Environmental Health And Safety (EHS) Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 9.64% CAGR |

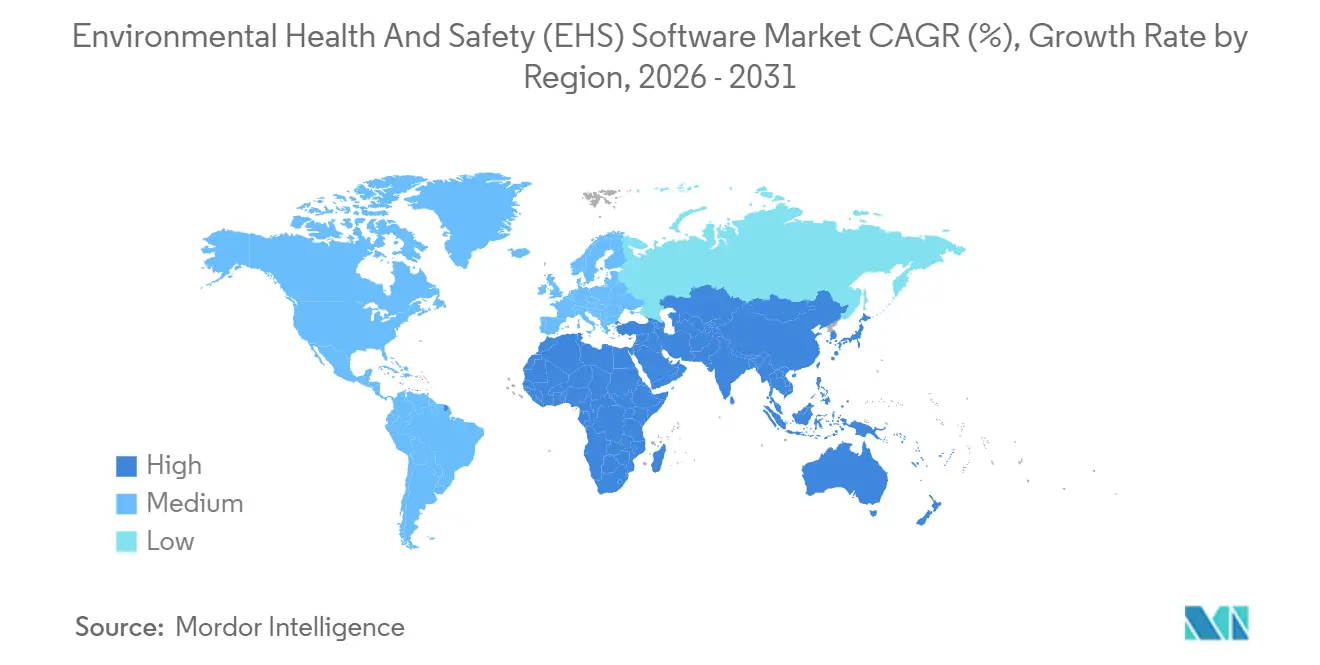

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

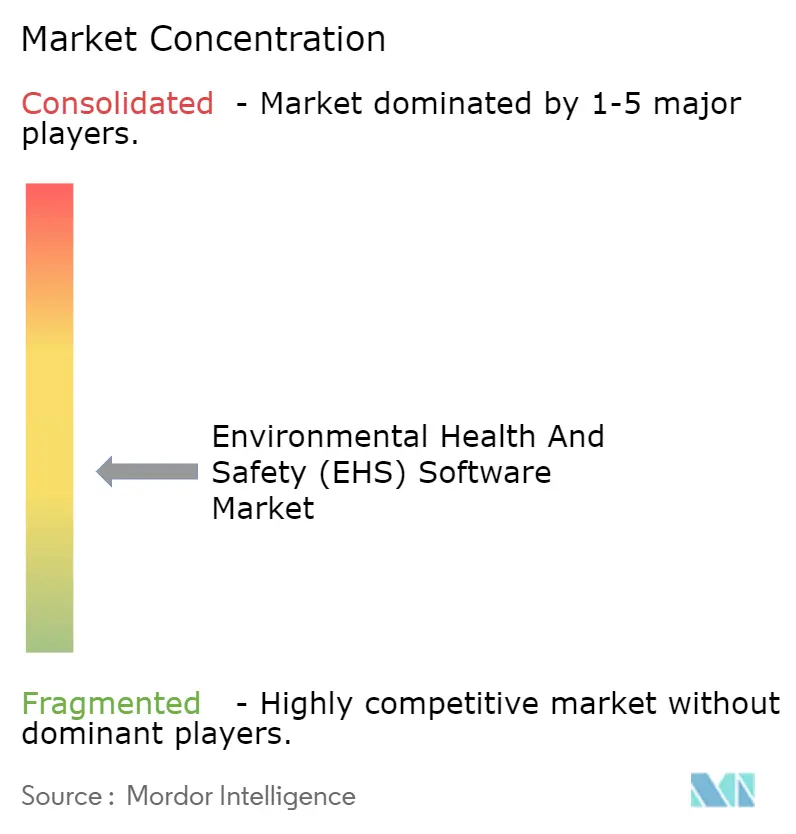

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Environmental Health And Safety (EHS) Software Market Analysis by Mordor Intelligence

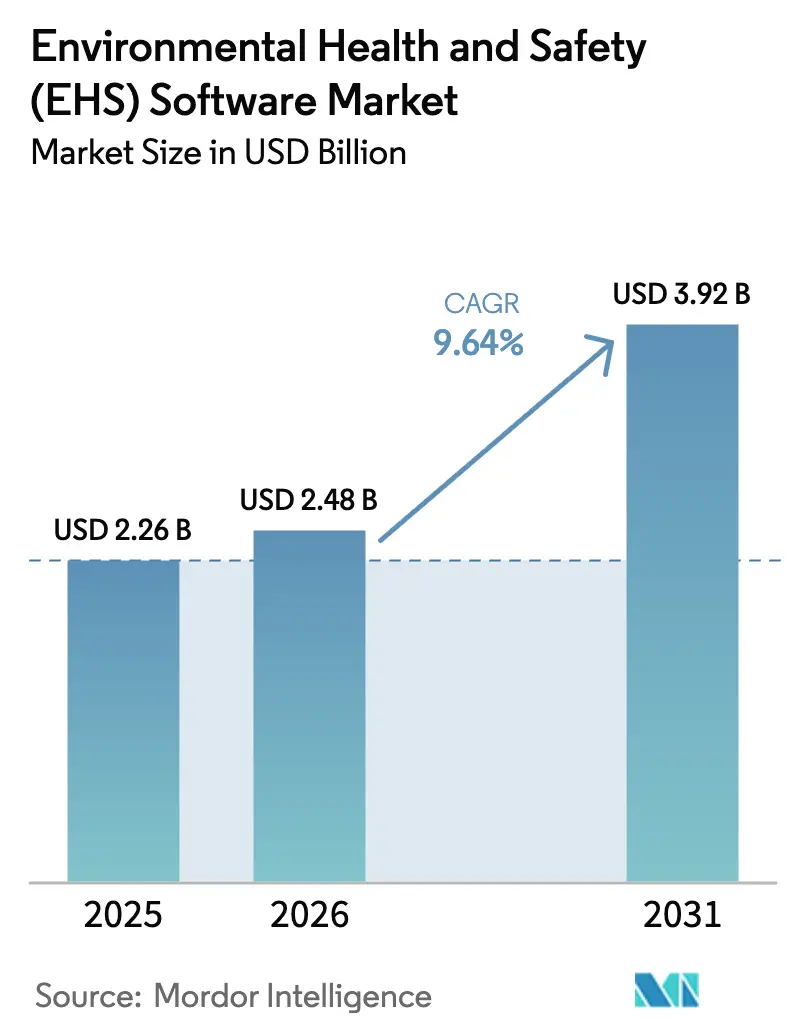

The Environmental Health And Safety Software Market size was valued at USD 2.26 billion in 2025 and is estimated to grow from USD 2.48 billion in 2026 to reach USD 3.92 billion by 2031, at a CAGR of 9.64% during the forecast period (2026-2031). Organizations now view EHS platforms as a strategic risk-intelligence layer that shapes insurance premiums, ESG ratings, and operational resilience instead of a compliance checkbox. Intensifying regulatory enforcement, especially in the United States and the European Union, is accelerating the shift from spreadsheets to real-time, cloud-native systems. Boards are also linking executive compensation to decarbonization goals, pushing ESG and carbon modules to the top of procurement lists. At the same time, software vendors are embedding artificial intelligence to predict incidents before they occur, strengthening business cases that hinge on lower injury rates and reduced insurance costs.

Key Report Takeaways

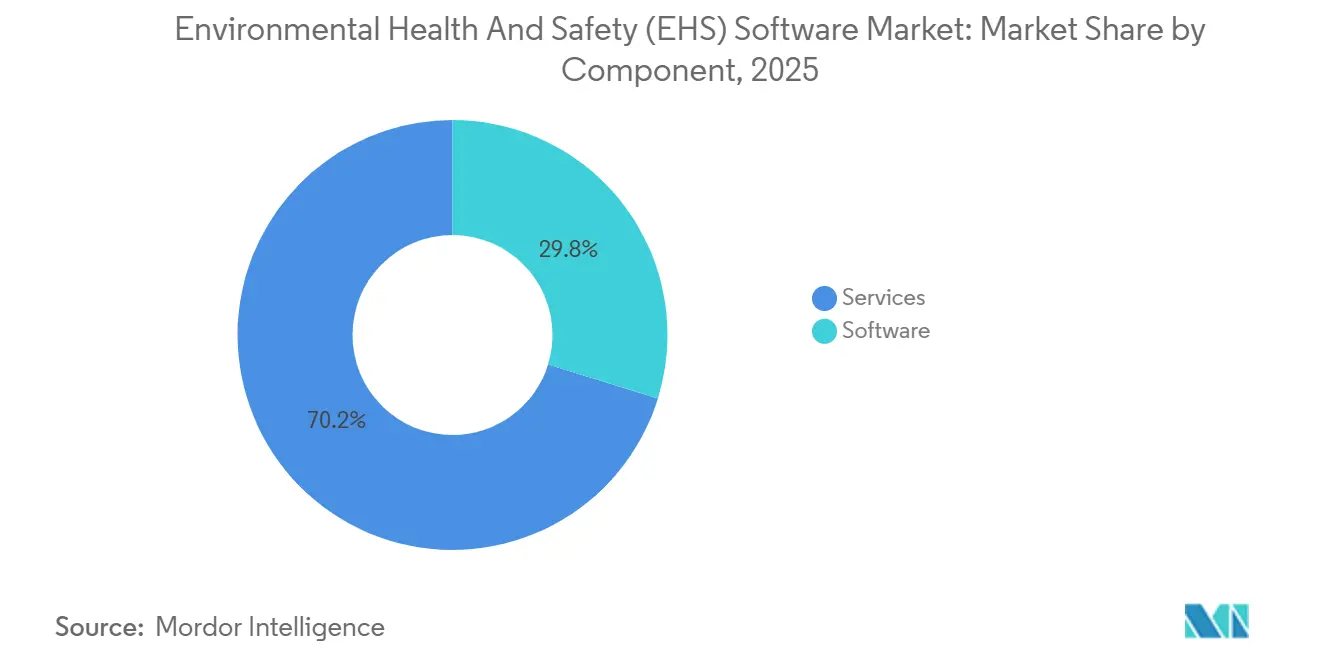

- By component, software captured 70.22% of 2025 revenue, while services are set to expand at an 11.42% CAGR through 2031.

- By deployment, cloud architectures represented 74.52% of 2025 spending and are advancing at a 12.84% CAGR over the outlook period.

- By solution type, incident and safety management led with a 35.64% slice of the EHS software market share in 2025, whereas ESG and carbon management tools are forecast to grow at an 11.68% CAGR to 2031.

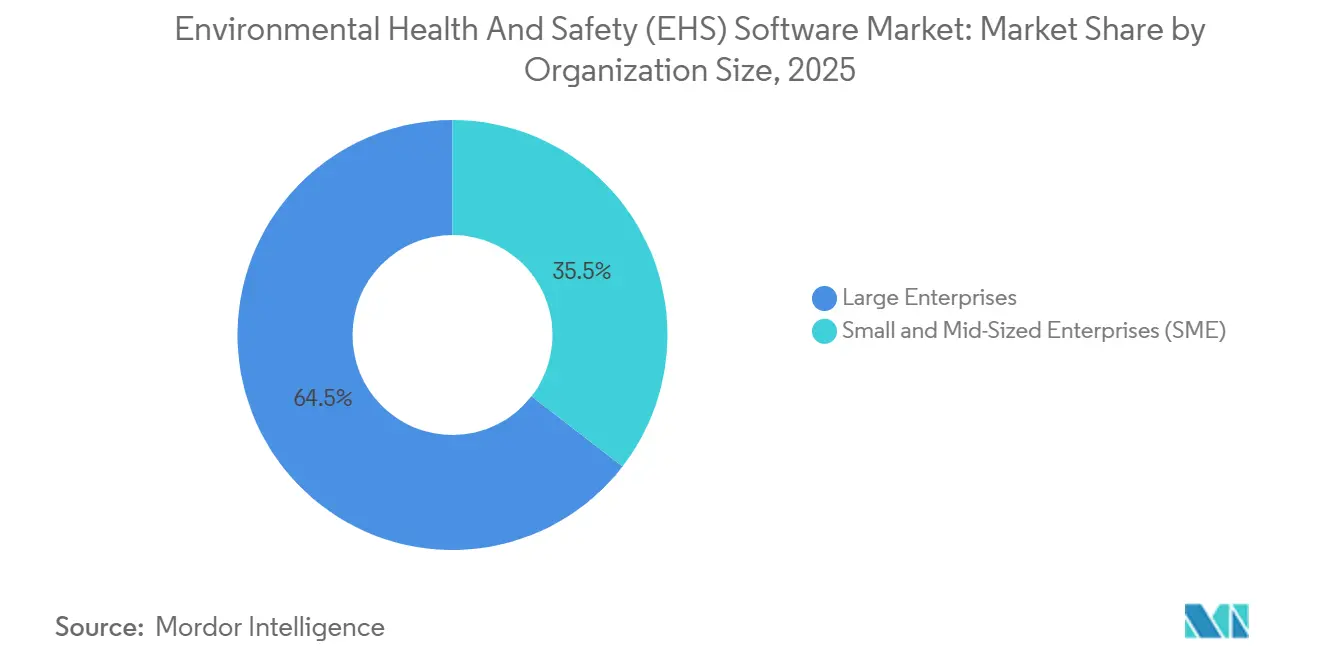

- By organization size, large enterprises accounted for 64.52% of 2025 outlays; small and mid-sized enterprises are adopting at a 12.12% CAGR to 2031.

- By end-user, energy and utilities held 22.84% revenue share in 2025; healthcare and life sciences are set to register a 10.24% CAGR through 2031.

- By geography, North America maintained 37.46% of 2025 revenue; Asia Pacific is projected to post a 10.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Environmental Health And Safety (EHS) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Enforcement and Rising Liability Exposure | +2.1% | Global, with peak intensity in North America and Europe | Short term (≤ 2 years) |

| Expansion of ESG and Sustainability Reporting Mandates | +1.8% | Global, led by Europe and North America, expanding to Asia Pacific | Medium term (2-4 years) |

| SaaS-first, Mobile-first EHS Platforms Reduce TCO | +1.5% | Global, with accelerated adoption in Asia Pacific and emerging markets | Medium term (2-4 years) |

| AI-driven Predictive Safety and Compliance Analytics | +1.3% | North America and Europe core, spillover to Asia Pacific manufacturing hubs | Long term (≥ 4 years) |

| Convergence with Digital Twin and Asset Management Stacks | +0.9% | North America and Europe industrial sectors, pilot deployments in Asia Pacific | Long term (≥ 4 years) |

| Corporate Insurance Linking Premiums to Real-time EHS Metrics | +0.7% | North America and Europe, early adoption in Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Enforcement and Rising Liability Exposure

United States OSHA lifted maximum penalties for willful violations to USD 165,514 and serious violations to USD 16,550 in 2025, moving annual adjustments to an indexed model that climbs each January. Public violation databases heighten reputational risk, prompting companies to automate audit trails and corrective-action records. In parallel, the European Union harmonized occupational safety directives with ISO 45001, nudging multinationals toward a single global platform that satisfies both Brussels and Washington. Chevron’s Operations Excellence Management System earned ISO 14001:2015 and ISO 45001:2018 recertification for the 2025-2028 cycle, illustrating how integrated software underpins dual environmental and safety compliance.[1]Chevron Corporation, “Operations Excellence Management System ISO Certification,” chevron.com Heightened personal-liability statutes in China and South Korea further reinforce the business case for predictive, auditable systems.

Expansion of ESG and Sustainability Reporting Mandates

The United States SEC’s March 2024 climate-disclosure rules require large accelerated filers to furnish assured Scope 1 and Scope 2 emissions, nudging firms toward platforms that merge environmental, safety, and carbon data streams. Europe’s Corporate Sustainability Reporting Directive extends detailed disclosures to 50,000 entities, including non-EU companies with sizable regional activity. Demand for ESG and carbon modules is climbing at an 11.68% CAGR because these tools automate data pulls from meters, asset systems, and supplier portals, then map them into disclosure templates. Sphera and Evonik’s TÜV-certified automated life-cycle assessment tool slashes product-footprint reporting cycles from weeks to hours, underscoring the operational upside.

SaaS-First, Mobile-First EHS Platforms Reduce TCO

Cloud deployments accounted for 74.52% of 2025 spending and deliver savings by eliminating on-premise servers, database licenses, and patch cycles. Mobile interfaces let frontline workers capture photos, voice notes, and geotagged observations, cutting the lag between hazard detection and remediation from days to minutes. CPChem’s SWIFT electronic permitting system processed 65,000 digital permits in 2024, shrinking approval windows from 48 hours to under 4 hours. Vendors bundle disaster-recovery and penetration-testing controls, easing CIO concerns while converting capital expense into predictable subscription fees.

AI-Driven Predictive Safety and Compliance Analytics

Cority’s Cortex AI engine mines near-miss logs, sensor telemetry, and maintenance data to flag emerging risks and recommend interventions before incidents materialize. Intelex released real-time data-quality validation that automatically highlights anomalous emissions figures and faulty sensor inputs, reducing the likelihood of erroneous regulatory filings. Early adopters report measurable declines in recordable injury rates and lower insurance premiums as underwriters begin referencing predictive-risk dashboards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Implementation and Change-management Cost | -1.4% | Global, with acute impact on SMEs in Asia Pacific and South America | Short term (≤ 2 years) |

| Cyber-security and Data-privacy Concerns in Cloud Roll-outs | -0.9% | Global, with heightened sensitivity in Europe (GDPR) and China (data localization) | Medium term (2-4 years) |

| Shortage of Data-science Talent for Next-gen EHS Tools | -0.7% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Vendor Consolidation Creating Integration Lock-in Risk | -0.5% | Global, affecting enterprises with multi-vendor IT stacks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Implementation and Change-Management Cost

A 5,000-employee deployment often exceeds USD 500,000 when licenses, consulting, data migration, and training are bundled, straining budgets for mid-tier manufacturers. Capital outlays compete with production upgrades, creating a deferral cycle that slows adoption even where long-run savings are clear. Change-management hurdles compound the burden: supervisors accustomed to clipboards resist new workflows, and harmonizing legacy taxonomies with modern data models absorbs scarce implementation hours. For many small and mid-sized enterprises, limited EHS staffing means project leadership falls to plant managers who juggle production targets alongside transformation tasks, extending timelines and diluting accountability.

Cyber-Security and Data-Privacy Concerns in Cloud Roll-Outs

Moving facility layouts, hazardous-material inventories, and incident records into multi-tenant clouds elevates exposure. Europe’s GDPR and China’s data-security laws restrict cross-border transfers, pushing vendors to launch regional data centers and maintain sovereign clouds that add cost and architectural complexity. Defense contractors and chemical producers worry that a breach could reveal sensitive process details, trigger shareholder lawsuits, and invite regulatory probes. Vendor consolidation heightens risk when newly merged platforms integrate disparate codebases, occasionally weakening controls during migration phases. Enterprises now demand SOC 2 Type II attestations and zero-trust architectures as contract prerequisites, extending procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Climb as Integration Needs Outpace Software Maturity

The services slice of the EHS software market posted an 11.42% CAGR outlook, outperforming software revenue growth despite software commanding 70.22% of 2025 turnover. Consulting engagements covering current-state mapping, API development, and multi-language user training routinely span 12 to 18 months for global roll-outs. Managed services appeal to mid-sized firms that prefer OpEx over CapEx, handing vendors the keys to upgrades, regulatory-rule updates, and help-desk support.

AI implementations are enlarging the services pipeline. Data-science teams tune machine-learning models, validate risk scores, and craft executive dashboards that convert raw predictions into board-ready insights. Parallel efforts to certify disclosures under new SEC and EU rules generate demand for assurance and data-lineage validation, again tilting budgets toward service providers. The modularization of incident, audit, ESG, and training tools multiplies integration points, ensuring that services remain the fastest-growing component through 2031.

By Deployment Mode: Cloud Dominance Rooted in Cost and Update Velocity

Cloud deployments held 74.52% share in 2025 and are tracking a 12.84% CAGR through 2031 in the environmental health and safety (EHS) software market. Continuous delivery lets vendors push regulatory templates within days of a new OSHA form or EU annex, a cadence on-premise customers cannot match without weekend maintenance windows and staff overtime. Subscription pricing spreads costs evenly, an advantage for enterprises under pressure to align cash flow with revenue.

On-premise installs persist in defense, nuclear, and certain Chinese operations where data-sovereignty laws require in-country hosting. However, five-year total cost modeling shows cloud deployments 30-40% cheaper once hardware refresh cycles, database patching, and disaster-recovery drills are counted. IoT sensor expansion reinforces the trend: streaming vibration, gas, and air-quality data directly into cloud dashboards is easier than installing edge servers at every site.

By Solution Type: ESG and Carbon Modules Outpace Legacy Incident Tools

Incident and safety management retained 35.64% revenue share in 2025, yet ESG and carbon management modules are rising at an 11.68% CAGR as boards link executive bonuses to decarbonization milestones. The environmental health and safety (EHS) software market size for ESG solutions is forecast to widen rapidly because new disclosure regimes demand auditable, time-stamped emissions ledgers instead of annual spreadsheet uploads. TÜV-certified life-cycle assessment add-ons compress customer-questionnaire response times, turning compliance into a procurement advantage for suppliers.

Audit and inspection modules still act as onboarding gateways for sectors such as construction that perform mandated walkthroughs each quarter. Training modules are increasingly embedded, auto-assigning refreshers after near-miss entries. Integration pressures mount as buyers favor best-of-breed stacks, encouraging API marketplaces and low-code connectors to tie disparate modules together.

By Organization Size: Mobile-First SaaS Narrows the Enterprise–SME Gap

Large enterprises accounted for 64.52% of 2025 spending, but SME adoption is growing at 12.12% CAGR as mobile-first SaaS removes the server and database hurdles that historically blocked smaller firms. Subscription tiers with pay-as-you-grow seat counts match seasonal labor swings in construction and agriculture. SMEs also value pre-configured templates that embed local regulations, allowing deployments in weeks rather than quarters.

The EHS software market share gap is narrowing as vendors roll out self-service onboarding and AI chat-assistants that replace costly classroom training. Yet predictive-analytics benefits still skew toward enterprises that hold a decade of digitized incidents to feed machine-learning models. Vendors respond by offering anonymized, cross-client benchmarks so newer customers can bootstrap risk-scoring engines without extensive historical data.

By End-User Industry: Healthcare Momentum Builds on EHR Integration

Energy and utilities retained 22.84% of 2025 revenue because unplanned outages and catastrophic events invite regulatory fines and investor backlash. Hospitals and life-science firms constitute the fastest-growing vertical at 10.24% CAGR, embedding EHS checks into electronic health records so infection-control teams can cross-reference staff exposures with patient outcomes. The environmental health and safety (EHS) software size for healthcare modules is set to accelerate as accreditation bodies demand proof of proactive worker-safety programs.

Oil and gas operators continue heavy investment to manage offshore drilling and LNG-terminal complexity, while chemicals firms use process-safety analytics to spot deviations before threshold breaches. Construction sites adopt mobile checklists that let supervisors geotag hazards and assign fixes without leaving the workface. Retail and logistics round out the long tail, drawn in by insurer incentives for real-time incident dashboards.

Geography Analysis

North America captured 37.46% of 2025 revenue, propelled by OSHA’s escalating penalties and the SEC’s climate-disclosure rule that effectively mandates continuous carbon accounting. High penetration among Fortune 500 firms intensifies competition for mid-market manufacturers and construction contractors still juggling clipboards and legacy databases. Vendor marketing increasingly highlights lower workers’ compensation premiums achieved by predictive-risk dashboards, resonating with CFOs seeking immediate savings.

Europe follows closely, anchored by the Corporate Sustainability Reporting Directive, which obliges granular, digitized disclosures across 27 member states. ISO 45001 certification rates are highest in Germany, France, and the United Kingdom, reinforcing the regional appetite for platforms that harmonize audit workflows with sustainability metrics. Cloud uptake is tempered by GDPR requirements, yet sovereign-cloud offerings mitigate data-transfer anxieties, unlocking growth among chemical and aerospace firms.

Asia Pacific is the fastest-growing theater at 10.48% CAGR in the environmental health and safety (EHS) software market. China’s revised Work Safety Law imposes criminal liability on executives after serious accidents, driving manufacturers to adopt real-time incident reporting and digital permit-to-work systems. India’s formal ISO 45001 guidance and new digital injury-reporting portal align local plants with multinational audit expectations. South Korea’s Serious Accidents Punishment Act, in force since 2022 but strictly enforced from 2024 onward, has catalyzed investments across shipbuilding and electronics supply chains.

The Middle East and Africa region gains momentum as national oil companies in Saudi Arabia and the United Arab Emirates embed EHS clauses into contractor agreements to satisfy Vision 2030 diversification goals. South Africa’s mining sector, historically plagued by high fatality rates, is shifting to cloud dashboards that surface geotechnical risks in near real-time. South America shows uneven progress: Brazil leads after high-profile dam and offshore incidents spurred Petrobras and Vale to fund enterprise-wide roll-outs, whereas smaller Andean markets remain in earlier adoption phases.

Competitive Landscape

The environmental health and safety (EHS) software market remains fragmented, with no vendor exceeding 15% share. Strategic buyers and private-equity investors are accelerating consolidation, convinced that EHS suites now form integral digital infrastructure rather than discretionary IT spend. Thoma Bravo explored a USD 2 billion divestiture of Cority in 2024, and EQT paid USD 3 billion for Avetta, underscoring double-digit valuation multiples tied to recurring revenue.[2]Reuters, “EQT Acquires Avetta for $3 Billion,” reuters.com

Competitive playbooks revolve around vertical depth, horizontal breadth, and technology differentiation. Cority released its Cortex AI engine in 2025 to strengthen predictive capabilities, while Intelex shipped AI data-quality validation the same year. Baker Hughes teamed with C3 AI to embed generative AI into the Cordant platform, enabling conversational analytics that lower the skills barrier for frontline users.[3]Baker Hughes Company, “Baker Hughes and C3 AI Announce Strategic Alliance for Cordant Platform,” bakerhughes.com

IoT hardware makers are emerging disruptors by bundling sensors and dashboards, bypassing traditional software RFPs. Vendors also court insurers that increasingly tie premium discounts to the presence of real-time safety analytics, creating cross-selling channels into risk-management divisions. However, rapid consolidation raises lock-in worries for customers with multi-vendor stacks, pushing demand for open APIs and data-export guarantees.

Environmental Health And Safety (EHS) Software Industry Leaders

Cority Software Inc.

VelocityEHS Holdings Inc.

Intelex Technologies ULC

Sphera Solutions Inc.

Enablon France SA (Wolters Kluwer NV)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cority launched Cortex AI, a predictive-safety engine that recommends interventions based on real-time sensor feeds and historical incidents.

- October 2025: Intelex unveiled AI-powered data-quality validation that flags anomalous emissions and safety observations before regulators do.

- September 2025: Sphera and Evonik debuted a TÜV-certified automated life-cycle assessment add-on that compresses product carbon-footprint calculations.

- May 2025: Baker Hughes and C3 AI formed a strategic alliance to embed conversational analytics in the Cordant platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Environmental Health and Safety (EHS) software market as purpose-built digital platforms that record, track, analyze, and report environmental metrics, occupational health incidents, and regulatory compliance obligations, monetized only through license, subscription, and support fees.

Scope exclusion: Hardware sensors, personal protective equipment, stand-alone consulting engagements, and custom one-off coded tools are outside the study's perimeter.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-premise

- By Solution Type

- Incident and Safety Management

- Audit and Inspection

- Compliance and Risk Management

- ESG / Carbon Management

- Training and Learning

- By Organization Size

- Large Enterprises

- Small and Mid-Sized Enterprises (SMEs)

- By End-user Industry

- Energy and Utilities

- Oil and Gas

- Chemicals and Petro-chemicals

- Healthcare and Life Sciences

- Construction and Manufacturing

- Mining and Metals

- Food and Beverages

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- South America

- Brazil

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed software product heads, corporate EHS directors in chemicals, utilities, mining, and healthcare, and IT resellers across North America, Europe, and Asia. An online survey of mid-sized manufacturers clarified cloud pricing spreads, module attach rates, and regional regulation triggers, letting us verify secondary findings and fill data gaps.

Desk Research

We drew first on public datasets such as OSHA injury logs, the U.S. EPA Toxics Release Inventory, Eurostat accident statistics, and UN Comtrade export codes that signal software flows, which helped size the potential user base and hazard intensity. Trade papers from bodies such as the International Labor Organization and the American Industrial Hygiene Association provided adoption benchmarks and rule changes. Annual reports, 10-K filings, and investor presentations of leading platform vendors revealed revenue splits, while Dow Jones Factiva news runs captured pricing shifts and contract wins. Questel patent clusters mapped new module launches, and D&B Hoovers offered triangulating company financials. The examples above are illustrative; many other sources supported data gathering and validation.

Market-Sizing & Forecasting

A top-down install-base reconstruction, industrial establishments multiplied by EHS software penetration multiplied by average annual spend yields the first cut, which is then balanced through sampled vendor roll-ups to confirm plausibility. Key inputs include OSHA recordable case-rate trends, ISO-14001/45001 certification counts, carbon-reporting rule rollouts, SME manufacturing growth, and cloud price erosion. A multivariate regression projects demand to 2030, with missing unit or price splits imputed from peer interviews and flagged for review.

Data Validation & Update Cycle

Every dataset passes a two-step peer review and automated variance checks that flag swings above five percentage points versus the prior cycle. We refresh figures annually, triggering interim updates when policy shocks, major acquisitions, or material technology shifts occur, so clients receive the latest vetted view.

Why Our EHS Software Baseline Commands Reliability

Published estimates rarely match because firms count different revenue streams and refresh at varying cadences. Some pool services, others stop at large-enterprise cloud deals, and currency conversions differ.

Mordor Intelligence filters revenue strictly to recurring software fees, calibrates SME uptake through primary survey ratios, and applies a blended mid-range price curve. A global consultancy narrows its tally to vendor self-reported 2023 license revenue, while an industry journal folds in multi-year implementation services, so gaps are inevitable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.24 bn (2025) | Mordor Intelligence | |

| USD 1.90 bn (2023) | Global Consultancy A | Early base year and relies on vendor-submitted license revenue only |

| USD 55.53 bn (2025) | Industry Journal B | Combines software with EHS services and training revenues |

| USD 7.90 bn (2024) | Market Watch Firm C | Includes hybrid compliance platforms beyond pure EHS scope and uses a fixed multi-year price matrix |

These comparisons show that a scope-disciplined, frequently refreshed approach, such as ours, delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the EHS software market in 2031?

It is expected to reach USD 3.92 billion, reflecting a 9.64% CAGR from 2026 to 2031.

Which deployment model is growing fastest?

Cloud deployments are expanding at a 12.84% CAGR because they eliminate on-premise hardware and enable rapid regulatory updates.

Why are ESG modules gaining traction?

New SEC and EU disclosure mandates require auditable emissions data, driving ESG and carbon tools to grow at an 11.68% CAGR.

How are AI capabilities influencing adoption?

Predictive-risk engines like Cority’s Cortex AI help lower incident rates and insurance premiums, strengthening ROI cases for buyers.

Which region is set to record the highest growth rate?

Asia Pacific is projected to grow at 10.48% CAGR thanks to stricter safety laws in China, India, and South Korea.

What factors limit adoption among SMEs?

High upfront implementation costs and limited change-management resources remain key hurdles despite falling software subscription prices.

Page last updated on: