Truck Axle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.82 Billion |

| Market Size (2030) | USD 2.42 Billion |

| Growth Rate (2025 - 2030) | 5.91% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Truck Axle Market Analysis by Mordor Intelligence

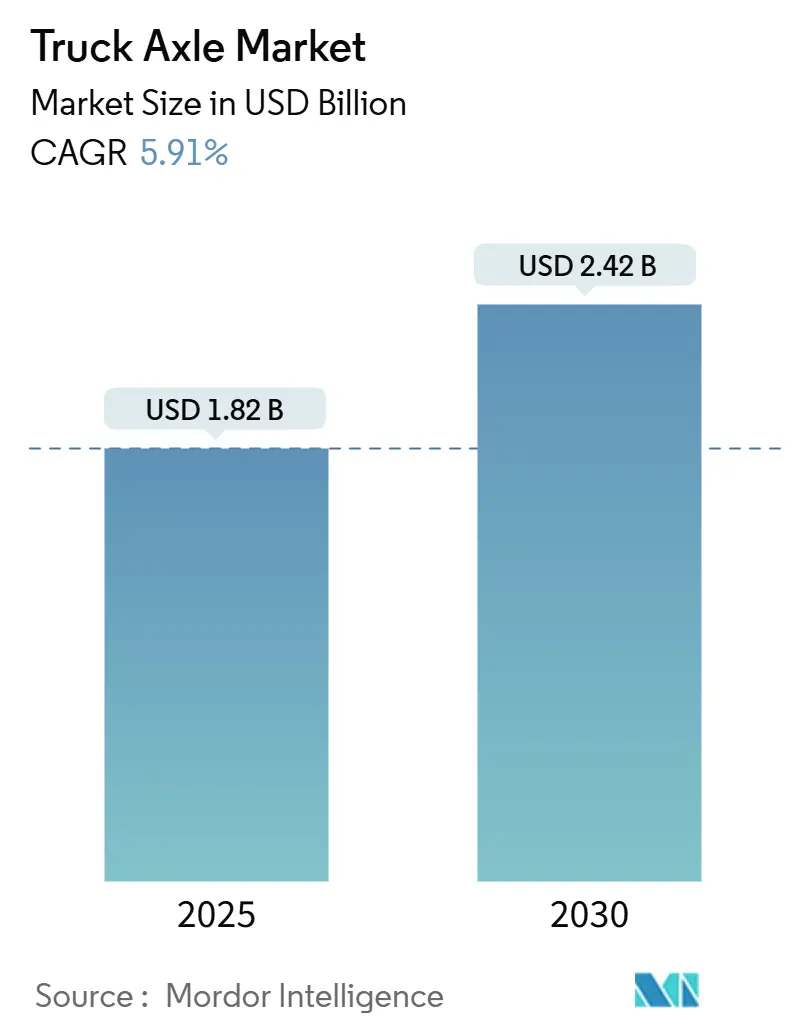

The Truck Axle Market size is estimated at USD 1.82 billion in 2025, and is expected to reach USD 2.42 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030). Elevated freight activity, electrification mandates, and infrastructure modernization align to underpin this trajectory. Heavy-duty trucks retained the most significant application slice, while light-duty platforms recorded the fastest growth because last-mile delivery and urban logistics demand nimbler vehicles. Diesel powertrains still dominate, but battery electric variants are scaling quickly as regulators enforce stricter greenhouse-gas targets. Tandem axles remain the preferred configuration for regional haulage, yet multi-axle systems are rising where heavy loads intersect with rough terrain. Across regions, Asia-Pacific leads the truck axle market, whereas South America shows the sharpest expansion amid mining and agricultural investment.

Key Report Takeaways

- By application, heavy-duty trucks held 45.17% of the truck axle market share in 2024; light-duty trucks are forecast to post a 5.95% CAGR to 2030.

- By fuel type, Diesel captured 67.73% of the truck axle market share in 2024; battery electric vehicles are on track for a 5.93% CAGR through 2030.

- By axle configuration, tandem systems led with 47.13% of the truck axle market share in 2024; multi-axle designs are poised for a 5.96% CAGR to 2030.

- By sales channel, the OEM route represented 73.47% of the truck axle market share in 2024; the aftermarket is projected to expand at a 5.98% CAGR by 2030.

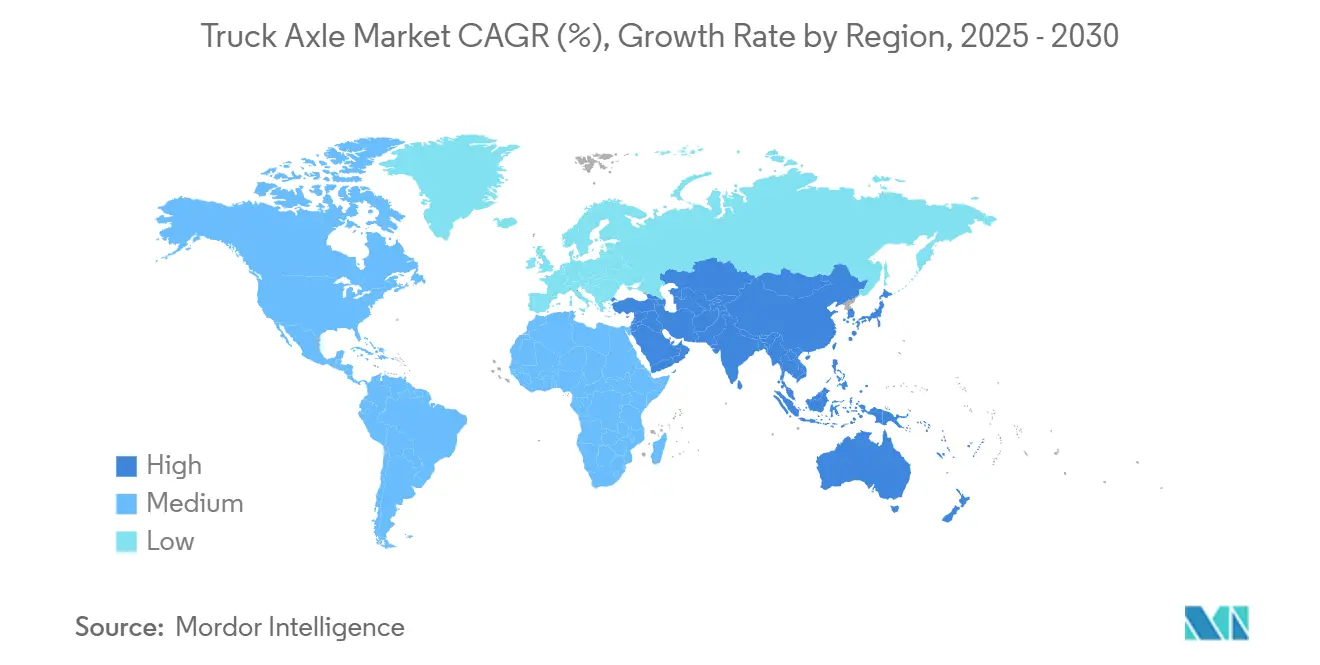

- By geography, Asia-Pacific commanded 37.83% of the truck axle market share in 2024; South America is expected to log a 5.97% CAGR through 2030.

Global Truck Axle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Global Freight Demand | +1.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Electrification Mandates | +1.6% | Europe, North America, China leading adoption | Long term (≥ 4 years) |

| Rising Preference For Multi-Axle Configurations | +1.2% | Asia-Pacific core, spill-over to South America and MEA | Medium term (2-4 years) |

| Integration Of Smart Axle Health-Monitoring Sensors | +0.9% | North America and EU early adoption, expanding globally | Short term (≤ 2 years) |

| Aftermarket Demand For Lightweight Retrofit Axles | +0.8% | Global, with emphasis on mature markets | Medium term (2-4 years) |

| Circular-Economy Push | +0.7% | Europe leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Global Freight Demand

European road freight is set to grow minimally in 2025, but demand now skews toward higher-value cargo that needs specialized axle layouts [1]“European Road Freight Rates Index Q1 2025,” International Road Transport Union, iru.org . E-commerce hubs require axles engineered for frequent stops and precise weight distribution, prompting a shift from single to tandem and tri-axle setups. Suppliers that bundle braking, suspension, and telematics into axle modules gain an edge as operators speed up replacement cycles to stay compliant with tightening emission rules. U.S. DOT Part 393 brake-performance rules also reinforce demand for integrated compliance solutions.

Electrification Mandates for Commercial Vehicles

The U.S. EPA Phase 3 rule seeks a three-fifths emission cut in heavy-duty trucks by 2032 [2]“Phase 3 Heavy-Duty Greenhouse Gas Rule,” U.S. Environmental Protection Agency, epa.gov . Reinforced housings, modified suspension mounts, and regenerative-ready brake assemblies now define e-axle specifications. Kenworth’s T680 FCEV integrates specialized axles to support hydrogen tanks and a 200-kWh battery while maintaining 82,000 lbs GCWR [3]“T680 Fuel Cell Electric Vehicle Specifications,” Kenworth Truck Company, kenworth.com . Early volumes stem from California and European fleets, yet broad uptake depends on charging buildouts and cost parity with diesel.

Preference for Multi-Axle Configurations in Developing Economies

Asia-Pacific construction and South American mining sites require axles that spread heavy loads and maintain traction on sub-par roads. Multi-axle rigs deliver one-third more payload and two-fifths stronger traction than tandem peers, pivotal where axle-load rules tighten to protect roadbeds. Demand accelerates for suppliers capable of pairing multi-axle assemblies with advanced steering and electronic stability systems.

Integration of Smart Axle Health-Monitoring Sensors

Predictive-maintenance tools shift servicing from reactive to proactive, trimming downtime by up to one-fourth for high-utilization fleets. Solutions such as SKF TraX and Hendrickson Watchman capture bearing temperature, vibration, and lubrication data, linking into fleet-management dashboards. Uptake is strongest in North America and Europe, where labor and downtime costs support the sensor premium.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Alloy-Steel Prices | -0.8% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| High R&D Costs | -0.6% | North America and EU development centers | Medium term (2-4 years) |

| Slow Charging Infrastructure Rollout | -0.5% | Global, particularly affecting long-haul routes | Long term (≥ 4 years) |

| Regulatory Uncertainty On Axle-Load Limits | -0.4% | Regional variations across jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Alloy-Steel Prices

Up to two-thirds of axle material costs are made of high-strength alloy steel, so price swings compress margins for fixed-price contracts. Shortages in electrical steel tighten supply for e-axle motors, extending lead times. Larger suppliers hedge with long-term agreements, but smaller firms often lack leverage.

High R&D Costs for E-Axle Platforms

Developing integrated motor, gear, and inverter systems demands a vast amount per platform. ZF’s collaboration with Range Energy underlines the capital intensity required to stay relevant in an electrified truck axle market. Smaller firms risk being locked out as OEMs gravitate toward partners with deep engineering resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Heavy-Duty Dominance Meets Light-Duty Growth

Heavy-duty trucks accounted for a 45.17% truck axle market share in 2024, underlining their position in long-haul and construction routes. Light-duty vehicles are set to record a 5.95% CAGR through 2030 as e-commerce boosts last-mile frequency. Medium-duty trucks form a stable mid-range niche, serving regional distribution where terrain and payload vary.

Fleet right-sizing is tilting investments toward smaller chassis. Advances in metallurgy deliver higher strength-to-weight ratios, allowing light-duty axles to handle greater payload without compromising durability. Regulatory frameworks such as FMCSA Part 393 accelerate the adoption of integrated brake-suspension axles that simplify compliance.

By Fuel: Diesel Dominance Faces Electric Disruption

Diesel still held 67.73% of the truck axle market share in 2024, but battery electric systems will expand at a 5.93% CAGR through 2030, recalibrating truck axle market size dynamics. Gasoline remains a North American niche. Fuel-cell and hybrid setups attract attention for long-haul missions where battery mass penalizes range.

E-axle suppliers benefit from premium pricing owing to the complex integration of motors and power electronics. Nikola’s Tre FCEV, with a 500-mile range and 20-minute refueling time, showcases how hydrogen storage reshapes axle architecture.

By Axle Configuration: Multi-Axle Innovation Drives Growth

Tandem axles delivered 47.13% of the truck axle market share in 2024, but multi-axle designs will pace the field with a 5.96% CAGR through 2030. Governments impose axle-load caps to protect roads, spurring demand for rigs that spread weight. Hendrickson’s TRLAXLE line offers capacities up to 27,000 lbs coupled with electronic stability modules, demonstrating how innovation supports payload while guarding infrastructure.

Electronic steering advances now grant multi-axle sets a turning radius close to tandem layouts, dissolving earlier maneuverability trade-offs and widening adoption.

By Sales Channel: Aftermarket Acceleration Challenges OEM Dominance

While OEMs owned 73.47% of the truck axle market share in 2024, the aftermarket will expand 5.98% annually due to cost-focused fleet strategies. Remanufactured axles deliver up to three-fifths savings and four-fifths energy cuts compared to new builds. LKQ’s processing of 735,000 vehicles and nearly 12 million parts signals scale potential that can rival OEM liquidity.

Circular-economy incentives plus extended warranties reassure operators about reman quality, steadily shifting volume toward the aftermarket.

Geography Analysis

Asia-Pacific generated 37.83% of the truck axle market share in 2024, with China’s electric-truck leadership and India’s freight reforms driving momentum. China captured the majority of global electric-truck sales, making the region a development center for e-axle scale-up. India’s GST regime and logistics corridors sustain demand for reliable heavy-duty axles.

South America will post the highest regional CAGR of 5.97% through 2030. Brazil leverages biodiesel and ethanol blends that require axle adaptations, while Argentina’s agricultural and mining sectors create steady orders for multi-axle rigs that can tackle rough terrain. Europe’s growth rests on electrification and circular-economy leadership. Rigorous emission ceilings cultivate premium demand for e-axle systems. Volvo’s 70-year reman heritage embodies the region’s circular ethos, with rear-axle transmissions central to sustainability mandates.

North America benefits from substantial freight volumes yet faces patchy infrastructure upgrades that temper growth. Across Canada and the United States, axle makers must navigate varied state weight limits, spurring interest in modular designs that can be re-rated with minimal overhaul.

Competitive Landscape

The truck axle market shows moderate concentration. Dana, ZF, and Meritor leverage deep OEM ties and scale production. Hendrickson’s 2024 purchase of Reyco Granning broadened its suspension know-how, reinforcing integrated axle-suspension packages. E-axle specialists such as Siemens and Bosch carve premium niches by offering turnkey electric drivetrain modules.

Partnerships are pivotal. Hendrickson paired with Voith in May 2025 to merge axle craftsmanship with electric drivetrain expertise, targeting medium and heavy-duty e-trucks [4]“Press Release: Voith and Hendrickson Joint Development,” Voith, voith.com . White-space opportunities lie in additive-manufactured housings, predictive-maintenance software, and e-axle remanufacturing, all of which favor agile players that can mesh mechanical heritage with digital capabilities.

OEM procurement strategies increasingly weigh total-lifecycle cost and carbon footprint, elevating suppliers that provide reman programs and recyclable materials. Compliance consulting bundled with axle hardware further differentiates offers as DOT and EU Transport Commission rules tighten.

Truck Axle Industry Leaders

Dana Incorporated

Meritor

ZF Friedrichshafen AG

American Axle & Manufacturing

Hendrickson Holdings LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hendrickson and Voith agreed to co-develop integrated e-axle packages for commercial vehicles, blending Hendrickson’s axle portfolio with Voith electric-drive modules.

- November 2024: Nextran Truck Centers acquired Quincy Mack, Decatur Mack, and H&L Mack, taking its dealership count to 31 locations and expanding aftermarket axle servicing across the U.S. Midwest.

- June 2024: Hendrickson Holdings finalized the purchase of Reyco Granning, adding specialized suspension assets to bolster its integrated axle-suspension footprint.

Global Truck Axle Market Report Scope

| Light-Duty Trucks |

| Medium-Duty Trucks |

| Heavy-Duty Trucks |

| Gasoline |

| Diesel |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Single Axle |

| Tandem Axle |

| Tri-Axle |

| Multi-Axle |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Light-Duty Trucks | |

| Medium-Duty Trucks | ||

| Heavy-Duty Trucks | ||

| By Fuel | Gasoline | |

| Diesel | ||

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Axle Configuration | Single Axle | |

| Tandem Axle | ||

| Tri-Axle | ||

| Multi-Axle | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the truck axle market?

The truck axle market reached USD 1.82 billion in 2025 and is on track for USD 2.42 billion by 2030.

Which axle configuration is growing fastest?

Due to infrastructure projects requiring heavy-haul capacities, multi-axle systems are expected to grow at a 5.96% CAGR through 2030.

How dominant are diesel axles versus electric?

Diesel held 67.73% of 2024 revenue, but electric axles are the fastest-growing at a 5.93% CAGR as mandates tighten.

Which region leads demand?

Asia-Pacific generated 37.83% of 2024 revenue, supported by China’s electric-truck adoption and India’s freight reforms.

Why is the aftermarket segment accelerating?

Fleet operators seek lifecycle savings, and remanufactured axles cut purchase costs by up to 60% while delivering same-as-new performance.

Page last updated on: