United States Real Estate Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

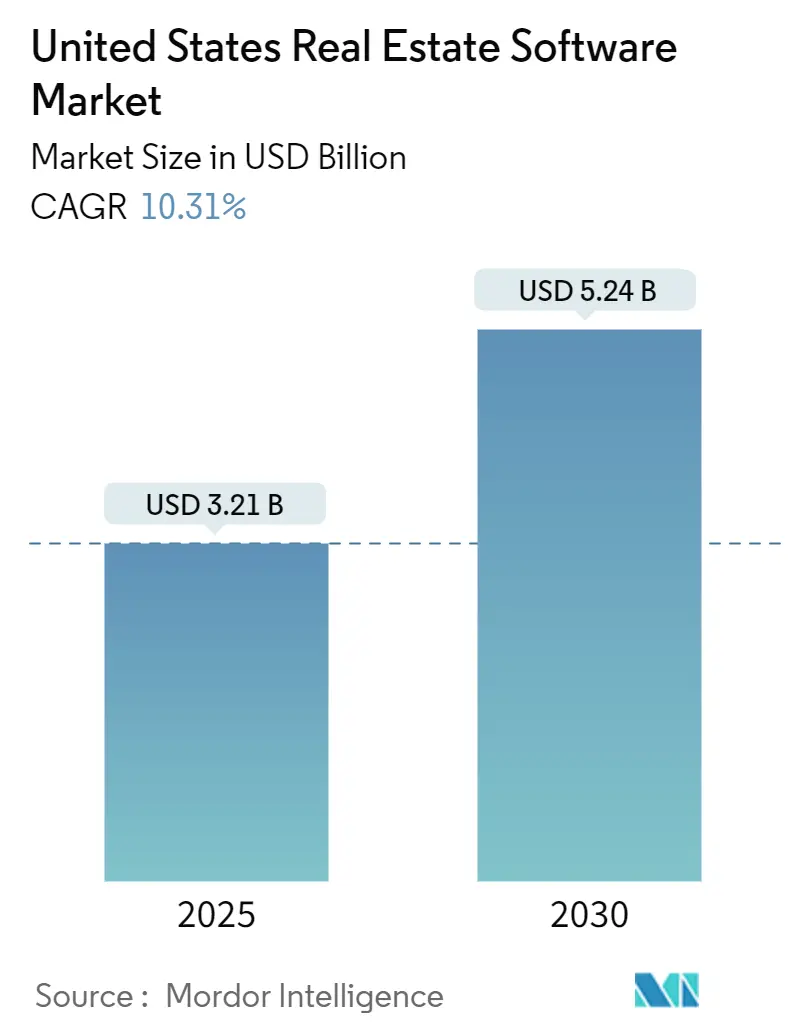

| Market Size (2025) | USD 3.21 Billion |

| Market Size (2030) | USD 5.24 Billion |

| Growth Rate (2025 - 2030) | 10.31% CAGR |

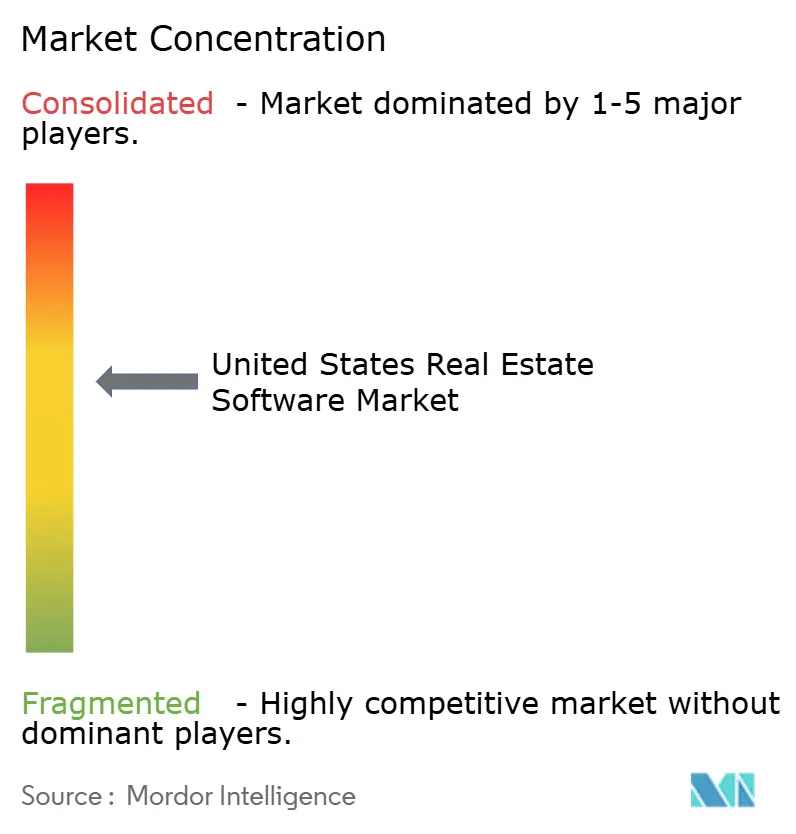

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Real Estate Software Market Analysis by Mordor Intelligence

The United States real estate software market is valued at USD 3.21 billion in 2025 and is projected to reach USD 5.24 billion by 2030, growing at a 10.31% CAGR. Rising venture-backed proptech funding, rapid cloud migration, stricter data-transparency rules, and AI-enabled workflow automation are accelerating software adoption across property management, brokerage, and investment functions. Market leaders are integrating predictive analytics, digital twin capabilities, and immersive 3D visualization into existing platforms to deepen client engagement and increase switching costs. Institutional investors’ record USD 3.2 billion allocation to proptech in 2024 underscores confidence that technology-centric operating models will widen performance gaps among real estate owners and intermediaries. Meanwhile, cybersecurity and privacy concerns, along with fragmented data standards, slow uptake among late adopters in highly regulated states. Overall, competitive dynamics favor vendors that combine robust compliance frameworks with modular, cloud-first architectures that can flex across residential, commercial, and corporate use cases.

Key Report Takeaways

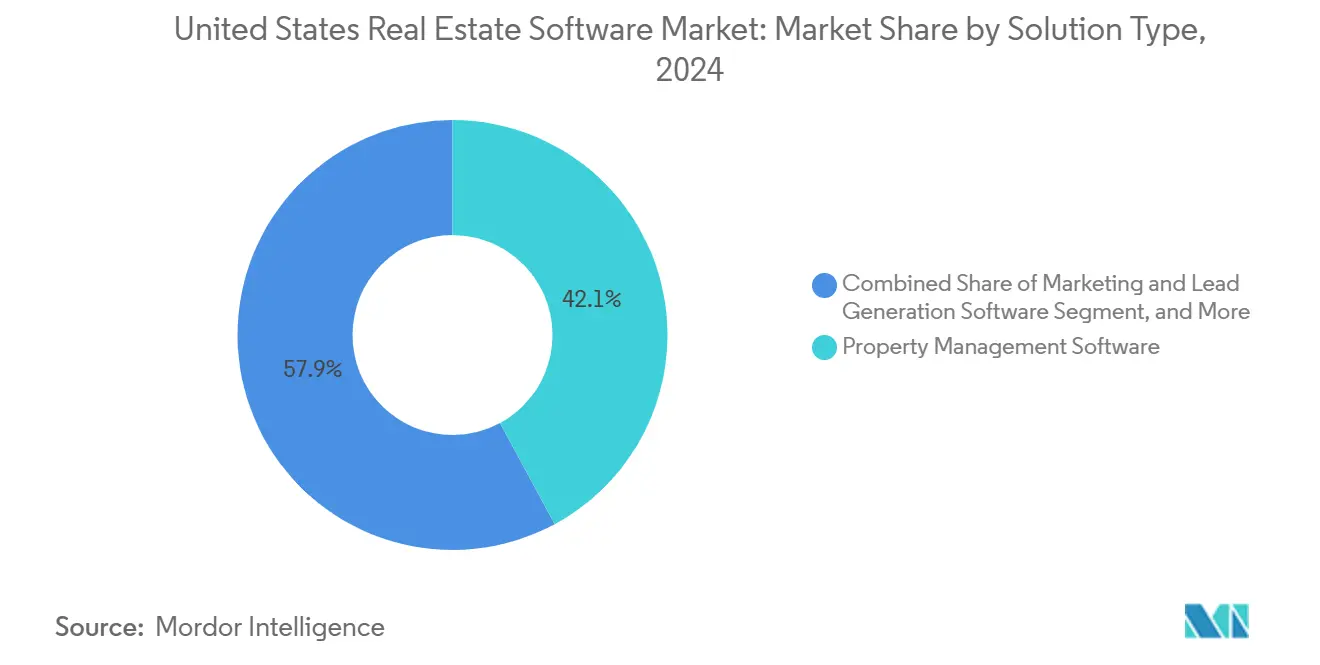

- By solution type, property management software led with a 42.12% share in 2024, while real estate CRM recorded the fastest growth rate of 10.43% through 2030.

- By deployment mode, cloud accounted for 78.16% of the United States Real Estate Software market share in 2024 and is projected to rise at a 11.57% CAGR to 2030.

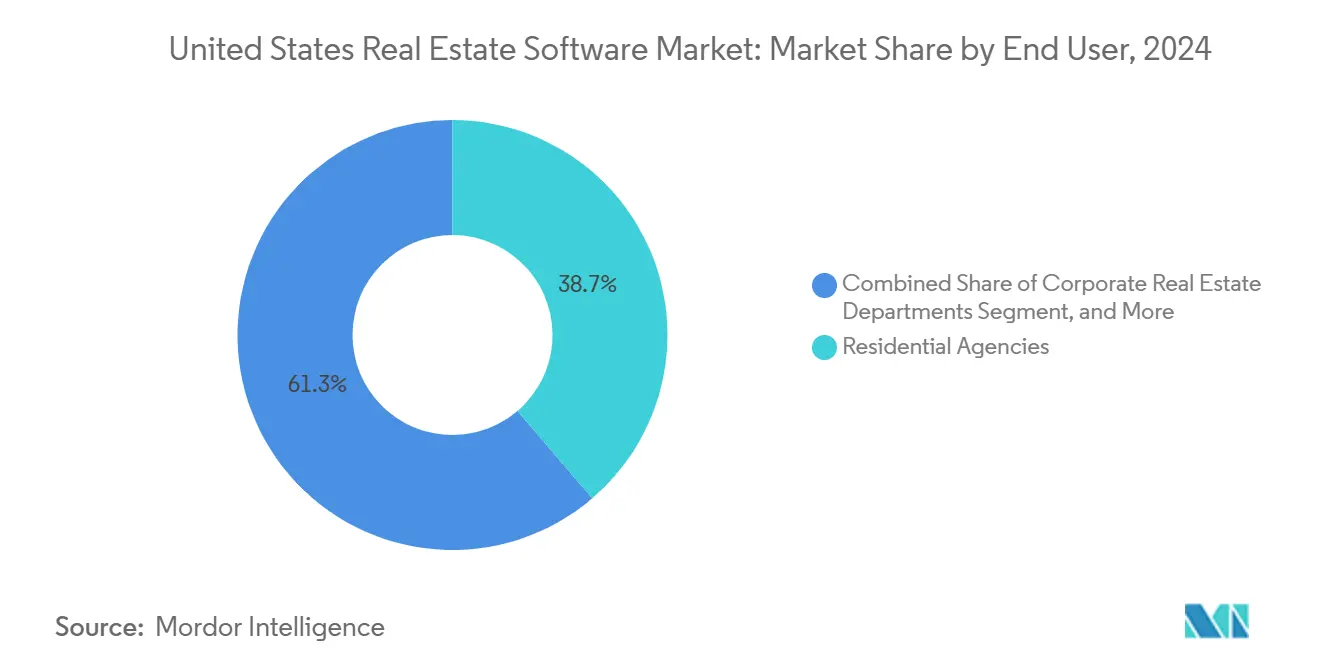

- By end user, residential agencies held a 38.73% revenue share in 2024, whereas corporate real estate departments are expected to advance at a 10.63% CAGR through 2030.

- By enterprise size, small and medium-sized enterprises represented 63.91% of the United States Real Estate Software market size in 2024 and are expected to expand at a 11.41% CAGR over the forecast period.

- By geography, the South captured a 35.36% share of the United States Real Estate Software Market in 2024, while the West is forecast to exhibit the fastest growth, with a 10.77% CAGR through 2030.

United States Real Estate Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating adoption of cloud-based property management platforms | +2.8% | National, early gains in West and South | Medium term (2-4 years) |

| Growing demand for integrated CRM and marketing tools among brokers | +2.1% | National, high-transaction markets | Short term (≤2 years) |

| Rising investments in proptech by institutional real estate investors | +1.9% | National, major metropolitan areas | Long term (≥4 years) |

| Increasing regulatory requirements for transaction transparency | +1.4% | National, varying state-level rules | Medium term (2-4 years) |

| Expansion of iBuyer ecosystems requiring real-time valuation software | +1.2% | West and South regions | Short term (≤2 years) |

| Emergence of digital twin integration for predictive maintenance | +0.9% | Major metropolitan commercial hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Cloud-Based Property Management Platforms

Cloud deployment reached 78.16% in 2024, up from 45% three years earlier, as hybrid work policies compelled property managers to access systems remotely.[1]Yardi Systems, “Annual Report 2024,” yardi.com Yardi’s Energy Relief suite illustrates the shift by enabling real-time utility optimization that cuts operating expenses by 12%. Lower upfront costs and subscription pricing enable small firms to adopt enterprise-grade functions quickly, thereby widening their competitive parity with larger companies. Enhanced audit trails and SOC 2 certification also align with tightening SEC and state-level data governance rules, reinforcing the cloud’s appeal among compliance-focused enterprises.

Growing Demand for Integrated CRM and Marketing Tools Among Brokers

Customer-acquisition costs have risen 40% since 2020, prompting brokers to consolidate their lead-generation and relationship-management workflows. AppFolio’s Realm-X, rolled out in 2024, combines AI lead scoring with automated nurturing to lift conversion rates by 25%.[2]AppFolio, “Q4 2024 Earnings Report,” investors.appfolio.com Tight integration reduces data silos, supports omnichannel outreach, and provides agents with predictive insights into client intent, a capability that drives the real estate CRM segment’s 10.43% CAGR.

Rising Investments in Proptech by Institutional Real Estate Investors

Institutional capital injected USD 3.2 billion into U.S. proptech startups in 2024, 15% above the prior year's level, despite broader venture capital pullbacks. Funds target AI valuation engines, automated property-management workflows, and blockchain transaction networks that compress settlement cycles. Pension and sovereign vehicles now allocate dedicated proptech sleeves, creating a stable pipeline of strategic funding that enables the rapid transition of novel tools from pilot to commercial scale, faster than in previous cycles.

Increasing Regulatory Requirements for Transaction Transparency

The Department of Justice's antitrust probe into RealPage’s rent-setting algorithms has spotlighted algorithmic accountability, and several states now mandate the disclosure of automated valuation model logic.[3]U.S. Department of Justice, “Justice Department Sues RealPage for Algorithmic Pricing Scheme,” justice.gov Vendors that can surface auditable datasets and decision trails gain adoption headroom, while smaller entrants face rising compliance costs that increase barriers to entry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and privacy concerns deterring adoption | −1.8% | National, heightened in California and New York | Short term (≤2 years) |

| High initial implementation and training costs for legacy firms | −1.3% | National, small firms most affected | Medium term (2-4 years) |

| Fragmented data standards across MLS and property databases | −0.9% | National, regional MLS variations | Long term (≥4 years) |

| Dependence on volatile API access policies of listing aggregators | −0.7% | National, high-volume markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns Deterring Adoption

Real estate software breaches increased by 67% in 2024, with the average incident cost reaching USD 4.8 million. California’s Consumer Privacy Act introduces significant non-compliance penalties, prompting many smaller firms to postpone migrations until vendors can certify their SOC 2 and ISO 27001 coverage. Because transaction data links sensitive personal and financial information, reputational risk from breaches can slow decision cycles, even when the ROI appears compelling.

High Initial Implementation and Training Costs for Legacy Firms

Comprehensive platform rollouts range between USD 150,000 and USD 500,000 and typically require 6-12 months for full utilization. Family-owned brokerages and regional operators often lack the necessary cash flow and dedicated IT staff to manage complex data migrations, which can delay the benefits of workflow automation. Vendors are experimenting with phased deployments, managed services, and consumption-based pricing, but capital constraints remain a headwind through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Property Management Leads While CRM Accelerates

Property management tools held 42.12% of the United States Real Estate Software market share in 2024, reinforcing their role as the operational core across residential and commercial assets. Conversely, CRM platforms expand at a 10.43% CAGR, reflecting brokers’ heightened focus on lifetime client value. Brokerage and transaction suites contribute 28.7%, serving as the backbone for deal execution, supporting title, escrow, and compliance workflows. Marketing and lead-generation applications occupy 8.9%, growing in tandem with digital advertising spending and omnichannel outreach requirements, while investment and portfolio analytics serve institutional owners at 15.2%. Integrated platform strategies are accelerating, with Yardi, RealPage, and CoStar bundling distinct modules to capture larger portions of customer spend.

Real Estate CRM vendors differentiate via AI-powered prospect scoring, campaign orchestration, and mobile-first interfaces that appeal to digital-native agents. Property management incumbents defend their share through deep accounting, maintenance, and resident portal functionality, yet must embed seamless API integrations to fend off specialized disruptors. Cross-module data visibility is emerging as a must-have, as owners increasingly demand unified dashboards that synthesize operational KPIs and tenant engagement metrics in real-time.

By Deployment Mode: Cloud Supremacy Reshapes Infrastructure

Cloud accounted for 78.16% of the United States Real Estate Software market size in 2024 and is advancing at a 11.57% CAGR, propelled by elastic scalability, automatic updates, and device-agnostic access. On-premise installations remain at 21.84%, largely within large enterprises that sunk costs into private data centers or adhere to strict on-site security mandates. SOC 2 audits, single-tenant architectures, and private cloud options alleviate lingering risk perceptions and open up hybrid pathways for cautious adopters.

Lower total cost of ownership, faster feature release cycles, and rising client expectations for mobile functionality position cloud vendors as default partners for small and medium enterprises. For large organizations, cloud adoption is increasingly driven by integration requirements with external data feeds, IoT sensors, and AI services that reside natively on public-cloud platforms. Consequently, migration roadmaps now blend lift-and-shift approaches for non-critical workloads with staged modernization of core transaction engines.

By End User: Corporate Departments Register Highest Growth

Residential agencies remain the largest user group at 38.73% in 2024 as consumer transactions dominate total deal volume, but corporate real-estate departments are the fastest climbers at 10.63% CAGR. Hybrid work has compelled Fortune 500 occupiers to rationalize their office footprints, necessitating granular space utilization analytics and flexible lease management modules. Commercial brokerages represent 24.8%, leveraging workflow platforms that integrate asset marketing, deal-room collaboration, and debt placement functions. Property-management firms account for 19.6%, relying on end-to-end suites covering tenant engagement, maintenance, and financial reporting, while investor-focused solutions serve 16.9%, combining acquisition pipelines, underwriting, and portfolio optimization.

The convergence of functionalities across user types intensifies platform competition. Vendors that deliver configurable interfaces, multi-entity accounting, and granular permissioning gain traction across various internal stakeholders, including asset managers and facilities teams.

By Enterprise Size: SMEs Dominate the Adoption Curve

Small and medium enterprises captured 63.91% market share in 2024 and are pacing at 11.41% CAGR, a trajectory enabled by subscription pricing that eliminates large capital outlays. Cloud-native architectures enable SMEs to implement best-practice processes without dedicated IT resources, thereby creating digital parity with their larger peers. Large enterprises hold 36.09%, prioritizing advanced customization, deep ERP integrations, and global support capabilities to manage complex, multi-jurisdictional portfolios.

Vendor roadmaps are increasingly featuring modular tiers that scale functionality and pricing to organization size. Embedded compliance and audit packages reduce the regulatory burden for SMEs, while enterprise clients utilize AI-driven anomaly detection, energy management analytics, and ESG reporting features that align with their corporate sustainability targets.

Geography Analysis

The South’s 35.36% share is driven by high transaction velocity and greenfield commercial projects, particularly in areas such as Austin, Dallas, Miami, and Atlanta. Companies deploy software to manage large multifamily pipelines, industrial property expansions, and build-to-rent portfolios that demand scalable tenant-experience and maintenance modules. State economic-development incentives further attract corporate headquarters, expanding the client base for vendor platforms.

The West is on track for the fastest 10.77% CAGR as technology employers accelerate the adoption of flexible workspaces and property valuations justify investments in premium, AI-enhanced analytics. California’s Consumer Privacy Act compels solution providers to embed granular consent management and real-time audit trails, establishing de facto technical standards that are later replicated nationwide.

The Northeast’s 28.4% share reflects dense urban markets where complex rent-control regulations push owners to adopt compliance-centric software. Transaction volumes in New York and Boston sustain demand for deal management, valuation, and investor-reporting tools that integrate seamlessly with institutional back-office systems. Midwest operators, comprising 21.7%, prioritize affordability and ease of implementation. Regional fragmentation among independent brokerages and property managers creates opportunities for SaaS vendors offering templatized onboarding, self-service configuration, and usage-based pricing that aligns with variable transaction cycles.

Competitive Landscape

Market concentration is moderate: Yardi, RealPage, and CoStar collectively command a sizeable share but face competitive pressure from AI-native startups targeting niche pain points. CoStar’s USD 1.6 billion purchase of Matterport embeds 3-D spatial analytics within its data ecosystem, signaling a strategic pivot toward immersive visualization capabilities. Yardi leverages deep accounting expertise to offer end-to-end suites that anchor strong customer relationships, while RealPage selectively invests in AI-driven rent optimization and resident engagement modules to defend multifamily strongholds.

Disruptors focus on mobile-first user experiences and point-solution excellence, particularly in digital closing, energy management, and ESG reporting. Cloud hyperscalers such as Microsoft and Google increasingly provide real-estate-specific toolkits atop their IaaS platforms, enabling partners to build vertical extensions that could disintermediate legacy vendors. Competitive moats now hinge on data network effects, open API ecosystems, and the ability to maintain compliance with rapidly evolving privacy and transparency mandates.

Incumbents respond by acquiring adjacent capabilities, forming strategic alliances with MLS organizations, and launching venture arms to invest in emerging partners. While top providers safeguard core accounting and lease-management revenue streams, white-space opportunities remain in predictive maintenance, occupancy analytics, and tokenized asset-trading infrastructures.

United States Real Estate Software Industry Leaders

Yardi Systems, Inc.

RealPage, Inc.

MRI Software LLC

AppFolio, Inc.

CoStar Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AppFolio announced a strategic partnership with Stripe to embed automated security‐deposit refund workflows, reducing average deposit return cycles from 21 days to five.

- March 2025: CoStar Group introduced Scout AI, a generative search assistant that delivers real-time market comps, zoning insights, and 3D parcel overlays to brokerage clients within its LoopNet interface.

- February 2025: RealPage launched a unified payments hub that consolidates rent, utilities, and ancillary fee processing into a single ledger, enabling property managers to cut reconciliation time by 40%.

- January 2025: Yardi Systems unveiled a beta version of its predictive maintenance engine that pairs digital twin data with IoT sensor feeds to forecast component failures up to 30 days in advance, targeting large multifamily portfolios.

United States Real Estate Software Market Report Scope

| Property Management Software |

| Brokerage and Transaction Management Software |

| Investment and Portfolio Management Software |

| Real Estate Customer Relationship Management (CRM) Software |

| Marketing and Lead Generation Software |

| Other Solution Types |

| Cloud |

| On-Premise |

| Residential Agencies |

| Commercial Agencies |

| Corporate Real Estate Departments |

| Property Management Firms |

| Real Estate Investors |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| By Solution Type | Property Management Software |

| Brokerage and Transaction Management Software | |

| Investment and Portfolio Management Software | |

| Real Estate Customer Relationship Management (CRM) Software | |

| Marketing and Lead Generation Software | |

| Other Solution Types | |

| By Deployment Mode | Cloud |

| On-Premise | |

| By End User | Residential Agencies |

| Commercial Agencies | |

| Corporate Real Estate Departments | |

| Property Management Firms | |

| Real Estate Investors | |

| By Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises |

Key Questions Answered in the Report

What is the current value of the United States Real Estate Software Market?

The market is valued at USD 3.21 billion in 2025 and is projected to grow to USD 5.24 billion by 2030.

Which deployment model is growing fastest in U.S. real estate software?

Cloud deployment dominates with 78.16% share in 2024 and is growing at a 11.57% CAGR through 2030.

Which solution segment has the highest growth outlook?

Real estate CRM platforms exhibit the fastest 10.43% CAGR as brokers prioritize integrated customer-engagement tools.

Which U.S. region offers the highest growth potential for vendors?

The West region posts the quickest 10.77% CAGR, driven by tech-centric adoption and privacy-compliance requirements.

What are the main barriers to software adoption among smaller firms?

Data-security concerns and upfront implementation costs deter many small and medium enterprises despite clear efficiency gains.

How concentrated is the competitive landscape?

The market scores 6 on a 1–10 scale, reflecting moderate concentration with room for niche disruptors alongside three dominant incumbents.

Page last updated on: