United States Medical Oxygen Concentrators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

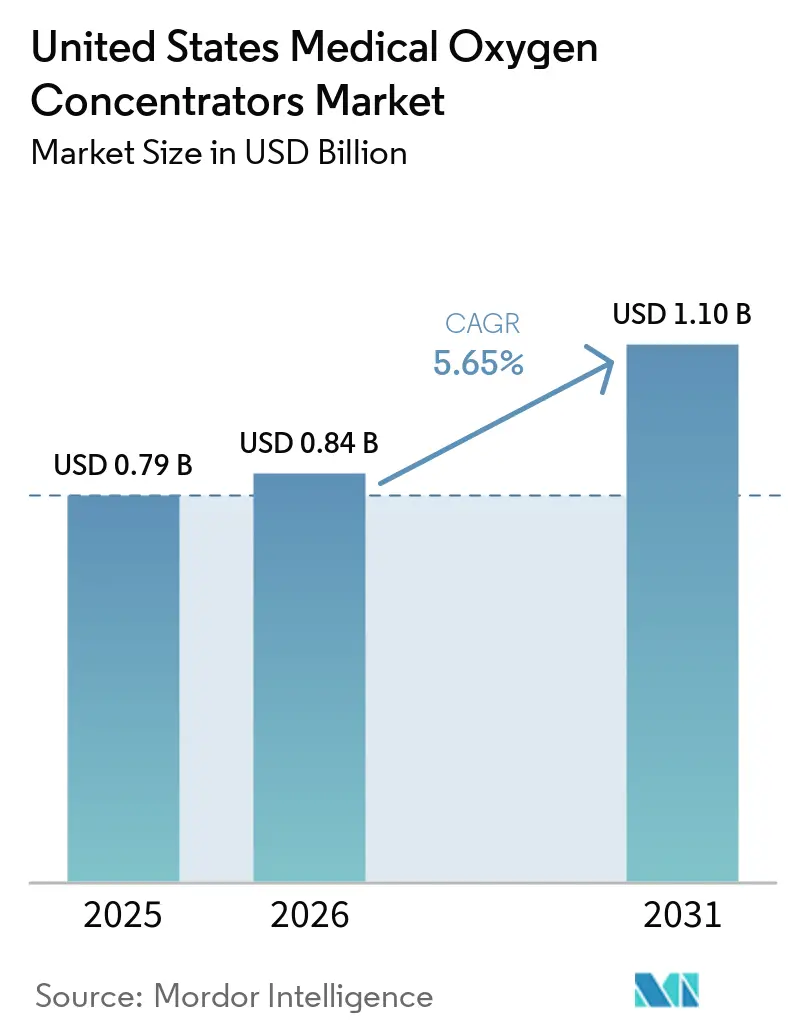

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 1.10 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

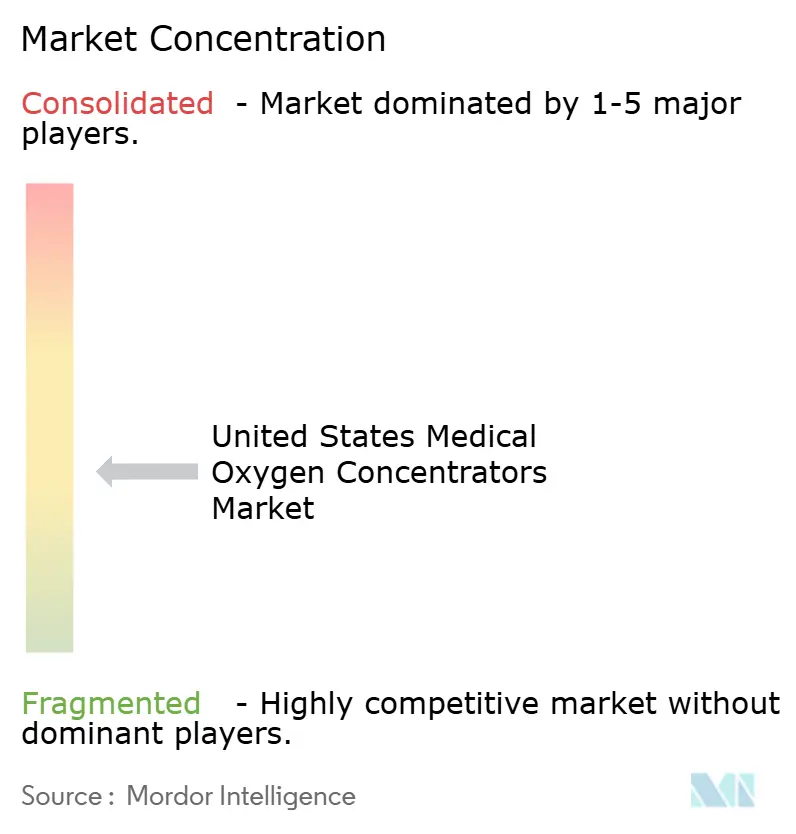

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Medical Oxygen Concentrators Market Analysis by Mordor Intelligence

The United States Medical Oxygen Concentrators Market size was valued at USD 0.79 billion in 2025 and is estimated to grow from USD 0.84 billion in 2026 to reach USD 1.10 billion by 2031, at a CAGR of 5.65% during the forecast period (2026-2031).

The market is supported by a large long-term oxygen therapy base, with more than 1 million Medicare beneficiaries receiving home long-term oxygen therapy in early 2025, while respiratory care continues to shift away from institutional settings and into the home. Demand is being shaped by a large chronic respiratory patient base and by rising oxygen use in sleep-related desaturation cases, which is pushing product design and payor planning in different directions across the United States medical oxygen concentrators market. Home-based care remains the core delivery model, and that pattern continues to direct investment toward devices that are easier to place, service, and monitor in residential settings. The market is also seeing stronger momentum in portable systems as mobility needs rise and as competitors move to capture replacement demand created by Philips Respironics' withdrawal from oxygen product lines in the United States. Reimbursement pressure remains the main operating risk, while the SOAR Act and new U.S.-assembled products show that policy change, margin protection, and logistics efficiency now sit at the center of competition in the United States medical oxygen concentrators market.

Key Report Takeaways

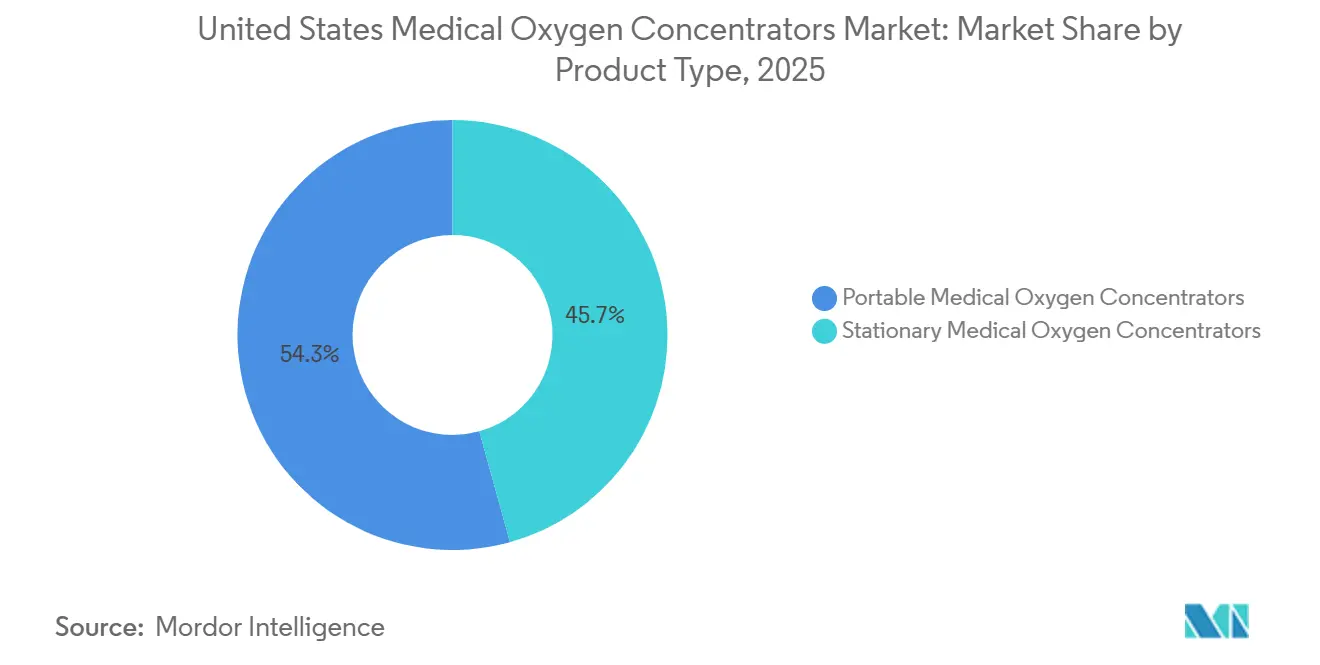

- By product type, portable medical oxygen concentrators held 54.31% of the United States medical oxygen concentrators market share in 2025, and they are also projected to record the fastest CAGR at 7.38% through 2031.

- By technology, continuous flow retained 61.24% of the United States medical oxygen concentrators market share in 2025, while pulse flow is projected to expand at the highest CAGR of 6.22% through 2031.

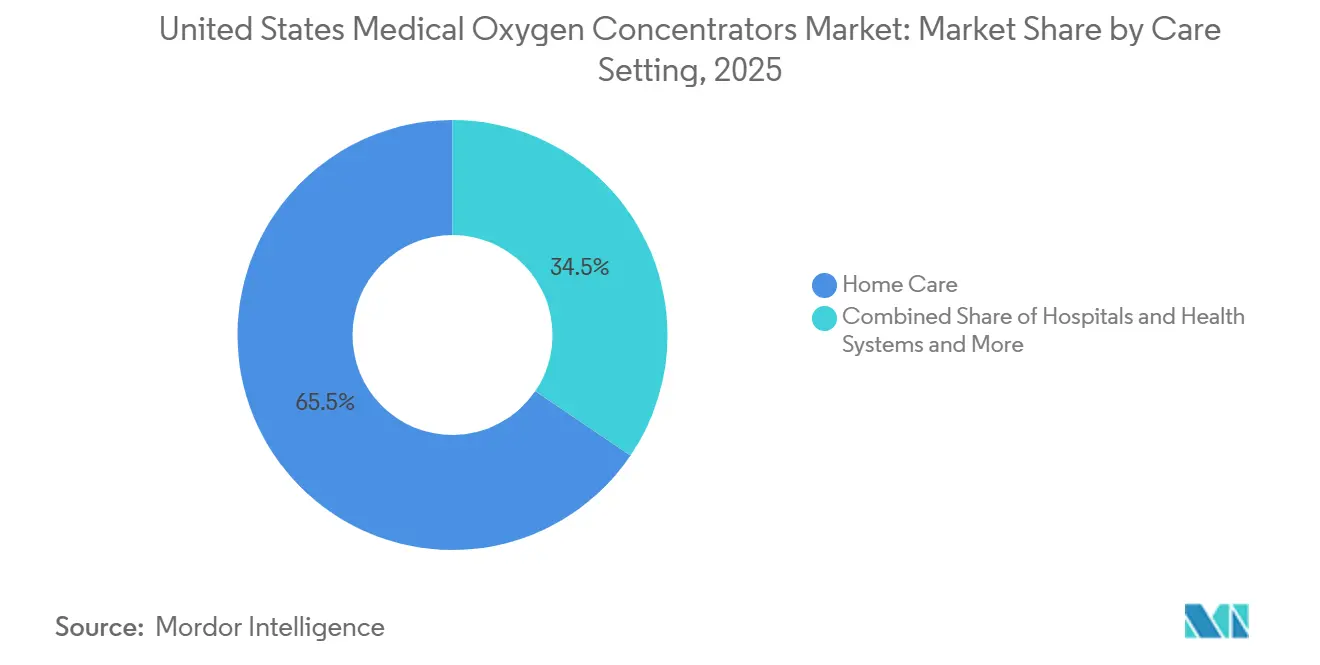

- By care setting, home care accounted for 65.52% of the United States medical oxygen concentrators market size in 2025, and it is forecast to advance at 6.25% CAGR through 2031.

- By indication, COPD represented 32.82% of the United States medical oxygen concentrators market size in 2025, while sleep apnea and sleep-related hypoxemia is projected to grow at 7.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Medical Oxygen Concentrators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| COPD Burden And Aging LTOT Population | +1.2% | South and Midwest, with 4.2% COPD prevalence each, and national relevance for the 75+ cohort | Long term (≥ 4 years) |

| Shift Toward Home-Based Oxygen Therapy | +1.0% | National, with strongest pull in the rural South and Midwest where hospital access is limited | Medium term (2-4 years) |

| Portable Concentrator Adoption And Mobility Demand | +1.1% | National, with highest uptake in suburban and urban Medicare-age populations | Medium term (2-4 years) |

| Reimbursement And Access Reform Momentum | +0.7% | National, with greatest importance in non-competitive bidding areas facing post-2023 rate resets | Short term (≤ 2 years) |

| Philips Exit-Driven Replacement Cycle | +0.6% | National, concentrated in DME-dense markets where Philips had the largest installed base | Short term (≤ 2 years) |

| Connected DME Fleet Management And Telehealth Integration | +0.4% | National, with earlier adoption in urban and technology-forward DME networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

COPD Burden and Aging LTOT Population

The market has a stable volume base in COPD, but the stronger growth driver is disease severity in older adults rather than new incidence. COPD was the fifth leading cause of death in the United States in 2023, with 141,733 deaths, and it generated annual medical costs of USD 24 billion among adults aged 45 and older. The age pattern is sharp, with prevalence rising from 0.4% in adults aged 18 to 24 to 10.5% in adults aged 75 and older, which helps explain why older Medicare patients account for a large share of continuous-flow prescriptions and long-duration use. As the Baby Boom population moves further into the 75+ bracket, the United States medical oxygen concentrators market will continue to see demand clustered in patients who need higher-capacity stationary systems for overnight and sustained daytime support. This concentration in older patients also increases dependence on Medicare reimbursement rules, because providers tend to narrow product choice when payment rates do not keep pace with device, service, and delivery costs. The result is a market where volume is dependable, but product mix can still be constrained by the economics of serving a large aging LTOT population.

Shift Toward Home-Based Oxygen Therapy

The United States medical oxygen concentrators market continues to benefit from the move toward home-based oxygen therapy, which is now tied as much to discharge planning as to patient preference. CMS National Coverage Determination 240.2 remains the key federal coverage framework for home oxygen, and the CY 2026 Home Health final rule also finalized supplier-related changes that affect how home oxygen is provided and managed[1]Federal Register, “CY 2026 Home Health Prospective Payment System Final Rule,” Federal Register, govinfo.gov. CAIRE's January 2025 launch of IntenOxy 5 was positioned directly around this setting shift, with a power draw below 350 W and a weight of 34.2 lbs, both of which support lower service and deployment costs in the home. Geographic demand reinforces the same direction, because COPD prevalence in the Midwest and South was 4.2% in each region in 2023, above the national 3.8% rate, and many of these patients live in areas where hospital access is more limited. Rural smoking patterns and slower smoking cessation in those areas further support a wide patient pool that is better served by home-ready oxygen systems than by repeated facility-based care. This keeps the United States medical oxygen concentrators market centered on residential delivery models and on products built for lower servicing cost per patient.

Portable Concentrator Adoption and Mobility Demand

Portable devices are reshaping the United States medical oxygen concentrators market more quickly than the stationary category because patient mobility is now part of the expected treatment experience. Inogen's Rove 4 launch introduced a sub-3 lb design that delivers 840 ml/min at pulse setting 4, which showed how portable performance has advanced beyond what older weight classes could support. CAIRE's FreeStyle Comfort with autoSAT became available in the United States in October 2025 and added clinically validated support for maintaining consistent FiO2 at breathing rates of 30 to 40 bpm during exercise, which addresses one of the common concerns around portable performance in active use. This matters because portable concentrators are no longer just supplemental devices for many ambulatory COPD patients, and they increasingly serve as the main daytime system in the home and outside it. Inogen's 2025 10-K also showed how closely portability is tied to reimbursement, with Medicare rentals accounting for 61.9% of the company's U.S. rental revenue in 2025[2]Inogen, Inc., “Annual Report on Form 10-K for Fiscal Year Ended December 31, 2025,” U.S. Securities and Exchange Commission Filing, investor.inogen.com. That linkage means the United States medical oxygen concentrators market is not moving toward portable devices only because patients want them, but also because the rental and service model increasingly supports them.

Reimbursement and Access Reform Momentum

Reimbursement policy is one of the few near-term issues that can quickly change the direction of the United States medical oxygen concentrators market. The SOAR Act of 2025 proposes to remove supplemental oxygen from competitive bidding and establish annual payment updates beginning January 1, 2026, which would mark the most meaningful oxygen payment reset in years[3]Bill Cassidy, “Supplemental Oxygen Access Reform (SOAR) Act of 2025,” United States Senate, cassidy.senate.gov. The policy push reflects continuing concern that the present rate structure favors basic equipment and limits the ability of suppliers to offer a broader range of clinically suitable oxygen options. If the legislation advances, suppliers would gain a clearer basis for product planning, service coverage, and equipment replacement decisions. That would also improve the alignment between clinical need and device choice, especially in cases where a portable system or a more specialized setup is more suitable than the lowest-cost stationary unit. Even before any final action, the policy debate is already influencing pricing strategy and fleet decisions across the United States medical oxygen concentrators market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Device And Battery Ownership Cost | -0.5% | National, most acute in rural and low-income areas with limited insurance coverage | Long term (≥ 4 years) |

| Reimbursement Bias Toward Basic Stationary Units | -0.6% | National, especially pronounced in competitive bidding areas | Medium term (2-4 years) |

| Post-Recall Regulatory Scrutiny And Supplier Qualification Delays | -0.4% | National, with FDA 510(k) delays affecting new entrants more than established players | Short term (≤ 2 years) |

| Portable Clinical Limits For High-Flow And Nocturnal Patients | -0.3% | National, particularly relevant in skilled nursing and hospital discharge settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device and Battery Ownership Cost

Ownership cost remains a real barrier in the United States medical oxygen concentrators market for patients who buy devices directly rather than rent them. Premium portable oxygen concentrators retail at USD 2,000 to USD 4,500, and extended battery packs add USD 200 to USD 600 per unit, which places a full portable setup beyond reach for many lower-income patients. The cost burden is more important because COPD prevalence reaches 8.2% among adults near the federal poverty level, which means financial strain and clinical need often overlap in the same patient group. The rental model softens some of that burden, but it does not eliminate it for long-term users. Inogen reported that capped patients accounted for 17.6% of its total patients on service in 2025, which shows the size of the cohort that can move into a post-cap period without a strong structural coverage pathway for ongoing device-related costs. Unless broader maintenance or supplemental coverage options become more common, this cost barrier will continue to limit direct ownership demand even as portable products improve.

Reimbursement Bias Toward Basic Stationary Units

Payment structure still steers the United States medical oxygen concentrators market toward basic stationary equipment more often than clinical flexibility would suggest. CMS reimbursement remains organized around HCPCS code E1390 for standard stationary concentrators and E1392 for portable models, and those rates have been shaped by competitive bidding and later fee corrections over time. In practice, that makes the lowest-cost 5 LPM stationary unit the most economical device for many suppliers to place, even when a portable system would better match the patient's daily activity and mobility needs. The April 2026 DMEPOS fee schedule quarterly update made changes to accessory codes, but it did not fundamentally change the core oxygen equipment rate structure. That leaves reimbursement parity for more advanced portable products dependent on legislative action rather than routine rule updates. Until that changes, suppliers will remain cautious in expanding portable offerings across the United States medical oxygen concentrators market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portable Devices Define Market Direction

Portable medical oxygen concentrators commanded 54.31% of the United States medical oxygen concentrators market share in 2025, and they are also the fastest-growing product type with a CAGR of 7.38% through 2031. That mix of current leadership and future growth is unusual and shows how decisively the United States medical oxygen concentrators market has moved toward ambulatory care. Demand is being supported by an aging but still active patient base, by FAA-compatible travel use, and by a broader patient preference for systems that fit daily movement rather than fixed-room use. Newer pulse-dose architectures have also improved the clinical standing of portable devices, which has narrowed the credibility gap that once favored stationary units in a much larger share of cases. CAIRE's autoSAT platform, supported by a 2025 Georgia State University study published in Pulmonary Therapy, showed stable FiO2 performance during higher breathing rates, which strengthens the case for portable use in more active patients.

Stationary medical oxygen concentrators still keep a meaningful installed base in home care, long-term care, and skilled nursing facilities because many patients need higher continuous-flow support, especially during overnight therapy. In the United States medical oxygen concentrators industry, that base remains important because high-flow home use, structured facility management, and limited patient mobility still favor stationary platforms. Inogen's 2025 move into stationary devices through the Yuwell-developed Voxi 5, backed by a USD 27.2 million equity investment, showed that even the leading portable specialist sees room for stationary therapy in the United States medical oxygen concentrators market. Philips' withdrawal from oxygen products has added to the stationary replacement cycle, because providers with legacy fleets need alternatives that can be deployed quickly. Drive Medical's 555 Compact, positioned as the first U.S.-assembled unit in the relaunched DeVilbiss by Drive line, was engineered for shipping efficiency with 36 units per pallet compared with 27 for the prior model, which matters in a category where freight and service costs are tightly managed.

By Technology: Pulse Flow Gains Ground Against a Larger Baseline

Continuous flow technology retained 61.24% of the United States medical oxygen concentrators market share in 2025, while pulse flow is projected to grow faster at a CAGR of 6.22% through 2031. Continuous flow remains the clinical standard for moderate-to-severe COPD and for overnight use because it delivers uninterrupted oxygen without depending on breath detection. That matters during sleep, when irregular breathing patterns and lower respiratory rates can make pulse-based delivery less reliable in some patients. The strength of continuous flow also reflects how much of the United States medical oxygen concentrators market still serves patients with higher acuity and more sustained oxygen need. At the same time, pulse flow continues to gain ground as ambulatory home use expands and as smaller devices deliver better battery life and lower carrying weight.

The more important technology shift is not flow mode alone, but the intelligence added to pulse delivery and to remote fleet oversight. CAIRE's UltraSense and autoDOSE functions in the FreeStyle Comfort deliver oxygen even when no breath is detected, which directly addresses a core clinical concern around frail or shallow-breathing patients. GCE Healthcare's Clarity Connected Care platform adds remote visibility into oxygen purity, battery status, and usage history for Zen-O and Zen-O Lite devices, which turns the device category into a more service-driven proposition for DME providers. This makes technology competition in the United States medical oxygen concentrators market less about headline flow rate alone and more about how consistently delivery, adherence, and fleet monitoring can be managed over time. As a result, the growth of pulse flow is tied not only to mobility demand, but also to smarter delivery systems that reduce the clinical tradeoff once associated with portable use.

By Care Setting: Home Care Consolidates Its Leadership Position

Home care accounted for 65.52% of the United States medical oxygen concentrators market size in 2025, and it is forecast to expand at a CAGR of 6.25% through 2031. This position reflects the combined effect of clinical practice, payor pressure, and patient preference, all of which continue to push oxygen delivery away from institutional settings and into the home. CMS NCD 240.2 already gives Medicare Administrative Contractors discretion to extend home oxygen coverage beyond the original hypoxemia thresholds in certain circumstances, which supports broader clinical use in residential settings. Reimbursement pressure has also reinforced this pattern by keeping facility-based oxygen pathways tighter and by pushing suppliers to focus on the delivery model that can serve the largest patient base. Inogen's U.S. revenue reached USD 209.8 million in 2025, and 25.4% came from direct-to-consumer rentals, a channel that sits almost entirely inside the home care setting.

Hospitals and health systems represent a smaller share because oxygen use in those settings often serves as a short bridge before discharge rather than a long-duration placement. Long-term care and skilled nursing facilities provide a steadier replacement cycle because equipment management, compliance checks, and depreciation schedules make purchasing more predictable than in acute care. That stability still matters in the United States medical oxygen concentrators market because OEMs with strong DME and enterprise relationships can hold recurring facility demand even when home care takes the larger volume share. Ambulatory transport and transitional care remain the smallest setting, but they carry strategic value because portable dual-power systems with strong battery performance are easiest to justify there. As sub-acute care pathways continue to develop, that smaller setting will keep supporting premium portable placements even if home care remains the main growth engine.

By Indication: COPD Anchors Volume, Sleep Apnea Commands Growth Trajectory

COPD represented 32.82% of the United States medical oxygen concentrators market size in 2025, making it the largest indication by volume. CDC BRFSS data for 2023 showed national COPD prevalence at 3.8%, which indicates that current volume growth is driven less by rising incidence and more by age, severity, and longer treatment duration in older adults. Regional variation reinforces that pattern, with adults in the Midwest and South recording 4.2% prevalence compared with 3.4% in the Northeast and 3.1% in the West. The link between COPD and LTOT is especially important because the older, more severe patient pool is the part of the United States medical oxygen concentrators market that most consistently needs continuous-flow support. Insurance mix matters as well, with a 2025 managed care study showing that 79.4% of insured COPD patients were covered by Medicare, which keeps this indication closely tied to DMEPOS reimbursement policy.

Sleep apnea and sleep-related hypoxemia is the fastest-growing indication, with a CAGR of 7.45% through 2031, and its rise is tied to growing clinical recognition that CPAP alone does not fully address nocturnal desaturation in every patient. Supplemental oxygen is increasingly being co-prescribed when concurrent hypoxemia is present, which broadens the addressable patient pool beyond classic LTOT categories. That pattern gives the United States medical oxygen concentrators market a second demand stream that differs from COPD because it is tied more to sleep management pathways and to overlap cases rather than to progressive airflow limitation alone. Asthma remains clinically important, but it creates more episodic oxygen need and therefore contributes less device volume than its population size would suggest. Other indications, including pulmonary fibrosis, post-COVID respiratory complications, and cardiac-origin hypoxemia, form a mixed but expanding group that broadens the clinical role of concentrators beyond traditional chronic obstructive disease use.

Geography Analysis

The United States medical oxygen concentrators market is heaviest in the South and Midwest because those regions have the highest COPD burden and a large Medicare-age population. CDC data for 2023 showed COPD prevalence of 4.2% in both the South and Midwest, compared with 3.4% in the Northeast and 3.1% in the West. States including West Virginia, Kentucky, Arkansas, and Mississippi combine high COPD burden with large rural populations, which makes home oxygen a more practical default than repeated facility-based care. The Midwest adds another layer of demand because lower urbanization and a large older patient base support centralized DME logistics for stationary fleets. Those conditions keep the United States medical oxygen concentrators market more volume-driven in the South and Midwest than in other regions. They also explain why stationary units remain important there even as portable devices gain national momentum.

The Northeast presents a different profile, with lower COPD prevalence but stronger private insurance coverage, higher healthcare spending, and greater willingness among some patients to self-pay for premium portable systems. That makes the direct-to-consumer channel more relevant in the region, which aligns with Inogen's positioning around lighter portable devices such as the Rove 4 and Rove 6 family. The West has the lowest COPD burden, but it still supports growth in pulse-flow portable demand through sleep apnea and hypoxemia cases that can sit alongside existing sleep device management. Across all regions, reimbursement pressure weighs most heavily on rural service models because longer delivery routes and thinner patient density raise the operating cost of oxygen provision. That regional difference shapes how the United States medical oxygen concentrators market balances portable growth against the economics of maintaining home service coverage.

Urban markets are moving faster toward connected DME operations because providers can more easily support telehealth workflows and remote documentation. CAIRE's myCAIRE platform and GCE's Clarity Connected Care system give DME operators access to device diagnostics, compliance data, and maintenance indicators across distributed fleets. CMS's April 2026 DMEPOS fee schedule update added new accessory and connectivity-related HCPCS codes, which begins to create a clearer billing path for connected monitoring services even though base oxygen rates did not change. That shift benefits urban providers first because they already have the systems needed to document, bill, and manage connected care activity. Over time, it will also influence fleet planning more broadly across the United States medical oxygen concentrators market.

Competitive Landscape

The United States medical oxygen concentrators market is moderately fragmented at the manufacturing level, but it remains fragmented at the DME provider level, which creates a two-layer competitive structure. A limited group of specialized manufacturers, including Inogen, CAIRE, Drive Medical, React Health, O2 Concepts, Nidek, and GCE Healthcare, compete mainly through product design, clinical support, and the breadth of their DME relationships. That structure means brand strength matters, but supplier economics and field service execution matter just as much once a device enters the provider channel. Inogen's 2025 10-K showed a broader platform strategy, with expansion beyond portables into stationary devices through Voxi 5, airway clearance through Simeox, and sleep therapy accessories through Aurora CPAP masks. CAIRE continues to differentiate through delivery algorithms such as autoSAT, while Drive Medical has emphasized domestic assembly and freight efficiency in its DeVilbiss by Drive offering.

White space in the United States medical oxygen concentrators market remains visible at both ends of the clinical spectrum. One gap sits with high-flow nocturnal patients whose needs still exceed what many portable platforms can provide consistently. The other sits with low-income LTOT users who need durable and affordable stationary systems that can stay in service for long periods with limited supervision. Philips' exit created a short-term replacement opportunity across legacy fleets, and that opening helped accelerate new stationary launches from competing manufacturers.

React Health's Phoenix 5L launch in August 2025 and Inogen's Voxi 5 launch in June 2025 both show how quickly suppliers moved to fill the stationary gap left in the market. The next competitive divide is likely to come from connected monitoring rather than from flow rate alone, because providers increasingly need adherence and service data that can be shared with payors and care teams. That is pushing the United States medical oxygen concentrators industry toward a model where device hardware, remote visibility, and provider workflow support are sold together rather than separately. In that setting, the United States medical oxygen concentrators market favors manufacturers that can support both product performance and ongoing fleet management.

United States Medical Oxygen Concentrators Industry Leaders

Inogen, Inc

Drive DeVilbiss Healthcare

CAIRE Inc.

React Health

O2 Concepts, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DeVilbiss by Drive announced the launch of the 555 Compact Oxygen Concentrator, a next-generation 5L platform engineered to help respiratory providers operate more efficiently, reduce long-term costs, and deliver a better patient experience.

- June 2025: Inogen, Inc. announced the launch of VoxiTM 5, a new stationary oxygen concentrator (SOC) designed to enhance access to high-quality oxygen therapy for long-term care patients in the United States.

United States Medical Oxygen Concentrators Market Report Scope

As per the scope of the report, a medical oxygen concentrator is a medical device that extracts oxygen from ambient air, concentrates it to a higher purity, and delivers it to patients who require supplemental oxygen therapy. It is commonly used in hospitals, clinics, and at home to treat conditions related to low oxygen levels in the blood.

The United States medical oxygen concentrators market is segmented by product type into portable medical oxygen concentrators and stationary medical oxygen concentrators. By technology, the market is categorized into continuous flow and pulse flow. Based on care settings, the segmentation includes home care, hospitals and health systems, long-term care and skilled nursing facilities, and ambulatory transport and transitional care. By indication, the market is divided into chronic obstructive pulmonary disease, asthma, sleep apnea and sleep-related hypoxemia, and other indications. For each segment, the market size and forecast are provided in terms of value (USD).

| Portable Medical Oxygen Concentrators |

| Stationary Medical Oxygen Concentrators |

| Continuous Flow |

| Pulse Flow |

| Home Care |

| Hospitals and Health Systems |

| Long-Term Care and Skilled Nursing Facilities |

| Ambulatory Transport and Transitional Care |

| Chronic Obstructive Pulmonary Disease |

| Asthma |

| Sleep Apnea and Sleep-Related Hypoxemia |

| Other Indications |

| By Product Type | Portable Medical Oxygen Concentrators |

| Stationary Medical Oxygen Concentrators | |

| By Technology | Continuous Flow |

| Pulse Flow | |

| By Care Setting | Home Care |

| Hospitals and Health Systems | |

| Long-Term Care and Skilled Nursing Facilities | |

| Ambulatory Transport and Transitional Care | |

| By Indication | Chronic Obstructive Pulmonary Disease |

| Asthma | |

| Sleep Apnea and Sleep-Related Hypoxemia | |

| Other Indications |

Key Questions Answered in the Report

What is the current and forecast value of the United States medical oxygen concentrators market?

The United States medical oxygen concentrators market was valued at USD 0.79 billion in 2025, is estimated at USD 0.84 billion in 2026, and is forecast to reach USD 1.10 billion by 2031 at a 5.65% CAGR.

Which product type leads demand in the United States?

Portable medical oxygen concentrators led with 54.31% share in 2025 and also recorded the fastest projected growth at 7.38% CAGR through 2031.

Why is home care the leading setting for oxygen concentrators?

Home care held 65.52% share in 2025 because coverage policy, discharge practices, and patient preference continue to move oxygen use away from institutional settings and into the home.

What is driving faster growth in sleep apnea and sleep-related hypoxemia use?

This indication is projected to grow at 7.45% CAGR through 2031 as supplemental oxygen is being used more often when CPAP alone does not fully address nocturnal desaturation.

Which technology still dominates clinical use?

Continuous flow retained 61.24% share in 2025 because it remains the preferred option for moderate-to-severe COPD and for overnight therapy where uninterrupted delivery is needed.

What is the biggest risk for manufacturers and DME providers?

Reimbursement remains the main risk, because current payment structures still favor basic stationary units and limit the economics of broader portable and premium device deployment.

Page last updated on: