Europe Urinary Catheters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

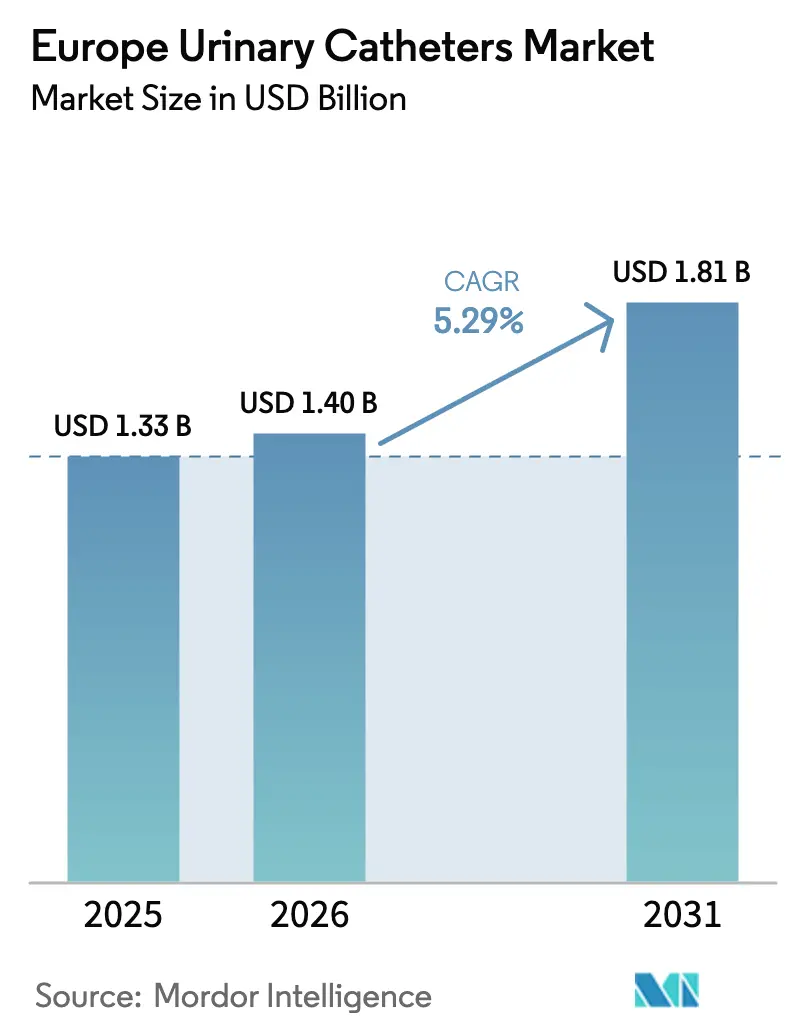

| Base Year Market Size (2025) | USD 1.33 Billion |

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

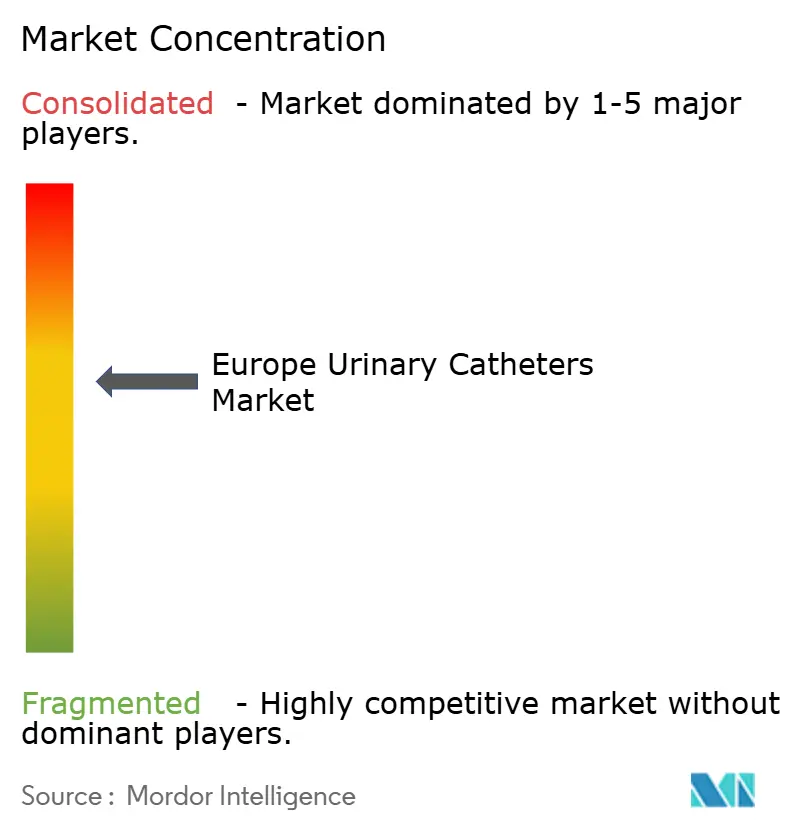

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Urinary Catheters Market Analysis by Mordor Intelligence

Europe urinary catheters market size in 2026 is estimated at USD 1.40 billion, growing from 2025 value of USD 1.33 billion with 2031 projections showing USD 1.81 billion, growing at 5.29% CAGR over 2026-2031. Growth reflects a confluence of demographic aging, tightening infection-control protocols, and manufacturer investment in advanced coatings that lower catheter-associated urinary tract infection (CAUTI) risk. Early removal strategies after surgery are lowering UTI incidence by 32% without harming patient safety, yet they also stimulate demand for specialized short-dwell devices. Regulatory change compounds these forces: manufacturers must now budget for EU MDR and post-Brexit UKCA submissions while simultaneously preparing for a per- and polyfluoroalkyl substances (PFAS) phase-out that threatens legacy PTFE-coated models. Hospitals remain the principal buyers, but home-care demand is rising as tele-urology services support intermittent self-catheterization. Competitive positioning therefore centers on coating science, regulatory readiness, and sustainability credentials in order to secure purchasing contracts across Europe’s reimbursement-driven health systems.

Key Report Takeaways

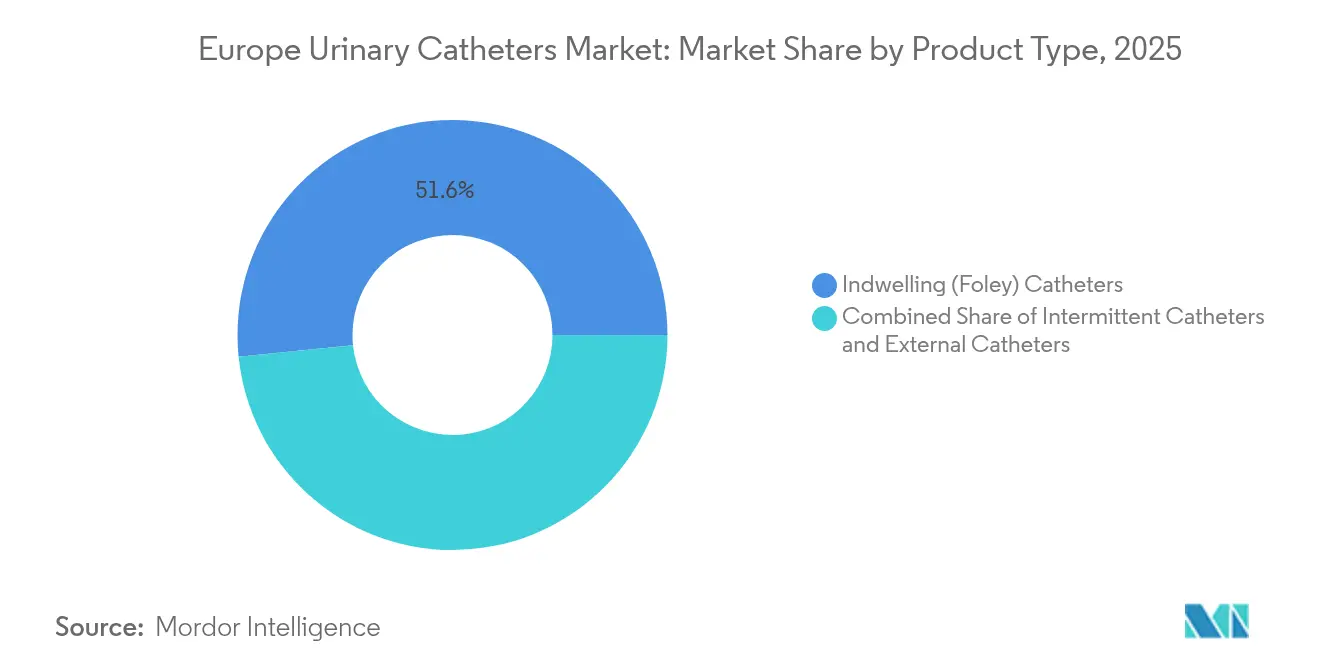

- By product type, indwelling Foley catheters led with 51.62% of Europe urinary catheters market share in 2025, while intermittent catheters are expected to grow at 5.67% CAGR through 2031.

- By application, urinary incontinence accounted for 41.88% of the Europe urinary catheters market size in 2025, whereas spinal cord injury cases are projected to advance at 6.42% CAGR to 2031.

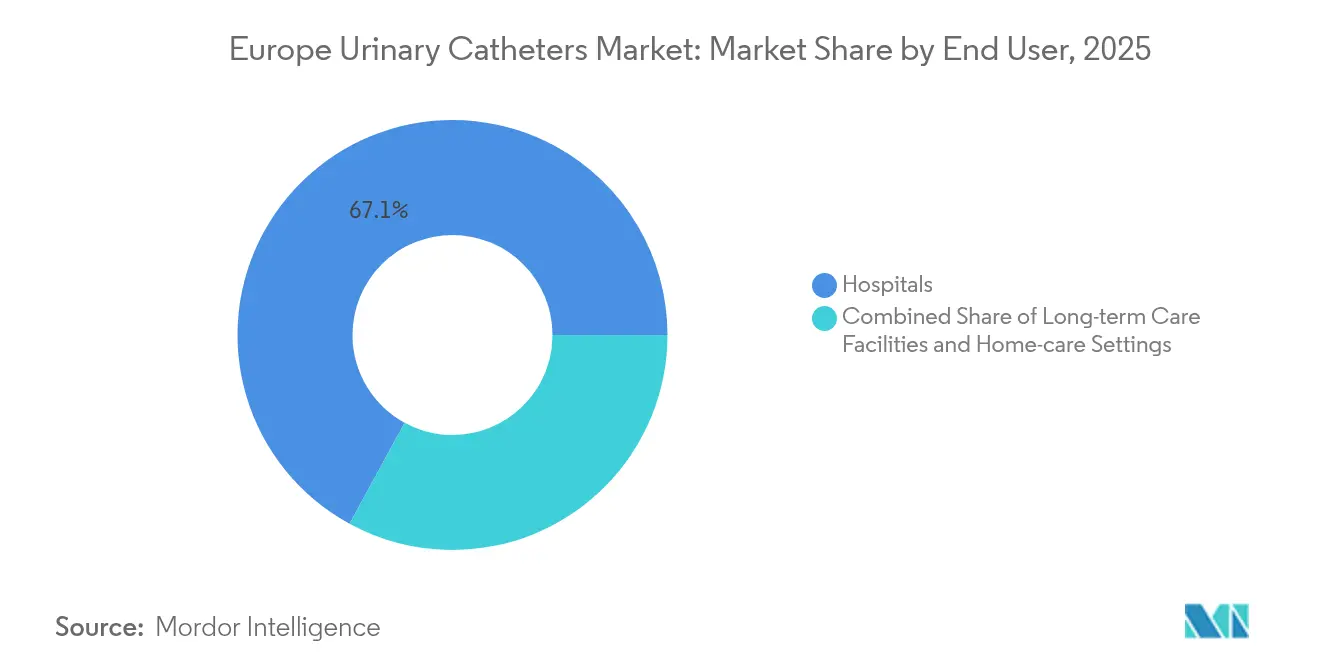

- By end user, hospitals held 67.05% revenue share in 2025; home-care settings register the fastest expansion at 6.86% CAGR to 2031.

- By gender, females represented 64.96% of 2025 sales, yet the male segment is forecast to post a 6.05% CAGR through 2031.

- By country, Germany commanded 22.33% of 2025 revenue while the United Kingdom is projected to grow at 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on urinary catheters market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Urinary Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Age-linked surge in urinary incontinence cases | +1.8% | Germany, Italy, Spain | Long term (≥ 4 years) |

| Higher post-surgical catheterization rates | +1.2% | Major surgical centers | Medium term (2-4 years) |

| National reimbursement for self-catheter kits | +0.9% | Germany, France, UK | Medium term (2-4 years) |

| Surge in antimicrobial-coated catheter adoption | +0.7% | Hospital-dense EU regions | Short term (≤ 2 years) |

| Impending EU eco-design and MDR amendments | +0.4% | EU-wide | Long term (≥ 4 years) |

| Tele-urology boosting home-based intermittent use | +0.5% | Nordic countries, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demographic shifts and rising urinary incontinence prevalence

Europe’s population aged 65 and older continues to expand, and the prevalence of incontinence has reached 76.5% among nursing-home residents in recent Spanish multicenter studies [1]Luque-Fernández, “Prevalence of Urinary Incontinence in Spanish Nursing Homes,” BMC Geriatrics, biomedcentral.com. On the payer side, Germany’s statutory system reimburses incontinence aids with a 10% co-payment capped at EUR 10 per month, eliminating meaningful cost barriers to catheter access. Because incontinent individuals experience healthcare costs four times those of continent peers, clinicians and payers treat catheter access as a cost-containment tool. Southern European cultures that once relied on family caregivers now confront institutional capacity limits, which further lifts demand. These demographic realities underpin the long-term expansion outlook for the Europe urinary catheters market.

Post-surgical catheterization protocol evolution

Surgical volumes have rebounded after COVID-19, but infection-control data drive earlier catheter removal. Meta-analysis shows that removal within 24 hours after vaginal procedures cuts UTI rates and shortens stays by up to three days. German orthopedic centers reduced catheter use from 62% to 38% and lowered infection rates from 4.7% to 1.2% when restrictive protocols were adopted [2]Bernhard-Steiner et al., “Restrictive Catheter Use Lowers CAUTI After Arthroplasty,” Antibiotics, mdpi.com. Hospitals consequently seek short-dwell hydrophilic devices that minimize urethral trauma and are compatible with same-day discharge pathways. The shift toward minimally invasive surgery also calls for catheters that deliver precise drainage within tighter time windows, reinforcing the technology-upgrade cycle across the Europe urinary catheters market.

Reimbursement frameworks and tele-urology expansion

Statutory and social-security programs across Germany, France, and the UK reimburse self-catheter kits, with Germany covering up to 200 intermittent catheters per patient each month once HCPCS-aligned codes take effect in January 2026. These policies remove out-of-pocket barriers and stimulate clinical adoption of hydrophilic variants despite premium prices. Tele-urology services supported by Nordic and German insurers allow clinicians to monitor catheterized patients remotely, cutting readmissions and enabling home-based care. The combination of reimbursement certainty and digital supervision accelerates adoption in the Europe urinary catheters market and shifts volume from hospitals to community settings.

Regulatory pressures and antimicrobial innovation

Silver-alloy and other antimicrobial coatings lower CAUTI incidence compared with standard materials, persuading procurement teams to accept higher unit costs when total-cost-of-care is favorable. At the same time, manufacturers shoulder EU MDR audits and UKCA filings, and they must also prepare for an EU-wide PFAS ban that would remove PTFE coatings between 2026 and 2027. These pressures encourage R&D spending on alternative biocompatible coatings. Hospitals are already favoring products that carry both infection-control and sustainability credentials, strengthening the competitive moat for early adopters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent risk of CAUTI | −1.1% | Global | Short term (≤ 2 years) |

| Public tender price ceilings | −0.8% | Southern and Eastern Europe | Medium term (2-4 years) |

| Stringent UKCA/EU MDR certification costs | −0.6% | UK and EU | Short term (≤ 2 years) |

| Proposed PFAS ban | −0.9% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent CAUTI risk and multidrug resistance

Up to 75% of nosocomial UTIs originate from catheter use, and European intensive-care units report CAUTI incidence at 6.99 events per 1,000 patient-days. Multidrug-resistant Klebsiella pneumoniae complicates treatment, prompting clinicians to emphasize catheter avoidance. Nurse-driven removal protocols lower postoperative retention without harming safety, yet they also curb routine use. This safety focus dampens volume growth and forces manufacturers in the Europe urinary catheters market to highlight infection-mitigation data when securing tenders.

Pricing pressures and fluoropolymer regulation

Public hospitals in Southern and Eastern Europe purchase via national tenders that reward the lowest compliant bid, compressing margins on premium devices. Certification requirements under UKCA and EU MDR add cost layers that small suppliers struggle to absorb. Looking ahead, a PFAS ban could eliminate PTFE-coated models unless replacements appear in time, risking supply gaps and forcing buyers to consider alternative materials. Price ceilings and regulatory overhead therefore restrain near-term growth in the Europe urinary catheters market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Indwelling leadership and intermittent momentum

Indwelling Foley catheters accounted for 51.62% revenue in 2025, reflecting entrenched use in acute and long-term care settings. Micro-hole zone technology has improved drainage and virtually eliminated mucosal suction according to randomized assessments, keeping indwelling designs clinically relevant. Yet intermittent devices are projected to register a 5.67% CAGR, the fastest within the Europe urinary catheters market, as clinical guidelines push infection-mitigation strategies and patient autonomy. Hydrophilic-coated variants command premium prices but demonstrate smoother insertion and lower urethral trauma, supporting their inclusion in new reimbursement codes taking effect in 2026.

Emerging external systems such as PureWick widen choice, especially for female users who prefer non-invasive options. Biodegradable materials also gain traction; Wellspect introduced the first eco-labeled catheter manufactured from renewable plastics, supporting net-zero ambitions by 2045. The Europe urinary catheters market size for intermittent solutions is projected to expand faster than indwelling lines, although risk-averse hospitals still depend on Foley designs for perioperative management.

By Application: Incontinence scale confronts neurogenic growth

Urinary incontinence represented 41.88% of 2025 demand, underscoring the weight of aging on the Europe urinary catheters market. German and Italian public insurers finance incontinence aids, so penetration levels already run high. In contrast, spinal cord injury cases, though smaller in volume, are forecast to rise at 6.42% CAGR. Neurologists increasingly prescribe clean intermittent catheterization (CIC) because guideline consensus shows lower infection risk and better renal outcomes compared with indwelling alternatives.

Benign prostatic hyperplasia (BPH) and acute urinary retention also pull-through catheter sales. French interventional centers reported 80.7% successful catheter removal following prostatic artery embolization in elderly patients, confirming that urology advances can still generate short-term catheter needs during recovery. These mixed clinical pathways keep demand diversified, supporting resilience in the Europe urinary catheters market.

By End User: Hospital scale meets home-care acceleration

Hospitals delivered 67.05% of 2025 revenue, supported by perioperative protocols and ICU necessity. Nonetheless, home-care settings should post a 6.86% CAGR as tele-urology platforms allow remote monitoring of intermittent users and reduce readmission costs. Machine-learning algorithms applied to home-collected data already show 65.2% sensitivity for UTI risk prediction among older adults, enabling earlier intervention and supporting payer acceptance.

Long-term care facilities contribute steady baseline demand: German nursing-home audits found 13.4% of residents carrying indwelling catheters, primarily male patients with severe impairment. Growth, however, concentrates in domiciliary care where patient preference and economic logic converge. The Europe urinary catheters market size for home-use products is likely to mirror the shift toward outpatient chronic care.

By Gender: Female volume contrasts male velocity

Females held 64.96% of 2025 sales due to higher incontinence prevalence and longer life expectancy. Yet male consumption is forecast to climb at 6.05% CAGR, driven by rising BPH interventions and gender-specific device innovation. Male users are 2.86 times more likely to require indwelling catheterization following hospitalization, underscoring the clinical gap that suppliers address through male-anatomy-optimized external systems.

Female external catheters such as QiVi FEC appeal to users seeking dignity and infection avoidance. Conversely, ConvaTec’s GentleCath Air for Women extends intermittent portfolios tailored to female urethral length, illustrating growing segmentation. Such gendered design advances should sustain differentiated growth across the Europe urinary catheters market.

Geography Analysis

Germany contributed 22.33% revenue in 2025 because statutory insurance covers catheter supplies with minimal copayments, ensuring consistent uptake across inpatient and outpatient settings. The United Kingdom, projected at 7.12% CAGR, benefits from UKCA’s streamlined innovation pathway and NHS procurement reform that elevates total-cost-of-care metrics over headline unit price .

The United Kingdom supplies the fastest CAGR at 7.12% through 2031. UKCA regulation gives compliant firms a head start while non-compliant competitors face market exit. NHS supply frameworks increasingly weigh life-cycle cost against headline price, permitting antimicrobial or hydrophilic devices to out-compete commodity lines when infection-reduction savings are demonstrated. Domestic assembly investment is rising as firms insulate themselves from cross-border frictions. These factors together underpin robust growth within the Europe urinary catheters market.

Southern Europe—France, Italy, Spain—shows structural demand tied to aging populations yet confronts budget caps that filter premium adoption via strict tender ceilings. Nonetheless, the economic burden of incontinence, valued at EUR 69 billion in 2023 and projected to rise 25% by 2030, forces policymakers to consider cost-effective catheter solutions that prevent hospitalizations. Eastern Europe represents white-space opportunity as hospital modernization programs improve funding pathways. Manufacturers that marry competitive price points with MDR compliance can secure early share in these growth pockets.

Competitive Landscape

The Europe urinary catheters market displays moderate concentration. Top regional suppliers such as Coloplast, B. Braun, BD, Teleflex, Hollister, Convatec, Wellspect, and Bactiguard hold meaningful share through broad portfolios and regulatory expertise. Wellspect has differentiated through renewable-plastic construction that secured the first eco-label in the category, aligning with hospital sustainability mandates. Boston Scientific’s USD 3.7 billion Axonics acquisition broadens exposure to bladder dysfunction therapies, signalling that consolidation is accelerating around complementary urology assets.

Technology competition hinges on antimicrobial coatings. Silver-alloy catheters reduce CAUTI relative risks, prompting large procurement contracts despite higher upfront cost. External systems such as PureWick gained 88% user satisfaction and lowered caregiver workload, offering a non-invasive alternative that could disrupt indwelling lines.

Regulatory hurdles meanwhile raise barriers for newcomers, favoring incumbents with established MDR and UKCA infrastructure. The looming PFAS ban also redistributes bargaining power toward suppliers that already possess fluoropolymer substitutes. Digital integration—remote monitoring algorithms and smart-packaging that signals usage—represents an emergent differentiator likely to widen gaps between innovation leaders and price-led followers.

Europe Urinary Catheters Industry Leaders

Coloplast Corp

B. Braun SE

Hollister Incorporated

Bactiguard AB

Convatec Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Convatec broadened its me+ program in the UK to support intermittent catheter users and clinicians, enhancing patient education and follow-up.

- May 2024: Coloplast extended its Luja range with a next-generation female intermittent catheter designed to enable single-flow bladder emptying and lower UTI risk.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe urinary catheters market as the manufacturer-level revenue from newly produced indwelling (Foley), intermittent, and external catheters that drain the bladder in hospitals, long-term care, and home settings across 32 European economies.

Scope Exclusions: Disposable drainage bags, suprapubic kits, nephrostomy tubes, and peritoneal dialysis catheters are outside this scope.

Segmentation Overview

- By Product Type

- Indwelling (Foley) Catheters

- Intermittent Catheters

- External (Condom) Catheters

- Coated vs Un-coated Catheters

- By Application

- Benign Prostatic Hyperplasia (BPH)

- Urinary Incontinence

- Spinal Cord Injury

- Acute Urinary Retention & Others

- By End User

- Hospitals

- Long-term Care Facilities

- Home-care Settings

- By Gender

- Male

- Female

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed urology nurses, procurement managers, and distributor sales leads in Germany, the UK, France, Italy, and Scandinavia. These discussions validated average selling prices, dwell times, and the accelerating switch toward intermittent kits, feeding directly into our model.

Desk Research

We began by extracting annual catheterization episodes, incontinence prevalence, and CAUTI rates from Eurostat, OECD Health Statistics, and national health ministries, giving us dependable demand markers. Trade volumes from UN Comtrade and tariff line 9018.39 clarified cross-border supply, while EUDAMED listings mapped the active CE-marked device base.

Further inputs came from PubMed studies, European Association of Urology papers, company 10-Ks, and paid databases such as D&B Hoovers and Dow Jones Factiva for manufacturer revenue splits. The sources noted are illustrative; numerous additional references guided checks and clarifications.

Market-Sizing & Forecasting

A top-down reconstruction links inpatient and outpatient catheter episodes to device-use multipliers and ASP curves. This is then cross-checked with selective bottom-up supplier roll-ups. Key variables include TURP surgery rates, grade-III incontinence prevalence in 65+ cohorts, average dwell duration, EU MDR-driven cost shifts, and hospital-to-home adoption ratios. Multivariate regression blended with scenario analysis projects each driver; any bottom-up variance beyond five percent triggers re-contact with experts before figures lock.

Data Validation & Update Cycle

Outputs undergo anomaly screens, two-layer peer review, and leadership sign-off. We refresh models annually, issuing interim updates when regulatory, macro, or recall events materially alter a core variable.

Why Mordor's Europe Urinary Catheters Baseline Commands Credibility

Published estimates diverge because firms choose different product baskets, apply varied currency dates, or extend historic ASPs without fresh tender checks.

Key gap drivers include studies that fold in suprapubic or dialysis catheters, freeze reimbursement assumptions, or stretch pandemic-era anomalies that our analysts smooth through quarterly ASP panels. Alternate publications quote values such as USD 1.32 billion for 2022, USD 1.84 billion for 2024, and USD 1.99 billion for 2025.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.33 B (2025) | Mordor Intelligence | - |

| USD 1.32 B (2022) | Regional Consultancy A | Excludes home-care channel; uses 2020 FX rates |

| USD 1.84 B (2024) | Trade Journal B | Adds suprapubic kits and OEM re-exports |

| USD 1.99 B (2025) | Industry Association C | Relies on survey-based ASPs unadjusted for tender caps |

These contrasts show that Mordor's timely price audits, disciplined scope, and documented update cadence deliver the balanced, transparent baseline on which planners can depend.

Key Questions Answered in the Report

How big is the Europe Urinary Catheters Market?

The market was valued at USD 1.40 billion in 2026 and is forecast to reach USD 1.81 billion by 2031.

Which product segment is expanding the fastest?

Intermittent catheters are projected to post a 5.67% CAGR through 2031 owing to infection-prevention advantages.

Who are the key players in Europe Urinary Catheters Market?

Coloplast Corp, B. Braun SE, Hollister Incorporated, Bactiguard AB and Convatec Inc. are the major companies operating in the Europe Urinary Catheters Market.

Why is the United Kingdom the fastest-growing country market?

Post-Brexit UKCA pathways and NHS procurement reform are accelerating adoption of premium, compliant devices, driving a 7.12% CAGR.

Page last updated on: