Veterinary Diagnostic Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

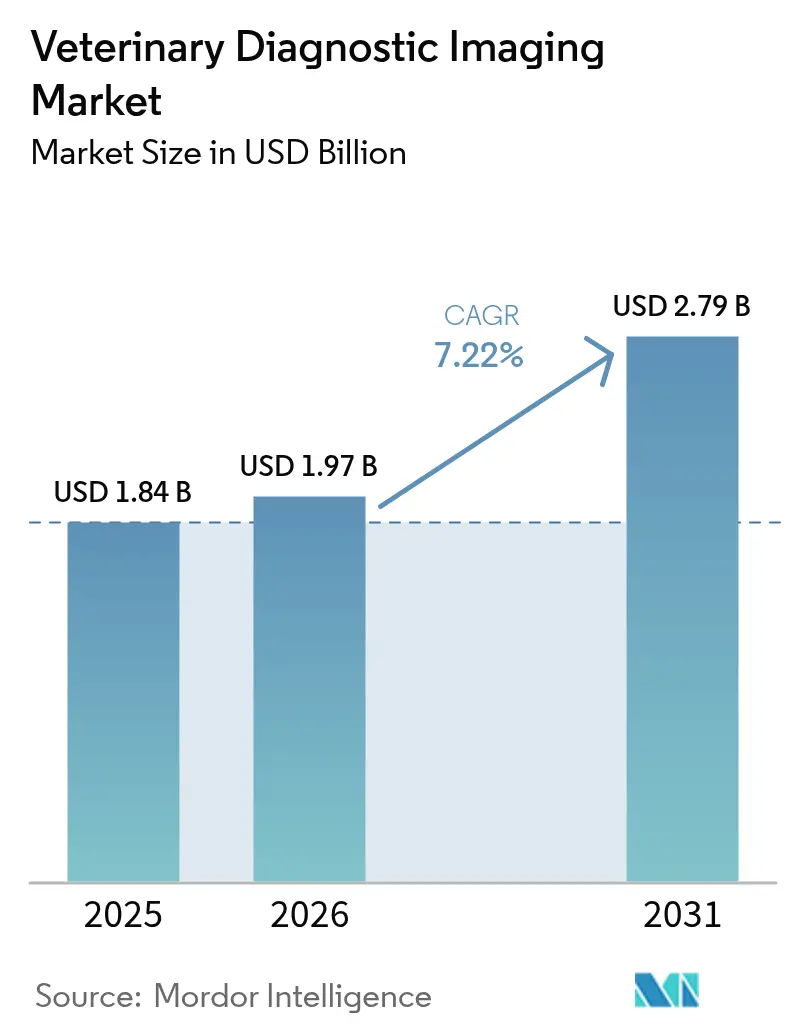

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

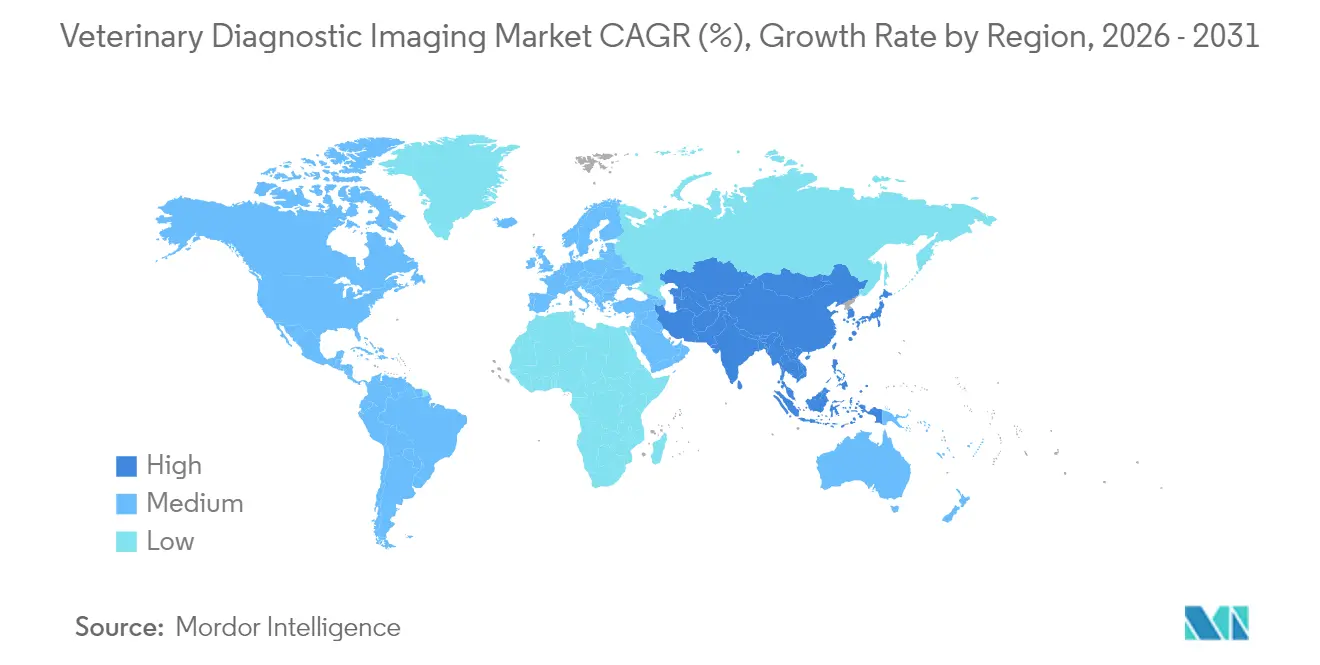

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Diagnostic Imaging Market Analysis by Mordor Intelligence

The Veterinary Diagnostic Imaging Market size was valued at USD 1.84 billion in 2025 and estimated to grow from USD 1.97 billion in 2026 to reach USD 2.79 billion by 2031, at a CAGR of 7.22% during the forecast period (2026-2031). The expansion reflects stronger demand for advanced screening as companion-animal owners seek human-equivalent care, wider clinical use of AI-assisted interpretation, and steady rollout of digital radiography, multi-slice CT, and other modalities. North America remains the revenue leader, while Asia Pacific records the fastest gains as rising disposable income and pet humanization reshape spending patterns. Equipment upgrades toward digital platforms, growth in oncology imaging, and regulatory livestock programs add further momentum. Structural headwinds such as shortages of board-certified radiologists and high capital costs persist but continue to spur interest in teleradiology and AI decision-support tools.[1]Source: American Veterinary Medical Association, “Artificial intelligence poised to transform veterinary care,” AVMA.org

Key Report Takeaways

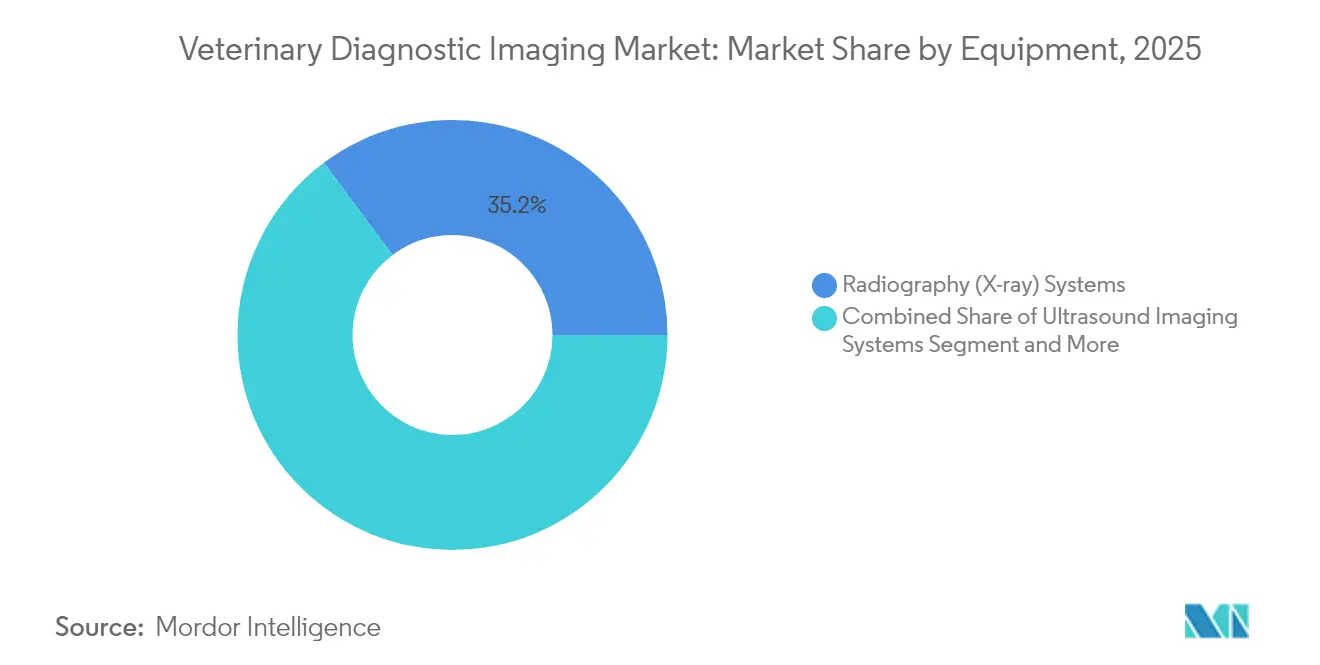

- By equipment, radiography systems led with 35.21% of the veterinary diagnostic imaging market share in 2025, while video endoscopy posted the highest projected CAGR at 8.63% through 2031.

- By application, orthopedics accounted for 34.02% share of the veterinary diagnostic imaging market size in 2025 and oncology is advancing at a 9.35% CAGR to 2031.

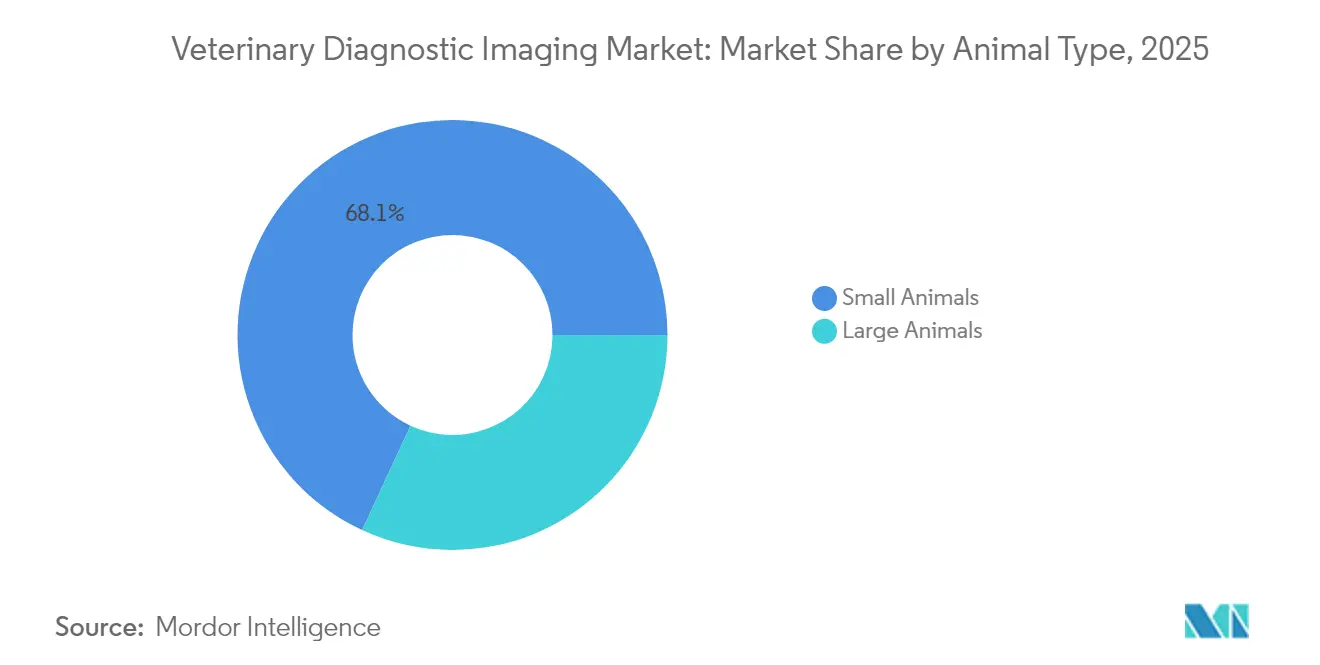

- By animal type, small animals held 68.10% of overall revenue in 2025; large animals advance the fastest at an 8.01% CAGR driven by mandated surveillance programs.

- By end user, veterinary hospitals and clinics captured 66.92% share in 2025, whereas diagnostic imaging centers are forecast to expand at an 8.29% CAGR through 2031.

- By geography, North America retained 41.35% revenue share in 2025, while Asia Pacific is projected to grow at a 9.08% CAGR and add the most incremental value by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Diagnostic Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Companion-Animal Population Fuelling Expenditure on Advanced Imaging Modalities | +1.2% | Global, with highest impact in North America & Asia Pacific | Long term (≥ 4 years) |

| Rapid Technological Innovations in Digital Radiography, Multi-slice CT and AI-based Image Analytics | +1.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Rising Burden of Chronic & Orthopedic Disorders in Pets Necessitating Early Diagnostic Imaging | +1.1% | Global, particularly developed markets | Long term (≥ 4 years) |

| Government-Led Livestock Disease Surveillance Programs Mandating Imaging-based Screening | +0.9% | North America, Europe, Australia & New Zealand | Short term (≤ 2 years) |

| Increasing Availability of Pet Insurance Policies Covering High-value Diagnostic Procedures | +0.8% | North America, Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| Expansion of Telemedicine and Remote Consultations | +0.6% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Global Companion-Animal Population Fuelling Expenditure on Advanced Imaging Modalities

Pet ownership among younger households is reshaping spending priorities and lifting routine demand for imaging beyond acute care. Pet insurance that reimburses X-rays and MRI lowers cost barriers, with MRI reimbursements ranging between USD 2,500 and USD 6,000, encouraging broader clinical use. Asia’s rapid rise in pet numbers, particularly in China and India, extends the customer base and opens niches for exotics and specialty services. Clinics such as Ohana Veterinary in Kuala Lumpur already employ AI-driven analyzers that benchmark blood and image data against global databases, demonstrating how demographic change directly translates into technology adoption. The sustained humanization narrative underpins long-term procedure volume growth, making advanced diagnostics part of routine wellness care rather than last-resort investigations.

Rapid Technological Innovations in Digital Radiography, Multi-slice CT and AI-based Image Analytics

Deep-learning algorithms embedded in systems such as Vetscan Imagyst flag abnormalities within seconds, raising diagnostic confidence and reinforcing client compliance. Professional bodies now publish guidance on validation and transparency, signaling an alignment between regulators and innovators. Photon-counting CT and zero-helium MRI units improve image clarity while trimming radiation dose and maintenance complexity, widening appeal among mid-sized practices. Early adopters report faster throughput and higher diagnostic yield, creating a competitive gap that presses lagging clinics to upgrade infrastructure. Collectively, technology convergence accelerates the replacement cycle and drives incremental equipment revenue within the veterinary diagnostic imaging market.

Rising Burden of Chronic & Orthopedic Disorders in Pets Necessitating Early Diagnostic Imaging

An aging pet population brings a higher prevalence of osteoarthritis, hip dysplasia, and neoplasia that require imaging to guide therapy plans. AI-assisted screening tools now enable non-invasive oncology detection that supports individualized interventions. Standing CT platforms for equine limbs, for example, allow full weight-bearing scans without general anesthesia, expanding preventive musculoskeletal surveillance in sports horses.[2]Source: Hallmarq Veterinary Imaging, “Guide to Standing Equine MRI: Everything You Need to Know,” hallmarq.net Preventive care programs introduced by corporate practice groups incorporate routine imaging into wellness packages, shifting revenue from episodic to recurring streams. Consequently, chronic disease management reinforces sustained equipment usage and positions imaging as a cornerstone of lifetime pet health tracking.

Government-Led Livestock Disease Surveillance Programs Mandating Imaging-Based Screening

Regulatory orders such as the USDA’s mandatory H5N1 testing in dairy cattle before interstate movement create unavoidable imaging demand and standardize minimum diagnostic capabilities. National plans in Australia allocate funding for portable screening platforms, ensuring that disease control strategies include imaging infrastructure. These directives stabilize capital-expenditure plans for suppliers and guarantee procedure volumes for service providers. Moreover, adherence to surveillance protocols elevates biosecurity credentials, which are vital for export-oriented producers seeking to avoid trade disruptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Shortage of Board-Certified Veterinary Radiologists and Trained Imaging Technicians | -1.4% | Global, most acute in North America & Europe | Long term (≥ 4 years) |

| High Capital & Lifecycle Cost of High-Field MRI and Multi-slice CT Systems for Smaller Practices | -1.1% | Global, particularly impacting smaller practices | Medium term (2-4 years) |

| Stringent Radiation-Safety Regulations and Licensing Requirements Extending Installation Timelines | -0.7% | Global, varying by jurisdiction | Short term (≤ 2 years) |

| Limited Pet Insurance and Cost Sensitivity | -0.9% | Emerging markets, rural areas globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Shortage of Board-Certified Veterinary Radiologists and Trained Imaging Technicians

Despite rising interest in imaging careers, training capacity remains flat, leading to a constrained talent pipeline that could leave a shortfall of more than 17,000 veterinarians by 2032, with imaging specialists among the scarcest.[3]Source: Hallmarq Veterinary Imaging, “Guide to Standing Equine MRI: Everything You Need to Know,” hallmarq.net The scarcity lengthens report turnaround times and limits the range of services smaller clinics can provide. Providers increasingly turn to teleradiology partnerships and AI-based preliminary reads to maintain service levels. While stop-gaps partly offset workload pressure, the underlying shortage continues to cap throughput, restraining the full growth potential of the veterinary diagnostic imaging market.

High Capital & Lifecycle Cost of High-Field MRI and Multi-slice CT Systems for Smaller Practices

Advanced modalities remain expensive, with CT scanners priced from USD 150,000 to more than USD 1 million, plus installation outlays and annual maintenance contracts. Even compact digital radiography units run USD 21,000–USD 35,000, stretching budgets for single-doctor practices. Financing packages and tax incentives soften upfront pain, yet lifecycle expenses such as room shielding, software upgrades, and staff certification persist. This cost profile keeps equipment penetration skewed toward corporate groups and specialty hospitals and explains why mobile imaging fleets and shared diagnostic centers grow faster than individual in-house purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Digital Innovation Drives Transformation

Radiography systems retained the largest revenue slice at 35.21% in 2025, demonstrating their role as the workhorse modality across companion-animal practice. The intuitive workflows, near-instant image availability, and lower radiation dose that accompany digital platforms encourage clinics to replace legacy film units, sustaining a vital pillar of the veterinary diagnostic imaging market. Ultrasound, bolstered by handheld probes and cloud-based AI triage, broadens access in first-opinion settings and farm calls.

Cone-beam CT units packaged in compact footprints unlock 3-D imaging for dental, orthopedic, and oncology cases within general practice environments. MRI, though premium in cost, differentiates referral centers, especially with innovations such as zero-helium magnets that mitigate helium supply risk and lower operational overhead. Video endoscopy, forecast to climb at an 8.63% CAGR, benefits from rising minimally invasive procedures and GI case complexity. Together, these trends keep the equipment landscape dynamic and spur continuous upgrades within the veterinary diagnostic imaging market

By Application: Oncology Emerges as Growth Leader

Orthopedics controlled 34.02% of 2025 revenue and remains core in small-animal referral workups, particularly for cruciate ligament, elbow dysplasia, and fracture management. Digital radiography allows rapid follow-up post-surgery, while 3-D CT refines pre-operative planning through virtual templating. In contrast, oncology claims the fastest trajectory with a 9.35% CAGR as early screening protocols penetrate routine check-ups. AI segmentation tools locate pulmonary nodules or abdominal masses at millimeter resolution, supporting treatment decisions and prognosis discussions.

Cardiology maintains stable demand through echocardiography and cardiovascular CT, helped by motion-compensating algorithms that capture accurate data despite respiratory and heart movement. Neurology benefits from standing MRI in equine and large breed dogs, mitigating anesthesia risk and post-procedure recovery time. Dentistry and gastroenterology leverage portable X-ray and high-definition endoscopes that broaden point-of-care capabilities. Cross-discipline blending of imaging and lab biomarkers solidifies imaging as the central pillar in multimodal diagnostics for the veterinary diagnostic imaging market.

By Animal Type: Large Animals Gain Momentum

The small-animal cohort—dogs, cats, and other household companions—accounted for 68.10% of revenue in 2025 and continues to drive bulk procedure volume. However, livestock and equine segments grow at 8.01% CAGR underpinned by policy-driven surveillance and sports medicine investments. The large animal segment's growth is driven by government-mandated surveillance programs and the increasing economic value of livestock in global food production systems. Dogs represent the largest individual segment within small animals, benefiting from advanced imaging technologies originally developed for human medicine and adapted for veterinary use. Cats present unique imaging challenges due to their size and temperament, driving innovation in portable and rapid imaging solutions.

Standing CT atlases for equine limb evaluation open new preventive pathways for athletic horses, while bovine ultrasound screens mastitis and reproductive status on-farm without needing transport to hospitals. Large animal imaging faces unique challenges including equipment portability requirements and the need for specialized restraint systems that ensure both animal welfare and diagnostic quality.

By End User: Diagnostic Centers Show Promise

Veterinary hospitals and clinics held 66.92% of spending in 2025 because most imaging is tied to direct clinical care. Consolidation trends among corporate groups deliver scale for multi-modality suites and negotiate favorable service contracts, deepening their foothold in the veterinary diagnostic imaging market. Dedicated imaging centers, expanding at an 8.29% CAGR, thrive on shared-service models that permit general practices to refer complex scans without heavy capital commitments.

Academic and research institutes invest steadily to pioneer modality advances—Tufts University recently allocated USD 7.5 million for a next-generation CT unit, underscoring the sector’s innovation engine. Mobile imaging fleets further widen access in rural corridors and during equine events, ensuring that advanced diagnostics reach animals independent of facility constraints.

Geography Analysis

North America retained a 41.35% share in 2025, anchored by high per-capita pet expenditures, mature insurance uptake, and dense specialty hospital networks. The United States continues to upgrade its digital infrastructure and adopt AI, yet it also grapples with acute radiologist shortages that accelerate teleradiology outsourcing. Canada’s strict radiation-safety codes prolong installation timelines but safeguard staff and animal welfare.

Europe delivers steady progress thanks to robust regulation and reimbursement structures. Germany and France sustain equipment renewal cycles, while the United Kingdom’s radiologist gap triggers policy discussion and increased AI pilot programs. EU-wide animal health strategies encourage cross-border knowledge exchange, reinforcing homogeneity in standards and supporting regional vendors.

Asia Pacific leads growth at a 9.08% CAGR as disposable incomes rise and millennials prioritize pet wellness. China’s urban market sees chain clinics adopting CT as a differentiator, whereas India’s emerging middle class lifts baseline demand for ultrasound and digital X-ray. Japan targets geriatric pet care, rolling out home-visit services equipped with portable imaging. Government programs across Australia and New Zealand strengthen livestock imaging to protect export revenue streams. Together, these dynamics underpin sustained expansion of the veterinary diagnostic imaging market in the region.

Competitive Landscape

The veterinary diagnostic imaging market exhibits moderate consolidation. IDEXX Laboratories alone controls substantial share of the global diagnostic revenues through its ecosystem that combines imaging, in-clinic analyzers, and cloud software, creating high client stickiness. Siemens Healthineers’ acquisition of Varian signals a move to comprehensive imaging-therapy packages that could migrate from human to veterinary settings.

Niche innovators emphasize species-specific or workflow-friendly solutions. Hallmarq’s standing equine MRI and zero-helium small-animal MRI reduce anesthesia risk and operating cost, carving a unique value proposition. Canon Medical introduces automated hybrid fluoro-rad suites, while GE HealthCare partners with cloud vendors to turbocharge AI pipeline releases.

Competitive strategies revolve around subscription models, integrated cloud archives, and training packages to offset equipment commoditization. Teleradiology start-ups and AI triage vendors collaborate with scanner manufacturers, ensuring that scarce radiologist capacity is amplified rather than replaced. Acquisitions of regional practice groups by private-equity buyers such as EQT fuel higher equipment purchasing power and accelerate technology standardization across networks.

Veterinary Diagnostic Imaging Industry Leaders

Esaote SPA

IDEXX Laboratories Inc.

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: IDEXX Laboratories, Inc. has unveiled the ImageVue DR50 Plus Digital Imaging System, marking its latest leap in diagnostic imaging for veterinarians. This cutting-edge system not only promises high-definition, AI-enhanced imaging but also prioritizes safety, cutting radiation exposure by up to 25% against IDEXX's top-tier ImageVue DR50 and a significant 60% when stacked against competing veterinary imaging solutions.

- January 2026: HT Vet, a pioneering veterinary health technology firm, has unveiled VISTA iQ, an advanced AI-driven successor to its original HT Vista scanner. This next-gen tool not only retains the trusted performance of its forerunner but also boasts enhanced usability, speed, and diagnostic efficiency.

- October 2024: The American College of Veterinary Radiology Annual Scientific Conference spotlighted artificial intelligence applications in workflow optimization, lesion detection, and diagnostic accuracy.

Global Veterinary Diagnostic Imaging Market Report Scope

As per the scope of this report, veterinary diagnostic imaging is defined as the non-invasive method of taking medical images of animals to diagnose a disease. It includes a detailed analysis of imaging equipment, application, and animal type, along with the areas in which they are being used. The market is segmented by equipment (Radiography (X-ray) Systems, Ultrasound Imaging Systems, Computed Tomography Imaging Systems, Magnetic Resonance Imaging Systems, Video Endoscopy Imaging Systems, and Other Equipment), Application (Cardiology, Oncology, Neurology, Orthopedics, Other Applications), Animal Type (Small Animals, Large Animals), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Radiography (X-ray) Systems | Digital X-ray Systems |

| Analog X-ray Systems | |

| Ultrasound Imaging Systems | 2-D Ultrasound |

| Doppler Ultrasound | |

| 3-D/4-D Ultrasound | |

| Computed Tomography Imaging Systems | Multi-slice CT |

| Cone-Beam CT | |

| Magnetic Resonance Imaging Systems | Low-field MRI |

| High-field MRI | |

| Video Endoscopy Imaging Systems | |

| Other Equipment (Fluoroscopy, Nuclear Imaging) |

| Cardiology |

| Oncology |

| Neurology |

| Orthopedics |

| Dentistry |

| Gastroenterology |

| Small Animals | Dogs |

| Cats | |

| Large Animals | Equine |

| Bovine | |

| Swine & Others |

| Veterinary Hospitals & Clinics |

| Diagnostic Imaging Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Equipment | Radiography (X-ray) Systems | Digital X-ray Systems |

| Analog X-ray Systems | ||

| Ultrasound Imaging Systems | 2-D Ultrasound | |

| Doppler Ultrasound | ||

| 3-D/4-D Ultrasound | ||

| Computed Tomography Imaging Systems | Multi-slice CT | |

| Cone-Beam CT | ||

| Magnetic Resonance Imaging Systems | Low-field MRI | |

| High-field MRI | ||

| Video Endoscopy Imaging Systems | ||

| Other Equipment (Fluoroscopy, Nuclear Imaging) | ||

| By Application | Cardiology | |

| Oncology | ||

| Neurology | ||

| Orthopedics | ||

| Dentistry | ||

| Gastroenterology | ||

| By Animal Type | Small Animals | Dogs |

| Cats | ||

| Large Animals | Equine | |

| Bovine | ||

| Swine & Others | ||

| By End User | Veterinary Hospitals & Clinics | |

| Diagnostic Imaging Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the veterinary diagnostic imaging market?

The veterinary diagnostic imaging market size is USD 1.97 billion in 2026 and is forecast to reach USD 2.79 billion by 2031.

Which equipment category holds the largest revenue share?

Radiography systems led with 35.21% of revenue in 2025, reflecting their essential role in routine diagnostics.

Which application segment is growing the fastest?

Oncology imaging shows the quickest pace, advancing at a 9.35% CAGR through 2031 due to earlier cancer screening uptake.

Why is Asia Pacific considered the fastest-growing region?

Rising pet ownership, larger middle-class populations, and growing awareness of advanced care drive a 9.08% CAGR in Asia Pacific.

How are workforce shortages being addressed?

Clinics increasingly adopt teleradiology and AI decision-support tools to compensate for limited numbers of board-certified radiologists.

What factors limit adoption of MRI and CT in smaller practices?

High capital expenditure, ongoing maintenance costs, and stringent installation regulations restrict uptake of high-field modalities.

Page last updated on: