Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

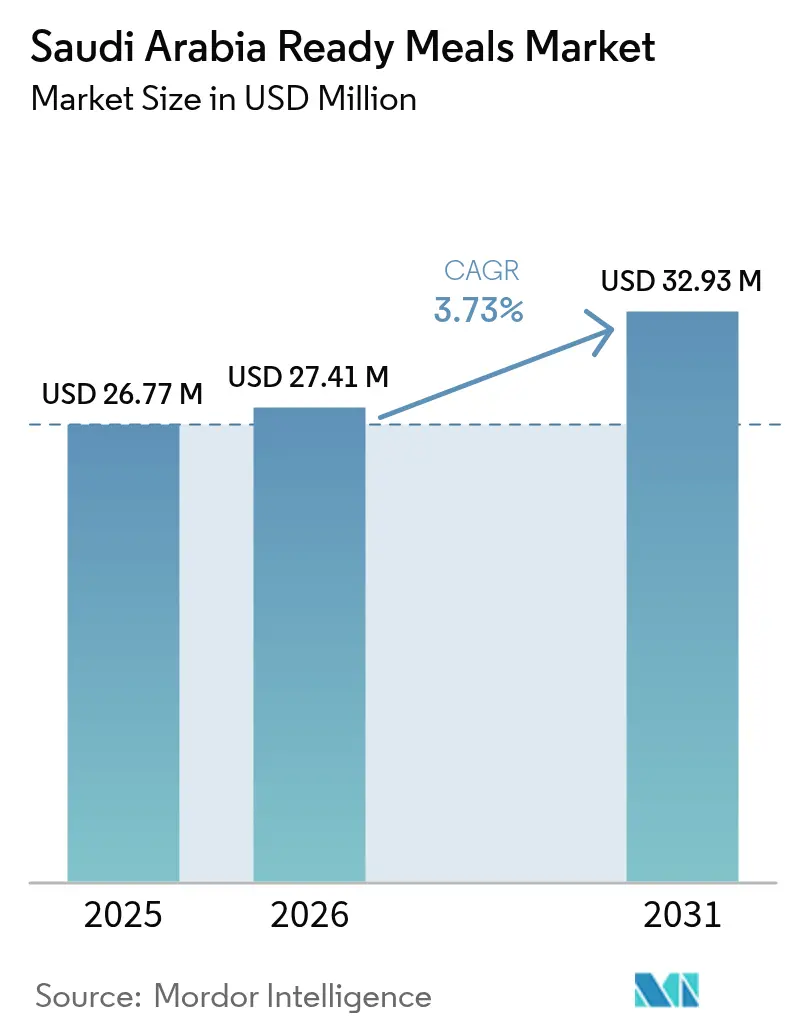

| Base Year Market Size (2025) | USD 26.77 Million |

| Market Size (2026) | USD 27.41 Million |

| Market Size (2031) | USD 32.93 Million |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

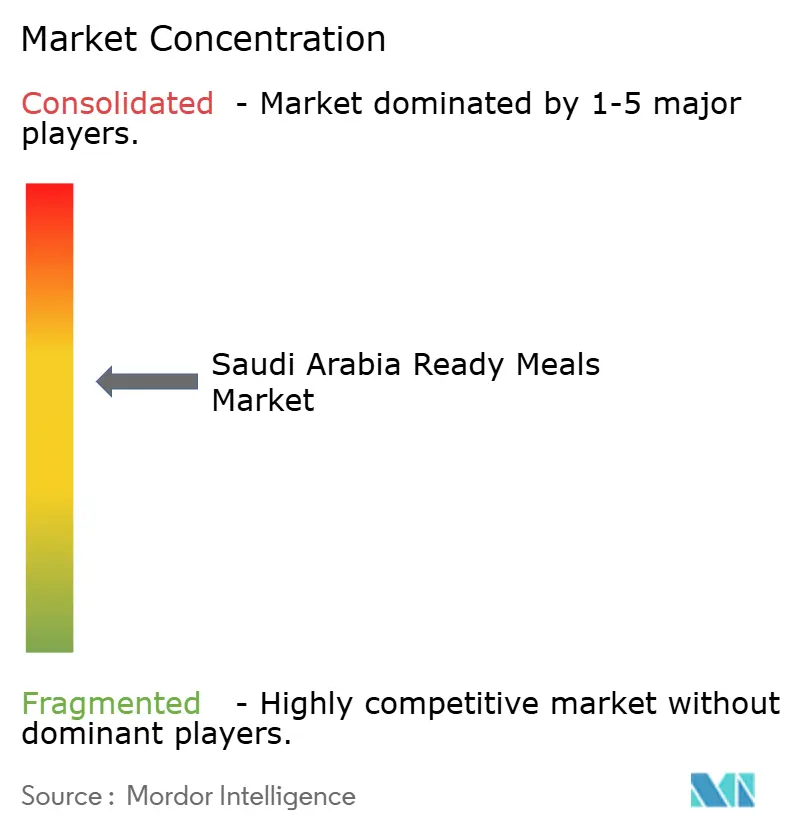

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Ready Meals Market Analysis by Mordor Intelligence

The Saudi Arabia ready meals market size is expected to grow from USD 26.77 million in 2025 to USD 27.41 million in 2026 and is forecast to reach USD 32.93 million by 2031 at 3.73% CAGR over 2026-2031. The measured growth trajectory conceals a significant structural shift in household meal preparation, influenced by the rise in female labor-force participation, projected to reach a notable percentage by 2025 under Vision 2030 mandates. This level of participation has historically driven significant growth in convenience food adoption across emerging markets. Frozen ready meals accounted for a substantial share of revenue in 2025, while chilled variants are projected to grow annually over the coming years. This growth reflects improvements in cold-chain infrastructure and a consumer preference for freshness over shelf-stable options. The online retail channel, though still developing, is growing steadily, driven by quick-commerce platforms that offer delivery times of under 30 minutes in cities like Riyadh and Jeddah. This trend is gradually reducing the dominance of traditional supermarkets, which held a significant market share in 2025. Additionally, demographic changes are reshaping demand patterns in ways that overall growth figures may not fully capture. Urban Saudi families are now predominantly nuclear households, a shift from the extended-family structure that was common a decade ago. These smaller households increasingly prefer portion-controlled formats to reduce food waste.

Key Report Takeaways

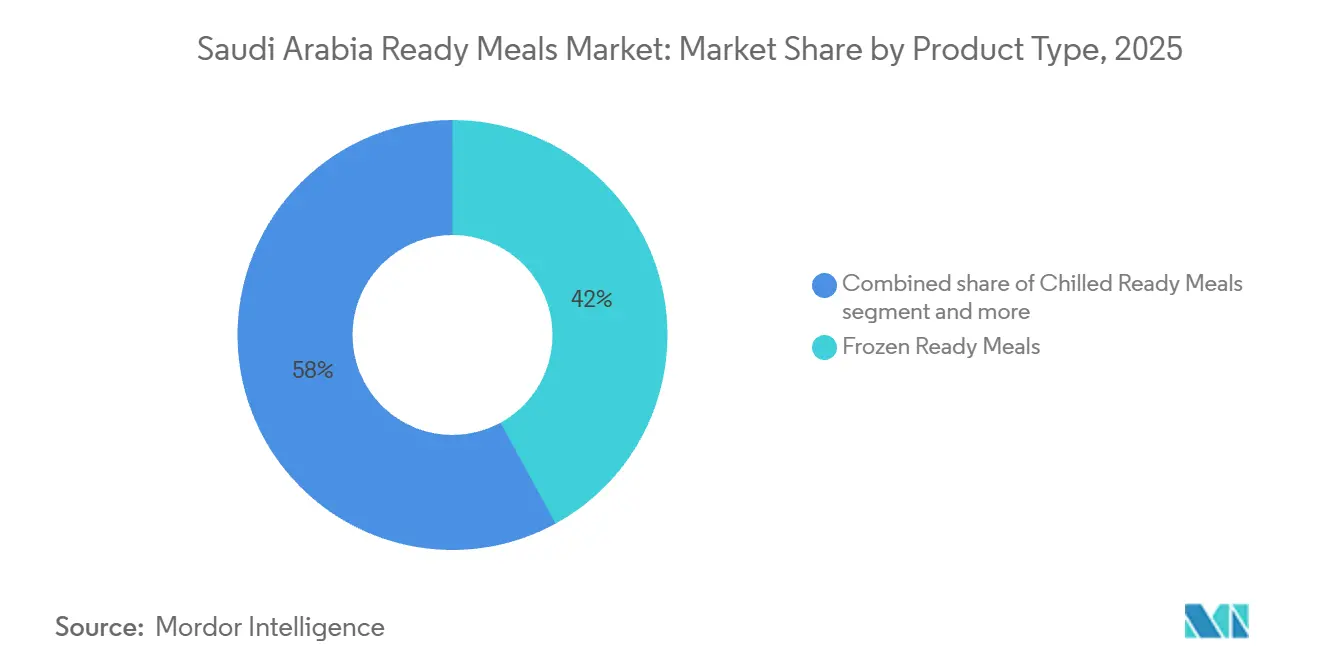

- By product type, frozen ready meals held 42.03% of the Saudi Arabia ready meals market share in 2025; chilled ready meals are forecast to expand at a 4.34% CAGR through 2031.

- By category, conventional products controlled 85.92% of the Saudi Arabia ready meals market size in 2025, while organic and free-from variants are projected to grow at a 5.48% CAGR to 2031.

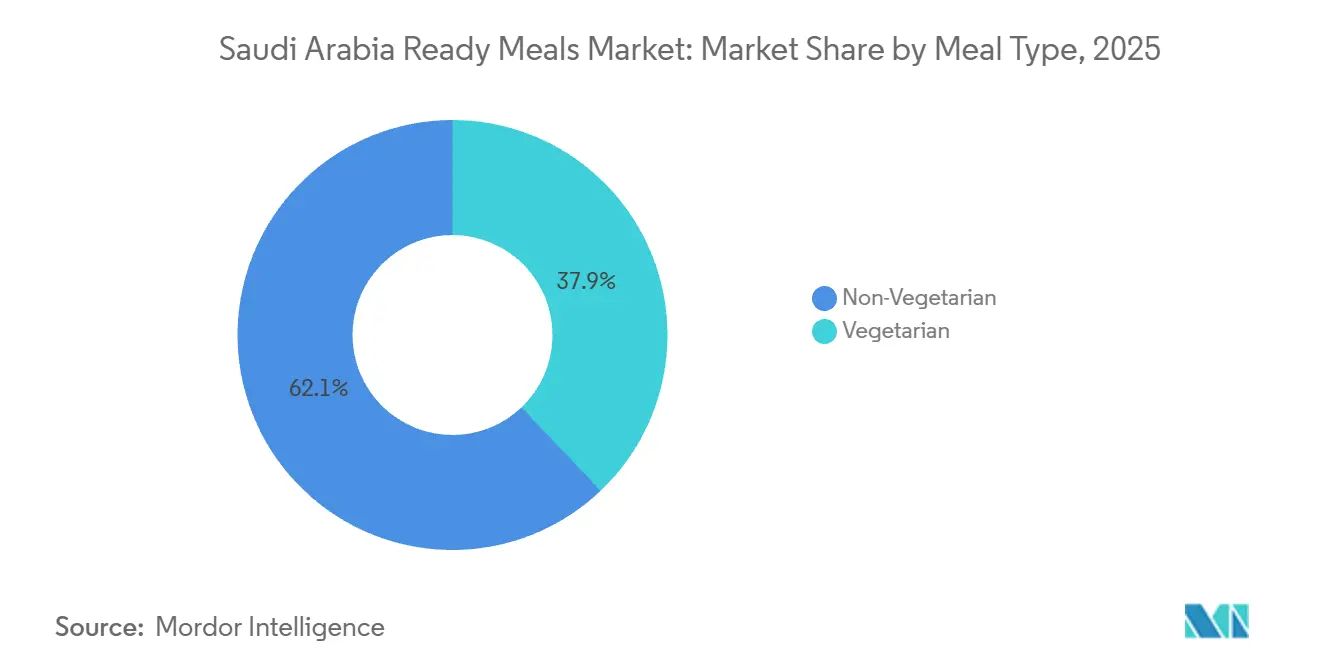

- By meal type, non-vegetarian offerings captured 62.11% revenue in 2025; vegetarian ready meals are advancing at a 4.21% CAGR between 2026-2031.

- By distribution channel, supermarkets and hypermarkets led with 48.32% of the Saudi Arabia ready meals market share in 2025, yet online retail is set to rise at 5.02% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Ready Meals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising working women reduce time for traditional home meal preparation | +1.2% | National, with concentration in Riyadh, Jeddah, and Eastern Province urban centers | Medium term (2-4 years) |

| Hectic lifestyles demand quick, on-the-go meal solutions | +0.9% | National, strongest in metropolitan areas with high expatriate populations | Short term (≤ 2 years) |

| Improved packaging makes products more attractive and convenient | +0.6% | National, with premium segments in affluent districts of major cities | Medium term (2-4 years) |

| Rise of nuclear families favors portion-controlled ready options | +0.8% | National, accelerating in newly developed residential zones | Long term (≥ 4 years) |

| Organic ready meals meet health-conscious consumer preference | +0.7% | Urban centers, particularly Riyadh Diplomatic Quarter and Jeddah Al-Hamra district | Medium term (2-4 years) |

| 24/7 convenience stores support impulsive last-minute purchases | +0.5% | National, with highest density in Riyadh, Jeddah, and Dammam metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising working women reduce time for traditional home meal preparation

Female labor force participation in Saudi Arabia has grown significantly in recent years, supported by Vision 2030 employment quotas and regulatory reforms, such as the removal of male-guardian consent requirements for women entering the workforce [1]Source: “Saudi Women’s Workforce Participation Reaches 35.6% in 2025,” Saudi Gazette, saudigazette.com.sa. This shift is reshaping household time management, with a growing preference for ready meals over traditional home-cooked options. A survey conducted among dual-income households in Riyadh revealed that a considerable percentage of respondents purchased ready meals multiple times a week. Convenience was highlighted as the primary factor driving this trend, ahead of taste or price. The link between rising female employment and the adoption of convenience foods is well-documented in developed markets. Typically, every 10% increase in female labor force participation correlates with a 15% to 20% rise in ready-meal consumption. Saudi Arabia is following a similar trend, although cultural preferences for home-cooked meals and multi-generational dining continue to moderate adoption rates compared to Western markets. Additionally, employers are influencing this trend by extending work hours and reducing mid-day breaks, leaving less time for meal preparation during traditional lunch periods.

Hectic lifestyles demand quick, on-the-go meal solutions

Urbanization and longer commute times are influencing meal habits in Saudi cities. By 2025, Riyadh's population exceeded 8 million, and the average one-way commute stretched to 47 minutes, a 12-minute increase since 2020, as residential development sprawls beyond the city's ring roads. This time compression is driving demand for portable, microwaveable formats that fit into car cup-holders and office microwaves. Convenience stores, which expanded to over 15,000 outlets nationwide by 2025, are capitalizing on this shift by installing refrigerated ready-meal sections and microwave stations, transforming from snack-focused outlets into quick-service meal destinations. Quick-commerce platforms such as Jahez and HungerStation reported that ready meals accounted for 18% of grocery orders in 2025, up from 9% in 2023, with peak demand occurring during evening hours when families seek last-minute dinner solutions. The Ministry of Transport's investment in metro and bus rapid-transit systems, which will connect 85 stations across Riyadh by 2030, is expected to further accelerate on-the-go consumption as commuters substitute sit-down meals for portable options consumed during transit.

Improved packaging makes products more attractive and convenient

Packaging innovations are bridging the sensory gap between ready meals and restaurant-quality offerings, which is a significant factor driving growth in the premium segment. Almarai introduced modified-atmosphere packaging for its chilled ready-meal line, extending shelf life without the use of preservatives. This advancement has enabled distribution to smaller cities that were previously inaccessible due to cold-chain limitations. Similarly, Sunbulah Group implemented steam-valve trays for its frozen rice-and-protein bowls, allowing microwave cooking without the need to puncture the film. This innovation reduces preparation steps and enhances texture retention, addressing common consumer concerns about soggy or unevenly heated microwaved meals. Sustainability is becoming an important consideration in packaging. Nestlé has pledged to use fully recyclable or reusable packaging for its Maggi ready-meal range in the Middle East, aligning with Saudi Arabia's circular economy goals under Vision 2030. Additionally, premium ready meals now incorporate Quick Response (QR) codes that link to recipe videos and ingredient sourcing information. This approach, inspired by European markets, aims to build trust with health-conscious consumers who are often skeptical of processed foods. The use of recyclable materials is expected to significantly contribute to achieving 100% sustainability targets in packaging.

Rise of nuclear families favors portion-controlled ready options

Household composition in Saudi Arabia is transitioning from extended, multi-generational units to nuclear families. This shift has been driven by government housing subsidies and mortgage programs, which have enabled many Saudis to purchase standalone homes in recent years. Nuclear households, which are smaller in size compared to extended families, generate less food waste when using portion-controlled ready meals instead of bulk cooking. This is particularly relevant in a country where food waste accounted for 33% of the total food supply in the previous year. Single-serve and two-serve formats made up the majority of chilled ready-meal stock-keeping units (SKUs) launched recently, reflecting manufacturers' focus on convenience for smaller households over per-unit cost savings. This demographic change has also reduced the social stigma previously associated with ready meals. While extended families often viewed pre-packaged meals as a hospitality shortcoming, nuclear households see them as practical, time-saving solutions. The trend is especially noticeable among young married couples in newly developed areas such as Riyadh's King Salman Park district, where a significant proportion of residents are under forty years old and dual-income households are common.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high preservatives and sodium content | -0.7% | National, with heightened sensitivity in affluent urban segments | Medium term (2-4 years) |

| Rising obesity risks linked to frequent ready meal consumption | -0.5% | National, with government intervention concentrated in high-prevalence regions | Long term (≥ 4 years) |

| Strict nutritional labeling and reformulation requirement | -0.4% | National, affecting all manufacturers selling packaged foods | Short term (≤ 2 years) |

| Supply chain disruptions cause product availability inconsistencies | -0.3% | National, with acute impact in smaller cities and remote areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns over high preservatives and sodium content

Consumer concerns about preservatives and sodium are increasing as health awareness grows and government initiatives highlight the risks of diet-related diseases. The Saudi Food and Drug Authority (SFDA) has mandated front-of-pack nutrition labels on all packaged foods, effective January 2025 [2]Source: Saudi Food and Drug Authority, “Eservices,” sfda.gov.sa. This regulation requires color-coded indicators for sodium, sugar, and saturated fat, making it more difficult for manufacturers to conceal high levels in ready-meal formulations. A 2025 analysis of ready-meal stock-keeping units (SKUs) available in Saudi supermarkets revealed that a significant proportion exceeded the World Health Organization's (WHO) recommended daily sodium intake per serving, with some frozen entrées containing extremely high levels. This increased transparency has driven reformulation efforts; for example, Americana Group reduced sodium content by 15% across its frozen ready-meal portfolio in 2025 by using potassium chloride and enhancing herb blends. However, taste-test panels reported a decline in flavor preference scores. The challenge is particularly significant for traditional Saudi recipes such as kabsa and mandi, where salt and spice levels are key characteristics. Organic and free-from variants, which are projected to grow at an annual rate through 2031, are attracting consumers willing to pay 30% to 40% premiums for clean-label assurances. However, these products are primarily available in premium supermarkets located in affluent neighborhoods, limiting their broader market impact.

Rising obesity risks linked to frequent ready meal consumption

In recent years, obesity prevalence among Saudi adults has reached concerning levels, marking the highest rate within the Gulf Cooperation Council. This has become a significant contributor to diabetes and cardiovascular diseases, which together account for a large proportion of deaths in the Kingdom [3]Source: “Obesity Prevalence in Saudi Arabia Reaches 35.5%,” WHO EMRO, emro.who.int. Public health authorities have increasingly linked the consumption of processed and convenience foods to this epidemic, creating reputational challenges for the ready-meals category. The Ministry of Health initiated a national campaign promoting home-cooked meals and limiting processed food consumption to twice a week. This message was reinforced through school curricula and social media influencers. The impact of these measures is particularly evident in the pediatric segment. Several school districts in Riyadh and Jeddah banned ready meals from cafeterias, citing concerns over childhood obesity rates, which exceeded 20% among children aged 10 to 14. In response, manufacturers have introduced calorie-controlled and macro-balanced products. For instance, Nestlé's Maggi "Balanced Plate" line limits each entrée to a specific calorie count and includes a defined amount of protein. However, these offerings face consumer skepticism, as ready meals are often associated with indulgence rather than nutrition. Looking ahead, sustained government intervention poses a potential risk to the category. Measures such as taxes on high-sodium or high-calorie processed foods could constrain market growth or drive demand toward unregulated informal channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chilled Variants Challenge Frozen Dominance

Frozen ready meals accounted for 42.03% of the market value in 2025, supported by Saudi Arabia's established frozen-food distribution networks and consumer familiarity with brands such as Al Kabeer and Sunbulah, known for their frozen appetizers and pastries. In contrast, chilled ready meals are projected to grow at an annual rate of 4.34% through 2031, marking the fastest growth among product types. This growth is driven by the maturation of cold-chain infrastructure and consumer preferences for chilled products, which are perceived as fresher and less processed compared to frozen alternatives. Almarai's investment of Saudi Riyal 300 million (approximately USD 80 million) in expanding chilled capacity at its Al-Kharj facility in 2025 reflects confidence in this trend, targeting premium consumers willing to pay 25% to 30% more for refrigerated meals that offer shorter shelf lives but avoid freezing-related texture degradation.

Shelf-stable ready meals, including retort-pouched and canned formats, hold the smallest market share due to taste and texture limitations, which Saudi consumers find unsuitable for primary meal occasions. However, these products maintain niche appeal for activities such as camping and emergency preparedness. The Saudi Food and Drug Authority's cold-chain certification program, introduced in 2024, is reducing spoilage rates in chilled distribution by requiring temperature-monitoring devices on refrigerated trucks. This initiative lowers retailer risks and supports the expansion of chilled meal assortments.

By Category: Organic and Free-From Variants Gain Premium Traction

Conventional ready meals accounted for 85.92% of the revenue in 2025, highlighting price sensitivity among middle-income households and the limited availability of organic and free-from alternatives outside major urban centers. However, organic and free-from variants are growing at an annual rate of 5.48% through 2031, the highest among all segmentation types. This growth is driven by affluent consumers in areas such as Riyadh's Diplomatic Quarter and Jeddah's Al-Hamra district, who prioritize clean-label claims over cost considerations. These products, which exclude artificial preservatives, flavor enhancers, and genetically modified ingredients, are priced 30% to 40% higher than conventional options but appeal to a demographic that views food as a health investment rather than a commodity.

Nestlé's Maggi "Garden Gourmet" line, launched in Saudi Arabia in 2025, includes plant-based proteins and organic vegetables sourced from European suppliers, targeting flexitarian consumers who are reducing meat consumption for environmental or health reasons. Local players are cautiously entering this segment. For instance, Tanmiah Food Company introduced a halal-certified organic chicken ready-meal range in late 2025. The company leverages its vertically integrated poultry operations to manage costs and ensure consistent supply.

By Meal Type: Vegetarian Options Expand Beyond Expatriate Niches

Non-vegetarian ready meals accounted for 62.11% of 2025 sales, reflecting Saudi Arabia's preference for meat-based cuisine and the cultural significance of dishes such as kabsa, mandi, and shawarma, which prominently feature lamb, chicken, or beef. In contrast, vegetarian ready meals are projected to grow at an annual rate of 4.21% through 2031. This growth is driven by expatriate communities from South Asia and the Levant, as well as a growing flexitarian trend among younger Saudis motivated by health and environmental concerns to reduce meat consumption.

Zen Frozen Foods, a Dubai-based company, entered the Saudi market in 2024 with a vegetarian ready-meal line featuring Indian and Thai recipes, targeting the Kingdom's 13 million expatriates seeking familiar flavors not widely available from local producers. Almarai tested vegetarian offerings in 2025 but discontinued them after six months due to low demand, highlighting the niche status of vegetarian meals among Saudi nationals, who often perceive them as side dishes rather than complete meals. The growth of the vegetarian segment depends more on changing consumer perceptions than on supply constraints. While Saudi supermarkets offer abundant fresh produce, legumes, and dairy, ready-meal manufacturers have been slow to develop convenient vegetarian options that appeal to busy consumers.

By Distribution Channel: Online Retail Disrupts Supermarket Hegemony

Supermarkets and hypermarkets accounted for 48.32% of ready-meal sales in 2025, maintaining a dominant position due to extensive refrigerated shelf space, promotional pricing strategies, and long-established consumer shopping habits. However, online retail is experiencing the fastest growth among distribution channels, expanding at an annual rate of 5.02% through 2031. This growth is driven by quick-commerce platforms that reduce delivery times and eliminate challenges such as parking, queuing, and checkout, which often deter time-constrained consumers. For example, Jahez, a Saudi-based quick-commerce application, reported delivering ready meals within 30 minutes of order placement. Additionally, Noon, a Dubai-based e-commerce company, partnered with Almarai and Americana in 2025 to offer exclusive ready-meal bundles available solely on its platform. This approach leverages digital channels to test new products without the shelf-space constraints faced by physical retailers. The shift toward online retail is particularly evident in Riyadh and Jeddah, where traffic congestion and expansive urban layouts make online ordering more convenient than visiting supermarkets.

Convenience stores, which held a smaller market share in 2025, are transforming into meal-solution hubs by incorporating refrigerated sections and microwave stations to facilitate on-site consumption. Circle K, a Canadian convenience-store chain, announced plans in 2025 to expand to 300 locations across Saudi Arabia by 2028. Each store will feature a dedicated ready-meal section and seating area, creating a format that merges elements of retail and quick-service restaurants.

Geography Analysis

Saudi Arabia's ready-meals market shows clear regional differences shaped by urbanization, income levels, and the state of cold-chain infrastructure. In 2025, Riyadh and Jeddah together accounted for approximately 58% of national sales, driven by higher per-capita incomes, greater female workforce participation, and well-developed retail networks that support both chilled and frozen distribution. The Eastern Province, which includes Dammam and Khobar, contributed about 18% of sales, benefiting from a high-income expatriate workforce tied to the petrochemical industry and its proximity to Bahrain, a regional logistics hub for imported ready meals. On the other hand, smaller cities such as Abha, Tabuk, and Hail remain underserved due to limited cold-chain infrastructure and lower population densities, making dedicated distribution routes for chilled products economically unviable.

The Saudi government is working to address these regional disparities through the National Industrial Development and Logistics Program (NIDLP), which allocated Saudi Riyal SAR 12 billion in 2025 to improve cold-storage facilities and refrigerated transport fleets. This initiative aims to bridge geographic gaps in the market by 2030. Urbanization trends are concentrating demand in mega-cities while also creating opportunities in smaller but growing population centers. Riyadh's population exceeded 8 million in 2025, and the city's ongoing expansion under the Riyadh Metro project, which will connect 85 stations by 2030, is expected to further densify residential and commercial zones. This development is likely to increase foot traffic in supermarkets and convenience stores, which are key channels for ready-meal sales.

As urbanization continues to grow, the demand for ready meals is becoming increasingly concentrated in major cities, with Riyadh and Jeddah accounting for a significant percentage of total sales. However, the government's investment in cold-chain infrastructure under the National Industrial Development and Logistics Program (NIDLP) is expected to create new opportunities in underserved regions, potentially reducing this gap by 2030. This initiative could enable smaller cities such as Abha, Tabuk, and Hail to gain better access to chilled and frozen ready-meal products, fostering more balanced growth across the country.

Regulatory Landscape

Ready meals sold in Saudi Arabia are regulated primarily by the Saudi Food and Drug Authority (SFDA) under the Kingdom's Food Law and its implementing rules for food safety, hygiene, and labeling. For imported ready meals, SFDA food import control requirements emphasize registration and clearance processes, including foreign establishment registration and product compliance checks, which affect market entry timelines and the documentation burden for cross-border brands.

Health and transparency-driven requirements are also tightening compliance for both retail packs and ready-to-eat offerings supplied into foodservice. From January 2025, SFDA mandated front-of-pack nutrition labeling for packaged foods, increasing formulation and labeling discipline for frozen and chilled ready meals, especially around sodium, sugar, and saturated fat disclosure. In parallel, menu nutrition disclosure rules effective July 1, 2025 (including sodium indicators) raise the bar for ready-meal suppliers selling through foodservice or hybrid retail-foodservice formats, reinforcing reformulation activity and more stringent claim substantiation.

Value Chain Analysis

The Saudi ready-meals value chain starts with raw-material sourcing (meat, poultry, grains, dairy, vegetables, oils, spices) and packaging inputs, followed by processing, portioning, cooking, and rapid chilling or freezing. Large local and regional manufacturers (including Almarai, Sunbulah, Americana, and poultry-linked players) benefit from integrated procurement and quality systems, while smaller brands rely more on co-manufacturing and imported ingredients. Upstream food-security initiatives also shape input availability: in April 2025, SALIC launched the National Grain Supply Company (SABIL) to manage strategic reserves across 14 silo branches, supporting staple grain logistics that feed into multiple processed-food categories.

Midstream execution depends on cold-chain performance and compliance. Cold-chain logistics is a stated priority under Vision 2030, and the market relies on temperature-controlled warehousing and reefer transport to keep chilled lines viable beyond major metros. SFDA cold-chain and hygiene requirements reinforce process control, inspection readiness, and documentation across transport and storage. Downstream distribution runs through supermarkets/hypermarkets, convenience stores with refrigerated bays and microwaves, and online quick-commerce platforms that require dense urban fulfillment and short order-to-delivery windows. These last-mile expectations push manufacturers toward shorter shelf-life planning, tighter demand forecasting, and closer coordination with retailers and 3PLs.

Competitive Landscape

The Saudi Arabia ready-meals market shows moderate consolidation, with a few large players holding significant market share while facing competition from niche entrants and regional specialists. Established local companies such as Almarai and Sunbulah benefit from vertically integrated supply chains and strong brand equity developed over decades in related categories. Meanwhile, multinational corporations like Nestlé and General Mills leverage global research and development resources and substantial marketing budgets to introduce premium and health-focused product variants. For instance, Almarai's SAR 300 million investment in chilled ready-meal expansion, planned for 2025, highlights the capital-intensive nature of competing in the premium segment, where cold-chain reliability and efficient distribution are critical for success. Smaller players, including Zen Frozen Foods and Tanmiah Food Company, are focusing on niche markets such as vegetarian, organic, and halal-certified offerings, which remain underserved by traditional portfolios tailored to conventional Saudi preferences. Additionally, technology adoption is becoming a key competitive advantage. For example, Americana Group implemented artificial intelligence (AI)-powered demand forecasting in 2025 to minimize inventory waste and optimize stock-keeping unit (SKU) assortments by store location, a capability that smaller competitors often lack.

White-space opportunities in the Saudi Arabia ready-meals market are concentrated in three key areas: organic and clean-label products, online-exclusive formats, and vegetarian or plant-based meals. The organic segment is projected to grow at an annual rate of 5.48% through 2031, outpacing the overall market growth by 47%. However, distribution of organic products remains largely limited to premium supermarkets, presenting an opportunity for direct-to-consumer models that can bypass retail markups and cold-chain challenges. Online-exclusive ready meals offer manufacturers the flexibility to produce smaller batches and test innovative concepts, such as fusion cuisines and varied portion sizes, without the need for shelf-space commitments from physical retailers. Vegetarian offerings, while still a niche segment, are underrepresented by incumbents focused on meat-centric Saudi preferences. This gap provides an opportunity for companies like Zen Frozen Foods to build a loyal customer base among expatriates and flexitarian consumers.

The Saudi Food and Drug Authority's front-of-pack labeling mandate, effective January 2025, is expected to favor manufacturers with the ability to reformulate products and maintain transparent supply chains. Companies reliant on high-sodium or preservative-heavy recipes may face challenges under the new regulations. This shift underscores the importance of innovation and adaptability in maintaining competitiveness within the evolving market landscape.

Saudi Arabia Ready Meals Industry Leaders

Sunbulah Group

Americana Group

Almarai Company

JBS Foods SA

Almunajem Foods

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven nutrition transparency is creating room for reformulated and clearly positioned ready meals, especially lower-sodium and cleaner-label options that still match local taste profiles. With SFDA front-of-pack labeling in force from January 2025 and additional nutrition disclosure rules effective July 1, 2025 for food establishments, manufacturers that can substantiate claims, manage shelf-life stability, and standardize nutrition data across SKUs have a clearer path to premium shelf space and digital assortment curation. This aligns with SKU architecture shifts already visible in the market, including portion-controlled chilled meals linked to nuclear households and reduced waste objectives.

Industrial infrastructure and ingredient localization initiatives also broaden the opportunity set beyond finished meals into adjacent inputs that improve cost and resilience for protein-rich ready meals. State-backed food manufacturing ecosystems such as the Jeddah Food Cluster (launched in 2024) provide integrated logistics and lab services that reduce friction for scale-up and compliance testing, which is especially relevant for chilled lines that require tighter microbiological control. On the ingredient side, March 2026 announcements around large-scale alternative protein capacity, including Unibio signing an agreement for a gas-fermentation single-cell protein facility in Saudi Arabia and a SAR 1.4 billion bio-protein project in Jubail Industrial City tied to aquaculture supply chains, point to an expanding domestic base for high-protein formulations that can be incorporated into ready meals and meal kits over time.

Recent Industry Developments

- April 2026: Americana Foods inaugurated a new corporate office in Jeddah and linked the move to scaling its presence in the frozen food ecosystem, including potato processing. The added on-ground operating capacity supports faster coordination with local customers and partners and strengthens execution for downstream categories that overlap with ready meals, such as frozen, ready-to-heat meal components.

- November 2025: Sunbulah Group signed a strategic partnership with Barn's Coffee to distribute products through the foodservice channel in Saudi Arabia. The agreement expands route-to-market reach beyond retail freezers into out-of-home consumption points that increasingly stock heat-and-eat or ready-to-serve items.

- November 2024: JBS opened a USD 50 million chicken nugget facility in Jeddah, quadrupling its production capacity in Saudi Arabia under its Seara brand. The capacity addition increased local availability of value-added, ready-to-eat protein products that compete for freezer space and meal occasions alongside frozen ready meals.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers ready meals sold in Saudi Arabia that are prepared and packaged for quick consumption at home, mainly in frozen, chilled, or shelf-stable formats, and captured at retail value.

Scope exclusions: Restaurant meals and made to order foodservice dishes are excluded, and ingredients sold as meal kits are also excluded.

Segmentation Overview

- By Product Type

- Frozen Ready Meals

- Chilled Ready Meals

- Shelf Stable

- By Category

- Conventional

- Organic/Free-From

- By Meal Type

- Vegetarian

- Non-Vegetarian

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the demand context and align the product scope to what consumers typically buy as ready meals in Saudi retail. We reviewed public sources such as the General Authority for Statistics (Saudi Arabia) for population and household indicators, SAMA for consumer spending signals, and Saudi Food and Drug Authority publications for food labeling and compliance cues that influence packaged meals.

We also used sources such as UN Comtrade for trade direction checks on packaged food categories, FAO data for broader food supply trends, and peer reviewed nutrition and cold chain papers to understand how chilled and frozen adoption can shift over time. Company annual reports, investor presentations, and reputable press were used to map distribution expansion and pricing moves, and a paid subscription database was used selectively for company financials, news screening, and patent lookups related to packaging and preservation. These sources are illustrative only, and many other public references were used to collect inputs, validate them, and clear up open questions.

Primary Interviews and Surveys

Primary work was used to confirm what is really counted as a ready meal on shelf, and to pressure test pricing, promo depth, and channel mix across modern retail and online. We spoke with a mix of manufacturers, importers, distributors, and retail category teams, and then validated the output with operations and sales managers who see volumes and shrink patterns in chilled and frozen lines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | |

| Mid tier: 49% | Functional/Unit leaders: 32% | |

| Smaller Players: 20% | Managers: 53% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where packaged food spending and retail channel splits are reconstructed into a ready meals demand pool for Saudi Arabia, and then filtered by the share of frozen, chilled, and shelf-stable formats that qualify as ready meals. To keep it grounded, we then corroborate the totals using selective bottom-up approximations, such as sampled SKU price points times observed sales cadence from retailer and distributor checks, followed by sanity checks against supplier mix and import exposure.

Key inputs in the model include format mix shifts (frozen versus chilled), the online retail share for packaged meals, average selling price movement driven by promo intensity, cold chain expansion that supports chilled penetration, and changes in household structure and working population that affect convenience demand. Forecasting uses scenario analysis, supported by simple time-series smoothing on pricing and channel shares, and then refined based on expert views on how quickly chilled lines expand versus frozen. When bottom-up signals are missing for smaller labels or niche cuisines, the gap is handled with category-level ASP bands and conservative volume proxies that are reviewed during primary validation.

Data Validation & Update Cycle

Outputs are checked through multiple steps so the final number stays consistent with real world signals. We compare the model against independent indicators like packaged food inflation, channel expansion news, and observable changes in freezer and chiller space, and then investigate any sharp jumps that do not match these signals.

A second analyst reviews key assumptions, including format definitions and pricing logic, before sign-off. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, step changes in retail pricing, or a clear shift in distribution coverage. Before delivery, we do a fresh review pass to ensure the latest public updates and interview learnings are reflected.

Mordor Intelligence's Saudi Arabia Ready Meals Market Market Estimate Compared With Other Published Estimates

Published market values for ready meals in Saudi Arabia can look far apart, and this usually happens because the scope is not aligned, pricing assumptions differ, and the refresh timing is not the same. We also see differences when some studies rely heavily on broad processed food ratios and do not validate them with channel checks.

Some external estimates bundle a wider ready-to-eat universe that can include snacks and other prepared packaged foods sold for quick consumption at home. For Mordor Intelligence, the count is limited to packaged ready meals in frozen, chilled, and shelf-stable formats, and restaurant prepared dishes and meal kits sit outside the scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 26.77 M (2025) | |

| Regional Consultancy A | USD 36.00 M (2025) | Applies a broader ready-to-eat definition and faster price progression, which can inflate value when promo depth and channel mix are not rechecked against retail conditions. |

| Industry Publisher B | USD 18.53 M (2024) | Tracks a narrower ready-to-eat subset and likely undercounts frozen and chilled ready meals sold through modern retail, with limited treatment of online retail growth and format mix shifts. |

The spread in published numbers is mainly explained by what gets included as a ready meal, plus how prices and channels are treated over time. By tying the value build to format mix, channel shares, and practical ASP bands that can be revalidated, our estimate stays repeatable for planning discussions.

Key Questions Answered in the Report

How fast is the Saudi Arabia ready meals market expected to grow to 2031?

It is projected to expand from USD 27.42 million in 2026 to USD 32.93 million by 2031, registering a 3.73% CAGR.

Which segment is gaining ground against frozen meals?

Chilled ready meals are advancing at 4.34% annually, outpacing other product types as cold-chain upgrades reassure consumers about freshness.

What role does online retail play in ready-meal sales?

Online channels, led by quick-commerce apps like Jahez, are projected to grow at 5.02% CAGR, eroding supermarket dominance by offering 30-minute deliveries.

Why are organic and free-from ready meals important?

Though only 14.08% of sales in 2025, they grow at 5.48% annually, catering to affluent consumers seeking clean-label assurances and lower sodium levels.

How are health concerns influencing product reformulation?

Front-of-pack labels expose high sodium and preservative levels, prompting manufacturers like Americana to cut sodium by 15% and launch calorie-controlled lines.

Page last updated on: