Catheter Introducer Sheaths Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

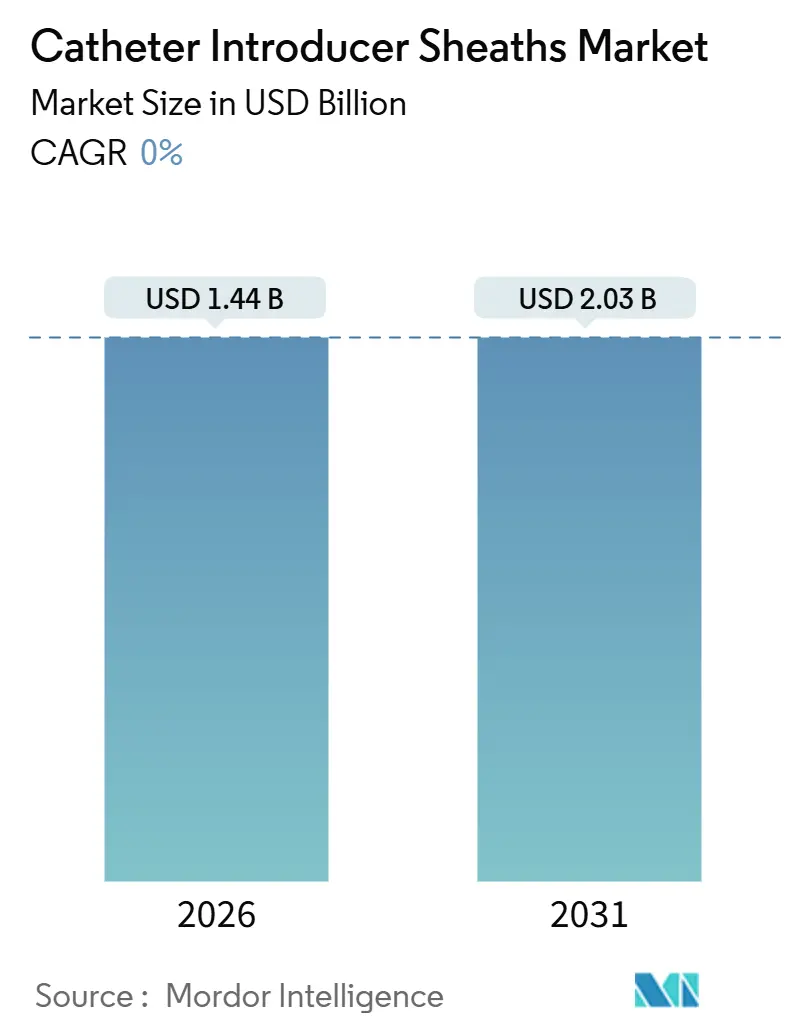

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 0.00% CAGR |

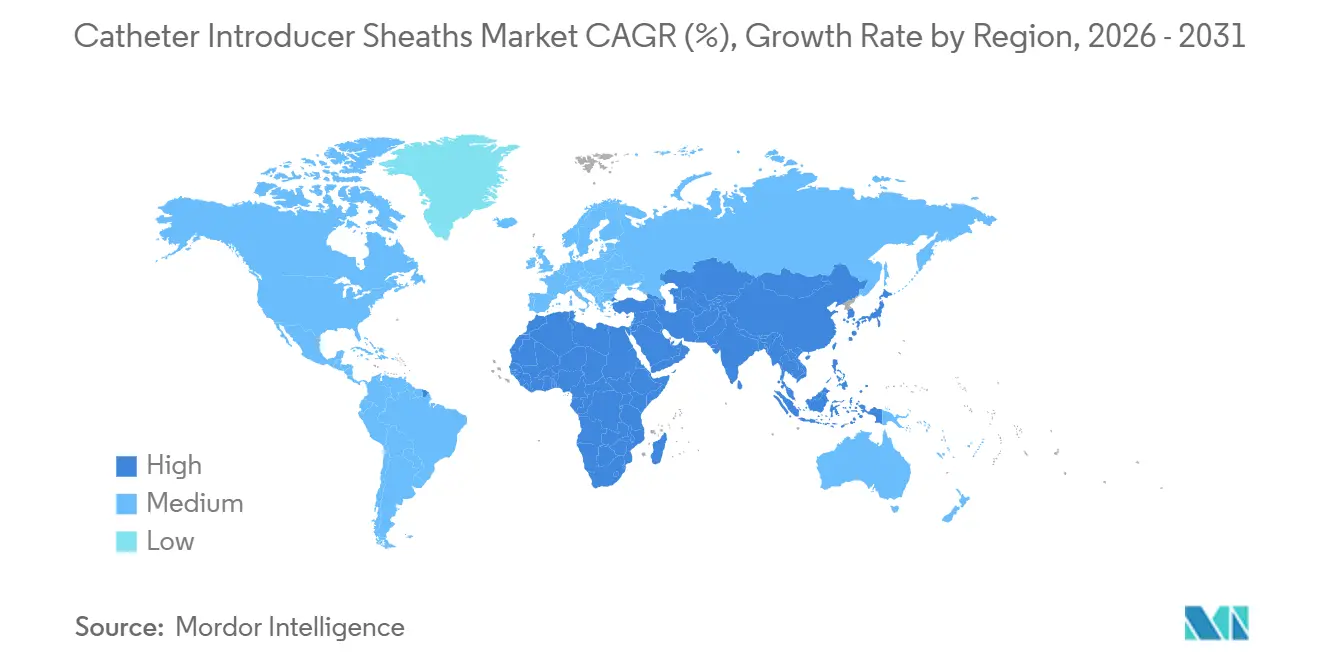

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

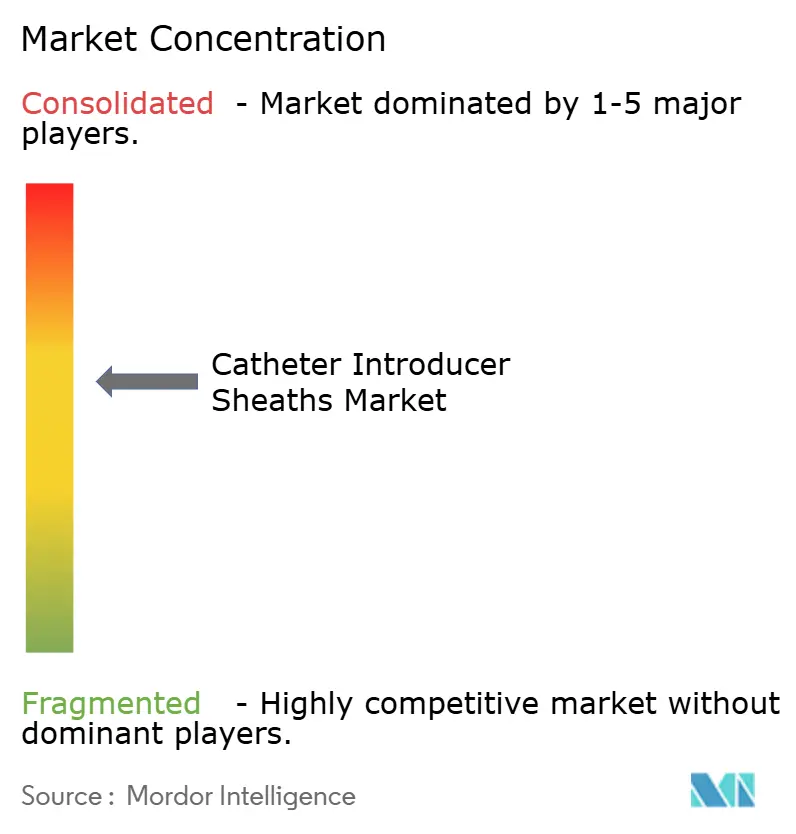

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Catheter Introducer Sheaths Market Analysis by Mordor Intelligence

The Catheter Introducer Sheaths Market size is estimated at USD 1.44 billion in 2026, and is expected to reach USD 2.03 billion by 2031, at a CAGR of 0% during the forecast period (2026-2031).

The expansion reflects sustained growth in percutaneous cardiovascular and neurovascular procedures, continued migration toward radial access, and steady material innovation in Pebax- and drug-eluting-based designs. Demand also mirrors the rising global cardiovascular disease burden, which created 19.8 million deaths in 2022. Hospitals, ambulatory surgical centers, and specialty clinics are standardizing thinner-profile, hydrophilic sheaths that limit arterial trauma, while manufacturers accelerate integrated sheath-catheter kits to improve procedural efficiency. Competitive intensity remains moderate because the top five companies control 55% of revenue, leaving room for nimble regional suppliers to win group-purchasing contracts.

Key Report Takeaways

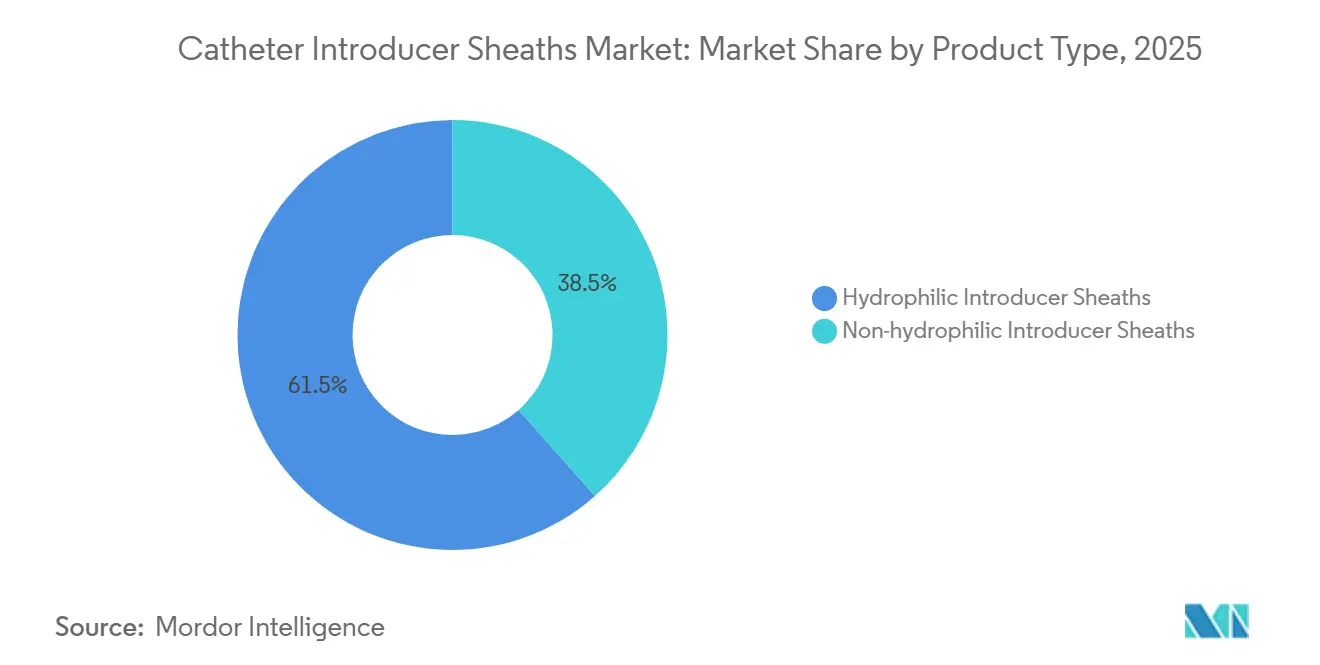

- By product type, hydrophilic sheaths led with 61.53% of the catheter introducer sheaths market share in 2025; non-hydrophilic counterparts are projected to expand at a slower 7% CAGR through 2031.

- By material, polyurethane accounted for 41.52% of the catheter introducer sheaths market size in 2025, whereas Pebax is advancing at a 10.78% CAGR to 2031.

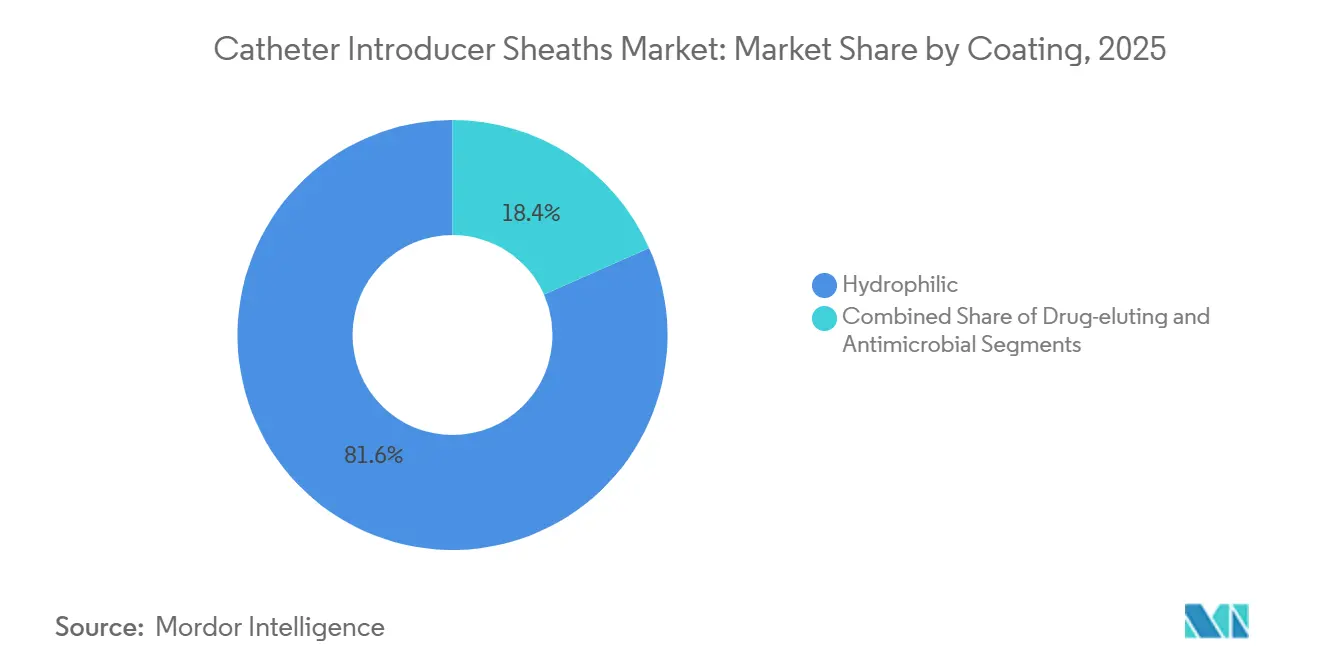

- By coating, hydrophilic layers covered 81.63% of demand in 2025, while drug-eluting coatings post the fastest 11.74% CAGR over the forecast window.

- By application, interventional cardiology dominated with 53.75% volume in 2025; neurovascular procedures are pacing growth with a 10.52% CAGR.

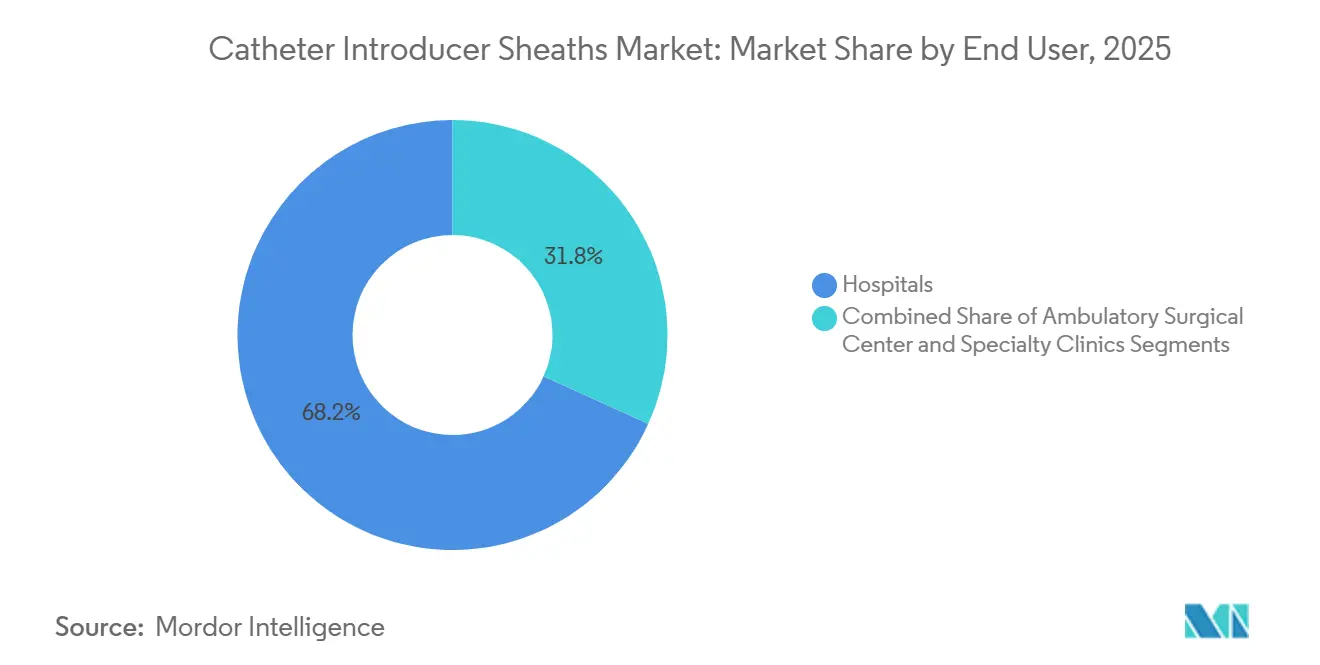

- By end user, hospitals captured 68.22% revenue in 2025, and ambulatory surgical centers are rising at a 9.46% CAGR on shifting lower-complexity work to outpatient settings.

- By geography, North America held 41.43% share of the catheter introducer sheaths market size in 2025, whereas Asia-Pacific is accelerating at a 9.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Catheter Introducer Sheaths Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Cardiovascular Diseases | +1.8% | Global, acute in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing Adoption of Minimally-Invasive Procedures | +1.5% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Technological Advancements in Sheath Materials & Coatings | +1.3% | North America, Europe, advanced APAC markets | Medium term (2-4 years) |

| Shift Toward Radial Access in Neuro-Interventional Care | +1.2% | North America, Europe, urban APAC centers | Short term (≤ 2 years) |

| Integration of Embedded Sensors for Position Feedback | +0.9% | North America, select European markets | Medium term (2-4 years) |

| Hospital Preference for Sheath-Catheter Kits | +0.7% | Global, early uptake in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular Diseases

Cardiovascular disorders still top global mortality charts and create the bulk of catheter-based interventions.[1]WORLD HEALTH ORGANIZATION, “Cardiovascular Diseases (CVDs),” World Health Organization, who.int Aging populations in wealthier regions and increasing hypertension and diabetes in emerging economies are enlarging procedure pools. The United States alone logged 695,000 cardiac deaths in 2021, prompting guideline updates that endorse radial-first access for percutaneous coronary interventions. Every vascular procedure requires at least one sheath, so volume growth directly lifts the catheter introducer sheaths market. Updated 2025 American College of Cardiology recommendations further accelerate adoption of smaller, hydrophilic designs suited to radial anatomy.[2]AMERICAN COLLEGE OF CARDIOLOGY TASK FORCE, “2025 ACS Guidelines,” American College of Cardiology, acc.org Global conformance with ISO 10555-1 keeps baseline performance and biocompatibility standards consistent.

Growing Adoption of Minimally-Invasive Procedures

Minimally invasive strategies have eclipsed open surgery in most coronary and peripheral cases, as shorter recovery and lower complication rates persuade payers and clinicians.[3]SOCIETY FOR CARDIOVASCULAR ANGIOGRAPHY AND INTERVENTIONS, “Radial Access Adoption Trends,” Society for Cardiovascular Angiography and Interventions, scai.org Radial access in the United States climbed from 20% of percutaneous coronary interventions in 2013 to 58% by 2022, spurring thin-wall sheath demand. Terumo’s Glidesheath Slender, with its 0.025-inch wall and hydrophilic coat, shows how design advances let 6 French performance slip through a 5 French outer diameter. Peripheral artery disease guidelines released in 2024 advocate endovascular-first tactics, expanding use beyond coronary suites. Medicare’s data confirm momentum: outpatient peripheral angioplasty cases increased 12% year over year in 2024.

Technological Advancements in Sheath Materials & Coatings

Material science is reshaping everyday performance. Pebax blends polyether and polyamide blocks to deliver 30% lower flexural modulus than polyurethane without sacrificing tensile strength, giving superior kink resistance. Cook Medical bench tests recorded 40% lower insertion force for its Pebax-based Flexor Check-Flo device. Hydrophilic coatings that reduce friction coefficients below 0.05 cover 81.63% of units sold in 2025, while heparin-bonded drug-eluting layers are emerging to trim thrombotic events by 35% in preclinical research. Antimicrobial films incorporating silver or chlorhexidine help contol costly device-related infections estimated at USD 46,000 per incident.

Shift Toward Radial Access in Neuro-Interventional Care

Mechanical thrombectomy for acute stroke, historically femoral, is pivoting to distal radial entry. A 2024 Lancet Neurology study reported a 60% cut in access-site hematomas with radial versus femoral routes while maintaining time-to-reperfusion parity. Penumbra’s CAT 5 distal access catheter received FDA clearance in 2025 and captured 18% of U.S. comprehensive stroke centers in its first year. American Heart Association guidelines now rate radial access Class IIa, signaling institutional endorsement. Thrombectomy volumes exceeded 100,000 U.S. cases in 2024, and stroke incidence is on a 20% climb toward 2030. Resulting demand for highly trackable 5-6 French sheaths fuels the fastest application CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of Vascular Complications and Product Recalls | −0.9% | Global, heavy scrutiny in North America and Europe | Short term (≤ 2 years) |

| Stringent Regulatory Approval Timelines | −0.7% | Global, especially FDA and European MDR | Medium term (2-4 years) |

| Supply-Chain Disruptions for Pebax and PTFE Resins | −0.6% | Global, production concentrated in North America and Europe | Short term (≤ 2 years) |

| Competition From Sheath-Less Catheter Systems in Structural Heart Care | −0.5% | North America, Europe, early APAC adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Risk of Vascular Complications and Product Recalls

Access-site issues such as hematoma, pseudoaneurysm, and arterial dissection occur in up to 5% of procedures and dominate safety concerns. The FDA logged 12 Class II recalls of introducer sheaths between 2024 and 2025, citing coating delamination, valve leaks, and shaft fractures. Merit Medical pulled 14,000 Prelude Sync units in March 2024 after reports of sheath separation. Teleflex followed with an Arrow Radial recall in September 2024 for hydrophilic coat adhesion defects. Besides direct costs—often USD 5–10 million per incident—recalls erode clinician confidence and drive hospitals to consolidate around suppliers with spotless surveillance records.

Stringent Regulatory Approval Timelines

Introducer sheaths are U.S. Class II devices requiring 510(k) clearance, with a 147-day median review in 2024 that can stretch past 12 months when novel coatings enter the picture. Europe’s Medical Device Regulation has tacked on another 6–12 months compared with the former directive framework, and notified-body capacity constraints add uncertainty. Japan often demands local clinical data that push timelines to 24 months, and while China’s NMPA approved 47 cardiovascular devices in 2024, domestic trials stay mandatory for first-in-class entrants. Extended paths weigh most on small innovators and tilt share toward incumbents with seasoned regulatory teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hydrophilic Dominance Reflects Procedural Efficiency Gains

Hydrophilic devices captured 61.53% of 2025 revenue, holding the largest catheter introducer sheaths market share thanks to lubricious coats that shrink insertion force and lower radial artery spasm. Terumo’s Glidesheath Slender cut occlusion rates 25% versus uncoated alternatives in a 2024 multicenter trial. The hydrophilic subsegment is set to post a 10.32% CAGR, outpacing non-hydrophilic lines as radial cases climb. Non-hydrophilic sheaths still serve femoral procedures and cost-constrained markets but lag at roughly 7% growth.

The catheters’ thin-wall, friction-reducing profiles also cut procedural times and improve patient comfort. As a result, hospitals seeking smooth room turnover increasingly default to hydrophilic kits. Operational data indicate average setup savings of 8 minutes per case, reinforcing demand gains. Non-hydrophilic sheaths, however, remain relevant where larger vessels tolerate marginally higher friction or in low-budget procurement environments that favor lower unit price.

By Material: Pebax Ascendancy Driven by Kink Resistance

Polyurethane held 41.52% of 2025 revenue because of its well-established supply chain and price advantage. Yet Pebax is advancing fastest, delivering a 10.78% CAGR as clinicians value its 30% lower flexural modulus and superior kink-through curves. Cook Medical found Pebax devices halved insertion force compared with polyurethane in bench work. PTFE maintains a 28% share for its low-friction surface but suffers brittleness in small-diameter radial setups.

Pebax adoption accelerates whenever complex tortuous anatomy demands flexible yet strong access tools, positioning the material as a long-term challenger to polyurethane dominance. Supply constraints, such as Chemours-led PTFE outages in 2024, also motivate diversification toward Pebax. The trend improves gross margins for suppliers because Pebax products often command premium pricing despite resin cost declines as production scales.

By Coating: Drug-Eluting Formulations Target Thrombotic Events

Hydrophilic layers dominate (81.63% in 2025) due to radial-centric use, but drug-eluting coats are climbing at 11.74% CAGR as hospitals seek to suppress access-site thrombosis without systemic anticoagulants. Heparin-bonded sheaths reduced thrombus by 35% in preclinical evaluations. Antimicrobial coats occupy 7% of the mix and grow near double-digits, propelled by infection-control budgets and proven 50% microbial-colonization reductions in Teleflex’s chlorhexidine-silver product.

Uncoated options decline in share yet retain a foothold in cost-sensitive femoral protocols. Regulatory paths for drug-eluting sheaths include elution-profile characterization and ISO 10993 testing, extending U.S. clearance by roughly nine months but ultimately raising adoption barriers against low-cost imitators.

By Application: Neurovascular Surge Reflects Thrombectomy Volumes

Interventional cardiology comprised 53.75% of 2025 use, anchored by 1.2 million annual U.S. coronary interventions, while neurovascular work is the fastest climber at 10.52% CAGR. Thrombectomy procedures exceeded 100,000 U.S. cases in 2024 and are tracking further 20% incident growth by 2030. Penumbra’s radial-optimized CAT 5 catheter underscores how neurovascular shifts drive demand for kink-resistant 5–6 French sheaths.

Endovascular surgery held 22% of applications and posts an 8.1% CAGR, echoing guideline-driven endovascular-first therapy for peripheral artery disease. Interventional radiology, including tumor embolization, retains 15% share and grows 7.5%. Overall, neurovascular momentum changes design priorities toward ultra-trackable, slender sheaths.

By End User: Ambulatory Centers Capture Lower-Complexity Cases

Hospitals own 68.22% of 2025 sales thanks to monopoly over high-acuity emergencies, yet ambulatory surgical centers will rise at a 9.46% CAGR through 2031. Medicare data show 12% annual growth in outpatient peripheral angioplasty in 2024, a trend supporting the catheter introducer sheaths market. Ambulatory settings reduce overhead and cycle patients quickly, making pre-packed sheath-catheter kits attractive.

Specialty clinics held 12% share in 2025 and advance 8.3% as physicians open office-based labs. State rulings in Florida, Texas, and California have expanded covered procedures, allowing 18,000 peripheral interventions in 2024 versus 12,000 in 2022. Hospitals remain indispensable for complicated cases, but competitive pressure on procurement prices intensifies as outpatient venues reach critical mass.

Geography Analysis

North America contributed 41.43% of 2025 revenue, buoyed by high procedural counts and early adoption of sensor-embedded designs. Yet reimbursement pressures—such as a 3.8% cut to diagnostic catheterization outpatient rates in 2025—are moderating growth. Canada’s quality programs reward radial access, pushing adoption up 9% in 2024. Mexico expands cath-lab capacity under social-security funding, adding 14 new labs in 2024.

Asia-Pacific is the fastest region, expanding at 9.13% CAGR. China’s NMPA cleared 47 cardiovascular devices in 2024, and the country’s over-60 population will reach 400 million by 2035. India’s cath-lab count surpassed 1,200 facilities, helped by Ayushman Bharat coverage that added 80,000 eligible coronary cases in 2024. Japan approved Terumo’s Glidesheath Slender in 2024, with 22% market capture in six months. Mature markets like South Korea and Australia hover above 70% radial adoption but post lower incremental growth.

In Europe, Germany, France, and the United Kingdom combine for 60% of continental demand, but MDR-related bottlenecks slowed new introductions by nine months on average in 2024. Germany’s DRG system incentivizes radial access with a 12% reimbursement premium, stimulating hydrophilic uptake. The Middle East and Africa generated 7% of global sales and grew 8.5% amid Gulf state tertiary-care investment, including three United Arab Emirates cardiac centers opened in 2024. South America, chiefly Brazil and Argentina, represented less share; currency volatility and tariffs restrain imports yet local distributors adapt pricing to sustain a 7.8% CAGR.

Competitive Landscape

The catheter introducer sheaths market is moderately concentrated. Players chase innovation across material science, procedural efficiency, and regional deployments. Medtronic’s 2024 Affera acquisition signals a vertical integration push linking mapping catheters to tailored sheaths. Boston Scientific’s Slender Radial line uses a dual-layer hydrophilic coat tested for 60-minute lubricity retention.

Sensor-embedded hubs that feed real-time pressure data to angiography consoles are under co-development between Medtronic and imaging vendors, echoing Philips’ Azurion ecosystem. Regionals such as Oscor exploit niche functionality, offering a rotating hemostasis valve that facilitates repeated catheter exchanges without air embolism risk. Regulation favors incumbents with robust 510(k) dossiers, yet the median 147-day U.S. review allows agile firms to iterate designs quickly and capture emerging procedural niches.

Catheter Introducer Sheaths Industry Leaders

Boston Scientific Corp.

Medtronic plc

Merit Medical Systems

Teleflex Inc.

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: BrosMed’s Pregarde Guiding Sheath won EU MDR certification, expanding peripheral intervention coverage.

- August 2025: Merit Medical commercially launched the Prelude Wave Hydrophilic Sheath Introducer with SnapFix Securement Technology in the United States.

- April 2025: ASAHI INTECC began distributing Medikit’s Super Sheath Introducer Sheath under a new partnership agreement.

Global Catheter Introducer Sheaths Market Report Scope

A catheter introducer sheath is a thin-walled plastic tube inserted over a guidewire into a blood vessel or body cavity to provide a stable pathway for catheters and interventional devices, minimizing vascular trauma and preventing bleeding via a hemostatic valve.

The Catheter Introducer Sheaths Market Report is segmented by Product Type, Material, Coating, Application, End User, and Geography. By Product Type, the market is segmented into Hydrophilic and Non-hydrophilic. By Material, the market is segmented into Polyurethane, PTFE, Pebax, and Others. By Coating, the market is segmented into Hydrophilic, Drug-eluting, and Antimicrobial. By Application, the market is segmented into Interventional Cardiology, Endovascular Surgery, Interventional Radiology, and Neurovascular. By End User, the market is segmented into Hospitals, ASCs, and Specialty Clinics. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Hydrophilic Introducer Sheaths |

| Non-hydrophilic Introducer Sheaths |

| Polyurethane |

| PTFE |

| Pebax |

| Others |

| Hydrophilic |

| Drug-eluting |

| Antimicrobial |

| Interventional Cardiology |

| Endovascular Surgery |

| Interventional Radiology |

| Neurovascular Procedures |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hydrophilic Introducer Sheaths | |

| Non-hydrophilic Introducer Sheaths | ||

| By Material | Polyurethane | |

| PTFE | ||

| Pebax | ||

| Others | ||

| By Coating | Hydrophilic | |

| Drug-eluting | ||

| Antimicrobial | ||

| By Application | Interventional Cardiology | |

| Endovascular Surgery | ||

| Interventional Radiology | ||

| Neurovascular Procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the catheter introducer sheaths market?

The segment is worth USD 1.44 billion in 2026 and is projected to reach USD 2.03 billion by 2031.

Which sheath type leads global demand?

Hydrophilic introducer sheaths hold 61.53% of 2025 revenue and continue to expand quickly.

Which region is growing fastest?

Asia-Pacific is projected to rise at a 9.13% CAGR through 2031, driven by procedure expansion in China and India.

What material shows the strongest growth outlook?

Pebax-based sheaths post a 10.78% CAGR because of superior kink resistance and flexibility.

Which application segment is expanding most rapidly?

Neurovascular procedures, especially mechanical thrombectomy, are advancing at a 10.52% CAGR to 2031.

Page last updated on: