NICU Catheter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

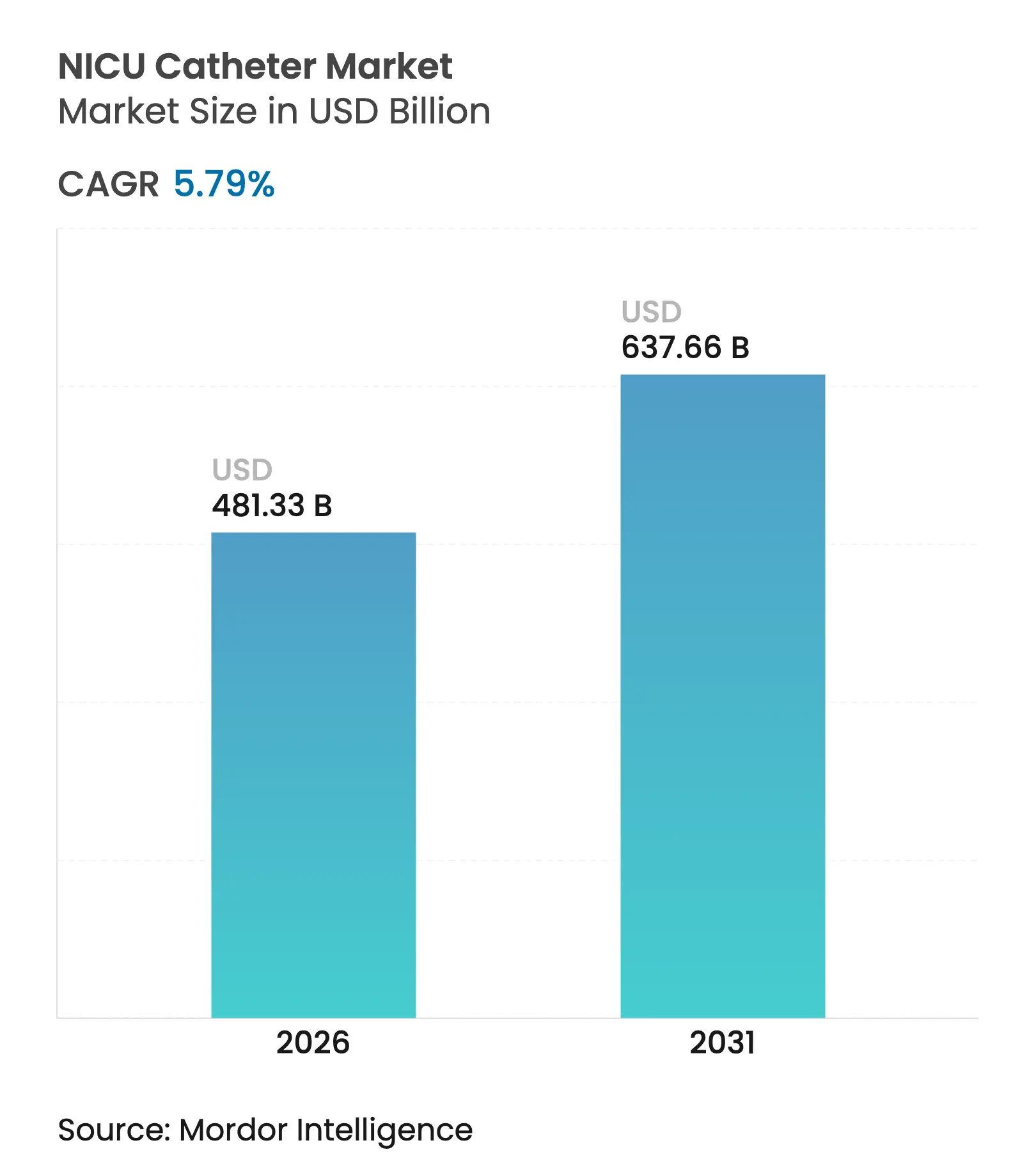

| Market Size (2026) | USD 481.33 Billion |

| Market Size (2031) | USD 637.66 Billion |

| Growth Rate (2026 - 2031) | 5.79 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

NICU Catheter Market Analysis by Mordor Intelligence

The NICU catheter market size was valued at USD 454.99 billion in 2025 and estimated to grow from USD 481.33 billion in 2026 to reach USD 637.66 billion by 2031, at a CAGR of 5.79% during the forecast period (2026-2031). Rising investments in Level-III and Level-IV units, especially across Asia-Pacific and Latin America, boost institutional demand for advanced lines that shorten procedure time and improve survival outcomes. Hospitals also favor catheters with embedded infection-prevention coatings because quality-of-care metrics now tie directly to reimbursement, driving systematic conversion to products that reduce central-line-associated bloodstream infection (CLABSI) risk. Meanwhile, supply-chain pressure on micro-bore polymers has encouraged material substitution and in-country manufacturing partnerships that stabilize inventory in high-growth regions. Vendors differentiate by layering AI-assisted navigation, antimicrobial surfaces, and pressure-sensing hubs onto product lines, a strategy that raises switching costs and sustains premium pricing within the NICU catheter market.

Key Report Takeaways

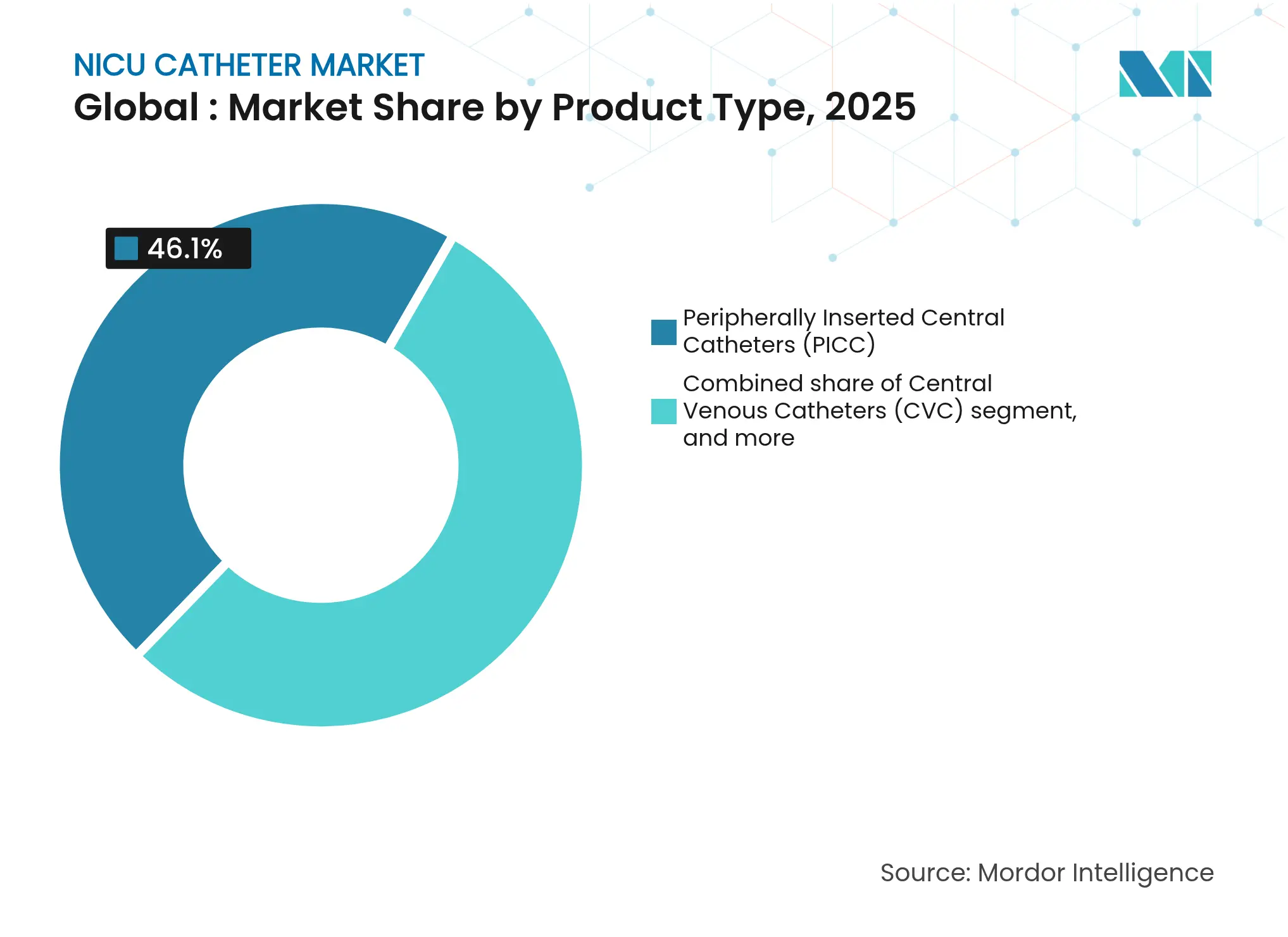

- By product type, Peripherally Inserted Central Catheters held 46.10% of the NICU catheter market in 2025, while Umbilical Venous Catheters are projected to rise at an 8.10% CAGR through 2031.

- By catheter material, Polyurethane captured 45.05% of NICU catheter market share in 2025; Polyethylene/PVC is expected to expand at an 8.20% CAGR to 2031.

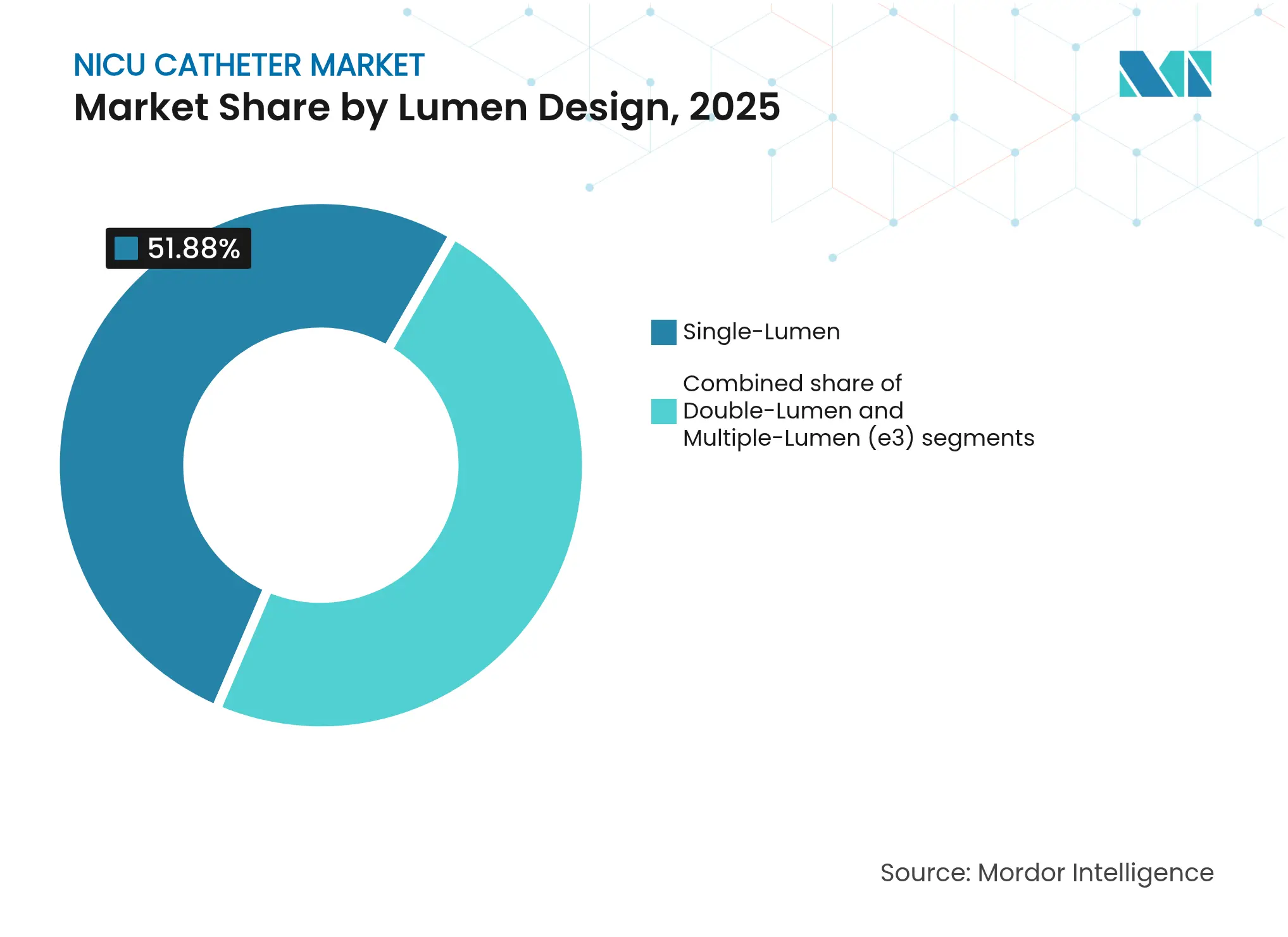

- By lumen design, single-lumen lines accounted for 51.88% of NICU catheter market size in 2025, whereas multiple-lumen devices are forecast to advance at a 7.85% CAGR between 2026 and 2031.

- By end user, hospitals held 57.10% share of NICU catheter market in 2025, but ambulatory surgical centers exhibit the fastest expansion with a 9.22% CAGR through 2031.

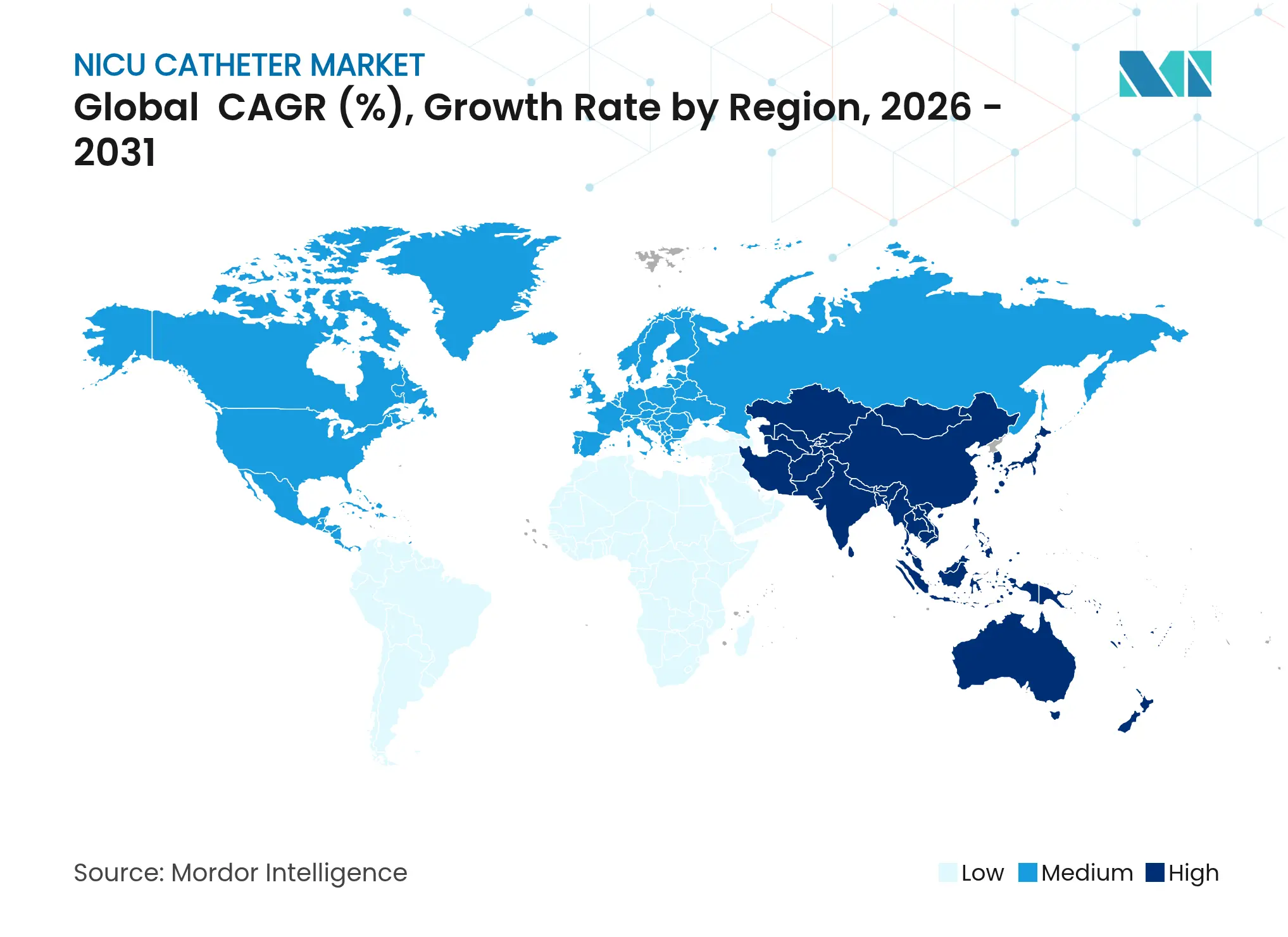

- By geography, North America dominated with 41.90% NICU catheter market share in 2025, yet Asia-Pacific is poised to register a 7.18% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global NICU Catheter Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising incidence of premature births globally Rising incidence of premature births globally | +1.8% | Global; highest in Asia-Pacific & Sub-Saharan Africa | Long term (≥4 years) | % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global; highest in Asia-Pacific & Sub-Saharan Africa | Impact Timeline:Long term (≥4 years) |

Technological advancements in neonatal vascular access devices Technological advancements in neonatal vascular access devices | +1.5% | North America & EU lead; APAC adoption follows | Medium term (2-4 years) | |||

Increasing investment in Level-III and Level-IV NICU infrastructure Increasing investment in Level-III and Level-IV NICU infrastructure | +1.2% | Asia-Pacific core; spill-over to MEA & Latin America | Long term (≥4 years) | |||

Growing adoption of infection-prevention protocols and bundles Growing adoption of infection-prevention protocols and bundles | +0.9% | Global; faster uptake in developed markets | Short term (≤2 years) | |||

Shift toward catheter manufacturing outsourcing by smaller NICUs Shift toward catheter manufacturing outsourcing by smaller NICUs | +0.6% | Primarily North America & EU | Medium term (2-4 years) | |||

Emergence of AI-assisted catheter tip navigation systems Emergence of AI-assisted catheter tip navigation systems | +0.4% | North America leads; EU & APAC follow | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence of Premature Births Globally

Roughly 15 million babies arrive preterm each year, and many require multiple catheters during prolonged NICU stays to manage infusions, nutrition, and diagnostics. Standardized umbilical catheter depths of 6 cm in extremely preterm neonates now guide placement accuracy and have helped push survival to 41% at 22 weeks and 64% at 23 weeks[1]National Institutes of Health, “Standardized Umbilical Catheter Depth Improves Outcomes,” pubmed.ncbi.nlm.nih.gov. Rising maternal age in developed nations further elevates prematurity risk, while enhanced reporting in low- and middle-income countries reveals higher baseline rates than previously documented. Each added catheter boosts total device volume, directly scaling demand across the NICU catheter market. Growing consensus on insertion-depth standards also drives hospital preference toward branded catheters with proven positioning precision.

Technological Advancements in Neonatal Vascular Access Devices

Intracavitary ECG (IC-ECG) guidance elevates first-attempt PICC success to 95% versus 78.8% using landmark techniques and slashes complications from 23.75% to 3.75%. Disposable pressure transducers now differentiate arterial from venous placement with 100% accuracy for umbilical artery and 97% sensitivity for venous lines at specific pressure cut-points[2]J. Smith et al., “Real-Time Pressure Transducers in Umbilical Catheterization,” nature.com. These innovations reduce X-ray exposure and procedure time, benefits that speed hospital adoption of premium lines in the NICU catheter market JA. AI-driven navigation augments IC-ECG by predicting optimal angles and issuing real-time deviation alerts, although uptake remains centered in tertiary hubs with robust digital infrastructure. Continuous sensor integration also feeds analytics dashboards that help clinicians track dwell time and performance for each catheter.

Increasing Investment in Level-III and Level-IV NICU Infrastructure

Asia-Pacific hospital systems are expanding tertiary neonatal capacity to meet growing middle-class expectations for specialized care. Capital programs integrate inventory-management tools, staff simulation labs, and multi-lumen catheter sets, collectively lifting device utilization per bed in the NICU catheter market. Queen’s Medical Centre in Nottingham followed a similar blueprint, modernizing facilities and adopting standardized catheter kits to address higher acuity newborns. Regulatory mandates on nurse-to-patient ratios in Level-IV units intensify demand for lines that permit concurrent infusions through fewer access points. Barcode-enabled tracking systems further accelerate reorder cycles and tighten vendor relationships, reinforcing growth for the NICU catheter market.

Growing Adoption of Infection-Prevention Protocols and Bundles

CLABSI bundles at Riley Hospital’s NICU cut infection rates from 4.8 to 0.37 per 1,000 line-days over 11 years. Simulation-based training lowered rates from 2.1 to 0.692 per 1,000 central-line days in another tertiary unit and has been widely replicated. Hospitals subsequently shift to coated or impregnated lines even though initial costs rise by 15% because each avoided CLABSI saves roughly USD 21,400 in care expenses. Purchasing committees now embed infection-control metrics into vendor scorecards, a move that favors premium devices in the NICU catheter market. Sustained outcome improvements validate continued budget allocation for advanced catheters with antimicrobial surfaces.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent regulatory and quality compliance requirements Stringent regulatory and quality compliance requirements | −0.8% | Global; intensity varies by jurisdiction | Long term (≥4 years) | (~) % Impact on CAGR Forecast:−0.8% | Geographic Relevance:Global; intensity varies by jurisdiction | Impact Timeline:Long term (≥4 years) |

High risk of catheter-related bloodstream infections High risk of catheter-related bloodstream infections | −0.6% | Global; more pronounced in resource-limited settings | Medium term (2-4 years) | |||

Supply chain constraints for medical-grade micro-bore polymers Supply chain constraints for medical-grade micro-bore polymers | −0.5% | Regional shortages in Asia-Pacific & Latin America | Short term (≤2 years) | |||

Adoption of extended-dwell peripheral IV catheters as substitute options Adoption of extended-dwell peripheral IV catheters as substitute options | −0.4% | North America & EU outpatient settings | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Regulatory and Quality Compliance Requirements

The FDA will harmonize its Quality System Regulation with ISO 13485 in February 2026, forcing catheter makers to upgrade tracking, documentation, and risk-management systems at notable expense[3]FDA, “Quality System Regulation Amendments,” federalregister.gov. Small firms face heavier proportional burdens that could delay product launches and slow the NICU catheter market. European MDR deadlines compound the challenge by demanding additional notified-body audits, prompting some companies to consolidate or license out technology. Predetermined change-control plans (PCCPs) offer one escape valve by allowing iterative improvements without new PMA submissions, but compiling the initial clinical evidence remains costly. Compliance overhead may therefore accelerate merger activity as smaller innovators pair with well-capitalized multinationals.

High Risk of Catheter-Related Bloodstream Infections

Hospital-onset bacteremia occurs at 1.1 events per 1,000 patient-days and significantly increases mortality when central lines are present. Late-onset neonatal sepsis affects 10.8% of very-low-birth-weight infants in culture-proven cases and 30% in culture-negative cases, underscoring persistent vulnerability despite bundle protocols. Resistant strains such as Staphylococcus capitis complicate therapy, often necessitating line removal that disrupts treatment and increases device use. In resource-constrained settings, limited staffing and inadequate sterilization amplify risks, urging cautious adoption of longer-dwell or multi-lumen lines that could otherwise expand NICU catheter market utilization. Economic fallout averages USD 50,000 per infection episode due to prolonged hospitalization and neurodevelopmental follow-up, straining budgets and reinforcing conservative purchasing patterns.

Segment Analysis

By Product Type: PICC Dominance Faces UVC Innovation

Peripherally Inserted Central Catheters held 46.10% of the NICU catheter market share in 2025 thanks to widespread clinician familiarity and AI-guided placement systems that deliver 95% first-attempt success. Umbilical Venous Catheters, however, are advancing at an 8.10% CAGR as standardized 6 cm insertion guidelines reduce malposition and boost survival among extremely preterm neonates. Utah Medical Products credits robust UVC demand for a sizeable slice of its 2024 revenue, illustrating growing clinical preference for specialized neonatal access. Device engineers have added pressure-sensing hubs to newer UVC lines, halving repositioning events and strengthening hospital confidence in the segment.

PICC innovation continues with anti-thrombogenic coatings and thinner wall profiles that maintain flow while easing insertion trauma, benefits that keep high-acuity centers loyal to the platform. Central Venous Catheters occupy critical niches for surgical neonates needing rapid volume resuscitation, while specialized drainage and monitoring lines command premium pricing because of low competition. Competitive rivalry therefore hinges on breadth of portfolio; suppliers offering both PICC and UVC options achieve wider formulary penetration and reinforce NICU catheter market growth.

Note: Segment shares of all individual segments available upon report purchase

By Catheter Material: Polymer Innovation Drives Growth

Polyurethane dominated 45.05% of NICU catheter market size in 2025 because its tensile strength and imaging visibility match everyday clinical requirements. Hospitals under cost pressure increasingly turn to Polyethylene/PVC blends that deliver equivalent rigidity at lower unit cost; the segment is expanding at an 8.20% CAGR through 2031. Antimicrobial PVC resins now demonstrate 99% Staphylococcus aureus kill in lab tests, providing a clinical justification beyond price. Silicone remains the go-to for chronic indwelling lines given its unmatched biocompatibility, despite a premium that limits widespread use.

Composite and advanced polymers integrate drug-eluting or silver-ion layers that cut CLABSI incidence by 42% in early trials, but scaling multi-layer extrusion requires expensive tooling that only large manufacturers can fund. Temporary shortages of medical-grade polyurethane in 2024 exposed single-source vulnerabilities, prompting strategic stockpiling and supplier diversification across hospital groups. Resin capacity additions in Southeast Asia should ease supply constraints by 2026, potentially narrowing the cost gap and reshaping material preference within the NICU catheter market.

By Lumen Design: Complexity Drives Multi-Lumen Adoption

Single-lumen catheters led demand at 51.88% in 2025, meeting needs for routine fluids and intermittent draws. Yet multiple-lumen devices are growing at an 7.85% CAGR because improved survival of <28-week neonates necessitates concurrent infusions, sampling, and monitoring through a single access point. Terumo’s Rika platform, already in 98 U.S. centers, combines optimized fluid dynamics with 20-25% projected market share capture post-installation, illustrating the commercial pull of advanced designs. While multi-lumen catheters can cost 1.8× more than single-lumen lines, hospitals often justify the premium through fewer insertions and shorter stays, reinforcing NICU catheter market expansion.

Device engineers now taper external profiles without sacrificing internal diameter, mitigating thrombosis risk and facilitating insertion in fragile vessels. Double-lumen lines serve transitional acuity needs, striking balance between functionality and infection risk. Manufacturers bundle simulation training that cuts occlusion events by 17% and cements user confidence, a strategy that tightens vendor-hospital relationships in the NICU catheter market.

Note: Segment shares of all individual segments available upon report purchase

By End User: ASC Growth Challenges Hospital Dominance

Hospitals controlled 57.10% of NICU catheter market demand in 2025 thanks to integrated imaging, surgical backup, and experienced vascular teams. Ambulatory surgical centers, however, are pacing with a 9.22% CAGR as miniaturized ultrasound and AI navigation enable safe outpatient catheter placements. Payers reinforce the shift by reimbursing ASC procedures at 10-15% lower rates than comparable hospital services, delivering savings without outcome compromise.

Specialty clinics that treat chronic neonatal conditions deploy roving catheter teams, extending expertise into regional hubs and raising device turnover. Home-health agencies now manage stable preterm infants with maintenance lines under telehealth supervision, a niche yet rising cohort within the NICU catheter market. Manufacturers that bundle disposable kits with remote-monitoring dashboards secure footholds among decentralized providers, while hospital consolidations funnel volume contracts through group-purchasing consortia that squeeze smaller vendors. Overall, multi-channel demand diversity underpins resilient growth for the NICU catheter market.

Geography Analysis

North America retained 41.90% NICU catheter market share in 2025 as mature NICU networks, clear FDA pathways, and outcome-based reimbursement sustained spending on premium lines. Major systems such as Memorial Hermann and AdventHealth Orlando added Level-IV beds and barcode inventory tools that streamline reorders, deepening vendor ties and stabilizing regional demand. Yet birth-volume plateaus and price negotiations moderate growth, prompting suppliers to focus on AI and antimicrobial add-ons that justify premium positioning within the NICU catheter market.

Asia-Pacific is the fastest-growing region with a 7.18% CAGR to 2031, powered by large birth cohorts and aggressive state spending on tertiary neonatal centers. Local-content rules spur joint ventures between multinationals and domestic OEMs, lowering import duties and expanding after-sales service footprints. Regulatory fragmentation across ASEAN and South Asia prolongs registration timelines, but regional hubs now consolidate dossier preparation to expedite launches, helping vendors tap underserved Tier-2 cities where NICU catheter market penetration remains low.

Europe posts steady expansion as universal healthcare and evidence-based procurement favor catheters with robust clinical-outcome data. Brexit’s divergence from EU MDR adds complexity, but mutual-recognition efforts aim to minimize dual-audit fatigue by 2027. Middle East & Africa and South America together hold single-digit shares yet show high elasticity; multilateral loans now fund NICU construction, positioning these geographies for accelerated growth once basic infrastructure and trained staff become available.

Competitive Landscape

Market Concentration

The NICU catheter market is moderately concentrated; leading firms leverage broad portfolios and regulatory expertise to protect share, while mid-tier players carve out niches in polymer science or regional distribution. ICU Medical’s integration of Smiths Medical bolstered its neonatal range, folding the Argyle line into enterprise contracts that combine infusion pumps and vascular access. Vygon’s Modified Seldinger Technique trims procedural steps by 25% and has gained guideline citations, enhancing brand prestige among European neonatal specialists.

Becton Dickinson’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical-Care unit deepened its monitoring and access portfolio, enabling bundled deals attractive to value-driven health systems. Teleflex acquired BIOTRONIK’s vascular business for EUR 760 million in July 2025, adding EUR 177 million revenue in the second half of 2025 and enhancing peripheral-intervention reach that complements neonatal offerings. Contract manufacturers like AMETEK EMC capture outsourcing demand from smaller brands, supplying ISO 13485-compliant extrusion and assembly services that underpin global expansion for the NICU catheter market.

Technology remains the key differentiator; AI navigation, antimicrobial coatings, and pressure-sensing hubs headline marketing campaigns as firms seek measurable outcome advantages. Patent filings increasingly target material innovations such as B. Braun’s elastically deformable valves that permit one-handed insertion without raising profile height. Geographic expansion often hinges on distributor alliances offering regulatory know-how and hospital relationships, particularly in Asia-Pacific and South America where local presence influences formulary wins.

NICU Catheter Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed acquisition of BIOTRONIK’s Vascular Intervention business for EUR 760 million, adding EUR 177 million revenue in H2 2025 with expected 6% annual growth from 2026.

- April 2025: Medtronic received FDA approval for OmniaSecure defibrillation lead, measuring 4.7 French and achieving 95.8% implantation success with no major complications.

- March 2025: FDA issued draft guidance on aluminum limits in small-volume parenteral drugs to protect preterm neonates from toxicity.

- November 2024: CMS granted pass-through payment for Medtronic Symplicity Spyral renal-denervation catheter effective Jan 2025, offsetting hospital adoption costs.

- August 2024: Terumo reported 98 Rika installations across U.S. centers, targeting 20–25% catheter market share post-deployment.

Table of Contents for NICU Catheter Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence of Premature Births Globally

- 4.2.2Technological Advancements in Neonatal Vascular Access Devices

- 4.2.3Increasing Investment in Level-III And Level-IV NICU Infrastructure

- 4.2.4Growing Adoption of Infection-Prevention Protocols and Bundles

- 4.2.5Shift Toward Catheter Manufacturing Outsourcing by Smaller NICUs

- 4.2.6Emergence of AI-Assisted Catheter Tip Navigation Systems

- 4.3Market Restraints

- 4.3.1Stringent Regulatory and Quality Compliance Requirements

- 4.3.2High Risk of Catheter-Related Bloodstream Infections

- 4.3.3Supply Chain Constraints for Medical-Grade Micro-Bore Polymers

- 4.3.4Adoption of Extended-Dwell Peripheral IV Catheters as Substitute Options

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Peripherally Inserted Central Catheters (PICC)

- 5.1.2Central Venous Catheters (CVC)

- 5.1.3Umbilical Venous Catheters (UVC)

- 5.1.4Other Product Types

- 5.2By Catheter Material

- 5.2.1Polyurethane

- 5.2.2Silicone

- 5.2.3Polyethylene / PVC

- 5.2.4Composite & Advanced Polymers

- 5.3By Lumen Design

- 5.3.1Single-Lumen

- 5.3.2Double-Lumen

- 5.3.3Multiple-Lumen (≥3)

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Specialty Clinics

- 5.4.3Ambulatory Surgical Centers

- 5.4.4Other End Users

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1ICU Medical (Smiths Medical)

- 6.3.2Cardinal Health

- 6.3.3Vygon SA

- 6.3.4Becton Dickinson & Company

- 6.3.5B. Braun Melsungen AG

- 6.3.6Utah Medical Products

- 6.3.7NeoMedical Inc.

- 6.3.8Greiner Bio-One

- 6.3.9Teleflex Inc.

- 6.3.10AngioDynamics

- 6.3.11Merit Medical

- 6.3.12Access Vascular

- 6.3.13Advin Health Care

- 6.3.14Marian Medical

- 6.3.15Footprint Medical

- 6.3.16Angiplast Pvt Ltd

- 6.3.17Medtronic plc

- 6.3.18Baxter International

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global NICU Catheter Market Report Scope

As per the scope of this report, the NICU catheter can be used as vascular access on a premature baby for nutrition, drawing blood, and delivery of medicines. For instance, an umbilical artery catheter (UAC) is used to draw blood from an infant at different times, without repeated needle sticks. Additionally, it can be used for a baby's blood pressure monitoring continuously. The NICU catheter market is segmented by product type (peripherally inserted central catheters (PICCs), central venous catheters (CVCs), umbilical venous catheters (UVCs), and others), end user (hospitals, specialty clinics, ambulatory surgical centers, and others) and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.