Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 29.89 Billion |

| Market Size (2026) | USD 31.56 Billion |

| Market Size (2031) | USD 41.44 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

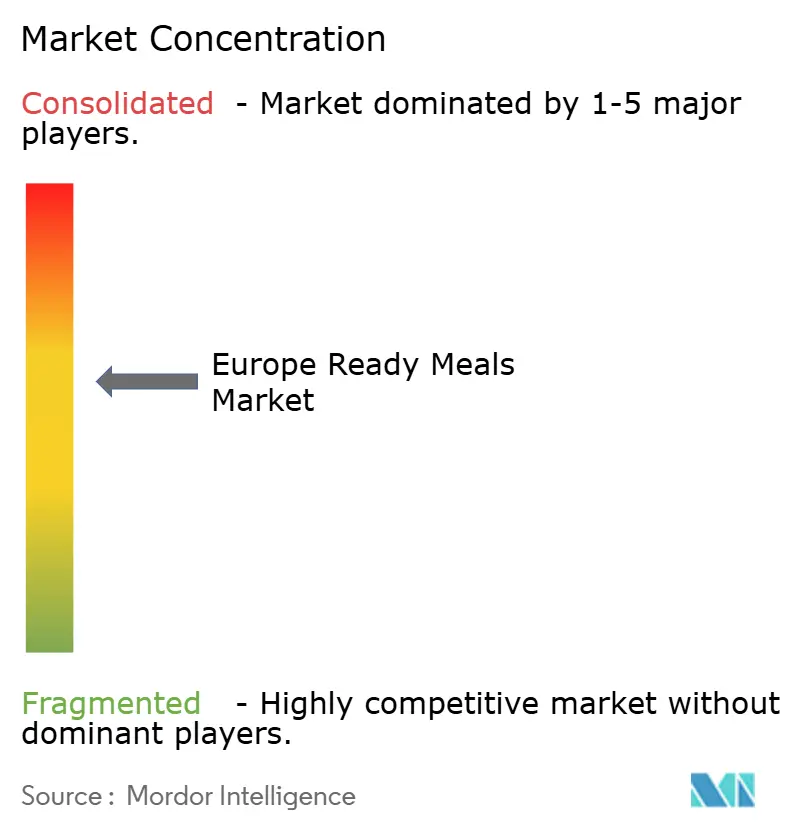

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ready Meals Market Analysis by Mordor Intelligence

The Europe ready meals market size is expected to grow from USD 29.89 billion in 2025 to USD 31.56 billion in 2026 and is forecast to reach USD 41.44 billion by 2031 at 5.6% CAGR over 2026-2031. The market's expansion reflects fundamental changes in European consumer behavior, with busy professionals and families increasingly seeking convenient meal solutions. The implementation of Europe Regulation 2025/40 on recyclable packaging is reshaping manufacturers' operational costs, while the moderation in food inflation to 2.4-4.9% enables companies to maintain more stable pricing strategies. The market benefits from several demographic shifts, including the continued trend of urbanization, the ongoing reduction in average household sizes, and the sustained increase in female workforce participation - factors that collectively strengthen the demand for quality, pre-portioned meals. The competitive environment continues to evolve as established food manufacturers leverage their extensive supply chain networks and distribution capabilities, while innovative start-ups address emerging consumer preferences for plant-based options, personalized nutrition, and sustainable products. The growth of digital platforms, especially quick-commerce applications, has created new distribution channels, particularly resonating with millennial and Gen Z consumers who prioritize convenience and immediate delivery options.

Key Report Takeaways

- By type, frozen ready meals led with 39.78% of Europe ready meals market share in 2025; freeze-dried ready meals are forecast to advance at a 5.78% CAGR through 2031.

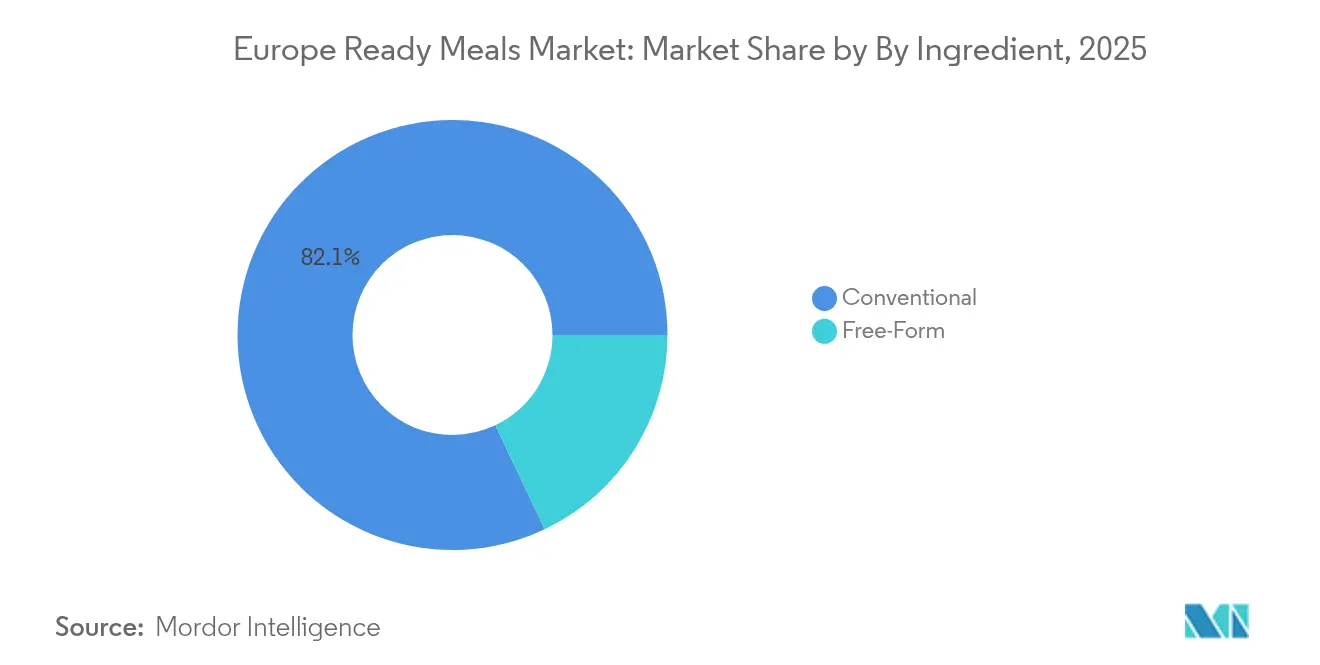

- By ingredient, conventional formulations accounted for 82.05% of the 2025 Europe ready meals market; free-form lines are projected to grow at a 6.05% CAGR between 2026-2031.

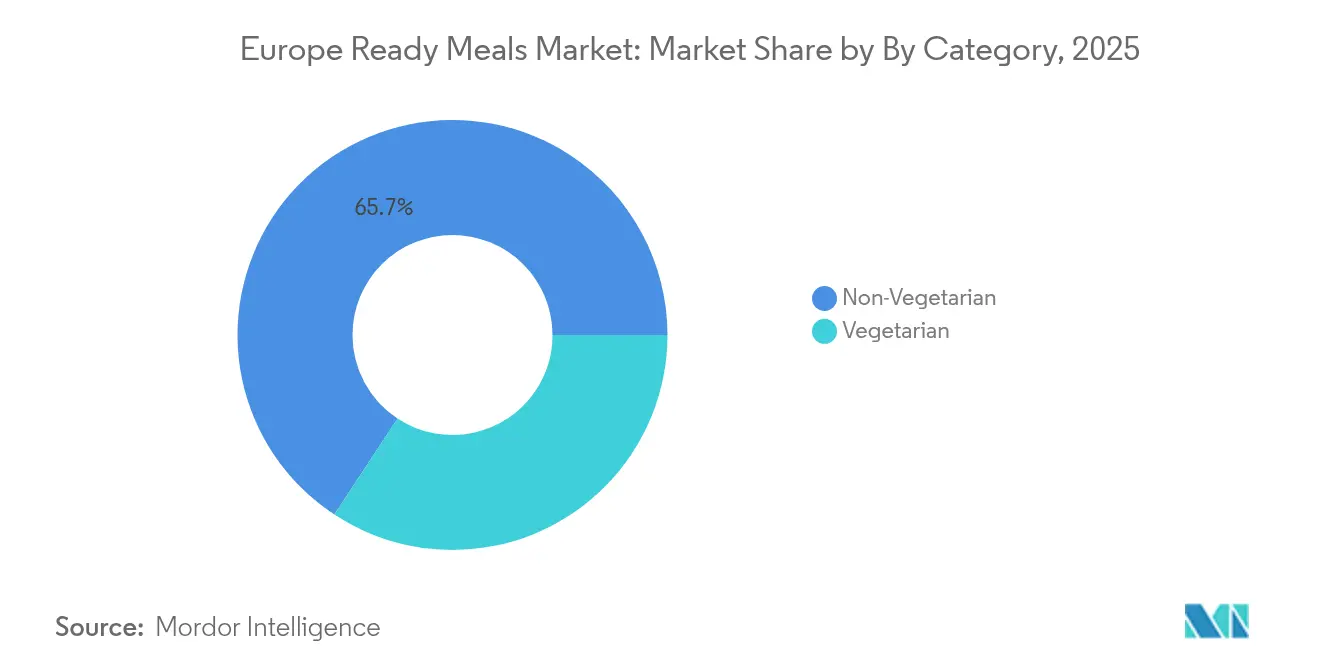

- By category, non-vegetarian SKUs captured 65.74% of 2025 sales while vegetarian lines are set for a 6.45% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets controlled 53.10% of 2025 sales, yet online retail stores are expected to post a 9.28% CAGR through 2031.

- By geography, the United Kingdom held 19.72% of 2025 value, whereas Italy is on track for the fastest 6.95% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ready Meals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising trend of on-the-go consumption demanding convenience and portability | +1.2% | Global, with stronger impact in United Kingdom, Germany, Netherlands | Medium term (2-4 years) |

| Innovations in product formats, flavors, and nutritional profiles | +0.9% | Europe-wide, particularly Italy, France, Spain | Long term (≥ 4 years) |

| Expansion of personalized meal options | +0.7% | Northern Europe, urban centers across Europe | Long term (≥ 4 years) |

| Advances in packaging technology enhancing shelf life and sustainability | +0.8% | Europe-wide due to Regulation 2025/40 compliance | Medium term (2-4 years) |

| Growing consumer acceptance of free-from and functional food claims | +0.6% | Germany, Netherlands, Sweden, Belgium | Medium term (2-4 years) |

| Increasing penetration of online grocery shopping and e-commerce platforms | +1.1% | Europe-wide, accelerated in Italy, Spain, Poland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Trend of On-the-Go Consumption Demanding Convenience and Portability

Changes in European consumer mobility patterns are fundamentally reshaping how individuals structure their daily meal consumption, creating a robust and growing market for portable ready meal solutions. According to the Agriculture and Horticulture Development Board's comprehensive research, ready meals now represent 41% of red meat convenience products, demonstrating resilient market performance despite volume decreases in traditional food categories [1]Source: Agriculture and Horticulture Development Board, “Consumers Crave Convenience,” ahdb.org.uk. This transformation reflects a significant evolution in consumer behavior, where conventional fixed mealtimes are transitioning to flexible eating patterns that accommodate modern professional schedules and daily commuting requirements. The ongoing urbanization and increasing population density across major European cities further amplify this market dynamic, as residents adapt to smaller living spaces that limit cooking capabilities while managing extended commuting hours between residential and workplace locations. The concurrent demographic shifts of an aging population combined with high workforce participation rates have elevated convenience foods from an occasional choice to an essential component of daily life for many European consumers.

Innovations in Product Formats, Flavors, and Nutritional Profiles

Product innovation cycles are accelerating as manufacturers work to meet stringent regulatory requirements while adapting to sophisticated consumer preferences. The establishment of Nomad Foods' Future Foods Lab in June 2025 exemplifies how traditional food companies are building strategic partnerships with startups to harness innovative technologies and gain deeper consumer behavior insights. Recent developments in freeze-dried technology have enabled manufacturers to produce shelf-stable products that deliver fresh, authentic taste experiences, effectively addressing consumer concerns about processed food quality without compromising on convenience. Ready meal manufacturers are diversifying their product portfolios by integrating authentic regional flavors and diverse ethnic cuisines, helping them expand their market presence beyond conventional European taste preferences. Through the strategic incorporation of functional ingredients, manufacturers are transforming ready meals into nutritionally beneficial options, positioning them as wholesome dietary choices rather than mere convenience alternatives.

Expansion of Personalized Meal Options

The ready meals market is evolving as consumers increasingly seek personalized nutrition options that match their specific dietary needs and health goals. According to the EIT Food Nutrition Trend Report 2025, 69% of nutrition experts identified personalized nutrition as a key priority, reflecting the growing consumer demand for individualized food solutions [2]Source: EIT Food, “Nutrition Trend Report 2025,” eitfood.eu. Manufacturers are leveraging technology to enable mass customization, producing variants that address specific dietary requirements, allergen restrictions, and nutritional targets. The subscription box model has gained significant traction across European markets, particularly in Italy, where food e-commerce growth accelerated during COVID-19 and continued through 2024 [3]Source: Università Ca’ Foscari, “Food e-commerce and the subscription box model,” unive.it. Personalization now encompasses multiple aspects including portion sizes, meal timing, and nutritional density, allowing companies to implement premium pricing strategies for customized offerings.

Advances in Packaging Technology Enhancing Shelf Life and Sustainability

The European Union's regulatory framework is reshaping packaging requirements through strict recyclability standards, responding to increasing consumer demands for products with longer shelf life and minimal environmental footprint. The regulation establishes a tiered grading system for recyclability, fundamentally altering how companies approach material selection and design. These requirements for recycled content in plastic packaging are creating immediate supply chain pressures, though they also present strategic advantages for businesses that proactively invest in compliant materials and manufacturing processes. Companies are implementing active packaging technologies that preserve food quality and safety while extending product longevity, enabling broader market reach and addressing food waste reduction goals. The incorporation of smart packaging elements, such as digital tracking codes and monitoring sensors, enhances consumer interaction while providing comprehensive supply chain visibility and product traceability.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Imapact Timeline |

|---|---|---|---|

| Increased consumer demand for freshly prepared meals | -0.8% | France, Italy, Spain - traditional food cultures | Medium term (2-4 years) |

| Regulatory challenges related to food labeling, health claims, and safety standards | -0.6% | Europe-wide, particularly complex in multi-country operations | Long term (≥ 4 years) |

| Environmental concerns over plastic and non-biodegradable packaging | -0.4% | Northern Europe, environmentally conscious markets | Short term (≤ 2 years) |

| Challenges in maintaining consistent taste and quality across product lines | -0.3% | Europe-wide, quality-sensitive markets like Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased Consumer Demand for Freshly Prepared Meals

European consumers demonstrate a strong inclination toward fresh food options over ready meals, primarily driven by their emphasis on nutritional benefits and superior taste experiences. The growing trend of home cooking has become deeply ingrained in consumer behavior, with many households developing and maintaining regular meal preparation routines. Markets with rich culinary heritage, particularly France, Italy, and Spain, exhibit notable resistance to ready meal adoption, as their deeply rooted food traditions and communal dining practices create natural barriers to convenience food acceptance. The gradual stabilization of food prices has enabled consumers to redirect their spending toward fresh ingredients, moving away from processed alternatives. This shift in consumer preference particularly impacts the premium ready meal segment, as improved household purchasing power makes fresh food alternatives increasingly accessible and appealing.

Regulatory Challenges Related to Food Labeling, Health Claims, and Safety Standards

The complex regulatory environment across Europe member states presents significant operational challenges that particularly burden small food manufacturers, while giving larger companies with well-established regulatory departments a competitive edge. The European Parliament's 2024 implementation report on Regulation 1924/2006 revealed an important trend: while 18% of new food products feature nutrition and health claims, many of these products marketed under the 'healthy' umbrella contain concerning levels of fat, sugar, or salt [4]Source: European Parliament, “Implementation Report on Regulation 1924/2006,” europarl.europa.eu. The fragmented regulatory harmonization between member states forces manufacturers to navigate through a maze of different labeling requirements, health claim approvals, and safety standards when distributing products across multiple countries. Adding to these challenges, the proposed front-of-pack nutrition labeling system creates substantial uncertainty in product development cycles, requiring manufacturers to simultaneously maintain current compliance while preparing for upcoming regulatory changes. The implementation of Bisphenol A restrictions in food contact materials, set to take effect from December 2024, illustrates how evolving safety requirements continue to demand substantial investments in packaging compliance from food manufacturers [5]Source: European Commission, “Restriction of Bisphenol A,” eur-lex.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

The freeze-dried segment demonstrates significant market potential, growing at a 5.78% CAGR through 2031. This growth trajectory positions freeze-dried products as a notable challenger to the well-established Frozen Ready Meals segment, which currently commands a substantial 39.78% market share in 2025. The freeze-dried preservation method delivers extended shelf stability without the need for refrigeration, enabling companies to expand their distribution networks and reduce cold chain expenses while maintaining the nutritional content and taste quality of their products.

Frozen Ready Meals continue to maintain their market leadership position through strong consumer acceptance and an optimized retail infrastructure. Their competitive pricing structure makes these products accessible to consumers across various income levels. In contrast, Chilled Ready Meals occupy the premium market segment, offering products with shorter shelf life but perceived higher quality. This premium positioning attracts consumers who prioritize fresh-like characteristics and are willing to pay higher prices for such attributes.

By Ingredient: Conventional Strength Versus Free-Form Acceleration

The free-form ingredients market continues to demonstrate robust growth, advancing at a 6.05% CAGR through 2031. This expansion is primarily fueled by increasing consumer awareness and demand for products with clean labels and allergen-free formulations. In contrast, conventional ingredients maintain their strong market position with an 82.05% share in 2025, supported by their inherent cost advantages and well-established supply chain networks. The BMEL Food Report 2024 highlights a significant shift in consumer preferences, with more than half of consumers actively seeking processed foods containing reduced sugar and fat content.

This evolving consumer behavior has prompted manufacturers to undertake extensive reformulation efforts across both conventional and free-form categories. Free-form products successfully maintain premium pricing strategies, justified by their health-focused positioning and specialized manufacturing processes that eliminate common allergens and artificial additives. Meanwhile, conventional ingredients continue to dominate the market through their ability to leverage economies of scale, long-standing supplier relationships, and broad consumer familiarity that minimizes the need for extensive market education.

By Category: Plant-Based Momentum Challenges Meat Dominance

The vegetarian ready meals segment demonstrates strong growth potential, with projections indicating a CAGR of 6.45% through 2031. This growth trajectory aligns with the broader consumer shift toward plant-based food options. Meanwhile, non-vegetarian ready meals continue to hold a substantial market position, maintaining a 65.74% share in 2025. This dominance stems from deeply rooted consumer preferences and the segment's ability to meet protein requirements effectively.

Industry validation comes from the EIT Food Nutrition Trend Report 2025, where an overwhelming 82% of nutrition experts highlighted plant-based diets as the primary trend. This professional consensus is reflected in strategic market movements, exemplified by Migros-Molkerei Elsa's acquisition of Sofine Foods, a specialist in vegan schnitzels and ready meals. The vegetarian segment's appeal extends beyond dietary preferences, encompassing sustainability benefits, growing health consciousness among consumers, and particular resonance with younger demographics. These factors enable companies to implement premium pricing strategies while establishing distinct brand identities in the market.

By Distribution Channel: Digital Transformation Accelerates Retail Evolution

The online retail segment of the ready meals market continues to demonstrate robust growth, with projections indicating a CAGR of 9.28% through 2031. Traditional brick-and-mortar establishments, specifically supermarkets and hypermarkets, remain the primary distribution channel, commanding a substantial 53.10% market share in 2025. The expansion of e-commerce platforms reflects the broader digital transformation in consumer behavior, which was initially accelerated by pandemic-related restrictions but has since become a permanent shift in shopping preferences.

Consumer preference for the convenience and extensive product selection offered by online platforms has sustained growth beyond the pandemic period. The Italian food segment demonstrates this shift through the adoption of e-commerce and subscription-based services, enabling direct-to-consumer delivery of personalized meal options. Online channels have been particularly effective for freeze-dried and shelf-stable products, as these items bypass the complexities of cold chain logistics and reach a broader geographic audience.

Geography Analysis

The United Kingdom stands as the powerhouse in the European ready meals market, commanding a significant 19.72% market share in 2025. This market leadership reflects the nation's deeply ingrained convenience food culture and highly developed retail infrastructure. British consumers have embraced ready meals as part of their daily lives, supported by major retail chains that understand and cater to this demand through extensive shelf space allocation and robust cold chain management. The market's maturity has opened doors for manufacturers to introduce premium offerings and innovative products, as consumers show increasing willingness to experiment with new meal formats, international flavors, and health-focused options. While Brexit initially presented supply chain challenges, it ultimately strengthened the United Kingdom's domestic food production capabilities and reduced its reliance on European suppliers. The country's continued adherence to EU food safety standards maintains valuable export opportunities while allowing manufacturers to develop products that resonate with local tastes and dietary preferences.

Italy has emerged as the market's rising star, achieving an impressive 6.95% CAGR through 2031. This growth story marks a significant evolution in Italian consumer behavior, particularly noteworthy in a country known for its traditional approach to home cooking. Modern Italian consumers, especially in urban areas, are increasingly balancing their love for authentic cuisine with the demands of contemporary lifestyles. The market has naturally segmented into three distinct consumer groups: tradition-focused buyers who prioritize local sourcing and sustainability, price-conscious consumers seeking value in their meal choices, and environmentally aware shoppers who gravitate toward organic and ethically produced options. This transformation reflects a broader shift in Italian society, where convenience no longer carries the stigma it once did.

The broader European landscape, encompassing markets such as Germany, France, and Spain, presents a diverse tapestry of growth patterns shaped by unique local characteristics. France, in particular, demonstrates how traditional culinary heritage can coexist with modern convenience, as urban professionals seek high-quality ready meals that honor traditional cooking methods and ingredient quality. Each market requires a nuanced approach that respects local food cultures while addressing the evolving needs of busy consumers. Success in these markets depends on understanding regional preferences, navigating specific regulatory requirements, and developing products that bridge the gap between convenience and culinary tradition.

Competitive Landscape

The United Kingdom has established itself as the cornerstone of the European ready meals market, holding a commanding 20.04% market share in 2024. This leadership position stems from years of cultivating a convenience food culture that resonates deeply with British consumers. Major retail chains across the country have responded to this consumer behavior by creating dedicated spaces for ready meals and investing in sophisticated cold chain networks. The market's maturity has created an environment where manufacturers confidently introduce premium products and innovative meal solutions, knowing that consumers are receptive to new dining experiences, global flavors, and nutritionally balanced options. While the initial Brexit transition posed distribution challenges, it ultimately strengthened the United Kingdom's food production capabilities and reduced European supply dependencies. By maintaining alignment with Europe food safety standards, the country preserves crucial export opportunities while developing products that cater specifically to local preferences.

Italy represents the market's most dynamic growth story, recording a remarkable 7.23% CAGR through 2030. This growth trajectory signals a profound shift in Italian consumer attitudes, particularly significant in a nation traditionally devoted to home-cooked meals. Today's Italian consumers, especially in urban centers, are actively seeking convenient meal solutions that complement their modern lifestyles. The market has naturally evolved into three distinct consumer segments: traditional buyers who value local sourcing and sustainability, value-seeking consumers who prioritize affordability, and environmentally conscious shoppers who prefer organic and ethically produced meals. This transformation reflects a broader cultural shift where convenience aligns with, rather than opposes, Italy's rich culinary heritage.

The wider European market, including Germany, France, and Spain, showcases diverse growth patterns influenced by unique regional characteristics. France exemplifies how traditional food culture can successfully blend with modern convenience, as urban consumers embrace high-quality ready meals that respect classical cooking methods and ingredient integrity. Each regional market demands a carefully crafted approach that honors local food traditions while addressing contemporary lifestyle needs. Success in these markets requires deep understanding of regional preferences, careful navigation of regulatory frameworks, and development of products that seamlessly combine convenience with cultural authenticity.

Europe Ready Meals Industry Leaders

Nomad Foods Ltd.

Nestlé S.A.

Dr. Oetker GmbH

Unilever PLC

Orkla ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nomad Foods launched Birds Eye's new Europe-wide masterbrand campaign "That's a Recipe for a Life Well Fed" with multi-million-pound investment across various media platforms, aiming to reframe frozen food as nutritious and emotionally connected rather than just convenient, reflecting cultural resurgence in frozen food consumption where 67% of United Kingdom adults recognize frozen food as nutritious as fresh.

- June 2025: Nomad Foods unveiled Future Foods Lab to accelerate startup innovation through venture clienting, establishing a platform for integrating emerging technologies and consumer insights into established product portfolios while maintaining competitive advantages in frozen food categories.

- February 2025: Chequers Capital acquired 100% of Gourmet Italian food from Alcedo SGR, supporting growth and strategic positioning in the Italian ready meals market where the company's turnover rose from EUR 17 million in 2019 to EUR 140 million in 2024, establishing leading market position through strategic acquisitions including Firma Italia S.p.a. and 100Grammi.

Europe Ready Meals Market Report Scope

A ready meal is a meal sold in a pre-cooked form that only requires reheating.

The European ready meals market provides an in-depth analysis of the sales and growth of the ready meals segment in Europe, along with the opportunities and trends in the market. The market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into frozen ready meals, chilled ready meals, canned ready meals, and dried ready meals. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into the United Kingdom, Germany, France, Italy, Spain, Russia, and the Rest of Europe.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion).

By Type

| Frozen Ready Meals |

| Chilled Ready Meals |

| Shelf-Stable Ready Meals |

| Freeze-Dried Ready Meals |

By Ingredient

| Conventional |

| Free-Form |

By Category

| Vegetarian |

| Non-Vegetarian |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channel |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Type | Frozen Ready Meals |

| Chilled Ready Meals | |

| Shelf-Stable Ready Meals | |

| Freeze-Dried Ready Meals | |

| By Ingredient | Conventional |

| Free-Form | |

| By Category | Vegetarian |

| Non-Vegetarian | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe ready meals market in 2026?

The Europe ready meals market size reached USD 31.56 billion in 2026.

What is the expected growth rate for ready meals in Europe through 2031?

The market is projected to post a 5.6% CAGR from 2026 to 2031.

Which product type leads sales across Europe?

Frozen Ready Meals held 39.78% of the Europe ready meals market share in 2025.

Which distribution channel is growing the fastest?

Online Retail Stores are forecast to expand at a 9.28% CAGR through 2031.

Why is Italy considered the fastest-growing European market?

Italy combines urbanization, rising dual-income households, and strong e-commerce uptake, driving a 6.95% CAGR forecast.

Page last updated on: