High Flow Oxygen Therapy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 2.25% CAGR |

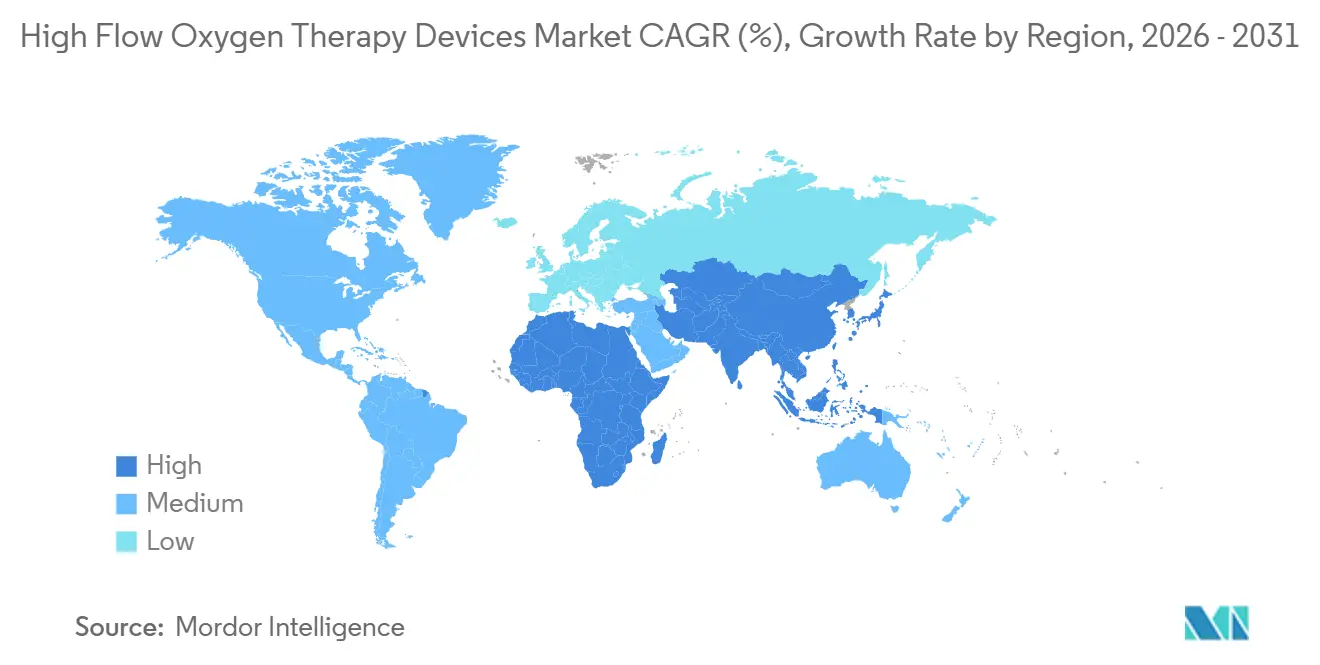

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Flow Oxygen Therapy Devices Market Analysis by Mordor Intelligence

The High Flow Oxygen Therapy Devices Market size is projected to be USD 1.51 billion in 2025, USD 1.53 billion in 2026, and reach USD 1.72 billion by 2031, growing at a CAGR of 2.25% from 2026 to 2031.

A modest topline masks opposing forces: pandemic-era overcapacity continues to pressure selling prices even as clinical protocols embed high-flow therapy in emergency rooms, ICUs, and increasingly the home. Hospitals are replacing legacy interfaces with precision heated-humidification modules, while manufacturers divert R&D toward portable, battery-backed systems and AI-guided flow titration that promise outcome gains and new reimbursement streams. North America remains the revenue anchor, yet Asia-Pacific provides the steepest growth curve as China and India build tier-2 respiratory infrastructure. Competitive intensity is moderate; the top five suppliers control roughly two-thirds of global sales, but regional specialists leverage cost leadership and carbon-tariff advantages to chip away at share. Overall, the high flow oxygen therapy devices market is shaped by a tug-of-war between cost containment and technology upgrades that keeps headline growth steady but hides rapid portfolio rotation.

Key Report Takeaways

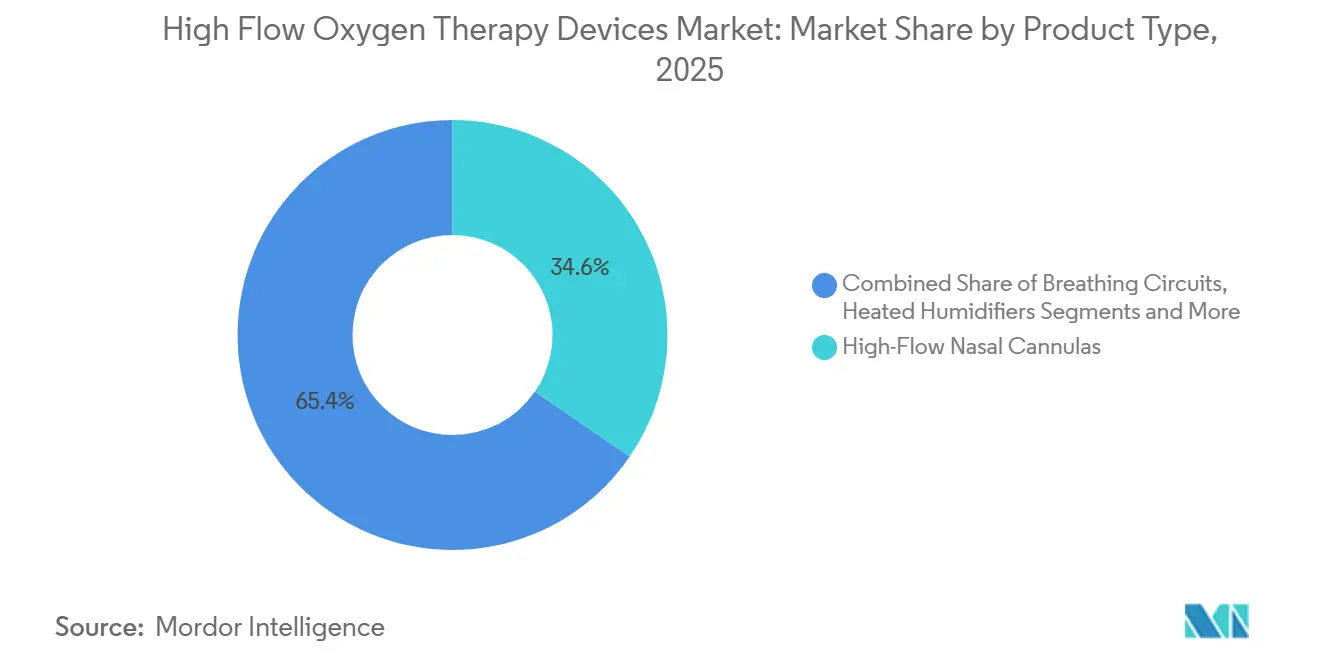

- By product type, high-flow nasal cannulas led with 34.56% revenue share in 2025, while heated humidifiers are advancing at a 5.26% CAGR through 2031.

- By device mobility, stationary hospital systems accounted for 61.21% share in 2025, yet portable and home systems are accelerating at a 6.54% CAGR to 2031.

- By humidification technology, active heated solutions dominated with 79.24% share in 2025; bubble humidification is expanding at a 6.83% CAGR through 2031.

- By application, acute respiratory failure represented 44.23% of the high flow oxygen therapy devices market size in 2025, whereas COPD management is projected to rise at a 4.72% CAGR to 2031.

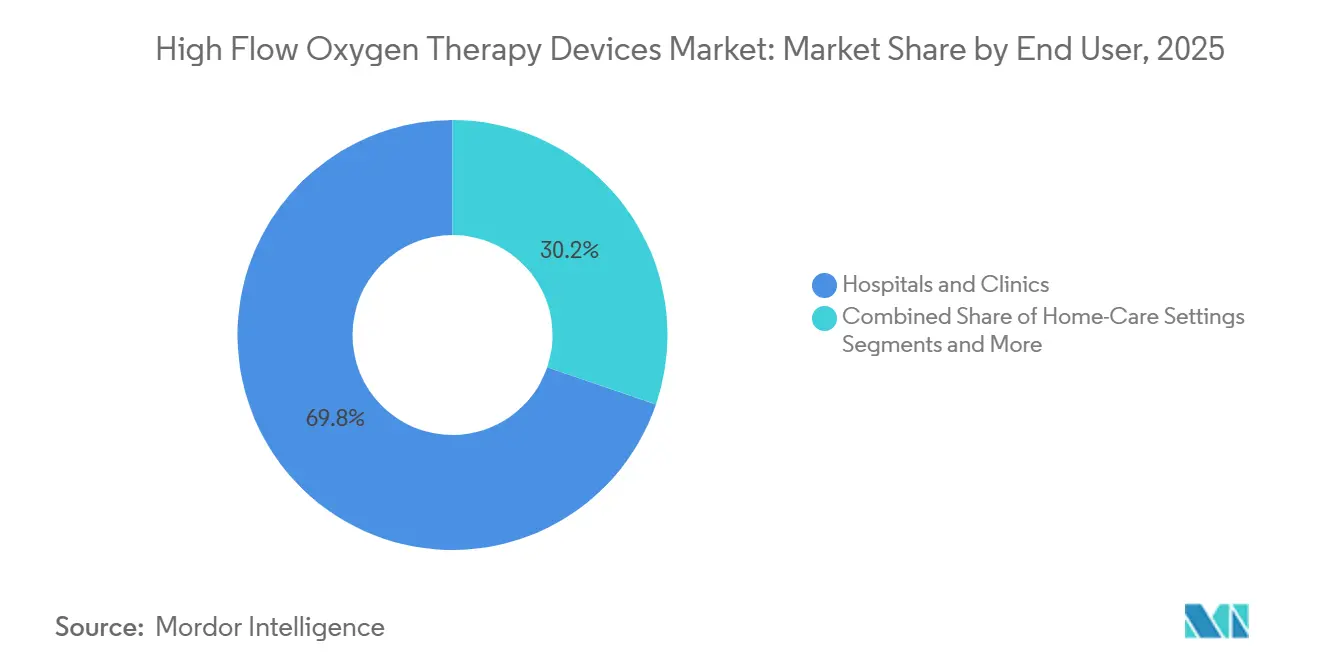

- By end user, hospitals and clinics held 69.77% share in 2025, but home-care settings are growing at a 5.48% CAGR through 2031.

- By geography, North America commanded 36.67% revenue share in 2025; Asia-Pacific is forecast to post the fastest 4.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Flow Oxygen Therapy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing COPD & Pneumonia Prevalence Elevating Non-Invasive Oxygen Demand | +0.6% | Global, acute burden in China, India, United States | Long term (≥ 4 years) |

| Post-COVID-19 Protocols Institutionalizing HFOT in Emergency Rooms & Wards | +0.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Shift to Home High-Flow Therapy Supported by Reimbursement Expansion | +0.4% | United States, Germany, Japan | Medium term (2-4 years) |

| Technological Advances in Humidification & Smart Flow Monitoring | +0.3% | North America, Europe, Australia | Long term (≥ 4 years) |

| Emergence of AI-Guided Flow Titration Improving Clinical Outcomes | +0.2% | North America, select European centers | Long term (≥ 4 years) |

| Regional Carbon-Tariff Incentives Favoring Locally Sourced Hardware | +0.2% | European Union, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing COPD & Pneumonia Prevalence Elevating Non-Invasive Oxygen Demand

Global COPD cases stand near 392 million and continue to rise, putting sustained pressure on respiratory resources.[1]World Health Organization, “Chronic Obstructive Pulmonary Disease Fact Sheet,” WHO, who.int Pneumonia admissions among U.S. seniors grew 18% between 2020 and 2024.[2]Centers for Disease Control and Prevention, “Pneumonia Fast Facts,” CDC, cdc.gov Multicenter trials published in 2024 showed that high-flow therapy lowers intubation rates by up to 20% in acute hypoxemic failure. These outcomes encourage earlier use of nasal cannulas for COPD exacerbations, reinforcing recurring consumable demand. Home-use protocols that keep saturation above 90% now qualify for Medicare coverage, broadening patient access.

Post-COVID-19 Protocols Institutionalizing HFOT in Emergency Rooms & Wards

A 2025 survey of 320 U.S. hospitals revealed that 78% deploy high-flow systems as a first-line response when SpO₂ dips below 92%, almost doubling pre-pandemic adoption.[3]American Association for Respiratory Care, “2025 Hospital HFOT Survey,” AARC, aarc.org Continued use reflects perceived infection-control benefits and reduced ICU transfers. European Respiratory Society guidelines issued in 2024 cemented high-flow oxygen as preferred therapy for immunocompromised patients. Infrastructure gaps linger, however: rural facilities in the United States Midwest experienced winter power outages that forced temporary shutdowns of high-flow equipment.

Shift to Home High-Flow Therapy Supported by Reimbursement Expansion

Medicare’s January 2025 decision to reimburse portable high-flow devices released roughly USD 240 million in annual funding for COPD management in the home. Germany and Japan are rolling out parallel policies, together adding tens of thousands of eligible patients. Suppliers responded by promoting starter kits that bundle cannulas, humidifiers, and circuits. Yet a CHEST study found 34% of home users needed emergency help to clear alarms, underlining the training gap.

Technological Advances in Humidification & Smart Flow Monitoring

Next-generation heated humidifiers such as Fisher & Paykel’s Optiflow+ hold delivered gas temperature within ±0.5 °C, minimizing mucosal drying. ResMed’s AirSpiral tubing all but eliminates condensation, lowering nursing workload. A 2025 randomized trial showed optimized humidification cut nasal inflammation by 28%. Meanwhile, Philips embedded cloud-linked flow sensors that flag deviations beyond 5 L/min, but stricter FDA cybersecurity rules are stretching launch timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Pandemic Equipment Overcapacity Depressing ASPs | -0.4% | Global, acute in North America & Western Europe | Short term (≤ 2 years) |

| High Electricity Dependence Limiting Adoption in Rural Hospitals | -0.3% | Sub-Saharan Africa, South Asia, Latin America rural zones | Long term (≥ 4 years) |

| Stringent FDA/CE Cybersecurity Rules Delaying Connected Launches | -0.2% | North America, Europe | Medium term (2-4 years) |

| Competition from Low-Cost NIV Kits in Price-Sensitive Markets | -0.3% | India, Southeast Asia, sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Equipment Overcapacity Depressing ASPs

U.S. hospitals held 2.8 high-flow units per ICU bed in 2024, more than double pre-pandemic norms. Surplus stock forced 15%–20% discounts on replacement tenders, squeezing margins. German university hospitals cited inventory leverage to win bids 18% below 2023 prices. Average stationary-system ASP dropped from USD 4,200 in 2023 to USD 3,500 in 2025, a direct drag on the high flow oxygen therapy devices market.

High Electricity Dependence Limiting Adoption in Rural Hospitals

Typical devices draw 80–150 W continuously. Rural clinics in Nigeria, Kenya, and Bangladesh face daily 4-hour outages and must run costly diesel generators. Solar pilots in India stalled when monsoon cloud cover cut output below operating thresholds. Portable units with 4–6-hour battery life help during transport but cannot sustain overnight therapy, curbing rural uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Drive Recurring Revenue

High-flow nasal cannulas generated 34.56% of 2025 sales, anchoring the high flow oxygen therapy devices market share within interfaces. Heated humidifiers, however, are growing at 5.26% and are pivotal to clinical comfort strategies. Fisher & Paykel’s MR850 became the U.S. ICU reference unit in 2025, appearing in 68% of surveyed protocols. Breathing circuits, water chambers, and probes form an annuity worth USD 180–240 per 30-day episode, a prop for the high flow oxygen therapy devices market size.

Accessories and full-face masks cover niche cohorts such as pediatric or claustrophobic patients. ResMed’s AirFit F30i found traction in European sleep centers treating overlap-syndrome cases. Portable kits bundled for home care compress margins 12%–15% versus hospital sales but simplify procurement for durable-medical-equipment suppliers. ISO 80601-2-90 testing obligations still favor incumbents with certified labs.

By Device Mobility: Portability Gains as Home Therapy Expands

Stationary hospital systems controlled 61.21% of 2025 revenue, yet portable platforms are sprinting ahead at 6.54% CAGR as payers push for earlier discharge. Medicare’s 2025 rule change unlocked battery-powered units under 3 kg like Vapotherm’s Precision Flow Go. Portable runtime averages 4–6 hours at 50 L/min, limiting overnight independence. Hamilton’s T1 extends to 8 hours via smart blower modulation, but the USD 1,200 premium curtails volume.

Ventilator-integrated modules that toggle between invasive and high-flow modes grow 3.8% annually as ICU teams accelerate weaning. Stationary systems remain favored in surge planning because they deliver up to 80 L/min and tie into central gas outlets, though pandemic lessons spurred stockpiling of portables for field deployment.

By Humidification Technology: Active Heating Dominates, Bubble Methods Resurge

Active heated humidifiers owned 79.24% of 2025 revenue, reflecting clinician demand for 37 °C, 100% relative-humidity gas delivery. A 2024 Cochrane review confirmed that active heating cuts therapy intolerance by 34% compared with passive alternatives. Yet bubble systems, free of electronics and 70% cheaper, are racing ahead at 6.83% CAGR, meeting needs in South Asia and Africa where budgets and power supply are thin. Apollo Hospitals documented 92% clinician satisfaction in bubble pilots despite lack of fine temperature control.

Passover and HME-based methods continue to fade as evidence links inadequate humidification to higher discontinuation. Manufacturers such as Vincent Medical sell retro-fit bubble chambers compatible with existing high-flow engines, allowing cash-strapped hospitals to upgrade cheaply.

By Application: COPD Management Rises as Chronic-Care Focus Shifts

Acute respiratory failure retained 44.23% of 2025 demand, but COPD management is climbing fastest at 4.72% CAGR as payers embrace chronic-care cost avoidance. CMS opened reimbursement to an estimated 340,000 U.S. beneficiaries in 2025, boosting the high flow oxygen therapy devices market. Neonatal and pediatric care contributes 18% and grows 3.9%; a 2025 meta-analysis showed a 22% intubation-rate reduction in preterms.

Post-operative and palliative uses expand 3.2% under enhanced-recovery protocols endorsed by the American Society of Anesthesiologists. Specialty cases such as carbon-monoxide poisoning remain niche but gained validation from the Undersea and Hyperbaric Medical Society in 2025.

By End User: Home-Care Settings Gain as Hospital Saturation Looms

Hospitals and clinics absorbed 69.77% of 2025 spending, yet their growth slows to 2.1% as equipment ratios near saturation. Home-care settings expand 5.48% as durable-medical-equipment networks offer subscription models at USD 280–350 per month. A 2025 Respiratory Care survey reported 41% of patients needed an unscheduled troubleshooting visit, adding USD 120–180 in service costs.

Hybrid discharge models cut 30-day readmissions by 19% in a Kaiser Permanente pilot, demonstrating value for integrated health systems. Ambulatory and long-term care centers grow 3.6%, filling the transition gap between inpatient and home.

Geography Analysis

North America contributed 36.67% of 2025 revenue, buoyed by Medicare reimbursement and entrenched ICU protocols. Yet post-pandemic overcapacity trimmed stationary-system ASPs 17% between 2023 and 2025, limiting top-line lift. FDA cybersecurity rules elongate new-product cycles, slowing connected-device penetration.

In Europe, Carbon tariffs now steer hospitals toward EU-made systems, advantaging Draegerwerk and Air Liquide while inflating import costs. Asia-Pacific is the fastest-growing region at 4.32% CAGR as national insurance in China and India funds tier-2 respiratory upgrades. Rural grid instability, however, keeps high-flow use concentrated in urban hubs.

In Middle East & Africa and South America, Oil-funded Gulf projects mirror Western adoption curves, while Brazil’s 2024 directive integrated high-flow therapy into public hospitals. South African solar pilots stalled when battery costs exceeded plan. Currency volatility in Argentina reduced device imports 23% in 2025.

Competitive Landscape

The high-flow oxygen therapy device is a moderately concentrated industry. Fisher & Paykel’s Optiflow and Airvo lines remain the hospital benchmark, driving NZD 1.68 billion (USD 1.04 billion) in 2025 respiratory sales. ResMed and Philips leverage sleep-apnea channels to cross-sell high-flow modules with cloud analytics. Regulatory cybersecurity hurdles raise entry barriers, giving incumbents breathing room while smaller entrants struggle to finance audits.

White-space niches are emerging. Masimo and Hamilton Medical commercialize AI titration that trims nurse interventions by one-third. Great Group Medical and Vincent Medical push bubble humidifiers 40% below multinational prices in South Asia. Portable-home units cleared by FDA in 2024 from Vapotherm and Teleflex now vie for payer approval beyond the United States. Patent filings, such as Fisher & Paykel’s 2025 adaptive humidification algorithm, signal a shift toward software-led differentiation.

High Flow Oxygen Therapy Devices Industry Leaders

Fisher & Paykel Healthcare

Vapotherm

ResMed

Teleflex Medica

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: VARON has launched the VP-8 Lite Portable Oxygen Concentrator, a lightweight and portable device for oxygen support on the go. It supports daily activities, travel, and active lifestyles while being user-friendly and affordable. The VP-8 Lite builds on the success of the VP-8G, known for its reliability and high oxygen output.

- January 2026: Air Liquide Healthcare began shipping carbon-neutral bubble humidifiers from its new Lyon line to European hospitals targeting Scope 3 emission cuts.

- May 2025: Tri-anim Health Services signed an exclusive U.S. distribution deal for Telesair’s Bonhawa high-flow oxygen device, with roll-out starting June 2025

Global High Flow Oxygen Therapy Devices Market Report Scope

As per the scope of the report, High Flow Oxygen Therapy (HFOT) devices are non-invasive systems that deliver heated, humidified, and oxygen-enriched air at high flow rates to meet respiratory needs and enhance comfort.

The High Flow Oxygen Therapy Devices Market Report is segmented by Product Type, Device Mobility, Humidification Technology, Application, End User, and Geography.

By Product Type, the market is segmented into High‑Flow Nasal Cannulas, Breathing Circuits, Heated Humidifiers, High‑Flow Oxygen Masks, and Accessories & Consumables. By Device Mobility, the market is segmented into Portable/Home HFNC Systems, Stationary Hospital Systems, and Ventilator‑Integrated HFOT Modules. By Humidification Technology, the market is segmented into Active Heated, Bubble, and Passover/Passive. By Application, the market is segmented into Acute Respiratory Failure, COPD Management, Neonatal & Pediatric Care, Post‑Operative & Palliative Care, and Others. By End User, the market is segmented into Hospitals & Clinics, Home‑Care Settings, and Ambulatory & Long‑Term Care Centers. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| High-Flow Nasal Cannulas |

| Breathing Circuits |

| Heated Humidifiers |

| High-Flow Oxygen Masks |

| Accessories & Consumables |

| Portable / Home HFNC Systems |

| Stationary Hospital Systems |

| Ventilator-Integrated HFOT Modules |

| Active Heated Humidification |

| Bubble Humidification |

| Passover / Passive Humidification |

| Acute Respiratory Failure |

| COPD Management |

| Neonatal & Pediatric Care |

| Post-Operative & Palliative Care |

| Others (e.g., CO toxicity) |

| Hospitals & Clinics |

| Home-Care Settings |

| Ambulatory & Long-Term Care Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | High-Flow Nasal Cannulas | |

| Breathing Circuits | ||

| Heated Humidifiers | ||

| High-Flow Oxygen Masks | ||

| Accessories & Consumables | ||

| By Device Mobility | Portable / Home HFNC Systems | |

| Stationary Hospital Systems | ||

| Ventilator-Integrated HFOT Modules | ||

| By Humidification Technology | Active Heated Humidification | |

| Bubble Humidification | ||

| Passover / Passive Humidification | ||

| By Application | Acute Respiratory Failure | |

| COPD Management | ||

| Neonatal & Pediatric Care | ||

| Post-Operative & Palliative Care | ||

| Others (e.g., CO toxicity) | ||

| By End User | Hospitals & Clinics | |

| Home-Care Settings | ||

| Ambulatory & Long-Term Care Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global demand for high-flow oxygen equipment be by 2031?

Revenue is projected to reach USD 1.72 billion by 2031, reflecting a 2.25% CAGR over 2026–2031.

Which product type is growing fastest?

Heated humidifiers are expanding at 5.26% CAGR as hospitals upgrade to precision climate control.

Why are portable high-flow systems gaining traction?

Medicare and other payers now reimburse home therapy, and new battery-backed units weigh under 3 kg, enabling earlier discharge.

What limits adoption in rural hospitals?

Continuous electricity needs of 80–150 W and frequent grid outages make operation costly without generators or solar backups.

Who leads the competitive landscape?

Fisher & Paykel Healthcare, ResMed, Philips, Vyaire Medical, and Draegerwerk together hold roughly two-thirds of global sales.

How do carbon tariffs affect procurement in Europe?

EU carbon-border levies add 4%–7% to imported device costs, nudging buyers toward locally manufactured systems.

Page last updated on: