India Magnet Free Electric Axle System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

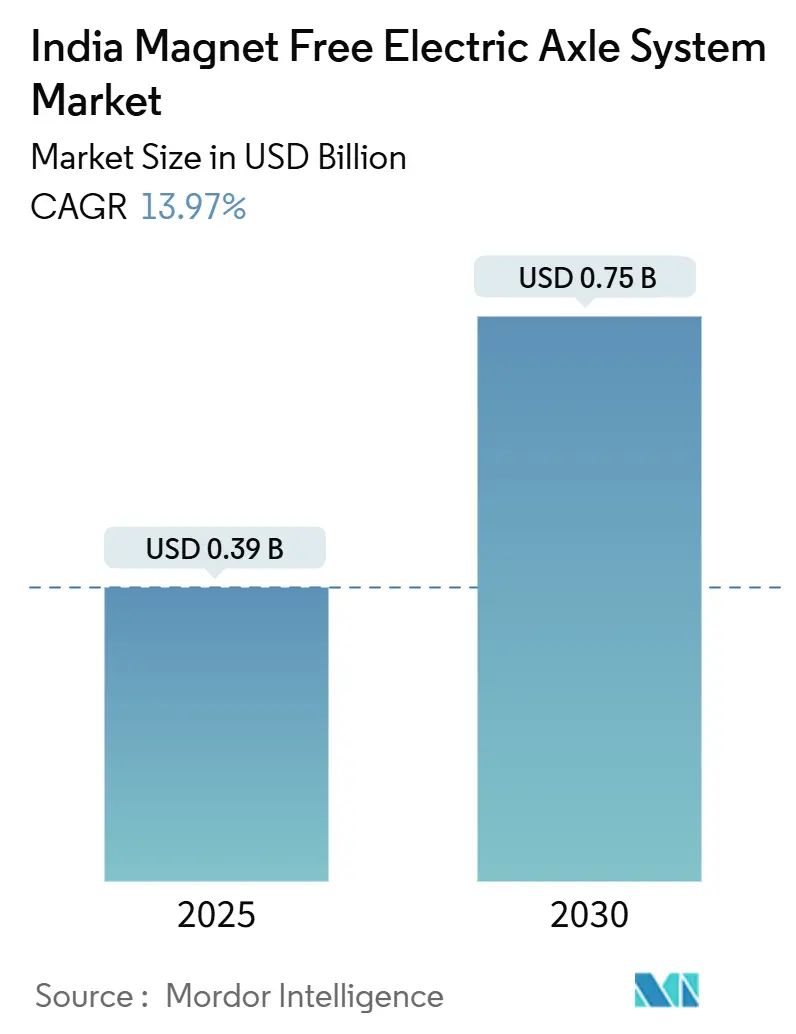

| Market Size (2025) | USD 0.39 Billion |

| Market Size (2030) | USD 0.75 Billion |

| Growth Rate (2025 - 2030) | 13.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Magnet Free Electric Axle System Market Analysis by Mordor Intelligence

The India magnet free electric axle system market size is USD 0.39 billion in 2025 and is projected to reach USD 0.75 billion by 2030, translating into a 13.97% CAGR over the period. Escalating localization incentives, the abrupt tightening of China’s rare-earth exports, and the steady fall in lithium-ion battery prices are nudging OEMs to adopt externally excited synchronous and induction motor platforms. Commercial vehicle electrification is surfacing as the largest incremental demand pool, while passenger cars continue to anchor volumes. The policy package led by the PM E-DRIVE and automotive PLI schemes is tilting capital expenditure toward domestic motor, gearbox, and power-electronics plants. At the same time, integrated e-axle architectures promise lower assembly complexity and better thermal management, positioning the India magnet free electric axle system market for sustained double-digit growth through the decade.

Key Report Takeaways

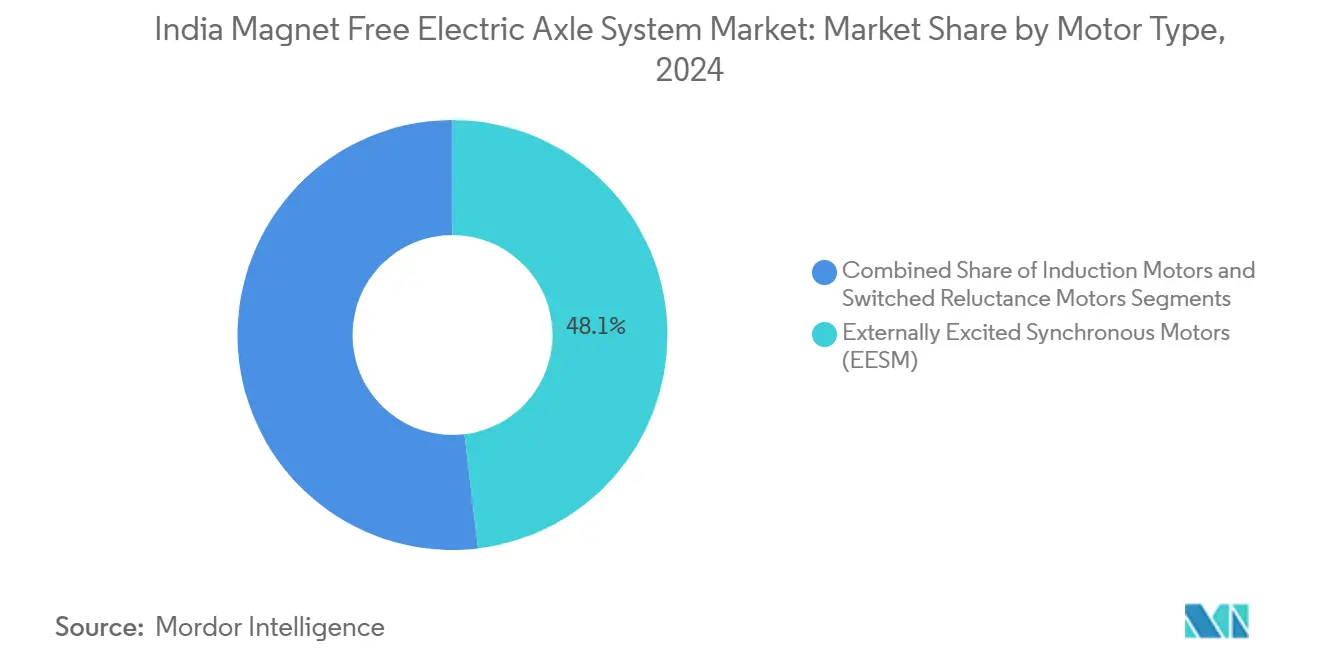

- By motor type, externally excited synchronous motors held a 48.12% share in 2024 and are projected to compound at a 15.16% CAGR through 2030.

- By drive type, fully electric drive systems accounted for a 58.66% share in 2024 and are poised to surge at an 18.33% CAGR to 2030.

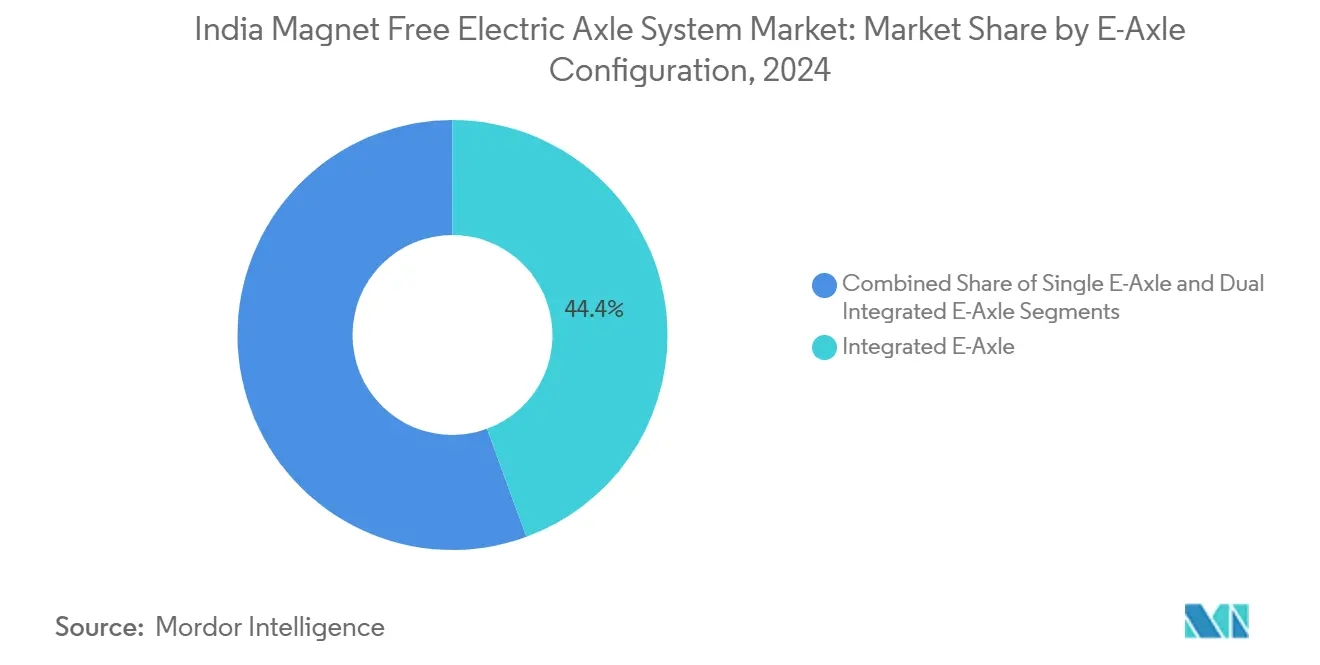

- By e-axle configuration, integrated units captured 44.38% share in 2024, while dual e-axles are the fastest-growing option at 17.48% CAGR over the forecast window.

- By vehicle type, passenger cars dominated with a 56.77% share in 2024, whereas commercial vehicles are forecast to expand at a 16.85% CAGR through 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with India being one of the contributors. Our global magnet free electric axle system market size represents that cumulative total.

India Magnet Free Electric Axle System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FAME-II & PLI Boosting Localization | +3.2% | National; strongest in Tamil Nadu, Maharashtra, Gujarat | Medium term (2-4 years) |

| Falling Li-Ion Prices Improving TCO | +2.8% | National; logistics hubs feel early gains | Short term (≤ 2 years) |

| Reducing Rare-Earth Import Dependence | +2.5% | Gujarat, Odisha clusters | Long term (≥ 4 years) |

| Zero-Emission Zones in Metros | +2.1% | Delhi NCR, Mumbai, Bangalore | Medium term (2-4 years) |

| OEM Shift to Integrated E-Axles | +1.9% | Tamil Nadu, Maharashtra, Haryana | Long term (≥ 4 years) |

| IIT–Supplier EESM R&D | +1.2% | Bangalore, Chennai, Delhi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FAME-II and PLI Incentives Accelerating Localization

The twin incentive stack of the PM E-DRIVE outlay and the automotive PLI program is redrawing supply-chain maps. Subsidies covering up to 18% of eligible capital spending are contingent on achieving 50% domestic value addition within five years, nudging global tier-1s to replace kit-assembly with full-scale manufacturing. Schaeffler’s Chennai facility exemplifies the shift, rolling out complete e-axle assemblies to meet localization thresholds. Battery incentives inside the same policy umbrella are catalyzing integrated drivetrain decisions because cell and pack makers co-locate near motor plants, compressing logistics costs. Budget 2025-26 raised advanced chemistry cell funding tenfold, signaling persistent government sponsorship [1]Press Information Bureau, “Union Budget 2025-26 Highlights,” pib.gov.in.

Falling Li-ion Battery Prices Improving TCO for CV Fleets

Annual battery pack cost deflation of nearly 20% since 2022 has slashed the upfront premium of electric trucks and vans. Operating data from major fleet operators show electric commercial vehicles now run 40-50% cheaper per kilometer than diesel rivals, even before city toll exemptions are added. As battery outlays shrink, the residual price gap between magnet-free e-axles and permanent-magnet units loses significance. Economics, therefore, tilt toward supply-secure motor topologies, driving fleet orders across logistics corridors. High-frequency battery-health analytics further extend usable life, squeezing total cost of ownership in favor of electrification.

Need to Curb Rare-earth Import Dependence

China’s April 2025 export curbs exposed single-country sourcing risks, prompting the Ministry of Heavy Industries to draft a dedicated incentive of USD 421-602 million to birth domestic rare-earth magnet plants. Parallelly, OEMs are future-proofing by substituting permanent magnets altogether. Ola Electric has publicly committed to large-scale production of heavy-rare-earth-free motors by the second quarter of FY 2025-26, underscoring a wholesale pivot toward magnet-free architectures. National Critical Mineral Mission allocations back upstream mining and processing, strengthening raw-material diversification.

Zero-emission Zones in Indian Metros

Delhi’s night-time ban on diesel cargo vans inside its central business district has matured into a template other metros are adopting. Mumbai is mapping goods-movement corridors that will be off-limits to internal-combustion trucks inside three years, forcing fleet upgrades toward electric drivelines. OEMs offering magnet-free e-axles gain an edge because compliance is guaranteed without exposing operators to rare-earth supply shocks. State-level purchase subsidies in Karnataka and Tamil Nadu stack atop federal grants, tilting comparative paybacks further toward electric vans that use India magnet free electric axle system market technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Domestic Power-Electronics Supply | -2.1% | Tamil Nadu, Karnataka, Maharashtra | Short term (≤ 2 years) |

| Part-Load Efficiency Gap vs. PM Motors | -1.8% | National highways | Medium term (2-4 years) |

| Thermal Stress in Tropical Climates | -1.4% | Northern plains | Long term (≥ 4 years) |

| Motor-Control Software Skill Shortage | -1.2% | Bangalore, Pune, Chennai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Power-Electronics Capacity

High-voltage silicon-carbide modules remain largely imported, stretching build cycles and adding forex exposure. Assembly houses in Tamil Nadu and Karnataka are investing but need at least two years to hit economic wafer volumes. Interim procurement from overseas fabs sustains production but erodes price competitiveness against global peers that enjoy home-grown semiconductor ecosystems.

Efficiency Gap vs PM Motors at Part-load

Magnet-free topologies consume extra field or slip energy when torque demand ebbs, trimming range in stop-start traffic. While algorithmic field-weakening narrows the delta, physical limits still eat into energy budgets on urban delivery routes. This drag nudges some OEMs to reserve induction motors for duty cycles where thermal margins outweigh efficiency losses, tempering full-spectrum adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: EESM Dominance Drives Innovation

Externally excited synchronous motors held the highest 48.12% share in 2024, anchoring the India magnet free electric axle system market share at the motor-technology level. Their head start also powers a 15.16% CAGR through 2030, placing them at the forefront of capacity additions. Integrated field coils eliminate rare-earth magnets, aligning OEM risk strategies with government import-substitution goals. Two IIT-led consortia have already validated AI-assisted excitation patterns that curtail copper losses at cruising speeds, lifting highway efficiency closer to permanent-magnet baselines.

Induction motors remain popular in heavy vans and buses because of their rugged rotor construction, though their growth trail is flatter as design teams wrestle with tropical heat loads. Switched-reluctance prototypes circulate in R&D labs, promising complete magnet elimination, but noise and vibration control need further refinement before significant volumes materialize. As localization rules tighten, the India magnet free electric axle system market is set to leverage EESM’s compatibility with existing stamping and winding lines, hastening scale economics.

By Drive Type: Full Electric Systems Accelerate

Fully electric drivetrains cornered 58.66% of 2024 shipments and are tracking an 18.33% CAGR to the end of the decade, reflecting decisive policy and fleet choices. Zero-emission zones deny hybrids access to key urban freight arteries, pushing operators toward battery-only vans that deploy magnet-free e-axles. Subsidy differentials sharpen the price gap: GST on hybrids stands at 43%, while pure electrics enjoy just 5%.

Plug-in hybrid and conventional hybrid designs survive mainly in intercity coach and SUV niches where charging stops remain sparse. Even there, better battery densities trim the value proposition of engine support, clearing the runway for future migrations to pure-play electric setups. As a result, the India magnet free electric axle system market embeds higher inverter and thermal-cooling content per vehicle, enlarging the domestic value-addition base.

By E-Axle Configuration: Integration Trends Reshape Design

Integrated e-axles controlled 44.38% of 2024 volumes, underscoring OEM appetite for factory-ready modules that collapse motor, gearbox, and inverter into one SKU. Their plug-and-play nature cuts assembly minutes and frees underbody space for larger battery packs, sharpening range advantages.

Dual e-axles, though starting from a smaller base, post the swiftest 17.48% CAGR as payload-intensive trucks adopt twin-drive layouts to distribute torque and limit axle weights. The India magnet free electric axle system market size for dual configurations stands to balloon once intercity freight routes electrify, a trend likely after battery charging hubs become commonplace along national highways.

By Vehicle Type: Commercial Vehicles Drive Growth

Passenger cars still led with 56.77% of 2024 shipments, supported by high-volume hatchback and compact-SUV launches sporting locally built e-axles. The India magnet free electric axle system market size for passenger applications is expected to widen steadily as consumer confidence rises on better charging reliability.

Commercial vehicles, however, post the headline 16.85% CAGR because depot-based logistics fleets capture clear cost savings per kilometer. Light-commercial vans for last-mile delivery are the first adopters, but state transport undertakings are now running pilots for 12-meter electric buses using magnet-free drivetrain kits. These institutional orders anchor predictable offtake, allowing suppliers to amortize tooling quicker and snowball economies of scale.

Geography Analysis

Southern India is the gravitational hub of the India magnet free electric axle system market, thanks to dense supplier clusters and EV-friendly policies. Chennai–Hosur’s corridor houses plants from Schaeffler, Continental, and Valeo, ensuring turnkey access to precision gears, wound stators, and inverter substrates. Tamil Nadu’s 2019 EV policy adds capital subsidies that trim payback periods for greenfield motor lines. Pune and Aurangabad in Maharashtra mirror this ecosystem for western OEMs such as Tata Motors and Mahindra, with proximity to steel and casting vendors containing logistics drag. Gujarat’s vendor parks, catalyzed by recurring Vibrant Gujarat meets, welcome fresh entrants, glad to tap port connectivity for component exports [2]Press Information Bureau, “State-wise Incentives for EV Manufacturing,” pib.gov.in.

Karnataka complements manufacturing heft with deep-tech software skills. Bengaluru-based control-algorithm specialists refine excitation tables and thermal maps before flashing code to ECUs on assembly lines in the adjoining states. Northern expansion gains pace as Haryana and Uttar Pradesh court bus and truck makers keen to serve Delhi-centric zero-emission corridors. State electricity boards in these zones publish concessional night-tariff slabs that soften depot charging bills, nudging fleet conversions.

Demand skews urban: Delhi NCR triggers early adoption in delivery vans, Mumbai ports pilot e-tractors for short-haul container moves, and Bangalore’s tech parks sign green-mobility pacts that lock in bus procurement. Semi-urban segments remain price-sensitive, but PM E-DRIVE top-ups now extend to tier-2 cities, opening fresh addressable volume for the India magnet free electric axle system market.

Coverage of the magnet free electric axle system market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for China, Japan, United States, and South Korea, each shaped by local operating conditions.

Competitive Landscape

Global tier-1 suppliers apply engineering depth and established OEM contracts to stay on the short list for high-spec programs. Dana, ZF, and Continental supply multi-ratio gearboxes and silicon-carbide inverters that meet commercial-vehicle duty cycles. Yet domestic champions such as Sona Comstar and Tata AutoComp use labor-cost arbitrage and localization credits to undercut imports on mid-range e-axle bids.

Technology licensing defines the middle ground: Sterling Tools recently inked an agreement with Advanced Electric Machines to fabricate magnet-free traction motors at its Faridabad plant, bypassing the design curve while retaining local cost structure [3]Sterling Tools Ltd., “Sterling Gtake to Produce Magnet-Free Motors,” sterlingtools.com. Joint ventures also mitigate semiconductor gaps; several OEMs co-source inverter substrates from Asian fabs while encapsulating final modules domestically.

Competitive intensity is rising in software. Start-ups staffed by ex-consumer-electronics engineers write FPGA-based gate-driver code that trims switching losses, providing unique selling points for otherwise commoditizing hardware. Rare-earth-supply turbulence reshuffles power equations, rewarding players ready with magnet-free portfolios and robust Indian footprints, cementing the India magnet free electric axle system market as a strategic rather than purely economic battleground.

India Magnet Free Electric Axle System Industry Leaders

Dana Incorporated

ZF Friedrichshafen AG

Schaeffler AG

Continental AG

Valeo SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ola Electric confirmed production of heavy-rare-earth-free motors beginning Q2 FY 2025-26 to cut import exposure and lower costs.

- May 2025: Sterling Tools signed a licensing pact with Advanced Electric Machines to manufacture rare-earth-free traction motors at its Faridabad facility.

India Magnet Free Electric Axle System Market Report Scope

| Externally Excited Synchronous Motors (EESM) |

| Induction Motors |

| Switched Reluctance Motors |

| Fully Electric Drive |

| Hybrid Drive |

| Plug-in Hybrid Drive |

| Single E-Axle |

| Dual E-Axle |

| Integrated E-Axle |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| By Motor Type | Externally Excited Synchronous Motors (EESM) | |

| Induction Motors | ||

| Switched Reluctance Motors | ||

| By Drive Type | Fully Electric Drive | |

| Hybrid Drive | ||

| Plug-in Hybrid Drive | ||

| By E-Axle Configuration | Single E-Axle | |

| Dual E-Axle | ||

| Integrated E-Axle | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUV and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

Key Questions Answered in the Report

How large is the India magnet free electric axle system market in 2025?

It stands at USD 0.39 billion and is projected to grow at a 13.97% CAGR to USD 0.75 billion by 2030.

Which motor topology leads current adoption?

Externally excited synchronous motors hold the top 48.12% share and are also the fastest-growing configuration.

Why are commercial vehicles adopting magnet-free e-axles faster than passenger cars?

Fleet operators see 40-50% lower operating costs per kilometer, and zero-emission zones in metros accelerate the switch.

What policy instruments support domestic e-axle manufacturing?

The PM E-DRIVE outlay and the automotive PLI program provide capital subsidies tied to localization thresholds.

Page last updated on: