Medical Oxygen Gas Cylinders Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

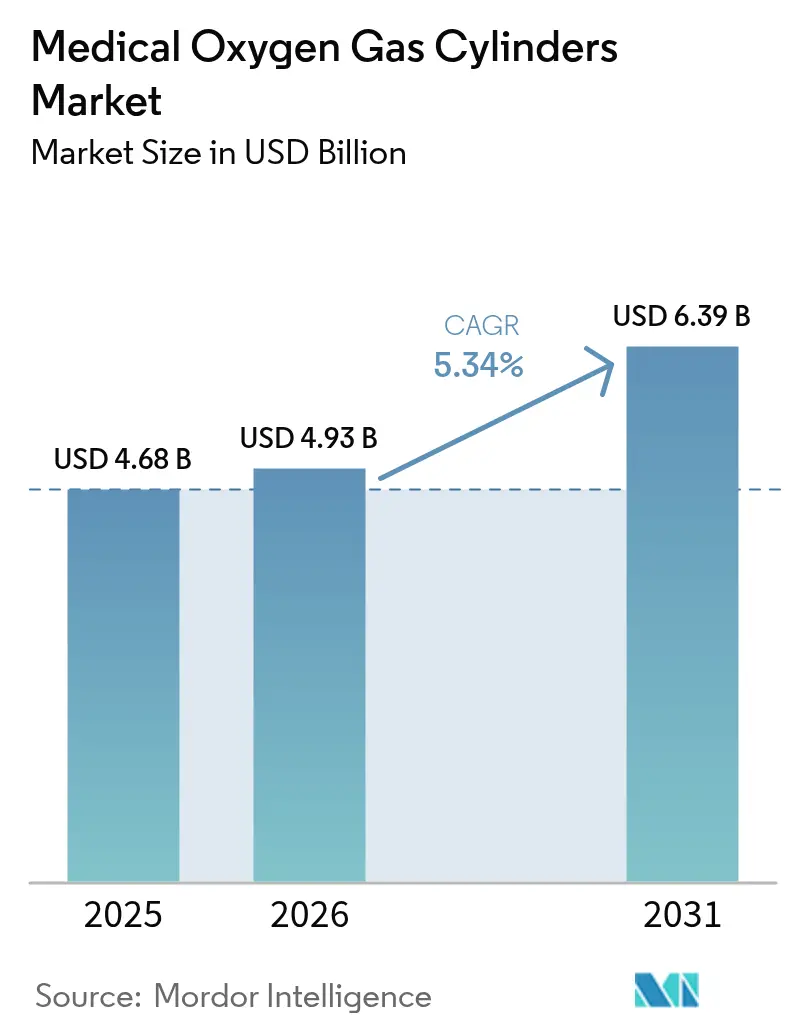

| Market Size (2026) | USD 4.93 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Oxygen Gas Cylinders Market Analysis by Mordor Intelligence

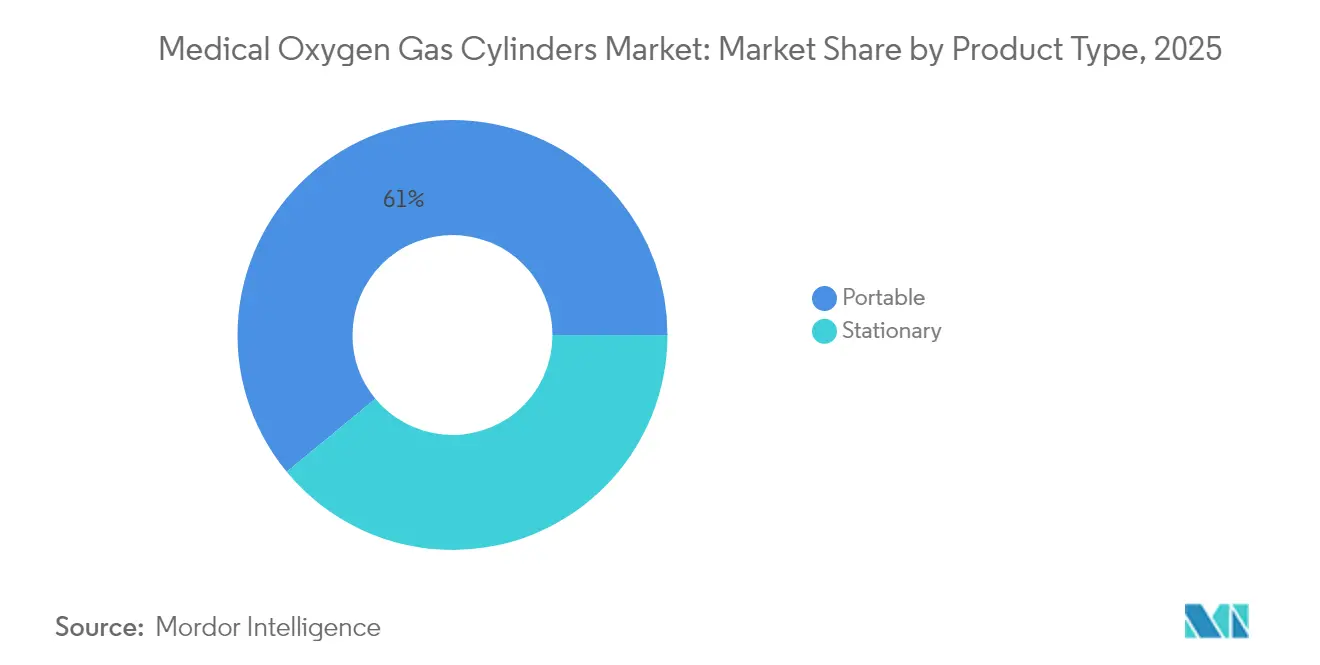

The medical oxygen gas cylinders market size in 2026 is estimated at USD 4.93 billion, growing from 2025 value of USD 4.68 billion with 2031 projections showing USD 6.39 billion, growing at 5.34% CAGR over 2026-2031. Portable and lightweight cylinders command a 61.55% revenue share and grow at 8.25% CAGR, while aluminum retains material leadership at 46.53% share despite composite cylinders expanding at 11.85% CAGR. Demand rises as chronic respiratory diseases affect 380 million people globally and the 65+ population in the United States alone reaches 57.8 million. Hospitals and clinics remain dominant users at 49.63% share, yet home healthcare now exhibits the fastest demand growth at 10.27% CAGR. Regional performance is led by North America at 36.63% share owing to robust Medicare reimbursement, whereas Asia–Pacific is the fastest-growing region at 9.87% CAGR as governments invest in oxygen security programs.

Key Report Takeaways

- By product type, portable and lightweight cylinders captured 60.98% of the medical oxygen gas cylinders market share in 2025; stationary units lag while portable units accelerate at 8.17% CAGR through 2031.

- By material, aluminum led with 46.11% share of the medical oxygen gas cylinders market size in 2025; carbon-fiber composites record the highest projected CAGR at 11.64% through 2031.

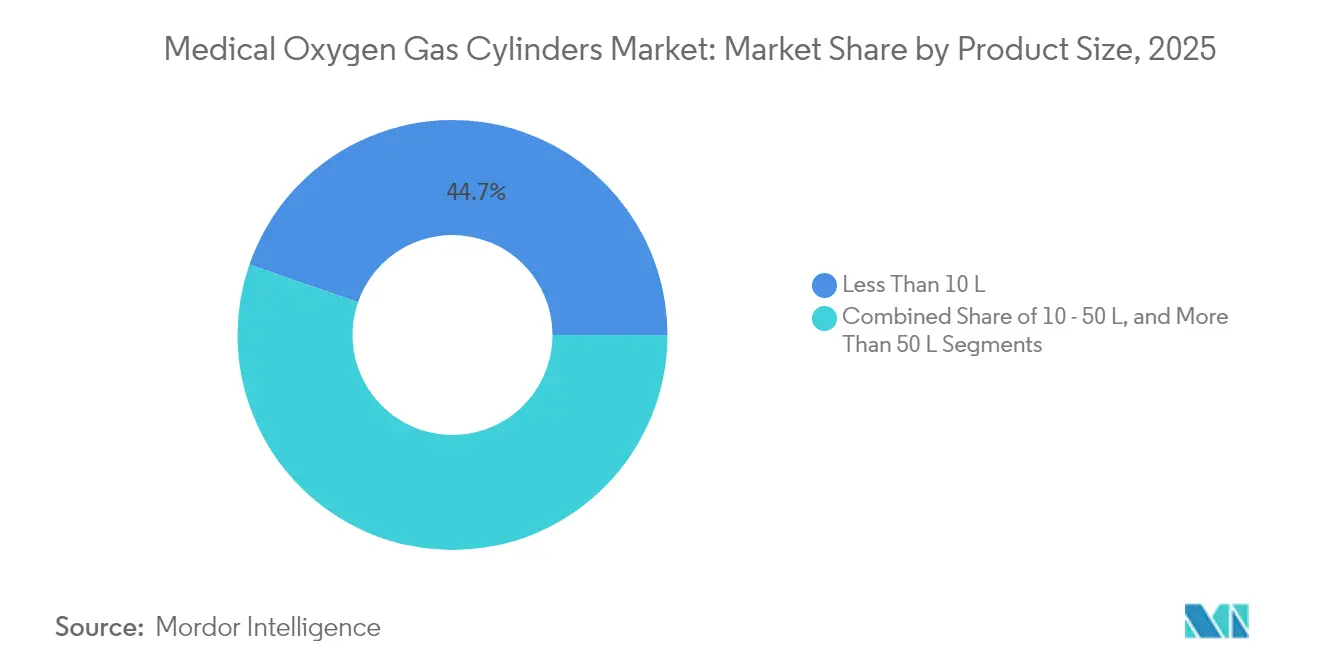

- By product size, the sub-10 liter category accounted for 44.68% of the medical oxygen gas cylinders market size in 2025 and advances at 9.22% CAGR to 2031.

- By end user, hospitals and clinics held 49.10% share of the medical oxygen gas cylinders market in 2025, while home healthcare posts the strongest CAGR at 10.12% through 2031.

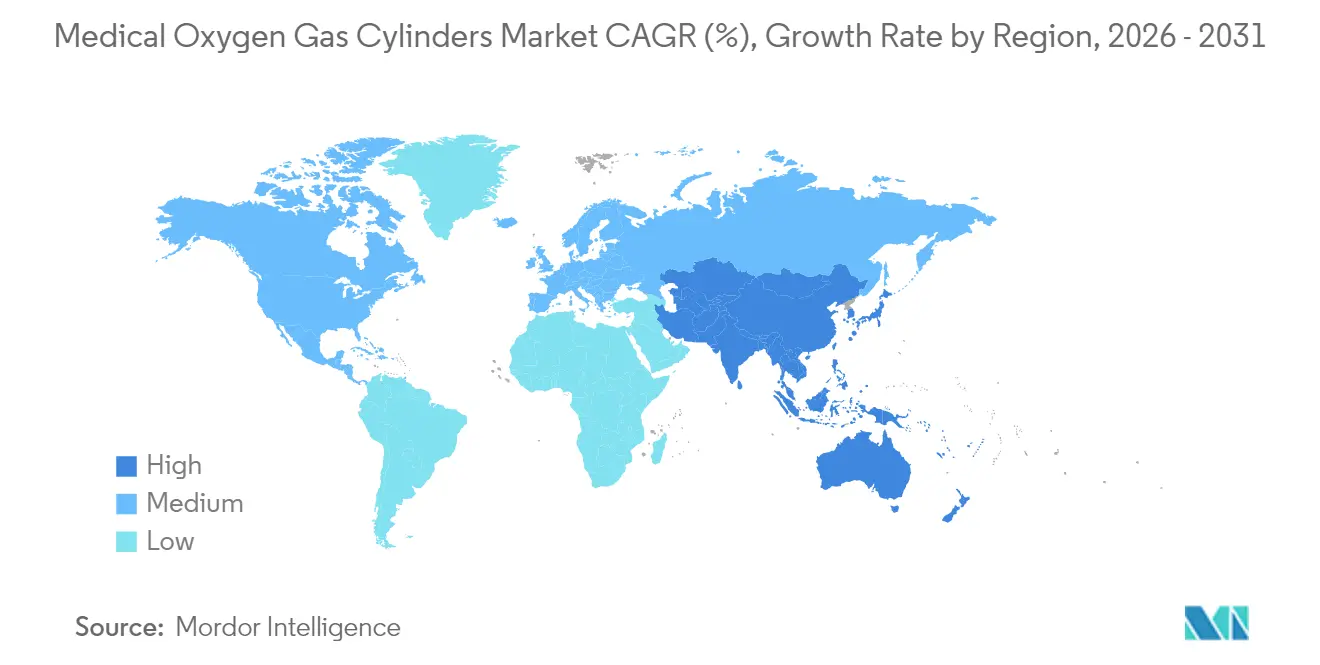

- By geography, North America led with 36.21% revenue share in 2025; Asia–Pacific records the highest forecast CAGR at 9.76% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Oxygen Gas Cylinders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Chronic Respiratory Diseases | +1.2% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Growing Geriatric Population Requiring Long-Term Oxygen Therapy | +1.8% | North America & Europe core, spill-over to APAC | Long term (≥ 4 years) |

| Technological Shift Toward Lightweight Composite & High-Pressure Cylinders | +0.9% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Government-Funded Oxygen Security Programs In LMICs | +1.1% | APAC, MEA, and South America | Medium term (2-4 years) |

| IoT-Enabled Telemetry Improving Refill Logistics & Reducing Leakage | +0.8% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Respiratory Diseases

Chronic obstructive pulmonary disease affects 12.64% of adults aged 40 and older, translating into 213.39 million prevalent cases in 2024. Roughly 85% of COPD deaths occur in low- and middle-income countries where oxygen access remains limited. Reliance on supplemental oxygen intensifies as disease progresses; 68% of idiopathic pulmonary fibrosis patients eventually require oxygen therapy. Smoking and ambient particulate matter together account for the majority of COPD disability-adjusted life years. WHO’s Global Alliance against Chronic Respiratory Diseases now targets nearly 4 million preventable deaths annually, reinforcing the centrality of cylinders to patient survival.

Growing Geriatric Population Requiring Long-Term Oxygen Therapy

The United States counts 57.8 million residents 65 years and older, equal to 17.3% of the population, and the share is projected to rise to 22% by 2040. Roughly 10% of this age group lives with COPD and 15% with coronary heart disease—both conditions demanding oxygen support during flare-ups. Around 1.5 million US adults already use supplemental oxygen at home to maintain quality of life. Lighter cylinders meet mobility preferences that enable independent living, especially for frail seniors. Medicare’s average outlay of USD 65 per patient each month for oxygen therapy underpins stable demand.

Technological Shift Toward Lightweight Composite & High-Pressure Cylinders

Composite Type III and Type IV cylinders lower weight without compromising pressure integrity. Worthington Enterprises agreed to acquire Hexagon Ragasco for USD 98 million in 2024 to integrate advanced composite know-how[1]Worthington Enterprises, “Worthington Enterprises Announces Planned Acquisition of Hexagon Ragasco,” worthingtonenterprises.com. Airgas markets INTELLI-OX+ cylinders featuring built-in gauges that deliver real-time supply visibility. High-pressure designs pack more liters of oxygen into smaller physical footprints, an attribute valued in home healthcare where closet space is scarce. Integrated monitoring cuts waste during patient transfers and supports preventative refill scheduling.

Government-Funded Oxygen Security Programs in LMICs

The Global Oxygen Alliance pledges USD 34 billion over five years to narrow oxygen access gaps for 5 billion people[2]Global Oxygen Alliance, “Global Oxygen Strategic Framework and Investment Case 2025-2030,” globaloxygenalliance.org. Unitaid’s 2024 regional program in sub-Saharan Africa aims to localize oxygen production and distribution. A pilot in Lesotho filled 1,565 cylinders across 21 facilities in 15 months. These initiatives stimulate demand for cylinders manufactured to international quality norms and open new opportunities for suppliers willing to invest in local partnerships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory & Quality-Assurance Requirements | -0.7% | Global, with strictest enforcement in North America & Europe | Short term (≤ 2 years) |

| Uptake Of Oxygen Concentrators & Onsite PSA Plants | -0.6% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Volatile Aluminum & Carbon-Fiber Supply Chains Raising Cylinder Costs | -0.4% | Global, with highest impact on cost-sensitive APAC & MEA markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory & Quality-Assurance Requirements

The FDA’s final rule effective December 2025 tightens current good manufacturing practice, labeling, and post-marketing safety for medical gases. Cylinders now require 360° wraparound labels with color codes specific to oxygen. Alignment with ISO 13485:2016 becomes mandatory as the Quality Management System Regulation takes effect in February 2026. Composite cylinders must be requalified every five years versus ten years for traditional materials, inflating lifecycle costs[3]Ecfr.gov, “49 CFR 180.207 — Requirements for requalification of UN pressure receptacles,” ecfr.gov. Smaller firms face higher compliance hurdles, potentially accelerating consolidation.

Uptake of Oxygen Concentrators & Onsite PSA Plants

Concentrators account for 94% of Medicare oxygen claims, reflecting a clear substitution threat to cylinders in home settings. NASA’s PSA prototype delivers 4 LPM at just 7.2 pounds. Portable concentrators achieve 95% purity using lithium zeolite media. Cost studies in India confirm lower total ownership for institutional concentrator systems than for cylinder supply chains. As concentrator weight drops, cylinder share of home therapy may erode, particularly where reimbursement schemes encourage equipment rental rather than gas delivery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portability Drives Market Evolution

Portable cylinders dominate 60.98% of the medical oxygen gas cylinders market and will expand at 8.17% CAGR to 2031. Growing preference for aging-in-place therapies puts mobility and self-administration at the forefront of purchase decisions. Hospitals still hold stock of stationary cylinders for operating suites and critical care wards because continuous flow reliability remains non-negotiable. Smart valves such as INTELLI-OX+ enable caregivers to track remaining supply and lower accidental runout risk. Medicare’s USD 65 monthly reimbursement keeps cylinder rental viable for providers managing chronic patients. The portable segment’s momentum underlines a larger shift toward outpatient chronic disease management.

In stationary sub-segments, demand persists for backup oxygen in operating rooms, psychiatric units, and emergency departments. Ambulance services carry portable cylinders but rely on centralized hospital supplies for rapid replenishment. Suppliers continue to refine safety features as regulatory standards evolve, creating differentiation on valve integrity, pressure consistency, and telemetry integration. The medical oxygen gas cylinders market therefore balances innovation in portability with institutional obligations for bulk capacity.

By Material: Aluminum Leadership Faces Composite Challenge

Aluminum retains 46.11% share of the medical oxygen gas cylinders market size thanks to its mature supply chain and lower purchase cost. Carbon-fiber composites post the highest 11.64% CAGR as healthcare systems value weight savings that ease lifting injuries among staff and encourage patient adherence. Worthington Enterprises’ Hexagon Ragasco deal highlights the strategic importance of composite capabilities. Steel continues to serve specialist high-pressure needs in military and hyperbaric applications. Composite cylinders must undergo five-year requalification, adding inspection cost yet extending service life through lower wear, a trade-off many hospital administrators accept for weight savings. Material choices therefore reflect a three-way balance among price, durability, and ease of handling.

Composite adoption gains traction in Asia–Pacific where new hospital builds specify modern equipment. Aluminum remains preferred in cost-sensitive facilities needing large cylinder inventories. Suppliers leverage diversified product lines to serve both ends of the spectrum, anticipating gradual share migration to composite as economies of scale reduce unit cost. The medical oxygen gas cylinders market consequently shows progressive but not disruptive material substitution.

By Product Size: Small Cylinders Enable Patient Mobility

Sub-10 liter cylinders account for 44.68% of the medical oxygen gas cylinders market share and post 9.22% CAGR through 2031. Lightweight design aligns with elderly users’ strength limitations. Smaller footprint units slip easily into wheelchairs and rollators, helping users maintain outdoor activities without excessive exertion. Composite construction furthers this objective by shaving off kilograms per cylinder. Mid-size 10–50 liter cylinders remain indispensable in step-down care units requiring longer therapy intervals, while 50+ liter models act as stationary reserve or manifold feeders during peak loads in surgery centers.

Manufacturers achieve higher gas density by optimizing wall thickness through finite-element modeling. IoT sensors track flow rates and humidity, alerting clinicians when consumption deviates from prescription norms. Such enhancements improve adherence, reduce emergency department visits, and contain payer costs. Patients report higher satisfaction when cylinder switchover frequency falls, a benefit that translates into repeat purchases. The medical oxygen gas cylinders market size thus leans toward smaller units that pack more oxygen.

By End User: Healthcare Shift Toward Home-Based Care

Hospitals and clinics held 49.10% share of the medical oxygen gas cylinders market in 2025, yet home healthcare grows fastest at 10.12% CAGR. Chronic disease pathways increasingly push oxygen therapy out of inpatient wards and into living rooms where services cost less and free hospital beds for acute cases. About 1.5 million US patients already manage oxygen at home. Providers ship cylinders along optimized milk-round routes enabled by telemetry, reducing mileage and spoilage. Emergency medical services require ruggedized portable units for ambulance transport and disaster response, while military field hospitals specify shock-resistant casings that meet strict durability tests.

In institutional settings cylinders remain critical redundancy elements even where PSA plants supply base load. Regulatory mandates for minimum reserve stock compel facilities to keep cylinder banks available during plant maintenance or power outages. For home healthcare firms, differentiation comes from nurse education programs helping caregivers handle regulators safely and avoid fire hazards. These nuances shape growth across end-user types and sustain diversified demand within the medical oxygen gas cylinders market.

Geography Analysis

North America records 36.21% revenue share in 2025. Medicare’s consistent USD 65 monthly reimbursement for supplemental oxygen supports recurring cylinder orders. The US population aged 65+ hits 57.8 million, feeding structural demand. FDA regulations effective December 2025 define global practice benchmarks and require new label formats that redirect purchase decisions toward compliant suppliers. Advanced telemetry adoption proceeds fastest in this region given strong digital infrastructure and higher reimbursement for innovative devices.

Asia–Pacific registers the highest 9.76% CAGR. Government-funded oxygen programs channel capital into cylinders as immediate capacity while permanent PSA plants are under construction. The Global Oxygen Alliance’s USD 34 billion plan earmarks large tranches for cylinder procurement. High COPD prevalence due to air pollution in populous economies amplifies need. Regional manufacturers ramp up aluminum extruders and composite winding lines to shorten logistics from foreign suppliers. Multilateral initiatives lift quality standards, ensuring cylinders meet ISO and CGA codes, a shift that favors firms investing early in certification.

Europe delivers steady growth as universal health systems reimburse long-term oxygen therapy. Aging demographics mirror US patterns and spur home care expansions. Regulatory parity with North America through ISO 13485 alignment eases cross-Atlantic supply agreements. Middle East & Africa and South America benefit from development programs such as Unitaid’s sub-Saharan Africa initiative that builds regional cylinder filling hubs. Partners In Health’s Lesotho model proves cylinder networks can serve mountainous terrain quickly. Collectively, these factors broaden the footprint of the medical oxygen gas cylinders market across emerging geographies.

Competitive Landscape

Competition remains moderate with a blend of diversified conglomerates and specialist producers. Luxfer Holdings posted USD 41.1 million in gas cylinder revenue for Q1 2025, a 9% year-over-year dip tied to soft demand in alternate fuels while healthcare volumes stay resilient. Worthington Enterprises’ planned acquisition of Hexagon Ragasco secures composite expertise and augments European market access. Airgas differentiates through smart cylinder technology, embedding valves and gauges that supply analytics to hospital logistics teams.

Smaller entrants focus on niche design features, such as shock-proof casings for EMS fleets or ultra-thin composites for pediatric use. Regulatory tightening favors firms that can absorb compliance costs and maintain robust documentation under FDA CGMP rules. Aluminum price volatility influences profit margins, pushing manufacturers to hedge raw materials and diversify supply chains. Composite resin shortages similarly expose firms with limited supplier bases. Intellectual property around telemetry modules and valve actuation becomes a key competitive lever as hospitals prioritize data integration with electronic medical records. The medical oxygen gas cylinders market thus rewards scale, compliance sophistication, and innovation alignment.

Medical Oxygen Gas Cylinders Industry Leaders

Luxfer Gas Cylinders

Worthington Industries

Faber Industrie S.p.A.

Catalina Cylinders

Tianjin Feitian Gas Cylinder

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The Lancet Global Health Commission reported that more than 5 billion people lack reliable access to medical oxygen and estimated USD 6.8 billion annual investment is needed to close the gap, with sub-Saharan Africa as the most affected region.

- October 2024: Unitaid launched a regional manufacturing initiative in sub-Saharan Africa with partners including Clinton Health Access Initiative to localize oxygen production and improve distribution networks.

Global Medical Oxygen Gas Cylinders Market Report Scope

As per the scope of the report, medical oxygen cylinders contain a high purity of oxygen gas used for medical purposes. The medical oxygen gas cylinders have major use for patients suffering from chronic obstructive pulmonary disease, asthma, cancer, etc. The key purpose of the medical oxygen cylinder is to maintain the supply of pure oxygen in the body.

The medical oxygen gas cylinders market is segmented by Product Type (Portable and Heavy), Product Size (Less than 10 liter, 10 liter - 50 liter, and More than 50 liter), End User (Hospitals, Home Healthcare, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD million for the above segments.

| Portable / Lightweight |

| Stationary / Heavy |

| Aluminum |

| Steel |

| Carbon-fiber composite (Type III/IV) |

| < 10 L |

| 10 - 50 L |

| > 50 L |

| Hospitals & Clinics |

| Home Healthcare |

| Emergency Medical Services / Ambulance |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Portable / Lightweight | |

| Stationary / Heavy | ||

| By Material | Aluminum | |

| Steel | ||

| Carbon-fiber composite (Type III/IV) | ||

| By Product Size | < 10 L | |

| 10 - 50 L | ||

| > 50 L | ||

| By End User | Hospitals & Clinics | |

| Home Healthcare | ||

| Emergency Medical Services / Ambulance | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical oxygen gas cylinders market?

The market is valued at USD 4.93 billion in 2026 and is projected to reach USD 6.39 billion by 2031.

Which cylinder type is most popular?

Portable and lightweight cylinders lead with 60.98% revenue share and grow at 8.17% CAGR owing to home-care adoption.

Why are composite cylinders gaining ground?

Carbon-fiber composites grow at 11.64% CAGR because their lower weight eases handling for elderly patients and staff.

How do regulations affect suppliers?

FDA rules effective December 2025 impose stricter CGMP and labeling, raising compliance costs and favoring large, well-capitalized manufacturers.

Which region shows the fastest market growth?

Asia–Pacific records the highest 9.76% CAGR through 2031 due to large COPD burden and multi-billion-dollar oxygen security programs.

Page last updated on: