Japan Magnet Free Electric Axle System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

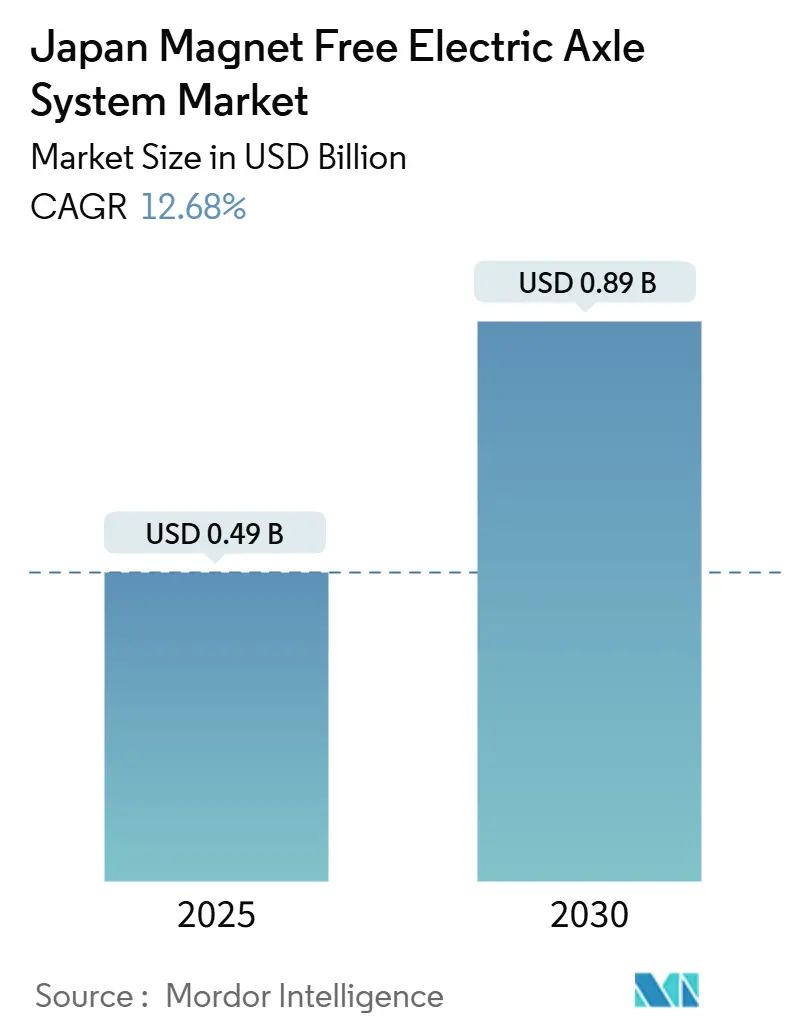

| Market Size (2025) | USD 0.49 Billion |

| Market Size (2030) | USD 0.89 Billion |

| Growth Rate (2025 - 2030) | 12.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Magnet Free Electric Axle System Market Analysis by Mordor Intelligence

The Japan Magnet Free Electric Axle System market size stands at USD 0.49 billion in 2025 and is forecast to reach USD 0.89 billion by 2030, translating into a 12.68% CAGR. Policymakers’ target 100% electrified vehicle sales by 2035, the Ministry of Economy, Trade and Industry’s (METI) JPY 129.1 billion clean-energy vehicle subsidy pool, and persistent rare-earth supply risk after China’s 2023 export restrictions collectively pull demand toward rare-earth-independent propulsion. Automakers are accelerating next-generation e-drive investment to meet tightened 2030 Corporate Average Fuel Economy standards, while the Green Innovation Fund’s backing for domestic silicon-carbide (SiC) module capacity is lowering total system costs in Japan Magnet Free Electric Axle System market powertrains. Integrated development of switched-reluctance and externally excited synchronous motors is also shrinking weight and improving thermal performance, easing OEM adoption barriers. Together, these forces position the Japan Magnet Free Electric Axle System market for double-digit expansion through 2030.

Key Report Takeaways

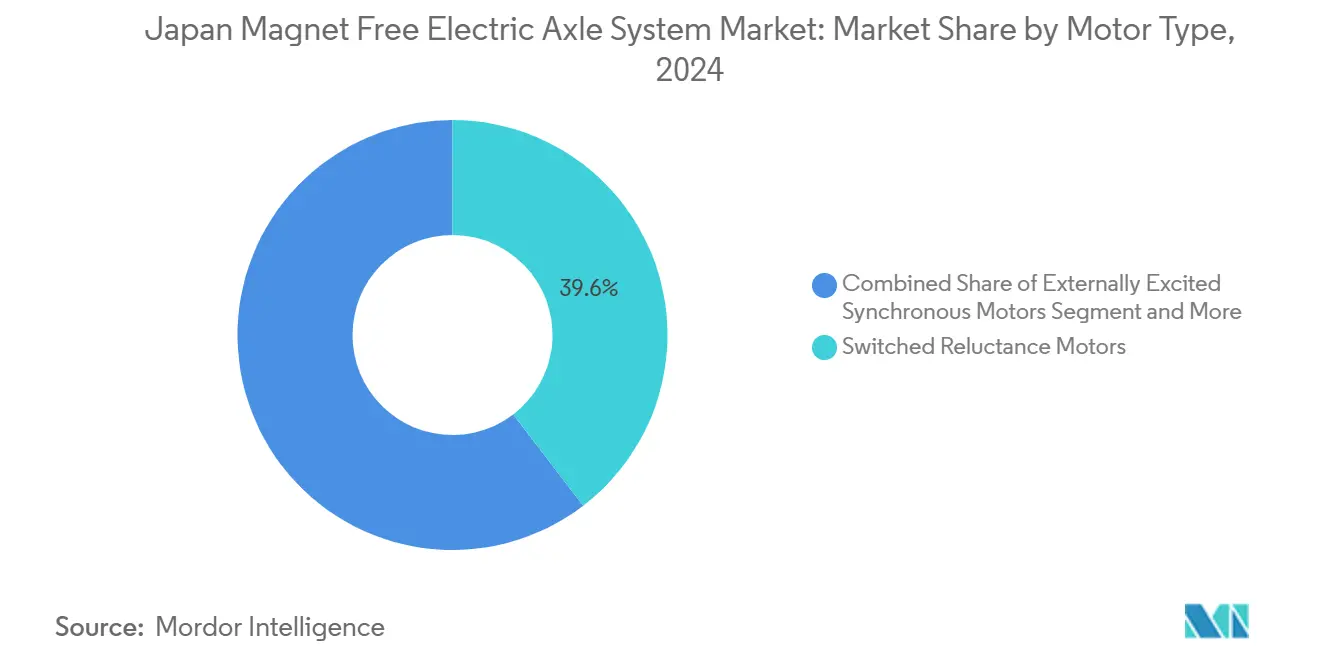

- By motor type, switched-reluctance designs led with 39.55% of Japan Magnet Free Electric Axle System market share in 2024, while externally excited synchronous motors are projected to grow at a 14.34% CAGR through 2030.

- By drive type, fully electric systems captured 63.58% of the Japan Magnet Free Electric Axle System market size in 2024 and are advancing at a 17.63% CAGR to 2030.

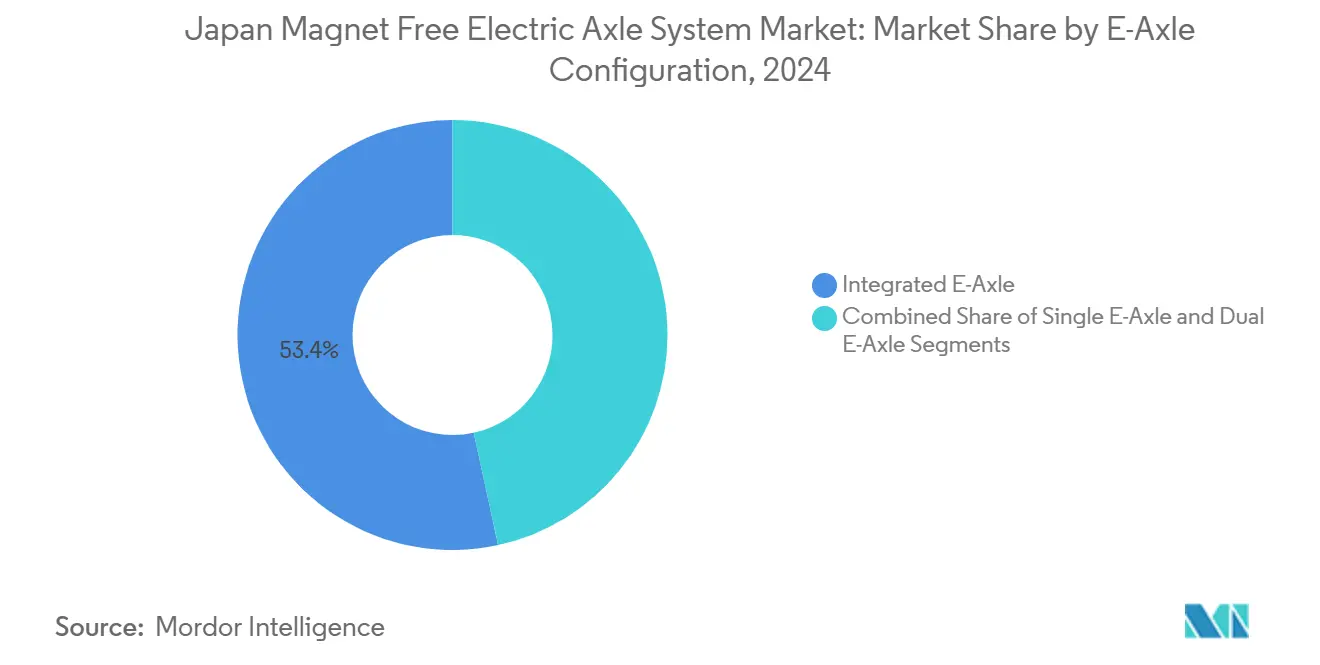

- By e-axle configuration, integrated units accounted for a 53.44% share of the Japan Magnet Free Electric Axle System market size in 2024, whereas dual e-axle setups are set to expand at a 16.42% CAGR during the same horizon.

- By vehicle category, passenger cars commanded 67.82% of the Japan Magnet Free Electric Axle System market share in 2024, but commercial vehicles are on track for the highest 15.48% CAGR through 2030.

Japan contributes to a system defined not by any single country or region but by the interaction of many. The global magnet free electric axle system market data by Mordor Intelligence represents that combined structure.

Japan Magnet Free Electric Axle System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Rare-Earth Risk Mitigation Post-2023 | +3.2% | Global supply chains, Japanese OEM focus | Short term (≤ 2 years |

| Incentives for 100% xEV Sales by 2035 | +2.8% | National – Tokyo, Osaka, Nagoya first | Medium term (2-4 years) |

| SiC Inverter Synergies in 800 V Platforms | +2.4% | National, premium EV makers | Medium term (2-4 years) |

| CAFE Standards Tightening from 2028 | +2.1% | National | Medium term (2-4 years) |

| Green Fund–Backed Domestic SiC Ramp-Up | +1.9% | National, semiconductor hubs | Long term (≥ 4 years) |

| Weight Savings vs. Dual-Motor E-Drives | +1.7% | National, premium segment first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Shift to Rare-Earth Risk Mitigation After 2023 Nd Price Spike

China’s dominance over 90% of rare-earth processing revealed a single-point failure that Japan-based automakers can no longer tolerate. Post-spike, Toyota pivoted toward switched-reluctance architectures while Proterial commercialized ferrite-based motors that remove neodymium entirely. Government support, including a JPY 200 billion Lynas partnership, offers an interim bridge but underscores the structural need for magnet-free drivetrains. This security calculus channels capital toward domestic Japan Magnet Free Electric Axle System market programs that substitute controlled semiconductor inputs for volatile mineral streams.

Government Incentives for 100% xEV Sales by 2035

Japan Magnet Free Electric Axle System market growth benefits directly from METI’s up-to-JPY 850,000 purchase subsidies that explicitly reward manufacturers proving resilient, low-carbon supply chains. Funding flows also cover charging infrastructure, with an official target of 300,000 public charge points by 2030—ten times the 2024 network. These incentives cluster first in metropolitan prefectures where charger density is already high, creating early-mover demand pockets for magnet-free powertrains. The seven-year policy horizon supports large-scale factory amortization, letting suppliers spread fixed R&D expenses over multiple product lifecycles. Ultimately, long-term certainty strengthens project finance conditions in the Japan Magnet Free Electric Axle System market [1]Ministry of Economy, Trade and Industry, “FY2024 Clean Energy Vehicle Subsidy Program,” meti.go.jp.

Integration Synergies with SiC Inverters in 800 V Platforms

SiC semiconductors slash inverter losses by 20% and permit higher switching frequencies, a perfect match for magnet-free switched-reluctance torque characteristics. Denso’s latest 800 V inverter is 30% smaller, easing chassis packaging constraints for e-axle assemblies. JR East’s rail deployments prove SiC durability in harsh thermal cycles, lending confidence to automotive qualification. As 8-inch SiC wafer supply ramps, cost curves are bending downward, broadening premium-EV tech diffusion across the Japan Magnet Free Electric Axle System market.

Corporate Average Fuel Economy Tightening from 2028

The Top Runner program’s 25.4 km/L fleet benchmark raises the energy-efficiency bar for every domestic automaker. Because efficiency gains from conventional hybrids are plateauing, corporate strategies emphasize pure EV rollouts fitted with power-dense magnet-free e-axles that beat target grams-per-kilometer thresholds. Well-to-wheel accounting further advantages domestically sourced, rare-earth-free motors, aligning compliance costs with the Japan Magnet Free Electric Axle System market roadmap. Financial penalties for non-compliance run into millions of USD annually, reinforcing investment urgency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow Charger Roll-Out Outside Key Corridors | -2.1% | Regional, rural prefectures | Short term (≤ 2 years) |

| High Cost Premium Until Post-2027 | -1.9% | National, price-sensitive tiers | Medium term (2-4 years) |

| No Local Tier-2 SRM Electronics Supply | -1.8% | National, legacy auto regions | Medium term (2-4 years) |

| Higher NVH Than PM E-Motors | -1.2% | National, premium models | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slow Charging-Station Roll-Out Outside Tōkai and Kantō Corridors

Urban drivers can already access an acceptable 4.5 charger-per-EV ratio, whereas secondary cities and rural prefectures fall below 25% of that density. Range anxiety curtails BEV penetration, making it harder for automakers to amortize magnet-free e-axle investments across nationwide volumes. Unless 2025–2027 charger deployments accelerate, the Japan Magnet Free Electric Axle System market risks a geographic demand plateau.

Higher Upfront Cost Premium Versus PM E-Axles Until Economies of Scale Are Achieved

Magnet-free systems cost 15-25% more today because specialized laminations, bus bars, and high-bandwidth controllers lack mass-production tooling. Learning curves should converge around 2027 once combined shipments exceed 1 million units, but early-cycle sticker shock still slows fleet conversions in cost-sensitive segments of the Japan Magnet Free Electric Axle System market [2]IEEE Spectrum, “Cost Parity Outlook for Magnet-Free Drives,” ieee.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Switched-Reluctance Dominance Amid EESM Innovation

Switched-reluctance designs owned the largest 39.55% slice of the Japan Magnet Free Electric Axle System market share in 2024. They deliver copper-heavy robustness that suits Japanese duty cycles, but externally excited synchronous motors are scaling fastest at 14.34% CAGR as OEMs target magnet-like refinement without rare-earths. Toshiba’s partial-magnet rotor proves a transitional path that buys time until full magnet elimination locks in, keeping the Japan Magnet Free Electric Axle System market size momentum intact through the forecast window [3]Toshiba Corporation, “Ferrite Rotor Innovation Press Note,” global.toshiba.

Higher-speed operating envelopes, enabled by SiC inverters, are squeezing drivetrain footprints further in both architectures. As patent pools expand, licensing opportunities create incremental revenue lines for technology owners. Meanwhile, induction motors sustain a niche among heavy commercial fleets, favoring proven simplicity, illustrating how multipronged design portfolios remain essential in the Japan Magnet Free Electric Axle System market.

By Drive Type: Fully Electric Supremacy Accelerates

Fully electric powertrains captured 63.58% of the Japan Magnet Free Electric Axle System market size in 2024 and will outpace hybrid counterparts at a 17.63% CAGR. Dedicated skateboard platforms integrate the e-axle, battery, and inverter into a structural unit, pushing new benchmarks on torsional rigidity and assembly time. Cost-optimized hybrid and plug-in configurations persist yet show declining share, confirming BEV prioritization in the Japan Magnet Free Electric Axle System market.

All-solid-state battery pilots, planned for post-2027 launch, are expected to amplify e-axle energy-density advantage once thermal envelopes tighten. Until then, the segment’s expansion remains tethered to rapid-charging roll-outs and lifecycle-cost parity, both trending positively in the Japan Magnet Free Electric Axle System market.

By E-Axle Configuration: Integrated Leadership Faces Dual-Axle Challenge

Integrated units controlled over half of 2024 shipments, underscoring the packaging and logistics benefits of single-housing solutions in the Japan Magnet Free Electric Axle System market. Dual-axle architectures, though, are adding volume fastest at 16.42% CAGR because high-performance and SUV buyers demand torque-vectoring and all-weather traction. Suppliers now hedge by offering modular gear-set options that enable one production line to satisfy both configurations cost-effectively.

Front-rear power-split strategies also open software revenue streams from over-the-air handling upgrades, illustrating convergence between electrified chassis and digital-service monetization. The trend broadens profit pools in the Japan Magnet Free Electric Axle System market while diversifying product risk exposure.

By Vehicle Type: Commercial Growth Outpaces Passenger Dominance

Passenger cars dominate absolute volume with a 67.82% share, reflecting Toyota, Honda, and Nissan model proliferations. Yet commercial fleets will post the sharpest 15.48% CAGR because predictable urban routes align with battery range constraints, and regulatory weight exemptions bolster payload economics. Battery-swap pilots across logistics hubs further de-risk downtime for light-duty trucks, pulling incremental unit demand into the Japan Magnet Free Electric Axle System market.

Mid-duty bus and truck electrification will gather pace once 400 kW public chargers are common, projected for late-decade deployment. As those milestones arrive, motor specifications will diverge—favoring induction or permanent-magnet-assisted reluctance in torque-heavy applications—highlighting design pluralism inside the Japan Magnet Free Electric Axle System market.

Geography Analysis

The Japan Magnet Free Electric Axle System market clusters along the Tōkai and Kantō industrial corridors. Automotive assembly footprints in Aichi, coupled with SiC wafer fabs in Mie, shorten supply loops and compress design iterations. Tokyo’s dense charger mesh accelerates early-adopter volumes, cementing first-mover scale advantages for local e-axle plants.

Northern prefectures lag because rural charger density remains sparse, prompting a twin-track policy response that bundles charger subsidies with rural economic-revitalization grants. As roll-outs gain speed, secondary cities like Sendai and Okayama forecast double-digit e-vehicle uptake, enlarging addressable pools for Japan Magnet Free Electric Axle System market suppliers by the late decade.

Geographic dispersion will deepen once semiconductor tax credits pull wafer capacity into Kyushu and Shikoku, balancing regional employment while cushioning disaster-risk concentration. The emerging multi-hub network improves resilience, ensuring stable product flow even during natural-hazard disruptions, and thus underpins a sturdy nationwide Japan Magnet Free Electric Axle System market expansion path.

The magnet free electric axle system market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe. This is complemented by country-specific insights for South Korea, China, India, and United States, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Competition is moderately concentrated; the top suppliers commanded a significant share of shipments, leveraging vertical integration across motors, gears, and SiC inverters. Nidec is targeting 40-45% global share by 2030, shelling out more than JPY 500 billion for capacity and R&D, while Mitsubishi Electric upgrades production lines to hybrid stator-welding processes that cut takt time by 20%. Toyota’s internal e-Drive unit banks on system-level optimization within its e-TNGA platform, sustaining economies of scope that few rivals can match.

Tier-2 disruptors are chipping away at control-electronics niches, exploiting open-source firmware and agile, low-overhead plants to underprice legacy vendors by as much as 15%. Partnerships bloom as incumbents secure specialized IP—Valeo and MAHLE’s iBEE project illustrates cross-border collaboration aimed at premium models. The Japan Magnet Free Electric Axle System industry also witnesses upstream power-device makers like Denso vaulting downstream via reference-design kits, blurring former supplier-OEM boundaries.

Patent filings in switched-reluctance rotor topologies and EESM excitation circuits have spiked 28% year-over-year, hinting at an arms race in electromagnetic IP. Defensive clusters deter new entrants lacking deep war-chests, yet licensing royalties promise healthy annuity streams for patent leaders. Meanwhile, Chinese contenders penetrate mid-market tiers, pressuring pricing and compelling Japanese firms to differentiate on quality and system integration excellence in the Japan Magnet Free Electric Axle System market.

Japan Magnet Free Electric Axle System Industry Leaders

Nidec Corporation

ZF Friedrichshafen AG

BorgWarner (Japan)

Dana Inc. (Japan)

GKN Automotive (Japan)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Valeo and MAHLE launched the iBEE inner-brushless electrical-excitation axle aimed at 220–350 kW premium EVs.

- September 2023: ZF unveiled the I2SM in-rotor inductive-excited synchronous motor, achieving higher torque density in a compact, magnet-free package.

Japan Magnet Free Electric Axle System Market Report Scope

| Externally Excited Synchronous Motors (EESM) |

| Induction Motors |

| Switched Reluctance Motors |

| Fully Electric Drive |

| Hybrid Drive |

| Plug-in Hybrid Drive |

| Single E-Axle |

| Dual E-Axle |

| Integrated E-Axle |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| By Motor Type | Externally Excited Synchronous Motors (EESM) | |

| Induction Motors | ||

| Switched Reluctance Motors | ||

| By Drive Type | Fully Electric Drive | |

| Hybrid Drive | ||

| Plug-in Hybrid Drive | ||

| By E-Axle Configuration | Single E-Axle | |

| Dual E-Axle | ||

| Integrated E-Axle | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUV and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

Key Questions Answered in the Report

How large is the Japan Magnet Free Electric Axle System market in 2025?

The market is valued at USD 0.49 billion in 2025, with a forecast CAGR of 12.68% to 2030.

What policy is driving adoption of magnet-free e-axles in Japan?

METI’s mandate for 100% electrified vehicle sales by 2035 and corresponding purchase subsidies are the primary drivers.

Which motor type currently leads in shipment share?

Switched-reluctance motors hold the lead with 39.55% share in 2024.

What segment is expected to grow fastest through 2030?

Commercial vehicles show the highest projected CAGR at 15.48%, propelled by fleet electrification mandates.

Page last updated on: