Basmati Rice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

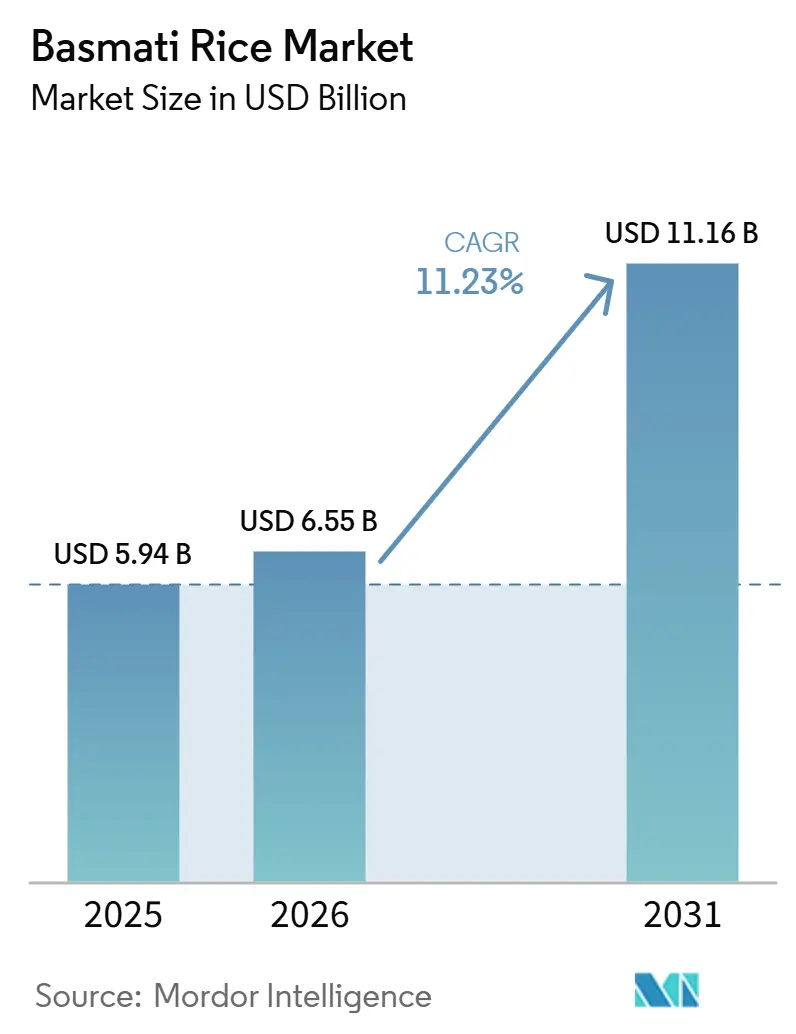

| Market Size (2026) | USD 6.55 Billion |

| Market Size (2031) | USD 11.16 Billion |

| Growth Rate (2026 - 2031) | 11.23% CAGR |

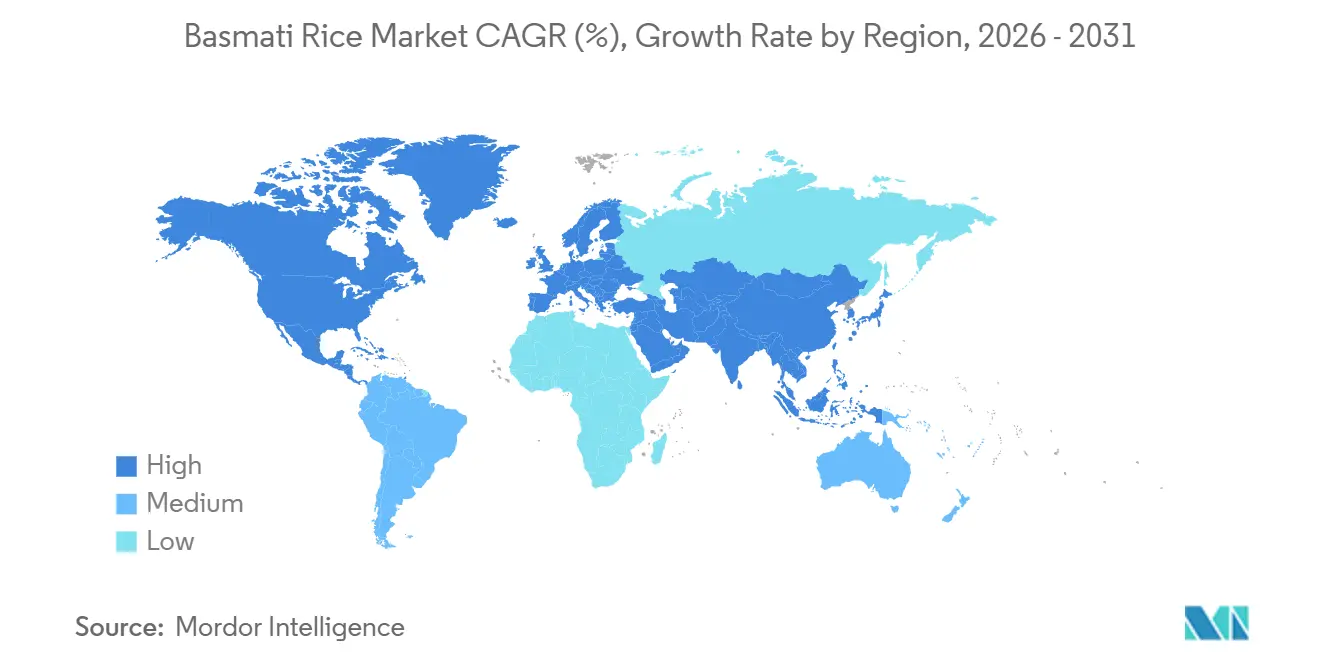

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Basmati Rice Market Analysis by Mordor Intelligence

The Basmati rice market size is expected to grow from USD 5.94 billion in 2025 to USD 6.55 billion in 2026 and is forecast to reach USD 11.16 billion by 2031 at 11.23% CAGR over 2026-2031. Demand in the Basmati rice market is rising as buyers continue to link basmati with lower glycemic response, cleaner processing, and stronger product authenticity than loose rice formats. Export momentum also remains central to the Basmati rice market, with India shipping 6.06 million metric tonnes in 2024-25 at an export value of USD 5.94 billion, which keeps branded retail and bulk trade tightly connected on the supply side. Growth is also supported by stronger procurement of certified packaged rice across retail and foodservice, while online grocery platforms are widening access to branded products in urban markets. The regional base remains strongest in Asia-Pacific, while Western markets continue to favor premium, traceable, and specialty variants, which supports pricing discipline across the Basmati rice market. Leading companies are responding with broader brand portfolios, channel-specific packs, and sourcing systems built around compliance, which keeps competition focused on trust, scale, and repeat purchase rather than price alone in the Basmati rice market.

Key Report Takeaways

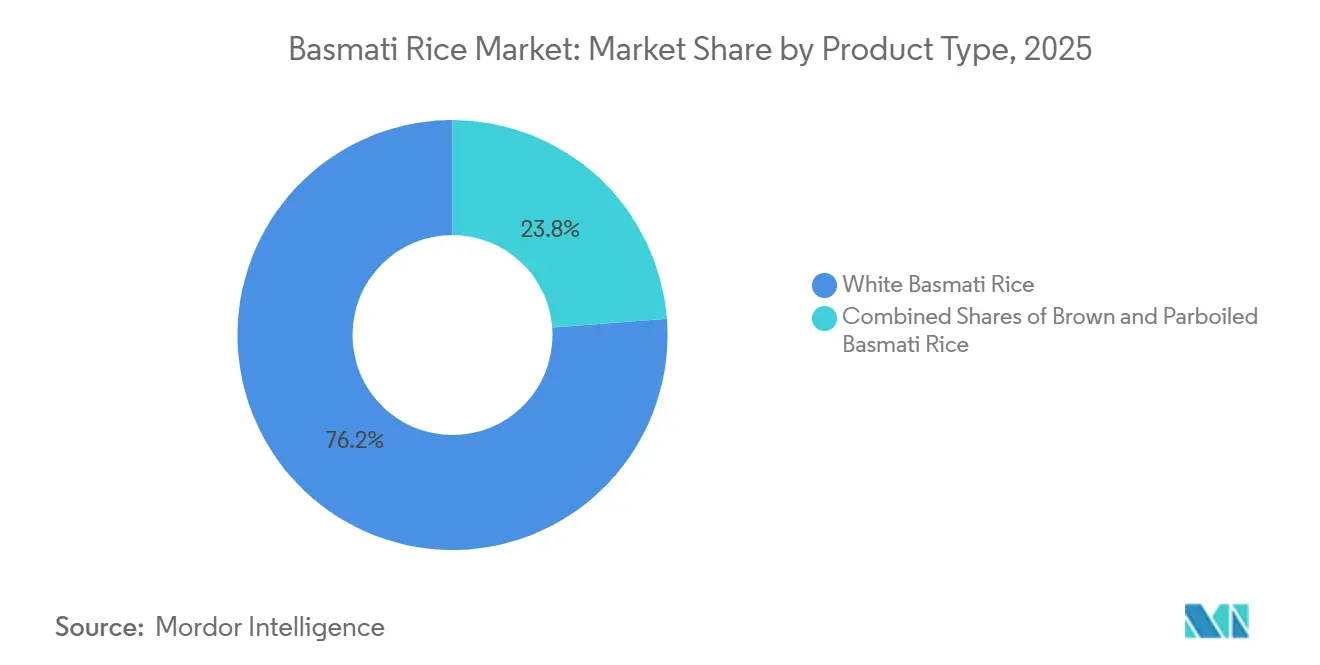

- By product type, white basmati rice held 76.21% of revenue in 2025, while brown basmati rice is projected to expand at 12.24% CAGR through 2031 in the Basmati rice market.

- By packaging size, retail packs accounted for 81.23% of the Basmati rice market size in 2025, while institutional packaging is projected to expand at 12.33% CAGR through 2031.

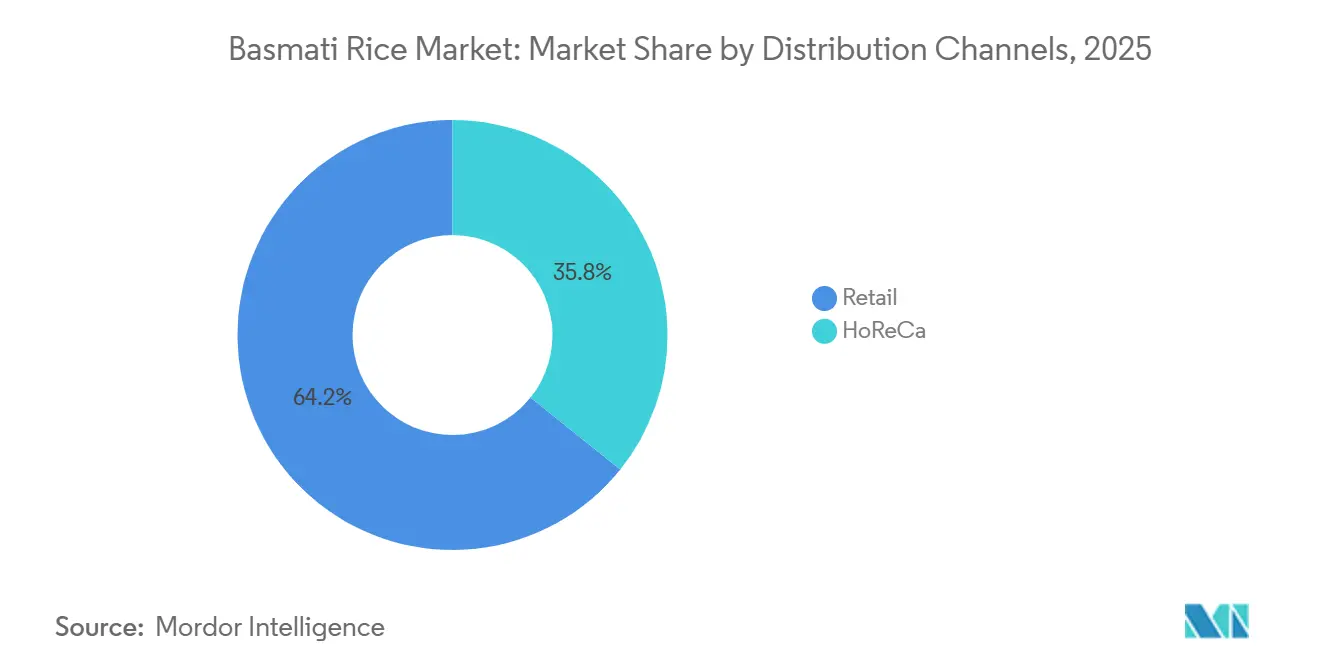

- By distribution channel, Retail held 64.24% of the Basmati rice market share in 2025, while HoReCa Channels are projected to grow at 19.74% CAGR through 2031.

- By geography, Asia-Pacific accounted for 44.52% of the Basmati rice market size in 2025 and is also forecast to grow at 11.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Basmati Rice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-Driven Shift Toward Low-Glycemic Basmati Rice | +2.5% | Global, led by North America, Europe, and urban APAC | Medium term (2-4 years) |

| Supportive Government Policies | +1.5% | India, Pakistan, with spillover to MEA and Europe | Long term (≥ 4 years) |

| Shift Toward Hygienically Processed Packaged Rice | +1.8% | Global, especially South Asia and MEA | Short term (≤ 2 years) |

| Preference for Authentic and Certified Basmati Products | +1.5% | Europe, North America, GCC | Medium term (2-4 years) |

| Emergence of Fortified and Functional Basmati Rice | +1.2% | South Asia, MEA, Sub-Saharan Africa | Long term (≥ 4 years) |

| Accelerating Adoption of Organic Packaged Basmati Rice | +1.0% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-Driven Shift Toward Low-Glycemic Basmati Rice

White basmati rice has a glycemic index of 50-58, compared with 68-80 for jasmine and short-grain varieties, which keeps it relevant in the Basmati rice market as health-led buying grows. Brown basmati rice goes further, with a glycemic index of 45-55 and fiber content of 3 g per 100 g serving, which supports premium positioning in the Basmati rice market among buyers focused on daily diet management. As clinical nutrition guidance becomes more visible in North America and Europe, branded packaged rice gains an edge because it can carry consistent labeling, provenance, and nutritional claims more effectively than loose rice. The same pattern is now visible in urban South Asia, where KRBL stated in its Q3 FY26 earnings discussion that it markets brown basmati SKUs under India Gate for gut health and low-GI dietary goals. That shift matters because it turns health positioning into a formal portfolio decision rather than a minor extension inside the Basmati rice market. It also helps explain why brown basmati is growing faster than the broader Basmati rice market, as premium shoppers and medically aware households move toward more targeted product choices.

Supportive Government Policies

Government support continues to shape the Basmati rice market through export administration, compliance frameworks, and cultivation support in producing states. India’s APEDA issued 43,262 Registration-cum-Allocation Certificates for basmati exports in 2024-25, which reinforced an organized export system tied to documentation and quality control[1]Source: Agricultural and Processed Food Products Export Development Authority, “Basmati Rice Export Statistics 2024-25,” Government of India, apeda.gov.in. In April 2026, DGFT Notification No. 07/2026-27 limited the EIC and EIA certificate requirement to EU member states and select European markets, while exempting other destinations until October 2026. That change reduced friction for exporters serving secondary markets and helped preserve shipment flexibility in the Basmati rice market. Punjab also continued to promote disease-resistant PUSA 1692, with yields of 22-24 quintals per hectare and a target to add at least 10,000 hectares of basmati cultivation in the current season. The result is a more stable raw material base for processors, which reduces pricing shocks and supports longer planning cycles across the Basmati rice market.

Shift Toward Hygienically Processed Packaged Rice

The Basmati rice market continues to benefit from a clear consumer shift toward hygienically processed rice with visible quality assurance. Packaged basmati can make specific process claims around milling, de-stoning, color sorting, and tamper-evident packing, while loose rice usually cannot support the same level of trust. In India, food safety standards and export registration systems have pushed processors to invest in cleaner facilities and traceable supply chains, which has raised the entry bar for unbranded sellers in the Basmati rice market. Sarveshwar Foods reported FY2025-26 revenue of INR 1,346 crore, or USD 160.00 million, up 18% year over year, which reflected continuing demand across branded and export-oriented packaged products. The same shift is influencing institutional procurement in the Middle East and Africa, where large buyers are moving toward certified packaged formats for cost visibility and liability control. This keeps formal processors in a stronger position as the Basmati rice market moves further away from untracked commodity trade in retail and foodservice.

Accelerating Adoption of Organic Packaged Basmati Rice

Organic and sustainability-linked sourcing is becoming a visible premium layer within the Basmati rice market, especially in Europe and North America. Certified organic basmati has been cited at a 40-60% premium to conventional products, which means its revenue effect can exceed its volume contribution in premium shelves. Tilda disclosed in its 2025 Impact Report that its sustainable basmati program covered 3,840 farms across 15,314 hectares in northern India, up from 50 farms in 2021. The company also stated that all farms in the supply chain now use alternate wetting and drying irrigation, which lowers emissions and water use. That scale matters because retailers are tightening expectations around traceable sourcing, pesticide controls, and environmental documentation in the Basmati rice market. Brands that cannot show certified sourcing at scale are likely to face weaker shelf access and lower premium pricing as the Basmati rice market becomes more selective in Western channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulations on GI, Origin Claims, and GMO Compliance | -1.2% | Europe, North America, with spillover to GCC | Long term (≥ 4 years) |

| Counterfeit Branding and Adulteration Eroding Consumer Trust | -0.8% | UK, Europe, South Asia | Medium term (2-4 years) |

| Geopolitical Tensions Disrupting Basmati Exports to Key Import Markets | -1.0% | MEA core, with spillover to global logistics | Short term (≤ 2 years) |

| Climate Variability Impacting Basmati Grain Quality | -0.9% | India, especially Punjab and Haryana, and Pakistan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations on GI, Origin Claims, and GMO Compliance

Compliance risk remains a meaningful restraint for the Basmati rice market because origin rules, testing standards, and labeling norms are getting tighter across importing regions. The EU Code of Practice for Basmati Rice, effective May 2024, set minimum physical and aroma thresholds and tied the basmati designation to defined varieties and geographies. The PGI application for “Basmati” also remains unresolved at the EU level, which has prolonged uncertainty for exporters and importers active in the Basmati rice market[2]Source: European Union, “Commission Implementing Decision Publication of Application for Registration of Basmati,” EUR-Lex, eur-lex.europa.eu. India’s 2026 export policy changes still require inspection certificates for EU member states, the UK, Iceland, Liechtenstein, Norway, and Switzerland, which adds time and cost for compliant sellers. The UK Basmati Code of Practice and domestic food safety requirements in India extend the same pressure across both export and home channels, which leaves smaller processors with less room to absorb compliance costs in the Basmati rice market.

Geopolitical Tensions Disrupting Basmati Exports to Key Import Markets

The Basmati rice market remains exposed to geopolitical disruption because a large share of export demand is concentrated in the Middle East. Saudi Arabia, Iran, Iraq, and the UAE absorbed more than 50% of India’s basmati export volume in 2024-25, and the broader Middle East accounted for 61% of tonnage. Regional conflict delayed cargo movement and strained logistics, with reports citing detentions of 400,000 metric tonnes at ports and sharp increases in shipping costs[3]Source: CMB News, “Basmati Rice Market June 2026,” CMB News, commodity-board.com. Crisil’s review of 47 rated companies covering 60% of industry revenue still suggested stable export volumes with up to 2% growth, but it also pointed to longer working capital cycles across the Basmati rice market. North America added another layer of pressure when U.S. tariffs on basmati rice rose to 50% and were later reduced to 25%, with Ebro Foods stating that the net 2025 impact absorbed by the company was USD 10.00 million. Together, those disruptions complicate pricing, receivables, and route planning for the Basmati rice market even when end demand stays firm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Brown Basmati Accelerates Health-Led Premiumisation

White basmati rice held 76.21% of revenue in 2025, which kept it as the dominant base of the Basmati rice market. Its lead comes from deep culinary use across the Middle East, South Asia, and diaspora households, where biryanis, pilafs, and festive meals still anchor repeat demand. The Basmati rice market also continues to favor white basmati because leading brands have spent years building it as the premium default across shelf and foodservice formats. LT Foods stated that its Basmati and Other Specialty Rice segment delivered 11% year-over-year revenue growth in FY2025-26, supported by 13% volume growth and favorable pricing across India and North America. That pattern shows how white basmati still combines volume depth and brand pricing power in a way commodity long-grain rice usually does not.

Parboiled basmati keeps a useful role inside the Basmati rice industry, especially in institutional and price-sensitive markets where easier cooking and fuel savings matter. Brown basmati, however, is the faster-moving part of the Basmati rice market, with a forecast CAGR of 12.24% through 2031. Its lower glycemic profile and fiber content support stronger health positioning, especially in modern retail and premium e-commerce channels. KRBL’s FY26 commentary showed that brown basmati and low-GI variants are now being developed as targeted functional offerings rather than simple line extensions. This means future value creation in the Basmati rice market is likely to become more concentrated in differentiated health-led rice rather than in standard commodity positioning alone.

By Packaging Size: Institutional Formats Emerge as the Fastest-Growing Size Tier

Retail packs accounted for 81.23% of the Basmati rice market size in 2025, which shows how strongly the category still depends on household consumption. Consumer packs from 1 kg to 10 kg remain the core brand-building format because packaging is where companies signal authenticity, quality, and value. Leading labels such as India Gate and DAAWAT use GI-linked cues, resealable formats, and traceability claims to defend premium pricing in the Basmati rice market. Convenience-oriented subsegments are also expanding in western retail, where pouches and ready-to-heat variants help brands enter faster meal occasions without leaving the rice category. This gives retail packaging continued relevance even as the Basmati rice market becomes more varied by usage occasion.

Institutional packaging is forecast to grow at 12.33% CAGR through 2031. Airlines, hospitals, contract caterers, and restaurant groups are increasingly shifting toward branded bulk packs because standardized quality matters more than simple low-price procurement. Foods and KRBL have both developed HoReCa-focused lines, which shows that major processors now treat institutional demand as a formal growth engine. Sarveshwar Foods’ 2025 export order pipeline for parboiled rice also underlined how a single large institutional buyer can create meaningful volume concentration in this part of the Basmati rice industry. As traceability rules grow tighter, institutional buyers are likely to rely even more on certified processors, which should keep this format structurally attractive in the Basmati rice market.

By Distribution Channel: HoReCa Scales as Retail Channels Digitise and Diversify

The Retail channels, encompassing supermarkets/hypermarkets, convenience/grocery stores, online retail channels, and other distribution channels, held 64.24% of packaged basmati rice distribution in 2025, a position anchored by the high-frequency, habitual nature of basmati purchases across MEA and South Asian geographies. Supermarkets and hypermarkets function as the primary launch platform for premium SKUs in North America and Europe, where 5 kg to 20 kg family formats serve both diaspora households and mainstream consumers expanding their grain repertoire beyond pasta and wheat. Convenience and grocery stores. Other distribution channels, such as wholesale distributors, ethnic specialty importers, and cash-and-carry formats, provide volume throughput for smaller regional and unbranded basmati players serving cost-sensitive bulk buyers.

HoReCa advances at 19.74% CAGR through 2026-2031, the fastest of any distribution channel and nearly double the market-level average of 11.23%, as professional kitchens, airline caterers, and institutional canteens standardise procurement toward certified branded bulk formats over commodity rice. IndexBox estimates that HoReCa already accounts for 35–40% of total EU basmati consumption and is the fastest-growing end-use segment across Europe, driven by Indian, Middle Eastern, and Southeast Asian restaurant concepts and contract catering operations.

Geography Analysis

Asia-Pacific accounted for 44.52% of revenue in 2025 and is forecast to grow at 11.98% CAGR through 2031, making it the largest and fastest-moving regional block in the Basmati rice market. India remains the center of this picture because it is the main producer and a deep domestic consumption base at the same time. APEDA confirmed exports of 6.06 million metric tonnes to 154 countries in 2024-25, while domestic branded demand kept rising as packaged rice displaced loose retail in major cities. KRBL’s Q4 FY26 results linked its record domestic quarterly revenue of INR 1,230.00 crore, or USD 146.00 million, to stronger reach in Tier-2 and Tier-3 cities. Other Asia-Pacific markets such as Japan, South Korea, Singapore, and Australia are also absorbing more premium imports through restaurant discovery and ethnic retail.

The Middle East and Africa remains the most important external demand corridor for the Basmati rice market because it shapes export economics for nearly every major supplier. Saudi Arabia imported 11.73 lakh metric tonnes of Indian basmati in 2024-25, while Iran, Iraq, the UAE, and Yemen helped drive 61% of India’s export tonnage. That scale means changes in Gulf procurement, conflict exposure, and shipping insurance can quickly affect inventory planning across the Basmati rice market. Arabic trade monitors still showed inquiry activity from Saudi Arabia, Iraq, and the UAE through mid-2026 despite logistics pressure, which suggests that food security demand remained active. African markets such as Egypt, Morocco, Nigeria, and South Africa offer longer-term room for penetration as urban consumers trade up in packaged staples. Europe remains a quality-driven destination where the UK and EU codes of practice reward authentic, compliant brands and narrow the path for adulterated supply in the Basmati rice market.

North America is one of the highest-value destinations in the Basmati rice market because diaspora demand and mainstream trial are now working together. Demand from South Asian, Middle Eastern, and Caribbean communities still provides the base, while broader consumer interest in global grains supports premium shelf growth. The tariff changes disclosed by Ebro Foods created short-term pricing stress, but they did not change the structural appeal of basmati in U.S. retail. South America remains earlier in development, but Brazil, Argentina, and Chile are gradually building demand through premium urban retail and restaurant channels in the Basmati rice market.

Competitive Landscape

The Basmati rice market is concentrated at the processing and brand level, with a relatively small group of companies controlling most certified export supply and branded shelf presence. LT Foods and KRBL remain the central players because both combine scale, established brands, export reach, and channel-specific execution across India and overseas markets. LT Foods reported FY2025-26 consolidated revenue of INR 11,023.00 crore, or USD 1.31 billion, up 26% year over year, while KRBL reported its highest-ever domestic quarterly revenue of INR 1,230.00 crore, or USD 146.00 million, in Q4 FY26. That gives both companies room to invest in advertising, inventory, and product architecture at a level many smaller processors cannot match in the Basmati rice market.

Ebro Foods remains the strongest Western incumbent because Tilda gives it a trusted UK platform, while Ebro’s broader network supports distribution beyond one country. The company reported record adjusted EBITDA of EUR 420.60 million in 2025, even after absorbing a USD 10.00 million tariff impact tied to basmati and jasmine rice in the United States. Pakistan-origin companies such as Matco Foods and Unity Foods remain active competitors, especially in export-led and value-oriented corridors across the Middle East and Africa. Matco’s April 2026 decision to transfer Falak operations to a wholly owned subsidiary showed that organizational reshaping is also part of competition in the Basmati rice market, not just capacity addition. The competitive field is therefore split between high-equity branded leaders and aggressive export-focused challengers with narrower moats.

Strategic moves in 2025 and 2026 showed that the Basmati rice market is expanding through product depth, geography, and supply-chain control rather than through simple volume chasing. LT Foods launched DAAWAT Mazza Basmati Rice in Saudi Arabia and generated INR 23.00 crore, or USD 2.70 million, in inaugural revenue from that market, which reflected a branded push into the largest single-country importer. KRBL expanded into brown rice and low-GI variants, which signaled a stronger push into functional health positioning. Tilda expanded its sustainable farm network and widened its adjacent rice portfolio, which helped reinforce both sourcing credentials and category reach. Those actions suggest that the Basmati rice market will continue to reward companies that can combine traceable sourcing, brand trust, and channel-specific execution at scale.

Basmati Rice Industry Leaders

LT Foods

KRBL Limited

Ebro Foods, S.A.

Pansari Group

Matco Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: India Gate, KRBL Limited's flagship basmati rice brand, partnered with WPP Media to execute an out-of-home (OOH) campaign supporting the launch of its new India Gate Pulav basmati variant across key markets in Gujarat. The rollout aims to strengthen the brand's presence in the state.

- December 2025: AWL Agri Business Limited strengthened the branding of its Kohinoor Basmati Rice portfolio by appointing renowned Gujarati folk singer Aditya Gadhvi as its brand ambassador and launching a dedicated brand song, “Kohinoor by Aditya Gadhvi.” The music-led campaign aimed to deepen the brand’s cultural connection with consumers in Gujarat and other key western markets.

- May 2024: Matco Foods expanded the digital retail presence of its premium brand Falak by making the brand available on Noon UAE. The online listing includes Falak’s rice and spice range, allowing consumers across the UAE, including Dubai and Abu Dhabi, to order products through Noon’s e-commerce platform.

Global Basmati Rice Market Report Scope

| Brown Basmati Rice |

| White Basmati Rice |

| Parboiled Basmati Rice |

| Retail |

| Institutional |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Channels | |

| Other Distribution Channels | |

| HoReCa |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Brown Basmati Rice | |

| White Basmati Rice | ||

| Parboiled Basmati Rice | ||

| Packaging Size | Retail | |

| Institutional | ||

| Distribution Channels | Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | ||

| Online Retail Channels | ||

| Other Distribution Channels | ||

| HoReCa | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Basmati rice market by 2031?

The Basmati rice market is forecast to reach USD 11.16 billion by 2031, up from USD 6.55 billion in 2026.

What is driving faster growth in brown basmati rice?

Brown basmati is projected to grow at 12.24% CAGR because its lower glycemic profile and fiber content support stronger health positioning.

Which region leads the Basmati rice market?

Asia-Pacific leads with 44.52% share in 2025 and is also the fastest-growing region with 11.98% CAGR through 2031.

Why are institutional packs gaining traction?

Institutional packaging is projected to grow at 12.33% CAGR as restaurants, caterers, and other professional kitchens shift toward certified branded bulk packs.

Page last updated on: