Peripheral Intravenous Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

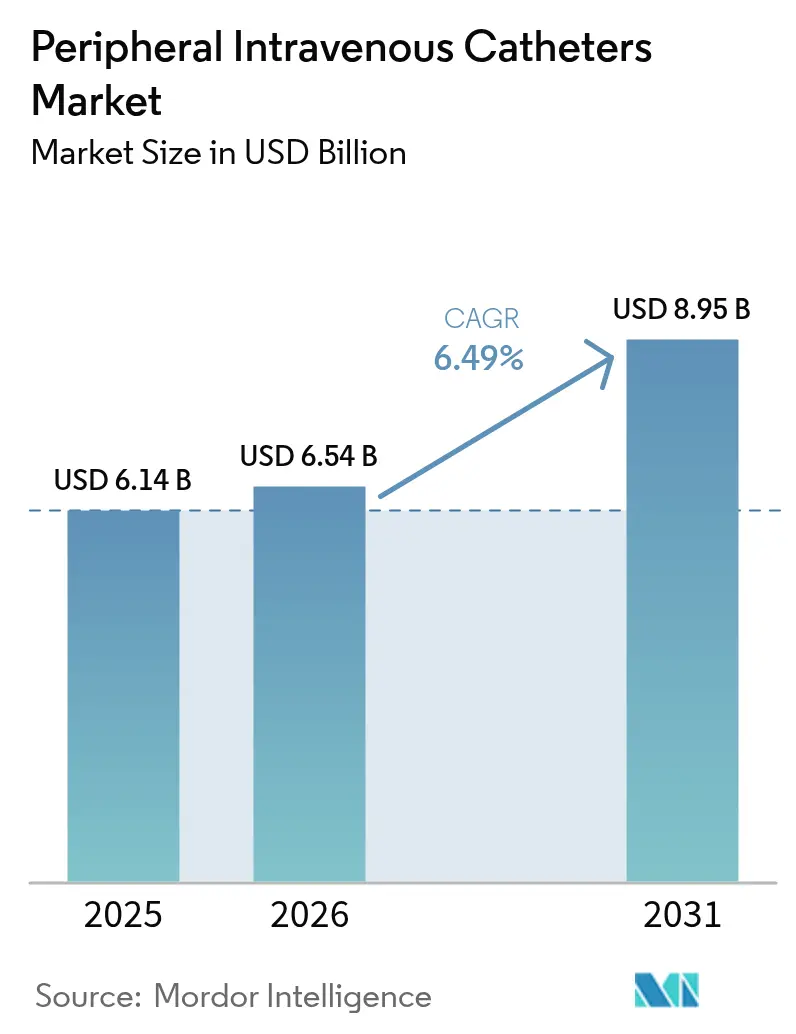

| Market Size (2026) | USD 6.54 Billion |

| Market Size (2031) | USD 8.95 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

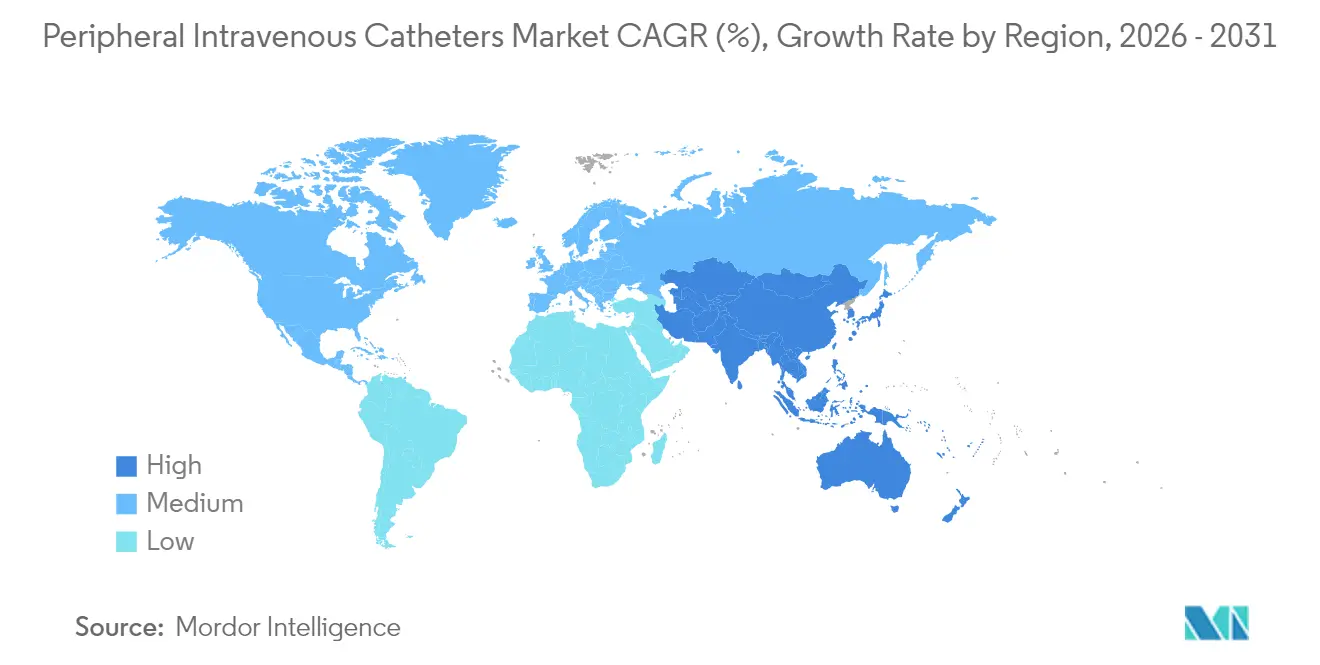

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peripheral Intravenous Catheters Market Analysis by Mordor Intelligence

The peripheral intravenous catheters market size is expected to grow from USD 6.14 billion in 2025 to USD 6.54 billion in 2026 and is forecast to reach USD 8.95 billion by 2031 at 6.49% CAGR over 2026-2031. Expanding outpatient care, strict safety regulations, and sustained product innovation are moving procurement decisions toward premium, safety-engineered devices. Higher chronic disease prevalence is widening the pool of patients who need reliable vascular access over longer dwell times. Ambulatory surgical centers (ASCs) are accelerating growth through higher procedure volumes and lower per-episode costs, while hospitals still dominate absolute device demand. Manufacturers are sharpening their competitive edge through closed-system designs, imaging-guided insertion tools, and advanced material formulations that cut complication rates and improve clinician workflows.

Key Report Takeaways

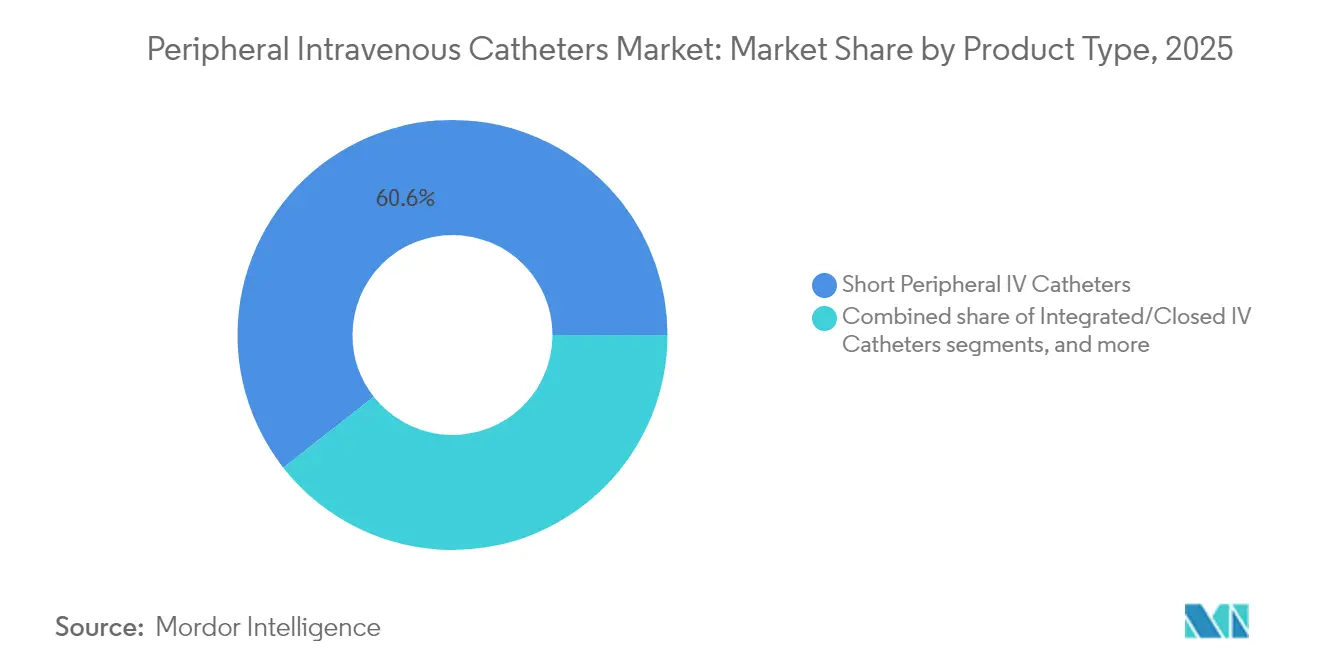

- By product type, short peripheral IV catheters held 60.58% of the peripheral intravenous catheters market share in 2025; midline catheters are expanding at an 8.21% CAGR through 2031.

- By technology, safety and blood-control designs captured 67.95% of the peripheral intravenous catheters market in 2025, and the segment is climbing at an 8.54% CAGR to 2031.

- By material, polyurethane maintained 57.02% of the peripheral intravenous catheters market in 2025, while silicone is poised for 8.33% CAGR growth through 2031.

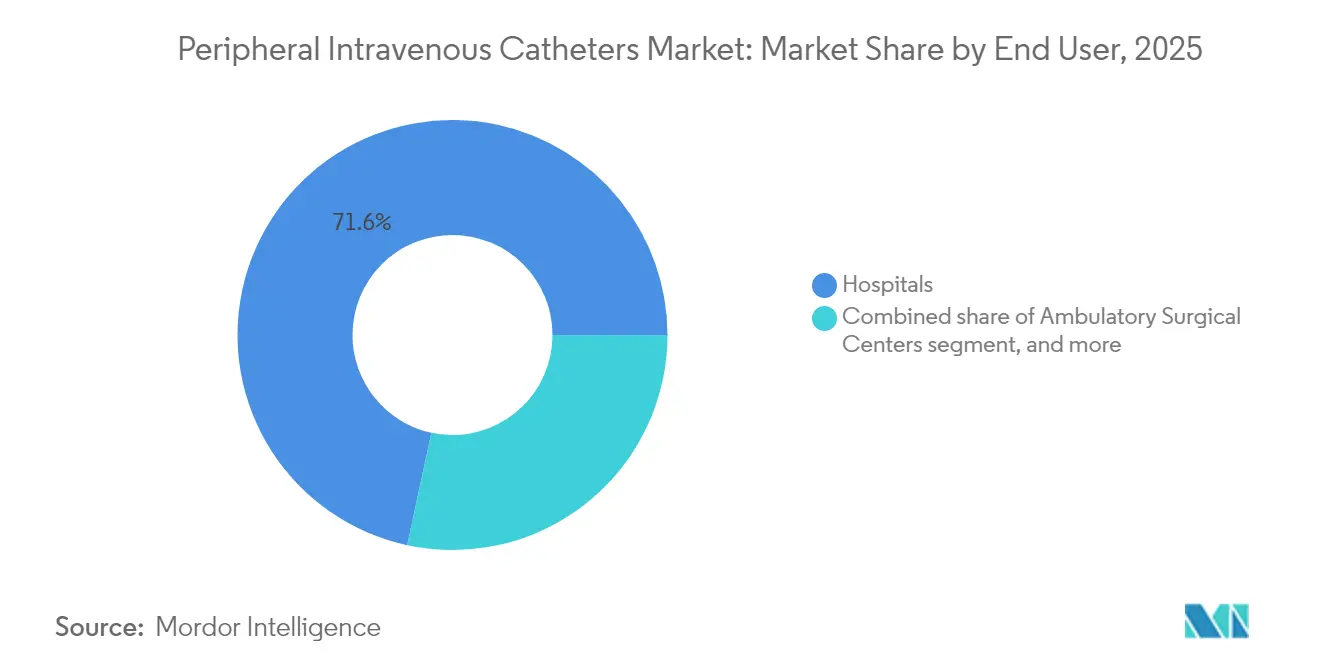

- By end user, hospitals accounted for 71.62% of the peripheral intravenous catheters market size in 2025; ASCs are the fastest-growing channel at 9.35% CAGR.

- By application, medication administration generated 44.15% of 2025 revenue, whereas diagnostic imaging contrast is forecast to rise at a 9.22% CAGR to 2031.

- By geography, North America commanded 39.88% revenue in 2025; Asia-Pacific is on track for the highest regional CAGR of 7.34% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peripheral Intravenous Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic and acute diseases | +1.2% | North America, Europe, Japan | Long term (≥ 4 years) |

| Expansion of outpatient and home infusion settings | +1.0% | North America, EU; accelerating in major APAC urban centers | Medium term (2–4 years) |

| Regulatory mandates on needlestick and blood-exposure safety | +0.8% | Global, with strictest enforcement in North America and EU | Short term (≤ 2 years) |

| Continuous product innovation in catheter materials and design | +0.7% | R&D hubs in North America, Europe, Japan | Medium term (2–4 years) |

| Government bulk procurement programs in emerging markets | +0.6% | India, China, ASEAN, MEA, Latin America | Long term (≥ 4 years) |

| Integration of imaging and digital guidance for vascular access | +0.4% | Early adoption in North America and EU; premium segments across APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic and Acute Diseases

Diabetes-related disability-adjusted life years climbed more than 80% since 2000, amplifying demand for dependable vascular access across acute and long-term care settings. Aging populations in the United States, Japan, and Western Europe are experiencing multi-morbidities that necessitate longer dwell catheters and higher infusion frequencies. Hospitals are validating polyurethane materials showing 52.9 MPa tensile strength yet 90% light transmittance, which improves site visualization and reduces unplanned restarts. Personalized oncology and biologic regimens demand consistent flow rates over extended durations, leading providers to favor midline and extended-dwell devices that decrease insertion trauma. Collectively, these epidemiological dynamics sustain steady volume growth and reward suppliers that bring infection-resistant, high-clarity catheters to market.

Expansion of Outpatient and Home Infusion Settings

ASCs are forecast to process 44 million procedures by 2034, a 21% jump from 2024, reshaping where vascular access is initiated. Outpatient migration accelerates purchasing of devices designed for maintenance outside the ICU, including integrated extension tubing that keeps systems closed during therapy. Home infusion protocols now emphasize devices that hold patency with minimal nurse intervention, as outlined in the 2024 Infusion Therapy Standards of Practice. Digital ultrasound systems such as BD’s SiteRite 9 pair imaging with needle tracking, increasing first-attempt success rates and reducing unscheduled hospital visits. These care-delivery shifts favor suppliers that bundle catheters with portable guidance tools, consumables, and education modules for non-hospital staff.

Regulatory Mandates on Needlestick and Blood-Exposure Safety

The FDA classified force-activated separation devices as Class II under special controls in 2024, driving procurement toward safety-engineered catheters[1]Federal Register, “Intravenous Catheter Classification,” FEDERALREGISTER.GOV. U.S. health systems face liability risks averaging USD 890 per needlestick episode, strengthening ROI arguments for blood-control hubs. Ultrasound guidance increases pediatric first-attempt success rates to 85.4% compared with 45.8% using palpation, lowering insertion-related injury events. Group purchasing organizations have aligned contract terms with these mandates, giving safety designs priority tiers in value-analysis committees. As regulators expand oversight, conventional open-hub products risk gradual phase-out, accelerating share shifts toward closed, automated safety systems.

Continuous Product Innovation in Catheter Materials and Design

Silicone-based adhesive platforms reduce visible skin damage versus acrylic fixtures, supporting patient comfort in outpatient and pediatrics. Radiopaque polyurethanes optimize in-procedure visibility without sacrificing flexibility, bolstering adoption in interventional imaging suites. Embedded sensor arrays enable real-time pressure and flow monitoring, while BD’s Cue needle-tracking algorithm improves placement accuracy during power injections up to 325 psi. Such multifunctional designs command premiums but demonstrate downstream cost offsets through fewer restarts and complications. Consequently, R&D pipelines target antimicrobial coatings, biodegradable shafts, and smart hubs that integrate with electronic medical records to document dwell times automatically.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High incidence of catheter failures and complications | -0.9% | Global; most acute in resource-constrained health systems | Short term (≤ 2 years) |

| Availability of alternative vascular access devices | -0.6% | North America, Europe; gaining traction in high-acuity tertiary centers | Medium term (2–4 years) |

| Environmental sustainability and waste-disposal concerns | -0.5% | EU and North America leading policy changes; spreading globally | Long term (≥ 4 years) |

| Purchasing power concentration of group purchasing organizations | -0.4% | United States dominant; emerging influence in Europe and selected APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Incidence of Catheter Failures and Complications

First-pass cannulation fails in 40% of attempts, spiking to 70% in difficult-access cohorts, adding an estimated USD 2.68 billion in emergency department costs each year in the United States. Device recalls, such as the FDA’s early alert on specific PowerPICC lots, erode clinician confidence and trigger unbudgeted replacement cycles. Central line-associated bloodstream infections still account for roughly 20% of healthcare-associated bacteremia, prompting exploration of hubs that generate on-site hypochlorous acid for continuous disinfection. Mitigating these failures requires more training, ultrasound capital, and robust data tracking, costs that smaller hospitals may struggle to absorb in the short term.

Environmental Sustainability and Waste-Disposal Concerns

Single-use catheter programs in the United States generate 206 million liters of waste annually, provoking calls for greener alternatives. The NHS is piloting centralized waste-reduction frameworks that reward suppliers offering recyclable or reusable sets[2]Brighton and Sussex Medical School, “Sustainable Medical Devices Report,” BSMS.AC.UK. Biodegradable polymers—polyhydroxyalkanoates, polylactic acid, polybutylene succinate—remain under investigation but must match clinical performance at competitive cost. U.S. policy makers are integrating life-cycle assessments into device approvals, requiring manufacturers to document carbon reductions across supply chains. Although sustainability boosts brand value, re-processing workflows and sterilization infrastructure create near-term complexity that may dampen adoption pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Midlines Strengthen Extended-Dwell Adoption

Midline catheters generated the fastest 8.21% CAGR through 2031, even as short IV catheters retained 60.58% revenue in 2025, a position underscored by their versatility in routine infusions. Clinical trials have verified that midlines cut bloodstream infection risk relative to peripherally inserted central catheters for intermediate-duration therapies. The peripheral intravenous catheters market size for midlines is forecast to widen further as chronic-care pathways migrate to outpatient venues.

Design updates center on soft-tip radiopaque shafts, integrated stabilizers, and closed connectors that remain occlusion-free longer than 28 days. Regulatory clearance for B. Braun’s Introcan Safety 2 Deep Access IV Catheter illustrates how automatic needle shielding and enhanced flow rates are converging to reinforce clinician confidence. While price-sensitive buyers still rely on basic short catheters, the clinical imperative to minimize reinsertion events positions midlines as a rising standard for oncology, heart-failure, and complex antibiotic regimens.

By Technology: Safety Systems Move From Premium to Mainstream

Safety and blood-control formats held 67.95% of 2025 revenue and are adding 8.54% CAGR, signaling that compliance is outpacing cost as the pivotal procurement criterion. Closed-hub valves and automatic retraction needles are now embedded across flagship portfolios such as BD Insyte Autoguard BC, which cuts blood exposure by 95%. The peripheral intravenous catheters market continues to phase out conventional open-hub products, especially in high-litigation regions.

Professional societies recommend pairing safety catheters with bedside ultrasound; 2024 guidelines from the American Society of Echocardiography endorse factory-integrated flashback chambers and blunt cannulae to cut insertion trauma. As hospitals track sharps-injury metrics on public dashboards, risk-adjusted reimbursement models are beginning to penalize facilities with high incident rates, reinforcing the switch to safety devices.

By Material: Silicone Gains Ground on Comfort Metrics

Polyurethane still accounts for 57.02% of revenue owing to its tensile strength and chemical compatibility, but silicone is charting the highest 8.33% CAGR as outpatient dwell times lengthen. The peripheral intravenous catheters market share leadership of polyurethane stems from broad SKU availability and price competitiveness; however, silicone’s softer modulus lowers phlebitis incidence, a value recognized in pediatric oncology protocols.

Manufacturers are experimenting with polyurethane-urea blends that retain 90% transparency at 550 nm while boosting durability, bridging the performance gap and allowing visualization during insertion. Future materials roadmaps focus on antimicrobial additives, hydrophilic interiors to reduce thrombosis, and recycled content that aligns with ESG procurement criteria.

By End User: ASC Growth Redefines Channel Mix

Hospitals captured 71.62% of 2025 revenues, reflecting their central role in trauma, critical care, and high-acuity procedures. Yet ASCs, advancing at 9.35% CAGR, are redefining channel priorities as payers encourage same-day discharge pathways. Medicare spent USD 6.1 billion on ASC services for 3.3 million beneficiaries in 2022, underscoring the volume at stake.

The peripheral intravenous catheters market now sees manufacturers fielding compact insertion kits with color-coded components specifically for outpatient turnover. Home health agencies and infusion pharmacies represent adjacent expansion zones, each requiring remote training portals and tamper-evident packaging to assure adherence and safety.

By Application: Diagnostics Propel High-Pressure Designs

Medication administration remained the largest use case with 44.15% of 2025 sales, while diagnostic imaging and contrast delivery is scaling at a 9.22% CAGR amid expanding CT and MRI capacity. BD’s Nexiva Diffusics employs a laser-cut diffusion tip that tolerates power-injection up to 325 psi without compromising vessel integrity. This capability broadens peripheral access into radiology suites, mitigating the need for central lines and reducing overall procedure time.

The peripheral intravenous catheters market size for diagnostic applications is set to increase as interventional radiologists rely on multi-phase contrast studies requiring rapid, high-flow bolus delivery. Fluid resuscitation and nutrition infusions remain core but mature, whereas transfusion-specific devices command niche volumes tied to hemovigilance protocols.

Geography Analysis

North America generated 39.88% of 2025 revenue, anchored by the United States, where annual consumption exceeds 300 million units. Robust reimbursement and hospital investment in safety portfolios sustain premium average selling prices. The region is adding ultrasound-guided insertion modules, remote vascular-access credentialing, and predictive analytics dashboards that monitor catheter dwell time compliance. Canada and Mexico broaden regional scale through public-sector tenders and new maquiladora manufacturing footprints, respectively.

Europe, a mature regulatory environment, balances patient-safety mandates with emergent circular-economy requirements. Germany, France, and the United Kingdom account for the majority of regional demand, while Spain and Italy adopt reuse pilots to curb single-use plastics. EU Medical Device Regulation enforcement compels suppliers to refresh technical documentation and post-market surveillance, elevating market-entry barriers for new entrants. Public procurement frameworks now weight sustainability alongside clinical evidence, fostering dialogue on recycled polymers and extended-life formats.

Asia-Pacific is the fastest-growing geography at 7.34% CAGR, driven by China, India, Japan, South Korea, and Australia. India’s medical technology sector is set to scale from USD 16–17 billion to USD 50 billion by 2030 under the New Drugs, Medical Devices and Cosmetics Bill of 2023, catalyzing domestic manufacturing alliances. China leverages cost-effective mass production yet is investing in premium image-guided systems to serve tertiary hospitals. Japan’s super-aged society necessitates advanced silicone designs for fragile veins, while Australia focuses on infection-prevention benchmarks that align with national quality indicators. Collectively, these trends expand the peripheral intravenous catheters market footprint across price tiers, compelling multinationals to localize supply chains and co-develop clinical education platforms.

Regulatory Landscape

In the United States, the FDA action in August 2024 reclassified intravenous catheter force-activated separation devices as Class II under special controls. This has reinforced procurement movement toward safety features intended to mitigate needlestick and blood exposure in hospital risk programs.

In Europe, EU MDR implementation has tightened documentation and registration requirements while creating relief paths for established technologies. In March 2026, the European Commission adopted delegated regulations expanding the Well-Established Technologies list to include peripheral catheters and cannulas under EU MDR 2017/745, with mandatory EUDAMED registration for new MDR/IVDR devices starting May 28, 2026. A parallel MDCG guidance refresh in April 2026, along with ongoing ISO 10555-5 revision influence, is expected to shape verification and submission planning.

Competitive Landscape

The peripheral intravenous catheters market features moderate consolidation, with the top five suppliers estimated to control 60–65% of global revenue. BD’s USD 4.2 billion acquisition of Edwards Lifesciences’ Critical Care division in 2025 signals a push toward integrated patient-monitoring ecosystems that link catheters with hemodynamic analytics. Teleflex’s EUR 760 million purchase of BIOTRONIK’s vascular intervention assets broadens its portfolio to drug-coated balloons, enabling cross-selling with existing sheath and access devices.

B. Braun invested more than USD 1 billion since 2020 to expand U.S. IV fluid capacity and add 30 million additional IV sets annually, reflecting strategic commitment to secure regional supply chains. Terumo launched a USD 75 million corporate venture fund to source breakthroughs in cardiovascular and digital health, reinforcing its pipeline diversification in vascular access. Niche innovators such as Poly Medicure are gaining traction via FDA-cleared Nouvo Safety Set, demonstrating that targeted R&D plus regulatory agility can win share in specialized channels.

Competitive differentiation revolves around closed-loop safety mechanisms, ultrasound-ready introducer technology, and data-connected hubs that feed utilization metrics to electronic health records. ESG credentials are emerging as tender differentiators in Europe, rewarding suppliers that quantify carbon reductions and implement take-back programs. Group purchasing organizations use AI-enabled analytics to identify complication-adjusted total cost of ownership, favoring devices with demonstrable dwell-time superiority and lower restart rates.

Peripheral Intravenous Catheters Industry Leaders

B. Braun Melsungen AG

Lineus Medical

Becton Dickinson & Company

ICU Medical (Smiths Medical)

Teleflex Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities around prevention of bloodstream infections, reduction of blood exposure, and preservation of peripheral veins are pushing providers toward closed systems and imaging-guided insertion workflows. The May 2024 WHO guideline on preventing bloodstream infections associated with peripheral catheters offers a commonly referenced baseline for insertion, maintenance, and timely removal, which supports bundled device and protocol offerings across hospitals, ambulatory surgical centers, and alternate care sites.

In Europe, regulatory modernization and in North America safety-driven tendering are both shaping procurement toward premium safety and closed designs. The EU MDR shift, including mandatory EUDAMED registration starting May 28, 2026 and the 2026 Well-Established Technologies expansion to peripheral catheters and cannulas, raises the bar for technical files and post-market surveillance readiness, and it narrows the window for new entries that do not align on classification and evidence. In parallel, growth in outpatient and home infusion care is extending demand for extended-dwell peripheral options and imaging-guided insertion workflows that are already visible in leading product portfolios.

Recent Industry Developments

- July 2026: Lineus Medical renewed its distribution agreement with Vizient for SafeBreak Vascular. The continuation supports access to large U.S. hospital accounts served by a major GPO, helping broaden standardization of breakaway tubing as a safety adjunct around peripheral IV therapy.

- December 2025: BD launched the BD Nexiva Closed IV Catheter System in Indonesia. The rollout extends closed-system peripheral IV adoption into a large, fast-scaling care market and reinforces the use of blood-control and closed-hub designs as a baseline feature set in new geographies.

- September 2024: FDA clearance for the Introcan Safety 2 Deep Access IV Catheter was granted, expanding availability of safety-engineered deep-access peripheral options. B. Braun Medical expands opportunities as hospitals seek longer dwell performance with automatic needle shielding to meet tightening sharps-injury prevention expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from peripheral intravenous catheters used to obtain short term venous access for infusion, drug delivery, or blood sampling in clinical care settings. We count the device value sold into hospitals and other care sites across the covered geographies.

Scope exclusions: Excludes central venous access devices, midline catheters, PICCs, IV administration sets, and needleless connectors unless they are sold as part of a PIVC specific integrated system.

Segmentation Overview

- By Product Type

- Short Peripheral IV Catheters

- Integrated / Closed IV Catheters

- Midline Catheters

- Extended-Dwell Catheters

- By Technology

- Safety / Blood-Control Catheters

- Conventional Catheters

- By Material

- Polyurethane

- Silicone

- Other Plastics

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home Healthcare & Alternate Care

- Clinics & Physician Offices

- By Application

- Medication Administration

- Fluid & Nutrition Administration

- Blood Transfusion

- Diagnostic Testing & Imaging Contrast

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand pool and to ground assumptions in public data that can be checked by readers. We leaned on sources such as the US CDC for infection prevention guidance, the US FDA for device and safety communications, and the WHO for treatment and patient safety references that influence IV access practices.

For utilization and setting mix, we referred to sources such as OECD health statistics, CMS and NHS level publications where available, and peer reviewed articles in vascular access and infusion therapy journals that report catheter dwell time, complication rates, and safety catheter adoption. Company filings, investor presentations, and reputable press were used to understand portfolio focus and pricing direction, and paid subscription data for company financials, patents, and shipment level import export checks supported cross validation when public data was thin. These are illustrative examples, and many other public and paid sources were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating real world usage patterns for peripheral IVs, because practice varies by country, care setting, and clinical protocol. We spoke with clinicians involved in vascular access, procurement and materials leaders, and distributor or channel participants across APAC, EMEA, and the Americas to confirm assumptions on average catheter consumption per admission, safety feature penetration, and typical price bands. We then checked outlier points against the broader catheter utilization discussion before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 47% |

| Mid tier: 47% | Functional/Unit leaders: 34% | EMEA: 29% |

| Smaller Players: 15% | Managers: 52% | Americas: 24% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build where admission volumes and procedure volumes are converted into a yearly catheter demand pool, and then refined by setting mix across hospitals and ambulatory centers. To keep the totals realistic, we corroborated results with selective bottom-up checks, such as sampled ASP by country times estimated unit volumes, plus channel feedback on annual consumption in high use facilities.

Key inputs that shaped the model included inpatient admissions and outpatient visit trends, IV line utilization rates by care setting, average catheters used per patient episode (including replacement frequency), the mix shift toward safety PIVCs, and price dispersion by region and tendering structure. Where public series did not break out peripheral IV usage cleanly, gaps were handled by using peer reviewed utilization ranges, followed by validation through primary respondents and sensitivity checks on the most variable parameters.

Forecasts were built using scenario analysis supported by short time series trend smoothing for admissions and utilization indicators, and then adjusted based on expert views on safety regulation adoption, staffing constraints in infusion therapy, and hospital purchasing cycles. The final trajectory reflects a practical mid case rather than an aggressive stretch case, so clients can map it to planning assumptions without relying on hard-to-observe inputs.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including demand pool math, pricing direction, and region level adoption trends for safety catheters. Variance checks were run to spot unusually high implied per patient usage, extreme ASP moves, or growth rates that did not match hospital activity indicators, and any anomalies were reviewed in a separate analyst pass before sign off.

The report is refreshed annually, and interim updates are triggered when a material event can shift volumes or pricing, such as major regulatory actions, supply disruptions, or a large technology transition. Before delivery, we do a final fact check pass so clients receive the most current view available at the time of purchase.

Mordor Intelligence's Peripheral Intravenous Catheters Market Estimate Compared With Other Published Estimates

Published sizes for peripheral intravenous catheters often do not line up, even when the growth story sounds similar, because the counted product set and the unit definition can change quietly over time. Differences can also come from the year used, currency timing, and whether estimates are anchored on procedures or on supplier revenue.

The main gap comes from whether central and midline catheters, as well as administration accessories, are rolled into the same number. Mordor Intelligence treats the market as PIVC devices only, and keeps adjacent vascular access and IV consumables out, which then changes the implied unit volumes and ASP ladders used in the model.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.54 B (2026) | |

| Industry Publisher A | USD 1.96 B (2024) | Uses a narrower priced device definition that appears closer to commodity short PIVCs, with limited visibility on safety PIVC pricing and setting mix, which can compress the revenue base for the same utilization pool. |

| Industry Publisher B | USD 1.06 B (2024) | Leans on a product scope that overlaps with PICC related categories and then reports a separate peripheral IV number, which can fragment unit counts and understate the value captured in integrated or closed PIVC systems. |

The spread in published values is largely explained by scope choices and how utilization is converted into revenue, rather than by disagreement on basic healthcare activity trends. By keeping the counted products tied to peripheral IV devices and checking assumptions like replacement frequency and safety mix with field feedback, the estimate stays traceable to a repeatable demand pool and pricing logic.

Key Questions Answered in the Report

What is the current value of the peripheral intravenous catheters market?

The market is valued at USD 6.54 billion in 2026 and is projected to grow to USD 8.95 billion by 2031.

Which segment is expanding fastest within the peripheral intravenous catheters landscape?

Ambulatory surgical centers lead growth, projected at 9.35% CAGR through 2031 as care shifts to outpatient settings.

How large is North America's share of peripheral intravenous catheter demand?

North America accounted for 39.88% of global revenue in 2025, driven by more than 300 million catheter units used annually in the United States.

What technological trend is reshaping catheter purchasing decisions?

Safety and blood-control designs dominate procurement, capturing 67.95% revenue in 2025 and rising at 8.54% CAGR.

Why are midline catheters gaining popularity?

Midlines offer extended dwell times with lower infection risk than central lines, fueling an 8.21% CAGR through 2031.

How are sustainability concerns influencing the catheter sector?

EU and North American regulators are integrating life-cycle assessments into approvals, prompting manufacturers to explore recyclable and biodegradable materials.

Page last updated on: