Erythropoietin Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.02 Billion |

| Market Size (2031) | USD 36.48 Billion |

| Growth Rate (2026 - 2031) | 11.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

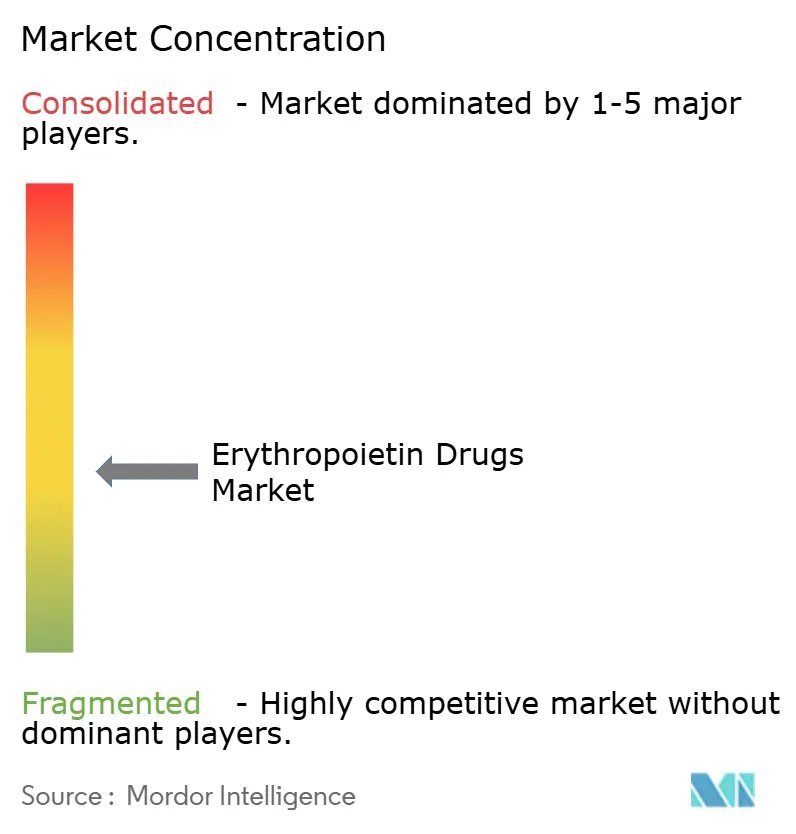

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Erythropoietin Drugs Market Analysis by Mordor Intelligence

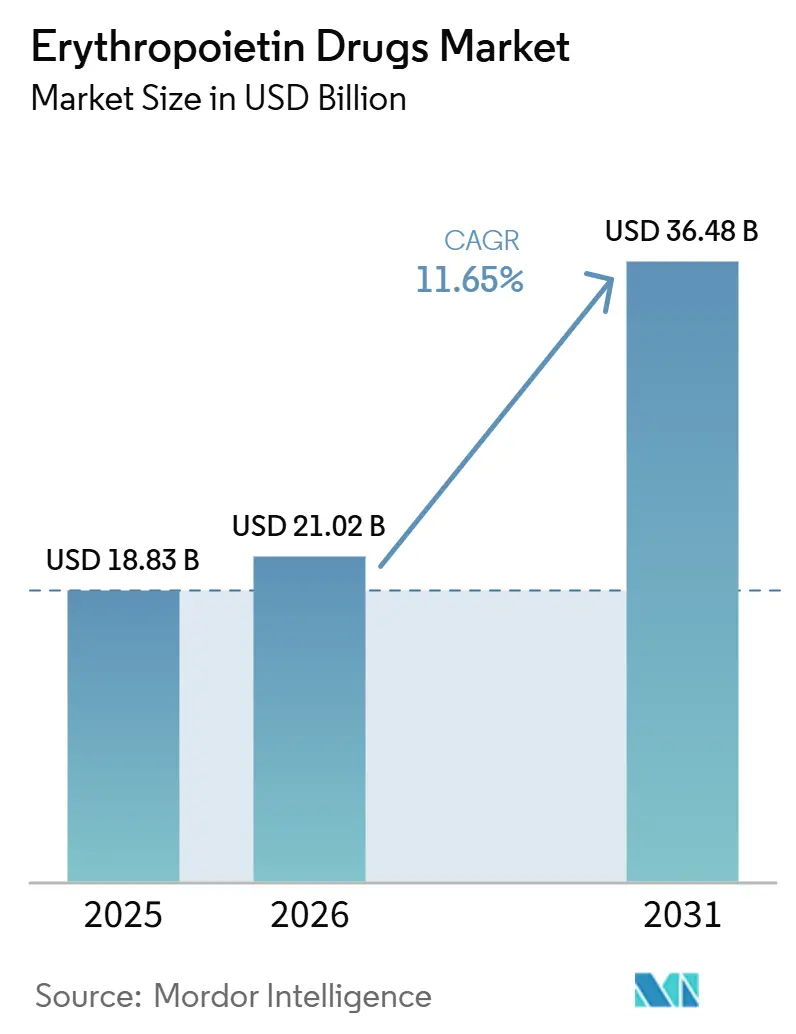

The Erythropoietin Drugs Market size was valued at USD 18.83 billion in 2025 and is estimated to grow from USD 21.02 billion in 2026 to reach USD 36.48 billion by 2031, at a CAGR of 11.65% during the forecast period (2026-2031).

The erythropoietin drugs market continues to gain from the expanding chronic kidney disease patient base, with the Global Burden of Disease Study 2025 reporting 788 million adults living with chronic kidney disease in 2025, up from 378 million in 1990. The Kidney Disease: Improving Global Outcomes (KDIGO) 2026 guideline supports steady prescribing by placing erythropoiesis-stimulating agents ahead of hypoxia-inducible factor prolyl hydroxylase inhibitors (HIF-PHIs) in chronic kidney disease anemia management.[1]GBD 2023 CKD Collaborators, “Global, Regional, and National Burden of Chronic Kidney Disease in Adults, 1990–2023, and Its Attributable Risk Factors,” The Lancet, thelancet.com Biosimilar expansion in cost-sensitive health systems is improving treatment access for dialysis and oncology patients, while extended-interval products strengthen value positioning by reducing injection frequency and supporting renal clinic and outpatient care workflows. However, HIF-PHI products remain credible oral substitutes in some countries, and the World Health Organization (WHO) did not support broader essential medicines expansion for chemotherapy-induced anemia.

Key Report Takeaways

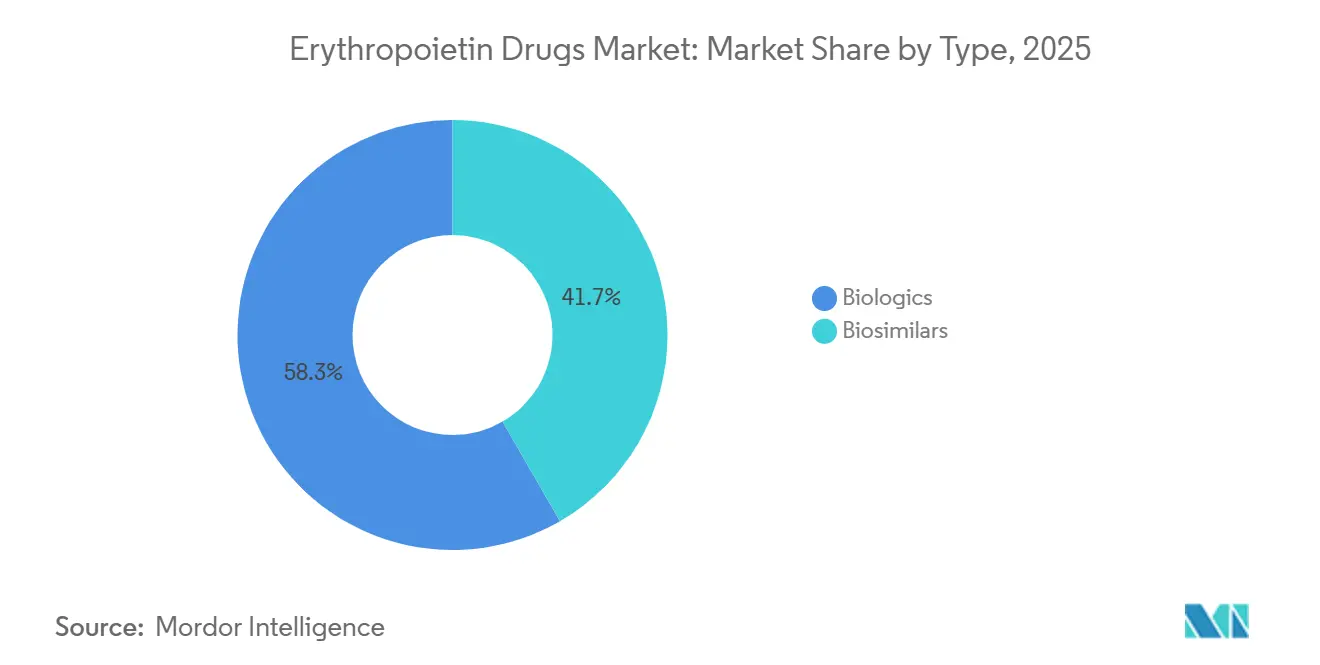

- By type, biologics held 58.34% share in 2025, while biosimilars are projected to grow at 14.53% CAGR through 2031.

- By product, epoetin alfa accounted for 35.45% share in 2025, while darbepoetin alfa is forecast to expand at 13.67% CAGR through 2031.

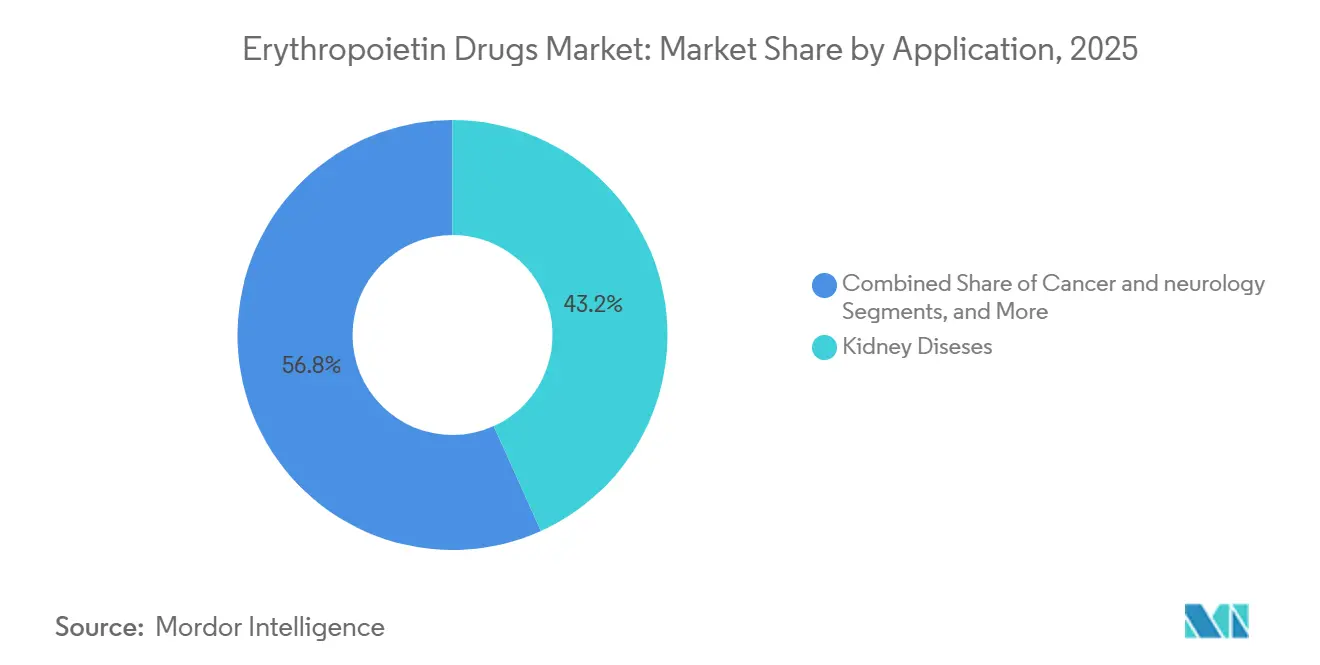

- By application, kidney diseases represented 43.24% share in 2025, while cancer is expected to record the fastest growth at 12.35% CAGR through 2031.

- By end user, hospitals captured 48.67% share in 2025, while home care settings are projected to grow at 14.67% CAGR through 2031.

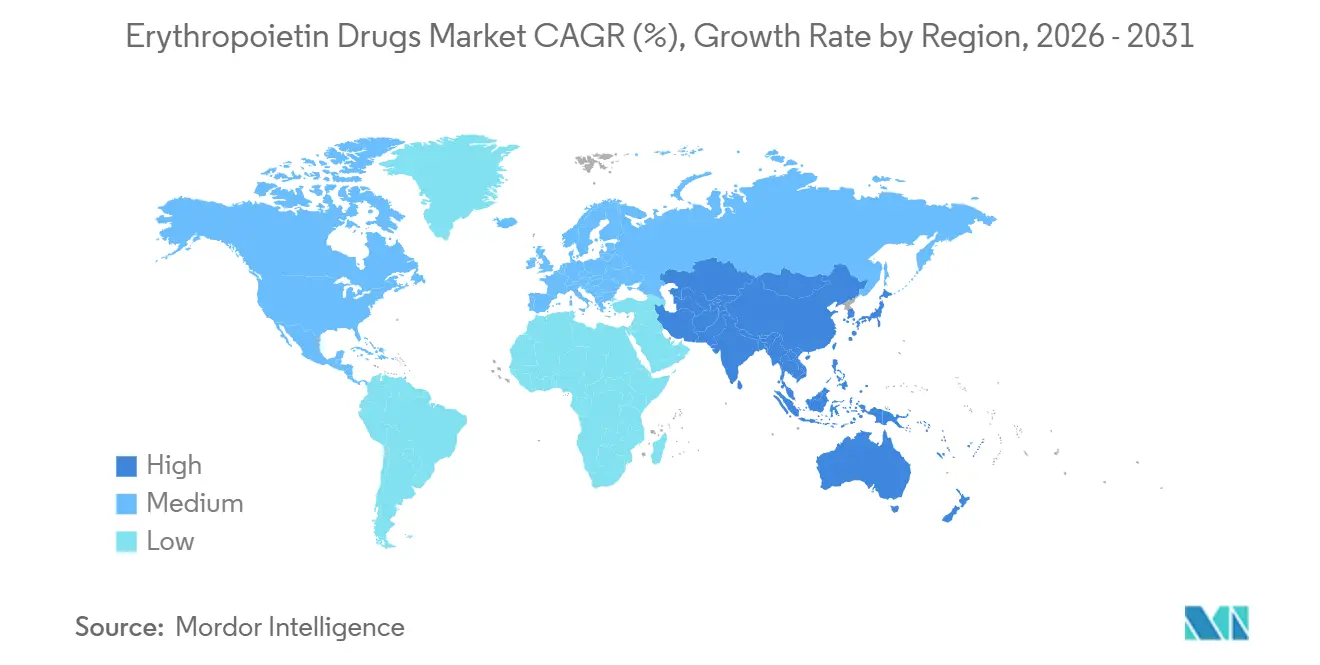

- By geography, North America held 39.86% share in 2025, while Asia-Pacific is expected to advance at 14.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Erythropoietin Drugs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of chronic kidney disease and anemia | +3.8% | Global, most acute in Asia-Pacific, Middle East and Africa, and North America | Long term (≥ 4 years) |

| Expanding chemotherapy-induced anemia supportive care use | +1.5% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Biosimilar penetration in price-sensitive hospital procurement | +2.0% | Asia-Pacific core, with spillover into Middle East and Africa and South America | Medium term (2-4 years) |

| Long-acting ESA adoption in dialysis and renal clinics | +1.2% | China, Japan, Germany, and the United States | Medium term (2-4 years) |

| Transfusion-avoidance protocols in surgical and oncology care | +0.8% | North America and Europe, with growing relevance in South Korea and Australia | Medium term (2-4 years) |

| Local manufacturing and public tender localization in emerging markets | +0.7% | India, China, Brazil, GCC, and South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Kidney Disease and Anemia

The erythropoietin drugs market is gaining from a growing chronic kidney disease (CKD) patient base rather than short-term pricing cycles. The Global Burden of Disease (GBD) Study 2025 reported 788 million adults living with CKD in 2025, compared with 378 million in 1990, expanding the long-term treatment pool for anemia management. KDIGO noted that anemia prevalence rises sharply with CKD progression and exceeds 90% in stage G5 across multiple cohorts, while the Indian Society of Nephrology’s 2025 guidance supports erythropoiesis-stimulating agent (ESA) initiation when hemoglobin falls below 10.0 g/dL.[2]Kidney Disease Improving Global Outcomes Anemia Work Group, “KDIGO 2026 Clinical Practice Guideline for the Management of Anemia in Chronic Kidney Disease,” Kidney International, kdigo.org Separate GBD 2021-based modeling showed 63.75 million CKD-related anemia cases globally and projected a further rise by 2035, with South and Southeast Asia, Central Europe, and Sub-Saharan Africa carrying a high age-standardized burden.

Expanding Chemotherapy-Induced Anemia Supportive Care Use

The erythropoietin drugs market also benefits from sustained use in chemotherapy-induced anemia, particularly in palliative care settings. The WHO noted that anemia affects 30% to 90% of patients receiving chemotherapy, depending on tumor type and treatment stage, supporting demand across oncology care pathways.[3]World Health Organization, “Chemotherapy-Induced Anemia: Application to the 25th WHO Expert Committee on Selection and Use of Essential Medicines,” WHO, who.int Current ASCO and ASH guidance supports ESAs for patients receiving non-curative chemotherapy when the treatment goal is to reduce transfusion need. A 2025 real-world study of Cresp, Dr. Reddy’s Laboratories’ darbepoetin alfa, found positive hemoglobin dynamics in 78.2% of 523 Indian patients on palliative chemotherapy, while oncology guidance also links intravenous iron use with better hematopoietic response when ESAs are prescribed.[4]Alaa El-Din Hassan et al., “Network Meta-Analysis of HIF-Prolyl Hydroxylase Inhibitors for Anemia in Dialysis-Dependent and Non-Dialysis CKD: Effects on Hemoglobin, Iron Markers, and Adverse Clinical Outcomes,” BMC Nephrology, springer.com

Biosimilar Penetration in Price-Sensitive Hospital Procurement

Biosimilars are reshaping growth in the erythropoietin drugs market across hospital and public tender channels. Their impact extends beyond price erosion, as lower-cost supply enables dialysis networks to adopt treatments that previously could not sustain originator pricing. This trend is especially important in emerging procurement systems, where constrained nephrology budgets and unit economics influence formulary decisions. India, South Korea, and China continue to strengthen glycoprotein manufacturing capabilities, improving supply reliability and supporting broader tender participation across Asia, Africa, and Latin America.

Long-Acting ESA Adoption in Dialysis and Renal Clinics

Long-acting agents are adding a premium growth layer to the erythropoietin drugs market, even as short-acting categories face pricing pressure. Mircera, methoxy polyethylene glycol-epoetin beta, supports dosing every two weeks or once monthly in adults with CKD, reducing administration burden in dialysis and renal clinics. China advanced this trend when the National Medical Products Administration (NMPA) approved 3SBio’s Loncipoetin Alfa Injection in March 2026, with a reported 120-hour half-life and biweekly dosing for hemodialysis patients already receiving EPO therapy. The UK Kidney Association’s 2025 update noted that long-acting ESAs may be preferred in some non-hemodialysis patients where subcutaneous dosing helps preserve vein access, while KDIGO 2026 keeps methoxy polyethylene glycol-epoetin beta within mainstream treatment algorithms for dialysis patients.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Safety concerns and conservative hemoglobin targeting | -1.2% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Pricing erosion from biosimilar competition | -1.5% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Complex cold-chain and biologics manufacturing requirements | -0.8% | Middle East and Africa, South America, and Southeast Asia | Medium term (2-4 years) |

| Substitution pressure from HIF-PHI and other non-ESA alternatives | -1.0% | Europe, Japan, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns and Conservative Hemoglobin Targeting

Safety guidance continues to limit dosing intensity in the erythropoietin drugs market. KDIGO 2026 is expected to recommend against targeting hemoglobin levels above 11.5 g/dL in erythropoiesis-stimulating agent (ESA)-maintained patients due to risks such as stroke, thromboembolism, and hypertension. This limits dose escalation and moderates volume upside from the rising chronic kidney disease population, while oncology use remains restricted to non-curative settings due to survival and tumor progression concerns. The UK Kidney Association also recommends clinical review for ESA hyporesponsiveness instead of repeated dose escalation, further limiting per-patient spending.

Substitution Pressure From HIF-PHI and Other Non-ESA Alternatives

Oral hypoxia-inducible factor prolyl hydroxylase inhibitor (HIF-PHI) products remain the most direct substitution pressure in the erythropoietin drugs market. A 2025 network meta-analysis in BMC Nephrology is expected to position roxadustat and daprodustat among the strongest agents for hemoglobin improvement and highlight daprodustat’s benefits on iron indices. These products reduce dependence on injections and cold-chain logistics, offering operational advantages in selected care pathways. However, KDIGO 2026 is expected to continue recommending ESAs before HIF-PHIs due to limited superior safety evidence and uneven regulatory acceptance, keeping substitution risk higher in China and parts of Europe than in markets with stronger ESA-first practice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Biosimilar Expansion Changes the Revenue Mix

Biologics are expected to hold 58.34% of the erythropoietin drugs market share in 2025, supported by strong formulary positions for originator brands such as Epogen, Aranesp, NeoRecormon, and Mircera across developed healthcare systems. Their position reflects physician familiarity, established hospital and dialysis procurement patterns, and demand for treatment continuity in chronic anemia care. Biosimilars are the fastest-growing type and are projected to expand at a CAGR of 14.53% through 2031, driven by lower costs and improved access to erythropoiesis-stimulating agents (ESAs). India, South Korea, and China are central to this shift as manufacturers scale complex biologics production and expand exports, gradually shifting share from originators to biosimilars without reducing the treatment base.

By Product: Longer Dosing Intervals Support Product Differentiation

Epoetin alfa is expected to account for 35.45% of the erythropoietin drugs market in 2025, maintaining its position as the largest product category by revenue due to broad formulary access and sustained use across dialysis networks, hospitals, and oncology settings. Epoetin beta and methoxy polyethylene glycol-epoetin beta remain important adjacent categories across Europe, Japan, and chronic kidney disease (CKD) maintenance therapy, while Mircera continues to benefit from monthly maintenance dosing. The erythropoietin drugs market size for darbepoetin alfa is projected to grow at a CAGR of 13.67% through 2031, supported by weekly to biweekly dosing and use across multiple indications. Other products, including novel glycoengineered variants such as Loncipoetin Alfa from 3SBio, are expected to strengthen the premium long-acting tier, supported by adherence benefits and lower dosing frequency following its March 2026 approval in China.

By Application: Kidney Disease Remains the Core Demand Base

Kidney diseases are expected to represent a 43.24% share in 2025, making them the largest application in the erythropoietin drugs market due to the strong clinical link between CKD progression and anemia burden, especially among dialysis-dependent patients. KDIGO noted that anemia prevalence rises sharply as kidney function worsens and becomes very common in stage G5, while its guidance supports ESA initiation in CKD G5D patients when hemoglobin falls to 9.0 to 10.0 g/dL. Cancer is projected to record the fastest application growth at a CAGR of 12.35% through 2031, although treatment intent and safety considerations continue to shape adoption. WHO did not support expanded essential medicines coverage for chemotherapy-induced anemia, while ASCO and ASH continue to support ESA use in non-curative chemotherapy when reducing transfusion needs is clinically important; neurology remains limited, and perioperative anemia may gain relevance as hospital blood management protocols expand.

By End User: Care Delivery Is Gradually Moving Beyond Hospitals

Hospitals are expected to capture a 48.67% share in 2025, making them the leading end-user group in the erythropoietin drugs market due to integrated nephrology and oncology services, established monitoring, and specialist-led dose management. Dialysis centers remain the next major channel as they concentrate recurring anemia care and negotiate supplier contracts at scale, while specialty clinics bridge inpatient care and outpatient anemia management. The erythropoietin drugs market size for home care settings is projected to grow at a CAGR of 14.67% through 2031, making it the fastest-growing end-user channel. KDIGO 2026 supports this shift by recommending subcutaneous administration for non-hemodialysis CKD patients and CKD G5PD patients, strengthening self-administration pathways while keeping hospitals involved in broader care oversight.

Geography Analysis

North America held 39.86% of the erythropoietin drugs market share in 2025, maintaining its position as the largest regional contributor. The region benefits from dense dialysis infrastructure, broad reimbursement coverage, and established use of erythropoiesis-stimulating agents (ESAs) across nephrology and oncology care. The United States remains the anchor market, where originator products and biosimilars compete within a mature treatment framework, while Canada and Mexico add incremental demand shaped by public procurement and reimbursement design.

Europe and Asia-Pacific define the next phase of competition in the erythropoietin drugs market. Europe remains supported by aging populations, structured disease management, and long-standing use of originator and biosimilar ESAs, with the United Kingdom, Germany, and France remaining key markets due to established renal care pathways and protocol-driven anemia management. The UK Kidney Association’s 2025 update maintained ESAs as first-line therapy and positioned hypoxia-inducible factor prolyl hydroxylase inhibitors (HIF-PHIs) as an additional option rather than a full replacement, helping preserve ESA demand in the near term. Asia-Pacific is the fastest-growing region and is forecast to advance at a 14.56% CAGR through 2031, supported by China’s dialysis expansion, India’s biosimilar supply strength, and wider anemia management efforts across developing healthcare systems. In China, 3SBio reported a 39.6% share of the domestic recombinant human erythropoietin (rhEPO) market in 2025 through its Yibiao and Epiao brands, and its March 2026 long-acting approval adds a premium layer to that franchise.

The Middle East and Africa and South America offer uneven but meaningful expansion opportunities across the erythropoietin drugs market. Demand fundamentals remain strong in these regions because chronic kidney disease burden is high and anemia treatment access remains below clinical need in many countries. North Africa and the Middle East recorded the highest age-standardized chronic kidney disease prevalence globally at 18.0%, indicating long-term demand potential even where infrastructure gaps slow immediate uptake.

Competitive Landscape

The erythropoietin drugs market has a moderately fragmented structure, with a few originator companies retaining strong brand positions while a broader group of biosimilar suppliers intensifies pricing pressure. Amgen, F. Hoffmann-La Roche, and Johnson & Johnson remain prominent as their products are deeply integrated into established treatment pathways and high-income formularies. These companies hold stronger positions where physician familiarity, outcomes history, and institutional procurement relationships outweigh unit price considerations. Indian, Chinese, and Korean manufacturers continue to expand the competitive landscape by supplying lower-cost alternatives across domestic and export channels, making the market more competitive while sustaining demand for premium long-acting brands.

Companies are prioritizing product differentiation instead of relying only on price defense. Roche’s long-acting Mircera continues to retain value as its lower dosing frequency supports clinic workflow efficiency and reduces patient burden. 3SBio’s March 2026 approval of Loncipoetin Alfa in China would strengthen its position beyond standard recombinant human erythropoietin (rhEPO) supply, supported by a 120-hour half-life and biweekly dosing profile. The company also reported 2025 revenue of RMB 17.7 billion (USD 2.4 billion) and R&D investment of RMB 1.52 billion (USD 206.1 million), indicating that regional leaders are using cash flow from established erythropoiesis-stimulating agent (ESA) franchises to fund the next phase of differentiation. Sandoz has adopted a partnership-led approach, with Samsung Bioepis announcing a March 2026 agreement covering up to five next-generation biosimilar candidates to support scale in global biologics competition.

Competitive pressure in the erythropoietin drugs market is coming from two directions: lower-cost biosimilar expansion and higher-value long-acting innovation. Public tenders in emerging markets favor suppliers that can combine competitive pricing with reliable manufacturing and pharmacovigilance support. Developed markets remain more stable, but purchasing decisions increasingly factor in administration efficiency and total cost of care. The strongest near-term opportunities are likely to emerge in long-acting formulations, home administration support, and underpenetrated renal care systems where patient access has not yet aligned with clinical need.

Erythropoietin Drugs Industry Leaders

Amgen Inc.

F. Hoffmann-La Roche Ltd.

Johnson & Johnson

Pfizer Inc.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: 3SBio reported 2025 revenue of RMB 17.7 billion (USD 2.4 billion), up 94.3% year over year, and held a 39.6% share of Mainland China’s rhEPO market.

- March 2026: China’s NMPA approved Loncipoetin Alfa Injection, NuPIAO, as the country’s first domestic Class 1 innovative long-acting recombinant EPO biweekly formulation for eligible hemodialysis patients.

- March 2026: Samsung Bioepis and Sandoz entered a global agreement to license, develop, and commercialize up to five next-generation biosimilar candidates.

- January 2026: KDIGO issued its 2026 anemia in chronic kidney disease guideline, reaffirming ESAs as first-line treatment over HIF-PHIs and setting hemoglobin target ceilings at 11.5 g/dL.

- April 2025: Huons Group increased its stake in PanGen Biotech to 36.7%, deepening integration of PanGen’s EPO biosimilar manufacturing and CDMO capabilities.

Global Erythropoietin Drugs Market Report Scope

As per the scope of the report, Erythropoietin (EPO) is a glycoprotein hormone primarily produced by the kidneys that stimulates the bone marrow to produce red blood cells. The synthesized or recombinant form (rhEPO) is a prescription medication used to treat anemia associated with chronic kidney disease, chemotherapy, and HIV treatments, and to reduce the need for blood transfusions during high-risk surgeries.

The erythropoietin drugs market is segmented by type, product, application, end user, and geography. By type, the market includes biologics and biosimilars. By product, the market is segmented into epoetin alfa, epoetin beta, darbepoetin alfa, methoxy polyethylene glycol-epoetin beta, and other erythropoietin products. By application, the market is categorized into kidney diseases, cancer, neurology, and other applications. By end user, the market is segmented into hospitals, dialysis centers, specialty clinics, home care settings, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Biologics |

| Biosimilars |

| Epoetin Alfa |

| Epoetin Beta |

| Darbepoetin Alfa |

| Methoxy Polyethylene Glycol-Epoetin Beta |

| Other Erythropoietin Products |

| Kidney Diseses |

| Cancer |

| Neurology |

| Other Applications |

| Hospitals |

| Dialysis Centers |

| Specialty Clinics |

| Home Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Biologics | |

| Biosimilars | ||

| By Product | Epoetin Alfa | |

| Epoetin Beta | ||

| Darbepoetin Alfa | ||

| Methoxy Polyethylene Glycol-Epoetin Beta | ||

| Other Erythropoietin Products | ||

| By Application | Kidney Diseses | |

| Cancer | ||

| Neurology | ||

| Other Applications | ||

| By End User | Hospitals | |

| Dialysis Centers | ||

| Specialty Clinics | ||

| Home Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the erythropoietin drugs space in 2026?

The erythropoietin drugs market size stands at USD 21.02 billion in 2026 and is forecast to reach USD 36.48 billion by 2031 at an 11.65% CAGR.

What is driving demand for erythropoietin therapies the most?

The largest demand driver is the rising burden of chronic kidney disease and related anemia, supported by 788 million adults living with chronic kidney disease in 2025.

Which product group is growing the fastest through 2031?

Biosimilars are the fastest-growing type at 14.53% CAGR, while darbepoetin alfa is the fastest-growing product at 13.67% CAGR through 2031.

Why does kidney disease remain the largest application area?

Kidney diseases held 43.24% share in 2025 because anemia becomes very common as chronic kidney disease progresses, especially in dialysis-dependent patients.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to record the fastest regional expansion at 14.56% CAGR through 2031, supported by China's dialysis growth and Asia's biosimilar manufacturing base.

How is competition changing in this space?

Competition is shifting in 2 directions, lower-cost biosimilar expansion and higher-value long-acting products, with companies such as 3SBio and Sandoz using product development and partnerships to strengthen position.

Page last updated on: