United States Marketing Agencies Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

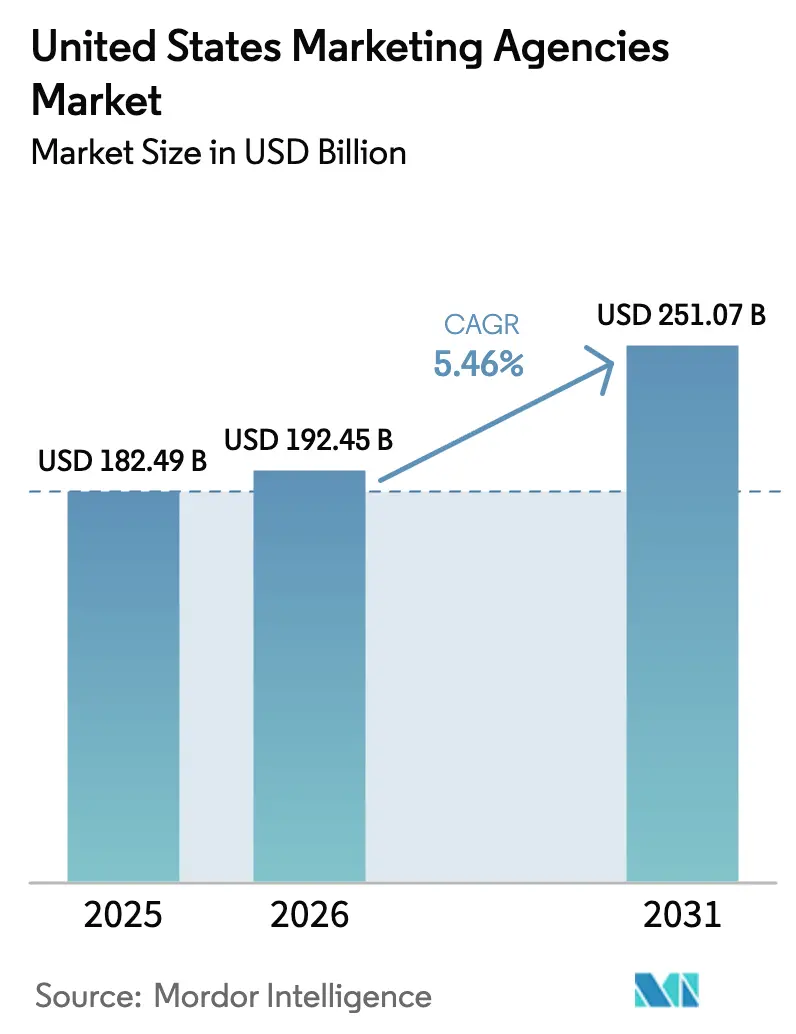

| Base Year Market Size (2025) | USD 182.49 Billion |

| Market Size (2026) | USD 192.45 Billion |

| Market Size (2031) | USD 251.07 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

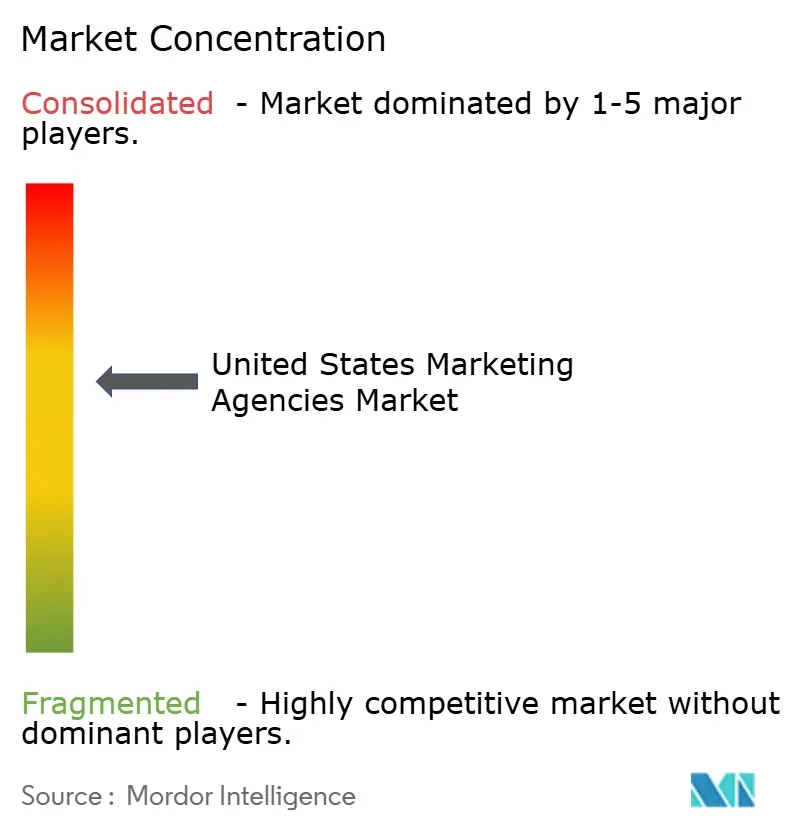

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Marketing Agencies Market Analysis by Mordor Intelligence

The United States marketing agencies market size was valued at USD 182.49 billion in 2025 and estimated to grow from USD 192.45 billion in 2026 to reach USD 251.07 billion by 2031, at a CAGR of 5.46% during the forecast period (2026-2031). This forward momentum illustrates how the United States marketing agencies market is absorbing shifts toward performance-based media, privacy-first data practices, and rapid artificial intelligence (AI) deployment across creative, media, and analytics workflows. Digital-first integrated services, now embedded across paid, owned, and earned channels, continue to gain budget share as advertisers demand closed-loop attribution and omnichannel orchestration. At the same time, experiential investments are rebounding as brands restore in-person engagement budgets, while connected TV (CTV) inventory outperforms linear television in reach, targeting precision, and addressability. Consolidation among holding companies is accelerating to fund AI at scale, yet smaller specialist shops still capture share by offering niche expertise in retail media, CTV planning, and AI-assisted creative production.

Key Report Takeaways

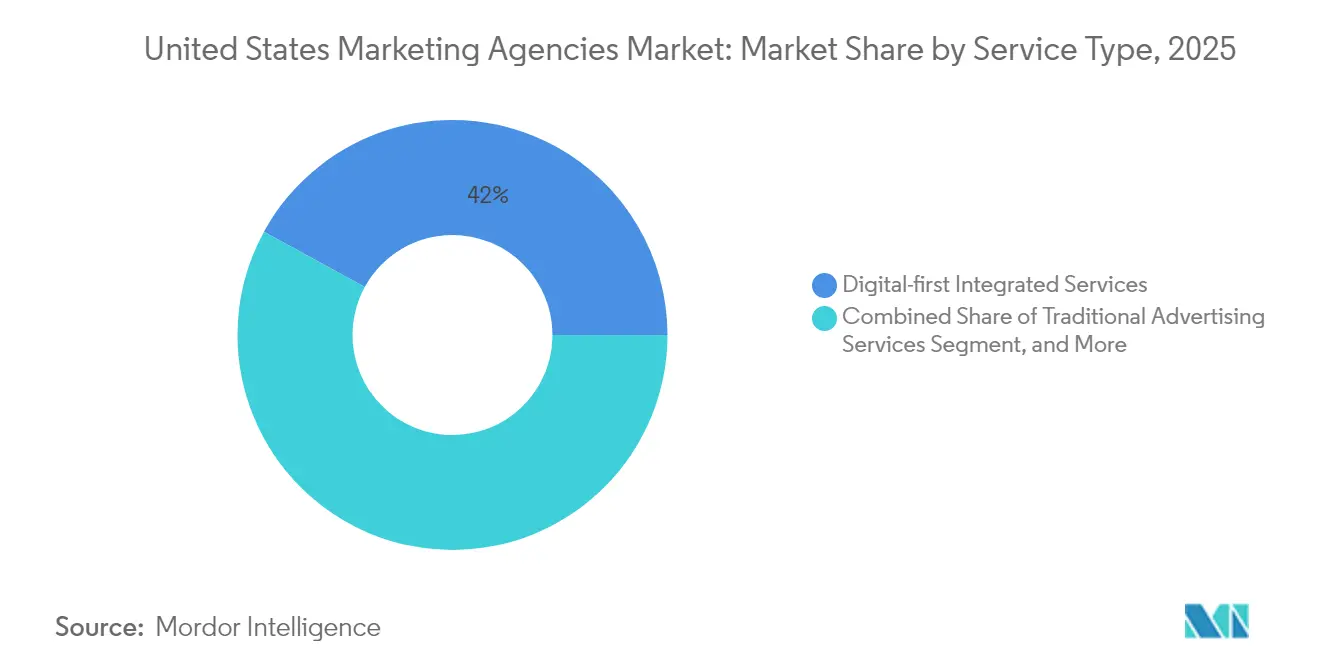

- By service type, digital-first integrated services led with 42.02% revenue share of the United States marketing agencies market in 2025. Experiential and event marketing is advancing at a 5.92% CAGR through 2031, the fastest rate among service categories.

- By organization size, large enterprises held 46.10% of the United States marketing agencies market share in 2025, while small enterprises are projected to post the highest 6.42% CAGR to 2031.

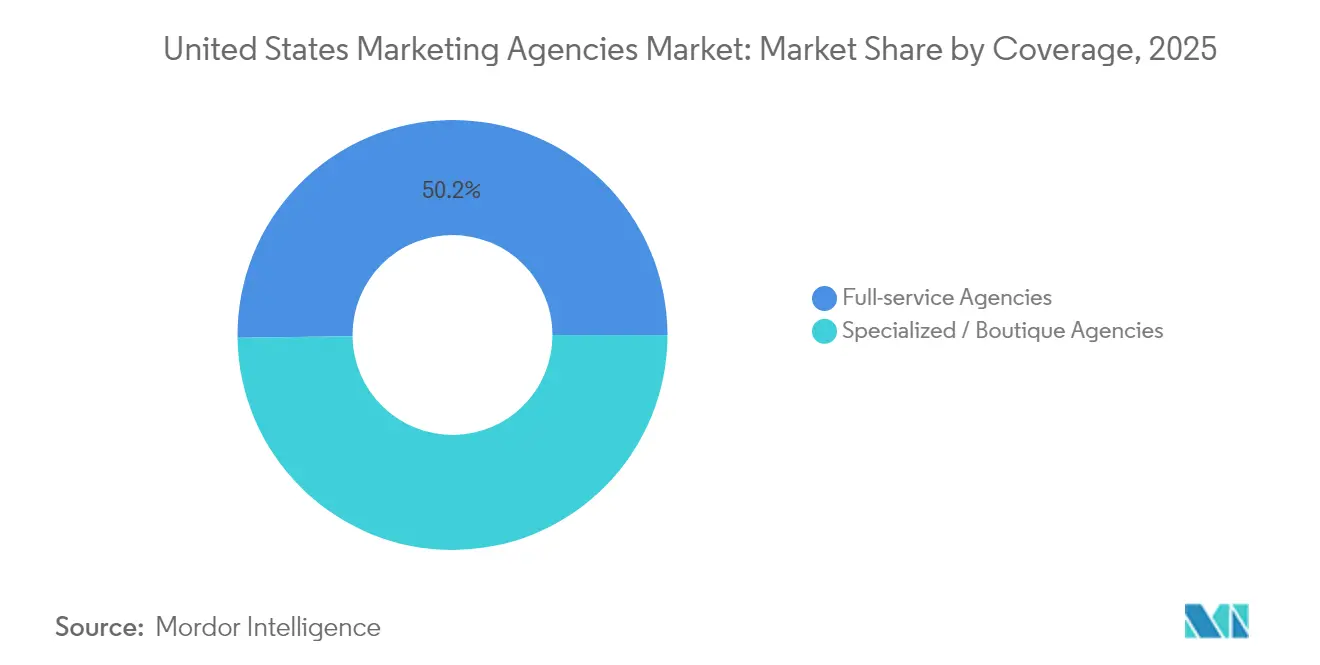

- By coverage, full-service agencies accounted for a 50.20% share of the United States marketing agencies market size in 2025; boutique specialists are growing at a 6.03% CAGR through 2031.

- By end-user industry, retail and e-commerce commanded 19.75% of 2025 revenues in the United States marketing agencies market and is projected to expand at a 5.78% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Marketing Agencies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in performance-based digital ad spend | +1.2% | Global, concentrated in North America | Short term (≤ 2 years) |

| Growing emphasis on first-party data strategies | +0.9% | Global, driven by US privacy regulations | Medium term (2-4 years) |

| Adoption of AI-driven creative and media optimization | +1.1% | North America and EU leading, Asia Pacific following | Medium term (2-4 years) |

| Expansion of retail media networks | +0.8% | Global, US market leadership | Short term (≤ 2 years) |

| Rise of connected TV (CTV) advertising inventory | +0.7% | North America primary, expanding globally | Short term (≤ 2 years) |

| Corporate demand for sustainability-oriented campaigns | +0.4% | Global, EU regulatory influence strongest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Performance-Based Digital Ad Spend

Performance budgets now represent 19% of average B2B and 22% of average B2C marketing outlays, reflecting a board-level insistence on measurable return under tighter budgets. The resulting demand for end-to-end attribution is accelerating investment in agency-built clean-room solutions, multi-touch modeling, and algorithmic bidding that links spend directly to revenue outcomes. Agencies demonstrating rapid optimization loops win larger retainer scopes, while firms without advanced analytics capabilities struggle to defend margin amid client requests for cost-per-acquisition guarantees. Digital marketplaces, subscription apps, and direct-to-consumer brands are the earliest adopters, yet legacy sectors such as automotive and financial services are also reallocating television dollars into trackable social and search formats, further lifting the United States marketing agencies market.

Growing Emphasis on First-Party Data Strategies

The California Privacy Rights Act (CPRA) is limiting third-party cookie use and reducing targeting accuracy by 25-40 percentage points for browser-reliant campaigns. Brands now prioritize customer data platforms, consent management, and safe-harbor identity graphs. Holding companies have responded with targeted acquisitions: Publicis agreed to purchase identity specialist Lotame in 2025 to add near-global deterministic profiles, while WPP bought InfoSum to extend privacy-first matching across partners. Agencies capable of connecting these assets to outcome metrics enjoy defensible pricing and longer-term contracts, widening the competitive gap within the United States marketing agencies market.

Adoption of AI-Driven Creative and Media Optimization

Significant rate of CMOs cite AI enablement as a 2024 investment priority, and leading networks such as WPP are investing USD 400 million annually in proprietary generative engines, predictive dashboards, and pricing models.[1]VML Press Office, “WPP & NVIDIA Partner on Omniverse Cloud,” vml.com Omnicom’s advertising segment grew 5.9% year-on-year in Q4 2024, a gain attributed partly to machine-assisted media buying and content personalization.[2]Finimize Newsroom, “Omnicom Surpasses Expectations with AI-Driven Advertising Growth,” finimize.com AI now governs everything from script generation to placement pacing, cutting creative iteration cycles by up to 30% and trimming non-working spend. Healthcare and pharmaceutical advertisers remain cautious due to compliance needs, producing a two-speed adoption pattern that agencies must navigate via modular service offerings. This technology race underpins the steady growth outlook for the United States marketing agencies market.

Expansion of Retail Media Networks

Retailers are commercializing first-party transaction data by launching advertising marketplaces that sit alongside e-commerce operations, creating new inventory for media planners. Amazon’s advertising unit alone produced USD 14.3 billion in quarterly revenue during 2024, reflecting the magnetism of shopper-level data for packaged-goods brands.[3]Amazon Investor Relations, “Q4 2024 Results,” amazon.com Agencies with commerce advisory talent design campaign constructs that tie onsite sponsored placements to off-site awareness channels and in-store conversions, often achieving 20-25% efficiency gains in cost per incremental sale. Full-service groups deploy cross-retailer dashboards, while boutique retail-media specialists deliver bespoke SKU-level analytics, collectively boosting the United States marketing agencies market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent acquisition and retention shortages | -0.8% | Global, acute in North America | Short term (≤ 2 years) |

| Margin squeeze from in-house brand teams | -0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Signal-loss due to privacy regulations (e.g., CPRA) | -0.4% | Global, US and EU regulatory leadership | Medium term (2-4 years) |

| Over-dependence on platform walled gardens | -0.3% | Global, concentrated in digital-first markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent Acquisition and Retention Shortages

A significant rate of U.S. advertising, PR, and media services positions remained unfilled in 2025, signaling a chronic skills shortage that dampens revenue realization. Specialized competencies in AI prompting, clean-room engineering, and advanced analytics carry 15-25% compensation premiums, pressuring operating margins for small and mid-tier agencies. Moreover, a notable rate of creative-services leaders reports year-on-year widening skills gaps, compelling more firms to increase contractor usage to preserve service-level agreements. The shortage disproportionately affects mid-market agencies that cannot match holding-company career paths, occasionally delaying campaign launches and diminishing client satisfaction in the United States marketing agencies market.

Margin Squeeze from In-House Brand Teams

Corporations are expanding internal studios for content production, performance media, and marketing operations to cut costs and shorten deadlines. Work allocation data from the Australian In-House Agency Council suggests the external-to-internal split has inverted to 30/70, and parallel surveys point to similar momentum among U.S. advertisers.[4]Kalila Welch, “Brand In-Housing to Agency Work Volume Flips to 70:30,” mi-3.com.au High-volume production billings, once a dependable margin contributor for agencies, now shift in-house, forcing external partners to refocus on high-value strategic counsel, innovation, and complex activations. Agencies that fail to reposition effectively confront fee pressure, scope erosion, and staff redundancies, shaving 0.6 percentage points from the forecast CAGR for the United States marketing agencies market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Integration Drives Market Leadership

Digital-first integrated services accounted for 42.02% of the 2025 United States marketing agencies market share, emphasizing advertiser preference for single-P&L partners who manage search, social, programmatic, and content within unified data stacks. This dominance stems from rising performance expectations: unified dashboards link media inputs to business outcomes in near real time, allowing brands to rebalance budgets daily. Traditional above-the-line services still attract spend for brand storytelling, yet their relative share is tapering as CMOs prioritize measurable KPIs. Downstream, public relations and reputation-management retain relevance in a polarized social climate, while influencer programs expand beyond celebrity endorsements to micro-communities that fuel consideration among Gen Z.

Experiential and event marketing, projected to post a 5.92% CAGR, reflects a corporate impulse to restore physical touchpoints that deepen emotional resonance post-pandemic. Fortune 1000 surveys show 74% plan to lift experiential budgets in 2025, citing improved brand perception among participants. Technological augmentation, ranging from mixed-reality demos to data-rich lead capture at events, extends the physical moment into a multi-channel nurture journey, further weaving experiential into omnichannel strategies within the United States marketing agencies market.

By Organization Size: Small Enterprise Democratization Accelerates

Large enterprises controlled 46.10% of the 2025 United States marketing agencies market size, reflecting complex global portfolios that leverage multi-disciplinary agency ecosystems. These brands contract fully integrated teams to coordinate creative, media, commerce, and data across dozens of markets, defending brand consistency and economies of scale. Mid-size clients balance internal capabilities with flexible agency rosters, often engaging partners for specialized analytics, platform integrations, or seasonal surge support.

Small enterprises, however, represent the fastest-expanding customer cohort with a 6.42% CAGR outlook. The rise of self-serve programmatic portals, templated website builders, and AI-driven content tools is lowering entry barriers, enabling agencies to productize services at SMB-friendly price points. Subscription bundles covering SEO, paid search, and social community management unlock recurring revenue while aligning deliverables with owner-operators’ focus on cash flow. This democratization broadens the total addressable pool of customers and powers incremental gains for the United States marketing agencies market.

By Coverage: Specialized Agencies Gain Competitive Edge

Full-service networks retained a 50.20% stake of the 2025 United States marketing agencies market share, wielding cross-disciplinary talent pools and global footprints that streamline vendor management for multinational marketers. Their negotiating heft secures preferred platform pricing, and end-to-end data custody helps prove incremental contribution against sales. That advantage is being challenged by boutiques scaling around single-capability centers, such as retail-media activation, CTV optimization, or creative-AI labs, growing 6.03% annually as they plug into client tech stacks with speed and minimal bureaucracy.

Specialists court disruptor brands and high-growth verticals willing to trade integrated convenience for breakthrough innovation. Moreover, megamergers such as Omnicom’s USD 13.25 billion bid for Interpublic underscore scale’s rising cost; integration distraction opens whitespace for nimble independents to win project-based scopes, adding diversity to the United States marketing agencies market.

By End-User Industry: Retail E-Commerce Sustains Leadership

Retail and e-commerce generated 19.75% of 2025 agency billings, buoyed by commerce-media convergence and direct-to-consumer brand launches. Agencies develop SKU-level creative, optimize sponsored product bidding, and implement end-to-end attribution that traces digital impressions to in-store basket lifts. Technology and telecom rank second as 5G adoption, cloud migration, and enterprise software subscriptions spur account-based marketing programs targeting IT decision groups.

Healthcare and life sciences produce consistent demand for agencies versed in Food and Drug Administration advertising codes, Health Insurance Portability and Accountability Act data handling, and omnichannel patient journeys. PulsePoint notes surging interest in privacy-compliant real-world data overlays for condition-specific outreach. Financial services, automotive electrification, and entertainment media each represent substantial slices of the United States marketing agencies market, with CTV campaigns driving new net spend in entertainment and audience-targeted display boosting fintech app installs.

Competitive Landscape

The United States marketing agencies market is moderately concentrated yet highly dynamic. Omnicom, Publicis, WPP, and (pending merger approval) Interpublic collectively account for an estimated mid-40s percentage of revenue, leveraging integrated service breadth, proprietary data, and strategic C-suite relationships. Large consulting entrants such as Accenture Song and Deloitte Digital acquire specialized shops to bundle transformation, commerce, and creative under unified contracts, threatening holding-company dominance. Omnicom’s USD 13.25 billion acquisition of Interpublic seeks USD 750 million in annual run-rate synergies through elimination of overhead and pooled AI investment.

Mid-tier challengers, Stagwell, Havas, and Dentsu, differentiate through agile network models, challenger-brand rosters, and integrated media-creative teams that avoid siloed P&Ls. Stagwell added 11 agencies in 2024, pushing digital services to 57% of revenue. At the frontier, AI-native boutiques deploy proprietary content engines and predictive spend allocators, promising turnaround times impossible within legacy structures. Retail-media specialists build direct retailer partnerships that bypass agency-trading-desk markups, cementing client ROI transparency.

Pricing pressure continues as brands pivot to outcome-based contracts tied to performance indicators such as incremental sales, lifetime value lift, or sustainability scorecards. Agencies owning end-to-end data fabrics can underwrite these risk-reward mechanics, whereas production-heavy shops without proprietary IP face commoditization. As a result, M&A is expected to intensify, especially for assets that accelerate AI roadmaps, enrich first-party identity graphs, or deepen sectoral compliance expertise, shaping the future trajectory of the United States marketing agencies market.

United States Marketing Agencies Industry Leaders

Dentsu Group Inc.

Interpublic Group of Companies, Inc.

Publicis Groupe S.A.

Omnicom Group Inc.

WPP plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: WPP acquired InfoSum, adding privacy-first identity matching to its global network.

- February 2025: Omnicom announced Q1 2025 revenue of USD 3.7 billion, with media and advertising up 7.2% and precision marketing up 5.8%.

- December 2024: Omnicom agreed to purchase Interpublic for USD 13.25 billion in an all-stock deal to form the world’s largest advertising network.

- July 2024: Publicis acquired Influential for USD 500 million, expanding creator-economy capabilities via a 3.5-million-strong influencer roster.

United States Marketing Agencies Market Report Scope

The US marketing agencies market forecast is segmented by organization size, coverage, and end user. By organization size, the market is segmented into small and medium-sized enterprises and large enterprises. By coverage, the market is segmented into full-service and specialized capabilities. In the end-user industry, the market is segmented into technology and telecom, healthcare, consumer goods, financial services, education, retail and e-commerce, and other end-user industries (automotive, media and entertainment, etc.). The report offers market sizing and forecasts for the US marketing agencies market in value (USD) for all the above segments.

| Digital-first Integrated Services |

| Traditional Advertising Services |

| Public Relations and Communications |

| Experiential and Event Marketing |

| Other Service Types |

| Small-sized Enterprises |

| Mid-sized Enterprises |

| Large Enterprises |

| Full-service Agencies |

| Specialized / Boutique Agencies |

| Technology and Telecom |

| Healthcare and Life Sciences |

| Consumer Packaged Goods |

| Financial Services |

| Education |

| Retail and E-commerce |

| Automotive |

| Media and Entertainment |

| Other End-user Industries |

| By Service Type | Digital-first Integrated Services |

| Traditional Advertising Services | |

| Public Relations and Communications | |

| Experiential and Event Marketing | |

| Other Service Types | |

| By Organization Size | Small-sized Enterprises |

| Mid-sized Enterprises | |

| Large Enterprises | |

| By Coverage | Full-service Agencies |

| Specialized / Boutique Agencies | |

| By End-user Industry | Technology and Telecom |

| Healthcare and Life Sciences | |

| Consumer Packaged Goods | |

| Financial Services | |

| Education | |

| Retail and E-commerce | |

| Automotive | |

| Media and Entertainment | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the United States marketing agencies market in 2026?

The United States marketing agencies market size is USD 192.45 billion in 2026 and is forecast to grow at a 5.46% CAGR during 2026-2031 to reach USD 251.07 billion by 2031.

Which service type holds the largest share of U.S. agency spend?

Digital-first integrated services lead with 42.02% share, driven by unified media-data orchestration.

Which end-user sector spends the most on agency services?

Retail and e-commerce accounts for 19.75% of 2025 billings and remains the biggest client vertical.

What is fueling the shift toward AI in agency workflows?

CMOs demand measurable efficiency gains, prompting networks such as WPP to invest USD 400 million annually in generative and predictive AI tools.

Why are small enterprises the fastest-growing client segment?

Self-service ad platforms and AI-powered tools lower entry barriers, enabling agencies to offer enterprise-grade bundles at small-business price points.

Page last updated on: