Global Portable Oxygen Concentrators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

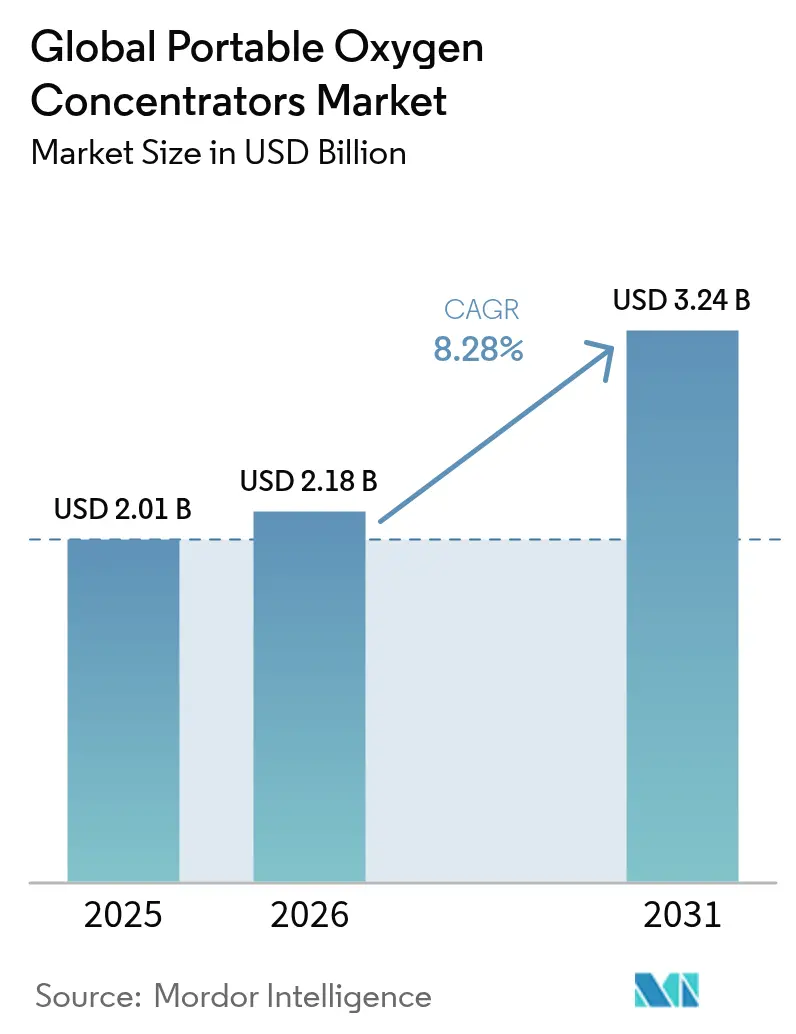

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 3.24 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Portable Oxygen Concentrators Market Analysis by Mordor Intelligence

The portable oxygen concentrators market size is expected to grow from USD 2.01 billion in 2025 to USD 2.18 billion in 2026 and is forecast to reach USD 3.24 billion by 2031 at 8.28% CAGR over 2026-2031. Device miniaturization, higher‐density batteries, and broader reimbursement for home oxygen therapy are keeping demand high even after the acute phase of the pandemic. Philips Respironics’ 2024 withdrawal removed two major models and opened capacity for rivals, accelerating production scale-ups at Drive DeVilbiss Healthcare and new launches from GCE Group. Continuous flow devices still dominate prescriptions, yet pulse flow units are growing fast thanks to lighter form factors and longer runtimes. Chronic Obstructive Pulmonary Disease (COPD) continues to anchor the portable oxygen concentrators market, while post-COVID respiratory distress and wellness travel use cases expand the customer base. Asia–Pacific is emerging as the fastest-growing region as China and India simplify medical-device registration and invest in local production capacity.

Key Report Takeaways

- By technology, continuous flow held 53.20% of portable oxygen concentrators market share in 2025, while pulse flow is on course to expand at a 9.29% CAGR through 2031.

- By application, COPD commanded 62.10% share of the portable oxygen concentrators market size in 2025; respiratory distress syndrome is projected to post the fastest 9.88% CAGR to 2031.

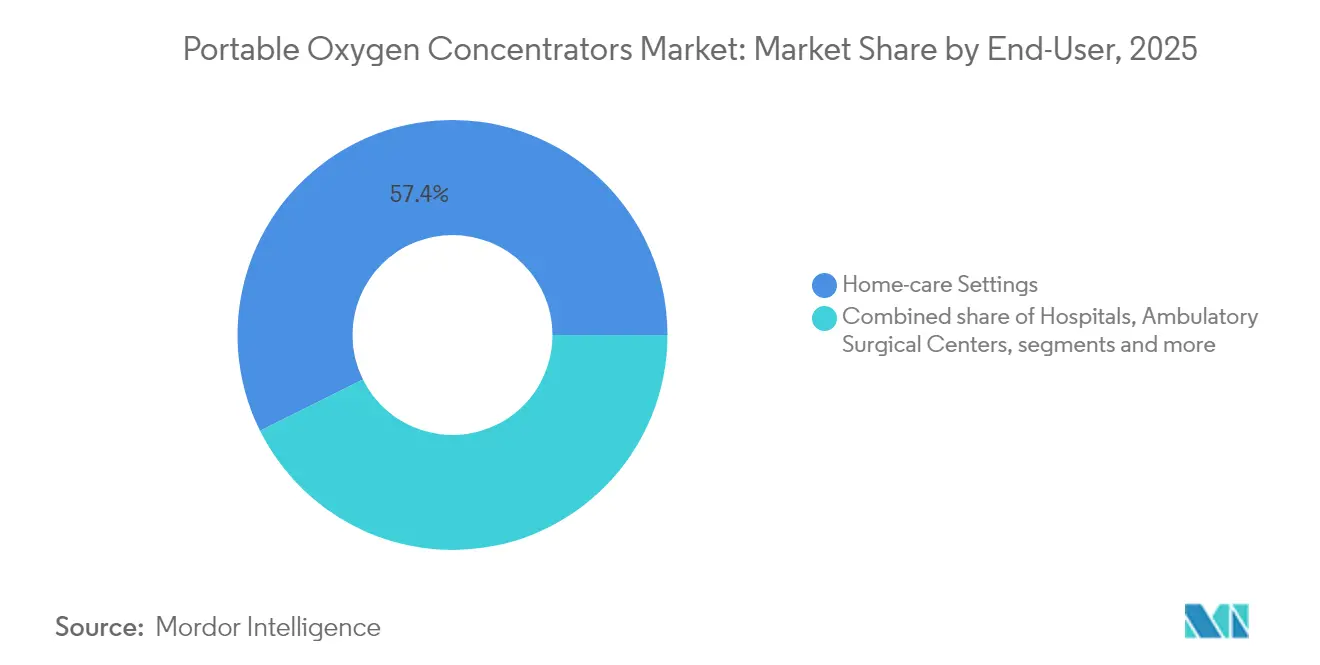

- By end-user, home-care settings represented 57.35% of revenue in 2025 and are advancing at an 8.71% CAGR to 2031.

- By distribution channel, Durable Medical Equipment (DME) stores led with 43.80% in 2025, while direct-to-consumer sales are forecast to climb at 11.16% CAGR.

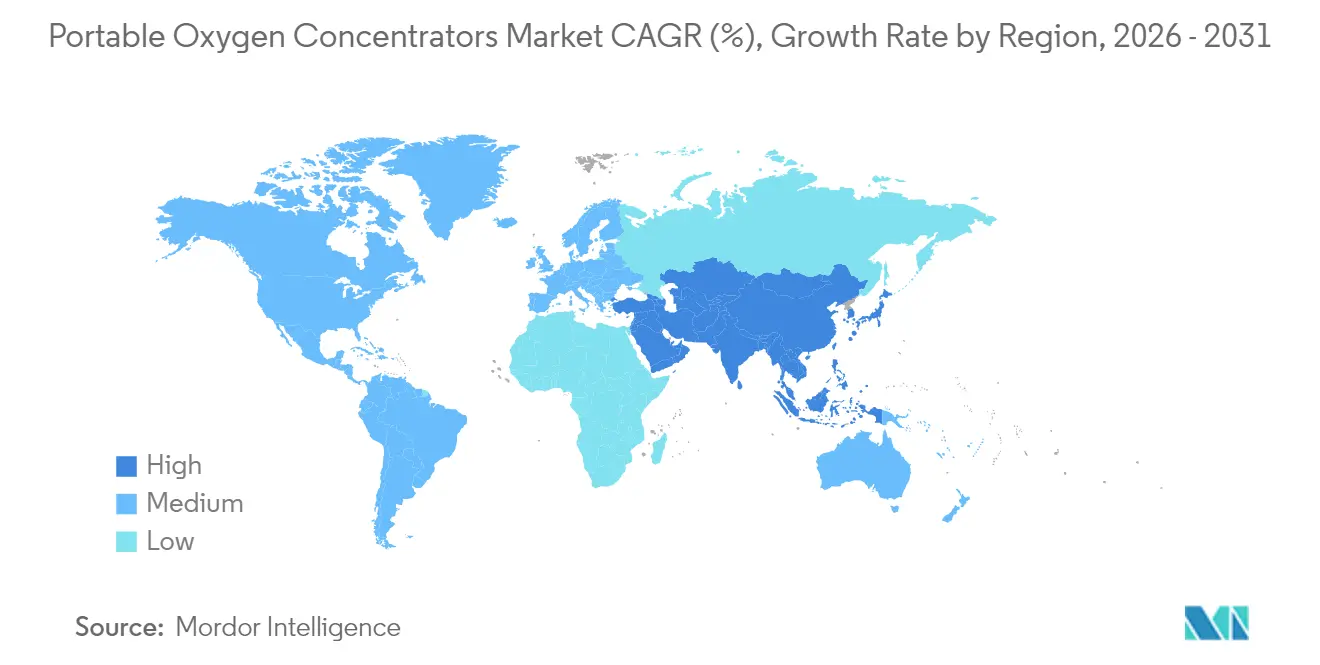

- By geography, North America contributed 43.25% revenue in 2025, yet Asia–Pacific is expected to record the strongest 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Portable Oxygen Concentrators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Re-imbursement expansion in home oxygen therapy | +1.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Miniaturisation & battery-density breakthroughs | +1.5% | Global, with early adoption in North America & Japan | Long term (≥ 4 years) |

| Increasing prevalence of chronic respiratory diseases | +2.1% | Global, highest impact in APAC & MEA | Long term (≥ 4 years) |

| Growth in adventure & wellness travel requiring portable oxygen | +0.7% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Ageing population with higher oxygen-dependency | +1.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Post-COVID home-based long-term oxygen therapy demand | +1.2% | Global, with highest impact in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement expansion in home oxygen therapy

Medicare caps monthly rentals at 36 months, after which suppliers must keep devices in service for the duration of medical need, giving providers predictable revenue while reducing payer outlays.[1]Centers for Medicare & Medicaid Services, “42 CFR 414.226 Oxygen and Oxygen Equipment,” ecfr.govHCPCS code updates in 2024 simplified billing and trimmed administrative friction for clinicians and DME suppliers. Commercial insurers are mirroring this framework as evidence mounts that home oxygen lowers readmissions. Telehealth assessments, first allowed during COVID-19 and now permanent, let rural or mobility-limited patients qualify without in-person visits. These policy shifts enlarge the addressable patient pool and reinforce the portable oxygen concentrators market.

Miniaturization and battery-density breakthroughs

Lithium-zeolite columns improve oxygen purity while shrinking canister size, letting manufacturers cut device weight below 3 pounds without compromising flow. Inogen’s Rove 4 produces up to 840 ml/min and lasts 5 hours 45 minutes on a single battery, reflecting rapid gains in energy efficiency. The OXFO system conserved 92.3% oxygen compared with continuous flow delivery during clinical testing. FAA-compliant electronics allow safe in-flight use up to 10,000 feet, widening mobility options for oxygen-dependent travelers. Real-time purity sensors built on Arduino platforms now deliver usage analytics, supporting preventive maintenance and boosting device reliability.

Rising prevalence of chronic respiratory diseases

The CDC reported COPD prevalence ranging from 3% in Hawaii to 12% in West Virginia in 2024, with death-rate disparities underscoring persistent unmet need for supplemental oxygen. A multiyear study found COPD rates in adults 50+ climbed from 9.02% in 2000 to 9.88% in 2020, with higher incidence among women and specific racial groups. The American Lung Association counted 11.68 million U.S. COPD cases in 2022, pointing to a stable core patient base. Global COPD burden of 213.39 million cases confirms long-term demand for ambulatory oxygen solutions. These epidemiological trends cement the centrality of COPD within the portable oxygen concentrators market.

Adventure and wellness travel adoption

FAA rules require FDA-cleared devices that meet electromagnetic-interference tests, prompting manufacturers to design purpose-built models for flight and high altitude. Research shows intermittent hypoxic pre-acclimatization combined with exercise raises tolerance to acute hypoxia, supporting wider recreational use of portable units. Wearable cerebral oximeters now give live feedback during mountain climbing or ski trips, enabling precise flow adjustments. The Department of Transportation mandates that U.S. carriers allow specific approved models, further normalizing airborne POC usage. Together, these developments lift discretionary demand beyond clinical settings.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of bacterial contamination from poor maintenance | -0.9% | Global, higher impact in regions with limited healthcare education | Medium term (2-4 years) |

| Adverse dermatological effects from prolonged cannula use | -0.6% | Global, with higher reporting in developed markets | Short term (≤ 2 years) |

| Import tariffs on lithium-ion cells raising BOM costs | -1.4% | North America, with supply chain impacts globally | Short term (≤ 2 years) |

| Counterfeit low-cost POCs eroding brand trust | -0.8% | APAC & MEA, with spillover effects in online channels globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import tariffs on lithium-ion cells

The United States imposed 125% duties on Chinese goods, affecting 75% of Chinese-made medical devices and many POC battery packs.[2]Case Medical, “The 2025 Tariffs: What It Means for Us,” casemed.com Hospitals devote 10.5% of budgets to medical supplies, so tariff-driven price hikes tighten procurement budgets. Manufacturers are moving assembly to Mexico and pursuing dual-sourcing strategies to manage costs. Transfer-pricing reviews and customs-valuation optimization are recommended to avoid margin erosion. Short-run price volatility may slow near-term growth in the portable oxygen concentrators market, yet long-term demand fundamentals remain intact.

Counterfeit low-cost POCs eroding trust

The FDA warned Shenzhen Moyeah and LEEL Tech in 2024 for marketing unapproved respiratory devices, spotlighting online marketplaces that bypass regulatory oversight. MAUDE reports cite device failures in unauthorized units such as the VARON VP-2, including inaccurate flow delivery. An Inogen G5 malfunction during air transport led to a patient fatality, underscoring the stakes of device integrity. Recalls for fire risk, such as the Invacare PerfectO2 V affecting 384,767 units, illustrate how safety lapses damage brand equity across the portable oxygen concentrators market. Heightened regulatory scrutiny and patient education campaigns aim to stem counterfeit penetration but add compliance overhead for legitimate manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Continuous Flow Retains the Lead while Pulse Flow Accelerates

Continuous flow units accounted for 53.20% of portable oxygen concentrators market share in 2025 and generated the largest slice of the portable oxygen concentrators market size, supported by clinician preference for uninterrupted delivery during severe hypoxemia. Advanced compressor designs and higher-efficiency sieves continue to raise L per minute output at lower noise levels. Pulse flow devices are posting a 9.29% CAGR as lighter casings and smarter breath-detection algorithms satisfy active users. Battery runtimes exceeding five hours make pulse models viable for day-long excursions. Industry emphasis on user-centric design means patients increasingly select devices that match lifestyle rather than just prescription parameters.

Hybrid modes that switch automatically between continuous and pulse delivery are emerging in the portable oxygen concentrators market. Algorithm-driven pulse modulation conserves oxygen during sleep without waking users, narrowing the clinical gap with stationary systems. Research at Texas A&M demonstrates machine-learning models that predict flow needs based on real-time accelerometer data, foreshadowing adaptive devices that minimize manual adjustments. These innovations should expand the portable oxygen concentrators industry footprint among moderate disease cohorts who previously relied on heavier stationary equipment.

By Application: COPD Dominates but Post-COVID Complications Lift New Segments

COPD represented 62.10% of portable oxygen concentrators market share in 2025 and formed the core contributor to portable oxygen concentrators market size because of well-established long-term therapy protocols. Rising diagnosis rates in women and aging populations keep the COPD segment stable. Respiratory distress syndrome is registering the fastest 9.88% CAGR as clinicians extend portable therapy beyond chronic care into early post-acute recovery. Post-COVID fibrosis cases require intermittent yet mobile oxygen, adding new cohorts.

Asthma and interstitial lung disease together form a moderate but important slice of the portable oxygen concentrators market. Nearly 38% of fibrosing ILD patients now initiate oxygen therapy, especially those with idiopathic pulmonary fibrosis. Evidence from a 2024 randomized trial suggests no outcome difference between 24-hour versus 15-hour oxygen use, implying shorter dosing regimens that favor portable units could become standard. Such findings are likely to reinforce physician confidence in mobile devices for diverse pulmonary conditions.

By End-User: Home-Care Remains the Growth Engine

Home-care settings captured 57.35% of revenue in 2025 and add the most incremental volume to the portable oxygen concentrators market. Payers prefer home therapy to limit costly inpatient stays, and patients value autonomy. About 1.5 million U.S. adults rely on supplemental oxygen, yet many caregivers still report equipment-handling challenges, pointing to the need for better education programs. Hospitals keep a meaningful share because mobile concentrators expedite early ambulation and facilitate discharge. Ambulatory surgical centers use portable units for short procedures that require transient oxygen support.

Long-term care facilities and emergency medical service fleets increasingly specify POCs rather than cylinders due to lower logistics costs and easier stock rotation. The FlexO2 patient-controlled selector improved autonomy scores from 14 to 92, highlighting how interface upgrades can widen acceptance among elderly users. Digital connectivity for remote performance monitoring now integrates with chronic-care management apps, supporting value-based payment models.

By Distribution Channel: Direct-to-Consumer Platforms Disrupt the DME Status Quo

Durable Medical Equipment outlets held 43.80% revenue in 2025, anchored by insurer contracts and local respiratory therapists who handle setup and education. However, direct-to-consumer e-commerce is expanding at 11.16% CAGR and is reshaping the portable oxygen concentrators market. Secure portals now connect prescriptions directly to manufacturer warehouses, cutting lead times and enabling rapid claims processing.

Hospital pharmacies act as bridge channels for inpatient-to-outpatient transitions, bundling concentrators into discharge kits. Specialty respiratory dealers address niche performance requirements such as adventure sports kits or pediatric needs. The broader DME sector is forecast to climb from USD 208.5 billion in 2022 to USD 331.1 billion by 2030, and acquisition multiples around 11× EBITDA illustrate investor confidence in scalable distribution models. As replenishment algorithms automate filter and battery ordering, patients experience fewer supply gaps and better adherence.

Geography Analysis

North America generated 43.25% of 2025 revenue for the portable oxygen concentrators market, supported by Medicare’s predictable payment ceilings and comprehensive FAA rules that enable unhindered domestic air travel with approved models. U.S. suppliers must now enroll in the revised CMS-855S form category for multifunction respiratory devices, ensuring tighter oversight and credentialing standards. Canada is expanding provincial funding for home oxygen and fostering cross-border trade in subcomponents, while Mexico positions itself as an alternative manufacturing hub for tariff-sensitive lithium-ion assemblies.

Asia–Pacific is the fastest-growing region at an 11.02% CAGR, contributing the largest incremental gain to portable oxygen concentrators market size through 2031. China recorded a 25.4% jump in medical device registrations in 2023 as regulators accelerated review pathways. India expects its medical-device market to hit USD 50 billion by 2025, yet still imports 70% of its devices, creating scope for joint ventures that combine Western technology with local assembly. Japan leads early adoption of miniaturized devices as an aging society aligns with robotics-enabled home care, and South Korea’s reimbursement parity with cylinders accelerates POC penetration.

Europe shows steady uptake as the Medical Device Regulation framework harmonizes safety standards, although supply chains feel margin pressure from energy costs and raw-material inflation. Middle East and Africa experience rising demand as Gulf states invest in national telehealth platforms and sub-Saharan countries build oxygen infrastructure in response to pandemic lessons. South America registers moderate growth, with Brazil leveraging public-private procurement frameworks to supply portable units to rural clinics and Argentina encouraging local production to offset currency volatility. Regional heterogeneity necessitates flexible go-to-market strategies that mix direct imports, contract manufacturing, and strategic partnerships.

Competitive Landscape

The portable oxygen concentrators market is moderately consolidated. Philips Respironics’ exit in 2024 reshuffled shares, creating openings that Drive DeVilbiss Healthcare and GCE Group rapidly filled through line expansions and manufacturing scale-ups.[3]GCE Group, “Addressing Concerns Amidst Philips Respironics Discontinuation,” us.gcegroup.com Inogen leverages Intelligent Delivery Technology to adjust doses breath by breath and posted 6.4% business-to-business revenue growth to USD 335.7 million in 2024. ResMed invests 7% of turnover in R&D and integrates sleep-apnea cloud platforms with oxygen delivery, seeking a unified respiratory-care ecosystem.

Strategic alliances shape regional access. In February 2025 Inogen bought a 9.9% stake in Chinese device maker Yuwell for USD 27.2 million to secure APAC manufacturing and distribution channels. Drive DeVilbiss collaborates with Mexican electronics firms to mitigate tariff exposure, while CAIRE emphasizes channel partnerships with adventure-travel outfitters for high-altitude models. Market entrants target underserved segments such as pediatric chronic lung disease and extreme sports, often using online-first sales to bypass traditional DMEs.

Product recalls and counterfeit crackdowns influence competitive standing. Invacare resolved its Class 2 recall in March 2025 after field corrections on 384,767 units. FDA warning letters to rogue manufacturers improve confidence in approved brands but also raise compliance costs. Overall, leading firms differentiate via safety records, connected-device roadmaps, and multi-flow flexibility, while smaller players exploit agility in niche markets and emerging economies.

Global Portable Oxygen Concentrators Industry Leaders

Koninklijke Philips NV

Chart Industries

Invacare Corporation

Inogen, Inc.

Precision Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Inogen announced a USD 27.2 million investment for a 9.9% stake in Yuwell to deepen Asia–Pacific reach.

- March 2025: FDA terminated the Class 2 recall of Invacare PerfectO2 V after completing field corrections on 384,767 units.

- October 2024: Inogen launched the Rove 4 portable concentrator delivering up to 840 ml/min in a sub-3-pound form factor.

- August 2024: FDA issued warning letters to Shenzhen Moyeah and LEEL Tech for distributing unapproved respiratory devices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the portable oxygen concentrators market as sales of compact, electrically powered devices that enrich ambient air to >= 90 % oxygen using pressure-swing adsorption and are intended for ambulatory, home-care, or travel use. Units approved for in-flight operation and dual-mode flow settings are included.

Scope Exclusion: Stationary oxygen concentrators, compressed gas cylinders, and liquid oxygen systems are outside the boundary of this assessment.

Segmentation Overview

- By Technology

- Continuous Flow

- Pulse Flow

- Others

- By Application

- Chronic Obstructive Pulmonary Disease (COPD)

- Asthma

- Respiratory Distress Syndrome

- Others

- By End-User

- Hospitals

- Home-care Settings

- Ambulatory Surgical Centers

- Long-Term Care Facilities

- Emergency Medical Services (EMS)

- By Distribution Channel

- Durable Medical Equipment (DME) Stores

- Direct-to-Consumer (Online)

- Hospital Pharmacies

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed pulmonologists, reimbursement consultants, and durable medical equipment distributors in North America, Europe, China, and India. These conversations validated real-world replacement rates, average rental durations, and the share of pulse-flow devices, filling gaps that literature alone could not bridge.

Desk Research

We began with public data sets from agencies such as the World Health Organization, the US Centers for Medicare & Medicaid Services, and Eurostat customs files that track HS 901920 shipments, which helped size patient pools and trade flows. Industry bodies, for example, the American Association for Respiratory Care, and regulatory portals listing FDA and CE clearances provided technology adoption clues. Company 10-K filings, investor decks, and reputable press articles further anchored average selling prices and warranty cycles. Select paid resources from D&B Hoovers and Dow Jones Factiva supplied company revenue splits and deal news. The sources cited above are illustrative; many additional references informed the desk phase.

Market-Sizing & Forecasting

A top-down patient prevalence-to-therapy uptake model estimated annual demand, which was then cross-checked through sampled manufacturer shipments and distributor channel checks. Key variables like COPD incidence, home-oxygen therapy penetration, average device life (4-5 years), FAA in-flight approvals, and country-level reimbursement limits drive the model. Multivariate regression on aging population growth, smoking rates, and disposable income creates the 2025-2030 projection. Bottom-up roll-ups correct for anomalies such as bulk tenders, ensuring totals remain grounded.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, followed by automated variance checks against new regulatory filings and trade data. Our models refresh every twelve months, with interim revisions when policy or recall events materially shift assumptions.

Why Our Portable Oxygen Concentrators Baseline Commands Reliability

Published market values often diverge because firms pick different device lists, price bands, and refresh cadences. By limiting scope to genuinely portable units and updating the baseline each year, Mordor delivers a figure decision-makers can trust.

Key gap drivers include rivals bundling stationary systems, omitting smaller regions, or fixing a single global ASP despite currency swings. Mordor's approach adjusts for these factors and blends both demand-side (patient) and supply-side (unit shipment) lenses.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.01 B (2025) | Mordor Intelligence | - |

| USD 2.14 B (2025) | Global Consultancy A | Includes selected stationary models and uses higher blended ASP |

| USD 0.92 B (2025) | Trade Journal B | Covers only pulse-flow units and excludes Latin America & MEA |

In sum, because our analysts tie every assumption to observable metrics and revisit the file annually, our baseline stands as the most balanced and reproducible starting point for strategy, budgeting, or investment planning.

Key Questions Answered in the Report

What is the current size of the portable oxygen concentrators market?

The portable oxygen concentrators market size reached USD 2.18 billion in 2026 and is projected to grow to USD 3.24 billion by 2031 at an 8.28% CAGR.

Which technology segment is growing fastest?

Pulse flow devices are the fastest-growing technology, registering a 9.29% CAGR as lighter batteries and adaptive algorithms gain acceptance among mobile users.

How are tariffs affecting industry costs?

125% U.S. duty on many China-made components raises bill-of-materials costs, prompting manufacturers to diversify supply chains or shift production to tariff-free zones.

Which region is expected to post the highest growth?

Asia–Pacific is forecast to expand at an 11.02% CAGR through 2031, driven by regulatory reforms, rising chronic respiratory disease prevalence, and local manufacturing incentives.

What safety checks should buyers consider?

Consumers should confirm FDA clearance, review recall histories, and purchase from authorized dealers to avoid counterfeit units that may fail to deliver therapeutic oxygen.

Page last updated on: