Building Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

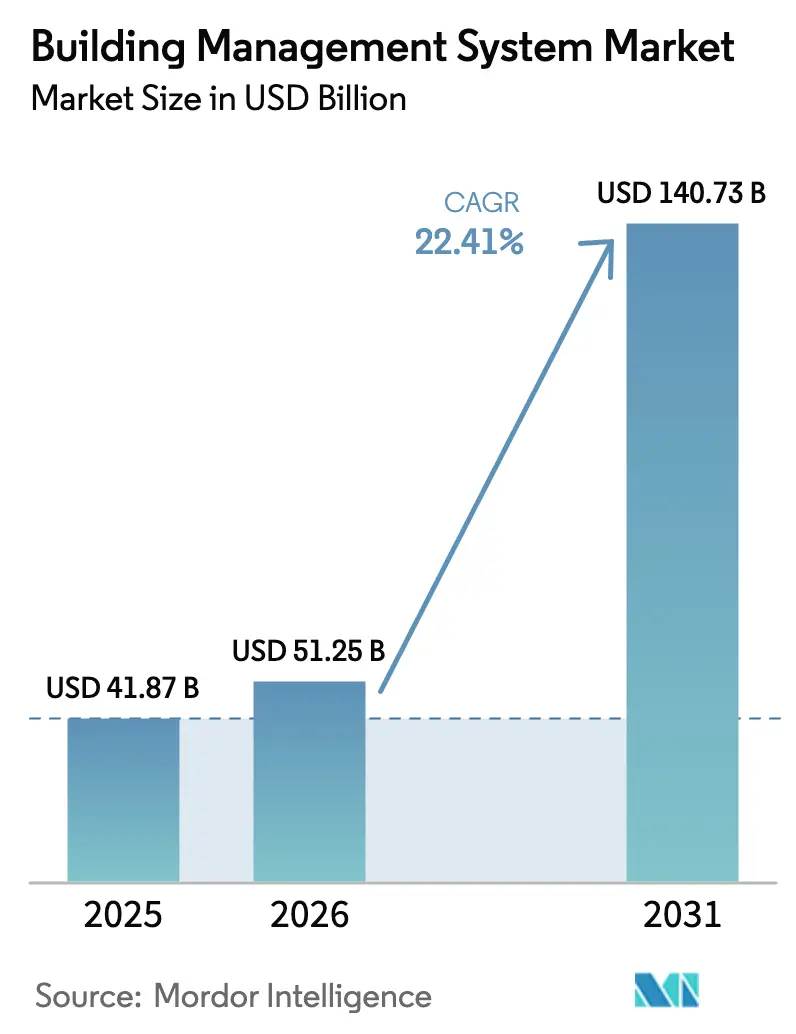

| Market Size (2026) | USD 51.25 Billion |

| Market Size (2031) | USD 140.73 Billion |

| Growth Rate (2026 - 2031) | 22.41% CAGR |

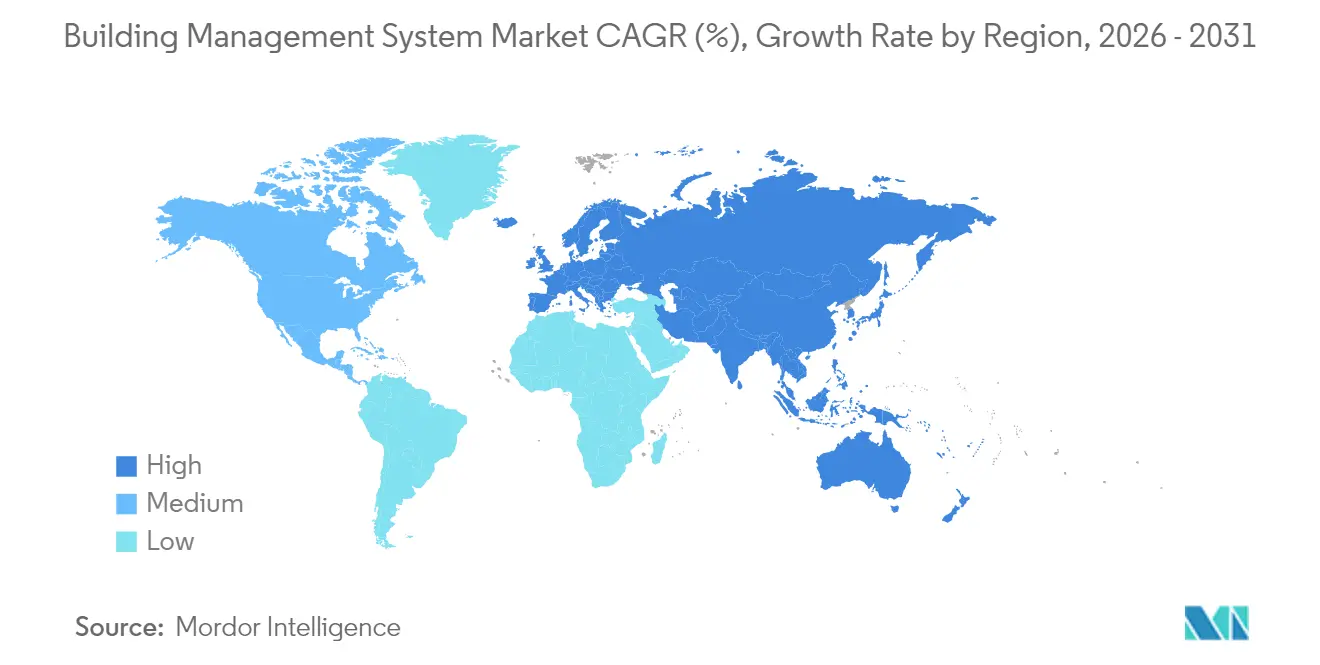

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Building Management System Market Analysis by Mordor Intelligence

The Building Management System Market size was valued at USD 41.87 billion in 2025 and estimated to grow from USD 51.25 billion in 2026 to reach USD 140.73 billion by 2031, at a CAGR of 22.41% during the forecast period (2026-2031).

Expanding smart-city budgets, stricter net-zero rules, and post-pandemic health priorities are accelerating digital modernization across new and existing facilities. Vendors that pair AI with cloud-native software gain an edge because predictive analytics lower energy bills and extend equipment life. Hardware remains essential, yet the fastest gains come from software modules that orchestrate sensors, controllers, and third-party devices through open protocols. Consolidation continues as established HVAC and automation suppliers acquire AI specialists to deliver unified platforms that meet regional compliance targets.

Key Report Takeaways

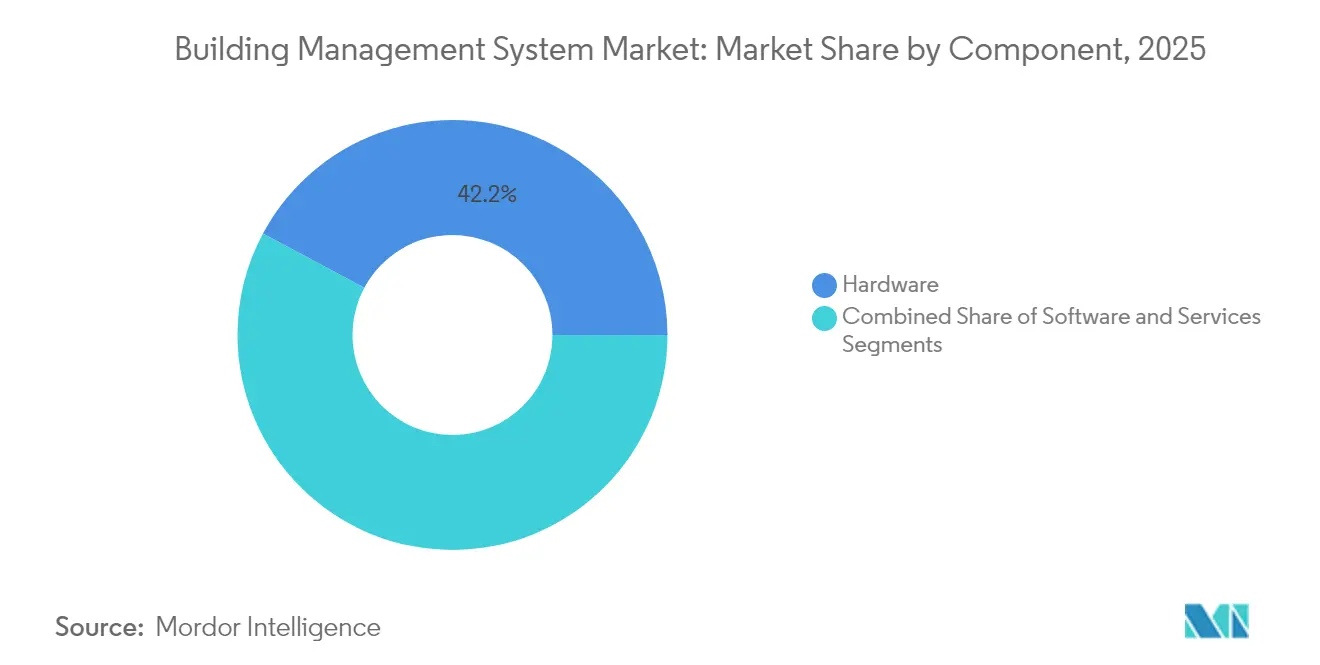

- By component, Hardware held 42.18% of the building management system market share in 2025, while software is forecast to grow at a 25.05% CAGR to 2031.

- By software module, Facility management commanded 32.10% share of the building management system market size in 2025; energy management is projected to expand at 27.15% CAGR through 2031.

- By deployment type, On-premise solutions captured 51.55% of the building management system market in 2025; cloud-based platforms show the highest projected CAGR at 25.80% to 2031.

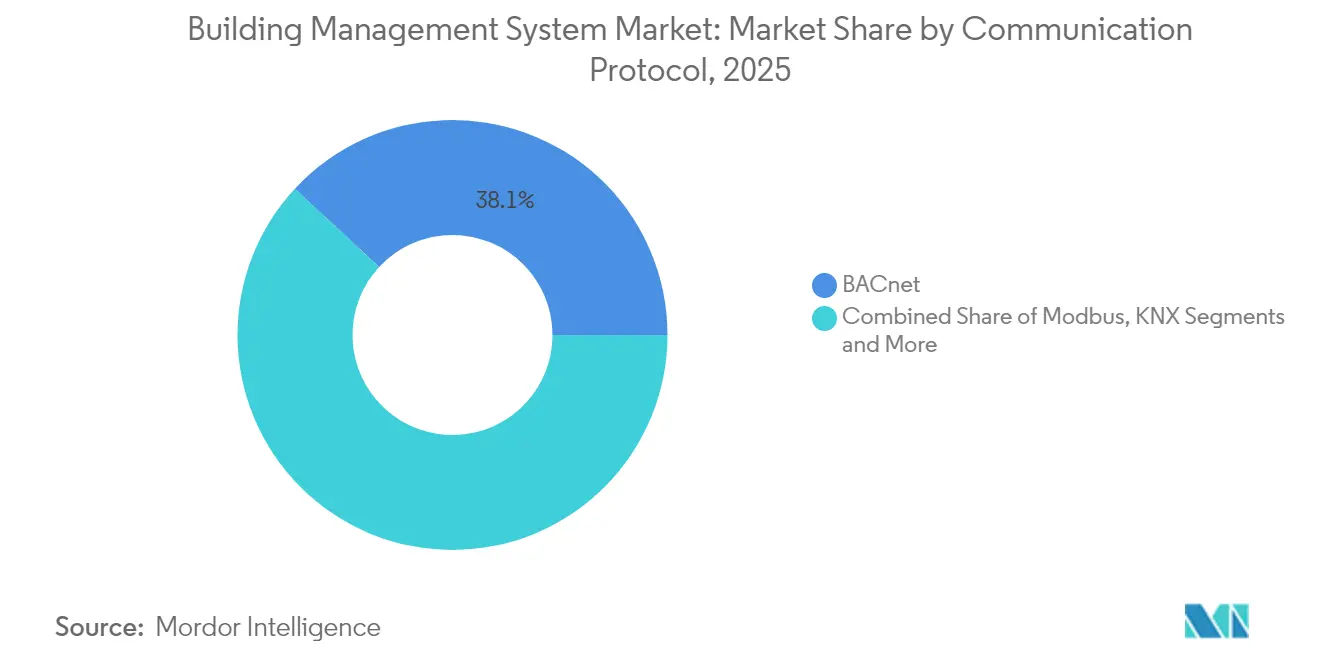

- By communication protocol, BACnet led with 38.10% share of the building management system market in 2025, whereas Modbus is advancing at 24.35% CAGR.

- By end-use industry, Commercial buildings contributed 61.70% revenue share in 2025; residential buildings are the fastest-growing segment at 24.20% CAGR.

- By geography, Europe accounted for 39.00% of the building management system market in 2025; Asia-Pacific is anticipated to post a 26.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Building Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid smart-city investments | +4.2% | Global, focus in Asia-Pacific and Europe | Medium term (2-4 years) |

| Sustainability and net-zero mandates | +3.8% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Post-pandemic healthy-building certifications | +2.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Declining IoT-sensor and wireless costs | +3.5% | Global | Medium term (2-4 years) |

| AI-driven predictive-maintenance ROI | +2.9% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Green-bond financing tied to performance | +1.7% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid smart-city investments

Municipal spending on smart-city ICT exceeded USD 63.4 billion between 2014 and 2023, and a sizable share funnels into building automation platforms that aggregate energy, occupancy, and safety data for urban dashboards. Venture funding in smart-building start-ups reached USD 6.9 billion in 2024, underscoring investor confidence that connected buildings form the digital backbone of smart-city ecosystems. Singapore’s Smart Nation initiative already connects more than 100,000 sensors in public and private buildings to enable real-time load balancing and comfort optimization. Barcelona’s adaptive street-lighting program uses building-linked controls to lower municipal energy costs by 30% while improving nighttime safety. These projects validate the return on integrated platforms and accelerate regional demand for interoperable building management solutions.

Sustainability and net-zero mandates

The European Union requires all new buildings to achieve zero operational emissions by 2030, a rule that pushes owners to adopt automation capable of measuring and correcting energy deviations in real time[1]European Commission, “Energy Performance of Buildings Directive,” ec.europa.eu. France’s RE2020 law sets embodied-carbon ceilings that fall every three years until 2031, encouraging continuous monitoring of construction and operational emissions. Only eight EU states fully met nearly-zero-energy-building targets by 2024, highlighting a shortfall that advanced automation can close. Climate-aligned bonds now require live performance data to verify decarbonization pathways, creating a financing advantage for facilities equipped with granular energy-management modules. These policies collectively elevate the building management system market because automated reporting and demand-response functions become prerequisites for capital access and occupancy permits.

Post-pandemic healthy-building certifications

Applications for WELL Health-Safety ratings surged after global lockdowns; Dubai’s Expo City alone certified more than 20 facilities in 2024. Hospitals illustrate the value: Ankara City Hospital integrates 22 subsystems and 800,000 data points to ensure optimal air changes and temperature control across 3.7 million sq ft. New platforms link IAQ sensors with ventilation drives so that CO₂ spikes trigger immediate airflow adjustments, sustaining indoor wellness without energy waste. Retail and education sites are copying the model because healthy-building seals now influence tenancy decisions and valuation. These certifications therefore reinforce demand for unified dashboards that track particulate levels, humidity, and pathogen risk alongside traditional HVAC metrics.

Declining IoT-sensor and wireless-network costs

Average multi-function sensor prices fell below USD 4 in 2024, opening retrofit opportunities for mid-tier offices and multifamily blocks previously priced out of automation upgrades. LoRaWAN and 6LoWPAN networks cut wiring needs, with Dubai office pilots reporting 25% energy savings after wireless deployments. A New York apartment building trimmed heating bills by USD 40,000 a year by installing battery-powered temperature sensors linked to AI-enabled HVAC controls. Advances in low-power edge chips shift computing to the device, reducing reliance on cloud bandwidth and lowering latency for critical alarms. Falling component costs thus widen the addressable base for the building management system market, particularly across aging stock that cannot justify full rewiring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX | -2.8% | Global, strongest among SMEs | Short term (≤ 2 years) |

| Cyber-security risks in OT networks | -1.9% | Global, critical in infrastructure | Medium term (2-4 years) |

| Fragmented legacy-protocol interoperability | -1.5% | North America, Europe | Medium term (2-4 years) |

| Vendor lock-in limiting open standards | -1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX

Turn-key building management projects range from USD 50,000 for small facilities to more than USD 1 million for multi-building campuses, putting pressure on cash-flow-focused owners. Upcoming EPA refrigerant rules are adding 10-30% to HVAC replacement costs, stretching budgets that could cover automation. Semiconductor shortages still inflate controller lead times, forcing owners to stock spares or absorb delays. Payback periods average 21 months, acceptable to corporates yet tight for smaller enterprises. Financing models such as energy-performance contracts and green bonds are easing adoption, but high CAPEX remains a near-term drag on the building management system market.

Cybersecurity risks in OT networks

More than 76% of firms experienced attacks on operational-technology assets during 2024, and half of commercial buildings host internet-exposed devices that invite ransomware. Legacy BACnet controllers often default credentials, letting intruders pivot from IT to HVAC and disrupt cooling in data-center spaces. Authorities now recommend Zero-Trust segmentation, yet many installations lack the staff to maintain continuous patching. High-profile breaches have delayed automation rollouts in healthcare and airports that cannot tolerate downtime. These security anxieties slow procurement cycles and raise insurance costs, tempering otherwise strong momentum for the building management system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software-led gains reshape modernization strategy

The building management system market recorded a 42.18% hardware share in 2025, reflecting widespread use of controllers, sensors, and gateways that handle real-time field tasks. Software revenue, though smaller, is climbing at a 25.05% CAGR because cloud dashboards and AI toolkits unlock predictive functions once the hardware baseline is in place. Services—including integration, remote monitoring, and cyber-security audits—form the fastest-rising revenue stream as owners outsource complex lifecycle tasks to specialists. Edge computing chips store local algorithms, safeguarding operations whenever the site loses connectivity. Competitive dynamics now revolve around software differentiation rather than proprietary devices, steering investment toward open-API platforms.

Building operators highlight condensed commissioning cycles when software auto-discovers devices and maps point data. Siemens retrofit packages, for example, slash project timelines by linking edge controllers to a no-code cloud studio that visualizes energy drift within hours of connection. Pricing pressure on commodity sensors means vendors must grow via analytics subscriptions, not mark-ups on physical parts. Over the forecast period, the building management system market will therefore see hardware margins contract while software sticks above 20%, validating a shift toward outcome-based service contracts.

By Software Module: Energy management outpaces facility oversight

Facility-management suites led with a 32.10% share of the building management system market size in 2025, bundling work-order tools, asset logs, and compliance reports. Energy-management modules, however, are expanding at 27.15% CAGR as corporate climate pledges require granular monitoring of kilowatt-hours and emissions. New releases combine machine-learning engines with weather APIs to shave peak demand charges without affecting occupant comfort. Infrastructure and emergency modules grow steadily in mission-critical sites that require centralized generator, fire, and evacuation oversight. Security dashboards converge access control and video analytics in a single pane, reducing operator workload.

Analytics-rich platforms now benchmark actual usage against Energy Use Intensity targets and issue alerts when deviations exceed 5%. The Carl T. Hayden VA Medical Center cut total utility bills by more than 25% after pairing chilled-water storage with predictive scheduling that flatten peak loads. Over the forecast period, owners seeking climate-bond financing will favor products that align with global reporting frameworks, locking energy-management functions into every major procurement.

By Deployment Type: Hybrid architecture balances sovereignty and scale

On-premise setups still hold 51.55% building management system market share because data-sensitive sectors prefer local control. Cloud platforms, though, post a 25.80% CAGR by 2031 thanks to multi-site chains that centralize analytics. Hybrid models blend both: edge devices execute latency-critical logic, while cloud engines run deeper optimizations. This dual-stack prevents service gaps during network outages and keeps sensitive data behind facility firewalls. Subscription pricing also converts CAPEX to OPEX, appealing to owners under budget caps.

Edge nodes run containerized apps that update over-the-air, shrinking truck rolls and carbon footprint. Retail groups with thousands of stores report 15% lower maintenance costs because technicians conduct remote triage first. By 2031, most large portfolios will adopt hybrid topologies, positioning the building management system market to shift from perpetual license sales to recurring revenue.

By Communication Protocol: Open standards erode proprietary niches

BACnet controlled 38.10% of communication traffic in 2025, supported by more than 800 certified manufacturers that guarantee multi-vendor interoperability. Modbus traffic is rising at 24.35% CAGR in industrial plants that value its simplicity. Wi-Fi and IPv6 frameworks enter retrofits where existing corporate LANs carry automation data after segmentation. Proprietary links continue in legacy campuses but shrink as new tenders demand open certificates. Interoperability lowers lock-in costs, letting owners competitively bid service contracts.

Emerging Thread and Matter standards promise encrypted mesh topologies suitable for dense device deployments. HPAC Engineering reports pilots where Thread nodes achieved sub-second fail-over, an advantage for life-safety alarms. Vendors that champion open ecosystems therefore gain share, and their success propels the building management system market toward de-facto interoperability norms by the decade’s end.

By End-Use Industry: Residential growth closes gap with commercial stronghold

Commercial facilities contributed 61.70% of 2025 revenue because office towers, retail chains, and mixed-use hubs seek lower operating expenses and tenant comfort. Residential demand, though smaller, is growing at 24.20% CAGR as smart-home hubs integrate HVAC and lighting into holistic dashboards. Healthcare campuses deploy redundant sensors and negative-pressure controls that comply with infection-control codes. Industrial plants now embed automation within production management to stabilize humidity and dust levels that affect yield. Universities and government offices embrace energy dashboards both to cut costs and to showcase sustainability leadership.

Home-energy-management kits can now shave 30-45% of annual consumption when linked to dynamic tariffs, prompting utilities to subsidize installations. Public-sector mandates such as California’s Title 24 further widen the addressable base. The spread of these programs ensures the building management system market steadily diversifies beyond its traditional commercial core.

Geography Analysis

Europe generated the largest regional revenue, holding 39.00% of the building management system market in 2025. EU zero-emission mandates and nearly-zero-energy-building rules turn automation from a discretionary upgrade into a planning prerequisite. France’s RE2020 carbon caps tighten every three years, compelling developers to adopt sub-metering and AI scheduling to remain within limits. Germany, the United Kingdom, and the Nordics deploy heat-pump-centric controls that combine weather forecasting with real-time energy pricing to maintain comfort at minimal cost. Established integrators supply turnkey retrofits that demonstrate double-digit IRRs, making automation a mainstream line item in refurbishment budgets.

Asia-Pacific is the fastest-growing region in the building management system market, forecast at a 26.10% CAGR. China pours municipal funds into IoT-ready districts that treat each building as a node in a larger grid-interactive system. India’s urban population surge doubles electricity demand, pushing states to adopt building codes that mandate smart controls for cooling efficiency. Singapore’s nation-wide sensor rollout proves the feasibility of granular oversight, inspiring similar programs in Kuala Lumpur and Bangkok. Japan and South Korea leverage semiconductor prowess to embed AI at the edge, shrinking latency for elevator dispatch and security analytics. Regional suppliers partner with global majors to localize software for language and compliance, further expanding the building management system market.

North America maintains sizeable volume through healthcare upgrades, campus modernizations, and residential electrification. U.S. federal tax incentives reimburse up to 30% of qualified efficiency investments, motivating owners to add advanced controls during HVAC swaps. Canada emphasizes cold-climate optimization, while Mexico accelerates adoption in its growing industrial corridors. Despite slower growth than APAC, rising healthy-building standards and decarbonization pledges sustain steady spending across the continent.

Competitive Landscape

The building management system market remains moderately fragmented, yet consolidation quickens as leading HVAC manufacturers acquire AI startups. Trane Technologies agreed to buy BrainBox AI, merging autonomous HVAC algorithms with Trane’s global service network. Bosch paid USD 8 billion for Johnson Controls’ residential and light-commercial HVAC unit, aiming to combine German sensor expertise with a vast installed base. Honeywell purchased Carrier’s Global Access Solutions portfolio for USD 4.95 billion, expanding from climate control into security and access management.

Competitive advantage hinges on three pillars: open-protocol support, AI-driven predictive maintenance, and hybrid cloud architecture. Vendors are offering all three-win multi-site deals because clients can mix legacy devices with new smart sensors and view everything on a single dashboard. Edge-to-cloud cybersecurity packages now accompany most proposals, reflecting customer concern over ransomware. Regional integrators hold niche share thanks to local codes and relationships, but must partner with platform providers to stay relevant. As a result, the top five suppliers account for roughly 45% of global revenue, a figure expected to rise as more tuck-in acquisitions close.

Building Management System Industry Leaders

Johnson Controls

Schneider Electric

Siemens AG

Hangzhou Hikvision Digital Technology Co., Ltd.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Carrier Global and Google Cloud launched an AI-based Home Energy Management System that balances HVAC demand with on-site battery storage.

- March 2025: Hussmann and Phoenix Energy Technologies introduced Refrigeration IQ, cutting supermarket leak rates by 30% in year one.

- February 2025: Daikin Applied bought Varitec Solutions to extend energy-efficient HVAC offerings across the U.S. Southwest.

- January 2025: Johnson Controls continued automation acquisitions during its CEO transition to deepen smart-building capabilities.

Global Building Management System Market Report Scope

The Building Management System (BMS) is a computer-based solution deployed in buildings to oversee and regulate various mechanical and electrical operations. These encompass HVAC (heating, ventilation, air conditioning), lighting, power distribution, fire safety measures, and security protocols.

The study tracks the revenue accrued through the sale of the building management system by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The building management system market is segmented by software (facility management, security management, energy management, infrastructure management, and emergency management), deployment type (on-premise, and cloud-based), end use industry (residential, commercial, industrial), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Hardware |

| Software |

| Services |

| Facility Management |

| Security Management |

| Energy Management |

| Infrastructure Management |

| Emergency Management |

| On-Premise |

| Cloud-Based |

| BACnet |

| Modbus |

| KNX |

| LonWorks |

| Zigbee |

| Wi-Fi / IP-Based |

| Proprietary Protocols |

| Residential Buildings |

| Commercial Buildings |

| Industrial Facilities |

| Public / Government Buildings |

| Healthcare Facilities |

| Education Campuses |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Software Module | Facility Management | ||

| Security Management | |||

| Energy Management | |||

| Infrastructure Management | |||

| Emergency Management | |||

| By Deployment Type | On-Premise | ||

| Cloud-Based | |||

| By Communication Protocol | BACnet | ||

| Modbus | |||

| KNX | |||

| LonWorks | |||

| Zigbee | |||

| Wi-Fi / IP-Based | |||

| Proprietary Protocols | |||

| By End-Use Industry | Residential Buildings | ||

| Commercial Buildings | |||

| Industrial Facilities | |||

| Public / Government Buildings | |||

| Healthcare Facilities | |||

| Education Campuses | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current size of the building management system market?

The market is valued at USD 51.25 billion in 2026 and is projected to reach USD 140.73 billion by 2031 at a 22.41% CAGR.

Which component segment is growing fastest?

Software is expanding at a 25.05% CAGR because cloud-native platforms deliver predictive analytics and remote commissioning.

Why is Asia-Pacific the fastest-growing region?

Rapid urbanization, smart-city investments, and government efficiency mandates are driving a 26.10% CAGR across major APAC economies.

How do net-zero regulations affect adoption?

EU and national carbon rules make real-time energy monitoring mandatory, so owners adopt advanced building management systems to meet compliance and financing criteria.

Page last updated on: