Automotive Axle And Propeller Shaft Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

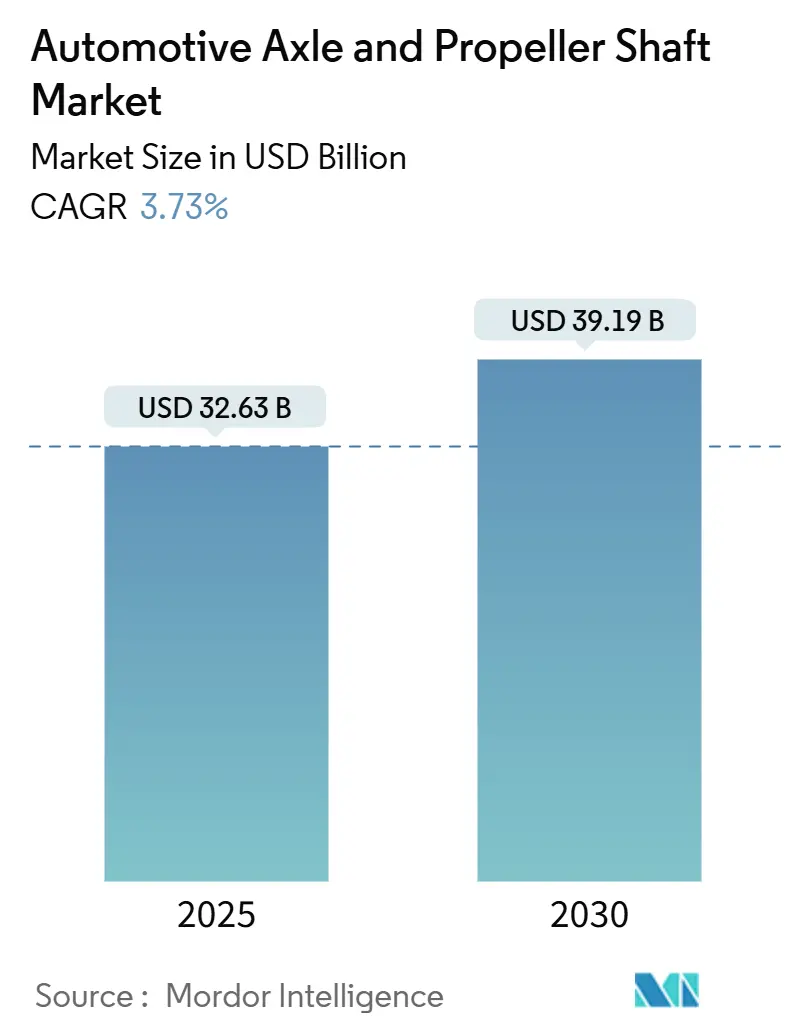

| Market Size (2025) | USD 32.63 Billion |

| Market Size (2030) | USD 39.19 Billion |

| Growth Rate (2025 - 2030) | 3.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Axle And Propeller Shaft Market Analysis by Mordor Intelligence

The automotive axle and propeller shaft market reached USD 32.63 billion in 2025 and is projected to expand at a 3.73% CAGR, lifting the automotive axle market size to USD 39.19 billion by 2030. Continuing vehicle-production recovery, simultaneous demand for traditional driveline architectures and e-axle configurations, and accelerating lightweight-material adoption underpin this steady growth. Passenger cars account for the bulk of global volume, yet commercial platforms lead electrification momentum, creating a two-speed product-development cycle. Asia-Pacific remains the center of gravity for supply and demand, while North American and European manufacturers retool around electric-vehicle (EV) programs emphasizing compact, integrated e-axles. Competitive intensity rises as established axle specialists consolidate to achieve scale and power-electronics players enter through in-wheel and modular motor systems. Suppliers that can deliver lightweight, sensor-enabled axles while meeting stringent noise, vibration, and harshness (NVH) regulations capture the most attractive margin pools.

Key Report Takeaways

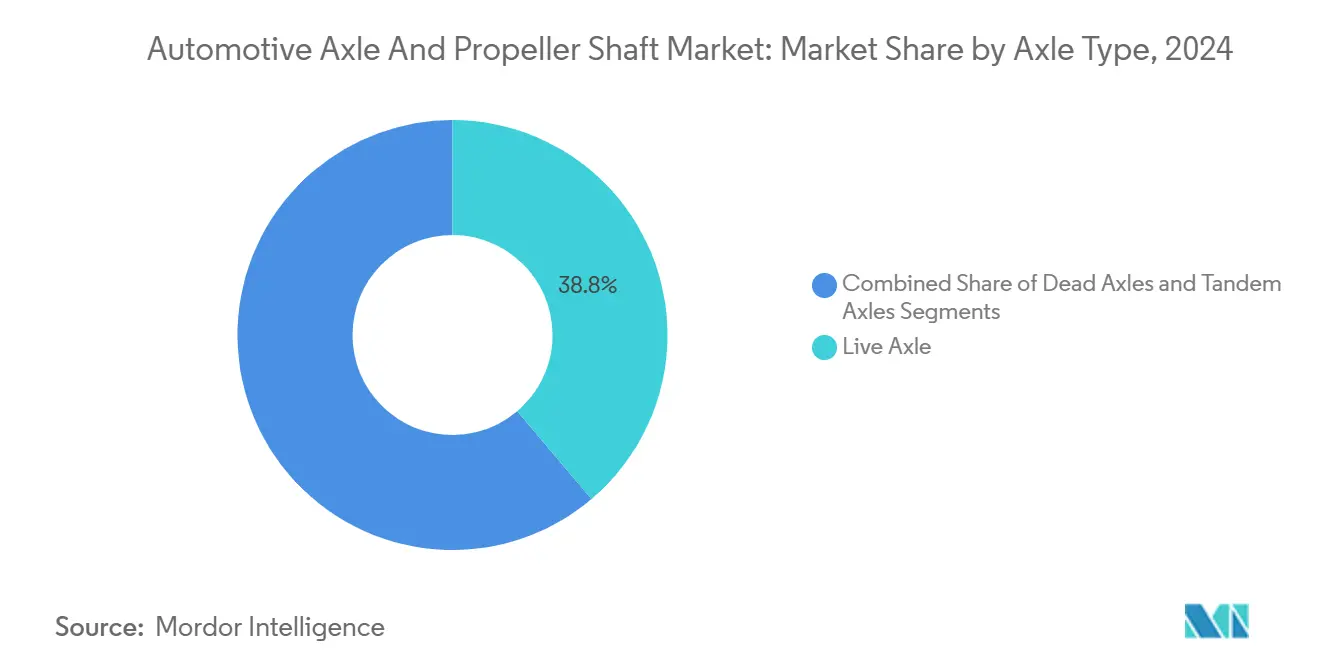

- By axle type, live axles led with a 38.81% automotive axle and propeller shaft market share in 2024 and are forecasted to post a 6.31% CAGR to 2030.

- By propeller-shaft type, single-piece shafts held 44.94% of the automotive axle and propeller shaft market size in 2024; multi-piece shafts are forecasted to advance at a 6.63% CAGR through 2030.

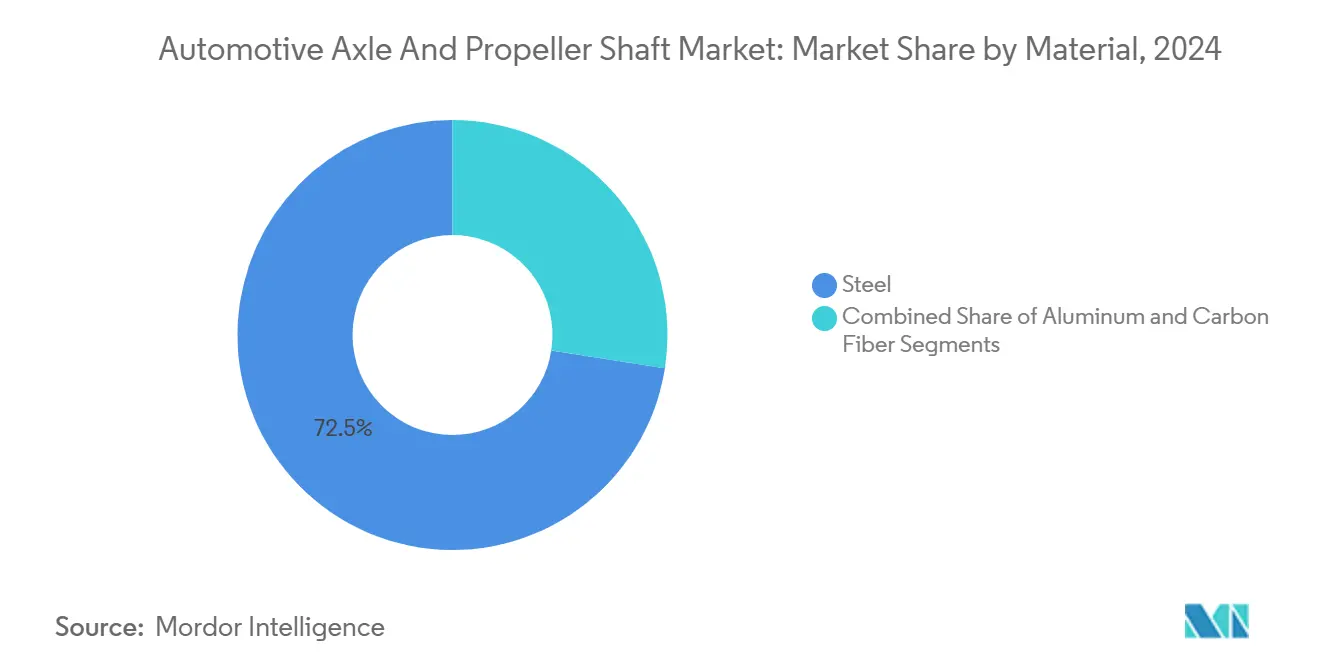

- By material, steel dominated with a 72.52% share of the automotive axle and propeller shaft market in 2024, whereas carbon fiber is projected to register a 7.28% CAGR to 2030.

- Front axles accounted for 46.98% of automotive axle and propeller shaft market revenue in 2024, while rear-axle demand is forecast to grow at a 6.39% CAGR through 2030.

- By vehicle type, passenger cars commanded 63.32% of the automotive axle and propeller shaft market size in 2024 and are forecasted to record the fastest 7.12% CAGR through 2030.

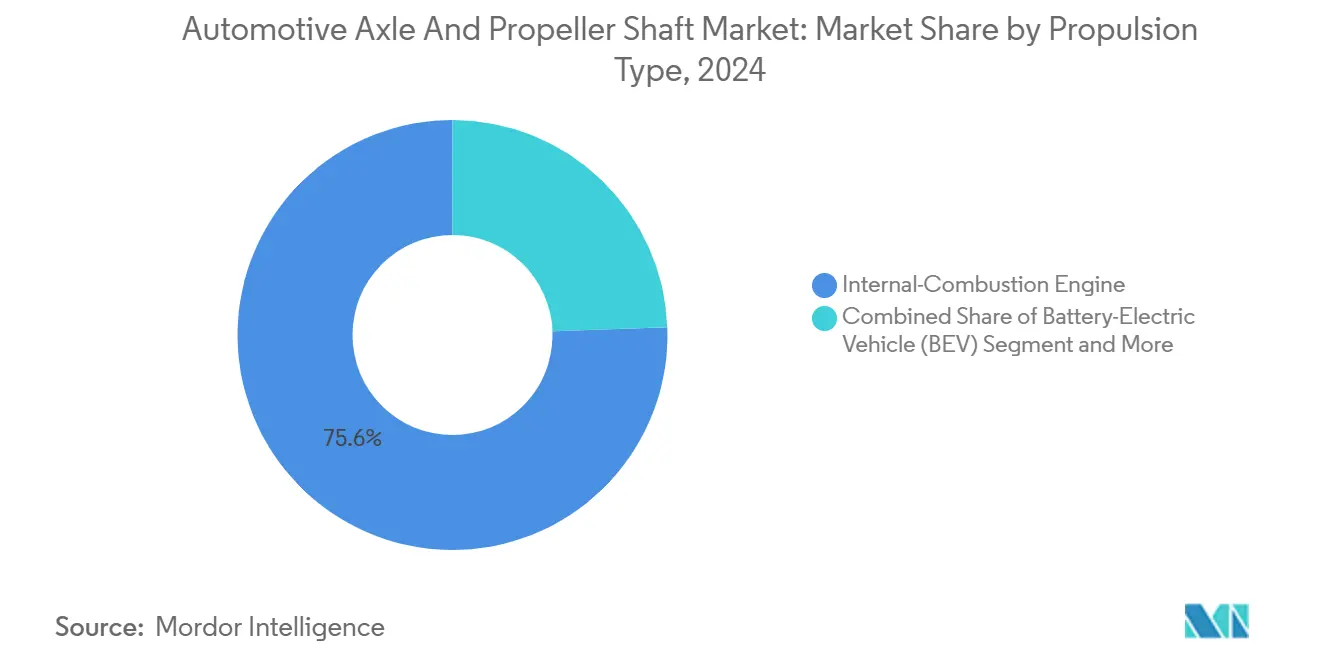

- By propulsion, ICE systems represented 75.58% of the automotive axle and propeller shaft market size in 2024, while battery-electric vehicles are forecasted to accelerate at a 12.79% CAGR over the forecast horizon.

- By distribution channel, OEMs controlled 80.69% of the automotive axle and propeller shaft market size in 2024, and the aftermarket is forecasted to grow at a 4.34% CAGR to 2030.

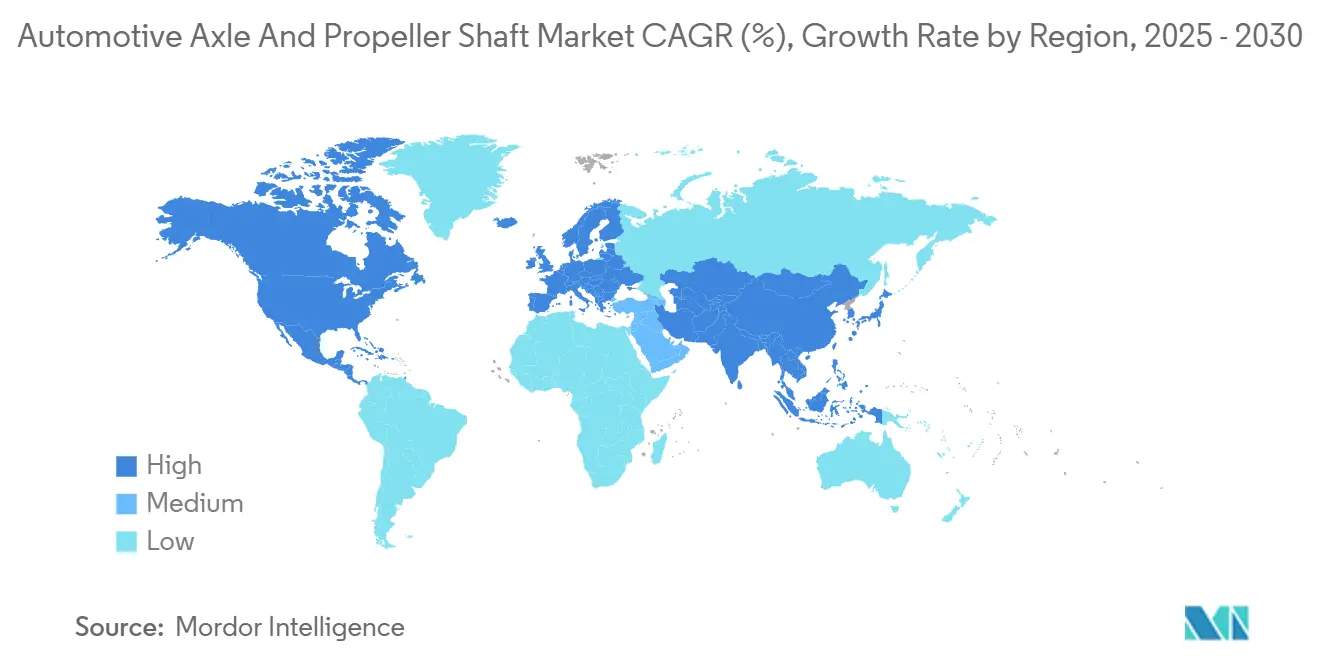

- By geography, Asia-Pacific contributed 49.02% of the automotive axle and propeller shaft market in 2024 and is projected to grow with a 4.93% CAGR to 2030.

Global Automotive Axle And Propeller Shaft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Push | +1.8% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| SUV / AWD Penetration | +1.2% | North America & EU core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Rising Vehicle and Power-train Production | +0.9% | Global, concentrated in major manufacturing hubs | Short term (≤ 2 years) |

| Regulatory Pressure | +0.7% | Europe, North America, with expanding to Asia-Pacific | Medium term (2-4 years) |

| Predictive-maintenance Service Revenue | +0.4% | North America & EU early adoption, global expansion | Long term (≥ 4 years) |

| Autonomous Delivery and Robo-taxi Platforms | +0.3% | Urban centers globally, pilot programs in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification Push Drives Lightweight E-Axle Integration

E-axle systems target 30-40% weight savings versus conventional assemblies, forcing platform engineers to combine motor, transmission, and power electronics inside compact housings while retaining torsional rigidity. Schaeffler’s new Ohio plant dedicated to 3-in-1 e-axles exemplifies capacity redeployment toward integrated units that serve both passenger and commercial EV programs[1]“Rigid Beam 3-in-1 E-Axle,” Schaeffler, schaeffler.us. Tier-1 suppliers run parallel production lines, one for traditional axles that support the sizeable ICE fleet and another for e-axles that meet automaker launch schedules. Functional-safety validation under ISO 26262 extends development cycles but creates entry barriers that shield compliant suppliers from low-cost competition. As EV penetration climbs, drivetrain content per vehicle rises because high-speed electric motors demand precision-machined gears, thermal-management jackets, and embedded sensors that feed predictive-maintenance platforms.

SUV and AWD Market Expansion Fuels Multi-Axle Demand

All-wheel-drive penetration in North America increased significantly in new-light-vehicle sales, with SUVs dominating this mix. Each AWD application requires both front and rear axle assemblies, and premium models layer torque-vectoring functions that mandate higher-specification differential housings. The shift toward electrified AWD introduces independent front and rear e-axles that elevate per-vehicle axle count. Heavy-duty trucks also migrate toward tandem setups as regulators authorize larger gross vehicle weights in exchange for added axles, boosting demand for high-torque live axles and robust propeller shafts.

Post-Pandemic Production Recovery Stabilizes Component Demand

Global light-vehicle output resumed its upward trajectory in 2024, and the United States assemblies rebounded, restoring predictability to axle order books. Asian producers lead volume gains, whereas European OEMs prioritize launch capacity for premium electric crossovers that command high-specification driveline components. Stabilized production schedules enable suppliers to increase automation investments deferred during semiconductor shortages, while nearshoring in North America shortens logistics chains and cushions raw-material volatility.

Fuel-Economy Regulations Accelerate Lightweight-Material Adoption

Tighter global efficiency standards boost aluminum and carbon-fiber shaft penetration, as each kilogram saved translates into quantifiable CO₂ compliance credits. EU Regulation 540/2014 further drives composite uptake by capping exterior noise levels, incentives that favor materials delivering both mass and NVH benefits[2]“Noise Reduction Rules,” European Commission, ec.europa.eu. Suppliers with in-house composite capabilities secure early design wins in premium EVs, while cost scales improve to support mid-segment adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility | -0.8% | Global, with particular impact on cost-sensitive markets | Short term (≤ 2 years) |

| Supply Bottlenecks | -0.6% | Global, affecting premium and performance segments | Medium term (2-4 years) |

| Shift Toward In-wheel Motors | -0.4% | Early adoption in urban mobility and premium EVs | Long term (≥ 4 years) |

| NVH Emission Limits | -0.3% | Europe leading, expanding to other developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Material Price Volatility Pressures Supplier Profitability

Raw materials represent upward trajectory of axle production cost, and recent swings in steel and aluminum pricing compress already-thin margins. Integrated steelmakers pass-through surcharges, yet independent axle fabricators often lock into fixed-price contracts, exposing them to spot-market gyrations. Suppliers respond by trimming contract durations, adopting indexed price clauses, and intensifying hedging programs, but OEM cost-reduction mandates restrict full recovery of inflationary spikes.

Carbon-Fiber Supply Constraints Limit Lightweight-Shaft Scaling

Projected precursor shortfalls by 2026, and the capital cost of new production lines keeps leading to long lead times. Automakers, therefore, triage allocations toward high-performance trims, slowing penetration in volume segments despite compelling weight and NVH advantages. Suppliers with secured feedstock or backward integration lock in premium programs, while late entrants struggle to win orders that hinge on assured composite supply. Manufacturing complexity compounds the challenge, with new carbon fiber production lines requiring significant investments and multi-year lead times that cannot quickly respond to demand fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Axle Type: Live Axles Retain Heavy-Duty Preeminence

Live axles captured 38.81% share of the automotive axle and propeller shaft market in 2024 as their rugged beam construction withstands payload, tow, and off-road requirements in pickup and commercial segments. The configuration’s adaptivity to e-motor packaging underpins a 6.31% CAGR to 2030, lifting live-axle value contribution within the automotive axle market. Modular housings now integrate high-speed electric motors, silicon-carbide inverters, and thermal channels while preserving drop-in compatibility for OEM frame designs.

Demand for dead axles persists in load-bearing trailer applications, yet incremental growth concentrates in tandem assemblies where regulatory weight credits reward multi-axle layouts. Suppliers refine welding processes and employ high-strength-low-alloy (HSLA) steels that shave curb mass without sacrificing durability. With electrified trucks adding battery weight, live axles face renewed payload demands, further reinforcing their dominant share of the automotive axle market.

By Propeller Shaft Type: Single-Piece Simplicity Meets Multi-Piece Versatility

Single-piece shafts held 44.94% of the automotive axle and propeller shaft market's 2024 revenue, owing to simple fabrication and lower cost for wheelbases under 3.2 meters. Upcoming compact EV architectures with integrated e-axles may forgo propshafts altogether, but hybrid and conventional SUVs still require robust tubular designs. Multi-piece assemblies, however, post a 6.63% CAGR through 2030 because longer pickup, van, and bus platforms need center supports to control critical-speed vibration, and carbon-fiber versions mitigate the mass penalty.

Slip-type shafts, although niche, remain vital safety components that collapse under frontal impact, protecting occupants in high-speed collisions. Suppliers now offer slip-joint modules with thermoplastic boots that tolerate higher articulation angles demanded by raised-ride-height crossovers. The emergence of over-the-air (OTA) driveline-health monitoring means many shafts ship with embedded acceleration sensors that feed predictive-maintenance dashboards, redefining the automotive axle industry's after-sales proposition.

By Material: Steel Dominates While Carbon Fiber Scales

Steel maintained a 72.52% share of the automotive axle and propeller shaft market in 2024 owing to its unmatched cost-performance ratio, but lightweight directives accelerate the carbon-fiber segment’s 7.28% CAGR through 2030. Suppliers leverage robot-wound carbon pre-forms and snap-cure resin systems that cut cycle times below four minutes, unlocking medium-volume feasibility. Aluminum offers a mid-tier solution where corrosion resistance and weight savings outweigh incremental cost, especially in ladder-frame EV pickups that inherit heavy battery packs.

Precursor bottlenecks and recycling hurdles constrain composite adoption; nevertheless, OEMs pilot cradle-to-cradle programs that reclaim fiber for second-life non-structural parts. Component validation follows stringent torsional-fatigue and stone-impingement standards, extending test cycles but assuring longevity under harsh duty. Net-shape forging of steel still underpins mainstream output, yet alloy-microalloy optimization and advanced quench-press tempering allow weight trims even in legacy material choices.

By Application: Front Axles Lead, Rear Axles Accelerate

Front-wheel-drive (FWD) packaging kept front axles at 46.98% of the automotive axle and propeller shaft market in 2024. But rear applications advance at 6.39% CAGR as crossover AWD penetration climbs. Electrified rear axles house independently controlled motors that enable torque vectoring without mechanical props, boosting handling and regenerative-braking efficiency.

Prop-shaft applications fluctuate with platform mix; battery-electric skateboards often delete central shafts, whereas plug-in hybrids employ shortened units to couple front engines with rear e-motors. Suppliers diversify application portfolios, integrating disconnect clutches that decouple rear axles under steady-state cruising to trim parasitic losses. Lifecycle economics now factor software-enabled functions such as trailer-sway mitigation and adaptive ride-height that rely on axle-mounted sensors.

By Vehicle Type: Passenger-Car Volume Dominance Meets Commercial-Vehicle Momentum

Passenger vehicles commanded 63.32% of the automotive axle and propeller shaft market size in 2024, because compact cars, sedans, and crossovers still account for most worldwide production. This high base means growth is steadier than spectacular, yet the segment is projected to log a respectable 7.12% CAGR through 2030 as affordability programs in Asia expand entry-level car ownership. Content per vehicle keeps climbing: modern crossovers pair higher ride heights with optional all-wheel-drive systems that add rear axles, and premium trims increasingly integrate torque-vectoring e-axles sold at margin-rich prices. Automakers also widen hybrid offerings that couple front ICE powertrains with rear electric axles, driving incremental demand even within a single platform. Innovations such as corner modules with built-in steering actuators further elevate axle complexity, pushing suppliers to refine lightweight beam designs that maintain durability while trimming mass.

Light commercial vehicles (LCVs), medium trucks, and heavy commercial vehicles (M&HCVs) together hold the remaining 36.68% share but generate greater revenue per chassis thanks to multi-axle layouts and higher torque ratings. Electrification accelerates fastest in this fleet segment because government incentives target zero-emission delivery vans and municipal buses, prompting OEMs to specify integrated 3-in-1 e-axles with peak outputs surpassing 250 kW. Tandem live axles proliferate as regulators allow heavier gross vehicle weights in exchange for extra axle count, advancing the automotive axle market size in the vocational-truck niche. Suppliers respond with modular housings that accept either traditional differentials or electric drive units, so fleet operators can migrate from diesel to battery power without re-engineering the entire chassis.

By Propulsion Type: Dual-Track Investment Across ICE and EV Programs

Internal-combustion-engine (ICE) vehicles retained a 75.58% share of the automotive axle and propeller shaft market in 2024, reflecting the vast installed base and ongoing production in cost-sensitive markets that still prioritize low sticker prices and long refueling range. Even here, axle specs evolve; lightweight steel alloys and optimized hypoid-gear geometries help OEMs squeeze every gram of CO₂ compliance from conventional drivelines. Tier-1s keep capital flowing to ICE lines to serve warranty-cycle replacements and emerging-market launches, yet they hedge with flexible machining cells that can swing to electric housings on short notice. Retrofit hybrids also sustain ICE-axle orders by combining mechanical differentials with compact e-motors that attach to existing casings. As a result, ICE may shrink proportionally but continues to provide critical fixed-cost absorption across the supply chain.

Battery-electric vehicles (BEVs) grow at a striking 12.79% CAGR to 2030, driving an equally brisk ramp in specialized e-axles that integrate motor, inverter, and reduction gear within a sealed unit. These systems demand higher thermal conductivity alloys and embedded coolant jackets, raising the bill of materials even as unit counts climb. Hybrid-electric and plug-in-hybrid models add complexity by requiring both conventional front axles and electrified rear modules, effectively doubling axle content per vehicle in some architectures. Fuel-cell-electric prototypes remain niche but specify ultra-lightweight carbon-fiber shafts to offset onboard hydrogen-tank mass, carving a profitable micro-segment for advanced-material suppliers. Consequently, axle makers must balance parallel R&D roadmaps, ensuring that breakthroughs in silicon-carbide power electronics or composite housings can cascade across multiple propulsion variants without cannibalizing existing revenue streams.

By Distribution Channel: OEM Control Persists While Aftermarket Evolves

Original-equipment-manufacturer (OEM) contracts captured 80.69% share of the automotive axle and propeller shaft market in 2024, as axles remain core safety components locked in during the earliest platform-development gates. Automakers favor long-term sourcing agreements that bundle design collaboration, just-in-sequence delivery, and functional-safety validation, creating high switching costs once a program enters series production. Suppliers invest in geographically diversified plants that mirror their customers’ final-assembly footprints, safeguarding continuity against geopolitical shocks. OEMs increasingly request software-defined features, such as drive-mode-select algorithms, embedded directly in axle controllers, cementing the supplier relationship for the vehicle’s entire life cycle. These deep integrations ensure that the automotive axle market share of OEM channels will remain dominant through the forecast horizon.

The aftermarket, though smaller, is on track for a 4.34% CAGR through 2030 as the global fleet ages and EV service complexity rises. Remanufactured e-axles, replacement constant-velocity joints, and over-the-air calibration packages form a growing product suite that commands premium prices. Tier-1s now market vehicle-lifetime solutions, shipping tool kits and cloud dashboards that independent garages subscribe to for diagnostics and predictive-maintenance insights. Regulation also plays a role; right-to-repair legislation in North America obliges OEMs to share service data, enabling more players to stock certified parts, yet raising the bar for technical training. Consequently, distribution strategies become omnichannel: factory-authorized service centers handle high-voltage disassembly, while e-commerce storefronts supply mechanical wear parts, ensuring that even a modest slice of the automotive axle market size remains profitable for agile participants.

Geography Analysis

Asia-Pacific’s 49.02% share of the automotive axle and propeller shaft market in 2024 is projected to grow at a CAGR of 4.93% through 2030, illustrating the region’s vertically integrated supply chains, abundant skilled labor, and high domestic vehicle demand. China’s extensive supplier base minimizes logistics costs, while India’s component exports expand to key assemblers on the back of tariff-free corridors. South Korea and Japan leverage advanced metallurgy and automation to retain premium programs as wages rise. Government incentives for EV production accelerate e-axle localization, prompting global suppliers to establish joint ventures and technology-transfer agreements.

North America enjoys a steady growth as nearshoring incentives attract axle casting and machining investments to Mexico and the United States. USMCA local-content rules direct program awards toward regional suppliers, and multi-billion-dollar EV truck programs require differential, gearbox, and shaft sub-assemblies that cannot tolerate trans-Pacific supply risk. Canada’s proximity to Great Lakes iron-ore routes anchors integrated steel-axle output, and recent grid modernization grants open opportunities for green powdered-metal sinter forging.

Europe's growth is driven by premium EV crossover launches that consume lightweight live axles, carbon-fiber shafts, and integrated e-drive electronics. Stringent CO₂ and noise-emission rules speed aluminum substitution, and circular-economy mandates push remanufacturing and closed-loop recycling of axle housings. Balkan-state foundries win volume contracts thanks to competitive energy costs and modern robotic molding lines. At the same time, Western European suppliers concentrate on high-speed machining of differential gears for performance EVs.

Competitive Landscape

The automotive axle and propeller shaft market exhibits moderate concentration, creating competitive dynamics that balance scale advantages with regional specialization opportunities. Following its acquisition of Dowlais Group, American Axle & Manufacturing leads, consolidating product lines and R&D while expanding e-axle offerings. Dana Incorporated occupies a pivotal position owing to its diversified propshaft and axle portfolio and global footprint that straddles ICE and EV programs. ZF and several Japanese suppliers restructure via joint ventures, pooling EV motor, inverter, and gearbox expertise to deliver turnkey e-axles that assure OEMs of single-source accountability.

New entrants from the semiconductor and advanced-materials sectors target in-wheel motors and carbon-fiber composite shafts, leveraging proprietary technologies to bypass conventional machining. Patent filings in integrated cooling jackets, silicon-carbide power stages, and additive-manufactured differential cages illustrate the escalating intellectual-property race. Tier-1s respond by embedding vibration sensors and AI-driven prognostics into axle housings, creating data-service revenue streams that complement metal-bending margins.

Suppliers also pursue vertical integration into raw-material processing to tame cost volatility. Steelmakers offer tailored alloy chemistries, while carbon-fiber producers sign long-term offtake agreements with axle specialists to stabilize precursor supply. Regions with renewable-energy surpluses attract green-steel investments, aligning sustainability credentials with OEM decarbonization targets and reinforcing competitive positioning in the automotive axle market.

Automotive Axle And Propeller Shaft Industry Leaders

Dana Incorporated

ZF Friedrichshafen AG

Meritor Inc.

GKN Automotive Limited

American Axle and Manufacturing Inc. (AAM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Maruti Suzuki confirmed its e-Vitara electric SUV will debut a locally sourced front e-axle supplied under a technology-transfer agreement with BluE Nexus.

- December 2024: Dana unveiled the AdvanTEK 40 Pro tandem axle, featuring a 2.05 ratio geared for advanced engine down-speeding and optional e-drive integration.

- October 2024: Bharat Forge acquired American Axle's Indian commercial-vehicle axle operation for USD 65 million, allowing American Axle to channel its capital towards e-axle programs.

- October 2024: MOOG unveiled a new CV-axle line, engineered explicitly for performance-tuned crossovers. This product line focuses on delivering enhanced durability and reliability, catering to the demanding requirements of high-performance vehicles. By prioritizing an extended service life, MOOG aims to address the needs of consumers seeking long-lasting and efficient solutions for their crossover vehicles.

Global Automotive Axle And Propeller Shaft Market Report Scope

| Driven / Live Axles |

| Non-Driven / Dead Axles |

| Tandem Axles |

| Single-Piece Shaft |

| Multi-Piece Shaft |

| Slip-Type Shaft |

| Steel |

| Aluminum |

| Carbon Fibre |

| Front Axle |

| Rear Axle |

| Propeller Shaft |

| Passenger Car |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal-Combustion Engine |

| Battery-Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Axle Type | Driven / Live Axles | |

| Non-Driven / Dead Axles | ||

| Tandem Axles | ||

| By Propeller Shaft Type | Single-Piece Shaft | |

| Multi-Piece Shaft | ||

| Slip-Type Shaft | ||

| By Material | Steel | |

| Aluminum | ||

| Carbon Fibre | ||

| By Application | Front Axle | |

| Rear Axle | ||

| Propeller Shaft | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal-Combustion Engine | |

| Battery-Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive axle market by 2030?

The automotive axle market size is expected to reach USD 39.19 billion by 2030.

Which region currently contributes the largest share of global axle revenue?

Asia-Pacific holds 49.02% of global sales on the strength of its integrated supply chain and domestic vehicle demand.

Which axle type will grow fastest through 2030?

Tandem live axles are set to expand at a 6.31% CAGR, reflecting heavier payload requirements in trucks.

How will electrification affect propeller-shaft demand?

Battery-electric architectures reduce prop-shaft count in some platforms, yet hybrid SUVs and long-wheelbase vans sustain multi-piece shaft demand at a 6.63% CAGR.

What materials are gaining traction to meet weight-reduction mandates?

Carbon fiber leads material growth with a 7.28% CAGR, followed by aluminum, as OEMs pursue both mass and NVH benefits.

What is driving aftermarket growth for axles and shafts?

An aging fleet and the complexity of e-axle maintenance boost aftermarket revenue at a 4.34% CAGR, especially for sensor-enabled service kits.

Page last updated on: