United States Magnet Free Electric Axle System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

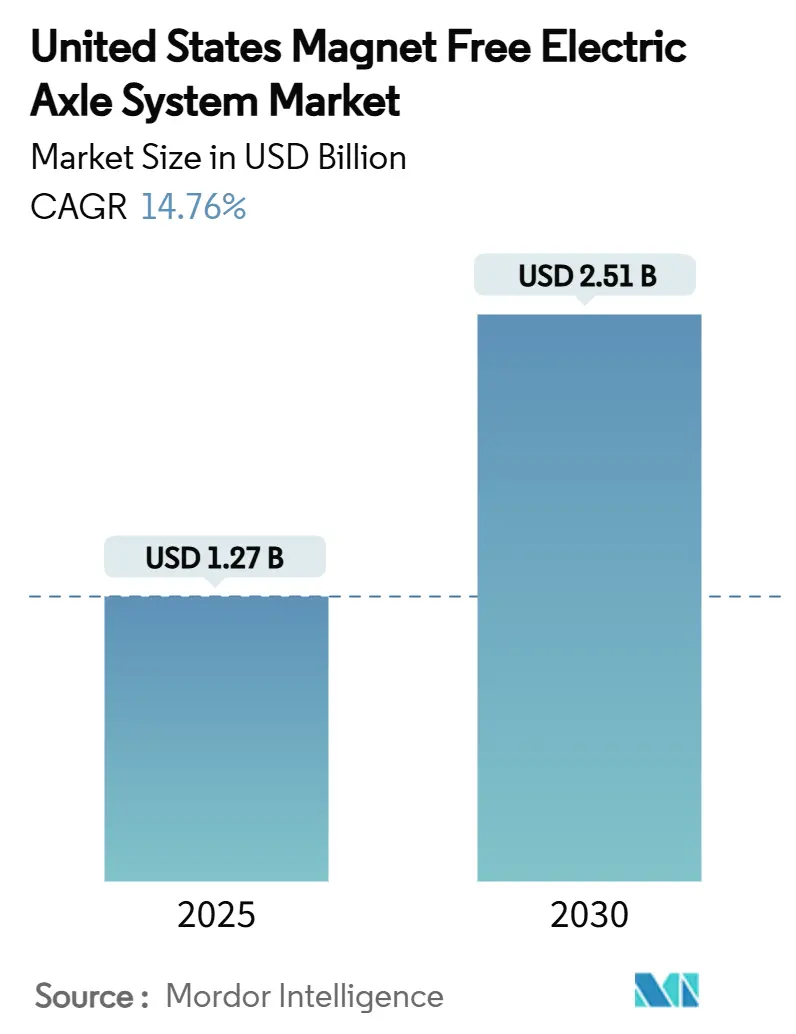

| Market Size (2025) | USD 1.27 Billion |

| Market Size (2030) | USD 2.51 Billion |

| Growth Rate (2025 - 2030) | 14.76% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Magnet Free Electric Axle System Market Analysis by Mordor Intelligence

The United States Magnet Free Electric Axle System market size stands at USD 1.27 billion in 2025 and is projected to reach USD 2.51 billion by 2030, reflecting a 14.76% CAGR through the forecast period. Strong policy tailwinds from the Inflation Reduction Act, expanding Department of Defense funding, and accelerating OEM moves away from rare-earth dependence form the core growth catalysts. Induction motor cost leadership, rising torque-density breakthroughs in externally excited synchronous motors (EESM), and integrated e-axle architectures are lowering ownership costs fast enough to offset modest efficiency penalties versus interior permanent-magnet (IPM) designs. Tier-1 suppliers are entering a heavy retooling phase, and the United States capacity additions in non-grain-oriented (NGO) electrical steel and wire-rod copper aim to relieve lamination and winding bottlenecks even as 50% copper tariffs complicate near-term sourcing. Competitive intensity is moderate, with top suppliers racing to lock OEM awards before Section 45X credits step down after 2030.

Key Report Takeaways

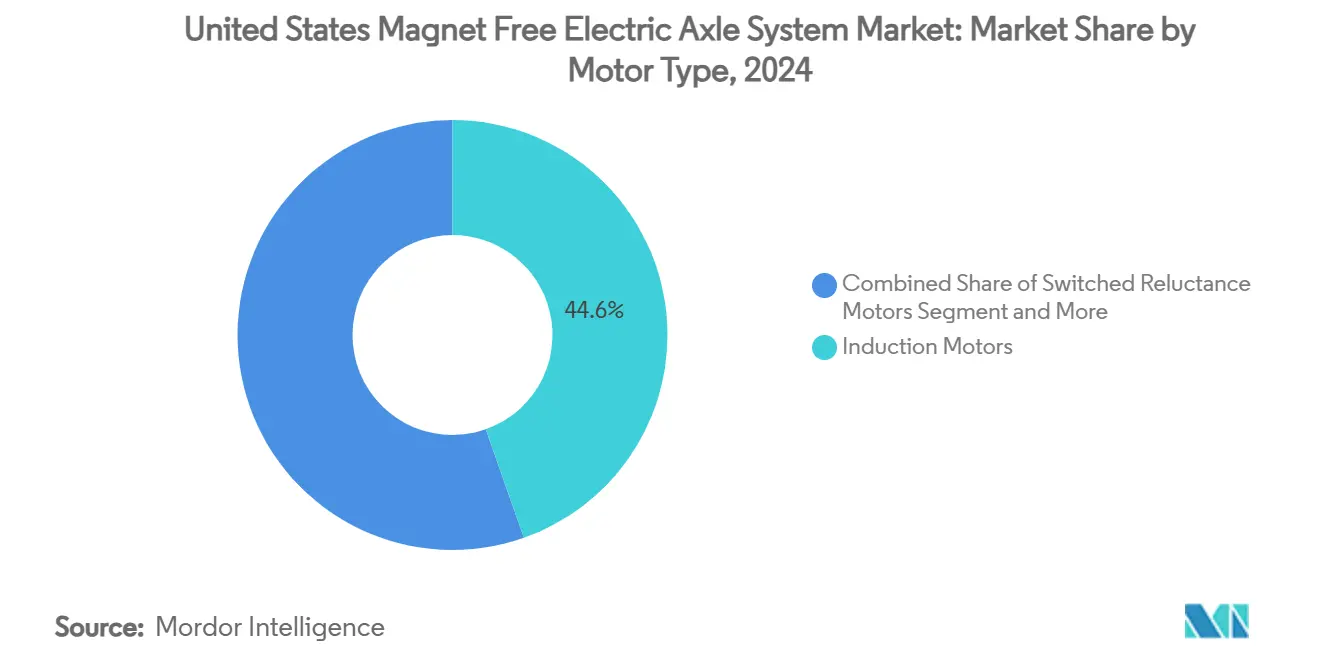

- By motor type, induction motors led with 44.56% of the United States Magnet Free Electric Axle System market share in 2024, while externally excited synchronous motors are advancing at a 19.42% CAGR through 2030.

- By drive type, fully electric systems captured a 61.28% share of the United States Magnet Free Electric Axle System market size in 2024 and are expanding at a 24.07% CAGR through 2030.

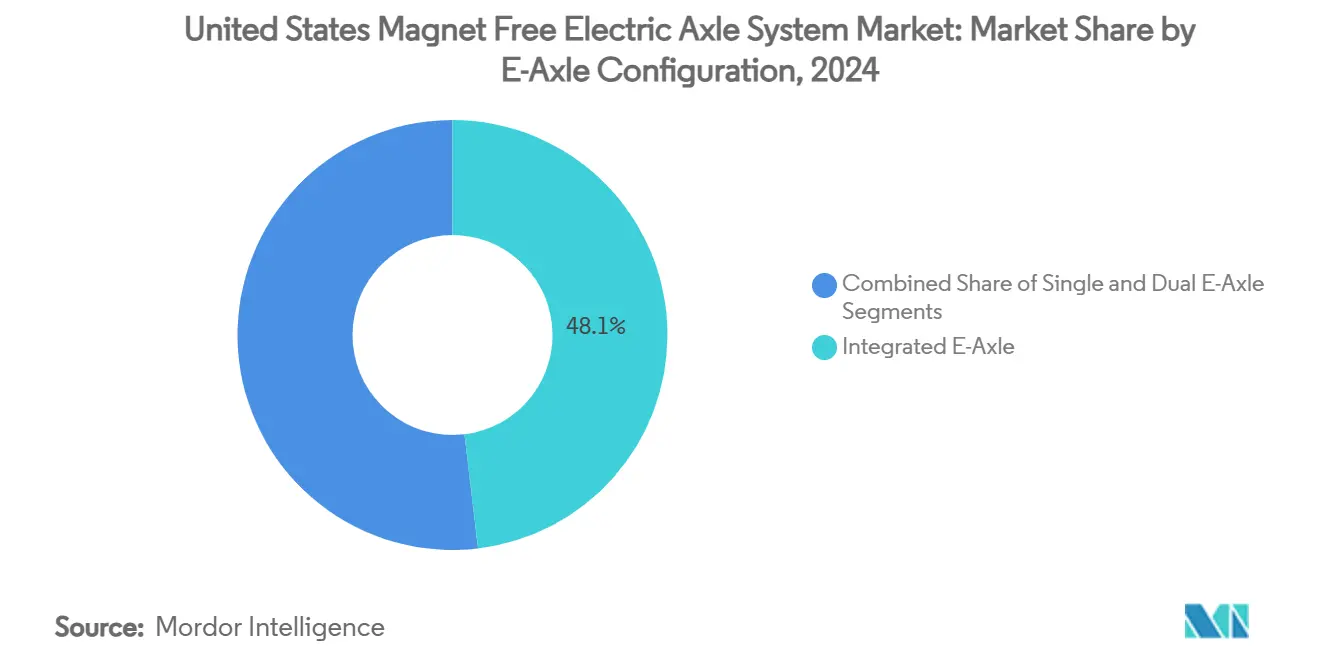

- By e-axle configuration, integrated e-axle units accounted for 48.13% share of the United States Magnet Free Electric Axle System market size in 2024, growing at a 22.14% CAGR to 2030.

- By vehicle type, SUVs and MUVs secured 32.21% of the United States Magnet Free Electric Axle System market share in 2024 and are growing at an 18.03% CAGR through 2030.

Competitive positioning in United states includes both locally based firms and those operating across multiple regions. The market landscape in the global magnet free electric axle system industry research shows how these players are arranged internationally.

United States Magnet Free Electric Axle System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRA Credits Boost E-Axle Production | +3.2% | United States | Short term (≤ 2 years) |

| OEM Push to Cut Rare-Earth Volatility | +2.8% | United States | Medium term (2-4 years) |

| Torque-Density Gains in EESM & SRM | +2.1% | United States | Medium term (2-4 years) |

| DOE Funds Non-Rare-Earth Motors | +1.9% | United States | Long term (≥ 4 years) |

| Defense Mandates Non-Rare-Earth Powertrains | +1.4% | United States | Long term (≥ 4 years) |

| Copper-Coil Costs Drop on Wire-Rod Glut | +1.2% | United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IRA Tax Credits Accelerating Domestic E-Axle Production

The Section 45X production tax credit creates unprecedented financial incentives for domestic magnet-free e-axle manufacturing, with credits covering essential components from motor stators to power electronics assemblies. This policy framework has triggered over USD 92 billion in announced battery-related manufacturing investments, with electric axle components benefiting from the same domestic content requirements. The credit structure particularly favors magnet-free technologies by eliminating foreign entity of concern restrictions that plague rare earth supply chains, enabling companies like American Axle & Manufacturing to secure USD 20 billion in lifetime revenues through 2030 with 50% related to electrification[1]"AAM Announces Successful Syndication Financing and Amendment to Credit Agreement,"aam.com.. However, the recent "Big Beautiful Bill" threatens to terminate the USD 7,500 clean vehicle credit by September 2025, potentially reducing EV sales by 42% and creating downstream pressure on e-axle demand. The credit's phase-down schedule through 2033 creates a narrow window for manufacturers to establish competitive cost structures before subsidy expiration. Companies like BorgWarner, reporting 47% year-over-year increase in light vehicle eProduct sales, demonstrate how tax credit optimization drives near-term capacity investments.

OEM Drive to Eliminate Rare-Earth Price Volatility

Automotive manufacturers face critical supply chain vulnerabilities as China's export restrictions on heavy rare earth metals create pricing volatility that can swing 30-40% within quarterly periods, forcing strategic pivots toward magnet-free architectures. The Department of Defense's mine-to-magnet supply chain initiative, investing over USD 439 million since 2020, reflects similar concerns about rare earth dependencies that extend beyond military applications into commercial vehicle electrification. ZF Friedrichshafen's I2SM motor development, achieving 96% efficiency without rare earth materials, demonstrates how OEMs can maintain performance while eliminating supply chain risks[2] Glenn Zorpette, "German EV Motor Could Break Supply-Chain Deadlock," IEE, spectrum.ieee.org.. General Motors' axial flux motor patent applications signal broader industry movement toward alternative magnetic architectures that reduce rare earth content by up to 80%. The volatility extends beyond pricing to availability, with dysprosium oxide becoming increasingly critical for high-temperature motor applications yet subject to export quotas that can shift without warning. Tesla's announced plans for rare earth-free drive units represent the most significant OEM commitment to magnet-free technologies, potentially catalyzing industry-wide adoption through demonstration of commercial viability at scale.

Rapid Torque-Density Gains in EESM and SRM Designs

Externally Excited Synchronous Motors and Switched Reluctance Motors are achieving breakthrough torque density improvements through advanced rotor topologies and electromagnetic optimization, with recent designs reaching power densities exceeding 5 kW/kg compared to 3-4 kW/kg in traditional configurations. IEEE research demonstrates that EESM designs with optimized Joule loss minimization control can achieve efficiency levels within 2-3 percentage points of Interior Permanent Magnet motors while eliminating rare earth dependencies. The development of connected C-Core hybrid SRM configurations shows torque density improvements of 18.14% over conventional designs, with experimental validation confirming 94.86% efficiency in prototype testing. Switched reluctance motor innovations focus on torque ripple reduction, with direct instantaneous torque control methods achieving over 30% ripple reduction while maintaining efficiency. Advanced thermal management through oil spray cooling systems enables higher power density operation by maintaining optimal temperatures during peak torque delivery, with multi-nozzle configurations achieving 20.3% performance improvements over traditional water jacket cooling. The torque density gains create new application possibilities in commercial vehicle segments where weight and space constraints previously favored permanent magnet solutions.

DOE R&D Funding for Beyond-Rare-Earth-Magnet Motors

The Department of Energy's Beyond-Rare-Earth-Magnet initiative represents a USD 88 million commitment to developing alternative motor technologies, explicitly focusing on iron-nitride permanent magnets and advanced reluctance motor designs that match or exceed rare-earth motor performance. The Vehicle Technologies Office's 2025 funding announcement targets ultra-long-cycle life batteries and thermal technologies for zero-emission vehicles, creating synergies with magnet-free motor development through integrated powertrain optimization. Critical Materials Accelerator funding selections include CorePower Magnetics' development of rare-earth element-free axial flux motors using nanocrystalline soft magnets, with USD 4 million in federal support for prototype development. The Biden-Harris Administration's USD 5.5 million investment in CorePower Magnetics targets rare-earth-free electric motor development, demonstrating federal commitment to supply chain independence. Research partnerships with Oak Ridge National Laboratory and the National Renewable Energy Laboratory focus on non-permanent magnet designs and improved thermal management, with goals of 50% motor cost reduction by 2030[3]"Electric Motors Research and Development," US Department of Energy, .energy.gov.. The funding timeline extends through 2027, providing sustained support for technology maturation and commercial demonstration phases.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficiency Gap vs. Latest IPM Motors | -2.4% | United States | Medium term (2-4 years) |

| High Up-Front Re-Tooling CAPEX for Tier-1s | -1.8% | United States | Short term (≤ 2 years) |

| Rotor Heat-Dissipation Limits in High-Power SRM | -1.5% | United States | Medium term (2-4 years) |

| Limited Domestic Precision-Lamination Supply Base | -1.2% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Efficiency Gap vs. Latest IPM Motors

Magnet-free electric axle systems typically operate at 92-94% efficiency compared to 96-98% for latest Interior Permanent Magnet motors, creating a 2-4 percentage point performance penalty that directly impacts vehicle range and energy consumption. This efficiency differential becomes particularly pronounced in high-speed applications where electromagnetic losses in reluctance-based designs increase quadratically with rotational velocity, limiting their effectiveness in highway driving scenarios. Advanced thermal analysis reveals that induction motors experience greater heating compared to SRM and IPM motors during continuous operation, requiring more sophisticated cooling systems that add weight and complexity. However, recent innovations in oil spray cooling and thermal management are narrowing this gap, with combined spray cooling systems achieving 96.84% efficiency in laboratory testing. The efficiency penalty translates to approximately 8-12% reduction in driving range for equivalent battery capacity, creating consumer acceptance challenges that OEMs must address through larger battery packs or improved aerodynamics. Companies like Magna International are addressing this challenge through 800-volt architectures and advanced cooling techniques, achieving 93% efficiency in their latest e-drive motors while reducing rare earth material usage by 5%.

High Up-Front Re-Tooling CAPEX for Tier-1 Suppliers

Traditional automotive suppliers face substantial capital expenditure requirements ranging from USD 200-400 million per facility to transition from permanent magnet motor production to magnet-free architectures, creating financial barriers that constrain market entry and expansion rates. Dana Incorporated announced USD 300 million in cost reduction savings, highlighting the magnitude of operational restructuring required for competitive positioning in magnet-free technologies. The retooling challenge extends beyond manufacturing equipment, including specialized testing facilities for electromagnetic compatibility and thermal validation, with precision lamination processing requiring investments in advanced stamping and assembly technologies. Schaeffler's USD 230 million investment in the Dover, Ohio, facility demonstrates the scale of capital commitment needed for competitive magnet-free e-axle production, with 650 new jobs and specialized equipment for electric beam axle manufacturing. Smaller Tier-1 suppliers face particular challenges in securing financing for these investments, with many opting for joint ventures or licensing agreements rather than independent development. The capital intensity creates consolidation pressure within the supply base, favoring larger suppliers with stronger balance sheets and established OEM relationships, potentially reducing competitive diversity in the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Induction Scale vs. EESM Momentum

Due to a deep supplier base and rugged construction, induction machines held 44.56% of the United States Magnet Free Electric Axle System market share in 2024. This dominance persists in commercial vans, where the total cost of ownership trumps absolute efficiency. The United States Magnet Free Electric Axle System market size booked a 19.42% CAGR for EESM through 2030 as OEMs exploit brush-free excitation and high torque density. Switched reluctance motors remain a niche technology but are gaining traction due to advanced torque-ripple control techniques that significantly improve performance.

Increased government grants and defense investments are directing resources toward EESM coil-optimization projects, enabling more compact and efficient designs. Inductively excited synchronous motor solutions have demonstrated strong commercial viability for premium electric vehicles, offering high efficiency without brushes. As a result, the U.S. market for magnet-free electric axle systems is increasingly reallocating R&D budgets toward EESM platforms, which deliver rare-earth independence without significant efficiency trade-offs.

By Drive Type: Fully Electric Platforms Dominate

Fully electric architectures contributed 61.28% of the United States Magnet Free Electric Axle System market size in 2024, expanding at 24.07% CAGR as battery prices fall and 800-V inverters improve drive-cycle efficiency. OEMs prefer magnet-free setups in last-mile delivery vans with intense regenerative duty cycles, and motor heating is manageable. Hybrid and plug-in hybrid drives collectively trail but persist in heavy-duty vocational trucks where battery mass constraints remain critical.

Major suppliers, including American Axle & Manufacturing and Cummins’s Meritor division, are expanding their capacities in response to a surge in purchases of fully electric axles. This shift is largely driven by tax credit incentives favoring domestic content. Spray-cooled induction e-axles, known for their robust efficiency and durability, are ideal for challenging applications, such as long-grade routes. As the national grid infrastructure progresses, the United States market for magnet-free electric axle systems is increasingly investing in pure-battery platforms.

By E-Axle Configuration: Integration Builds Momentum

Integrated e-axles had a 48.13% share of the United States Magnet Free Electric Axle System market size in 2024. They will post a 22.14% CAGR through 2030 as suppliers fuse motor, gearbox, and inverter to shrink packaging and simplify cooling. Unified housings allow oil commonality for gears and stators, cutting thermal gradients that plagued early induction prototypes. Single-axle layouts prevail in budget crossovers, whereas dual-motor all-wheel-drive systems target performance EVs yet still face cost hurdles absent economies of scale.

ZF's EVSys800 showcases the industry's pivot towards sophisticated e-axle systems. It boasts high-voltage operations, braided windings, and integrated oil-cooling loops, all accomplished without rare-earth magnets. Meanwhile, Magna pushes the envelope further by incorporating control ASICs directly within the e-axle. This move not only simplifies wiring but also bolsters reliability. Such engineering strides propel the United States market's transition to entirely integrated, magnet-free electric axle assemblies, promising cost savings and superior thermal performance.

By Vehicle Type: SUV Leadership Continues

SUVs and MUVs delivered 32.21% United States Magnet Free Electric Axle System market share in 2024, rising at an 18.03% CAGR as buyers gravitate to larger BEVs with more packaging headroom for cooling jackets. Weight tolerance in this segment softens the energy-density penalty of magnet-free motors, letting OEMs prioritize secure supply chains. Passenger sedans remain price sensitive, tilting decisions toward induction machines where copper price hedges counter tariff uncertainty.

Commercial vans and buses increasingly specify switched-reluctance drives, thanks to their low maintenance and fault-tolerant operation, which is valuable for fleet uptime. Cummins’s demonstration e-Powertrain logged 400,000 mi on a parcel-delivery route with less than 1% uptime loss. Consequently, the United States Magnet Free Electric Axle System market registers strong pull from lifestyle SUVs and high-duty-cycle fleet applications.

Geography Analysis

Federal incentives position the United States as the undisputed demand center for magnet-free e-axles through 2030. Section 45X reimburses up to USD 35 per kilowatt-hour of qualifying components, tilting global supply chains toward the United States' final assembly. Defense mandates inject a further USD 439 million of directed R&D to guarantee rare-earth independence in tactical fleets. These levers anchor the United States Magnet Free Electric Axle System market ahead of Canadian and Mexican manufacturing corridors.

Regional industry clusters emerge along the Midwest-South corridor, pairing NGO electrical-steel mills in Arkansas with winding and inverter plants in Ohio and Michigan. U.S. Steel’s Big River mill doubled NGO slab output in 2025, cutting lamination lead times by 40%. Copper tariffs raise input costs but catalyze new smelting capacity in Arizona, promising long-run coil cost stability despite near-term volatility.

However, policy risk looms: the proposed 2025 sunset of the USD 7,500 clean-vehicle credit threatens a 42% drop in EV uptake, which would reverberate across e-axle demand. Suppliers hedge by expanding export programs to Europe and Japan, where rare-earth anxiety also pushes magnet-free adoption but without equivalent fiscal support.

Mordor Intelligence tracks the magnet free electric axle system market across other major regions such as Europe, with additional country-level coverage spanning China, Japan, India, and South Korea, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Market fragmentation prevails because no single supplier dominates the market. BorgWarner, Dana, American Axle & Manufacturing, Schaeffler, and ZF comprise the leading cohort, each investing heavily annually in retooling.

Strategic moves spotlight vertical integration. Schaeffler merged with Vitesco Technologies to pool power electronics, while Cummins completed the Meritor acquisition, sealing captive inverter and brake-by-wire expertise. Start-ups add disruptive pressure: Niron Magnetics scales iron-nitride magnets for small motors, while Conifer raised USD 20 million for magnet-agnostic e-powertrains.

Patent publications surged to a substantial share year-on-year, centered on rotor topology and spray-cooled stator channels. Litigation risk remains low because open academic collaboration through DOE contracts fosters cross-licensing. Consequently, the United States Magnet Free Electric Axle System market exhibits mid-level concentration but high technological churn, rewarding players who can fast-track design wins with domestic content compliance.

United States Magnet Free Electric Axle System Industry Leaders

-

BorgWarner

-

ZF Friedrichshafen

-

American Axle & Manufacturing

-

Magna International

-

Dana Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ricardo completed the development of the Alumotor prototype, a rare-earth and copper-free electric propulsion motor that achieves 214 kW power output with over 92% efficiency through aluminum hairpin windings and oil cooling technology. The Innovate UK-funded project addresses the environmental impacts of critical raw materials while demonstrating scalability for light commercial vehicle applications.

- January 2025: Niron Magnetics showcased Clean Earth Magnets made from iron nitride, achieving 2.4 teslas of magnetic strength, surpassing neodymium magnets while producing 80% less CO2 emissions and reducing water usage. The company is transitioning to ton-scale production, with the facility expected to be operational by 2026. It targets electric vehicle and wind energy applications with domestic iron-salt waste and renewable energy-sourced nitrogen.

United States Magnet Free Electric Axle System Market Report Scope

| Externally Excited Synchronous Motors |

| Induction Motors |

| Switched Reluctance Motors |

| Fully Electric Drive |

| Hybrid Drive |

| Plug-in Hybrid Drive |

| Single E-Axle |

| Dual E-Axle |

| Integrated E-Axle |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| By Motor Type | Externally Excited Synchronous Motors | |

| Induction Motors | ||

| Switched Reluctance Motors | ||

| By Drive Type | Fully Electric Drive | |

| Hybrid Drive | ||

| Plug-in Hybrid Drive | ||

| By E-Axle Configuration | Single E-Axle | |

| Dual E-Axle | ||

| Integrated E-Axle | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUV and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

Key Questions Answered in the Report

What is the current value of the United States Magnet Free Electric Axle System market?

The market is valued at USD 1.27 billion in 2025.

How fast is demand for magnet-free e-axles growing?

Market revenue is forecast to rise at a 14.76% CAGR to reach USD 2.51 billion by 2030.

Which motor type leads sales today?

Induction motors hold 44.56% market share on the back of mature supply chains and low cost.

Why are OEMs moving away from rare-earth magnets?

Price volatility, export restrictions, and Section 45X credits make magnet-free designs more resilient and financially attractive.

What policy supports exist for U.S. production?

Inflation Reduction Act Section 45X production credits reimburse domestic content and run through 2033.

Which vehicle segment shows the highest uptake?

SUVs and MUVs account for about one-third of 2024 demand and are growing at an 18.03% CAGR.

Page last updated on: