Indonesia CRM Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

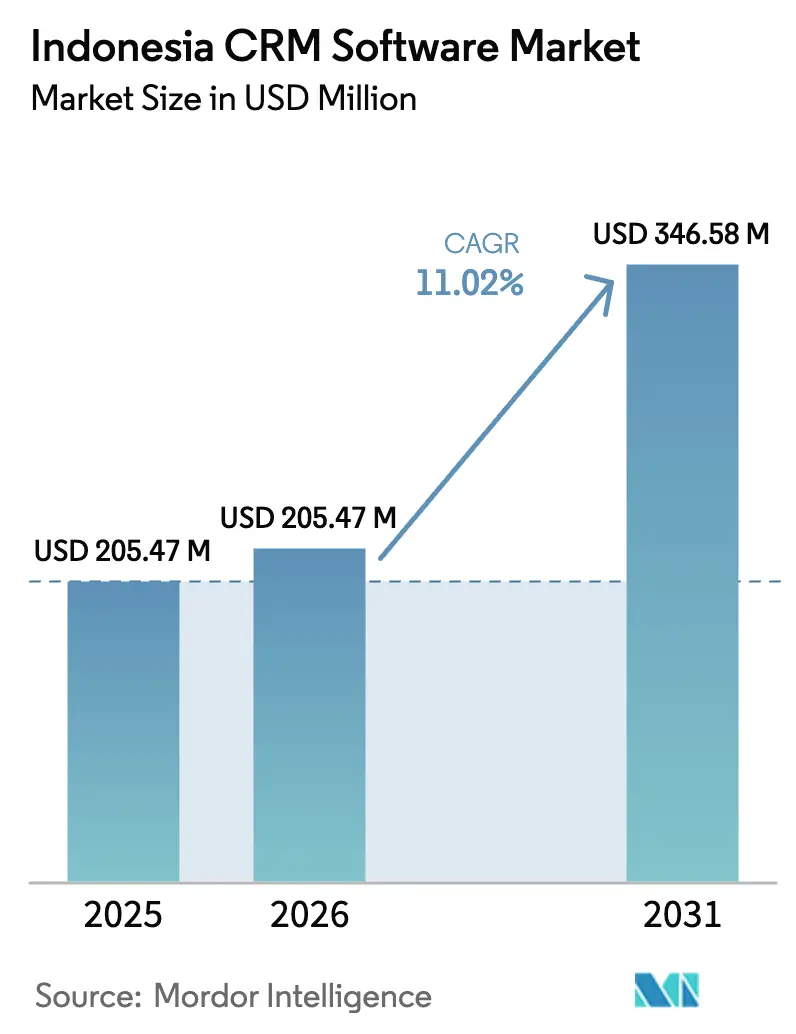

| Base Year Market Size (2025) | USD 205.47 Million |

| Market Size (2026) | USD 205.47 Million |

| Market Size (2031) | USD 346.58 Million |

| Growth Rate (2026 - 2031) | 11.02% CAGR |

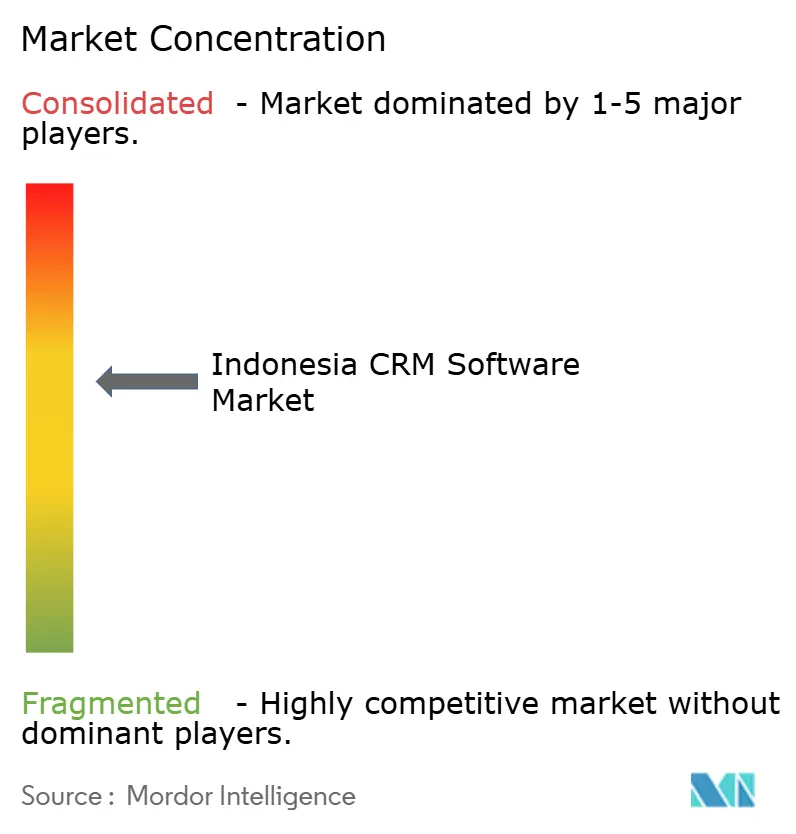

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia CRM Software Market Analysis by Mordor Intelligence

Indonesia CRM Software market size in 2026 is estimated at USD 205.47 million, growing from 2025 value of USD 185.0 million with 2031 projections showing USD 346.58 million, growing at 11.02% CAGR over 2026-2031. Rapid cloud adoption, expanding SME digitalisation, and supportive policy frameworks such as Making Indonesia 4.0 and the Digital Indonesia Roadmap 2021-2024 continue to shape demand. Mandatory e-invoicing, expanding mobile-first commerce, and the introduction of AI-based personalisation tools are widening the addressable user base and intensifying solutions differentiation. Competitive intensity is rising as global vendors deepen local partnerships while domestic providers focus on regulatory-aligned, vertically specialised offerings. Heightened cybersecurity awareness following recent data breaches and gaps in CRM-skilled talent outside Greater Jakarta present tangible challenges but also stimulate growth in consulting, upskilling, and security-focused sub-segments across the Indonesia CRM Software market.

Key Report Takeaways

- By deployment mode, cloud solutions captured 61.30% of Indonesia CRM Software market share in 2025; on-premise is projected to grow 11.55% CAGR to 2031.

- By organisation size, SMEs held 57.40% of Indonesia CRM Software market size in 2025, while large enterprises recorded the highest projected CAGR at 10.55% through 2031.

- By function, sales-force automation accounted for 41.40% share of the Indonesia CRM Software market size in 2025 and is advancing at a 9.18% CAGR through 2031.

- By industry, BFSI led with 22.70% of Indonesia CRM Software market share in 2025; healthcare is projected to expand at 12.87% CAGR to 2031.

- By CRM Type, operational CRM commanded 48.30% of Indonesia CRM Software market in 2025 as firms pursued quick wins in process automation. Retail implementations cut repeat-purchase cycle times and lifted retention by up to 40%, validating operational ROI. Analytical CRM is projected to expand 12.34% CAGR to 2031.

- By region, Java contributed 64.20% revenue share in 2025, whereas Papua & Maluku is forecast to grow at 13.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia CRM Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first digitalisation push by Indonesian SMEs | +3.5% | National (Java and Sumatra core) | Medium term (2-4 years) |

| Mandatory e-invoicing and PEPPOL roll-out | +2.8% | National | Short term (≤ 2 years) |

| AI-driven hyper-personalisation | +2.1% | Java, Sumatra, Bali and Nusa Tenggara | Medium term (2-4 years) |

| Mobile-first commerce and super-apps | +1.9% | National | Short term (≤ 2 years) |

| Government's Making Indonesia 4.0 incentives for manufacturing CRM | +3.5% | National | Medium–Long term (3–5 years) |

| Jakarta Smart-City and regional e-gov projects adopting citizen-CRM | +2.8% | Urban/regional public sectors (Jakarta and other major cities/provinces) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cloud-first digitalisation push by Indonesian SMEs

Cloud CRM adoption has risen from 25% in 2020 to 77% in 2025 among SMEs, which together contribute more than 60% of national GDP. Government schemes such as UMKM Go Digital offer grants and training that reduce entry barriers, enabling SMEs in secondary cities to leverage scalable CRM capabilities once confined to Greater Jakarta. This diffusion is widening the Indonesia CRM Software market, with hybrid cloud configurations addressing data-sovereignty norms while preserving cost efficiency. Improved accessibility also expands the ecosystem of implementation partners, creating fresh revenue streams and accelerating local innovation.

Mandatory e-invoicing & PEPPOL roll-out catalysing CRM integrations

Indonesia’s nationwide e-Tax Invoice regime, now aligned with PEPPOL standards, compels taxable entities to synchronise invoicing data with the Directorate General of Taxes. [1]Directorate General of Taxes, “Electronic Invoicing Landscape in ASEAN,” asean.orgRetailers and e-commerce platforms embed invoicing workflows inside CRM modules, eliminating duplicate records and producing 20–35% operational efficiency gains. These integrations streamline compliance while heightening data accuracy for cross-sell analytics. Vendors offering pre-built connectors see shortened sales cycles, thus expanding the Indonesia CRM Software market further.

AI-driven hyper-personalisation raising ROI of CRM deployments

Large e-commerce firms such as Tokopedia achieved a 20% stock-error reduction by combining Vertex AI with CRM analytics.[2]Google Cloud, “Real-world Gen AI Use Cases,” cloud.google.comBukalapak reported incremental monthly transaction value of IDR 50 billion (USD 3.2 million) after deploying predictive recommendations. Banking leaders employ natural language processing for sentiment analysis, raising cross-sell conversion and reducing churn. These use cases validate AI investment and accelerate feature adoption across mid-tier enterprises, deepening the Indonesia CRM Software market penetration.

Surge in mobile-first commerce & super-apps demanding embedded CRM

E-commerce transactions reached IDR 533 trillion (USD 34.41 billion) in 2023, up 10.7% year-on-year. [3]U.S. Department of Commerce, “Indonesia Digital Economy,” trade.gov Super-apps such as Jakarta’s JAKI integrate citizen relationship management, standardising rapid response and data collection. Businesses now seek embedded CRM APIs that operate within payments, chat, and fulfilment flows, shortening buying journeys. Demand for mobile SDKs is rising, driving platform vendors to open marketplaces for plug-in CRM modules and expanding the Indonesia CRM Software market scalability.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and local-hosting rules | -1.80% | National (more acute for multinationals) | Medium term (2-4 years) |

| Shortage of CRM-skilled talent outside Greater Jakarta | -1.30% | Sumatra, Kalimantan, Sulawesi, Papua and Maluku | Long term (≥ 4 years) |

| Legacy core-banking and ERP stacks hindering seamless CRM integrations | –3.0% | National, with acute impact in established financial services and traditional enterprises | Short–Medium term (1–3 years) |

| Cyber-security incidents eroding end-user trust | –2.5% | National, with higher sensitivity in regulated industries (finance, government) | Short–Medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty & local-hosting rules inflating compliance cost

The 2023 Personal Data Protection Law enlarges data-processing obligations, forcing providers to maintain local infrastructure or contract Indonesian hyperscalers. A tier-one bank incurred 15–20% higher project costs when hosting Microsoft Dynamics 365 on AWS instead of Azure to meet residency requirements. Compliance pressures favour domestic vendors and delay multinational roll-outs, tempering Indonesia CRM Software market growth momentum.

Shortage of CRM-skilled talent outside Greater Jakarta

Only 23% of CRM practitioners operate beyond Java, resulting in 3-4-month average project delays in eastern provinces.[4]Economist Impact, "Bridging the Skills Gap: Fuelling Careers and the Economy in Indonesia.", impact.economist.comLimited broadband and high training costs compel firms to fly experts from Jakarta, inflating implementation budgets by up to 30%. Remote-first deployment models and vendor-led certification programs aim to narrow the gap, yet the talent deficit remains a drag on the Indonesia CRM Software industry expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud widens lead amid regulatory adaptations

Cloud solutions accounted for 61.30% of Indonesia CRM Software market share in 2025, reflecting enterprises’ preference for scalable subscriptions and faster deployment cycles. The segment is set to outpace the overall market at 11.60% CAGR, supported by sovereign-cloud partnerships that ease residency concerns. Localised data centres launched by hyperscalers shorten latency and ensure PDP Law compliance, positioning cloud as the default choice for new roll-outs. On-premise deployments persist in defence, banking, and manufacturing sites integrating with legacy systems; yet gradual hybrid adoption indicates a controlled transition rather than outright displacement. Vendors now bundle compliance services, further accelerating cloud’s grip on the Indonesia CRM Software market.

On-premise projects increasingly use containerised architectures to mimic cloud elasticity while keeping sensitive data in-house. Manufacturing firms participating in Making Indonesia 4.0 link plant-floor sensors to locally hosted CRM analytics for real-time customer-order status. Sovereign cloud frameworks from providers such as VMware enable phased migration strategies, signalling that hybrid models will underpin compliance-conscious transformations.

By Organisation Size: SMEs drive volume while large enterprises deepen sophistication

SMEs represented 57.40% of Indonesia CRM Software market size in 2025 and are forecast to grow 10.20% CAGR as cloud subscription tiers match micro-segment budgets. Government incentives, marketplace plug-ins, and simplified onboarding workflows lower barriers. SMEs in secondary cities employ CRM chatbots to engage customers without dedicated call centres, broadening reach and smoothing regional adoption curves. Large enterprises contribute disproportionate revenue as they deploy multi-layer CRM stacks across omnichannel operations. Top banks integrate CRM with core systems via open banking APIs to consolidate customer profiles and launch real-time offers. Such complex implementations grow service revenue for integrators, diversifying value capture within the Indonesia CRM Software market.

Large organisations also pioneer AI layers that subsequently trickle down to mid-market users through templated modules, reinforcing an innovation loop. Rising cyber-risk management budgets among corporates intensify the search for unified security controls across CRM, setting new baseline requirements that suppliers must satisfy.

By CRM Type: Operational leads, analytical accelerates

Operational CRM commanded 48.30% of Indonesia CRM Software market in 2025 as firms pursued quick wins in process automation. Retail implementations cut repeat-purchase cycle times and lifted retention by up to 40%, validating operational ROI. Analytical CRM is projected to expand 12.34% CAGR to 2031, outpacing all other categories as AI democratises predictive modelling. Tokopedia’s 5% rise in unique SKUs following data-quality upgrades showcases measurable uplift, prompting wider adoption in mid-tier firms. Collaborative CRM adoption is rising in healthcare networks where multi-stakeholder coordination is essential. Convergence between operational, analytical, and collaborative modules is creating integrated platforms that reinforce vendor lock-in and elevate barriers to entry in the Indonesia CRM Software market.

By Function: Sales automation dominates while social CRM surges

Sales-force automation held 41.40% share of Indonesia CRM Software market size in 2025, delivering standardised pipelines and mobile field-sales capabilities. Predictive lead-scoring, route optimisation, and auto-proposal generation illustrate the function’s deepening sophistication. Social CRM is set to grow 13.62% CAGR as Indonesia remains one of the world’s most active social media markets. Marketplace operators combine listening tools with transaction data to track sentiment and product feedback in near real-time. Marketing automation and customer service modules continue to mature, converging into unified journey-orchestration engines. The integrated stack mitigates channel silos and elevates lifetime-value strategies, reinforcing the Indonesia CRM Software market’s competitive differentiation.

By Industry: BFSI leads, healthcare accelerates

BFSI accounted for 22.70% Indonesia CRM Software market share in 2025 by leveraging CRM to unify digital and branch interactions and ensure regulatory reporting compliance. Fintech investment of USD 246 million in the first nine months of 2024 underscores sector momentum. AI-enabled CRM supports credit scoring inclusion, allowing banks to serve previously unbanked demographics. Healthcare is projected to record 12.87% CAGR as EMR mandates create natural touchpoints with CRM systems to enhance patient engagement. Retail, telecom, and manufacturing verticals each show distinctive adoption catalysts, such as omnichannel loyalty platforms and Industry 4.0 supply-chain visibility, further enlarging the Indonesia CRM Software market.

Geography Analysis

Java’s 64.20% contribution to Indonesia CRM Software market revenue in 2025 mirrors its dominance in enterprise density and broadband infrastructure. Jakarta’s Smart City initiatives demonstrate advanced citizen relationship strategies, while Bandung and Surabaya anchor regional development corridors. Although market penetration is highest here, growth is maturing at 10.78% CAGR as addressable demand approaches saturation.

Sumatra and Kalimantan display 11.95% and 12.56% projected CAGRs respectively. Energy, agriculture, and manufacturing firms in these islands integrate CRM with ERP to manage commodity supply chains and government-mandated reporting. Expanded fibre access and edge data centres are narrowing latency gaps, facilitating cloud adoption and enriching the Indonesia CRM Software market.

Papua & Maluku lead in growth velocity at 13.98% CAGR off a small incumbent base, reflecting targeted government connectivity programs such as Palapa Ring East. Sulawesi’s urban hubs adopt CRM to support service-sector expansion, while Bali & Nusa Tenggara’s tourism operators exploit CRM for personalised visitor experiences. Nevertheless, limited local talent and patchy connectivity constrain project timelines, underscoring the importance of remote deployment models to unlock expansion across the archipelago.

Competitive Landscape

The Indonesia CRM Software market exhibits moderate concentration. Global providers including Salesforce, Microsoft, SAP, and Oracle leverage broad ecosystems and AI roadmaps, yet face compliance hurdles that extend implementation cycles. Domestic players such as Barantum and Mekari Qontak exploit their Jakarta-based data centres and regulatory know-how to attract SME and mid-market buyers seeking lower total cost of ownership and faster localisation. Sovereign-cloud alliances with hyperscalers diversify channel strategies and reduce time-to-compliance for multinationals.

Strategic moves highlight the market’s AI pivot. Salesforce introduced Agentforce autonomous agents in 2024 to automate service workflows at USD 2 per conversation. NTT DATA is investing USD 15 million to expand local CRM delivery capacity, signalling an upstream shift into vertical micro-solutions. VMware’s sovereign-cloud service with Lintasarta offers multinational banks a compliant landing zone, reflecting growing demand for residency-aligned architectures.

Emerging white-space is visible in verticalised CRM modules for manufacturing traceability and healthcare’s patient-lifecycle management. Talent scarcity outside Jakarta has prompted vendors to create remote implementation toolkits and certification tracks, fostering a partner-led ecosystem. Price competition remains contained due to localisation barriers, yet bundled AI features and compliance dashboards are accelerating feature commoditisation across the Indonesia CRM Software market.

Indonesia CRM Software Industry Leaders

-

Salesforce, Inc.

-

Barantum

-

Pipedrive

-

Oracle Corporation

-

Zoho Corporation Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: NTT DATA Business Solutions announced a USD 15 million expansion to enhance Indonesian CRM and ERP delivery capacity

- February 2025: Salesforce launched AI capabilities tailored to Indonesian financial institutions, embedding compliance checks for local regulations

- January 2025: Odoo opened an Indonesia office and planned 40+ events to target manufacturing and retail CRM implementations

- October 2024: Salesforce released Agentforce, enabling enterprises to deploy autonomous AI agents for customer-facing processes

- July 2024: PanGrow introduced SME-focused CRM & ERP suites designed for Indonesian taxation and invoicing norms.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Indonesian customer-relationship-management (CRM) software market as all commercially licensed or subscription-based application suites that help enterprises capture, store, and act on customer data across sales, marketing, and service touchpoints, whether delivered via public cloud, private cloud, or on-premise servers.

Scope Exclusion: Custom-built in-house CRM platforms, standalone contact-center or marketing-automation tools, and broader enterprise suites where CRM is only a minor module are not counted.

Segmentation Overview

-

By Deployment Mode

- On-premise

- Cloud

-

By Organisation Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

-

By CRM Type

- Operational CRM

- Analytical CRM

- Collaborative / Strategic CRM

-

By Function

- Sales-force Automation

- Marketing Automation

- Customer Service and Support

- Social CRM

-

By Industry

- BFSI

- IT and Telecom

- Manufacturing

- Healthcare

- Retail and E-commerce

- Energy and Utilities

- Travel and Hospitality

- Others (Government, Education)

-

By Region

- Java

- Sumatra

- Kalimantan

- Sulawesi

- Bali and Nusa Tenggara

- Papua and Maluku

Detailed Research Methodology and Data Validation

Primary Research

Interviews with Indonesian CIOs, CRM resellers, cloud-infrastructure providers, and industry consultants across Jakarta, Surabaya, and Makassar supplied average seat counts, churn triggers, and typical discounting. Follow-up surveys with SMEs in retail, BFSI, and manufacturing helped our team verify penetration assumptions and the pace at which legacy spreadsheets are replaced.

Desk Research

Mordor analysts began with macro signals from sources such as Bank Indonesia's ICT spending tables, Ministry of Communication and Information Technology cloud-migration surveys, and Statistics Indonesia's enterprise census, which are then cross-checked with ASEANstats, World Bank digital-economy trackers, and trade data from UN Comtrade. Company filings and investor decks of leading SaaS vendors, along with press coverage archived on Dow Jones Factiva and financial snapshots from D&B Hoovers, provide revenue splits and pricing curves. Patent abstracts via Questel and tender notifications on Tenders Info help us gauge upcoming public-sector demand. This illustrated list is not exhaustive; many other open datasets and specialist portals supported secondary validation.

Market-Sizing & Forecasting

Top-down modeling starts with Indonesia's total enterprise-software outlay, reconstructing the CRM slice by applying vertical-level adoption ratios, license pricing bands, and cloud-migration multipliers. Outputs are subsequently tested against a bottom-up roll-up of sampled vendor revenues and channel checks, with gaps bridged through weighted averages. Key variables include: 1) annual SME formation, 2) public-cloud spend per enterprise, 3) smartphone penetration (proxy for mobile CRM usage), 4) digital-payment transaction volume, and 5) data-center capacity additions. Forecasts employ a multivariate regression that ties these drivers to historical CRM revenue, before scenario analysis adjusts for data-localization regulations or fiscal shocks.

Data Validation & Update Cycle

Model outputs pass a three-stage review: variance scans versus independent ICT indices, peer inspection by senior analysts, and reconciliation callbacks with earlier interviewees. Our reports refresh each year, while material events such as tax policy shifts or major vendor pricing changes trigger interim updates. A final analyst pass just before publication ensures clients receive the latest view.

Why Mordor's Indonesia CRM Software Baseline Stands Up to Scrutiny

Published estimates often diverge because firms choose different product baskets, rely on unverified vendor declarations, or extrapolate regional SaaS figures straight into Indonesia without adjusting for data-sovereignty rules.

Key gap drivers include broader "customer-experience" scopes that fold in contact-center suites, the use of global average selling prices instead of local tiers denominated in rupiah, and longer refresh cycles that miss Indonesia's rapid SME onboarding to cloud CRM. Mordor's disciplined segmentation, annual source refresh, and on-ground primary probes mitigate these issues, giving decision-makers a value they can trace back to clear variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 185.04 million (2025) | Mordor Intelligence | - |

| USD 1.20 billion (2024) | Global Consultancy A | Bundles broader SaaS categories; relies on vendor revenue allocation without local validation |

| USD 1.30 billion (2023) | Regional Consultancy B | Treats CRM as share of total software spend, applies regional averages, updates every three years |

| USD 1.40 billion (2025) | Industry Association C | Uses investment intent surveys; excludes discounting and churn, inflating totals |

The comparison underscores that our tighter scope, fresher inputs, and dual validation steps deliver a balanced, transparent baseline that managers can replicate and audit with limited effort.

Key Questions Answered in the Report

What is the projected growth rate of the Indonesia CRM Software market to 2031?

The market is forecast to expand at an 11.02% CAGR, rising from USD 205.47 million in 2026 to USD 346.58 million by 2031.

Which deployment model dominates Indonesian CRM adoption?

Cloud deployments hold 61.30% market share because they offer flexible pricing, rapid roll-out, and streamlined compliance through local sovereign-cloud partnerships.

How are SMEs influencing the Indonesia CRM Software industry?

SMEs account for 57.40% of current spending and drive volume growth, supported by government digital-upskilling programs and subscription-based CRM tiers.

Why is data sovereignty a critical issue for CRM vendors?

The 2023 Personal Data Protection Law requires personal data to be stored onshore, increasing compliance costs for international vendors and favouring providers with Indonesian data centres.

Which region is expected to grow fastest in CRM adoption?

Papua & Maluku lead with a projected 13.98% CAGR through 2031 due to improving connectivity initiatives such as the Palapa Ring project.

What functional CRM area shows the highest future growth?

Social CRM is forecast to grow at 13.62% CAGR as Indonesian consumers’ heavy social-media usage prompts firms to integrate listening and engagement tools into core customer platforms.

Page last updated on: