Medical Ozone Generator Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Ozone Generator Market Analysis by Mordor Intelligence

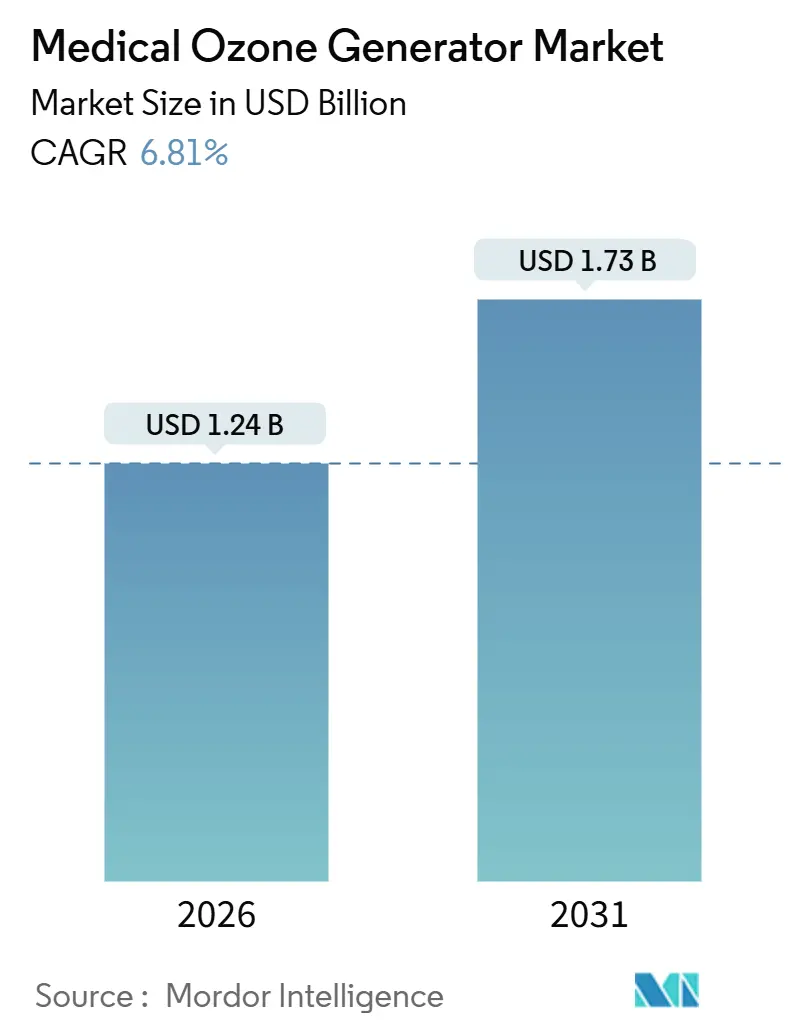

The Medical Ozone Generator Market size is estimated at USD 1.24 billion in 2026, and is expected to reach USD 1.73 billion by 2031, at a CAGR of 6.81% during the forecast period (2026-2031).

This steady trajectory rests on stronger infection-control protocols, a high burden of chronic wounds, and incremental technology upgrades that simplify dose control. Hospitals continue to anchor demand, yet decentralized care models are expanding as home healthcare providers and integrative clinics adopt portable devices. Cold plasma dielectric barrier discharge (DBD) reactors are eroding the incumbency of traditional corona-discharge systems because they deliver stable ozone concentrations without heat-related nitrogen oxide by-products. At the same time, cabinet-style machines that contain emissions below OSHA’s 0.1 ppm limit are gaining favor in open-plan clinics, addressing workplace-safety objections. Intensifying regulatory scrutiny in the United States and the European Union complicates new-product clearances, but it also deters large multinationals, opening white space for specialists with focused portfolios and regional compliance expertise.

Key Report Takeaways

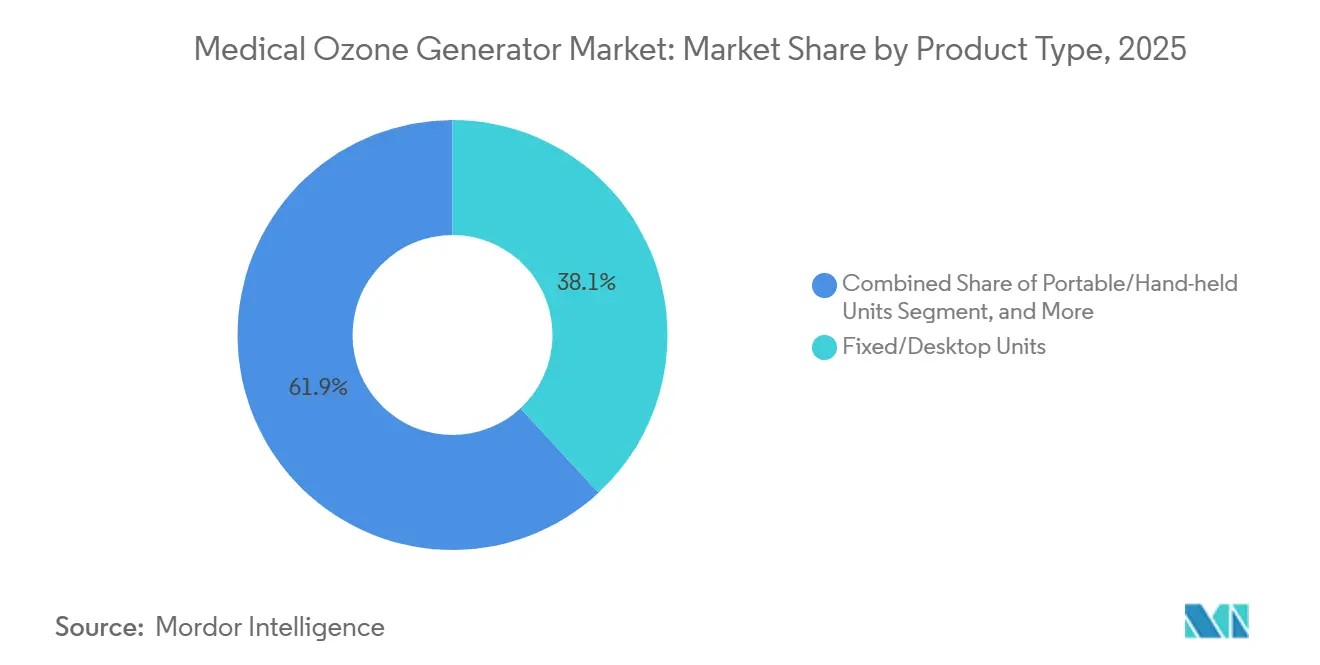

- By product category, fixed desktop units led the medical ozone generator market with 38.11% market share in 2025; portable handheld devices are forecast to advance at an 8.17% CAGR through 2031.

- By technology, corona discharge accounted for 46.09% of revenue in 2025, while cold plasma DBD reactors are expanding at an 8.98% CAGR through 2031.

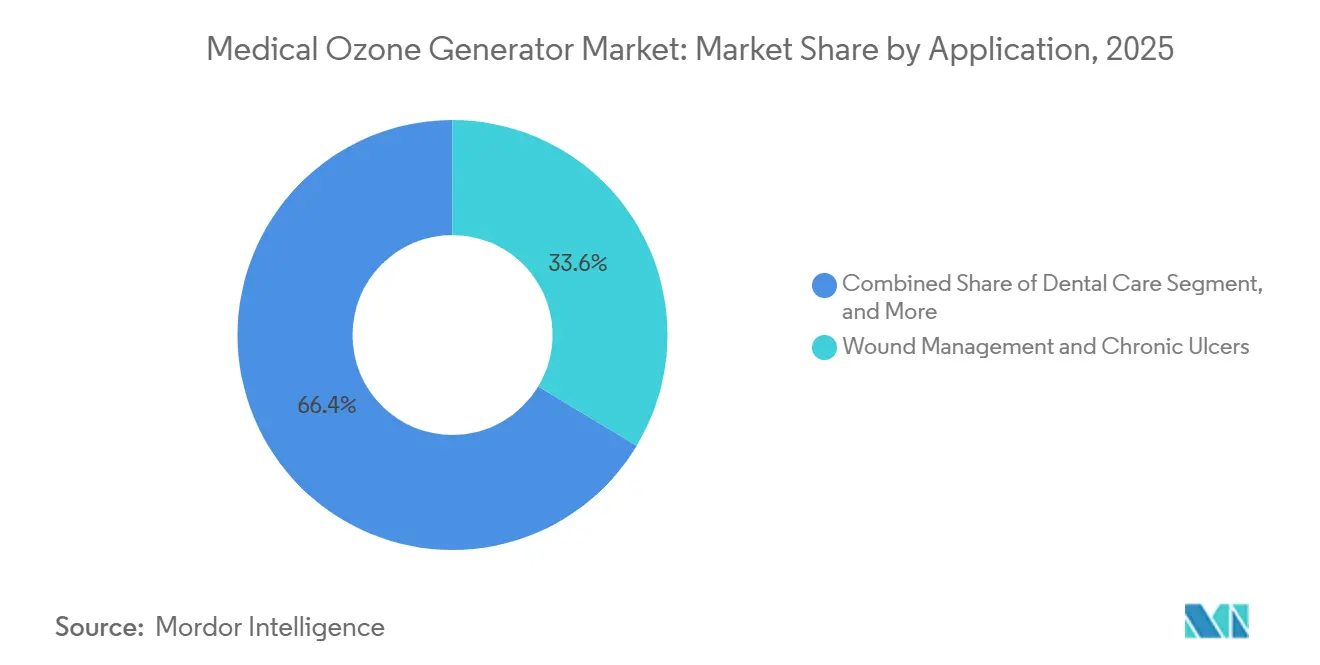

- By application, wound management and chronic ulcers accounted for 33.61% of the medical ozone generator market in 2025, and infection control and sterilization are growing at a 11.18% CAGR through 2031.

- By end user, hospitals retained a 54.39% share of the medical ozone generator market size in 2025, whereas home healthcare is growing at an 8.84% CAGR to 2031.

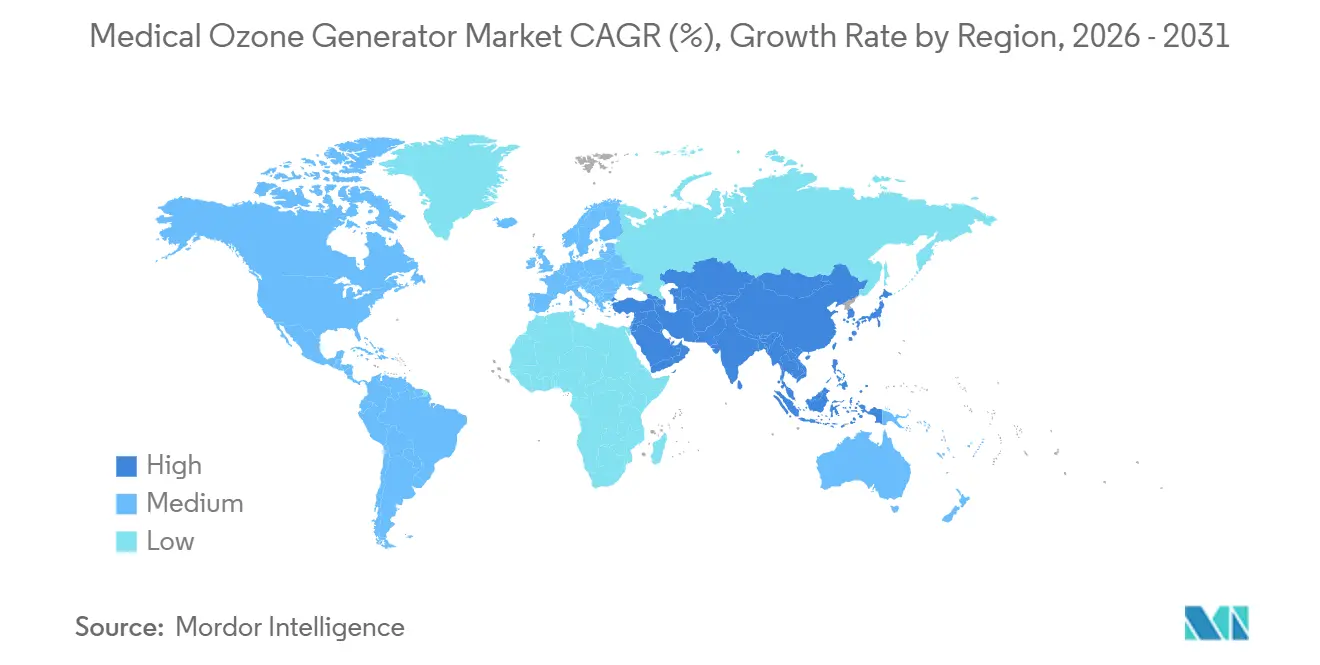

- By geography, North America captured 40.03% of revenue in 2025; Asia-Pacific is forecast to post the fastest expansion at a 9.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Ozone Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic Wounds & Infections | +1.8% | Global, pronounced in North America and Europe | Long term (≥ 4 years) |

| Growing Adoption in Integrative Medicine Clinics | +1.2% | North America, Europe, Latin America | Medium term (2-4 years) |

| Technological Advances in Dose-Control & Safety | +1.5% | Global, led by Europe and Asia-Pacific | Medium term (2-4 years) |

| Post-COVID Infection-Control Standards Boost Demand | +0.9% | Global, strongest in hospital-dense regions | Short term (≤ 2 years) |

| Wearable Micro-Ozone Patches Enabling Homecare | +0.7% | North America, Western Europe, Australia | Long term (≥ 4 years) |

| Fast-Track PPE Re-Processing Approvals | +0.6% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Wounds & Infections

Diabetic foot ulcers, venous leg ulcers, and pressure sores affect more than 25 million patients worldwide, with U.S. treatment costs exceeding USD 25 billion annually.[1]Centers for Disease Control and Prevention, “Decontamination and Reuse of Filtering Facepiece Respirators,” cdc.gov A 2025 meta-analysis covering 1,420 patients showed that ozone therapy trimmed amputation risk by up to 40% when combined with standard wound protocols. Ozone’s ability to upregulate hypoxia-inducible factor-1α accelerates angiogenesis and curbs bacterial growth, thereby attracting wound-care centers in Gulf Cooperation Council states with high diabetes prevalence. Nonetheless, reimbursement gaps in Medicare continue to exclude standalone ozone therapy, thereby restraining uptake in cost-sensitive surgical centers.

Growing Adoption in Integrative Medicine Clinics

The number of North American integrative clinics rose 18% between 2024 and 2025, and many deploy ozone generators for autohemotherapy and topical applications.[2]American Hospital Association, “AHA Annual Survey Database,” aha.org Germany’s Federal Institute for Drugs and Medical Devices (BfArM) categorizes these devices as Class IIa, which requires only CE marking, thereby accelerating market entry compared with FDA pathways. U.S. operators rely on state-level naturopathic licensure, creating a gray zone that directs medical tourism flows from Canada and Mexico. The divergence encourages focused manufacturers to tailor regulatory dossiers to each jurisdiction rather than pursue universal approvals.

Technological Advances in Dose-Control & Safety

Cold plasma DBD reactors achieve ±2% concentration stability across eight-hour cycles, far tighter than the ±8% typical of legacy corona units. Integrated sensors now modulate discharge voltage based on humidity and oxygen purity, satisfying dermatologists who need sub-80 µg/mL concentrations to avoid tissue irritation. Electrolytic systems that split water, though limited to superficial wounds, weigh 60% less and run four hours on battery by eliminating external oxygen tanks. These gains bolster the medical ozone generator market as clinicians demand portable, precise, and repeatable dosing equipment.

Post-COVID Infection-Control Standards Boost Demand

Seventy-three percent of U.S. hospitals upgraded sterilization protocols in 2025, with ozone adopted as an ethylene oxide substitute because it leaves no toxic residues. Studies demonstrate 99.9% virucidal efficacy at 20 ppm over 30 minutes, making cabinet-style ozone units ideal for rapid N95 mask and endoscope reprocessing. NHS Scotland shortened endoscope turnaround to 90 minutes after installing 120 cabinets across 14 health boards in 2024, increasing throughput by 22%. Pandemic-era FDA Emergency Use Authorizations familiarized regulators with ozone sterilizers, smoothing subsequent 510(k) submissions for permanent use.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambiguous FDA/CE Regulatory Pathways | -1.4% | North America, Europe | Long term (≥ 4 years) |

| Limited Large-Scale RCT Evidence | -0.9% | Global, acute in evidence-based markets | Medium term (2-4 years) |

| Oxygen-Supply Constraints for Feed Gas | -0.5% | South Asia, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| Workplace-Safety Scrutiny on Ozone Exposure | -0.7% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ambiguous FDA/CE Regulatory Pathways

The FDA has never cleared internal medical ozone use, forcing U.S. manufacturers to label devices strictly for external or sterilization purposes, while clinics offering autohemotherapy operate in a legal gray area.[3]U.S. Food and Drug Administration, “Ozone Generators Sold as Air Cleaners,” fda.gov Europe’s Medical Device Regulation (EU 2017/745) now requires post-market clinical evidence, extending recertification timelines by 12-18 months. Germany’s BfArM issued 14 compliance notices in 2024 for deficient data, triggering temporary withdrawals that unsettled supply chains. These uncertainties dissuade diversified medtech majors, thereby fragmenting the medical ozone generator industry.

Limited Large-Scale RCT Evidence

Meta-analyses rely on trials averaging just 80 participants, well below payer thresholds for inclusion in reimbursement. A 2025 Cochrane review identified only 6 high-quality randomized controlled trials on diabetic foot ulcers, each with different dosing schedules and outcome metrics. Without consistent endpoints, health technology assessment bodies such as NICE defer coverage decisions, slowing adoption in markets that adhere to evidence-based funding models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portability Reshapes Care Delivery

Fixed desktop units delivered 38.11% of the medical ozone generator market size in 2025, because their 10 g/h output meets hospital sterilization cycles. Portable, hand-held models are forecast to expand at an 8.17% CAGR, driving the medical ozone generator market toward decentralized care as visiting nurses and rural clinics seek backpack-friendly solutions. Cabinet machines, designed for OSHA-compliant closed-loop operation, are gaining visibility in dental offices that sterilize instruments between patients without venting ozone into treatment rooms. Portable devices using electrolytic generation remove oxygen-tank logistics, cutting monthly costs by USD 150 per patient, but lower peak concentrations limit deep-tissue efficacy, keeping fixed systems indispensable for chronic, complex wounds.

Mobile trolley units occupy the middle ground, accounting for roughly 22% of 2025 shipments because ambulatory surgical centers can roll them between procedure rooms. IoT connectivity is now standard in many trolley and desktop models, allowing biomedical engineers to track ozone output and receive maintenance alerts that reduce downtime by 25%. As home-health agencies expand, demand tilts toward smaller, rechargeable equipment, reinforcing portability as a decisive value driver in the medical ozone generator market.

By Technology: Cold Plasma Disrupts Legacy Systems

Corona discharge technology dominated the medical ozone generator market with 46.09% market share in 2025, reflecting its modest price point of USD 800-1,200. Cold plasma DBD reactors, however, are growing at 8.98% annually by eliminating nitrogen oxide by-products and delivering tight concentration control, ideal for dermatology and dental endodontics. Energy-hungry electrolytic systems are carving out a niche for portable applications despite consuming 150 W per gram of ozone, three times that of corona discharge units. Ultraviolet generation remains confined to low-output air purifiers.

A 2026 European patent filing described a hybrid DBD reactor using nanocatalysts to boost yield by 35%, potentially narrowing the cost gap with corona systems. Pulsed-power corona designs are likewise cutting energy draw by 40%, a compelling proposition for electricity-cost-sensitive clinics in South Asia. The unfolding technology race keeps the medical ozone generator market vibrant and innovation-led.

By Application: Infection Control Outpaces Wound Care

Wound management and chronic ulcers accounted for 33.61% of 2025 revenue, yet infection control and sterilization applications are growing by 11.18% annually as hospitals hunt for chemical-free disinfection. Ozone achieves 99.9% sporicidal efficacy against Clostridioides difficile at 25 ppm over 60 minutes, complementing UV-C robots that struggle with shadowed surfaces. Dental care accounted for about 18% of demand, buoyed by a 2024 trial showing that ozone irrigation halves post-treatment pain. Orthopedic pain management, especially intra-articular injections, reimbursed in Italy, accounted for 12% of demand, while gastrointestinal and dermatology uses are smaller but rising in consumer-facing medical spas across South Korea and Japan.

The veterinary and produce-sterilization niches account for the remaining 8%. As hospital environmental services departments intensify disinfection regimens, sales of cabinet-style sterilizers are pushing infection control toward equal footing with wound care in the medical ozone generator market.

By End User: Homecare Gains as Hospitals Plateau

Hospitals maintained 54.39% of 2025 demand, but growth is flattening as capital budgets normalize post-pandemic. Home healthcare is growing at an 8.84% CAGR, propelled by aging populations—Japan and Italy have populations over 65 exceeding 28%—and the cost benefits of avoiding hospital readmissions. Portable generators priced USD 1,500-3,000 fit agency budgets that bill USD 150 per wound visit. Specialty clinics and integrative centers, which together held 22% of sales, market ozone as an antimicrobial differentiator. Ambulatory surgical centers account for 12% and favor ozone for fast instrument turnover. Research institutes remain a small yet steady buyer group focused on oxidative-stress studies.

Hospital networks are decentralizing wound-care services into outpatient units, shifting purchasing preferences toward mobile trolley units that serve multiple exam rooms. Compliance with ISO 13485 quality standards is now a gating factor for procurement, driving consolidation inside the medical ozone generator industry as smaller players struggle to fund certification.

Geography Analysis

North America accounted for 40.03% of 2025 revenue, underpinned by more than 2,800 integrative clinics that exploit regulatory ambiguities in which ozone therapy is neither explicitly approved nor banned. Growth is moderated by reimbursement gaps—Medicare and Canadian provincial plans exclude ozone, forcing clinics to bundle treatments under debridement codes. Mexico’s emerging manufacturing base supplies cost-effective corona units to Central and South America, growing exports 22% in 2025. Enhanced sterilization mandates in U.S. hospitals sustain cabinet-system purchases, anchoring the regional medical ozone generator market.

Asia-Pacific is the fastest-growing region at a 9.23% CAGR, driven by China’s USD 850 billion Healthy China 2030 hospital-upgrade program. India’s USD 9 billion medical-tourism sector markets ozone as a low-cost adjunct for orthopedic pain, attracting Middle Eastern patients. Japan approved three ozone sterilizers in 2025 under expedited pandemic-preparedness protocols, signaling regulatory warmth. South Korean medical spas integrate ozone facials, adding a consumer channel to the medical ozone generator market. Australia’s Therapeutic Goods Administration remains conservative, slowing launches but assuring product quality.

Europe represents a mature yet sizable base, with Germany, Italy, and Spain capturing 62% of regional demand. Germany’s Class IIa device classification accelerates market entry, nurturing domestic champions such as Dr. J. Hänsler and Herrmann Apparatebau. The United Kingdom’s NHS Scotland deployed 120 ozone cabinets in 2024, reducing endoscope turnaround time from 6 hours to 90 minutes. Eastern European private clinics are adopting ozone to differentiate their services, driving 12% growth. The Middle East and Africa, led by GCC diabetes hotspots, account for 8% of global revenue, though oxygen-supply gaps curb broader uptake. South America contributes 7%, concentrated in Brazilian and Argentine private clinics targeting affluent patients.

Competitive Landscape

Competitive concentration is low: the top five firms held significant revenue, resulting in a market concentration score of 6. Strategic differentiation centers on regulatory navigation, vertical integration into consumables, and regional expansion. Firms that secure both FDA 510(k) clearance for sterilizers and CE marks gain access to the largest regulated markets. Others prioritize Southeast Asia and Latin America, where oversight is lighter but demand is rising. Closed-loop cabinet designs that meet OSHA’s 0.1 ppm limit unlock placements in open-plan clinics, a white space many smaller players target.

Electrolytic portable-device innovators remove oxygen-logistics hurdles, trimming patient operating costs by USD 150 per month. A 2025 hybrid DBD patent promises a 35% increase in ozone yield, potentially eroding corona discharge's cost advantage. Established brands respond by bundling training and clinical support, shifting competition toward service quality. IoT-enabled generators transmit performance metrics, reducing hospital maintenance expenses by 25% and embedding vendors deeper into customer workflows. Technology bifurcation persists: premium segments favor DBD precision, while price-sensitive regions remain loyal to rugged corona units.

Medical Ozone Generator Industry Leaders

Evozone GmbH

Promolife LLC

Ozone Solutions Inc.

BMS Service GmbH

Dr. J. Hänsler GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Konica Minolta and Tamura TECO began mass-producing the BACTECTOR 2.0SC cabinet ozone sterilizer at a smart factory in Toyokawa, Japan, targeting hospitals upgrading infection-control equipment.

- September 2024: Promolife partnered with a 14-state U.S. home-health network to deploy 500 portable generators integrated with telehealth wound-monitoring software, aiming to cut hospital readmissions by 18% over two years.

Global Medical Ozone Generator Market Report Scope

Medical Ozone Generator Market refers to the global industry involved in the design, manufacturing, distribution, and sale of medical-grade ozone generators, specialized devices that produce controlled, high-purity ozone (O₃) from medical-grade oxygen for therapeutic and disinfection purposes in healthcare settings.

The Medical Ozone Generator Market Report is segmented by product type into fixed/desktop, mobile/trolley, portable, and cabinet models; by technology into corona discharge, electrolytic, UV, and cold plasma/DBD; by application into wound management, dental, pain management, GI care, dermatology, and infection control; by end user into hospitals, clinics, ambulatory surgical centers (ASCs), home healthcare, and research institutes; and by geography into North America, Europe, Asia-Pacific, Middle East & Africa (MEA), and South America. Market forecasts are provided in terms of value (USD).

| Fixed/Desktop Units |

| Mobile/Trolley Units |

| Portable/Hand-held Units |

| Cabinet Machines |

| Corona Discharge |

| Electrolytic |

| Ultraviolet |

| Cold Plasma / DBD |

| Wound Management & Chronic Ulcers |

| Dental Care |

| Pain Management & Orthopedics |

| Gastrointestinal Care |

| Dermatology & Aesthetics |

| Infection Control & Sterilization |

| Other Applications |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Home Healthcare |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Fixed/Desktop Units | |

| Mobile/Trolley Units | ||

| Portable/Hand-held Units | ||

| Cabinet Machines | ||

| By Technology | Corona Discharge | |

| Electrolytic | ||

| Ultraviolet | ||

| Cold Plasma / DBD | ||

| By Application | Wound Management & Chronic Ulcers | |

| Dental Care | ||

| Pain Management & Orthopedics | ||

| Gastrointestinal Care | ||

| Dermatology & Aesthetics | ||

| Infection Control & Sterilization | ||

| Other Applications | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Home Healthcare | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the medical ozone generator market in 2026?

The market reached USD 1.24 billion in 2026 and is projected to grow at a 6.81% CAGR to USD 1.73 billion by 2031.

Which product category holds the highest medical ozone generator market share?

Fixed desktop units led with 38.11% share in 2025, driven by their high output suited to hospital sterilization needs.

What segment is growing fastest within the medical ozone generator market?

Portable hand-held units are expanding at an 8.17% CAGR through 2031 as home healthcare and rural clinics seek mobile solutions.

Which region is expected to see the quickest growth?

Asia-Pacific is forecast to record a 9.23% CAGR, driven by hospital upgrade programs in China and growing medical tourism in India.

Why are cold plasma DBD reactors gaining traction?

DBD technology delivers precise ozone dosing at room temperature, without nitrogen oxide by-products, making it ideal for dermatology and dental applications.

Page last updated on: