Adalimumab Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 15.72 Billion |

| Market Size (2031) | USD 20.09 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

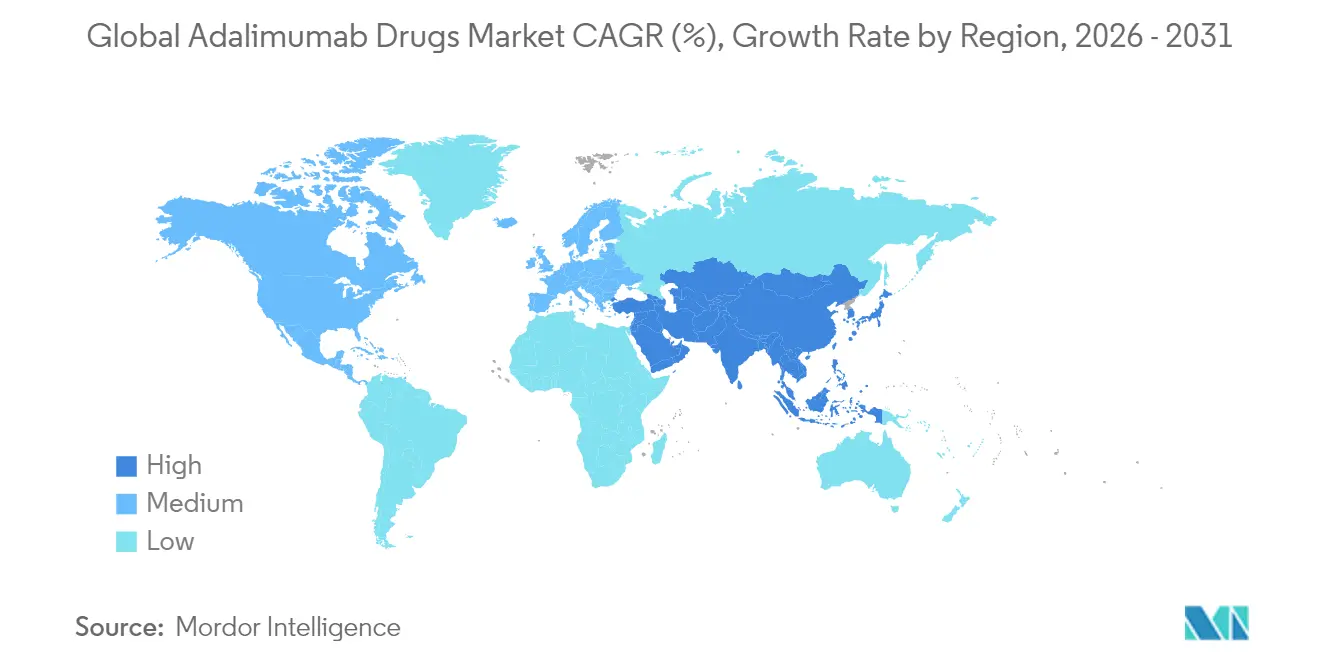

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adalimumab Drugs Market Analysis by Mordor Intelligence

The adalimumab market size was valued at USD 14.96 billion in 2025 and estimated to grow from USD 15.72 billion in 2026 to reach USD 20.09 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). Strong clinical demand across autoimmune disorders, rapid biosimilar penetration after Humira’s loss of exclusivity, and continuous device innovation jointly sustain revenue momentum. North America commands cost-intensive specialty-pharmacy networks that protect premium pricing even as payers accelerate formulary switches, while Asia-Pacific registers the quickest uptake on the back of government tender reforms that widen biologic access. Intensifying competition among 10-plus FDA-approved biosimilars is compressing list prices by as much as 80%, yet high-concentration, citrate-free formulations preserve value differentiation. Pipeline diversification into IL-23 inhibitors such as Skyrizi and Janus kinase inhibitors like Rinvoq reveals originator defensive strategy rather than market withdrawal, ensuring the adalimumab market retains commercial vibrancy. Specialty-pharmacy integration with digital adherence platforms, coupled with emerging outcomes-based contracts, further raises switching incentives and reshapes stakeholder economics.

Key Report Takeaways

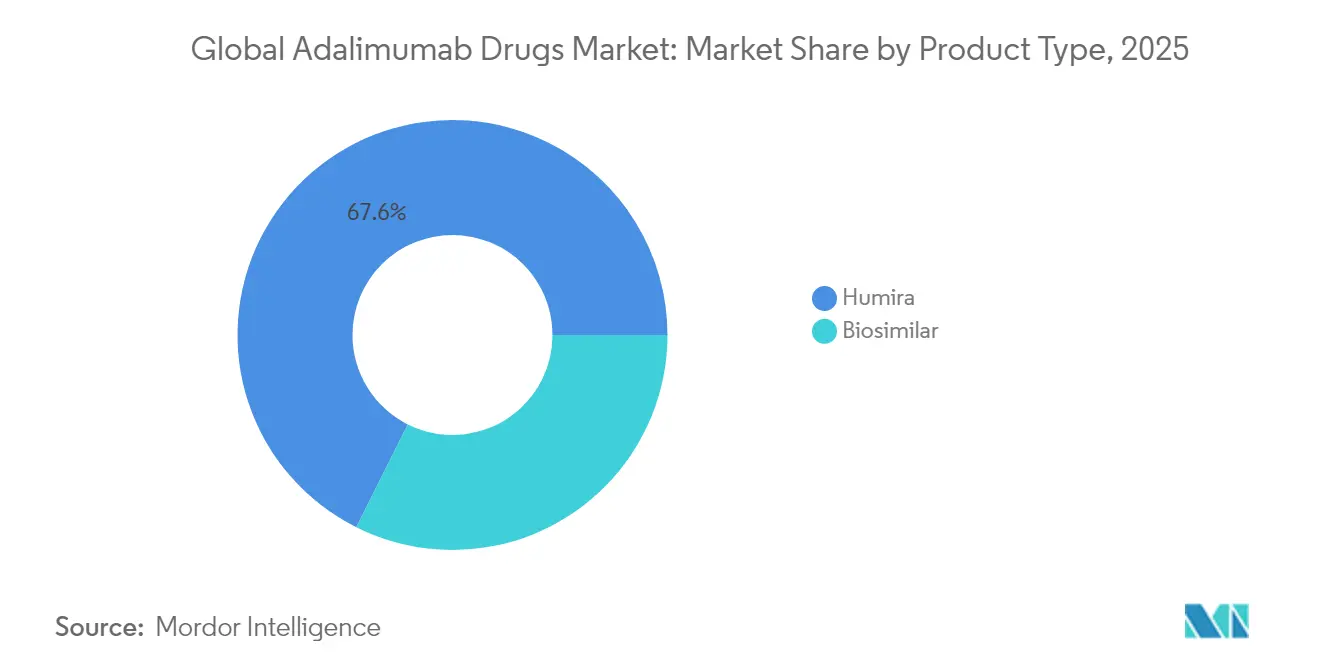

- By product type, Humira sustained 67.62% of adalimumab market share in 2025, whereas biosimilars are expanding at a 5.62% CAGR through 2031.

- By indication, rheumatoid arthritis led with 37.88% revenue share in 2025, while hidradenitis suppurativa is projected to advance at a 5.86% CAGR to 2031.

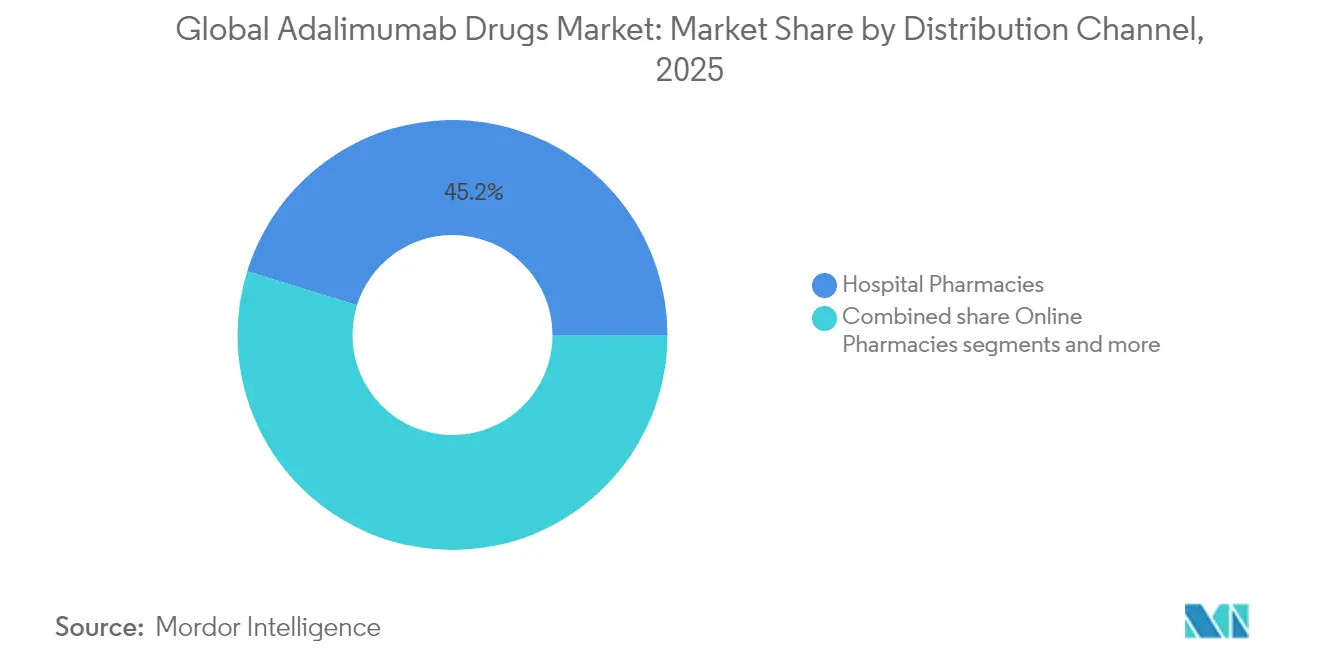

- By distribution channel, hospital pharmacies controlled 45.21% of the adalimumab market size in 2025, whereas online pharmacies display the fastest trajectory at a 6.05% CAGR over the forecast horizon.

- By geography, North America captured 55.64% revenue share in 2025, while Asia-Pacific is expected to post the quickest expansion at a 5.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adalimumab Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Loss of Humira exclusivity spurring biosimilar launches | +1.8% | Global, with North America and Europe leading | Short term (≤ 2 years) |

| Escalating global autoimmune disease prevalence | +1.2% | Global, with higher impact in aging populations | Long term (≥ 4 years) |

| Increasing specialty-pharmacy penetration in the U.S. | +0.9% | North America, spill-over to developed markets | Medium term (2-4 years) |

| Patient-friendly autoinjector upgrades enhancing adherence | +0.7% | Global, with premium markets leading adoption | Medium term (2-4 years) |

| Value-based contracting gaining traction in Europe | +0.5% | Europe, with expansion to other developed markets | Medium term (2-4 years) |

| Government tender reforms in Asia-Pacific boosting biosimilar uptake | +0.3% | Asia-Pacific core, with regulatory spillover effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Loss of Humira Exclusivity Spurring Biosimilar Launches

A synchronized wave of FDA approvals has placed 10+ biosimilars on U.S. shelves within eighteen months of Humira’s patent cliff, cutting pre-rebate prices by up to 80% and tripling prescription volume for preferred biosimilars under major PBMs. Updated interchangeability guidance issued in June 2024 shaved 18-24 months off development cycles, reducing capital requirements and lowering entry barriers. Simlandi secured first-to-market interchangeability for the high-concentration 40 mg/0.4 mL strength that covers 88% of U.S. dispenses, briefly restoring pricing leverage for its sponsors. Nevertheless, subsequent designations for Yuflyma and Hyrimoz eliminated this exclusivity buffer inside twelve months, intensifying price erosion. Parallel direct-purchase models—exemplified by Blue Shield of California’s USD 525 monthly dose agreement—demonstrate purchaser appetite for bypassing PBM spreads.

Escalating Global Autoimmune Disease Prevalence

The global rheumatoid arthritis population is adding 2-3% annually, psoriasis cases have climbed 15% since 2020, and inflammatory bowel disease diagnoses in developing economies are rising by 5-7% per year. Increased disease surveillance, improved diagnostic imaging, and longer life expectancy collectively expand biologic-eligible cohorts. Long-term registries reveal 40-50% mortality reduction when TNF-α inhibitors are initiated early, reinforcing first-line biologic placement in treatment guidelines. Asia-Pacific’s underdiagnosed patient pool is transitioning into treated prevalence as reimbursement reforms fund specialty care, unlocking substantive volume growth. Emerging indications such as non-infectious uveitis and juvenile idiopathic arthritis further widen usage scenarios, sustaining addressable demand despite competitive biologic classes.

Increasing Specialty-Pharmacy Penetration in the U.S.

Specialty channels processed roughly 70% of adalimumab prescriptions in 2025, up from 50% in 2023, reflecting payer drive toward tighter clinical oversight and better cost capture. Enhanced patient support services—encompassing injection training, adherence analytics, and adverse-event triage—push 12-month persistence rates to 85-90%, significantly above retail baseline. Home-delivery volumes have surged 40% since 2024, aligning with telehealth expansion and supporting home-based disease management. Outcomes-based contracts, in which pharmacy bonuses hinge on validated lab markers or hospitalization frequency, are now piloted by two of the top three PBMs. Such models incentivize timely switching to interchangeable biosimilars once high adherence is demonstrated, multiplying pressure on incumbent pricing.

Patient-Friendly Autoinjector Upgrades Enhancing Adherence

Device designers have introduced large-volume autoinjectors capable of delivering 5.5 mL high-viscosity solutions without patient discomfort. Citrate-free formulations cut injection-site pain scores by 30-40%, a meaningful determinant of real-world persistence. Bluetooth-enabled or cellular-connected devices integrate seamlessly with disease-management apps, giving clinicians real-time adherence dashboards. Electromechanical reusable platforms reach 90%+ fulfillment over twelve months versus 75% for disposable syringes, according to cross-indication surveys. These enhancements not only buttress patient satisfaction but also strengthen payer confidence in switching stable patients to lower-cost biosimilars fitted with premium delivery systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of biologics in low-income markets | -0.8% | Emerging markets, particularly Sub-Saharan Africa and Southeast Asia | Long term (≥ 4 years) |

| Interchangeability hurdles for biosimilars in the U.S. | -0.6% | North America, with regulatory spillover to other markets | Short term (≤ 2 years) |

| Cold-chain bottlenecks in emerging markets | -0.4% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Physician reluctance to switch stable patients in Asia-Pacific | -0.3% | Asia-Pacific core, with cultural factors influencing adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing in Low-Income Markets

In many developing economies a single monthly adalimumab dose exceeds the average household income, leading to treatment discontinuation or complete non-initiation. Government drug budgets allocate under 5% to specialty pharmaceuticals, restricting coverage to a fraction of clinically eligible patients. Biosimilar manufacturing locally has yet to unlock meaningful discounts, with compliance overheads keeping unit costs at 60-70% of originator levels. Parallel import risks deter tiered-pricing schemes that could otherwise broaden affordability. Without structured health technology assessment pathways, reimbursement committees struggle to justify budget diversion toward biologics, elongating access latency and flattening uptake curves.

Cold-Chain Bottlenecks in Emerging Markets

Temperature excursions above 8 °C affect 25-40% of biologic shipments in tropical climates, resulting in product wastage that inflates effective therapy costs. Intermittent electricity grids and limited refrigerated trucking capacity hamper consistent supply, especially in remote provinces. Cold-chain logistics add USD 200-500 per shipment in emerging Asia compared with USD 50-100 in developed nations, squeezing distributor margins. Less than 30% of peripheral health facilities possess validated temperature monitoring, breaching WHO storage mandates. These inefficiencies discourage wholesalers from stocking biologics, curtailing availability outside major urban centers and dampening regional demand trajectories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biosimilars Accelerate Market Realignment

Biosimilars captured escalating volume yet Humira still held 67.62% adalimumab market share in 2025 thanks to entrenched physician preference programs and copay assistance. The vigorous 5.62% CAGR projected for biosimilars illustrates payer leverage following interchangeable approvals that authorize pharmacy-level substitution without prescriber intervention. Competitive focus centers on high-concentration, citrate-free formulations, the presentation that accounts for nearly nine in every ten U.S. injections. Simlandi’s initial exclusivity window temporarily raised its net realized price, but follow-on entrants such as Yuflyma quickly nullified this premium, reinstating downward pricing momentum. Quallent Pharmaceuticals’ private-label platform aggregates multisource supply, enabling employers to procure unbranded adalimumab at less than one-quarter of Humira’s 2023 net price. On a global scale, unbranded biosimilars already account for 15-20% of adalimumab market size in large-payer tenders, signaling an irreversible commoditization trend.

Manufacturers pursue differentiation via device ecosystems and wrap-around patient services rather than molecular variance. Electromechanical reusable autoinjectors bundled with digital adherence monitoring offer tangible clinical benefits that justify modest price premiums over discount biosimilars lacking such integrations. AbbVie’s strategic pivot toward novel mechanisms—most visibly IL-23 blockade with Skyrizi and JAK1 selectivity with Rinvoq—aims to protect franchise earnings as adalimumab revenue slides. Despite pipeline promise, cross-indication uptake of next-generation assets partially cannibalizes Humira demand, amplifying biosimilar growth headroom. Regulatory shifts that shorten approval timelines by nearly two years further embolden new entrants, ensuring sustained competitive churn through 2031.

By Indication: Rheumatoid Arthritis Leads; Hidradenitis Suppurativa Surges

Rheumatoid arthritis absorbed 37.88% of 2025 revenue, a share grounded in well-validated clinical algorithms that schedule TNF-α inhibition early in the treatment cascade. Nevertheless, selective JAK inhibitors and IL-6 modulators are gradually displacing adalimumab in newly diagnosed patients, tempering the segment’s forward trajectory. Hidradenitis suppurativa emerges as the quickest climber, propelled by 5.86% CAGR through 2031 on heightened clinician awareness and the absence of biologic alternatives with comparable efficacy. Psoriatic arthritis and ankylosing spondylitis maintain steady mid-single-digit expansion, leveraging improved imaging modalities that accelerate accurate diagnosis. Inflammatory bowel disease segments experience mixed fortunes: Crohn’s disease persists given surgical deferral advantages, whereas ulcerative colitis sees margin pressure from tighter guideline positioning that promotes vedolizumab and ustekinumab.

Plaque psoriasis, once a core growth engine, now contends with superior skin-clearance benchmarks from IL-17 and IL-23 targeted biologics that erode adalimumab prescription share. Juvenile idiopathic arthritis and uveitis remain niche yet stable, constrained by pediatric safety considerations that slow biosimilar penetration. The progressive shift toward rarer dermatologic and ophthalmologic indications heightens pricing flexibility due to limited therapeutic competition. Consequently, pharmaceutical marketers prioritize label-expansion programs into under-served diseases to offset mainstream erosion and defend overall adalimumab market size against next-generation classes.

By Distribution Channel: Digital Dispensing Redefines Access Models

Hospital pharmacies retained 45.21% adalimumab market size in 2025 courtesy of embedded infusion services and integrated disease-management teams. Yet online and mail-order channels are scaling fastest, with 6.05% CAGR forecast as patients gravitate toward home delivery and virtual consultation packages. Retail outlets increasingly partner with specialty-pharmacy banners to safeguard relevance, outsourcing high-touch clinical services they cannot economically replicate. Digital therapeutics now plug directly into dispensing workflows, streaming adherence and symptom data back to prescribers, which in turn enables dynamic therapy adjustments without physical appointments.

Manufacturers have embraced omnichannel engagement by bundling nurse coaching, mobile injection reminders, and refill coordination into single-click platforms. These value-added services, financed partly through outcomes-based contracts, elevate patient satisfaction metrics to 90% versus 75% in conventional brick-and-mortar pickup. Regulators encourage such innovation under combination-product guidance that clarifies quality requirements for drug-device-software ensembles. The distribution landscape therefore migrates toward a hybrid model where hospital settings manage initiation and complex cases, while chronic maintenance doses flow through digitally optimized direct-to-patient logistics.

Geography Analysis

North America generated 55.64% of 2025 revenue and remains the axis of competitive disruption owing to payer-driven biosimilar substitution rules. Four biosimilars now hold interchangeability status, introducing automatic pharmacy-level substitution and compressing brand loyalty cycles. Specialty-pharmacy proliferation ensures robust cold-chain stewardship and real-time clinical monitoring, supporting continued high biologic utilization despite intensified price negotiations. Yet transparency mandates and state-level reference-pricing bills apply incremental pressure on net-price realization, prompting manufacturers to refine contracting tactics around documented outcome guarantees.

Europe adopts sophisticated value-based arrangements, with health technology assessment agencies tying reimbursement to dermatology severity scale improvements or rheumatology composite scores. Tender-driven procurement has pushed biosimilar penetration above 25% in Germany, the Netherlands, and France, while Italy and Spain lag due to slower formulary updates. Physician reluctance to switch stable patients persists, though national switching mandates in Scandinavian states display adherence rates exceeding 85% within twelve months of policy enactment. Centralized regulatory reviews under the EMA’s streamlined biosimilar pathway now permit dossier acceptance in as little as 150 days, shaving roughly one year off historic timelines.

Asia-Pacific records the highest regional growth at a 5.71% CAGR, fueled by rising middle-class insurance coverage and public tender reforms that favor domestically produced biosimilars. China’s volume-based procurement rounds have slashed adalimumab prices by upward of 75%, igniting demand elasticity that offsets unit margin contraction. Japan’s super-aged demographic underpins consistent baseline use, while Australia’s Pharmaceutical Benefits Scheme guarantees predictable reimbursement cycles attractive to multinational suppliers. India exemplifies a dual-track market: urban tertiary centers exhibit adoption rates approaching OECD averages, whereas rural districts remain supply constrained by inadequate cold-chain infrastructure. Across Southeast Asia, coordinated ASEAN regulatory convergence aims to fast-track biosimilar approvals, potentially aligning national reviews within a two-year window and magnifying regional demand uplift.

Competitive Landscape

The adalimumab market operates at moderate concentration: AbbVie retains the largest individual stake but the top five suppliers collectively hold significant share, reflecting a dispersed yet structured oligopoly. AbbVie’s strategy pivots on rapid revenue migration to Skyrizi and Rinvoq, shielding corporate earnings from Humira attrition. Biosimilar contenders—Teva/Alvotech, Celltrion, Boehringer Ingelheim, Sandoz, Viatris, Fresenius Kabi—deploy tiered pricing, private-label alliances, and device differentiation to carve niches. Pharmacy benefit managers exercise unprecedented leverage, structuring formularies that prioritize lowest-net-cost offerings and sometimes delist originator Humira altogether.

Technological arms races now complement pricing skirmishes. Connected autoinjectors, reusable electromechanical devices, and on-body delivery systems such as enFuse are central to next-phase messaging that transcends molecular sameness. Manufacturers back these tools with real-time dashboards, generating de-identified adherence datasets that bolster cost-effectiveness dossiers. Regional manufacturing partnerships—exemplified by Fresenius Kabi’s tie-ups with Korean CDMOs—shorten supply chains and insulate logistics risk. Meanwhile, venture-backed entrants explore high-concentration ultra-low-volume formulations aimed at five-second injections, a potential disruptor of established device hierarchies. The competitive field is thus defined less by patent status and more by executional agility across manufacturing, digital health integration, and payer contracting sophistication.

Adalimumab Drugs Industry Leaders

AbbVie Inc

Amgen Inc

Cadila Healthcare Ltd

Hetero Healthcare Limited

Pfizer Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: FDA granted Yuflyma (adalimumab-aaty) interchangeable status, marking the fourth biosimilar eligible for pharmacy substitution and compressing Humira’s remaining U.S. exclusivity.

- October 2024: Bio-Thera and Gedeon Richter closed a USD 110 million commercialization deal for a Stelara biosimilar, signaling geographic diversification beyond adalimumab while leveraging shared distribution platforms

Global Adalimumab Drugs Market Report Scope

As per the scope of the report, Adalimumab, which is a patent product of Abbott, is a medication used for the treatment of ulcerative colitis, psoriatic arthritis, and rheumatoid arthritis. It is also known as HUMIRA, intended to inject subcutaneously. It can help in preventing conditions causing damage to the body. Adalimumab drug market is segmented by disease type and geography. The Adalimumab Drugs Market is Segmented By Disease Type (Rheumatoid Arthritis, Psoriatic Arthritis, Crohn's Disease, Ulcerative Colitis, Others) and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Biologics (Humira) |

| Biosimilars |

| Rheumatoid Arthritis |

| Psoriatic Arthritis |

| Ankylosing Spondylitis |

| Crohn’s Disease |

| Ulcerative Colitis |

| Plaque Psoriasis |

| Hidradenitis Suppurativa |

| Juvenile Idiopathic Arthritis |

| Uveitis |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Biologics (Humira) | |

| Biosimilars | ||

| By Indication | Rheumatoid Arthritis | |

| Psoriatic Arthritis | ||

| Ankylosing Spondylitis | ||

| Crohn’s Disease | ||

| Ulcerative Colitis | ||

| Plaque Psoriasis | ||

| Hidradenitis Suppurativa | ||

| Juvenile Idiopathic Arthritis | ||

| Uveitis | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Global Adalimumab Drugs Market size?

The Global Adalimumab Drugs Market is projected to register a CAGR of 5.05% during the forecast period (2026-2031)

Who are the key players in Global Adalimumab Drugs Market?

AbbVie Inc, Amgen Inc, Cadila Healthcare Ltd, Hetero Healthcare Limited and Pfizer Inc are the major companies operating in the Global Adalimumab Drugs Market.

Which is the fastest growing region in Global Adalimumab Drugs Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Adalimumab Drugs Market?

In 2025, the North America accounts for the largest market share in Global Adalimumab Drugs Market.

What years does this Global Adalimumab Drugs Market cover?

The report covers the Global Adalimumab Drugs Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Global Adalimumab Drugs Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: