United States SMS Marketing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 9.99 Billion |

| Market Size (2030) | USD 28.19 Billion |

| Growth Rate (2025 - 2030) | 23.05% CAGR |

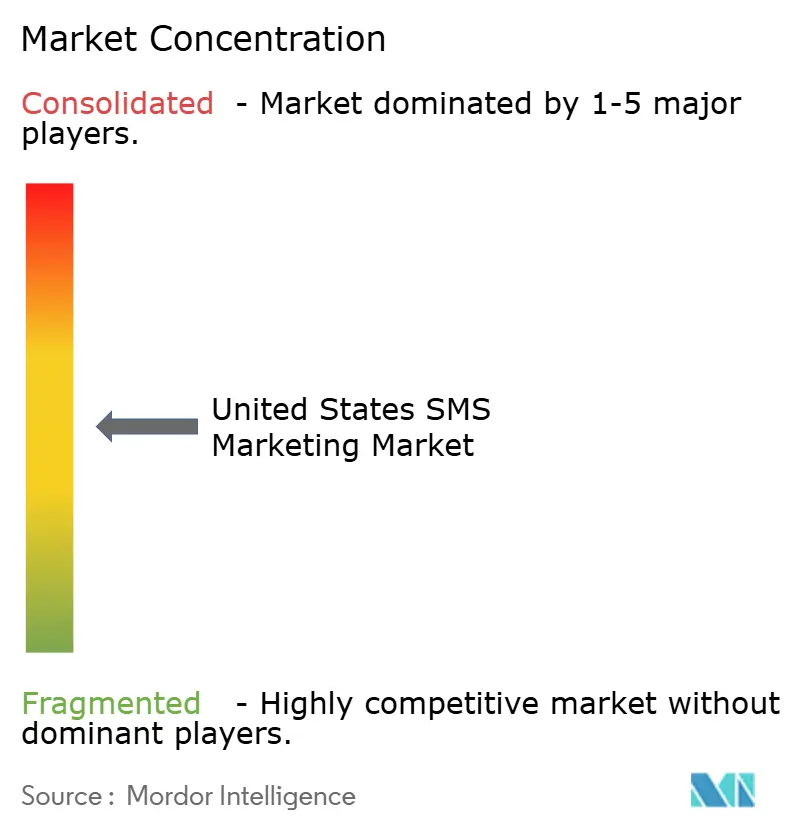

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States SMS Marketing Market Analysis by Mordor Intelligence

The United States SMS Marketing market size is estimated at USD 9.99 billion in 2025 and is projected to reach USD 28.19 billion by 2030, growing at a 23.05% CAGR from 2025 to 2030. Rising smartphone penetration, unlimited-text plans, and the nationwide shift to 10DLC registration have moved text messaging from a low-cost alert tool to a strategic engagement channel. Marketers increasingly weave SMS into omnichannel stacks to offset email saturation and third-party cookie deprecation, while AI personalization tools lift click-through rates and return on ad spend. Cloud platforms dominate delivery because they scale to growing campaign volumes and streamline TCPA compliance. Competitive intensity remains moderate as global CPaaS vendors defend their share against e-commerce specialists and vertical-focused challengers; yet, escalating carrier pass-through fees and message fatigue pose near-term headwinds for the United States SMS Marketing market.

Key Report Takeaways

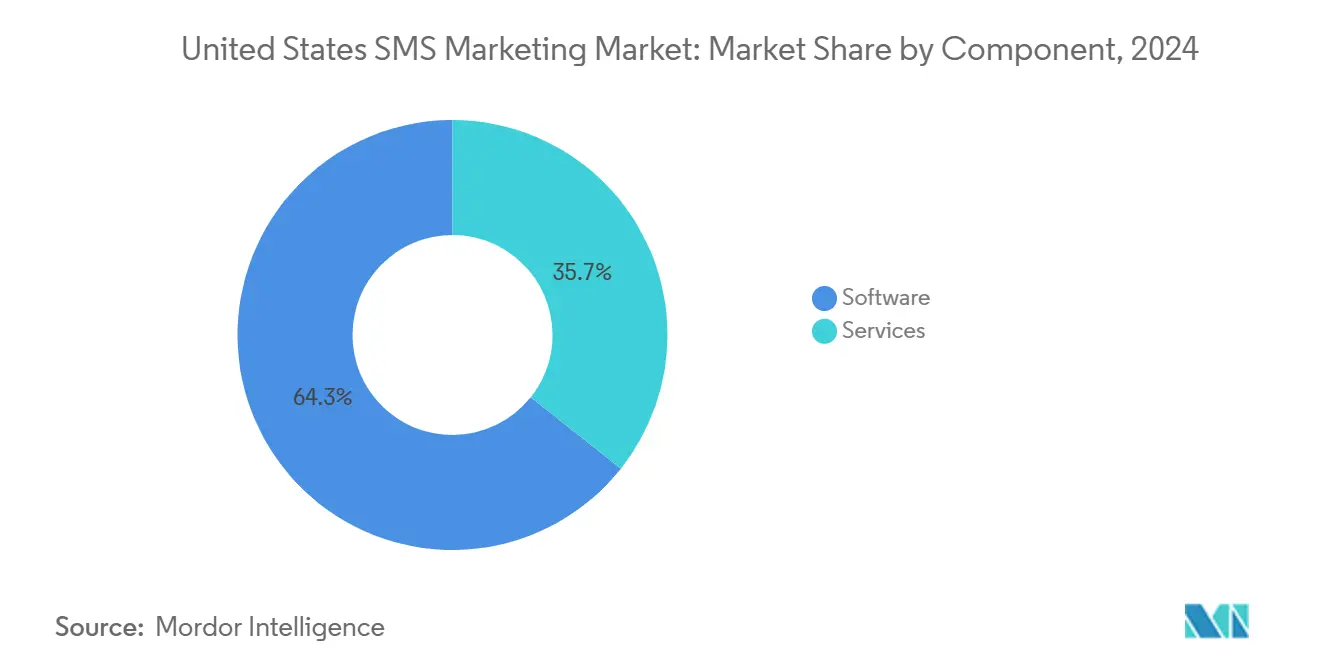

- By component, software led with a 64.32% share of the United States SMS Marketing market in 2024; services are projected to expand at a 24.87% CAGR through 2030.

- By enterprise size, large enterprises accounted for 57.89% of the United States' SMS Marketing market size in 2024. Small and medium-sized enterprises are poised to grow at a 24.94% CAGR through 2030.

- By deployment mode, cloud-based solutions accounted for 74.53% of the United States' SMS Marketing market size in 2024; cloud implementations are expected to maintain a 24.71% CAGR through 2030.

- By industry vertical, retail and e-commerce captured 23.87% revenue share in 2024; healthcare is forecast to expand at a 23.24% CAGR to 2030.

United States SMS Marketing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust smartphone and unlimited-text adoption | +4.2% | Nationwide, stronger in South and West | Medium term (2-4 years) |

| Omnichannel engagement stack integration | +5.8% | Metro areas across all regions | Long term (≥ 4 years) |

| Mandatory 10DLC A2P compliance | +3.7% | Nationwide, stricter in Northeast and West | Short term (≤ 2 years) |

| AI-driven personalization | +6.1% | Early adoption in West and Northeast | Medium term (2-4 years) |

| First-party data urgency | +2.9% | Digital-first states | Short term (≤ 2 years) |

| RCS fallback enablement | +1.8% | Dependent on carrier coverage nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Smartphone and Unlimited-Text Adoption

Near-universal smartphone ownership, paired with unlimited-text plans, removes per-message cost barriers, making SMS a scalable engagement channel. Carriers already handle more than 613 million daily RCS messages, demonstrating sufficient network headroom to support expanding campaign volumes. [1]Infobip, “Global Mobile Messaging Report 2024,” INFOBIP.COM Enterprises consequently design multi-step nurture flows that once required email, thereby deepening reliance on the United States SMS Marketing market.

Omnichannel Engagement Stack Integration

Marketers now embed SMS triggers inside customer-data platforms and journey builders, which lifts channel response by aligning timing with real-time behaviors. Klaviyo reports 29× higher revenue per recipient for SMS relative to email when the two channels are orchestrated together. [2]Klaviyo, “SMS vs Email Marketing,” KLAVIYO.COM The United States SMS Marketing market benefits because integration complexity encourages platform standardization on full-featured CPaaS offerings.

Mandatory 10DLC A2P Compliance

The carrier-led shift from peer-to-peer routes to registered 10DLC campaigns formalizes brand identity, restricts spam, and allocates dedicated throughput. Compliance imposes registration fees and operational overhead that smaller providers struggle to absorb, thereby consolidating revenue toward established vendors and supporting long-term expansion of the United States SMS Marketing market.

AI-Driven Personalization

Large-language-model capabilities within SMS platforms enable predictive send times, copy variations, and next-best-offer logic, which increase click-through rates and reduce opt-outs. Within three months of launch, more than 25% of Klaviyo customers adopted generative audience tools, underscoring the rapid commercial uptake. These gains reinforce marketers' preference for the United States SMS Marketing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carrier pass-through fee escalation | -2.8% | Nationwide, heavier on high-volume senders | Short term (≤ 2 years) |

| TCPA class-action litigation risk | -1.9% | Higher exposure in Northeast and West | Medium term (2-4 years) |

| Rising consumer opt-out rates | -1.4% | Urban centers with saturated channels | Medium term (2-4 years) |

| Competition from in-app and push alerts | -1.2% | Digitally mature industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carrier Pass-Through Fee Escalation

Major carriers introduced A2P surcharges that inflate per-message economics and complicate budget forecasting. Twilio separates these fees from organic revenue because of their material impact, signaling direct margin pressure for brands. Smaller senders, lacking volume discounts, feel the sharpest cost shock, potentially tempering overall traffic growth within the United States SMS Marketing market.

TCPA Class-Action Litigation Risk

Settlements involving Fashion Nova and other retailers highlight the costly consequences of consent mismanagement. [3]Reuters, “Fashion Nova agrees to settle TCPA class action over text messages,” REUTERS.COM The fear of litigation prompts brands to moderate their campaign cadence and invest in compliance tooling, which adds friction to adoption, even as it opens up service revenue opportunities for specialized providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Underpin Revenue

Software accounted for 64.32% of the United States SMS Marketing market size in 2024, reflecting demand for automation, analytics, and omnichannel orchestration features. Professional services, although smaller, are expected to outpace software with a 24.87% CAGR to 2030, as enterprises hire specialists to configure integrations, manage consent, and design AI-driven journeys. The software layer captures recurring subscription revenue while services monetize expertise, together forming the operational backbone of the United States SMS Marketing market.

Between 2025 and 2030, services are expected to expand as stringent TCPA audits and complex 10DLC registrations require hands-on guidance. API-centric vendors position consulting as a margin enhancer, offsetting the volatility of carrier surcharges. As AI features mature, services teams will tune models for industry-specific language and compliance, keeping the United States SMS Marketing market on a capability-driven growth path.

By Enterprise Size: SME Uptake Accelerates

Large enterprises retained 57.89% of the United States SMS Marketing market share in 2024, leveraging high-volume throughput and advanced segmentation to support nationwide campaigns. Yet SMEs deliver faster revenue growth, at a 24.94% CAGR, because self-service interfaces compress onboarding time, and subscription tiers align with smaller budgets. This democratization widens the addressable base of the United States SMS Marketing market and diversifies revenue concentration.

SMEs prioritize ease of use and pre-built ecommerce integrations, enabling stores on Shopify or WooCommerce to launch campaigns in minutes. Podium and other localized platforms demonstrate how quickly value can be created for non-technical teams, converting first-time users into recurring spenders. Meanwhile, large enterprises double down on AI and data enrichment, expanding wallet share within incumbent platforms. Both segments enlarge average revenue per user, reinforcing the growth trajectory of the United States SMS Marketing market.

By Deployment Mode: Cloud Remains Dominant

Cloud solutions represented 74.53% of the United States' SMS Marketing market size in 2024 and are expected to sustain a 24.71% CAGR through 2030, thanks to elastic scaling, built-in redundancy, and automatic carrier-rule updates. On-premises implementations persist only where data sovereignty or legacy integrations are required, and their share continues to shrink yearly.

Global CPaaS vendors invest heavily in U.S.-based data centers and multi-cloud resilience, assuring message throughput during peak events such as holiday sales. Cloud deployment also speeds up access to new compliance features, as vendors push updates centrally. Together, these factors make cloud the de facto standard for most new projects in the United States SMS Marketing market.

By Industry Vertical: Healthcare Surges While Retail Leads

Retail and e-commerce captured 23.87% of spending in 2024 through order confirmations, shipping alerts, and promotional blasts that drive immediate revenue. Healthcare is projected to grow at the fastest rate, with a 23.24% CAGR, as providers deploy SMS for appointment reminders, prescription pickups, and telehealth triage. HIPAA mandates heightened interest in partners offering secure messaging, driving up the average contract values.

Financial services rely on SMS for fraud alerts and two-factor authentication, while hospitality and travel utilize instant itinerary updates and check-in links to enhance the guest experience. Government agencies utilize SMS for citizen notifications, emergency alerts, and program enrollment, thereby expanding the societal footprint of the United States' SMS Marketing market. Success in healthcare could trigger similar privacy-centric use cases across adjacent regulated industries.

Geography Analysis

Regional adoption mirrors economic patterns. In the South, fast-growing e-commerce businesses and third-party logistics firms send high-volume transactional texts that anchor regional revenue. The strength of warehouse logistics along the I-10 corridor sustains day-to-day throughput and underpins scale advantages for vendors serving the United States SMS Marketing market.

The West’s technology clusters accelerate feature innovation and RCS pilots. Companies there beta-test conversational commerce that blends images, buttons, and payments inside messages. This experimentation influences feature roadmaps that later roll out nationwide. Venture funding is concentrated in San Francisco, Los Angeles, and Seattle, providing start-ups with immediate access to cutting-edge CPaaS APIs and fostering robust partner ecosystems.

In the Northeast, regulatory scrutiny is strongest, shaping demand for audit trails and consent orchestration. Banks and insurers deploy SMS primarily for security-sensitive tasks, contributing to premium unit economics. The Midwest combines manufacturing alerts and healthcare appointment reminders, offering stable, if unspectacular, growth for the United States' SMS Marketing market.

Competitive Landscape

The market remains moderately fragmented. Twilio reported USD 4.46 billion in 2024 communications revenue, equivalent to 93% of its overall business, demonstrating scale advantages in carrier-rate negotiation and network uptime. Sinch secured full RCS coverage across all Tier 1 carriers in 2025, differentiating itself through its rich-media delivery capabilities.

Vertical specialists intensify competition. Attentive and Postscript focus on Shopify brands, bundling creative templates and revenue attribution. Klaviyo combines email and SMS into a unified platform, capturing market share where merchants seek channel consolidation. Enterprise buyers evaluate AI maturity, compliance tooling, and total cost of ownership, driving convergence of roadmaps across vendors.

Strategic moves include Sinch’s Model Context Protocol for conversational AI and Twilio’s first GAAP operating profit, which strengthens free cash flow to fund product expansion. M&A activity-such as Link Mobility acquiring FireText-signals ongoing consolidation as vendors seek to scale and absorb carrier fees to fund AI innovation. These dynamics collectively enhance functionality and maintain high switching costs within the United States SMS Marketing market.

United States SMS Marketing Industry Leaders

Twilio Inc.

Sinch AB

Infobip Ltd.

Vonage Holdings Corp.

EZ Texting (CallFire Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sinch launched nationwide RCS for Businesses, enabling branded carousels and media-rich messages across all Tier 1 carriers

- August 2025: Sinch unveiled Model Context Protocol to power context-aware conversational agents for enterprise messaging

- February 2025: Link Mobility closed the FireText acquisition to expand U.S. customer reach

- February 2025: Twilio reported its first GAAP operating profit, signaling operational maturity in the United States SMS Marketing market

United States SMS Marketing Market Report Scope

| Software | SMS Marketing Automation Platforms |

| Bulk SMS Gateways | |

| Services | Professional Services |

| Managed Services |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Cloud-Based |

| On-Premises |

| Retail and E-Commerce |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Hospitality and Travel |

| Media and Entertainment |

| Government and Non-Profit |

| Other Industry Verticals |

| By Component | Software | SMS Marketing Automation Platforms |

| Bulk SMS Gateways | ||

| Services | Professional Services | |

| Managed Services | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Industry Vertical | Retail and E-Commerce | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare | ||

| Hospitality and Travel | ||

| Media and Entertainment | ||

| Government and Non-Profit | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

How large will SMS spending be in the United States by 2030?

The United States SMS Marketing market size is forecast to reach USD 28.19 billion by 2030 at a 23.05% CAGR.

Which region is expanding the fastest?

The West is projected to post the highest 23.83% CAGR as technology firms adopt AI personalization and RCS features.

What is the main compliance requirement for business texting?

Brands must register 10DLC campaigns and manage consent under TCPA rules to avoid carrier blocks and litigation.

Which industry is showing the quickest adoption beyond retail?

Healthcare is advancing at a 23.24% CAGR thanks to appointment reminders and secure patient communications.

Why are carrier fees a concern for marketers?

New A2P surcharges raise per-message costs, pressuring campaign budgets and prompting brands to optimize send volume.

What differentiates leading SMS platforms today?

Key factors include AI-driven personalization, omnichannel integration, automated compliance, and full RCS support.

Page last updated on: