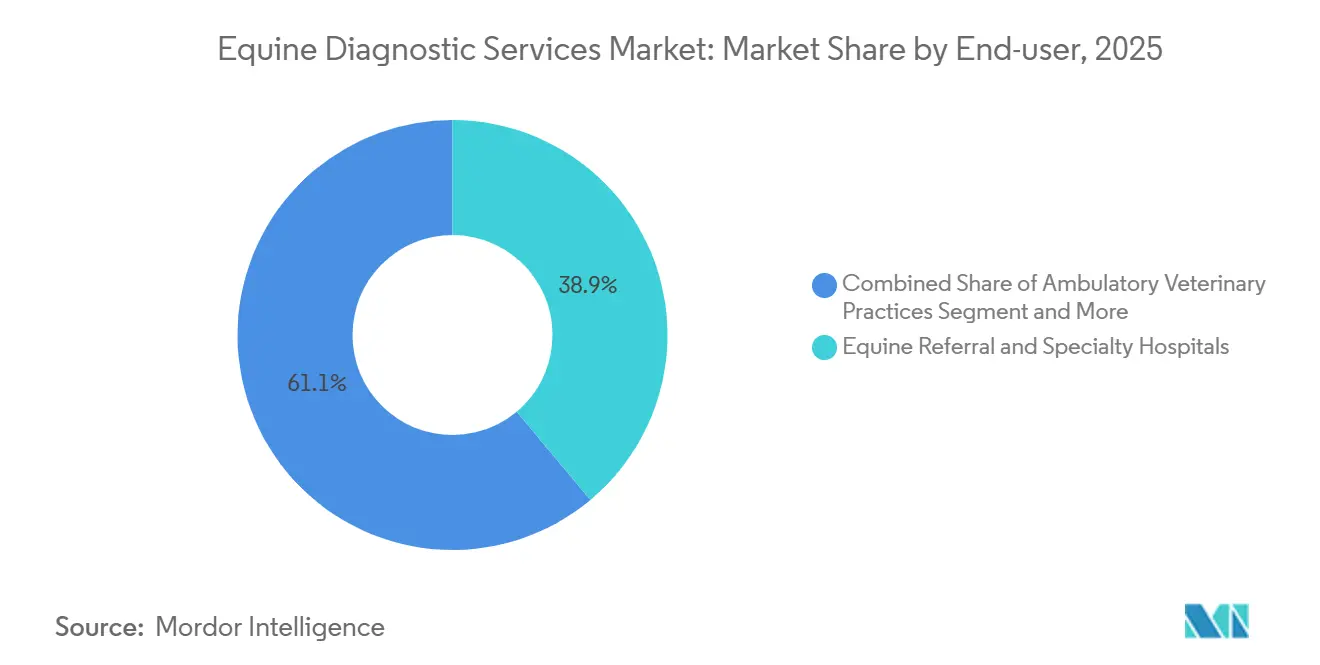

- By end-user or provider setting, equine referral and specialty hospitals commanded 38.91% of the equine diagnostic services market share in 2025, while commercial veterinary reference laboratories posted the fastest CAGR at 7.93% to 2031 in the equine diagnostic services market.

- By geography, North America captured 41.66% share in 2025; Asia-Pacific registers the fastest regional CAGR at 8.12% through 2031 in the equine diagnostic services market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Equine Diagnostic Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Standing MRI or CT Speeds Lameness Diagnosis | +1.2% | Global, concentrated in North America and Western Europe, early gains in Australia and Japan | Medium term (2-4 years) |

| PCR Adoption for Outbreak Management | +1.0% | Global, regulatory driven in North America and Europe, expanding in Asia-Pacific | Short term (≤ 2 years) |

| Stall-Side and Ambulatory Diagnostics Expansion | +0.9% | North America and Europe, spillover to Asia-Pacific urban centers | Medium term (2-4 years) |

| Organized Sport Growth and Stricter Biosecurity and Anti-Doping | +1.3% | Global, strongest in FEI-affiliated nations, Hong Kong, and Australia racing | Short term (≤ 2 years) |

| Imaging as a Service Lowers Capex Barriers | +0.8% | North America and Western Europe, emerging in Asia-Pacific metros | Medium term (2-4 years) |

| Objective Gait Analytics Scale Referrals | +0.7% | North America and select EU racing hubs, pilots in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Imaging Access (standing MRI/CT) Accelerating Definitive Lameness Diagnosis

Standing MRI and weight-bearing CT have compressed workups from anesthesia-based day procedures to short sedated sessions, which cuts risk and enables same-day treatment planning in performance horses.[1]Hallmarq Veterinary Imaging, “Down vs. Standing Equine MRI, What’s the Difference?,” Hallmarq reports that standing MRI improves visualization of early bone and soft-tissue changes relevant to high-value athletes that traditional radiography can miss when changes are subtle, which supports earlier offloading protocols and better outcomes. Weight-bearing CT from vendors such as Asto CT adds 3D assessment under physiological load that can reveal pathology not seen with recumbent imaging, which is critical for distal-limb evaluation in racing and jumping cohorts. Large-bore systems have extended standing coverage into proximal regions and cervicothoracic junctions in major centers, which widens case eligibility for sedation-only protocols.[2]Royal Veterinary College, “The Big Picture, New Big Bore CT Scanner Revolutionizes Equine Imaging,” Royal Veterinary College Practices are pairing modalities to correlate findings within a single visit, and teleoperated scanning is helping sites without on-staff specialists to run advanced cases efficiently. These shifts are raising the diagnostic baseline across referral hubs and lifting throughput in the equine diagnostic services market.

Rapid Adoption of Molecular PCR/qPCR for Outbreak Management

High-profile EHV-1 events have pushed PCR from confirmatory testing to frontline screening at event arrival and during quarantine, which hardwires molecular workflows into routine movement and competition.[3]Cornell University College of Veterinary Medicine, “AHDC Testing Horses for EHV-1 or EHM,” Reference centers such as Cornell AHDC and Colorado State ramped surge capacity during outbreaks, while panels for fever-of-unknown-origin broadened to close blind spots in septic and enteric causes of pyrexia.[4]Cornell University College of Veterinary Medicine, “AHDC Update, Equine Fever of Unknown Origin Panel,” Evidence-based sampling is central to strangles control since guttural pouch lavage is far more sensitive than nasopharyngeal swabs and qPCR outperforms culture, which reduces the risk of silent carriers seeding new cases.[5]University of Guelph AHL, “AHL Labnote 67, Diagnosis of Strangles,” University of Guelph Time-to-result is becoming a key differentiator as stall-side LAMP units and next-generation multiplex PCR panels compress decisions from days to hours, which improves quarantine precision and reduces facility downtime. New integrated respiratory kits, such as bioMérieux VETFIRE, place multi-pathogen PCR into a single self-contained cartridge, which removes cold-chain hurdles and supports adoption in regions with limited courier networks. This operational evolution shifts steady volumes into the equine diagnostic services market and raises the baseline for outbreak readiness at shows and sales.

Expansion of Stall-Side/Ambulatory Diagnostics in Equine Practice

Point-of-care platforms are turning the farm call into a full diagnostic encounter by moving endocrine, hematology, and electrolyte testing to the barn aisle, which reduces reliance on overnight shipments and accelerates care plans. Zoetis’s OptiCell analyzer and its AI-enabled Imagyst platform extend on-site blood and fecal workflows, which refines deworming decisions and aligns with rising resistance concerns in strongyles and ascarids. Handheld blood gas units such as Antech’s Element POC provide critical care parameters from micro-samples in under a minute, which supports more precise triage for colic and endurance cases during off-hours. Lightweight ultrasound platforms with long-life batteries and species presets are enabling high-quality tendon and ligament imaging in the field, which reduces the need for hospital referrals for many soft-tissue injuries. Field protocols remain vital since syringe additives can skew electrolytes, and recent veterinary studies call for cartridge-based or non-heparinized approaches to preserve ionized calcium integrity in colic workups. As adoption deepens, more first-opinion cases convert to data-driven plans, which adds steady volume to the equine diagnostic services market and narrows the turnaround gap with referral centers.

Growth in Organized Equestrian Sport and Stricter Biosecurity/Anti-Doping Programs

Federation rules are embedding diagnostics into entry, arrival, and on-venue procedures, which turns episodic testing into a consistent operating expense for teams and organizers. Racing authorities have raised pre-travel imaging thresholds for international contenders and encouraged standing CT use to assess distal-limb pathology before marquee events, which increases demand for advanced imaging in the lead-up to major races. The Hong Kong Jockey Club maintains extensive pre-import imaging and laboratory screens, which shifts much of the diagnostic burden to origin-country clinics and builds cross-border volumes. The Breeders’ Cup instituted out-of-competition testing and covered advanced imaging requested by regulatory veterinarians in 2025, which directly socialized high-end diagnostic costs across purse structures. Organizers and regulators are also logging temperature checks and symptom screens tied to PCR triggers, which formalizes infectious disease surveillance at scale across event calendars. The net effect is steady demand growth in the equine diagnostic services market, anchored in compliance and welfare frameworks rather than discretionary behavior.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure and Per-Test Costs with Uneven Insurance Coverage | -1.1% | Global, acute in the USA and UK, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Scarcity of Board-Certified Equine Imaging Specialists and Radiologists | -0.8% | North America and Western Europe, severe in rural Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Inter-Laboratory Variability and Limited Standardization in Some Equine PCR Assays | -0.4% | Global, impacting multi-site research and cross-border diagnostics | Medium term (2-4 years) |

| Field Logistics, Sample Integrity, Biosecurity, and Connectivity Delays | -0.6% | Global, pronounced in rural regions, developing markets in MEA and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure and Per-Test Costs with Uneven Insurance Coverage

Advanced imaging prices and multi-modality cascades can exceed annual coverage limits for many owners, which suppresses elective utilization for non-elite horses. Even basic imaging packages include sedation, interpretation, and facility fees that raise the final bill beyond the headline scan price, which makes transparent estimates and tiered offerings an important trust driver. Stall-side diagnostics reduce courier expenses and time lost to shipping, but they add cartridge and consumable costs that practices must price into emergency and after-hours services. Insurance structures often impose deductibles and co-pays that compound when cases require follow-up scans or interventional procedures, which can cause owners to pause between modalities even when clinical urgency remains. Clinics are responding with menu-based options that align scan scope to a single region and same-day discharge, which helps price-sensitive clients move forward without committing to full hospitalization or multi-region imaging. Until insurance coverage rises or bundled care models spread, cost friction will temper volume growth in certain owner segments within the equine diagnostic services market.

Scarcity of Board-Certified Equine Imaging Specialists/Radiologists

Training pathways to radiology and equine imaging require many years, which constrains supply and leaves regional gaps that slow scan interpretation and case flow. University hospitals and large referral centers are expanding training capacity, but annual cohorts remain small relative to equipment adoption trends at private sites. Teleconsult and remote operations models help distribute expertise and unlock scanning hours, but subspecialty reads for complex joints still bottleneck when demand spikes in sports seasons. Standing MRI and weight-bearing CT have reduced anesthesia risk, yet they still require trained operators and experienced readers for optimal value, which raises staffing needs during expansion. Regional hubs such as the University of Melbourne Equine Center provide high-end modalities and act as referral magnets for neighboring markets, which further concentrate specialist workloads. Advances in AI-assisted reads for fracture localization and pattern recognition may ease the burden over time, but liability and validation frameworks will govern the pace of clinical deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Field Platforms Chip Lab-Diagnostic Dominance

Laboratory Diagnostics held 36.98% of the 2025 share of the equine diagnostic services market size, reflecting entrenched use of reference centers for hematology, immunoassays, and complex culture workflows that still outperform many field kits for breadth and sensitivity. Point-of-care or field diagnostics is projected to expand at an 8.93% CAGR through 2031 as cartridge platforms, portable blood gas analyzers, and mobile ultrasound improve case throughput at the stable, which reduces dependency on overnight couriers and aligns decisions to the clinical clock. Imaging Services, including radiography, ultrasound, MRI, CT, and endoscopy, concentrate revenue because advanced modalities command higher per-case fees despite lower unit volumes than basic scans, and standing MRI and weight-bearing CT are now core offerings in many referral networks. Genetic testing remains a niche but is gaining relevance in high-value breeding decisions as reproductive programs formalize pre-implantation risk checks via targeted panels run through university or commercial labs. Endoscopy and specialty procedures such as guttural pouch lavage are critical for strangles carrier identification, and sampling guidance from academic labs is improving sensitivity and lowering reinfection risk, which reduces false reassurance from negative swab-only protocols.

In this context, on-instrument AI and software integration are pulling routine review tasks closer to the patient, which compresses lab-to-vet communication loops and helps ambulatory clinicians justify more complete workups in a single visit. FEI rule changes and competition medicine are raising same-day documentation needs for medications and welfare checks, which boosts demand for in-venue chemistry and hematology panels to document medical necessity and support eligibility under federated rules. Regional adoption paths diverge since mature markets build around advanced imaging hubs while fast-growing regions emphasize portable platforms that improve access without major facilities investment. As these patterns reinforce, a larger share of first-opinion cases complete the workup within the same day, which expands recurring demand in the equine diagnostic services industry while shifting mix from send-outs to stall-side decisions.

By End-User/Provider Setting: Reference Labs Narrow Referral Hospitals' Lead

Equine Referral and Specialty Hospitals accounted for 38.91% share of the equine diagnostic services market size in 2025, reflecting their control of high-cost imaging and interventional capabilities that ambulatory clinics do not carry. Commercial Veterinary Reference Laboratories are projected to grow at the fastest 7.93% CAGR as logistics, co-location with air hubs, and integrated software improve turnaround and consistency for clinicians, which increases share-of-wallet from mixed-animal practices that route equine samples through the same networks. Ambulatory or Field Veterinary Practices keep first-touch volumes and now retain more testing in-house thanks to portable imaging and stall-side assays, yet they still refer complex lameness and surgical cases to hospitals for MRI, CT, PET, and arthroscopy. University and State Diagnostic Laboratories blend public-health surveillance with fee-for-service testing and update panels to close diagnostic gaps for field clinicians, which helps stabilize access during seasonal surges and outbreaks.

Hospitals are expanding modality breadth and pairing imaging with interventional procedures during the same admission, which reduces repeat anesthesia and consolidates spend within the same facility. Reference labs continue to invest in capacity and differentiated offerings such as multiplex respiratory PCR and standardized digital reporting, which raises consistency across large catchment areas and supports multi-site clinical groups. Remote-operator services for advanced imaging help smaller hospitals and large ambulatory practices capture high-end scans without staffing them locally, which spreads capabilities into secondary markets and sustains case growth in the equine diagnostic services industry. As each setting strengthens its comparative advantages, referral pathways are becoming more structured and predictable, which helps reduce patient drop-off between initial exam and definitive diagnosis.

Geography Analysis

North America held 41.66% of the 2025 share, sustained by state and federal requirements for disease surveillance and import biosecurity that institutionalize diagnostic use across movements and competitions. Interstate movement commonly hinges on recent Coggins tests and veterinary certificates, and imported breeding stock must clear multi-step quarantine screens such as serial cultures for contagious equine metritis, which embeds diagnostic demand in routine workflows. Event organizers and regulators maintain temperature logs and trigger PCR when thresholds are exceeded, which spreads molecular testing throughout show circuits and training centers. During EHV-1 events, university and state labs coordinate surge capacity and communications, which normalizes response times and reduces spread risk in large barns and event venues. Advanced imaging access is concentrated in and around university hubs and high-density equestrian regions, and teleoperations are extending coverage into adjoining states by decoupling scans from on-site specialist availability. These factors support steady growth in the equine diagnostic services market across the United States and Canada.

Europe pairs leading academic centers and racing hubs with mixed insurance environments, which produces strong adoption in referral clusters and more cautious uptake among non-racing clients in select countries. The Royal Veterinary College installed a large-bore standing CT system that enables sedation-only scans in wider anatomical regions, which broadens case eligibility and improves throughput in the UK’s referral ecosystem. European manufacturers and labs continue to launch multi-pathogen respiratory PCR kits and other integrated offerings, which helps synchronize workflows across clinics and reduces training overhead for new users. Federation harmonization and WOAH capacity building on laboratory expertise for equine diseases support improved cross-border movement and standardized surveillance practices, which is important for pan-European competition calendars. As referral hospitals educate clients on the value of standing imaging and as labs align result formats, predictable case flows can develop across national boundaries, which sustains demand in the equine diagnostic services market in Europe.

Asia-Pacific is the velocity leader on a percentage basis, anchored by Japan’s racing-driven imaging growth and Australia’s referral concentration, while large markets build advanced capacity in metro hubs. Japan Racing Association data on training center MRI use and regulatory discussions around distal-limb imaging reinforce how formal racing systems lift baseline demand for advanced modalities. Australia benefits from the University of Melbourne’s concentration of high-field imaging and CT in a single equine center, which acts as a regional magnet for complex cases in neighboring states and countries. Educational resources on CT techniques and cross-sectional anatomy continue to spread through training platforms, which accelerates skill diffusion among clinicians and radiographers in growing markets. As hubs in Asia-Pacific add standing CT and MRI alongside robust PCR programs, they seed concentric catchments that raise regional volumes in the equine diagnostic services market.

Competitive Landscape

The equine diagnostic services market shows a blend of multi-species platforms and equine-focused specialists, with the former leveraging global lab networks and the latter driving category innovation in imaging and gait analytics. Zoetis expanded its U.S. lab footprint by opening a reference lab adjacent to UPS Worldport in Louisville, which reduces time-in-transit and improves same-day processing for priority tests. IDEXX maintains a comprehensive equine test menu that integrates with practice software and cloud reporting, which increases stickiness for clinics that route cross-species diagnostics through a single ecosystem. University labs such as Cornell AHDC update fever-of-unknown-origin panels and EHV-related guidance as new data emerge, which helps align practitioners to validated workflows during outbreak seasons.

Specialist imaging vendors are expanding access through product and service innovation. Hallmarq introduced motion correction on standing MRI to improve image quality in regions susceptible to patient movement, and it is scaling remote operations to widen access where trained operators are scarce. Asto CT partnered with IMV Imaging to accelerate the deployment of weight-bearing CT, which brings this modality into mixed practices that already rely on IMV for other imaging tools . University centers continue to expand leadership in advanced modalities that enable sedation-only scans over broader anatomic spans, which raises throughput and case diversity at major hubs.

Molecular and stall-side diagnostics are extending clinical reach at the barn and in the truck. bioMérieux’s VETFIRE kit puts a multi-pathogen respiratory panel onto an integrated platform with rapid turnaround, which helps veterinarians make early isolation and treatment decisions without shipping samples to a central lab. Texas A&M TVMDL launched a comprehensive respiratory PCR panel that consolidates multiple pathogens into a single submission, which simplifies outbreak management and standardizes reporting for practitioners and show officials. On the stall-side, AI-enabled fecal egg counting and rapid blood gas or electrolyte analysis are rebalancing test menus toward more on-visit decisions, which increases clinical efficiency and improves adherence to parasite control guidelines.

Equine Diagnostic Services Industry Leaders

Antech Diagnostics, Inc.

Cornell University (Animal Health Diagnostic Center)

Equinosis, LLC

IDEXX Laboratories, Inc.

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Texas A&M Veterinary Medical Diagnostic Laboratory launched its comprehensive equine respiratory disease rtPCR panel detecting nine pathogens with a 1–4 day turnaround, simplifying outbreak workflows for field veterinarians.

- March 2026: Royal Veterinary College published an AI-driven fracture detection study showing 71–84% localization accuracy in equine radiographs and expanded its collaboration with the Hong Kong Jockey Club.

- December 2025: Royal Veterinary College Equine Referral Hospital installed a large-bore CT scanner, enabling broader standing coverage and deeper anesthesia-based reach for complex regions.

Global Equine Diagnostic Services Market Report Scope

As per the scope of the report, equine diagnostic services refer to specialized laboratory and clinical testing offered for horses to detect, confirm, and monitor diseases, genetic traits, and performance‑limiting conditions. These services encompass reference laboratory assays, molecular/genetic diagnostics, and pathology testing, distinct from routine veterinary care. They provide veterinarians and owners with evidence‑based results that guide treatment, breeding, and preventive health strategies in equine medicine.

The equine diagnostic services is segmented by service type, end-user / provider setting, and geography. By service type, the market is segmented into laboratory diagnostics, imaging services, point-of-care / field diagnostics, genetic testing, endoscopy & other procedures. By end-user / provider setting, the market is segmented into commercial veterinary reference laboratories, equine referral & specialty hospitals, ambulatory / field veterinary practices, and Others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Laboratory Diagnostics |

| Imaging Services |

| Point-of-Care / Field Diagnostics |

| Genetic Testing |

| Endoscopy & Other Procedures |

| Commercial Veterinary Reference Laboratories |

| Equine Referral & Specialty Hospitals |

| Ambulatory / Field Veterinary Practices |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Laboratory Diagnostics | |

| Imaging Services | ||

| Point-of-Care / Field Diagnostics | ||

| Genetic Testing | ||

| Endoscopy & Other Procedures | ||

| By End-user / Provider Setting | Commercial Veterinary Reference Laboratories | |

| Equine Referral & Specialty Hospitals | ||

| Ambulatory / Field Veterinary Practices | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 outlook for the equine diagnostic services market and expected growth through 2031?

The equine diagnostic services market stands at USD 314.20 million in 2026 and is expected to reach USD 422.80 million by 2031 at a 6.09% CAGR.

Which service types lead and which grow fastest in equine diagnostics?

Laboratory Diagnostics led with 36.98% share in 2025, while point-of-care or field diagnostics is projected to grow at 8.93% through 2031.

How are FEI biosecurity rules influencing diagnostic demand?

FEI rules require temperature monitoring and PCR triggers at events, which formalizes molecular testing and supports steady volumes at venues and reference labs.

How do imaging-as-a-service models change access to MRI and CT?

Subscription and remote-operator models reduce upfront costs and staffing needs, which allows mid-sized practices to add MRI or CT and expand access regionally.

Which regions are set to expand most quickly in equine diagnostics?

Asia-Pacific is the velocity leader as Japan’s racing ecosystem and Australia’s referral hubs add capacity, while North America maintains the largest share under strong biosecurity protocols.

Which technologies will make the biggest impact on demand by 2031?

Weight-bearing CT and standing MRI, rapid multiplex PCR, and objective gait analytics are converging to lift early detection and throughput across clinical settings.

Page last updated on: