Veterinary Sutures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

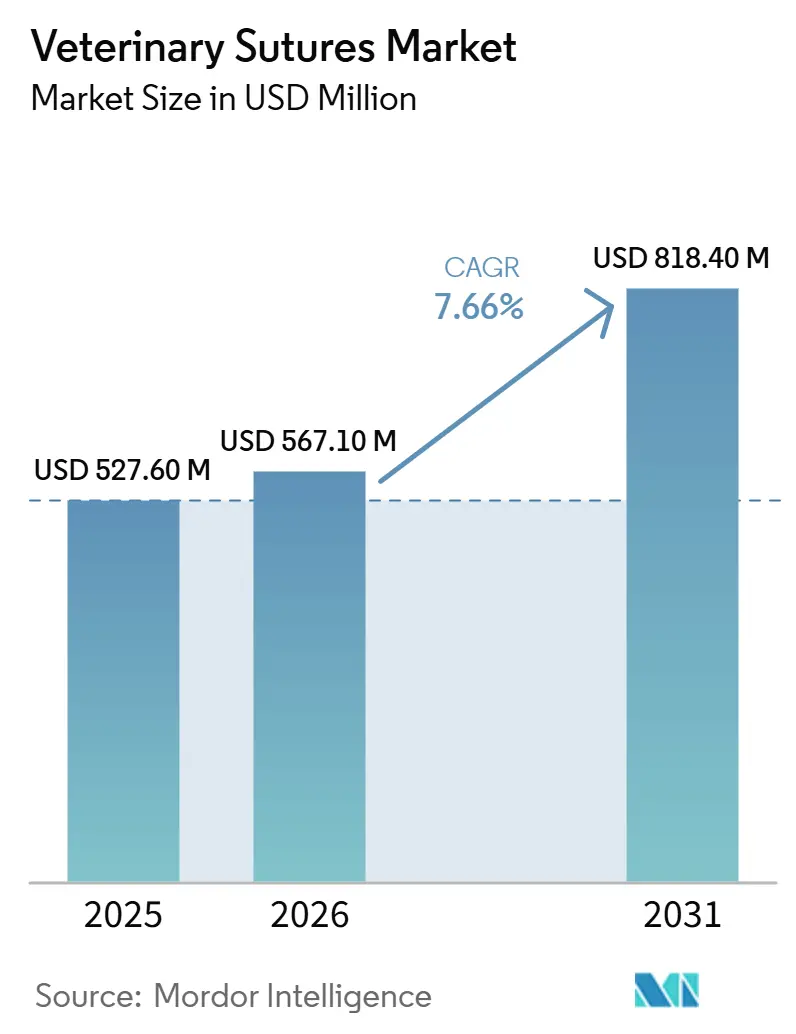

| Market Size (2026) | USD 567.10 Million |

| Market Size (2031) | USD 818.40 Million |

| Growth Rate (2026 - 2031) | 7.66% CAGR |

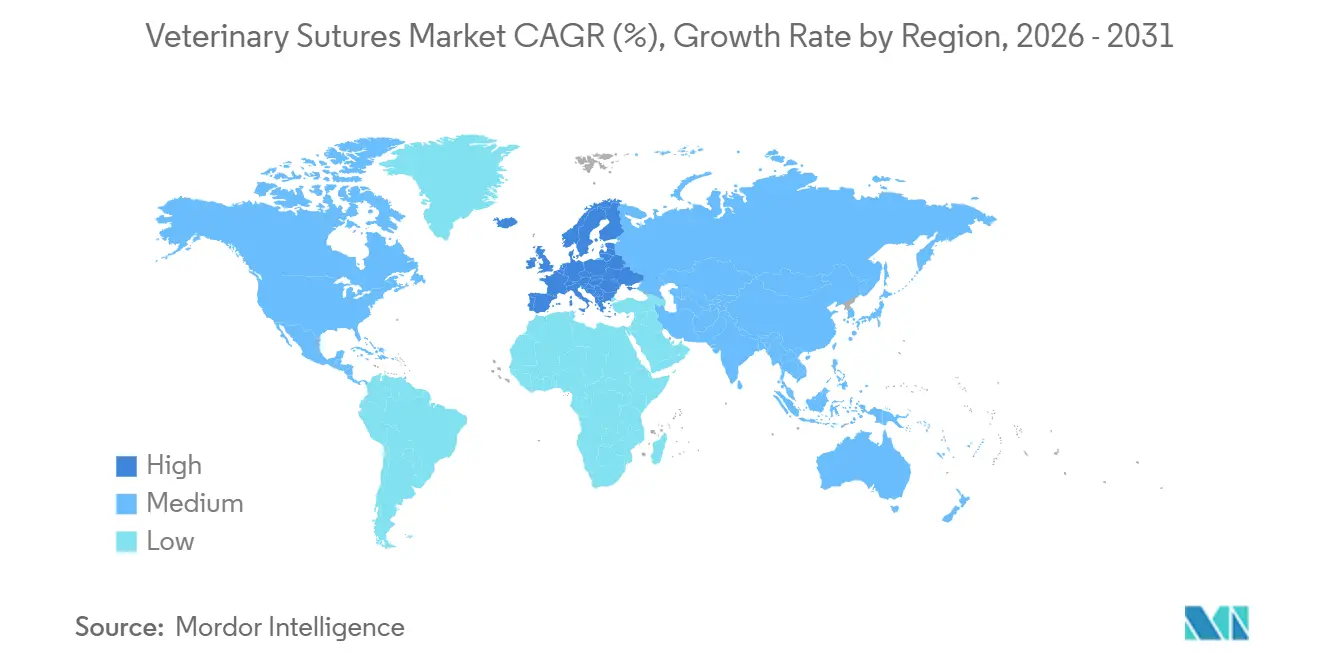

| Fastest Growing Market | Europe |

| Largest Market | North America |

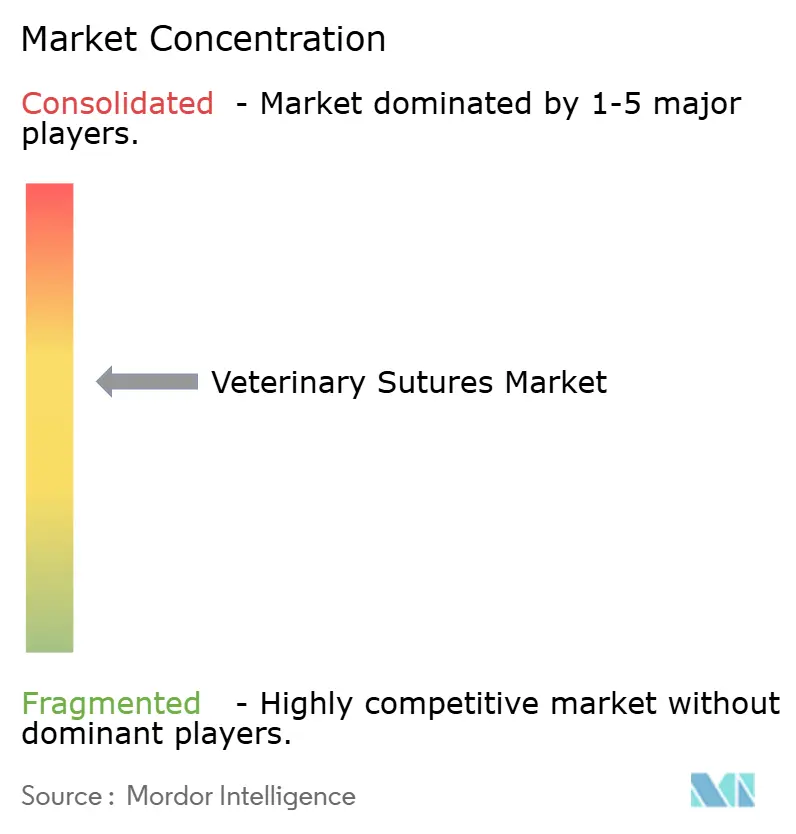

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Sutures Market Analysis by Mordor Intelligence

The Veterinary Sutures Market size was valued at USD 527.60 million in 2025 and is estimated to grow from USD 567.10 million in 2026 to reach USD 818.40 million by 2031, at a CAGR of 7.66% during the forecast period (2026-2031).

Increasing companion-animal surgical volumes, wider pet-insurance coverage, and the shift toward absorbable and barbed products that shorten operating-room time are the leading growth catalysts. North America retained the largest regional share in 2025, yet Europe is set to grow fastest as hospital consolidation under Mars Petcare’s AniCura group streamlines procurement and harmonized European regulations accelerate device approvals. Across applications, dermatologic and plastic procedures are rising quickly because barbed sutures remove knot-tying steps, while antimicrobial stewardship policies are pivoting clinics toward triclosan-coated lines that limit infection without systemic antibiotics. Price pressure persists in the veterinary sutures market as hospital chains leverage private-label contracts, but demand for coated, knotless, and absorbable innovations supports premium price points.

Key Report Takeaways

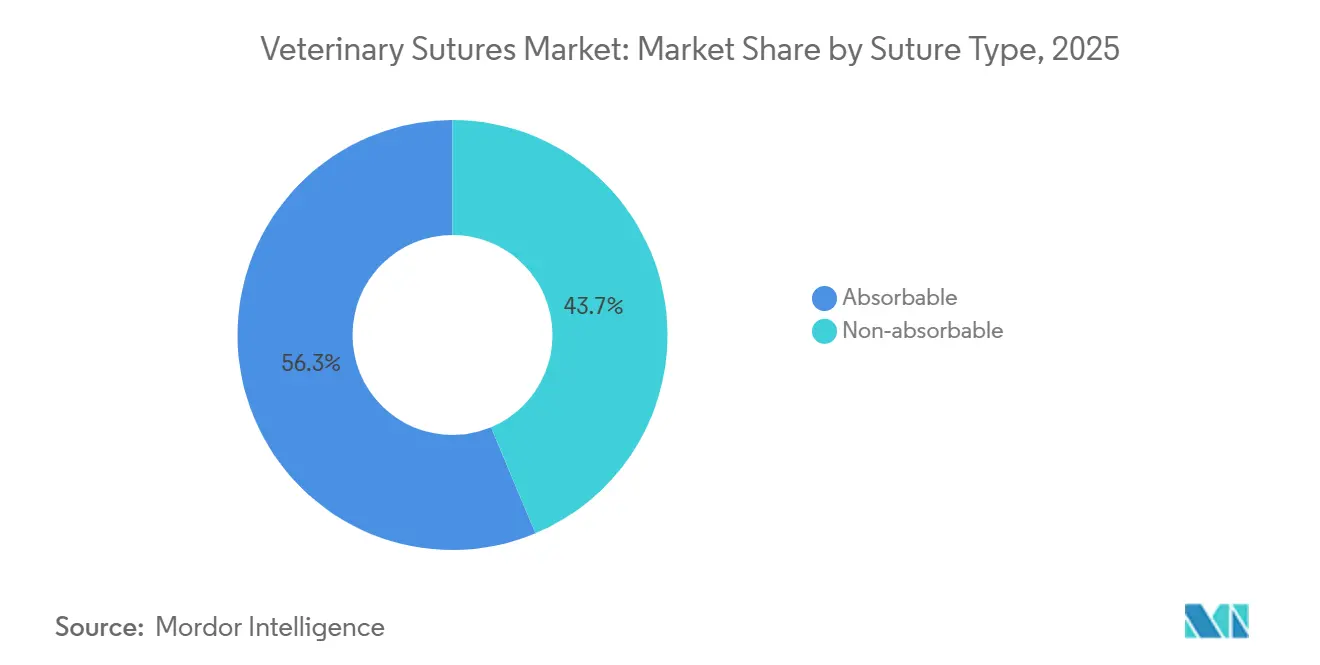

- By suture type, absorbable sutures led with 56.30% of the veterinary sutures market share in 2025 and are expanding at an 8.12% CAGR through 2031.

- By structure, monofilament structures commanded 61.67% share of the veterinary sutures market size in 2025 and are advancing at an 8.21% CAGR over the forecast horizon.

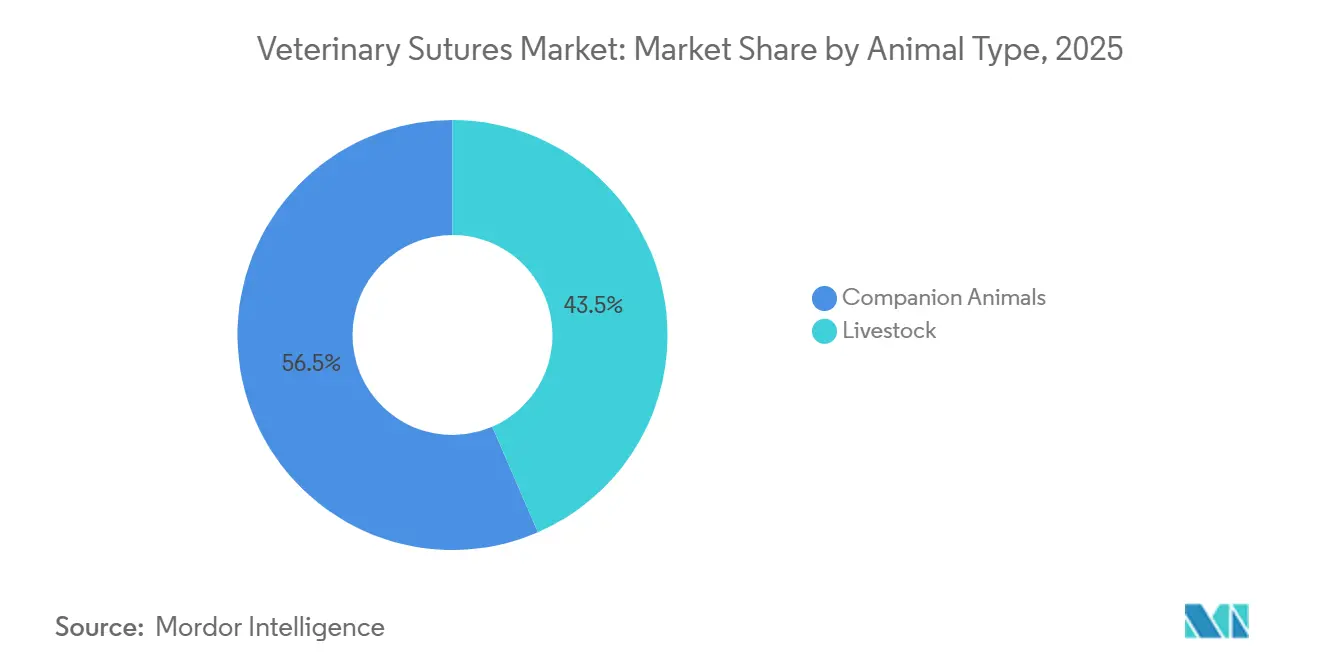

- By animal type, companion animals generated 56.50% of demand in 2025, and is expected to grow by 7.98% CAGR through 2031.

- By end users, veterinary hospitals accounted for 45.82% of 2025 revenue; ambulatory and specialty centers are the fastest-growing channel, with a 7.9% CAGR to 2031.

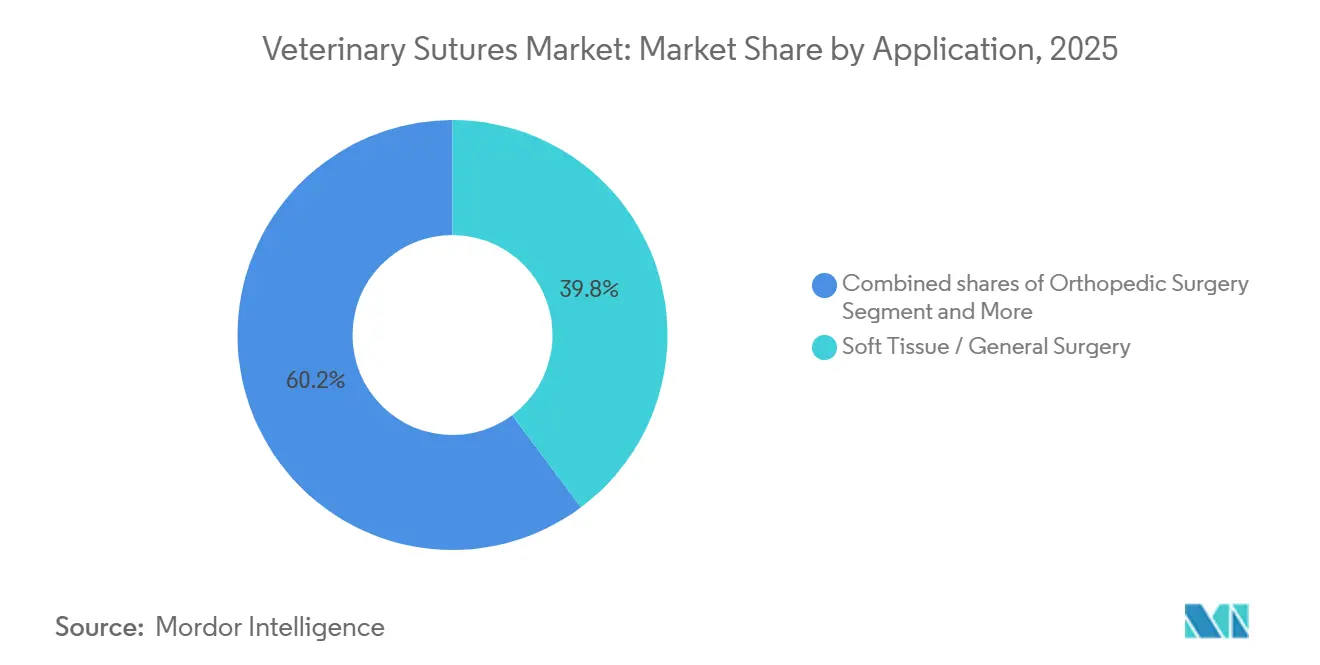

- By application, Soft Tissue / General Surgery accounted for 39.80% of 2025 revenue, while dermatologic and plastic procedures rose at a 7.93% CAGR through 2031.

- By geography, North America captured 35.78% of 2025 revenue, while Europe is poised to post the fastest 8.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Sutures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High surgical volumes in companion animals | +1.8% | North America & Europe core, global relevance | Medium term (2-4 years) |

| Pet-insurance expansion | +1.5% | North America, Europe, emerging APAC cities | Medium term (2-4 years) |

| Preference for absorbable sutures | +1.2% | Global | Short term (≤ 2 years) |

| Asia-Pacific veterinary infrastructure buildout | +1.4% | APAC focus, spillover to Middle East | Long term (≥ 4 years) |

| Adoption of barbed and antibacterial sutures | +1.0% | North America & Europe early, APAC following | Medium term (2-4 years) |

| HQHVSN and mobile-clinic expansion | +0.9% | North America, Latin America, pilot APAC programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Surgical Volumes in Companion Animals Drive Baseline Demand

Shelters admitted 2.8 million animals in the United States during the first half of 2025, and adoption rates climbed to 76%, seeding future elective surgeries that consume large suture quantities [1]Shelter Animals Count, “National Shelter Database,” shelteranimalscount.org. High-quality high-volume spay-neuter (HQHVSN) clinics now complete 25-60 procedures daily, standardizing barbed absorbable sutures to maximize throughput. Lower procedure costs from these efficiencies broaden access for cost-sensitive pet owners and municipalities, stabilizing demand even in downturns. Rising diagnostic-imaging use is pushing tumor resections higher, layering additional volume. Together, shelter sterilization and owner-funded elective work form a resilient dual-engine that underpins the veterinary sutures market.

Pet Insurance Expansion Unlocks Advanced Procedures

North American pet-insurance premiums grew 20.8% in 2024 to USD 5.15 billion, lifting insured pets to 6.4 million and reducing out-of-pocket hurdles for advanced surgeries [2]North American Pet Health Insurance Association, “State of the Industry 2025,” naphia.org. Policies now routinely cover orthopedic repairs and complex oncologic work, driving uptake of absorbable and barbed lines that reduce anesthesia episodes. European penetration already exceeds 25% in the United Kingdom and Scandinavia, and pilot products in urban China and India are replicating this model. As insurance spreads, case-mix shifts to higher-acuity interventions that need more and more sophisticated closure materials, lifting both volume and average selling price. Insurers’ reimbursement guidelines also validate premium products, reinforcing their position in the veterinary sutures market.

Absorbable Sutures Reduce Follow-Up Visits and Anesthesia Risk

Polyglycolic acid, polydioxanone, and poliglecaprone sutures degrade predictably over 60-180 days, aligning with tissue-healing timelines and eliminating removal visits. Clinics report fewer no-shows and smoother scheduling when removal appointments are unnecessary. Owners appreciate the reduced anesthesia exposure, and veterinarians gain workflow efficiency. Though absorbable materials carry a price premium, avoided follow-up labor offsets the differential. FDA-CVM oversight on degradation kinetics imposes quality standards that shield incumbents from subpar imports.

Asia-Pacific Veterinary Infrastructure Expansion Creates Long-Term Growth

Private-equity investors in this region are funding hospital chains in tier-one cities, widening surgical capacity [3]PetHadoop, “China Pet Industry White Paper 2024,” pethadoop.com. Japan’s 24.2 million pets sustain a mature specialty-care ecosystem, while India’s veterinary colleges add hundreds of graduates yearly, easing practitioner shortages. Governments in South Korea and Australia are subsidizing mobile clinics that reach rural owners, seeding demand where brick-and-mortar hospitals are scarce. The region’s growth story centers on volume expansion as first-time pet owners access basic surgery, positioning APAC as a pillar of the future veterinary sutures market revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tissue adhesives and staples substitution | -0.8% | North America & Europe first adopters | Short term (≤ 2 years) |

| Private-label & low-cost regional suppliers | -0.6% | Global, sharpest in APAC & Latin America | Medium term (2-4 years) |

| Veterinary workforce shortages | -0.5% | North America & Europe | Medium term (2-4 years) |

| Rising antimicrobial-performance standards | -0.3% | North America & Europe regulatory settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tissue Adhesives and Staples Erode Share in Select Applications

Cyanoacrylate glues and skin staples close low-tension wounds in seconds, saving surgeon time and allowing technicians to handle routine closures under supervision. HQHVSN clinics adopt them aggressively because minutes shaved per case multiply across dozens of daily procedures. Nonetheless, adhesives cost more per use when waste from partially used tubes is factored in, and staples require a removal visit unless absorbable variants are chosen, narrowing their appeal. The substitution risk is therefore confined to roughly 10-15% of the veterinary sutures market, mainly within commodity non-absorbable lines.

Private-Label and Regional Manufacturers Intensify Price Pressure

Hospital chains such as Mars Petcare’s VCA leverage scale to source private-label sutures from ISO-13485-certified factories in India and Turkey at significant discounts to branded equivalents. Regional makers like Orion Sutures and KATSAN are winning bids in Latin America and Southeast Asia, commoditizing basic monofilament offerings. Branded incumbents respond by focusing on patented coatings and barbed structures, but margin compression is unavoidable in the price-sensitive tiers of the veterinary sutures market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Suture Type: Absorbable Materials Extend Leadership

Absorbable products captured 56.30% of the veterinary sutures market share in 2025 and are forecast to grow with 8.12% CAGR. Hospitals prefer polyglycolic-acid and polydioxanone lines for soft-tissue closures because they negate removal visits, reduce anesthesia risk, and satisfy owner convenience. The veterinary sutures market size tied to absorbables is therefore rising faster than overall revenue growth, even in price-sensitive regions where follow-up logistics are difficult.

Barbed absorbable variants compound the speed advantage by eliminating knots, and early adoption in HQHVSN programs signals mainstream diffusion. Non-absorbables keep niche roles in tendon repairs and large-animal external skin closures where lasting tensile support is vital, yet their share is eroding as polymer science boosts absorbable strength. Regulatory scrutiny from FDA-CVM on hydrolysis profiles sets a quality baseline that discourages low-grade imports, maintaining brand loyalty where surgical risk is highest.

By Structure: Monofilament Gains on Infection Control Priorities

Monofilament lines held 61.67% of market revenue in 2025, and are expected to grow at 8.21% CAGR by 2031. Reduced tissue drag shortens operating time, and lower bacterial adherence aligns with antimicrobial-stewardship goals. Consequently, the value slice of the veterinary sutures market size earned by monofilament is growing faster than braided alternatives.

Barbed monofilament adds another layer of utility, merging infection control with time savings. Braided sutures still dominate cardiovascular and ophthalmic procedures where pliability overrides infection concerns. Manufacturers counter monofilament gains by adding antibacterial coatings to braided lines, but structural disadvantages remain. As clinics measure post-operative complication rates more rigorously, surgeons default to monofilament for contaminated fields, reinforcing the shift.

By Animal Type: Companion Pets Sustain the Core Demand Base

Companion animals generated 56.50% of sales in 2025 and are advancing at a 7.98% CAGR, reflecting sustained dog and cat procedure counts in urban centers with high disposable income. Pet-insurance adoption and owner willingness to pay for tumor resections, cruciate repairs, and cosmetic closures underpin this growth. Consequently, the companion slice of the veterinary sutures market remains the strategic focus for premium innovations such as barbed antibacterial lines.

Livestock demand lags, growing notably, as cattle and swine surgeries emphasize emergency interventions where cost trumps sophistication. Equine procedures form a small premium niche but cannot shift aggregate market dynamics. Unless farm-animal welfare regulations tighten surgical requirements, livestock will remain a modest share contributor through 2031.

By End User: Hospitals Lead, Ambulatory Centers Accelerate

Veterinary hospitals captured 45.82% of 2025 revenue and are expected to grow with 7.87% CAGR through 2031, thanks to referral cases that require multi-layer closures and drive higher per-procedure suture consumption. Consolidation within corporate chains allows these hospitals to negotiate bulk discounts while retaining branded absorbable and barbed lines for complex cases. Clinics and mobile HQHVSN units collectively account for a significant share and are racing ahead with notable CAGR, propelled by standardized kits and outreach programs.

Academic institutes, though small purchasers, influence product selection by validating new materials in controlled trials, thereby shaping future demand across the veterinary sutures market. Tele-consult platforms further redistribute case flow, routing advanced surgeries to specialty centers that stock higher-margin closure devices.

By Application: Dermatologic Procedures Outpace Soft-Tissue Core

Soft-tissue and general surgery remained the volume leader at 39.80% in 2025, anchoring baseline consumption. Yet dermatologic and plastic procedures are expanding at a 7.93% CAGR thanks to barbed sutures that quicken cosmetic skin closures and rising owner demand for scar-minimal outcomes, lifting the veterinary sutures market size dedicated to these treatments.

Orthopedics holds substantial value because high-strength braided polyester and UHMWPE lines carry premium prices, even though case counts are lower. Ophthalmic and dental surgeries rely on ultra-fine absorbables, and their incremental gains collectively add meaningful volume. Overall, applications with both technical complexity and strong owner pay propensity are reshaping the product-mix toward barbed and antibacterial innovations.

Geography Analysis

North America accounted for 35.78% of the veterinary sutures market in 2025, underpinned by more than 30,000 U.S. practices and 6.4 million insured pets that authorize elective interventions. Workforce shortages temper growth, yet HQHVSN programs performing up to 60 sterilizations daily keep baseline volumes healthy. FDA-CVM regulations on biocompatibility maintain a quality floor that favors established suppliers.

Europe is projected to post an 8.03% CAGR through 2031, the fastest among all regions. AniCura’s 400-clinic network centralizes purchasing and accelerates adoption of triclosan-coated lines under uniform protocols. EMA device-approval harmonization lowers launch hurdles, and pet-insurance penetration above 25% in the United Kingdom sustains demand for premium absorbables. Eastern Europe emerges as a price-competitive manufacturing base for private-label sutures, while Scandinavian countries pilot next-gen antimicrobial coatings.

Asia-Pacific trails in market share but leads in incremental volume, driven by China’s USD 39.8 billion pet economy and rapid hospital build-outs. Japan provides a mature template for specialty practice, and Indian chains open flagship hospitals in metros, widening access. Regional makers like Genia Group and Orion Sutures win on price, yet rising quality expectations open lanes for branded coated and barbed imports. Middle East & Africa and South America remain small but rising as disposable incomes widen surgical access, with Brazil’s large dog population anchoring Latin American demand.

Competitive Landscape

The veterinary sutures market shows moderate fragmentation, with B. Braun Vet Care, Ethicon, and Medtronic anchoring the multinational tier. Corza Medical’s Quill Vet barbed range and DemeTECH’s antibacterial coated lines differentiate through patented technology. Consolidating buyers Mars Petcare, National Veterinary Associates, and Covetrus-backed distributors exert downward price pressure by sourcing private-label sutures from ISO-13485 plants in India and Turkey.

Innovation remains the principal moat: barbed geometries cut closure time 30-40%, and new antimicrobial peptides under development aim to replace triclosan and sidestep resistance concerns. Arthrex Vet Systems leverages human-sports-medicine fiber technology to supply ultra-strong orthopedic tapes, while Securos Surgical markets anchor-plus-suture kits that simplify cruciate repairs. FDA-CVM and EMA compliance costs still deter some low-cost entrants, yet rising regional suppliers narrow the gap as they invest in cleanrooms and automated packaging lines.

Future competition will likely polarize into high-performance coated and barbed segments, where incumbents retain pricing power, and commoditized monofilament tiers, where private-label gains share. Strategic alliances between hospital chains and device firms, as well as bundled procurement platforms that integrate inventory software with consumable supply, will shape bargaining dynamics through 2031.

Veterinary Sutures Industry Leaders

Medtronic plc

Johnson & Johnson

B. Braun Melsungen AG

Corza Medical, Inc.

Dolphin Sutures

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Assut Europe announced the launch of its veterinary suture line under the brand name of GexFix Veterinary Medical Devices in the United States.

- May 2025: B. Braun established a private label manufacturing partnership with AIP Medical to produce biodegradable veterinary sutures.

- February 2025: Mars Petcare secured full ownership of AniCura, allowing centralized suture procurement across 400 European clinics and amplifying buyer leverage.

Global Veterinary Sutures Market Report Scope

As per the scope of the report, veterinary sutures are indispensable tools used to oppose damaged tissues, close surgical incisions, and ligate blood vessels to facilitate natural healing.

The veterinary sutures market is segmented by suture type, structure, animal type, end users, application, and geography. By suture type, the market is segmented into absorbable and non‑absorbable. By structure, the market is segmented into monofilament and multifilament. By animal type, the market is segmented into companion animals and livestock. By end user, the market is segmented into veterinary hospitals, veterinary clinics, ambulatory & specialty centers, and academic & research institutes. By applications, the market is segmented into soft tissue / general surgery, orthopedic surgery, ophthalmic surgery, dental/oral surgery, gastrointestinal & urologic surgery, and dermatologic & plastic procedures.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Absorbable |

| Non‑absorbable |

| Monofilament |

| Multifilament (Braided) |

| Companion Animals |

| Livestock |

| Veterinary Hospitals |

| Veterinary Clinics |

| Ambulatory & Specialty Centers |

| Academic & Research Institutes |

| Soft Tissue / General Surgery |

| Orthopedic Surgery |

| Ophthalmic Surgery |

| Dental / Oral Surgery |

| Gastrointestinal & Urologic Surgery |

| Dermatologic & Plastic Procedures |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Suture Type | Absorbable | |

| Non‑absorbable | ||

| By Structure | Monofilament | |

| Multifilament (Braided) | ||

| By Animal Type | Companion Animals | |

| Livestock | ||

| By End User | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Ambulatory & Specialty Centers | ||

| Academic & Research Institutes | ||

| By Application | Soft Tissue / General Surgery | |

| Orthopedic Surgery | ||

| Ophthalmic Surgery | ||

| Dental / Oral Surgery | ||

| Gastrointestinal & Urologic Surgery | ||

| Dermatologic & Plastic Procedures | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Where is regional growth strongest?

Europe is the fastest-growing geography with an 8.03% CAGR through 2031, driven by hospital consolidation and high insurance penetration.

Which product category leads global demand?

Absorbable sutures hold the top position, accounting for 56.30% of 2025 revenue and expanding faster than the overall market.

Why are barbed sutures gaining popularity?

Bidirectional barbs eliminate knot-tying, trimming closure time by up to 40% and freeing operating-room capacity in staff-constrained clinics.

What limits market growth despite rising pet ownership?

Veterinary-staff shortages lengthen wait times for elective surgeries, capping procedure counts in North America and Europe.

How big is the Veterinary Sutures Market?

The Veterinary Sutures Market size is estimated to be USD 527.60 million in 2025.

Page last updated on: