Magnet Free Electric Axle System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

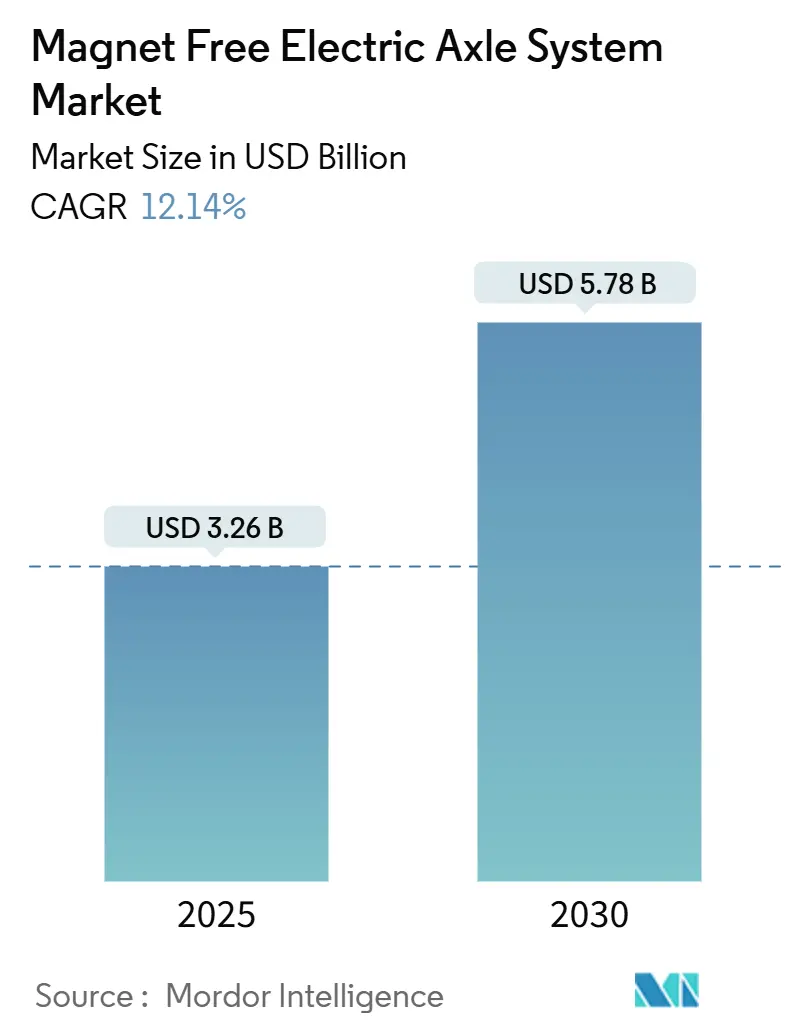

| Market Size (2025) | USD 3.26 Billion |

| Market Size (2030) | USD 5.78 Billion |

| Growth Rate (2025 - 2030) | 12.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnet Free Electric Axle System Market Analysis by Mordor Intelligence

The Magnet Free Electric Axle System market size is USD 3.26 billion in 2025 and is forecast to reach USD 5.78 billion by 2030, advancing at a 12.14% CAGR over the period. This growth reflects a decisive move away from rare earth reliance as supply-chain exposure and sustainability targets reshape powertrain strategies across all major vehicle classes. The Magnet Free Electric Axle System market is benefiting from cost-competitive, magnet-independent motor architectures, regulatory incentives that reward material substitution, and rapid advances in high-silicon electrical steels that close the efficiency gap with permanent-magnet units. OEM investments now prioritize externally excited and switched reluctance designs, while Tier 1 suppliers integrate motor, inverter, and gearbox functions to unlock packaging advantages. Unlocking circular-economy value from fully recyclable drivetrains further accelerates mainstream acceptance, especially among fleet operators sensitive to lifetime operating costs. Competitive intensity is rising as traditional transmission specialists, semiconductor vendors, and materials innovators contest the same white-space opportunities.

Key Report Takeaways

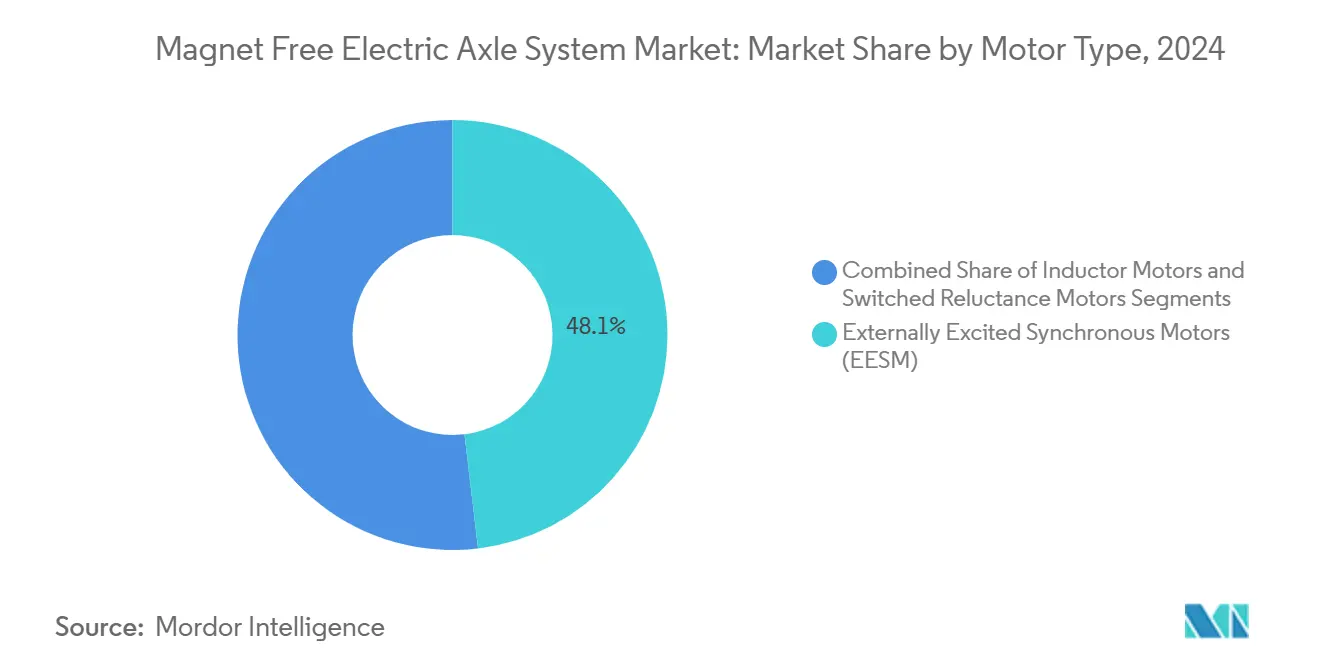

- By motor type, externally excited synchronous motors led with 48.13% Magnet Free Electric Axle System market share in 2024, while switched reluctance motors are projected to grow at 14.17% CAGR through 2030.

- By drive type, hybrid architectures accounted for 57.22% of the Magnet Free Electric Axle System market size in 2024, and fully electric drives are set to expand at a 17.64% CAGR over 2025-2030.

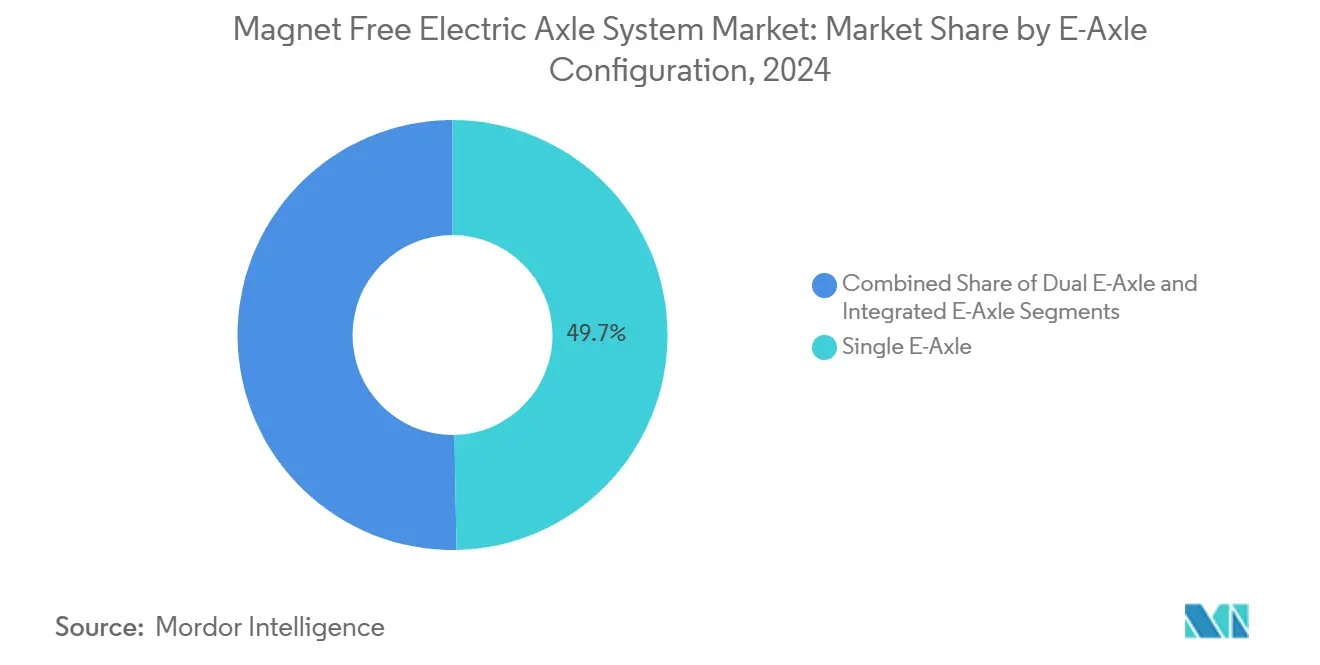

- By e-axle configuration, single e-axles held 49.65% share of the Magnet Free Electric Axle System market size in 2024; dual e-axles are forecast to record a 16.61% CAGR to 2030.

- By vehicle type, passenger cars captured 57.33% Magnet Free Electric Axle System market share in 2024, whereas commercial vehicles will advance at 15.29% CAGR through 2030.

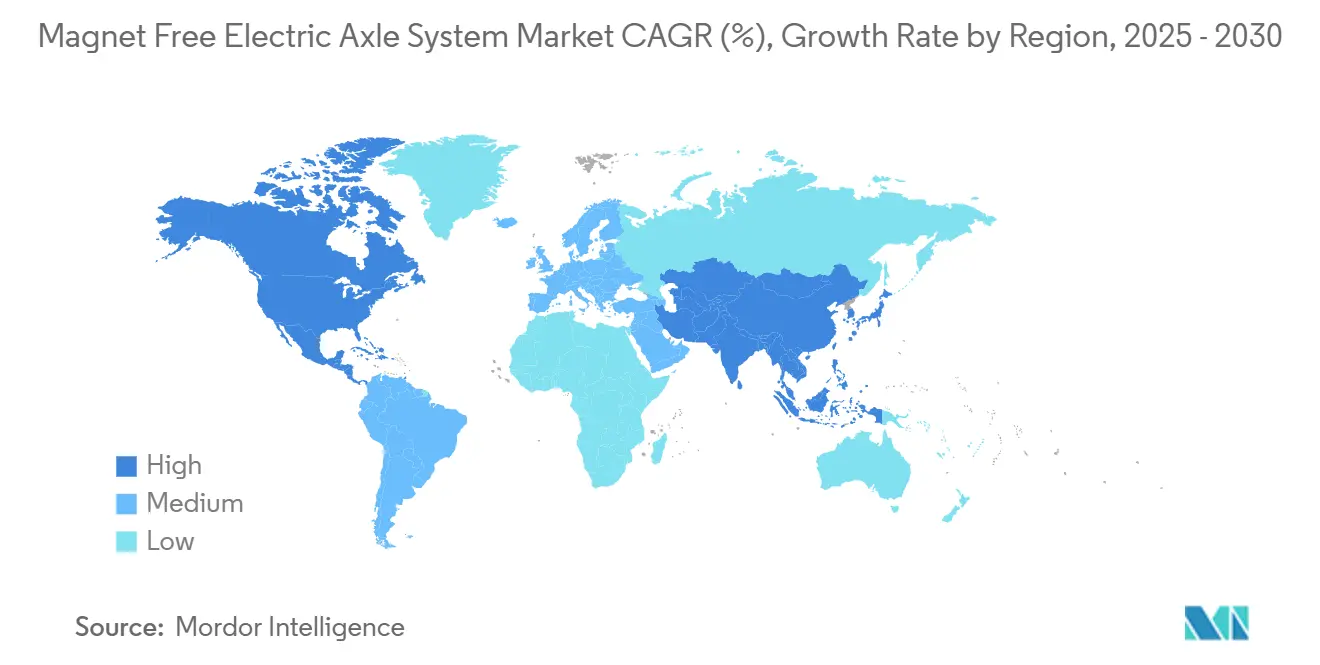

- By geography, Asia-Pacific represented 44.61% of 2024 revenue and is set to grow at a 15.71% CAGR to 2030, giving it the fastest regional trajectory within the Magnet Free Electric Axle System market.

Global Magnet Free Electric Axle System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rare-Earth Supply Chain Security | +2.8% | North America, EU, APAC | Medium term (2-4 years) |

| Lower Lifetime Cost Than PM E-Axles | +2.1% | Global (early adoption in commercial fleets) | Short term (≤2 years) |

| OEM Carbon-Neutral & ESG Goals | +1.9% | Europe, North America | Long term (≥4 years) |

| Incentives for Non-Rare-Earth Motors | +1.6% | North America, EU, spillover to APAC | Medium term (2-4 years) |

| High-Si Electrical Steel Breakthroughs | +1.4% | APAC manufacturing hubs | Long term (≥4 years) |

| Demand for Recyclable Powertrains | +1.0% | EU, North America, and developed APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Security from Rare-Earth Independence

China controlled 69% of global rare earth mine output in 2024, making magnet supply a strategic vulnerability for automakers. A single-motor EV contains roughly 550 grams of rare earth metals, a volume that multiplies exposure compared with ICE vehicles [1]U.S. Department of Homeland Security, “Supply Chain Risk Report 2024,” dhs.gov. U.S. national-security reviews have now flagged magnet dependence as a critical risk, prompting legislation that backs domestic substitutes. India’s USD 602 million scheme to lift local rare earth mining mirrors similar efforts aimed at insulating supply chains. Tesla’s next-generation drive unit, announced in 2024, eliminates rare earth magnets, validating industrial-scale alternatives. These geopolitical realities elevate magnet-free architectures from cost play to supply-assurance imperative within the Magnet Free Electric Axle System market.

Lower Lifetime Cost Versus PM E-Axles

Total-cost-of-ownership modeling confirms that aluminum-wound magnet-free motors cut propulsion costs by up to 60% against standard PM units under volatile neodymium pricing. Cost parity tightens further as economies of scale favor abundant materials such as iron and aluminum. Magna’s 800 V eDrive trims rare earth content while cutting CO₂ by 20% relative to its prior platform, signaling dual economic and environmental benefits [2]Magna International, “Next-generation 800V eDrive,” magna.com. Switched reluctance topologies avoid demagnetization at high temperatures, reducing thermal-management spend in heavy-duty cycles. BorgWarner’s Ultra-Short Hairpin design shrinks copper use and motor mass, raising material efficiency as volumes increase. These economics underpin wider Magnet Free Electric Axle System market adoption across both passenger and commercial programs.

OEM Carbon-Neutral Targets and ESG Mandates

Ford commits USD 50 billion to electrification through 2026 and explicitly links that spend to sustainable material sourcing. Stellantis’ Dare Forward 2030 plan aims for net-zero by 2038, anchoring drivetrain decisions to circular-economy metrics. Mercedes-Benz pursues Ambition 2039, covering CO₂-neutral operations across 30 manufacturing plants worldwide. General Motors channels USD 27 billion into zero-tailpipe vehicles by 2035, tying procurement criteria to lifecycle emissions. ESG scoring frameworks increasingly penalize rare earth mining’s ecological toll, pushing OEMs toward magnet-free e-axles that align with investor expectations. As a result, decarbonization goals materially bolster demand in the Magnet Free Electric Axle System market.

Regulatory Incentives Favoring Non-Rare-Earth Motors

The U.S. Rare Earth Magnet Security Act proposes a production tax credit that directly subsidizes domestically sourced magnet alternatives. European Regulation 2019/1781 enforces IE4 efficiency from July 2023 on 75–200 kW motors, indirectly steering design away from neodymium magnets [3]European Commission, “Regulation 2019/1781 motor efficiency,” ec.europa.eu. The measure promises 110 TWh energy savings and 40 million t annual CO₂ cuts by 2030. India’s critical-materials roadmap similarly aligns incentives with local magnet production targets. The European Raw Materials Alliance now pools public-private capital for rare-earth-light technologies. Cross-regional policy convergence provides a powerful pull that accelerates the Magnet Free Electric Axle System market beyond pure cost drivers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower Power/Torque Density | -1.8% | Global (performance vehicle focus) | Short term (≤2 years) |

| Higher Noise & Torque Ripple | -1.2% | Global (passenger cars) | Medium term (2-4 years) |

| High-Frequency Inverter Losses | -0.9% | Global (high-power e-axles) | Medium term (2-4 years) |

| SRM Control Software IP Limits | -0.7% | Regionally varied patent landscapes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Lower Power/Torque Density Versus PM Motors

Permanent-magnet machines exceed 5 kW/kg, while magnet-free architectures often deliver 3–4 kW/kg, requiring larger housings that strain compact vehicle packaging. MAHLE’s rare-earth-free unit posts 96% efficiency but relies on advanced cooling to offset lower flux density. ZF’s I²SM shows comparable output yet still faces packaging constraints in small electric sedans. High-performance segments, where every kilogram counts, continue to favor PM solutions. Induction motors powering 50 kW often weigh well above 200 kg, dwarfing equivalent PM units. Bridging this density gap demands further R&D and remains a headwind for the Magnet Free Electric Axle System market.

Higher Acoustic and Torque Ripple Issues

Switched reluctance designs generate intrinsic torque ripple due to their doubly salient topology, leading to vibration that degrades cabin NVH unless mitigated. Advanced control techniques curtail ripple by 30% but impose processing overhead and an increase in inverter cost. Axial-gap SRMs promise better acoustic signatures yet require sophisticated electromagnetic force balancing. Comparative studies still rank PM synchronous motors quieter across typical driving profiles. Random-frequency PWM and current-tail shaping cut noise but raise implementation complexity. Passenger-car brands that prioritize refinement, therefore, move cautiously, slowing Magnet Free Electric Axle System market penetration in premium segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Innovation Anchors EESM Leadership

Externally excited synchronous motors held 48.13% of the Magnet Free Electric Axle System market share in 2024, underscoring their blend of high efficiency and precise field control. Switched reluctance motors are set to log a 14.17% CAGR to 2030, thanks to rugged construction and attractive cost curves for commercial fleets. Induction motors continue to serve cost-sensitive applications, although their lower peak efficiency limits uptake in premium passenger segments. ZF’s inductively excited I²SM earned the 2024 CLEPA Innovation Award for matching PM performance without rare earth content, demonstrating how smart excitation bridges historical efficiency gaps. Vitesco’s magnet-free rotor trims global-warming potential, illustrating that sustainability advantages can stand alongside performance gains.

Continuous advances in control electronics reinforce EESM’s market command. Multi-phase inverters with field-oriented control modulate excitation on the fly, maintaining optimal efficiency under varying torque loads. Segment leaders also apply high-bandwidth flux observers that mitigate demagnetization risk under transient overloads. As a result, OEMs increasingly specify EESM for next-generation skateboard platforms that demand both efficiency and flexible packaging. Switched reluctance prospects remain bright as improvements in acoustic signatures unfold through physics-based predictive controllers. The Magnet Free Electric Axle System market, therefore, balances mature EESM volumes with fast-growing SRM demand, creating diversified revenue streams for suppliers.

By Drive Type: Hybrid Flexibility Sustains Volumes

Hybrid drive configurations owned 57.22% of 2024 revenue, reflecting OEM hedging behavior during charging-infrastructure build-out. Fully electric drive lines will climb at 17.64% CAGR through 2030 as batteries scale energy density and cost per kWh declines. Plug-in hybrids continue to support rural and long-haul use cases where fast-charging availability lags. Magna’s DHD Duo hybrid pairs dual e-motors with a multi-speed transmission, packaging magnet-free motors into an 800 V system that debuts in Q3 2025 production for Chinese OEM programs. BorgWarner’s new hybrid eMotor deal with a North American truck maker underscores how fleet operators leverage blended propulsion to meet duty-cycle diversity.

Hybrid platforms are pivotal stepping stones for the Magnet Free Electric Axle System industry, giving suppliers volume that drives down the bill of materials for fully electric variants. 3-in-1 integration of motor, inverter, and reduction gear reduces wiring harnesses and shrinks assembly footprints, benefiting both hybrid and battery electric builds. Regulatory frameworks that count electric mileage within carbon compliance schemes further lock in hybrid demand until public charging networks mature across emerging markets. Consequently, hybrid momentum sustains Magnet Free Electric Axle System market volumes even as the long-term horizon tilts toward pure battery electric drivetrains.

By E-Axle Configuration: Integration Yields Efficiency

Single e-axle solutions captured 49.65% of 2024 shipments by offering cost-effective propulsion for compact and midsize passenger cars. Dual e-axle systems, projecting a 16.61% CAGR, satisfy all-wheel-drive performance requirements in luxury crossovers and light commercial vans. Integrated 3-in-1 e-axles compress motor, inverter, and gearbox into one casting, slicing weight and assembly steps. American Axle & Manufacturing’s modular unit, awarded production status at Stellantis, reduces parts count by 30% while boosting manufacturability. ZF’s holistic platform standardizes mechanical interfaces but lets OEMs swap motor technologies, easing design reuse across model families.

Packaging and thermal benefits multiply when magnet-free motors are chosen. Eliminating demagnetization risk allows higher operating temperatures, enabling smaller cooling jackets and tighter installation envelopes. High-voltage architectures elevate partial-load efficiency, critical for long-haul duty cycles. As automakers adopt skateboard chassis with flat battery packs, the ability to mount thin integrated e-axles above or below the deck gains importance. These dynamics reinforce the Magnet Free Electric Axle System market’s shift toward highly integrated dual-axle layouts in performance and commercial segments while single-axle systems remain mainstream for cost-sensitive passenger programs.

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars retained 57.33% Magnet Free Electric Axle System market share in 2024, yet commercial vehicles will post a 15.29% CAGR owing to fleet electrification mandates. Urban delivery vans and heavy-duty trucks face tightening emission standards and total-cost-of-ownership scrutiny, making magnet-free technology’s lifetime maintenance savings appealing. ZF booked EUR 5 billion in commercial orders and expects e-axle output to double year on year, spotlighting market traction among logistics providers. The TrailTrax electrified trailer reduces diesel truck CO₂ by 40% and extends range up to 16%, demonstrating auxiliary electrification use-cases that sit outside conventional power units.

Chinese OEMs such as GAC and Great Wall lock hybrid pickup and light truck awards with BorgWarner’s magnet-free e-motors for 2025 rollouts. Municipal bus fleets in Europe and North America also pivot, capitalizing on simpler motor recycling at end-of-life. Passenger SUVs and multipurpose vehicles, benefiting from ample underbody space, more readily accommodate larger magnet-free housings. Conversely, compact sedans and hatchbacks demand further motor volumetric efficiency gains. Nonetheless, rising commercial volume underpins overall Magnet Free Electric Axle System market momentum, stabilizing revenue even if passenger uptake varies with economic cycles.

Geography Analysis

Asia-Pacific commanded 44.61% of the 2024 Magnet Free Electric Axle System market revenue and is forecast to advance at a 15.71% CAGR to 2030. Chinese policy blends manufacturing scale with directives to diversify away from rare earth, galvanizing domestic magnet-free R&D. ZF’s Shenyang facility, utilizing hairpin winding to raise power density, comes online in 2025 and exemplifies local content strategy. Japan’s Proterial targets ferrite magnet solutions that phase in by the early 2030s to cut neodymium dependence. South Korean science agencies report breakthroughs in heavy-rare-earth-free magnetic alloys that could reshape regional supply chains.

Europe advances through regulation and collaborative manufacturing. IE4 mandates strengthen technical pull, while the European Raw Materials Alliance channels investment toward alternative motor designs. The Emotors joint venture between Stellantis and Nidec produces more than 1 million units annually at Trémery, proving local volume economics. Valeo and MAHLE’s iBEE motor pushes magnet-free innovation into higher vehicle classes, widening addressable share. Renault’s partnership with Valeo targets a 200 kW rare-earth-free propulsion module by 2027, reinforcing strategic self-reliance.

North America focuses on secure domestic supply and manufacturing reshoring. The proposed production-tax-credit framework stimulates magnet-alternative plants, countering overseas concentration. Schaeffler invests USD 230 million in Ohio for electric axle builds, creating 450 jobs and embedding European expertise stateside. BorgWarner scales eMobility assembly in Mexico to serve U.S. OEMs seeking tariff-neutral sourcing. American Axle & Manufacturing’s combination with Dowlais builds a USD 12 billion revenue propulsion specialist able to meet evolving drivetrain demand across the continent. These developments collectively expand regional capacity and amplify cross-border supply-chain resilience within the Magnet Free Electric Axle System market.

Mordor Intelligence provides coverage of the magnet free electric axle system market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China, Japan, India, United States, and South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

The Magnet Free Electric Axle System market displays moderate concentration, where the top suppliers collectively manage a significant share, leaving room for specialized entrants. ZF leads in patent depth for inductive excitation and modular e-axle platforms, winning the 2024 CLEPA Innovation Award for the I²SM concept that eliminates rare earths without surrendering power density. Continental, BorgWarner, and Schaeffler aggressively reallocate R&D budgets toward magnet-independent solutions to shield revenue as ICE content declines.

Strategic collaborations proliferate. Stellantis and Nidec’s Emotors plant aligns mass production capability with in-house control electronics know-how, lowering unit costs at scale. Magna’s equity stake in Niron Magnetics secures early access to iron-nitrogen magnet technology, offering future supply optionality. White-space innovators pursue disruptive niches: C-Motive develops electrostatic motors generating torque without magnetic fields, while Materials Nexus uses AI to design magnet chemistries that bypass critical elements. These varied approaches intensify competitive dynamics as incumbents and start-ups chase differentiated IP and cost curves.

Revenue growth underscores the rapid commercialization pace. BorgWarner reported 47% year-over-year eProduct sales growth in Q1 2025, driven by Chinese and European awards. ZF forecasts doubled e-drive production within 12 months, anchored by Asia-Pacific orders. Continental leverages its semiconductor division to integrate inverter functionality directly onto stator end windings, reducing parts count. Market entry barriers remain manageable for niche players focusing on software control or high-grade electrical steel, but scale advantages in manufacturing and supply-chain leverage still favor top-tier suppliers. Overall, rivalry centers on cost-optimized magnet-free architectures, integrated power electronics, and sustainable material sourcing.

Magnet Free Electric Axle System Industry Leaders

ZF Friedrichshafen AG

Continental AG

Dana Incorporated

GKN Automotive

Schaeffler AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ricardo completed Alumotor, a 214 kW aluminum-wound propulsion unit delivering 92% efficiency for light commercial vehicles, funded by Innovate UK

- March 2025: Advanced Electric Machines introduced HDRM300C, a second-generation magnet-free motor designed for heavy-duty commercial vehicles.

- October 2024: Valeo and MAHLE extended iBEE magnet-free motor technology to upper-segment automotive applications, enhancing efficiency and power output.

Global Magnet Free Electric Axle System Market Report Scope

| Externally Excited Synchronous Motors (EESM) |

| Induction Motors |

| Switched Reluctance Motors |

| Fully Electric Drive |

| Hybrid Drive |

| Plug-in Hybrid Drive |

| Single E-Axle |

| Dual E-Axle |

| Integrated E-Axle |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Motor Type | Externally Excited Synchronous Motors (EESM) | |

| Induction Motors | ||

| Switched Reluctance Motors | ||

| By Drive Type | Fully Electric Drive | |

| Hybrid Drive | ||

| Plug-in Hybrid Drive | ||

| By E-Axle Configuration | Single E-Axle | |

| Dual E-Axle | ||

| Integrated E-Axle | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUV and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Magnet Free Electric Axle System market in 2025?

The Magnet Free Electric Axle System market size stands at USD 3.26 billion in 2025 with a forecast CAGR of 12.14% to 2030.

Which motor type leads adoption?

Externally excited synchronous motors hold the highest share at 48.13% in 2024 due to efficient field control and rare-earth independence.

Which region is growing fastest?

Asia-Pacific records the quickest expansion, projected at 15.71% CAGR on the strength of Chinese manufacturing scale and supportive policy.

Why are commercial vehicles important to growth?

Fleet electrification mandates and favorable total-cost-of-ownership economics drive a 15.29% CAGR in commercial applications through 2030.

Page last updated on: