Peripherally Inserted Central Catheters Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

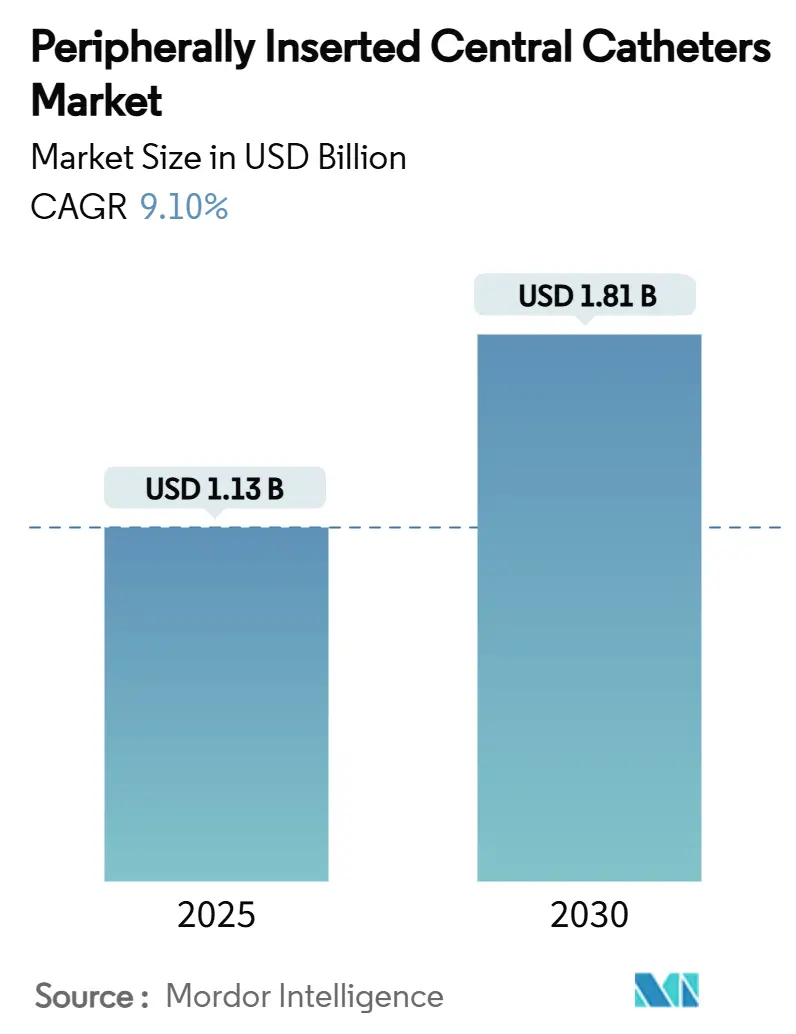

| Market Size (2025) | USD 1.13 Billion |

| Market Size (2030) | USD 1.81 Billion |

| Growth Rate (2025 - 2030) | 9.10% CAGR |

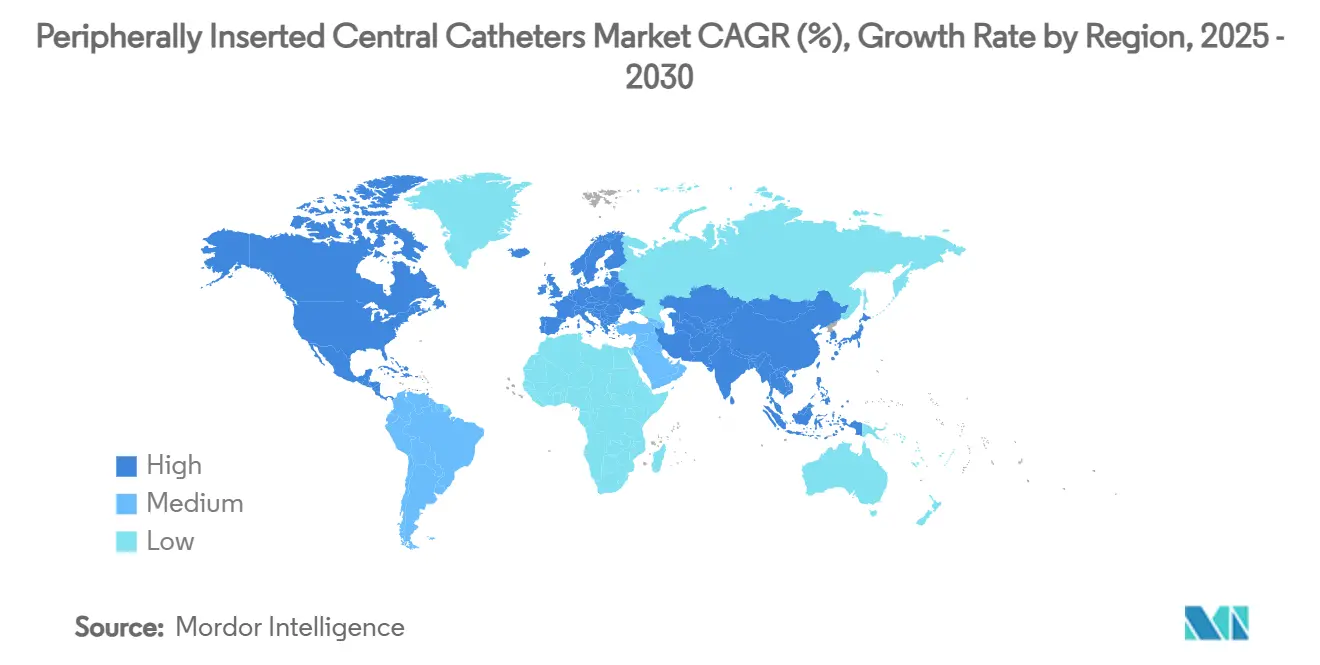

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peripherally Inserted Central Catheters Market Analysis by Mordor Intelligence

The PICC market size is USD 1.13 billion in 2025. It is forecast to advance to USD 1.81 billion by 2030 on a 9.9% CAGR, propelled by oncology‐driven infusion demand, outpatient shift, and hospital mandates to curb central-line infections. Expanding chemotherapy regimens, with 3.2 million U.S. patients receiving infusion therapy each year, elevate procedural volumes and reinforce the need for durable venous access. Providers focus on preventing CLABSI episodes that cost USD 45,814 per event, intensifying clinical stewardship, and catalyzing upgrades to anti-infective materials. Parallel growth stems from power-injectable requirements in CT imaging, where radiology teams prefer catheters capable of 5 mL/s flow rates to streamline diagnostics. Finally, AI-guided navigation systems that raise first-attempt success above 95% shorten procedures and extend PICC adoption into lower-acuity settings.

Key Report Takeaways

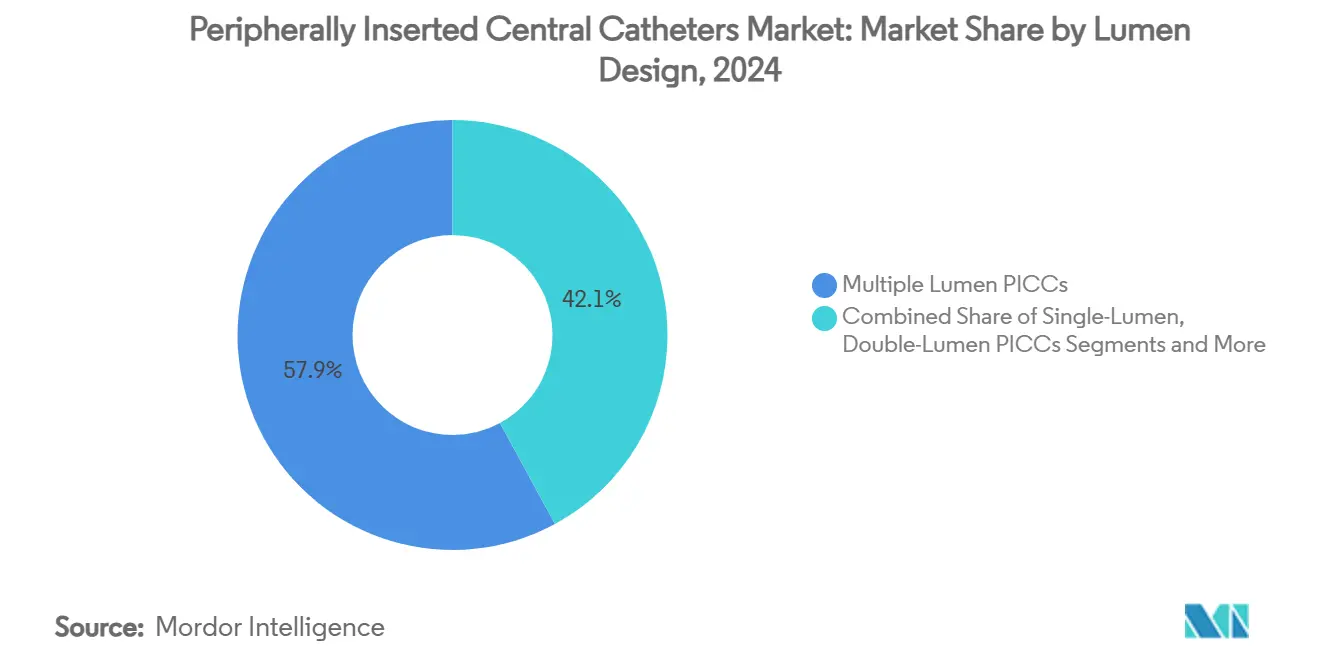

- By lumen design, Multiple-lumen designs led with 57.9% PICC market share in 2024; triple-lumen devices are projected to grow at 7.9% CAGR through 2030 as complex regimens become routine.

- By material, Polyurethane held 70.3% of the PICC market size in 2024, while hydrophilic polymer catheters posted the fastest 9.4% CAGR on superior thromboresistance.

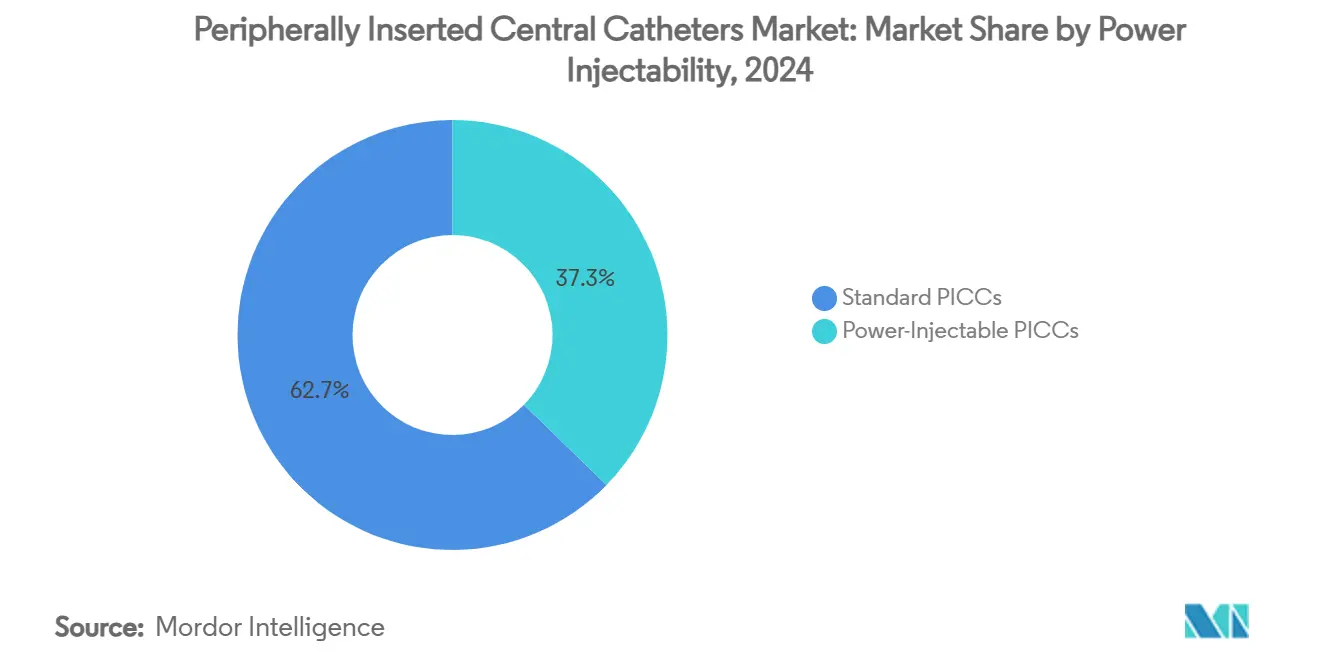

- By power injectability, standard configurations dominated 62.7% of the PICC market in 2024; power-injectable models expand at 8.3% CAGR on imaging demand.

- By end user, hospitals accounted for 68.5% of the PICC market size in 2024; home care settings recorded an 8.8% CAGR on post-COVID patient preference.

- Geographically, North America led with 38.9% PICC market share in 2024, whereas Asia-Pacific registers the quickest 7.6% CAGR to 2030.

Global Peripherally Inserted Central Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cancer & long-term infusion prevalence | +2.10% | North America & Europe lead, global impact | Long term (≥ 4 years) |

| Expansion of outpatient & home infusion | +1.80% | Global; North America accelerates post-COVID | Medium term (2-4 years) |

| Shift toward power-injectable imaging | +1.30% | North America & EU front-runner, APAC catching up | Medium term (2-4 years) |

| Hospital push to cut CLABSI | +1.70% | Developed markets strongest | Short term (≤ 2 years) |

| Adoption of hydrophilic polymer PICCs | +1.50% | Early uptake in North America & EU | Long term (≥ 4 years) |

| AI-guided catheter navigation | +1.00% | North America leads, selective EU adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cancer & Long-Term Infusion Prevalence

The sustained climb in global oncology incidence cements chemotherapy as a core volume driver for the PICC market. Combination drug regimens often demand parallel lumens to avoid incompatibilities, reinforcing multi-lumen selection. Older patients with fragile veins magnify the need for central lines that can dwell beyond 30 days, where PICCs offer cost advantages over implantable ports. Studies report equivalent safety between PICCs and ports but note easier insertion and immediate usability with PICCs. Consequently, oncology wards prioritize training and inventory for flexible lumen options that simplify dose cycling.

Expansion of Outpatient & Home-Infusion Programs

Ambulatory infusion spending is tracking toward USD 142 billion by 2027, reinforcing demand for central catheters, patients can self-manage after discharge. Home therapy cuts institutional cost by up to 50% while boosting satisfaction, but dependability becomes critical because clinical rescue is distant. Manufacturers answer with kink-resistant polymers and antimicrobial hubs that limit maintenance. U.S. Medicare CPT codes 36569, 36571, and 36573 now pay for nurse visits and supplies, softening economic barriers.

Shift Toward Power-Injectable Imaging Protocols

Radiology workflows increasingly stipulate catheters that tolerate 300 psi pressures and 5 mL/s flow, sparking an 8.3% CAGR in power-injectable sales. Using a single vascular access for therapy and imaging reduces sticks, accelerates scans, and shortens the length of stay. Testing shows 5F and 7F polyurethane lines withstand contrast injection, but 3F variants fail, guiding purchase decisions.[1]Journal of Computer Assisted Tomography, “Assessing the Adequacy of Peripherally Inserted Central Catheters for Power Injection of Intravenous Contrast Agents for CT,” journals.lww.com Integration of power capability with hydrophilic surfaces is the next performance frontier.

Hospital Drive to Cut CLABSI Via PICC Stewardship

Each central line infection costs U.S. hospitals USD 45,814; accordingly, facilities embed daily necessity checks and chlorhexidine dressings into care bundles. A meta-analysis shows a 20-70% reduction in CLABSI when bundles are rigorously applied. Device makers respond with integrated securement wings, antimicrobial cuffs, and transparent caps that align with protocol requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Catheter-related bloodstream infection risk | -1.40% | Higher in resource-limited facilities | Short term (≤ 2 years) |

| Midline substitution for ≤ 14-day therapy | -1.80% | North America & Europe spearhead | Medium term (2-4 years) |

| Polyurethane supply chain volatility | -0.90% | Global; Asian resin plants concentrated | Short term (≤ 2 years) |

| Reimbursement pressure in low-income markets | -1.10% | Emerging APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Catheter-Related Bloodstream Infection Risk

Systematic reviews still report 1.6% infection and 7.0% occlusion even with current devices, creating clinician caution, especially where nurse-to-patient ratios are low. Resistant pathogens such as Candida auris further complicate therapy, emphasizing the call for antimicrobial coatings. Guidelines now press daily evaluation and early removal, capping dwell duration in some hospitals and tempering procedural growth.

Rising Midline Catheter Substitution for ≤ 14-Day Therapy

Randomized data show midlines reach similar therapeutic goals with fewer bloodstream infections for short courses, prompting protocol revisions.[2]JAMA Network Open, “Safety and Efficacy of Midline vs Peripherally Inserted Central Catheters Among Adults Receiving IV Therapy,” jamanetwork.com B. Braun’s FDA-cleared Introcan Safety 2 device allows deeper peripheral placement up to 5.7 days, chipping away at standard PICC indications. Economic teams favor midlines due to lower insertion cost and reduced radiology involvement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lumen Design: Versatile Access Dictates Preference

Multi-lumen formats captured 57.9% of the PICC market share in 2024. Triple-lumen lines command the highest growth at 7.9% CAGR to 2030, reflecting complex anti-cancer protocols that require incompatible drug co-administration. The PICC market size for single-lumen devices is stable in pediatric sepsis and outpatient antibiotic therapy, where reduced diameter lowers thrombosis risk. Double-lumen lines strike a balance, supplying blood sampling capability without increasing outer diameter excessively.

Combination therapies and parenteral nutrition converge to lift lumen counts. ECG-conductive tips drive 99.3% first-attempt accuracy, which is critical as the catheter outer diameter rises. Bundle compliance—specifically, flushing and locking protocols—preserves patency and extends dwell, ensuring multi-lumen performance offsets thrombotic concerns.

By Material: Hydrophilic Composites Challenge Status Quo

Polyurethane held 70.3% of the PICC market share in 2024, owing to low cost and manufacturability. Ye,t hydrophilic hydrogel composites post 9.4% CAGR as providers link surface chemistry to lower failure. The PICC market size attached to silicone remains niche in neonatal and renal applications, where flexibility is paramount but lacks power-injectable tolerance. Other materials, including hybrid polyurethane-siloxane matrices, are under evaluation for simultaneous strength and biocompatibility.

Clinical data highlight zero occlusion with hydrogel composites, swaying value-analysis committees toward premium spend. Supply disruptions in PTFE push procurement teams to qualify alternative polymers, incidentally accelerating the adoption of new chemistries.

By Power Injectability: Imaging Requirements Fuel Demand

Standard devices sustained a 62.7% PICC market share in 2024 due to routine infusion volumes. Power-injectable variants grew at an 8.3% CAGR as imaging protocols cement 5 mL/s flow prerequisites. The PICC market size tied to power-injectable formats spans oncology, trauma, and critical care, where CT angio is frequent.

Cost analysis shows one power-injectable line displaces multiple peripheral sticks, cutting consumables and accelerating diagnosis. Manufacturers now pair hydrophilic coatings with high-pressure fittings to deliver a dual benefit: better biocompatibility and imaging capability.

By End User: Home Care Disrupts Traditional Flows

Hospitals absorbed 68.5% of PICC market revenue in 2024 on the back of inpatient oncology and ICU use. Yet home care settings advance 8.8% CAGR as telehealth oversight and nursing networks expand. The PICC market share for ambulatory surgical centers is widening because same-day placement models lower procedural cost and free hospital OR time.

Medicare reimbursement for home infusion supplies via CPT code 36571 improves access. Device makers package maintenance kits with clear patient instructions, and AI-enabled tip confirmation lets trained nurses place PICCs without fluoroscopy, fitting the outpatient environment.

Geography Analysis

North America held 38.9% PICC market share in 2024, underpinned by broad reimbursement and stewardship programs that place infection prevention at center stage. CMS quality metrics link payment to CLABSI rates, encouraging procurement of antimicrobial and hydrophilic innovations. BD signaled 12.7% vascular access revenue growth in Q2 2025, reflecting provider appetite for premium lines. Regulatory clarity also accelerates device rollouts, exemplified by the Class II designation for force-activated separation accessories in August 2024.[3]Federal Register, “Medical Devices; Classification of the Intravenous Catheter Force-Activated Separation Device,” federalregister.gov

Asia-Pacific registers the fastest 7.6% CAGR on aging demographics and rising chronic disease burden. China’s clinical studies document successful PICC use in frail elderly, validating broader uptake. Japan and Australia maintain stringent approval pathways that favor well-documented devices, while India’s growing private hospital network prefers value-optimized polyurethane lines. Manufacturers tailor portfolios consequently, offering cost-controlled standard PICCs alongside flagship hydrophilic models for tier-1 centers.

Europe exhibits steady but slower expansion as mature markets emphasize cost-effectiveness. The Medical Device Regulation imposes post-market surveillance obligations, raising compliance cost yet elevating product quality. Infection-control initiatives under the European Centre for Disease Prevention and Control align with hospital drive to adopt antimicrobial dressings, supporting gradual replacement cycles. Middle East & Africa and South America contribute incremental demand; Brazil’s economic upswing increased catheter sales despite infrastructure gaps.

Competitive Landscape

The PICC market demonstrates moderate consolidation as diversified med-tech majors reposition around high-margin, technology-heavy portfolios. BD’s USD 4.2 billion acquisition of Edwards Lifesciences’ Critical Care Product Group expands smart-connected care, enriching bundled vascular solutions. Teleflex’s EUR 760 million takeover of BIOTRONIK’s vascular interventions business brings drug-coated balloons and stents, cementing cross-selling leverage with its Arrow PICC line.

AngioDynamics’ USD 45 million divestiture of its PICC portfolio to Spectrum Vascular signals a strategic pivot toward endovascular thrombectomy and oncology platforms. Patent settlements remain pivotal: the 2025 BD–AngioDynamics accord involves USD 7 million upfront and USD 2.5 million annually, ending litigation over Bard IP and stabilizing U.S. share dynamics.

Competition now focuses less on unit price and more on clinical outcomes. Sherlock 3CG’s procedural time cut from 176 minutes to 34 minutes illustrates value-based selling that resonates with hospital administrators. Start-ups pursue antimicrobial and hydrophilic niches; Access Vascular’s MIMIX polymer earned citation in updated Infusion Nurses Society standards, lending guideline leverage for adoption.

Peripherally Inserted Central Catheters Industry Leaders

Becton, Dickinson & Co.

Teleflex Inc.

AngioDynamics Inc.

Cook Medical LLC

ICU Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed its EUR 760 million acquisition of BIOTRONIK’s vascular intervention unit, adding drug-coated balloons and stents to its catheter franchise.

- June 2025: BD and AngioDynamics settled their Bard patent dispute; AngioDynamics will pay USD 7 million upfront plus USD 2.5 million annually through Feb 2029.

- February 2025: BD announced its intent to separate its Biosciences and Diagnostic Solutions arm to intensify its focus on medical technology, including PICCs.

- September 2024: B. Braun obtained FDA clearance for the Introcan Safety 2 Deep Access IV Catheter targeting mid-term therapies.

Global Peripherally Inserted Central Catheters Market Report Scope

| Single-Lumen PICCs |

| Double-Lumen PICCs |

| Triple/Multi-Lumen PICCs |

| Polyurethane PICCs |

| Silicone PICCs |

| Hydrophilic Polymer/Hydrogel PICCs |

| Other Materials |

| Standard PICCs |

| Power-Injectable PICCs |

| Hospitals |

| Ambulatory Surgical Centers |

| Oncology & Specialty Clinics |

| Home Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Lumen Design | Single-Lumen PICCs | |

| Double-Lumen PICCs | ||

| Triple/Multi-Lumen PICCs | ||

| By Material | Polyurethane PICCs | |

| Silicone PICCs | ||

| Hydrophilic Polymer/Hydrogel PICCs | ||

| Other Materials | ||

| By Power Injectability | Standard PICCs | |

| Power-Injectable PICCs | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Oncology & Specialty Clinics | ||

| Home Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current PICC market size and 2030 outlook?

The PICC market size stands at USD 1.13 billion in 2025 and is projected to reach USD 1.81 billion by 2030 on a 9.9% CAGR.

Which lumen configuration leads usage?

Multiple-lumen designs hold 57.9% share, with triple-lumen variants rising fastest at 7.9% CAGR through 2030.

Why are power-injectable PICCs gaining popularity?

Radiology protocols require 5 mL/s contrast injection, and power-injectable PICCs let clinicians perform imaging via the existing line, cutting extra sticks and time.

How are home-infusion trends influencing PICC demand?

Home care settings post an 8.8% CAGR because patients prefer outpatient therapy and Medicare codes cover associated nursing and supplies.

Which material innovation is most disruptive?

Hydrophilic hydrogel composites demonstrate zero catheter occlusion in clinical studies, driving a 9.4% CAGR as hospitals weigh reduced complication costs.

What score reflects the competitive concentration of PICC suppliers?

A score of 6 indicates that the top players command about 60% of sales, leaving room for niche innovators to gain ground.

Page last updated on: