A2P SMS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 54.22 Billion |

| Market Size (2031) | USD 65.05 Billion |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

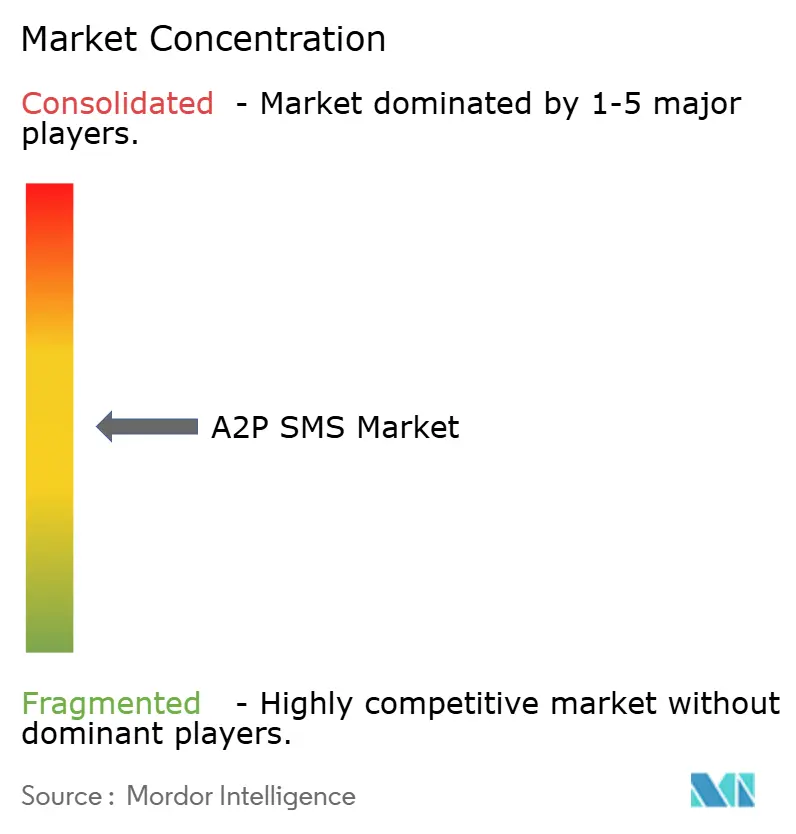

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

A2P SMS Market Analysis by Mordor Intelligence

The A2P SMS Market size was valued at USD 52.28 billion in 2025 and is estimated to grow from USD 54.22 billion in 2026 to reach USD 65.05 billion by 2031, at a CAGR of 3.71% during the forecast period (2026-2031).

The A2P SMS market continues to benefit from device-level reach that works across 2G, 3G, 4G, and 5G networks without internet access or application installs. That reach keeps the channel relevant for authentication, transactional alerts, and critical notifications where delivery certainty matters more than media richness. Growth remains measured because promotional traffic is facing stronger competition from RCS and OTT messaging apps, while authentication and transactional traffic continues to expand across regulated and service-heavy sectors. Enterprise buying behavior is also shifting, with provider selection now shaped more by latency performance, fraud control, and orchestration capability than by message price alone. This keeps the A2P SMS market commercially attractive for scaled CPaaS platforms and compliant aggregators that can combine reliable delivery with stronger platform intelligence.

Key Report Takeaways

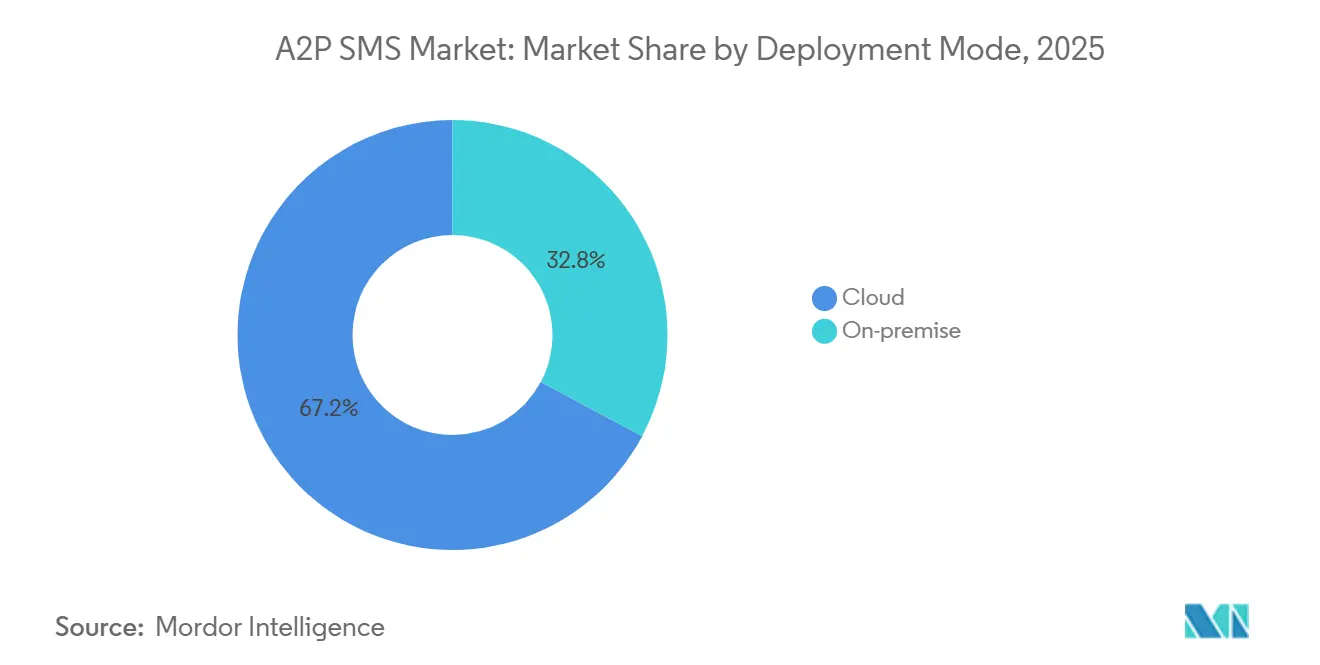

- By deployment mode, cloud held 67.20% share in 2025, and cloud is also forecast to grow at a 6.84% CAGR through 2031.

- By end-user enterprise size, large enterprises held 54.30% share in 2025, while SMEs recorded the highest projected CAGR at 6.20% through 2031.

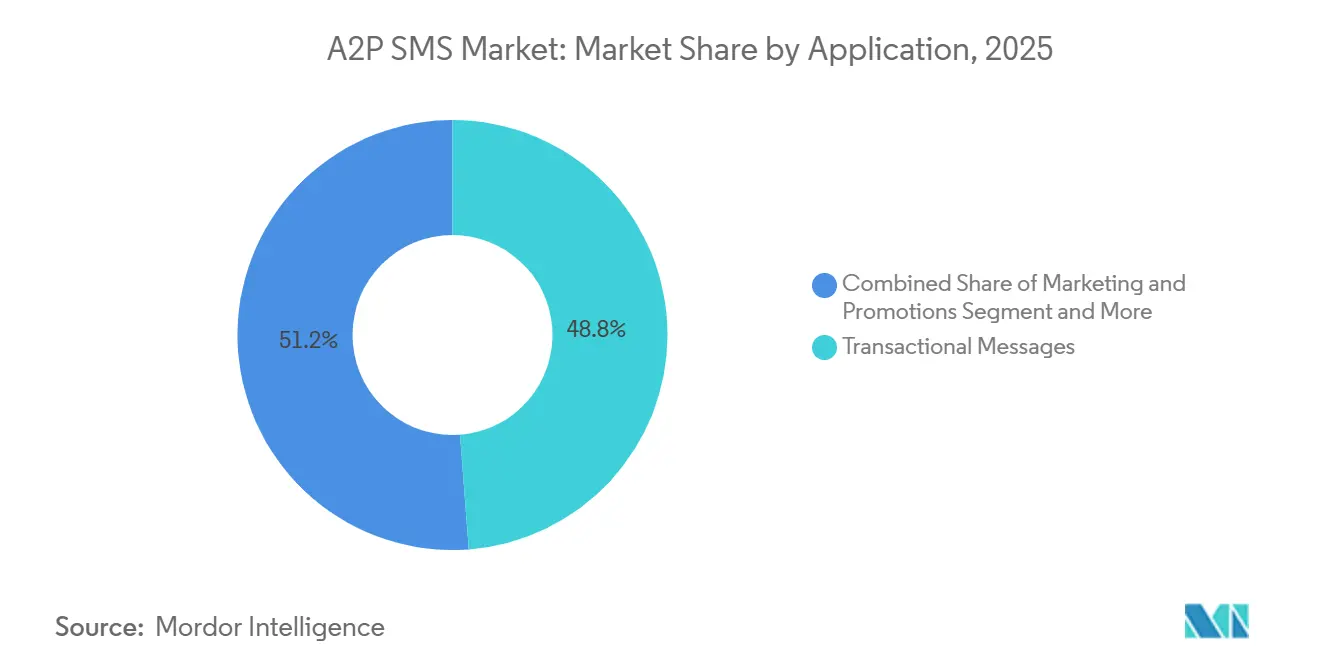

- By application, transactional messages accounted for 48.80% share in 2025, while authentication and security is advancing at a 7.35% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance represented 27.50% share in 2025, while healthcare is projected to expand at a 6.48% CAGR through 2031.

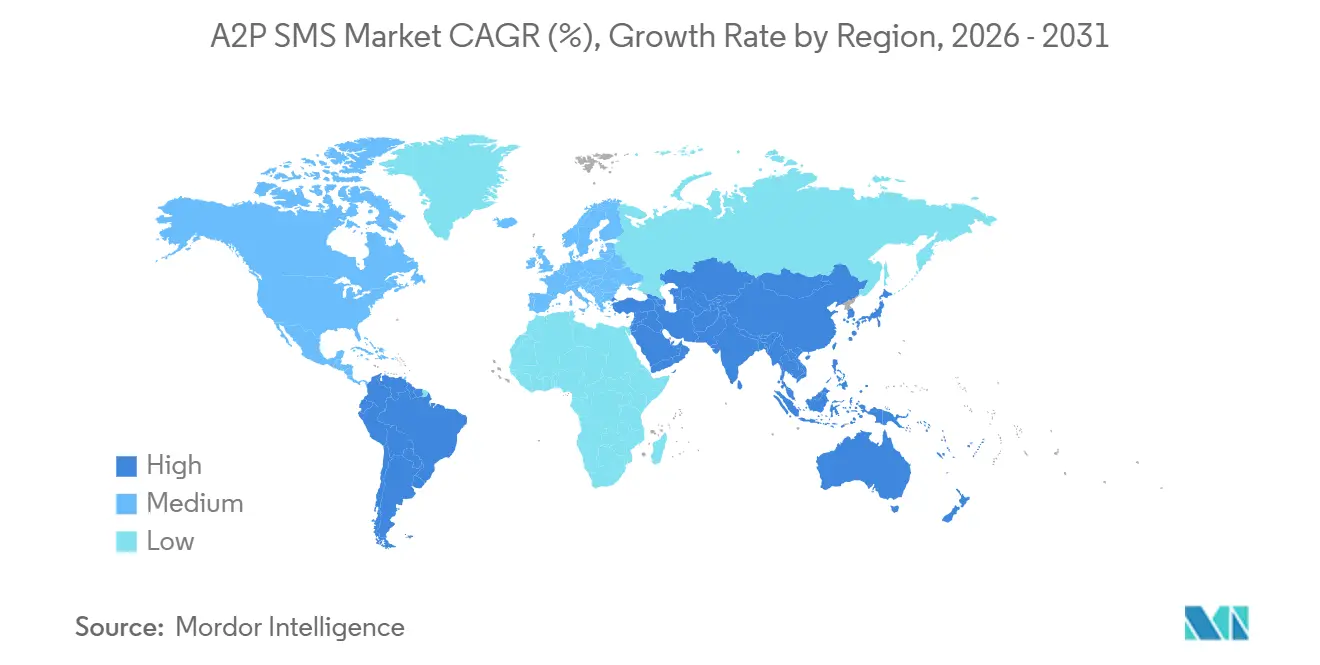

- By geography, North America held 37.90% share in 2025, while the Asia Pacific is set to grow at a 7.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global A2P SMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Need for Secure Two-Factor Authentication | +1.2% | Global, with high concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Increasing Demand for Real-Time Transactional Messaging | +0.9% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of Network APIs Enabling Low-Code SMS Integration | +0.7% | North America and EU, Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| AI-Driven Hyper-Personalization Boosting Campaign Conversion | +0.5% | North America, Europe | Medium term (2-4 years) |

| Carrier-Grade SMS Firewalls Monetizing Grey-Route Traffic | +0.3% | Global, highest revenue recovery potential in Africa and Southeast Asia | Short term (≤ 2 years) |

| Deployment of 5G Stand-Alone Cores Enabling Ultra-Low-Latency Messaging | +0.2% | East Asia, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Need for Secure Two-Factor Authentication

Multi-factor authentication mandates are turning SMS OTP delivery into a compliance-linked service across much of the A2P SMS market. India required two-factor authentication for digital payments from April 2026, and SMS remained an accepted factor within tiered authentication frameworks even as premium alternatives continued to develop.[1]Press Information Bureau, “TRAI Achieves Key Milestone in Ensuring SMS Traceability for Secure Messaging,” Government of India, pib.gov.in At the same time, enterprise-grade users in North America are facing more caution around SMS-based authentication, which is creating a split between advanced users moving to passkeys and mid-market users still relying on OTP at scale. That divergence is producing a corridor-by-corridor compliance model, especially where markets such as the UAE and Singapore are stricter, while parts of South Asia and Africa remain more permissive. The A2P SMS market, therefore, keeps drawing demand from enterprises that cannot rapidly replace legacy identity flows. This pattern is reflected in authentication and security, which is the fastest-growing application segment at a 7.35% CAGR for 2026-2031.

Increasing Demand for Real-Time Transactional Messaging

Real-time transactional communication remains one of the strongest supports for the A2P SMS market because many use cases still require broad and immediate delivery. Transactional messaging accounted for 48.80% of total application demand in 2025, which shows how payment alerts, delivery updates, appointment reminders, and account notifications continue to dominate business traffic. The expansion of e-commerce logistics across the Asia Pacific is increasing message volumes outside traditional financial use cases, especially in last-mile delivery networks serving very large customer bases. Embedded finance is also multiplying message volumes because payment activity inside super apps, ride-hailing platforms, and online marketplaces triggers more confirmation and alert messages than older bank-led communication flows. Healthcare is also contributing to this pattern as telehealth services and digital patient engagement platforms scale appointment reminders, prescription notices, and test result alerts across wider populations. These conditions keep the A2P SMS market relevant even when richer messaging channels are available, because time-sensitive delivery remains the first requirement.

Expansion of Network APIs Enabling Low-Code SMS Integration

The GSMA Open Gateway initiative is changing how enterprises consume carrier capabilities across the A2P SMS market by exposing network features through standardized APIs. More than 239 operators are now participating in the GSMA Open Gateway ecosystem, which supports services such as number verification, SIM swap detection, and OTP delivery through CAMARA-aligned interfaces.[2]GSMA, “What Is GSMA Open Gateway? Open Network APIs,” GSMA, gsma.com That model reduces the need for traditional SMPP and SS7 expertise and makes low-code integration much more practical for enterprises and software developers. Telefónica’s Number Verification API shows the direction of travel because it validates identity by checking IP and SIM records without sending a visible SMS, which lowers interception risk and creates a premium identity product on top of messaging relationships. GSMA also states that the wider network API framework could unlock a USD 300 billion opportunity, which positions API-augmented messaging as an upgrade path rather than a simple replacement story. This is supporting the A2P SMS market by making integration faster, simpler, and more strategic for early adopters.

AI-Driven Hyper-Personalization Boosting Campaign Conversion

AI tools are changing the marketing layer of the A2P SMS market by moving from basic segmentation toward one-to-one message orchestration. Twilio reported in 2025 that 88% of consumers are more likely to purchase when engagement is personalized in real time, while only 44% of brands are achieving that level at scale. That gap favors large CPaaS platforms because effective personalization depends on customer data unification, behavioral feedback loops, and decisioning engines that commodity aggregators usually do not control. Twilio’s multi-year partnership with Microsoft, announced in May 2025, integrated Azure AI Foundry into Twilio’s platform to support conversational AI workflows across customer engagement use cases. In practical terms, this means message copy, timing, and interaction flow are becoming platform-level differentiators rather than simple campaign settings. The A2P SMS market is therefore seeing stronger competitive separation between providers that only route messages and providers that can optimize outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SMS Spam and Fraud Driving Automated Filtering | -0.6% | Global, highest impact in Africa, Southeast Asia, and South Asia | Short term (≤ 2 years) |

| Competition from OTT Chat and RCS Channels | -0.4% | North America, Europe, East Asia, Asia-Pacific, and South America | Medium term (2-4 years) |

| Passkey Adoption Diluting SMS-Based OTP Volumes | -0.3% | North America, Europe, East Asia | Medium term (2-4 years) |

| Inflation-Linked SMS Termination-Fee Hikes by MNOs | -0.2% | Africa, Southeast Asia, South Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

SMS Spam and Fraud Driving Automated Filtering

Fraud is one of the clearest operational restraints on the A2P SMS market because it affects both revenue integrity and message quality. Artificial inflation of traffic, grey-route bypass, and sender ID spoofing are forcing carriers and aggregators to invest more heavily in screening and firewall tools. Sinch stated in its 2025 annual report that AI-powered fraud detection has become a standard platform investment, using message context and behavioral patterns to identify malicious campaigns in real time. Carrier-level compliance frameworks are also becoming stricter, especially where registration, consent evidence, and campaign approval are required before scale traffic can move. That improves trust in compliant traffic but also raises the risk of silent blocking or throughput limits for enterprises that fail onboarding checks. The result is that the A2P SMS market is rewarding high-quality routing relationships and penalizing low-cost paths that cannot protect delivery performance.

Competition from OTT Chat and RCS Channels

OTT chat apps and RCS are a limiting part of the growth runway for the A2P SMS market, especially in richer marketing and engagement use cases. Twilio stated in August 2025 that businesses using RCS saw a 32% increase in customer engagement and conversion rates compared with traditional SMS.[3]Twilio Inc., “Twilio Announces General Availability of Rich Communication Services to Transform Business Messaging With Branded, Interactive Experiences,” Twilio, twilio.com Since iOS 18 expanded RCS support in September 2024, richer business messaging has become more viable across a broader device base, which increases pressure on promotional SMS. Even so, the competitive pattern in 2026 is mostly coexistence because major providers are deploying automatic upgrades to RCS with SMS fallback when richer delivery cannot be confirmed. WhatsApp is also pressuring promotional traffic in Brazil, India, and Southeast Asia, though its pricing structure and session rules still limit full replacement for authentication and transaction alerts. This leaves the A2P SMS market increasingly centered on high-reliability communications while richer channels capture more of the engagement layer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Platforms Redefine A2P Infrastructure Economics

Cloud deployments held 67.20% of the A2P SMS market share in 2025, and cloud is also the fastest-growing mode with a 6.84% CAGR through 2031. This leadership reflects a steady shift away from on-premise SMSC infrastructure toward multi-tenant CPaaS environments that expose messaging through REST APIs and managed connectivity layers. Enterprises are favoring this model because integration cycles are shorter, traffic capacity can scale more easily, and analytics can be monitored in real time without new hardware investment. The A2P SMS market has also benefited from the ability of cloud platforms to support burst traffic during seasonal peaks and major commercial events. Sinch said it processed more than 27 billion customer interactions during Black Friday week alone, which shows why elastic infrastructure has become central to platform economics.

On-premise deployments still retain strategic importance in regulated settings where traffic governance and data handling rules remain strict. That pattern is visible in financial services in China, healthcare operations under GDPR-linked controls in Europe, and government-related messaging in parts of the Middle East. Even in these settings, full isolation is slowly giving way to hybrid models that separate routing and orchestration from storage and local controls. This means the A2P SMS industry is not moving toward a simple cloud-only structure, but it is moving toward cloud-led architecture as the default operating model. Over time, this leaves fully isolated on-premise deployments as a smaller but higher-value niche inside the broader A2P SMS market. The net result is a two-tier structure where agility and scale favor cloud, while compliance sensitivity preserves a narrower premium segment.

By End-User Enterprise Size: Large Enterprises Anchor Volumes While SMEs Gain Ground

Large enterprises accounted for 54.30% share in 2025, while SMEs are projected to expand at a 6.20% CAGR through 2031. Large organizations continue to dominate message volumes because they run more authentication flows, more transactional alerts, and more regulated customer communications across large installed user bases. They also have stronger bargaining power in routing, dedicated aggregator relationships, and internal compliance teams that can manage multi-stream messaging programs. In the A2P SMS market, these advantages make large enterprises the most consistent source of high-volume traffic and premium delivery requirements. They commonly separate authentication, transactional, and promotional flows into different operating lanes so that routing quality and governance can be managed more precisely.

SMEs are still narrowing the gap because the technical and commercial barriers to adoption have fallen sharply. Self-serve API platforms, instant sender onboarding, and pre-built connectors for tools such as Salesforce, HubSpot, and Shopify are making messaging usable without large engineering teams. The rise of AI-native development tools is shortening the build cycle even further, and Sinch announced a partnership with Lovable in February 2026 to embed communications infrastructure into AI-native application creation workflows.[4]Sinch AB, “Sinch Announces Strategic Partnership With Lovable to Power Communications for AI-Native Applications,” PR Newswire, prnewswire.co.uk Sinch also disclosed that it secured new agreements with 2 Fortune 10 companies in the Americas during 2025, taking its total Fortune 10 customer count to 7, which shows that even the largest enterprises still depend on specialist platforms for scale and reliability. This combination of scale-led incumbency and easier SME onboarding is widening the addressable base of the A2P SMS market rather than shifting it away from large customers.

By Application: Authentication Traffic Raises the Value of Delivery Quality

Transactional messages represented 48.80% share of the A2P SMS market size in 2025, while authentication and security is forecast to expand at a 7.35% CAGR through 2031. Transactional traffic remains the largest application block because payment confirmations, delivery notices, balance updates, and appointment reminders still depend on rapid one-way communication. Authentication and security are growing faster because regulatory pressure is increasing around identity checks, especially in financial and digital service environments. India’s DLT framework had registered more than 55 million approved templates by early 2025, and the mix was largely concentrated in transactional and authentication messaging categories. That depth of template registration reflects how dependent high-volume digital ecosystems remain on OTP and related verification flows. In the A2P SMS market, message value is therefore shifting from broad promotional volume toward reliability-sensitive application traffic.

The remaining application segments are still important, but they are evolving in different directions. Marketing and promotions are facing stronger competition from RCS because verified sender identities, richer content, and reply options improve branded engagement for campaign-oriented communication. Customer support and feedback is moving toward AI-mediated two-way messaging, where conversational handling can reduce contact center load without asking users to install new apps. Notifications and alerts are expanding steadily as more connected services generate event-triggered messages for product availability, flight status, subscription renewal, and service changes. Twilio’s August 2025 RCS rollout also reinforced the logic of multi-channel messaging with automatic SMS fallback, which supports a hybrid model rather than a single-channel decision. That structure helps the A2P SMS market keep a durable role in delivery assurance even as application mix continues to shift.

By End-User Industry: Financial Services Lead While Healthcare Expands Faster

Banking, financial services, and insurance accounted for 27.50% of the A2P SMS market size in 2025, while healthcare is projected to grow at a 6.48% CAGR through 2031. Financial institutions remain the largest vertical because they must authenticate transactions, issue fraud alerts, and notify users of account events in real time. These are communications where failure can create legal exposure, operational risk, and direct customer harm, which supports higher routing standards and stronger compliance oversight. Infobip states that authentication message delivery rates for financial services clients reached 89.2%, which highlights how delivery performance directly shapes buyer decisions in this vertical. The A2P SMS market, therefore, continues to draw a large part of its value from workflows where trust and timing matter more than rich content.

Healthcare is expanding faster because telehealth, patient engagement tools, and digital prescription workflows are increasing the frequency of provider-to-patient communication. Sinch identifies healthcare as a strategic vertical for secure messaging that can reduce missed appointments and lower administrative burden through automated notifications. Retail and e-commerce remain the second-largest vertical in practical usage terms, using messaging for order confirmation, delivery updates, promotional campaigns, and post-purchase engagement. Travel and hospitality uses SMS for itinerary changes, hotel check-in instructions, and travel notifications where immediacy is essential. Media and entertainment and education are smaller but growing users, while insurance is becoming more active as telematics and digital claims processing add new automated messaging triggers. This keeps the A2P SMS market diversified by end-user demand even though financial services remains the anchor vertical.

Geography Analysis

North America held 37.90% of the A2P SMS market share in 2025, which made it the largest regional contributor to global revenue. The United States supports that position through mature CPaaS adoption, deep enterprise use in financial services and e-commerce, and carrier-led compliance frameworks built around 10DLC registration and verified sender practices. In 2026, stricter consent and registration expectations are concentrating legitimate traffic among approved brands and compliant routing partners, which is raising the quality threshold for participation. Canada and Mexico also add incremental demand, with Mexico’s growing fintech base increasing transactional and authentication traffic across digital financial services. This leaves North America as the most mature part of the A2P SMS market, where scale, compliance, and delivery quality are closely linked.

Asia Pacific is the fastest-growing region with a 7.14% CAGR for 2026-2031, and this reflects several different growth engines operating at once. India’s DLT framework formalized commercial messaging flows through mandatory registration, and the system covered more than 250,000 registered principal entities and over 55 million approved message templates by late 2024.[5]Press Information Bureau, “TRAI Achieves Key Milestone in Ensuring SMS Traceability for Secure Messaging,” Government of India, pib.gov.in China adds high transactional volume through its digital payment ecosystem, especially for rural and underbanked users who still rely on carrier-grade communication for alerts and verification. Southeast Asia is also adding new flows as fintech platforms in Indonesia, the Philippines, Vietnam, and Thailand expand mobile-first financial services at scale. These patterns give the A2P SMS market a strong regional growth base that is driven by both compliance structures and everyday transaction activity.

Europe remains strategically important because the United Kingdom, Germany, and France continue to generate substantial financial and retail messaging volumes. The region is also further ahead on RCS coexistence, which means richer channels are gaining in marketing use cases while SMS continues to anchor authentication and alert traffic. South America, led by Brazil and Argentina, remains a meaningful growth corridor because SMS still supports digital banking and e-commerce authentication across populations with varied device and app behavior. The Middle East and Africa is more uneven, with the UAE moving away from SMS OTP while Sub-Saharan Africa still depends heavily on SMS for mobile money and digital identity workflows. Infobip and Bayobab formed a five-year partnership in February 2025 to deploy firewall protection, grey-route detection, and route management across MTN’s network, which underlines the revenue recovery opportunity tied to compliant traffic formalization in Africa. Together, these regional patterns show that the A2P SMS market is growing for different reasons across regions, with maturity in some corridors and formalization in others.

Competitive Landscape

The A2P SMS market is moderately fragmented, with competition spread across global CPaaS companies, regional specialists, operator-linked hubs, and independent aggregators. Twilio Inc., Sinch AB, and Infobip Ltd. remain the clearest platform-scale benchmarks because they combine routing depth with fraud control, orchestration tools, and broader enterprise communications offerings. Their positioning matters because customers are no longer choosing vendors only on message delivery; they are also choosing on compliance support, latency performance, and how well SMS fits into a wider messaging stack. The A2P SMS market has therefore become more demanding for small aggregators that compete only on price and basic connectivity. Platform breadth is increasingly tied to strategic relevance, especially where enterprise clients want SMS, RCS, WhatsApp, and identity tools under one operating layer.

Sinch’s scale illustrates why larger providers hold an advantage in this environment. The company reported 2025 net sales of SEK 27,080 million (~USD 2.62 billion) and said it handled more than 900 billion customer interactions annually across more than 200,000 customers in 59 countries. That scale supports carrier relationships, platform investment, and the ability to absorb higher product development costs in AI, fraud prevention, and richer messaging channels. Regional specialists still hold defensible positions in their home corridors, including Tanla Platforms Ltd. in India and LINK Mobility Group Holding ASA in Europe. LINK’s acquisition of SMSPortal in 2025, which added a South African footprint with 23 billion annual messages and 65,000 customer accounts, shows how regional players are extending their reach beyond mature core markets.

Strategic moves in the A2P SMS market are increasingly centered on AI, richer messaging, and operator monetization. Twilio’s May 2025 partnership with Microsoft aimed to accelerate conversational AI capabilities inside customer engagement workflows, which strengthened its position beyond basic transport. Infobip expanded its partnership with BT in October 2025 and broadened its Azure Communication Services integration in August 2025, both of which reinforced its multi-country enterprise positioning across SMS, voice, and richer channels. The operator-facing part of the market is also becoming more valuable, and Infobip says its SMS firewall capabilities are deployed across more than 120 mobile network operators, which shows how fraud protection is turning into a durable competitive moat. Overall, the A2P SMS market is rewarding vendors that can combine assured delivery with compliance depth, richer channel integration, and platform intelligence.

A2P SMS Industry Leaders

Twilio, Inc.

Vonage America LLC

Infobip Ltd

Sinch AB

Route Mobile Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Twilio and KPN Netherlands announced a nationwide RCS Business Messaging partnership at Mobile World Congress Barcelona, enabling verified, branded interactive messaging across all major Dutch mobile operators powered by Google. The rollout makes the Netherlands one of Europe's newest fully enabled RCS for Business markets, extending Twilio's RCS footprint to 20+ countries and 55+ carriers.

- February 2026: Sinch AB announced a strategic partnership with Lovable, a Sweden-based AI software creation platform, to embed Sinch's communications infrastructure into AI-native applications built on the Lovable Cloud. The collaboration initially covers email via Mailgun and expands to additional messaging and voice capabilities, positioning Sinch as foundational infrastructure for the AI application development ecosystem.

- October 2025: Infobip and BT expanded their global partnership to deliver AI-powered communication services to multinational businesses, combining BT's Global Voice and Inbound Contact capabilities with Infobip's omnichannel CPaaS platform.

- August 2025: Infobip expanded its integration with Microsoft Azure Communication Services, making advanced SMS capabilities available in 100+ additional countries, significantly extending enterprise reach for authentication and transactional messaging with full regulatory compliance and real-time analytics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Application-to-Person (A2P) SMS market as all paid, one-way text messages that originate from an enterprise or software platform and terminate on a consumer handset for authentication, alerts, or marketing. Messages delivered by OTT apps, e-mail, RCS, or peer-to-peer texting are not included.

Scope exclusion: Bulk peer-to-peer SMS routes that are later re-sold to enterprises (grey routes) are excluded because pricing and volumes cannot be audited reliably.

Segmentation Overview

- By Deployment Mode

- On-Premise

- Cloud

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SME)

- By Application

- Marketing and Promotions

- Transactional Messages

- Authentication and Security

- Customer Support and Feedback

- Notifications and Alerts

- Other Applications

- By End-user Industry

- Retail and E-commerce

- Banking, Financial Services and Insurance

- Healthcare

- Travel and Hospitality

- Media and Entertainment

- Education

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed mobile network operators across Asia-Pacific, North America, and MEA, plus CPaaS platform managers and digital retailers. Conversations focused on average selling prices, authentication success rates, and channel-mix shifts, allowing us to validate grey-route leakage assumptions and refine regional traffic ratios.

Desk Research

Our desk work began with traffic and tariff data from regulators and trade bodies such as the ITU, GSMA, FCC, and the Mobile Ecosystem Forum, which clarify national message volumes and termination fees. We mapped these with customs statistics on SIM card imports, central-bank e-commerce spend tables, and regional PSD2 and 10DLC compliance notices that indicate 2FA demand. Company 10-Ks, operator ARPU filings (via D&B Hoovers), and news archives (Dow Jones Factiva) provided price benchmarks and enterprise uptake signals. These examples illustrate, but do not exhaust, the secondary sources reviewed.

Market-Sizing & Forecasting

We applied a top-down build that begins with reported carrier A2P traffic, SIM penetration, and blended termination fees, which are then stress-tested with bottom-up checks from sampled CPaaS invoice volumes and large-sender ASP times message counts. Key variables include: - annual A2P SMS per active smartphone, - share of e-commerce checkouts using SMS OTP, - average international surcharge per message, - growth in RCS substitution, and - carrier firewall-filtered grey traffic. A multivariate regression links these drivers to historical spend and supports our 2025-2030 forecast, while scenario analysis adjusts for rapid RCS adoption.

Data Validation & Update Cycle

Outputs pass variance checks against independent traffic audits and are peer-reviewed by senior analysts. Reports refresh each year; interim updates trigger when major fee, regulatory, or traffic shifts exceed preset thresholds.

Why Mordor's A2P SMS Baseline Earns Decision-Maker Trust

Published market values often diverge because firms mix SMS with OTT channels, apply different fee stacks, or freeze exchange rates.

Key gap drivers here are scope creep into RCS, reliance on unverified global ASPs, and outdated traffic baselines that ignore 10DLC and PSD2 surcharges. Mordor's model isolates billable SMS only, applies dynamic FX, and refreshes with carrier filings every twelve months.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 52.28 B (2025) | Mordor Intelligence | - |

| USD 73.10 B (2024) | Global Consultancy A | Includes OTT/business chat traffic and fixed 2023 FX rates |

| USD 71.50 B (2024) | Trade Journal B | Uses single global ASP, omits grey-route dilution |

These comparisons show that, by grounding totals in audited carrier traffic and refreshed fee schedules, Mordor delivers a balanced, transparent baseline that clients can replicate and defend.

Key Questions Answered in the Report

How large is the A2P SMS market in 2026 and what is the outlook through 2031?

The A2P SMS market is valued at USD 54.22 billion in 2026 and is projected to reach USD 65.05 billion by 2031 at a 3.71% CAGR, according to Mordor Intelligence.

Which deployment model leads business messaging infrastructure adoption?

Cloud leads deployment with a 67.20% share in 2025 and is also the fastest-growing mode at a 6.84% CAGR through 2031.

What is driving the fastest application growth in business messaging?

Authentication and security is the fastest-growing application at a 7.35% CAGR, supported by multi-factor authentication requirements and OTP-led digital workflows.

Why does banking, financial services and insurance remain the largest user segment?

The sector held 27.50% share in 2025 because it depends on SMS for fraud alerts, transaction authentication, and account notifications where delivery certainty is critical.

Which region currently leads global demand and which region is growing the fastest?

North America led with 37.90% share in 2025, while Asia Pacific is projected to record the fastest growth at a 7.14% CAGR through 2031.

How are RCS and OTT channels affecting enterprise messaging strategies?

They are taking a larger role in branded and interactive communication, but SMS remains central for fallback delivery, authentication, and time-sensitive alerts.

Page last updated on: