China Magnet Free Electric Axle System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

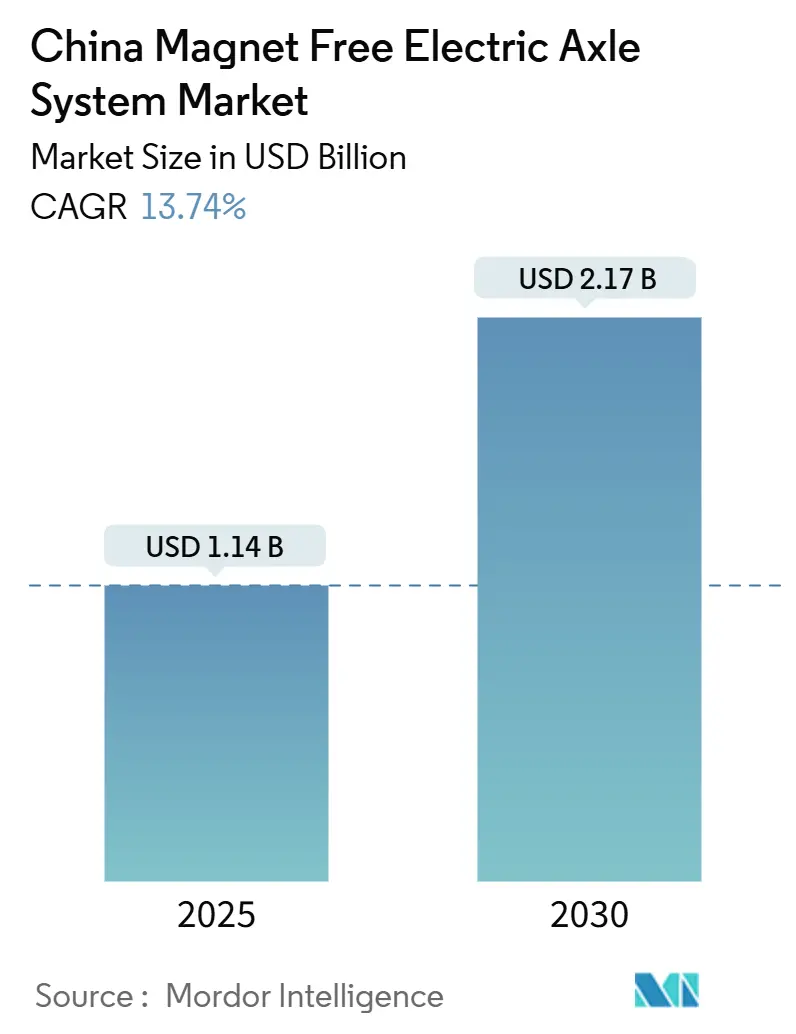

| Market Size (2025) | USD 1.14 Billion |

| Market Size (2030) | USD 2.17 Billion |

| Growth Rate (2025 - 2030) | 13.74% CAGR |

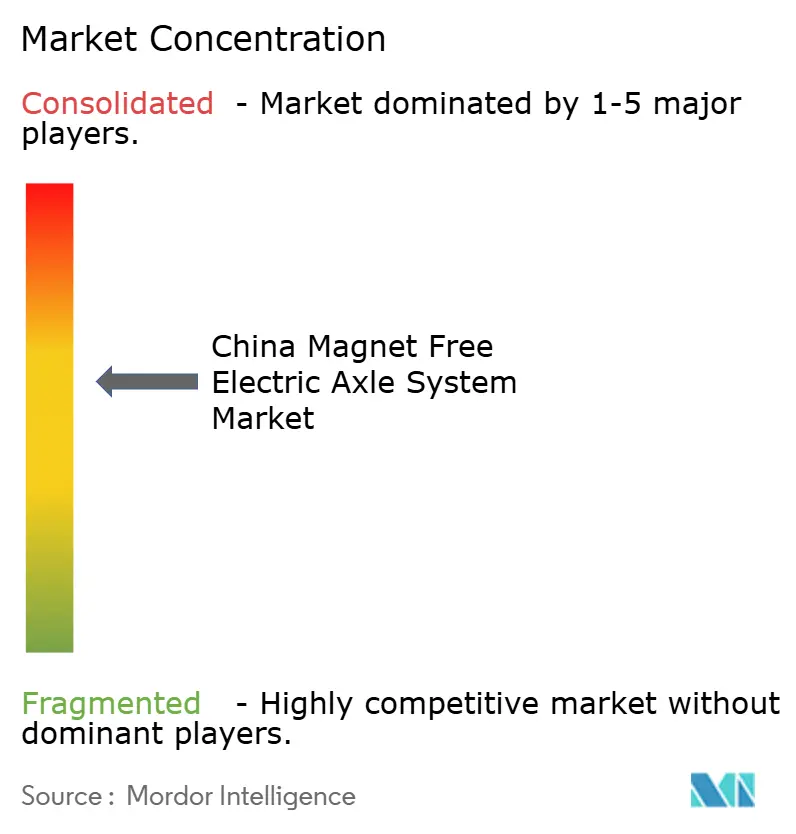

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Magnet Free Electric Axle System Market Analysis by Mordor Intelligence

The China magnet-free electric axle system market size stands at USD 1.14 billion in 2025 and is forecast to grow to USD 2.17 billion by 2030, reflecting a 13.74% CAGR over the period. A widening gap between rare-earth supply and demand, sustained government incentives for new-energy vehicles, and accelerating silicon-carbide adoption are converging to lift demand for induction, switched-reluctance, and externally excited synchronous motor e-axles. OEMs are responding to neodymium price swings that averaged almost 50% intrayear volatility in 2024 by prioritizing designs that remove rare-earth risk. Rapid expansion of China’s charging network, which added 850,000 public charging points in 2024, further underpins e-axle penetration, while domestic semiconductor advances drive parity—or better—against permanent-magnet solutions on total cost of ownership. Together, these dynamics position the China magnet-free electric axle system market as a strategic pillar in the country’s wider decarbonization agenda.

Key Report Takeaways

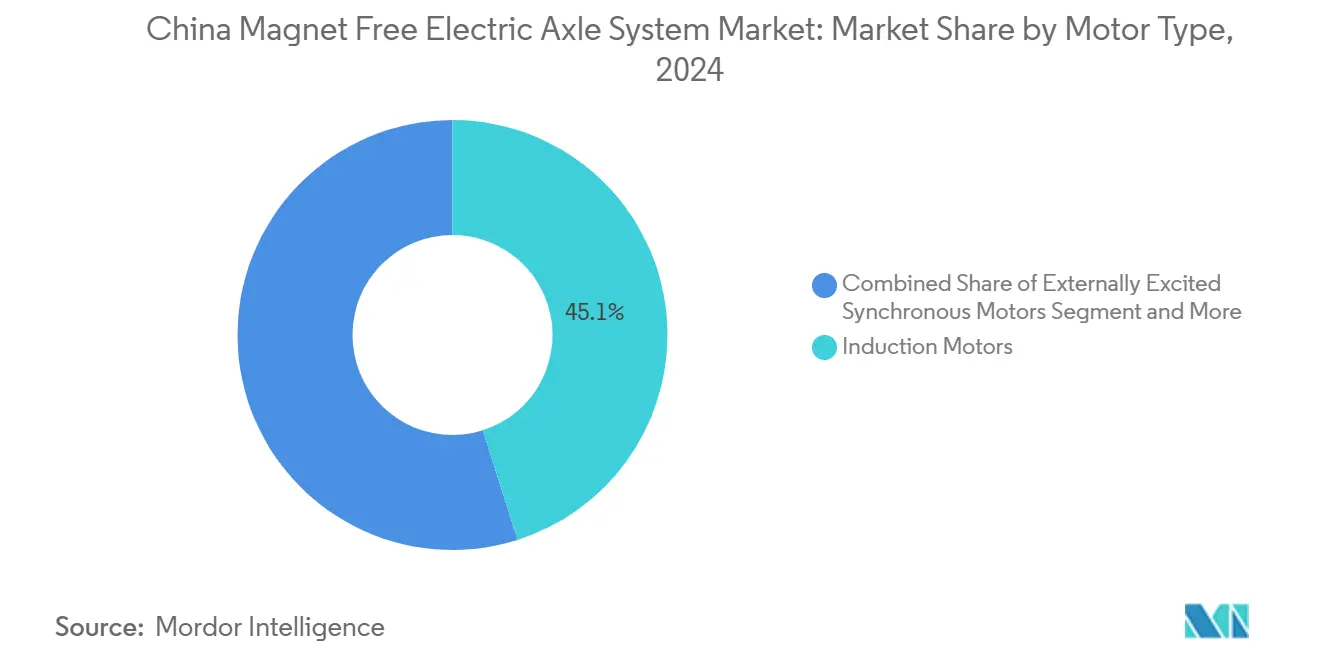

- By motor type, induction motors led with a 45.12% share of the China magnet-free electric axle system market in 2024, whereas switched-reluctance motors are projected to record the fastest 15.13% CAGR through 2030.

- By drive type, fully electric systems commanded 64.33% revenue share in 2024 and are forecast to advance at an 18.03% CAGR over 2025–2030.

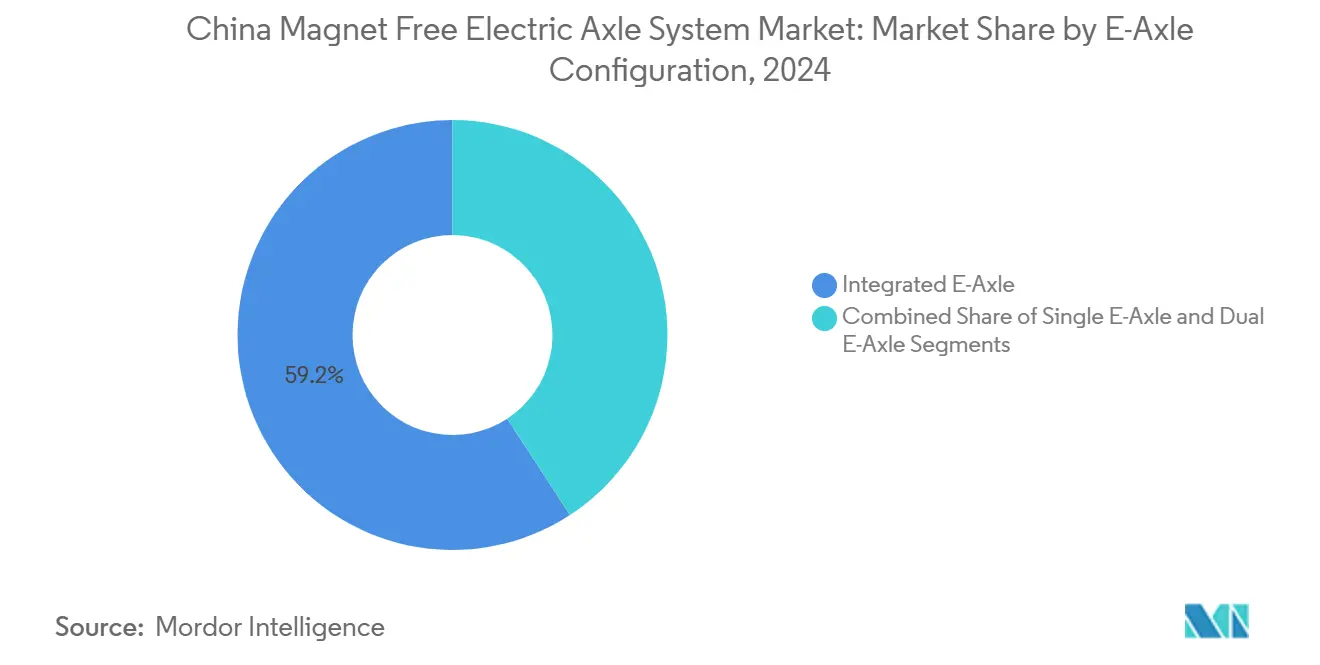

- By e-axle configuration, integrated designs captured 59.15% of 2024 sales and are expanding at a 17.44% CAGR through 2030.

- By vehicle type, passenger cars held 73.46% of deliveries in 2024, while commercial vehicles showed the highest 16.42% CAGR potential to 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on magnet free electric axle system market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Magnet Free Electric Axle System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NEV Mandates & Local-Content Rules | +3.2% | National, provincial implementation | Medium term (2–4 years) |

| Rare-Earth Price Volatility Driving Magnet-Free Shift | +2.8% | National | Short term (≤ 2 years) |

| SR & EESM Control Algorithm Advances | +2.4% | China manufacturing | Short term (≤ 2 years) |

| Lower Ownership Cost Than PM E-Axles | +2.1% | Core markets, tier-2 expansion | Medium term (2–4 years) |

| Carbon-Footprint Reporting for Tier-1s | +1.9% | National, multinational chains | Long term (≥ 4 years) |

| Domestic SiC Chip Breakthroughs | +1.8% | National, export potential | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government NEV Mandates and Local-Content Rules

The dual-credit policy requires 20% NEV penetration by 2025, translating into explicit motor-efficiency and energy-density thresholds that favor magnet-free motors capable of high peak-temperature operation. Provincial subsidies now weight scorecards toward components sourced within China, giving domestic induction and switched-reluctance motor suppliers a procurement edge over imported permanent-magnet drives. Updated environmental information disclosure rules obligate listed automakers to publish lifecycle emissions, further boosting alternatives that avoid high-intensity rare-earth mining. In parallel, local governments offer tax rebates covering up to 30 % of incremental R&D outlays for magnet-free e-axle integration, reducing payback periods on new production lines. The regulatory suite creates durable demand insulation for the China magnet-free electric axle system market.

Rare-earth Price Volatility Accelerates OEM Shift to Magnet-Free Motors

Neodymium spot prices moved in a 2.3-fold range during 2024, unsettling production planning and prompting OEMs to lock in magnet-free strategies that decouple drivetrain cost from commodity swings. China’s 70% share of global rare-earth output paradoxically increases domestic exposure to export quotas and speculative stockpiles, making supply security a board-level priority. Industry forecasts point to a 3,000 metric-ton shortfall in praseodymium-neodymium oxide by 2025, intensifying the rush toward alternative motor topologies. Tesla’s decision to trim silicon-carbide use by 75% while hitting efficiency targets shows that substituting constrained materials can improve profitability without diluting performance. For Chinese automakers, magnet-free designs are no longer a cost hedge; they are becoming the default architecture in next-generation platforms.

Breakthroughs in Control Algorithms for SR and EESM Motors

Adaptive sliding-mode controls now shave torque ripple by 80% in low-load conditions and 37% at high load, erasing historic NVH gaps that sidelined switched-reluctance architectures in premium applications. Tula Technology’s dynamic motor drive demonstrates that software-defined pulse patterning can trim energy use by up to 5% during urban duty cycles, bringing real-world efficiency in line with laboratory best-in-class permanent-magnet motors. Machine-learning-enhanced field-oriented control optimizes phase current in real time, unlocking 0.5 % incremental range per charge. These advances accelerate the China magnet-free electric axle system market transition from material-driven to algorithm-centric differentiation.

Lower Total Cost of Ownership vs. PM E-axles

Magnet-free e-axle platforms benefit from simplified rotor structures, lower cooling-loop complexity, and elimination of demagnetization risks, thereby cutting five-year fleet operating costs despite higher inverter content. Ricardo’s Alumotor showed material savings of nearly 60% versus permanent-magnet baselines by swapping copper windings for aluminum and removing rare-earth entirely. Durability tests under −40 °C to +150 °C cycles indicated a negligible dip in torque output, reducing downtime and warranty reserves for operators. Although silicon-carbide inverters add roughly USD 300 per axle today, cost curves are falling in line with local wafer capacity expansions, setting up parity by 2027. The aggregate economics strengthen the China magnet-free electric axle system market’s appeal to logistics fleets targeting predictable maintenance schedules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Inverter Cost at High Frequencies | -2.1% | National, cost-sensitive segments | Medium term (2–4 years) |

| NVH & Torque-Density Gap | -1.8% | Acute in premium segments | Short term (≤ 2 years) |

| Complex Thermal Management for E-Axles | -1.6% | Manufacturing hubs | Medium term (2–4 years) |

| No Unified Motor Insulation Standards >800 V | -1.2% | National, regulatory uncertainty | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Inverter Cost for High-Frequency Operation

Magnet-free motors rely on 40 kHz-plus switching to match the dynamic response of rare-earth alternatives, pushing designers toward SiC MOSFET topologies priced 30–40% above silicon IGBT stacks [1]Infineon Technologies, “Cost Comparison: Si vs. SiC Inverters,” INFINEON.COM. Elevated switching also generates additional losses in gate-driver circuitry, compelling advanced cooling plates and higher-conductivity busbars. Cost spread is narrowing as Chinese fabs reach yield parity with overseas peers, yet entry-level models face retail-price sensitivity of USD 15–20 per kWh that can swing purchase decisions. OEMs hedge by offering mixed portfolios—induction for high-volume trims and permanent-magnet options in premium lines—maintaining pressure on the China magnet-free electric axle system market until silicon-carbide wafer prices fall another 30%.

NVH and Torque-Density Gap with PM Motors

Double-salient stator geometry in switched-reluctance motors produces radial force harmonics that elevate audible noise, limiting uptake in luxury models where cabin refinement is non-negotiable. Even with skewed rotor pole designs and improved slot-fill factors, torque density trails permanent-magnet counterparts by 15–20%, forcing larger housings that complicate platform packaging. Hybrid noise-cancellation systems can mask high-frequency whine, yet they add four to six kilograms and USD 80–90 of bill-of-materials cost. Randomized pulse-width modulation mitigates current harmonics but boosts thermal load in the inverter section, demanding higher-grade power modules. Continuous NVH improvements remain essential for premium offerings, but are less critical in commercial vans and entry sedans, containing the restraint’s long-term drag on the China magnet-free electric axle system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Induction Motors Anchor Share as Switched-Reluctance Gains Traction

Induction motors accounted for 45.12% of the China magnet-free electric axle system market in 2024 by virtue of mature tooling and robust supplier networks. They deliver rugged performance and accept standard inverters, allowing OEMs to amortize development costs over several vehicle generations. The 15.13% pace is expected for switched-reluctance motors, due to their simple rotor architecture and absence of windings, lower materials outlay, and assembly time. Achieving quieter operation through adaptive control loops, switched-reluctance motors increasingly feature in compact SUVs, especially those positioned for mobility-platform fleets seeking low lifecycle cost.

Induction designs are evolving through high-silicon steel laminations and dual-side cooling jackets to push continuous power density beyond 6 kW/kg, narrowing the historical gap with permanent-magnet machines. ZF’s I²SM prototype demonstrated 96% peak efficiency by pairing an inductively excited rotor with advanced slot geometry and variable-frequency drive logic [2]IEEE Spectrum, “I²SM Motor Reaches 96% Efficiency,” SPECTRUM.IEEE.ORG. Meanwhile, externally excited synchronous motors hold share but resonate with premium marques that demand tight torque control and regenerative-braking smoothness. The interplay of control sophistication and materials substitution cements algorithm-centric innovation as the main battleground within the China magnet-free electric axle system market.

By Drive Type: Full-Electric Dominance Underpins Volume Growth

Fully electric drive lines held 64.33% revenue in 2024 and are set to deliver an 18.03% CAGR through 2030, aided by falling battery pack prices that dipped below USD 90/kWh in 2024. Consumer confidence in charging accessibility rose sharply after national coverage reached 0.37 piles per vehicle added. Hybrid configurations still serve peri-urban commuters, reflecting diminishing subsidies and rising compliance costs linked to tailpipe thresholds. Plug-in hybrids remain popular in mountainous provinces where cold-weather range retention is critical, yet their high complexity limits broader adoption.

Intensifying full-electric take-rate accelerates learning curves in e-axle assembly and inverter packaging, driving 5–7% annual unit-cost erosion. That scale enables small runabout vehicles at USD 10,000 retail to adopt magnet-free e-axles without price hikes, widening diffusion in tier-3 cities. The result is a reinforcing loop in which higher full-electric penetration magnifies addressable volumes for the China magnet-free electric axle system market.

By E-Axle Configuration: Integrated Systems Shrink Mass and Cost

Integrated e-axles captured 59.15% of 2024 shipments thanks to consolidated housings that place motor, gearbox, and inverter inside a single casing. Doing so trims 15 kg of mounting hardware and removes three high-voltage connectors, cutting both bill-of-materials and assembly time. Their 17.44% CAGR mirrors OEM hunger for chassis space freed up for larger battery footprints. Single-axle arrangements still dominate minicars priced below USD 12,000, but dual-axle variants are emerging in midsize SUVs to deliver on-demand all-wheel drive without a central propshaft.

Thermal integration remains the design sticking point: magnet-free motors run warmer because of higher current densities, yet innovative cold-plate routing and phase-change composite inserts now keep winding temperatures below 180 °C during peak load. Modular casings allow OEMs to mix induction motors for cost-sensitive trims and switched-reluctance units for torque-heavy variants without altering body-in-white mounts. The flexibility underpins the China magnet-free electric axle system market’s future scalability across diverse vehicle classes.

By Vehicle Type: Commercial Fleets Accelerate Adoption Curve

Passenger cars generated 73.46% of 2024 e-axle volumes, reflecting the country’s 12.9 million NEV sales milestone. Yet commercial vehicles—from last-mile vans to 18-ton rigid trucks—are poised to outpace with a 16.42% CAGR to 2030. Fleet-operator economics favor magnet-free systems that minimize rare-earth exposure and cut down time by leveraging rugged rotor designs. Light commercial vehicles post the fastest early adoption because duty cycles match the high-efficiency window of induction motors operating at partial load.

Medium and heavy trucks benefit from externally excited synchronous drives mated with 800-V battery systems that hold highway speeds at 2.8 kWh/km. GAC’s 30,000 RPM concept motor, achieving 98.5% peak efficiency, illustrates how speed-doubling gear stages can slash drive-train mass by 20 kg in refrigerated trucks, directly improving payload. As municipal clean-air mandates tighten and zero-emission zones proliferate, commercial buyers will continue to pull demand forward, cementing the China magnet-free electric axle system market leadership in fleet segments.

Geography Analysis

China’s magnet-free electric axle system market benefits from production clusters in Guangdong, Jiangsu, and Zhejiang that together yield a significant share of national e-axle output. Guangdong’s Pearl River Delta concentrates motor winding and power-module suppliers within a 100-km radius, compressing lead times to under eight days. Jiangsu leverages its entrenched precision-gear ecosystem to supply 60% of domestic reduction gears, while Zhejiang’s tooling specialists support rapid prototype iteration for medium-volume automakers. Proximity accelerates co-development cycles, allowing OEMs to refresh drivetrain variants every 24 months—half the global average.

Regional policy incentives magnify manufacturing advantages. Shenzhen refunds 15% of capital expenditure on SiC wafer lines, steering fabs to co-locate near e-axle integrators. Shanghai piloted carbon-intensity tradable quotas in 2024, rewarding suppliers that replace permanent-magnet motors with magnet-free alternatives, effectively monetizing embedded-emissions reductions. These measures funnel new investment into motor-control software labs, cementing the technical backbone of the China magnet-free electric axle system market.

Export potential is also rising. ASEAN import duty exemptions for Chinese e-axle subassemblies entered effect in 2025, and local content thresholds in Thailand and Indonesia classify control software as domestically added value when developed in Chinese R&D centers. As European CO₂ fleet-average rules tighten in 2027, several Chinese OEMs plan Hungary and Spain final-assembly plants relying on e-axles shipped from Yancheng and Ningbo, extending the China magnet-free electric axle system market footprint beyond national borders.

Mordor Intelligence provides coverage of the magnet free electric axle system market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India, South Korea, Japan, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

The China magnet-free electric axle system market shows moderate fragmentation. Domestic leaders BYD, GAC Components, and Shuanglin Group combine vertical battery and semiconductor integration with cost-efficient motor assembly lines. International suppliers ZF, Nidec, and BorgWarner defend their share through modular platforms that support multiple motor types and voltage classes. Competitive intensity pivots on software: firms race to patent control algorithms that suppress torque ripple and optimize inverter switching patterns.

Strategic partnerships flourish. BorgWarner secured four China-specific e-drive programs in June 2025, expanding its Wuhu footprint to 6 million units annual capacity [3]BorgWarner Press Room, “BorgWarner Wins Four China EV Programs,” BORGWARNER.COM. ZF added a Shenyang e-mobility plant in late 2024, complementing Shanghai and Hangzhou sites to cut logistics cost per unit by 18%. BYD leverages in-house SiC chips, permitting rapid cost downs and 12-week design-to-production cycles, a tempo few foreign rivals match.

Innovation white-space persists in high-speed rotor balancing, carbon-nanotube winding, and graphene-enhanced thermal interface materials. Start-ups such as YunDian Motors focus on AI-generated control code that iteratively refines itself via cloud-fleet telemetry. Early pilot fleets indicate 1.4% energy-saving over conventional static maps, signaling a shift toward over-the-air drivetrain upgrades that lock customers into proprietary software ecosystems. These developments collectively reinforce the dynamic, tech-centric profile of the China magnet-free electric axle system market.

China Magnet Free Electric Axle System Industry Leaders

ZF Friedrichshafen AG

Nidec Corporation

BYD Co. Ltd.

Magna International

Meritor (Cummins)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BorgWarner secured new electric-motor contracts with major Chinese OEMs and will double Wuhu plant capacity to serve platform-based e-axle programs.

- November 2024: ZF opened an e-mobility facility in Shenyang focused on modular electric-axle drives adaptable to multiple motor technologies.

China Magnet Free Electric Axle System Market Report Scope

| Externally Excited Synchronous Motors (EESM) |

| Induction Motors |

| Switched Reluctance Motors |

| Fully Electric Drive |

| Hybrid Drive |

| Plug-in Hybrid Drive |

| Single E-Axle |

| Dual E-Axle |

| Integrated E-Axle |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| By Motor Type | Externally Excited Synchronous Motors (EESM) | |

| Induction Motors | ||

| Switched Reluctance Motors | ||

| By Drive Type | Fully Electric Drive | |

| Hybrid Drive | ||

| Plug-in Hybrid Drive | ||

| By E-Axle Configuration | Single E-Axle | |

| Dual E-Axle | ||

| Integrated E-Axle | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUV and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

Key Questions Answered in the Report

What is the forecasted value of the China magnet-free electric axle system market in 2030?

The market is expected to reach USD 2.17 billion by 2030, growing at a 13.74% CAGR.

Which motor type currently holds the largest share?

Induction motors captured 45.12% of 2024 sales, leveraging mature manufacturing infrastructure.

How fast are switched-reluctance motors projected to grow?

Switched-reluctance motors are set to expand at a 15.13% CAGR between 2025 and 2030.

Why are integrated e-axles preferred by Chinese OEMs? |

Integrated e-axles cut mass, reduce connectors, and simplify thermal management, factors that drove 59.15% market share in 2024.

Page last updated on: