Europe Magnet Free Electric Axle System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

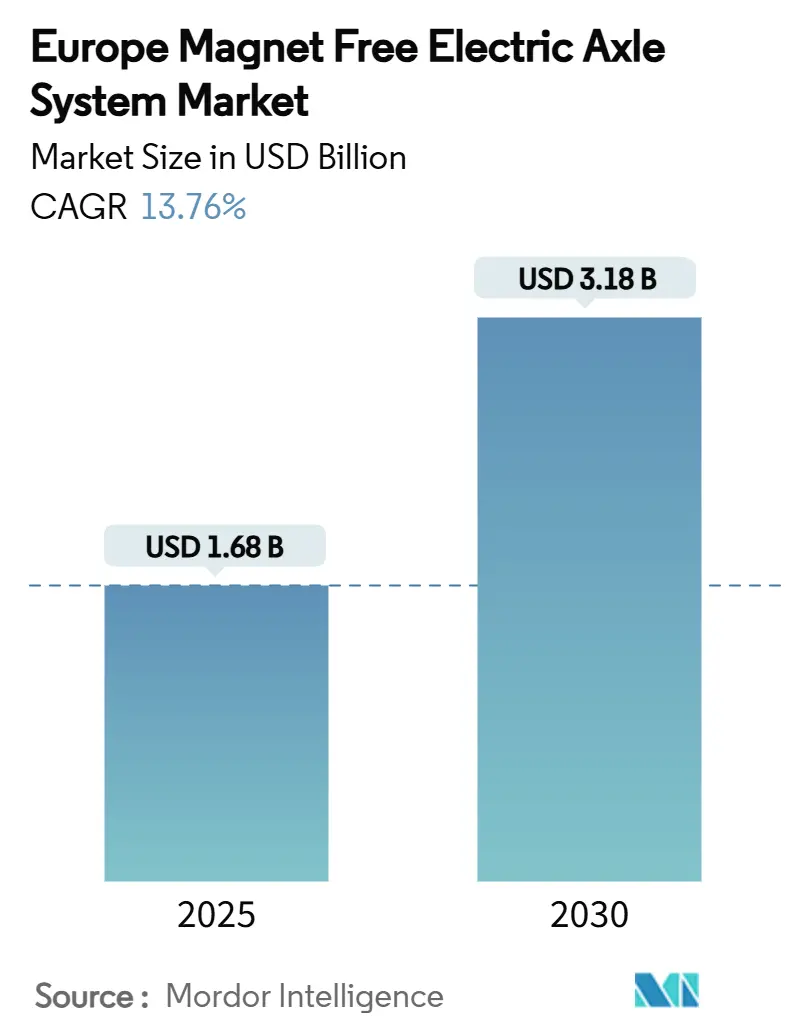

| Market Size (2025) | USD 1.68 Billion |

| Market Size (2030) | USD 3.18 Billion |

| Growth Rate (2025 - 2030) | 13.76% CAGR |

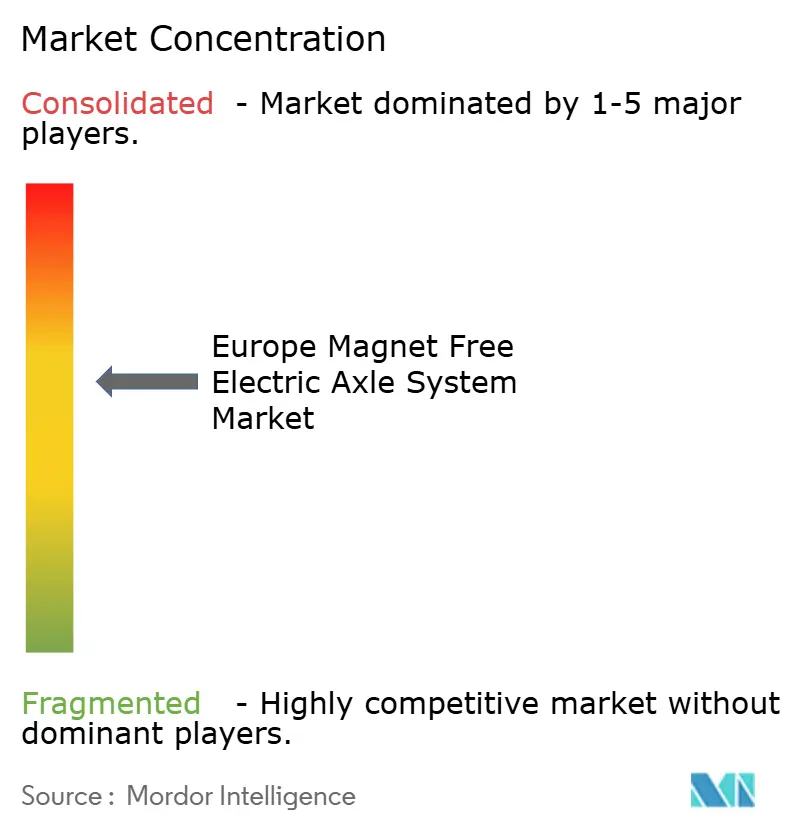

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Magnet Free Electric Axle System Market Analysis by Mordor Intelligence

The Europe Magnet Free Electric Axle System market size stood at USD 1.68 billion in 2025 and is projected to reach USD 3.18 billion by 2030, translating into a CAGR of 13.76% over the forecast window. Demand climbs as automakers seek supply-chain security from rare-earth risk, leverage 800 V silicon-carbide (SiC) architectures, and comply with the European Union’s post-2025 CO₂ caps. Integrated e-axles compress weight and packaging, while high-voltage SiC inverters narrow efficiency gaps with permanent-magnet drives. Spain’s rapid-charge roll-out, Germany’s semiconductor investments, and city-level zero-emission zones amplify adoption in both passenger and commercial fleets. Competitive intensity rises as incumbents and start-ups race to patent thermal-management breakthroughs that push wound-rotor power densities toward 30 kW/kg.

Key Report Takeaways

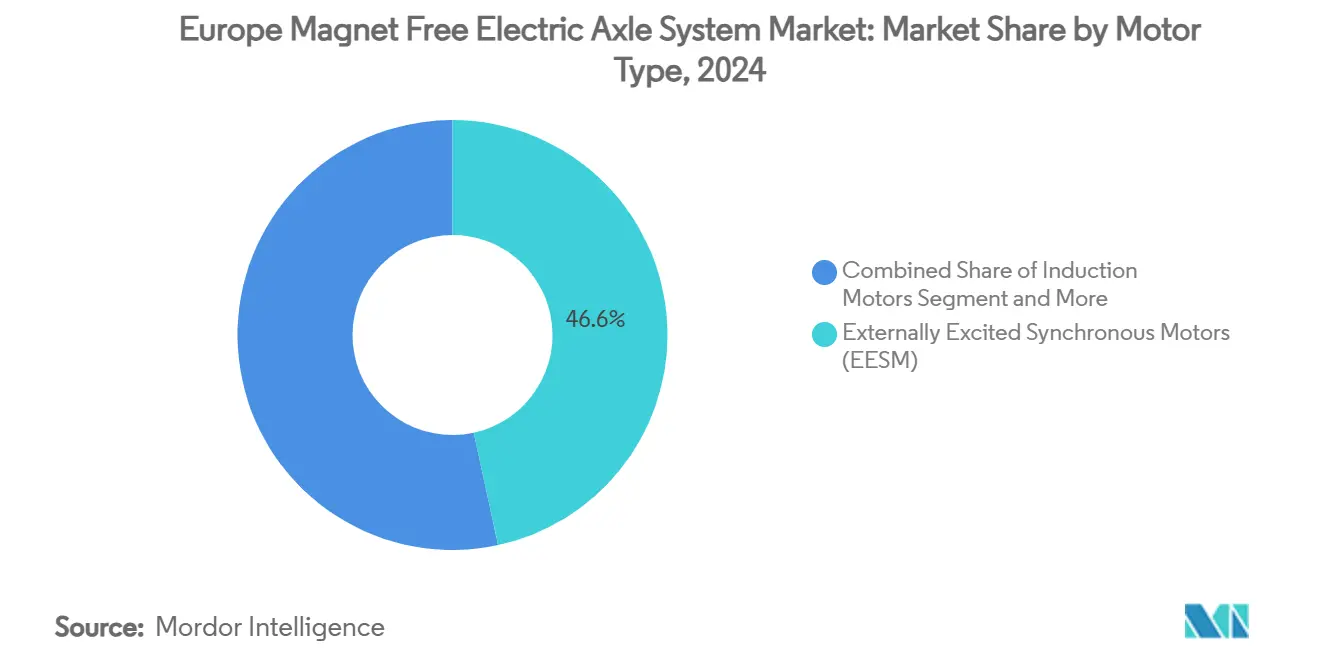

- By motor type, externally excited synchronous motors held 46.56% of the Europe Magnet Free Electric Axle System market share in 2024, whereas switched reluctance motors recorded the fastest 18.42% CAGR through 2030.

- By drive type, fully electric captured 63.28% of the Europe Magnet Free Electric Axle System market size in 2024 and is advancing at a 24.07% CAGR to 2030.

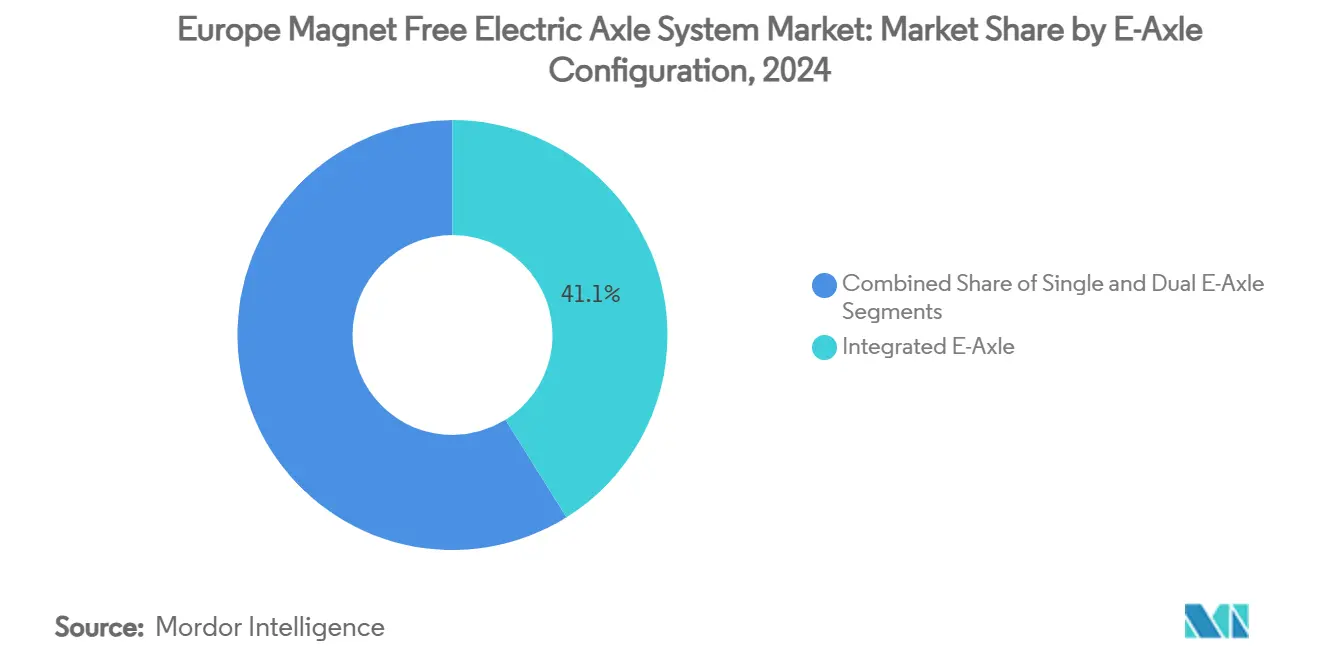

- By e-axle configuration, integrated layouts accounted for 41.13% of 2024 revenue while expanding at a 19.54% CAGR through 2030.

- By vehicle type, passenger cars led with 57.21% revenue share in 2024, while buses and coaches posted the highest 17.03% CAGR between 2025 and 2030.

- By geography, Germany commanded 32.47% of 2024 sales; Spain delivered the swiftest 15.19% CAGR on the back of the EUR 400 million MOVES III extension.

Proportional positioning is established by comparing regional contributions against the global total, including that of Europe. The magnet free electric axle system market share in our global report expresses these relative weights.

Europe Magnet Free Electric Axle System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EU CO₂ Mandates | +3.2% | EU-27 with strongest impact in Germany, France, Netherlands | Medium term (2-4 years) |

| OEM Strategy Shift | +2.8% | Global with primary focus on Germany, UK, France | Long term (≥ 4 years) |

| Battery Cost Parity | +2.1% | EU-27 with early adoption in Nordic countries, Netherlands | Short term (≤ 2 years) |

| Fleet TCO Advantage | +1.9% | Germany, UK, Spain with commercial vehicle concentration | Medium term (2-4 years) |

| High-Voltage SiC Inverters | +1.7% | Germany, France, Italy with semiconductor manufacturing base | Medium term (2-4 years) |

| Joint IP Innovations | +1.5% | Germany, France with automotive R&D clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-led CO₂-cut Mandates Across EU-27 Tighten Post-2025

European Union's escalating emissions regulations create an inflection point for magnet-free e-axle adoption as automakers face EUR 95 per gram CO₂ penalties above 2025 targets. The regulatory framework's 55% emissions reduction mandate by 2030 compels manufacturers to prioritize supply chain-resilient propulsion technologies over performance-optimized permanent magnet systems. Fleet electrification mandates in major European cities accelerate commercial vehicle adoption, with London's Ultra Low Emission Zone expansion driving 35% growth in electric commercial vehicle registrations during 2024. The regulatory cascade effect extends beyond passenger vehicles. The EU's proposed Euro VII standards target heavy-duty vehicles, creating downstream demand for magnet-free e-axles in buses and trucks where supply chain security outweighs marginal efficiency gains.

OEM Shift to Rare-Earth-Free Motors to De-Risk China Supply Chain

China's 60% control of global rare earth processing capacity drives European automakers toward magnet-free motor architectures as geopolitical tensions intensify supply chain vulnerabilities. Renault Group, Valeo, and Valeo Siemens eAutomotive formed a strategic partnership through a memorandum of understanding to design, develop, and manufacture a new automotive electric motor in France. The motor will operate without rare earth materials. The collaboration aims to begin mass production of a 200kW electric motor in 2027, marking the first such initiative in the automotive industry[1]"Renault Group, Valeo and Valeo Siemens eAutomotive join forces to develop and manufacture a new-generation automotive electric motor in France,"renaultgroup.com.. BMW's announcement of 800V SiC-based drive systems for its Neue Klasse platform exemplifies this transition, emphasizing supply chain resilience over peak power density[2]"BMW reveals revolutionary electric drive concept with 800V technology for the Neue Klasse," press.bmwgroup.com..

Battery Cost Parity Accelerates Demand for Fully-Electric E-Axles

Battery prices declined in 2023 after significantly increasing in 2022. According to a study, lithium-ion battery pack prices decreased by 14% to reach $139/kWh, the lowest recorded level. This cost convergence enables automakers to optimize for manufacturing efficiency rather than fuel economy compromises, with Mercedes-Benz's EDU 2.0 achieving 93% battery-to-wheel efficiency through integrated thermal management[3]"The Next Level of Efficiency Becomes Reality," media.mbusa.com.. The economic shift particularly benefits commercial vehicle operators, where total cost of ownership models favor integrated e-axles over dual-motor configurations. European charging infrastructure expansion supports this transition, with Spain reporting significant growth in rapid charging points during 2024, reducing range anxiety that previously justified hybrid systems. Fleet operators increasingly recognize that fully-electric configurations eliminate maintenance complexity associated with internal combustion engine components while providing superior torque characteristics for urban delivery applications.

Fleet-Operator TCO Models Favor Integrated E-Axles

Commercial fleet operators' adoption of sophisticated total cost of ownership analytics reveals integrated e-axle systems' operational cost advantages over distributed motor configurations. The economic benefits stem from reduced cabling complexity, simplified thermal management, and consolidated maintenance requirements that particularly benefit high-utilization commercial vehicles. European logistics companies report maintenance cost reductions of EUR 0.08 per kilometer for integrated e-axle systems compared to dual-motor setups, with Hyundai WIA's integrated thermal management module demonstrating fewer components than traditional architectures. The TCO advantage amplifies in urban delivery applications where stop-start driving patterns stress distributed systems more severely than integrated configurations. Fleet electrification accelerates as operators recognize that integrated e-axles enable vehicle platform standardization across different payload requirements, reducing inventory complexity and driver training costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stator Copper Price Volatility Inflates BOM Cost | -1.8% | Global with manufacturing concentration in Germany, Italy | Short term (≤ 2 years) |

| Limited Field Experience with SRM Acoustic NVH in Europe Buses | -1.2% | Germany, UK, Netherlands with established bus fleets | Medium term (2-4 years) |

| Standards Gap for EESM Rotor Insulation Longevity | -0.9% | EU-27 with regulatory focus in Germany, France | Long term (≥ 4 years) |

| Scarcity of EU-Scale Laminations Stamping Capacity | -0.7% | Germany, Italy, France with automotive manufacturing base | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stator Copper Price Volatility Inflates BOM Cost

Copper price volatility reaching USD 5.20 per pound in May 2024 creates significant bill-of-materials pressure for magnet-free motors that utilize 3x more copper than permanent magnet alternatives. The commodity price surge increases manufacturing costs for building wire applications, with similar impacts expected on motor windings, representing a considerable share of total e-axle system costs. European automakers face particular exposure as electric vehicles require 70% more copper than internal combustion engines, with demand projected to increase 70% by 2050. The cost volatility disproportionately affects switched reluctance motors, where permanent magnet cost reductions cannot offset copper-intensive stator windings. Supply chain hedging strategies become critical as automakers balance inventory costs against price volatility, with some manufacturers exploring aluminum conductor alternatives despite performance compromises.

Limited Field Experience with SRM Acoustic NVH in Europe Buses

Switched reluctance motors' inherent torque ripple and acoustic signature create adoption barriers in European commercial vehicle applications where noise regulations and passenger comfort standards exceed global benchmarks. The technology's noteworthy growth potential faces headwinds from limited field validation in European bus fleets, where acoustic performance directly impacts regulatory compliance and operator acceptance. Technical solutions, including advanced control algorithms and structural modifications, show promise, with research demonstrating 15-20 dB noise reduction through optimized switching patterns. However, fleet operators remain cautious about large-scale deployment without extensive field validation, particularly in urban environments where noise ordinances restrict commercial vehicle operation. The acoustic challenge proves most acute in overnight charging applications where SRM motor noise can violate residential area sound limits, requiring additional acoustic shielding that increases system cost and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: EESM Dominance Faces SRM Disruption

Externally excited synchronous motors (EESM) captured 46.56% of the market in 2024, leveraging established automotive supplier expertise and proven thermal management solutions. However, switched reluctance motors (SRM) emerged as the fastest-growing segment at 18.42% CAGR through 2030, driven by their rare-earth independence and simplified manufacturing requirements. Induction motors maintain steady adoption in cost-sensitive applications, while permanent magnet motors face declining market share as automakers prioritize supply chain resilience over peak efficiency.

The motor type landscape reflects European automakers' strategic pivot toward supply chain independence, with ZF's I2SM (Interior-permanent-magnet Synchronous Motor) technology winning the CLEPA Innovation Award in December 2024 for achieving permanent magnet-level performance without rare earth materials. Ricardo's completion of the Alumotor development in April 2025 demonstrates the feasibility of rare-earth and copper-free motor architectures, though commercial viability remains limited to niche applications. The segment evolution accelerates through joint development programs, with Valeo and MAHLE's iBEE technology targeting 200kW output by 2027 while eliminating permanent magnet dependencies.

By Drive Type: Fully Electric Systems Dominate Growth

Battery cost parity fundamentally reshapes drive type preferences, with fully electric systems commanding 63.28% market share in 2024 while simultaneously achieving the highest growth rate of 24.07% CAGR through 2030. This dual leadership reflects fleet operators' recognition that simplified drivetrains reduce maintenance complexity and total cost of ownership compared to hybrid configurations. Hybrid drive systems face declining relevance as battery energy density improvements eliminate range anxiety, while plug-in hybrid configurations occupy a shrinking middle ground between full electrification and internal combustion engines.

The drive type convergence toward fully electric systems gains momentum through infrastructure investments, with Spain's 60.86% rapid charging network expansion in 2024 reducing the economic justification for hybrid complexity. Mercedes-Benz's EDU 2.0 architecture exemplifies this transition, achieving 93% battery-to-wheel efficiency through integrated thermal management that eliminates the need for hybrid system compromises. Commercial vehicle operators particularly favor fully electric configurations where predictable duty cycles enable precise energy management without the operational complexity of dual-power systems.

By E-Axle Configuration: Integration Drives Efficiency

Integrated e-axle systems achieve market leadership with 41.13% share in 2024 while maintaining the highest growth trajectory at 19.54% CAGR, reflecting automakers' preference for thermally optimized, space-efficient solutions. The configuration advantage stems from consolidated thermal management, reduced cabling complexity, and simplified assembly processes that particularly benefit high-volume manufacturing. Single e-axle configurations serve cost-sensitive applications, while dual e-axle systems target performance-oriented segments where all-wheel-drive capability justifies additional complexity.

Integration benefits extend beyond manufacturing efficiency as demonstrated by AISIN's Xin1 eAxle, which targets 50% size reduction in its third-generation design scheduled for 2025 introduction. The thermal integration advantage proves particularly significant for magnet-free motors where copper losses generate more heat than permanent magnet alternatives, requiring sophisticated cooling strategies. Hyundai WIA's integrated coolant distribution module demonstrates 25% component reduction compared to distributed architectures while improving thermal management effectiveness. The configuration trend accelerates as automakers recognize that integrated systems enable platform standardization across multiple vehicle variants, reducing development costs and manufacturing complexity.

By Vehicle Type: Commercial Vehicles Drive Innovation

Passenger cars maintain a dominant market position with a 57.21% share in 2024, yet buses and coaches emerge as the fastest-growing segment at 17.03% CAGR, reflecting accelerated commercial vehicle electrification timelines. The growth divergence signals fleet operators' recognition that commercial vehicles' predictable duty cycles and centralized maintenance optimize the total cost of ownership for electric drivetrains. Light commercial vehicles benefit from urban delivery applications where zero-emission zones mandate electric propulsion. In contrast, medium and heavy commercial vehicles face longer adoption cycles due to payload and range requirements.

Commercial vehicle electrification accelerates through regulatory pressure, with European cities implementing zero-emission zones that mandate electric propulsion for urban delivery applications. Electric bus sales increased 16% across Europe in 2024, driven by municipal fleet replacement programs and EU funding initiatives. The commercial vehicle focus on magnet-free technologies reflects fleet operators' preference for supply chain resilience over marginal efficiency gains, particularly in applications where maintenance predictability outweighs peak performance requirements. SUV and MUV segments within passenger cars show strong adoption rates as consumers embrace electric powertrains' torque characteristics and reduced operating costs.

Geography Analysis

Germany held 32.47% of 2024 turnover, underpinned by entrenched OEM clusters, cross-licensing between ZF, Bosch, and BMW, and Infineon’s Dresden SiC fab ramping in 2025. Federal R&D grants support rotor-cooling start-ups, and municipal zero-emission zones press local bus operators to switch. Still, labor cost pressures and environmental permitting slow greenfield expansion, nudging suppliers to satellite plants in Eastern Europe.

Spain charts the fastest 15.19% CAGR, buoyed by the MOVES III grant top-up and competitive labor rates. Stellantis Zaragoza and Volkswagen’s Valencia gigafactory anchor production ecosystems, while solar-heavy grids cut EV life-cycle emissions, a selling point in fleet tenders. Rapid-charge density in Catalonia and Madrid halves trip-planning downtime for ride-hailing and light delivery operators, cementing domestic demand.

France, Italy, the UK, and the Netherlands collectively provide diversified pull. France leverages its EUR 8 billion stimulus to subsidize Tier-1 conversion lines. Italy’s tooling heritage supports lamination die output, the UK cultivates SiC module packaging in post-Brexit enterprise zones, and the Netherlands leads charging-point density per capita. Nordic markets, though smaller, boast Europe’s highest per-capita EV penetration, ensuring above-average magnet-free axle uptake in harsh-climate bus fleets. Geographic dispersion reduces single-country risk and broadens the Europe Magnet Free Electric Axle System market foundation.

Mordor Intelligence examines the magnet free electric axle system market across diverse other regional markets as well, offering granular country-level perspectives for China, Japan, India, United States, and South Korea and more.

Competitive Landscape

Legacy Tier-1s dominate yet face escalating disruption. ZF, Bosch, and Vitesco bundle e-motor, inverter, and gearbox IP into turnkey axles, leveraging scale to supply multiple OEMs.

Emergent specialists like Infinitum Electric and Conifer pursue printed-circuit stators or magnet-agnostic designs to reduce weight and material cost. Start-up capital flows freely: Conifer’s USD 20 million Series A in June 2025 funds pilot production aimed at niche performance vans. Partnerships multiply; Valeo-MAHLE share rotor-cooling patents to truncate time-to-market. BorgWarner wins e-axle differentials by offering cross-differential torque vectoring on the same bill of materials.

The technology race pivots on thermal management and acoustics. Patents around two-phase cooling, advanced pulse control, and inductive excitation fill EPO filings as suppliers chase 30 kW/kg density ceilings. OEM sourcing shifts toward integrators that present one-invoice solutions, rewarding those with harmonized motor-inverter-gear architectures. Consequently, although incumbents retain revenue lead, market entry hurdles fall, elevating competitive churn inside the Europe Magnet Free Electric Axle System market.

Europe Magnet Free Electric Axle System Industry Leaders

-

ZF Friedrichshafen AG

-

Robert Bosch GmbH

-

Vitesco Technologies Group AG

-

Valeo SA

-

MAHLE GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BorgWarner secured multiple new electric cross differential projects in China while expanding its eMotor programs across global markets, demonstrating its strategic pivot toward integrated electric drivetrain solutions. The wins reflect growing OEM preference for consolidated supplier relationships that reduce complexity in electric vehicle development programs.

- April 2025: Conifer raised USD 20 million in Series A funding to accelerate its magnet-agnostic motor technology development. The company targets automotive applications where supply chain resilience outweighs peak efficiency requirements. The investment enables the company to scale production capabilities and compete directly with established Tier-1 suppliers.

Europe Magnet Free Electric Axle System Market Report Scope

| Externally Excited Synchronous Motors (EESM) |

| Induction Motors |

| Switched Reluctance Motors |

| Permanent Magnet Motors |

| Fully Electric Drive |

| Hybrid Drive |

| Plug-in Hybrid Drive |

| Single E-Axle |

| Dual E-Axle |

| Integrated E-Axle |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| Germany |

| United Kingdom |

| Spain |

| Italy |

| France |

| Netherlands |

| Rest of Europe |

| By Motor Type | Externally Excited Synchronous Motors (EESM) | |

| Induction Motors | ||

| Switched Reluctance Motors | ||

| Permanent Magnet Motors | ||

| By Drive Type | Fully Electric Drive | |

| Hybrid Drive | ||

| Plug-in Hybrid Drive | ||

| By E-Axle Configuration | Single E-Axle | |

| Dual E-Axle | ||

| Integrated E-Axle | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUV and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Geography | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What revenue value does the Europe Magnet Free Electric Axle System market touch in 2030?

Forecasts place the market at USD 3.18 billion by 2030, reflecting a 13.76% CAGR from 2025.

Which motor type grows the fastest through 2030?

Switched reluctance motors expand at an 18.42% CAGR as OEMs chase rare-earth independence.

How large is Germany’s share of sales today?

Germany accounted for 32.47% of 2024 market revenue, the region’s highest national share.

Why do fleets prefer integrated e-axles?

Integrated units lower operating cost about EUR 0.08/km by trimming cabling, cooling loops, and maintenance tasks.

What drives Spain’s rapid growth?

MOVES III grants and a 60.86% jump in rapid chargers propel Spain’s 15.19% CAGR.

Which technology narrows efficiency gaps with permanent-magnet drives?

800 V silicon-carbide inverters deliver up to 99.5% conversion efficiency, boosting magnet-free motor competitiveness.

Page last updated on: