Automotive Axle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

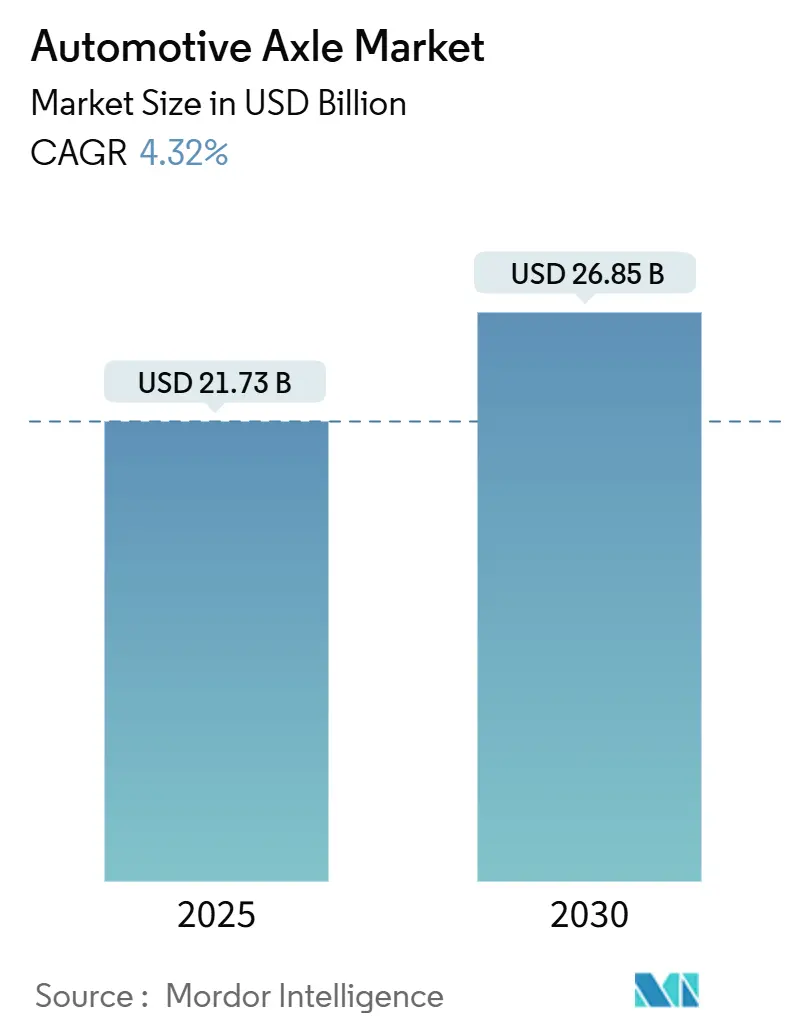

| Market Size (2025) | USD 21.73 Billion |

| Market Size (2030) | USD 26.85 Billion |

| Growth Rate (2025 - 2030) | 4.32% CAGR |

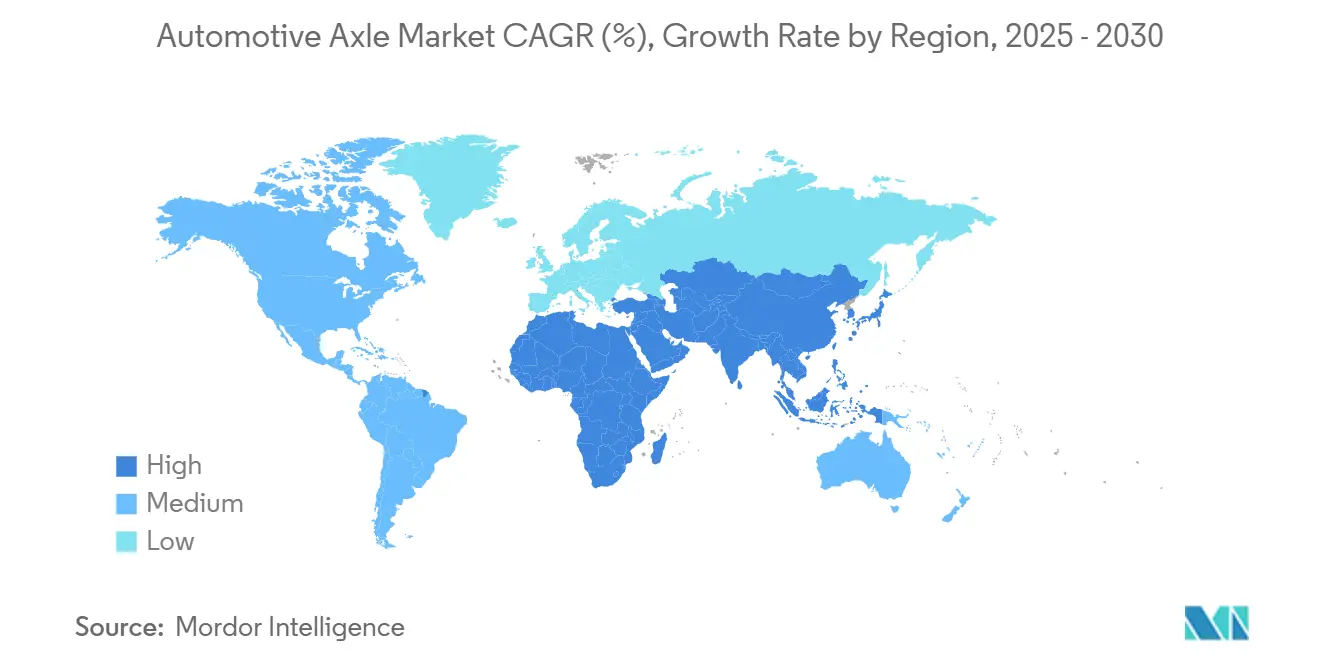

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Axle Market Analysis by Mordor Intelligence

The automotive axle market size stands at USD 21.73 billion in 2025 and is set to expand at a 4.32% CAGR, reaching USD 26.85 billion by 2030. Over the outlook period, the primary growth catalyst is the shift from internal-combustion platforms toward electrified powertrains and modular skateboard chassis. Drive axles hold clear leadership, lightweight materials accelerate, and integrated e-axle units compress component counts, enabling cost‐effective electrification. Suppliers pursue global footprints and automation to counter raw-material volatility and meet stricter load and durability rules, while regional production moves closer to end-markets.

Key Report Takeaways

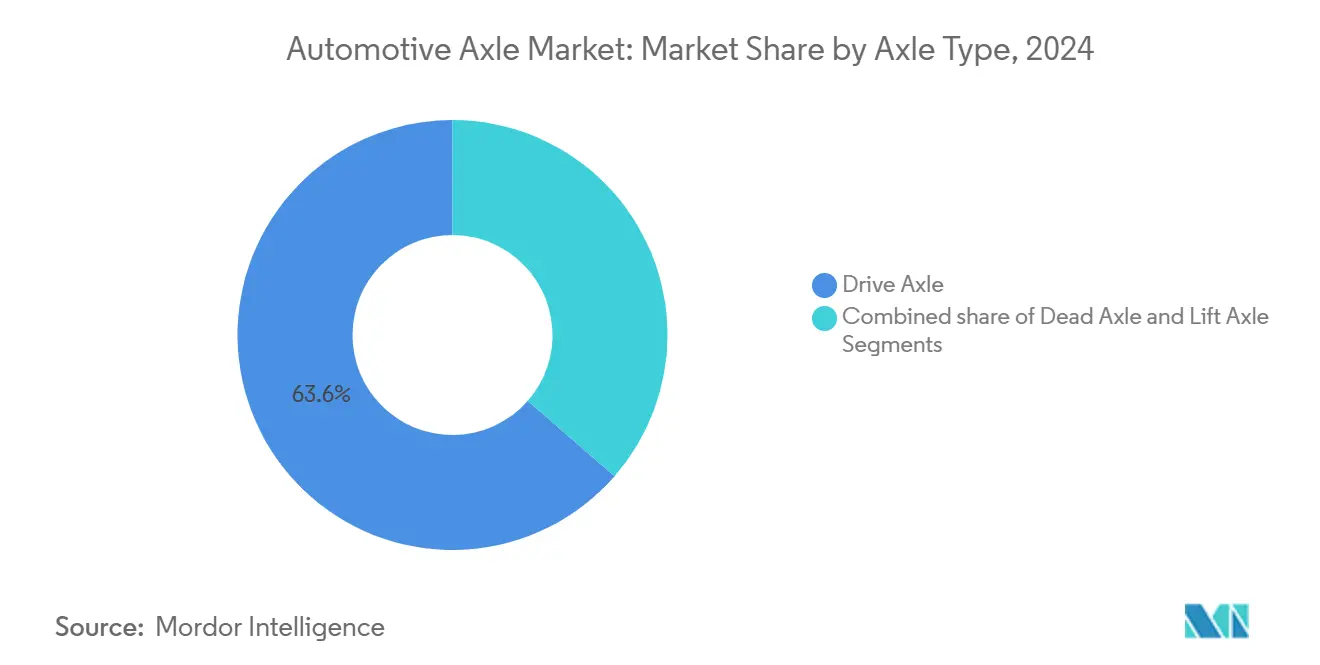

- By axle type, drive axles led with 63.58% revenue share in 2024; lift axles are projected to advance at a 7.11% CAGR through 2030.

- By position, rear axles captured 38.97% of automotive axle market share in 2024, while composite axles are forecasted to expand at an 8.88% CAGR to 2030.

- By material, steel commanded 72.81% of the automotive axle market size in 2024, whereas composite materials are rising at a 10.12% CAGR.

- By vehicle type, passenger cars accounted for 62.55% of the automotive axle market size in 2024 and commercial vehicles are growing at a 5.72% CAGR.

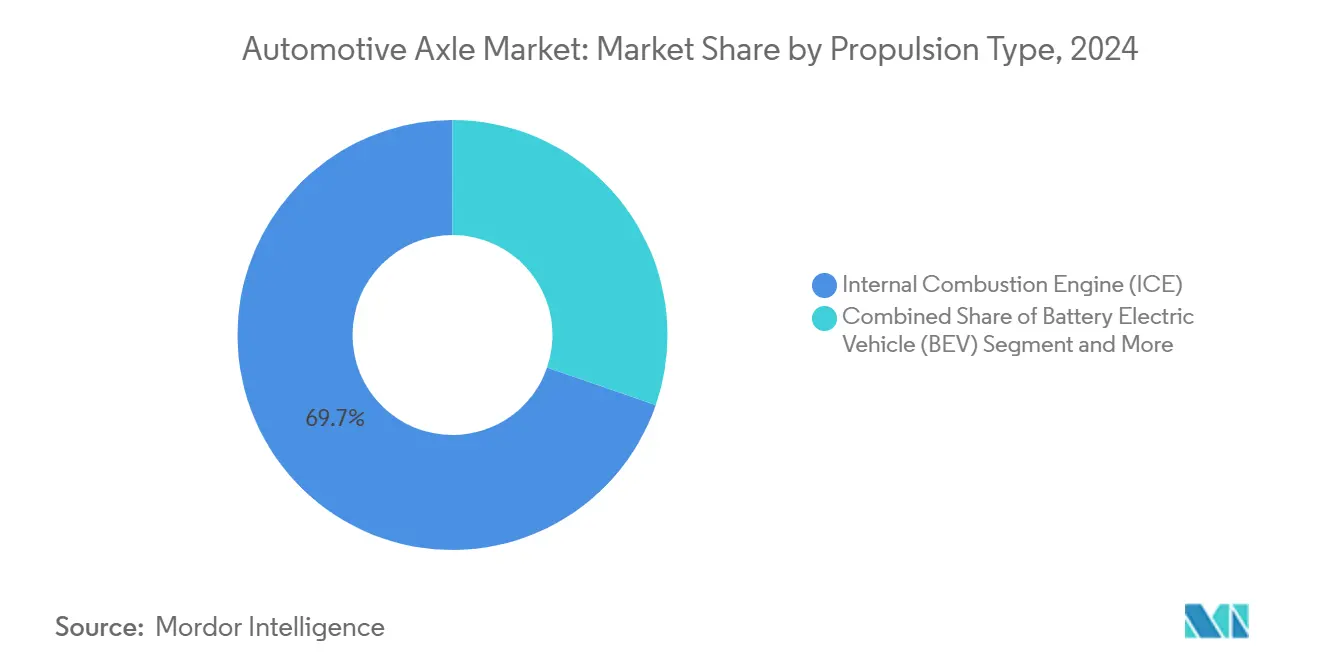

- By propulsion, ICE vehicles held 69.73% share of automotive axle market share in 2024; battery-electric vehicles are projected to register the fastest 16.65% CAGR to 2030.

- By sales channel, OEMs controlled 75.88% of automotive axle market share in 2024, while the aftermarket records a 6.87% CAGR to 2030.

- By geography, Asia-Pacific dominated with 46.14% of automotive axle market share in 2024; the Middle East & Africa region is pacing at a 6.41% CAGR through 2030.

Global Automotive Axle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification | +2.1% | Global, with early gains in China, Europe, North America | Medium term (2-4 years) |

| Demand for Lightweight Axles | +1.8% | Global, strongest in EU and North America regulatory zones | Short term (≤ 2 years) |

| Surging Vehicle Production | +1.2% | Asia-Pacific core, spill-over to South America and MEA | Long term (≥ 4 years) |

| Safety and Load Regulations | +0.9% | EU, North America, with adoption spreading to APAC | Medium term (2-4 years) |

| Modular Skateboard Platforms | +0.7% | Global, led by premium OEMs in developed markets | Long term (≥ 4 years) |

| Additive Manufacturing | +0.4% | North America and Europe early adoption, scaling globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification Increasing E-axle Adoption

Integrated e-axle assemblies merge motor, gearbox, and inverter functions, dropping mass and freeing chassis space for larger battery packs. Commercial examples show heavy-duty e-axles delivering 380 kW continuous power while slotting into existing mounting envelopes to ease OEM conversion programs. Instant torque demands tougher gear metallurgy and optimized thermal paths, driving investment in new machining and testing lines. Suppliers adopt scalable design toolkits that cover passenger cars to Class 8 trucks, shortening launch cycles. National incentives and zero-emission quotas in China and Europe bring e-axle volumes into the tens of millions by decade-end.

Rising Demand for Lightweight Axles to Meet Fuel-efficiency Norms

Regulatory pressure for improved fuel economy drives systematic weight reduction across vehicle architectures. Advanced high-strength steels raise yield strength 30% with 10% weight savings versus conventional grades. Aluminum and magnesium extrusions processed through shear-assisted methods further trim axle beam mass while sustaining crash-energy absorption[1] “Lightweight Materials,” Pacific Northwest National Laboratory, pnnl.gov. Composites with carbon fibers and glass micro-spheres now move from prototype to limited-series runs in rear axles for premium SUVs. Lightweighting gains are magnified when paired with low-friction bearings and optimized lubricant channels, lowering drivetrain losses and compliance costs.

Surging Vehicle Production in Emerging Economies

Asia-Pacific accounts for almost half of global vehicle output, spearheaded by China’s and India’s expanding export-oriented programs. Government road-building, rising disposable incomes, and localized supply chains fuel axle demand in ASEAN, South Asia, and Africa. OEMs localize high-capacity forging, heat-treatment, and machining lines to avoid import duties and logistics delays. Tier-1s add service hubs and engineering centers near new final-assembly plants, shortening development loops and growing regional talent pools. Over the long term, ride-sharing fleets and e-commerce trucks sustain volume growth even as private car ownership plateaus in mature markets.

Stringent Safety and Load Regulations Mandating Robust Axle Designs

Global rules tighten braking-distance targets, rollover thresholds, and axle-load ceilings, compelling stronger housings, thicker flanges, and higher-capacity bearings. ISO 9815:2024 introduces lateral-stability tests that influence axle placement and suspension geometry[2]“ISO 9815:2024 — Road vehicles — Passenger-car and trailer combinations — Lateral stability test,” International Organization for Standardization, iso.org. EU truck type-approval frameworks specify electronic brake and traction-control integration, raising electronics content in axle modules. Continuous load monitoring sensors embedded in axle beams feed real-time data to fleet telematics, preventing overload fines and premature wear. Compliance costs are offset by reduced liability exposure and better residual values for certified vehicles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel and Aluminum Prices | -1.4% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| High CAPEX | -1.1% | Global, particularly challenging for smaller suppliers | Medium term (2-4 years) |

| Durability Concerns | -0.8% | Global, with regulatory scrutiny in safety-focused markets | Medium term (2-4 years) |

| Non-uniform Axle Load Standards | -0.5% | Global, with complexity highest in multi-region suppliers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel & Aluminum Prices

Raw material cost volatility significantly impacts axle manufacturing economics. OEMs apply hedging, dual-sourcing, and recycled-content strategies to stabilize costs. Aluminum billet and magnesium ingot quotes track energy futures, exposing foundries to utility-price spikes. Contract clauses now index axle prices to commodity baskets, sharing risk between assembler and supplier. Automation, scrap-recovery systems, and near-net forming cut waste, softening the blow when spot markets spike.

High CAPEX for E-Axle Production Lines

Integrated e-axle plants require high-precision stator lamination stacks, HV winding, and automated end-of-line testers that cost hundreds of millions of dollars. Smaller tier-2s struggle to fund such lines, favoring joint ventures or contract manufacturing. State-level incentives, accelerated depreciation schedules, and cheap land grants in emerging markets mitigate financing hurdles but do not erase scale economics. Consequently, mergers like the 2025 AAM-Dowlais deal compress the supplier league table.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Axle Type: Drive Axles Command Market Leadership

Drive axles captured 63.58% of the automotive axle market share in 2024 and are projected to advance at a 7.11% CAGR by 2030, due to their essential role in torque transfer across most vehicle architectures. The automotive axle market size for drive axles is forecast to climb with new demand for integrated e-drive modules that couple motor, gearbox, and differential. Lift axles grow quickly as fleet operators pursue fuel and tire savings by retracting idle wheels under light loads, aligning with regulatory pushes for lower CO₂. Dead axles remain crucial for load support in heavy trucks, where air-suspension compatibility and disc-brake readiness shape specifications.

Suppliers now offer modular axle families covering drive, dead, and lift variants sharing common housings to economize tooling. Digital torque vectoring via embedded clutch packs increases traction while preserving mechanical simplicity. Lightweighting through high-strength steels and hollow-tube designs trims unsprung mass, improving ride without sacrificing durability. Steerable lift axles enter refuse and urban-delivery fleets, boosting maneuverability in tight streets. Over the forecast window, the automotive axle market will see mixed-mode systems pairing electric drive axles with mechanical lift companions to balance range and payload.

By Position: Rear Axles Dominate Traditional Architecture

Rear axles held 38.97% of the automotive axle market share in 2024 because most rear-wheel-drive and all-wheel-drive layouts depend on them for propulsion. The automotive axle market share for rear units benefits from the proliferation of pickups, SUVs, and electric crossovers adopting rear-biased torque distribution. Composite axles are forecasted to expand at an 8.88% CAGR to 2030, as it deliver up to 40% mass savings compared with cast-iron predecessors, easing OEM compliance with fuel-economy regulations. Front axles evolve alongside steer-by-wire and ADAS sensor packaging, demanding tight tolerances and integrated cooling channels for electric motors in e-corner modules.

Independent front suspensions appear increasingly on heavy trucks, improving ride comfort and tire life. Axle suppliers develop quick-ratio gearsets optimized for high-speed EV torque curves, contrasting with taller ICE final drives. Steering axles integrate precision angle sensors supporting lane-keeping and automated parking functions. Position-specific requirements, therefore, multiply part numbers, but shared knuckle castings and bearing families temper complexity. Rear-e-axle systems now deliver up to 540 kW peak output, rivaling dual-motor setups and affirming their continuing centrality.

By Material: Steel Maintains Dominance Despite Composite Surge

Steel controlled 72.81% of the automotive axle market share in 2024 as its cost efficiency and entrenched supply base remain hard to outmatch. Even so, composite materials expand at a 10.12% CAGR, suggesting the automotive axle market is entering a multi-material era. Advanced high-strength grades enable around 10% weight cuts at critical load paths without redesigning interfaces, an attractive drop-in upgrade. Aluminum usage spreads from housing covers to complete axle tubes, spurred by additive manufacturing of complex end-caps with integrated cooling fins.

Carbon-fiber sleeved shafts demonstrate doubled torsional stiffness at half the mass of steel analogs, appealing to super-cars and long-range EVs. Providers apply nano-ceramic coatings inside steel tubes for corrosion resistance, extending service life in salt-belt regions. Hybrid material joints using friction stir welding link aluminum carriers to steel tubes, balancing weight and fatigue. The automotive axle market size advantage of steel persists near-term, yet cost curves for mass-produced composites fall as filament-winding lines scale.

By Vehicle Type: Passenger Cars Lead Despite Commercial Growth

Passenger cars represented 62.55% of the automotive axle market share in 2024, driven by high global production volumes. Rooftop solar-charging hybrids and mass-market EV hatchbacks boost light-duty axle demand, although miles driven per vehicle decline in shared-mobility fleets. Commercial vehicles post a faster 5.72% CAGR as e-commerce pushes medium-duty vans and heavy trucks into service, escalating average axle load ratings. Fleet operators specify easily serviceable hub-reduction gears and long-drain lubricant systems to cap total cost of ownership.

Passenger-car axles increasingly integrate active sound dampers to mask EV gear whine and adopt hollow shafts to meet pedestrian impact norms. Conversely, truck axles focus on durability beyond 1.5 million km, adding induction-hardened splines and shot-peened bearings. Thermal management grows critical for both segments as high-power regen braking elevates temperature swing cycles. Modular designs enable suppliers to reuse motor stators across passenger and commercial e-axle variants, boosting volume leverage across the automotive axle market.

By Propulsion Type: ICE Dominance Faces EV Disruption

ICE vehicles still held 69.73% of the automotive axle market share in 2024, but battery-electric models surge at 16.65% CAGR, realigning the automotive axle market structure. Electric architectures dispense with prop-shafts, redirecting value to integrated e-drive assemblies. Hybrid designs require axles tolerant of combustion and electric torque pulses, spawning new damper technologies to quell NVH. Fuel-cell trucks and hydrogen ICE prototypes introduce high-speed axle gears to match motor rpm ranges, testing heat-treatment limits.

Motor torque arriving instantaneously demands thicker gear teeth and optimized bearing preload to prevent micro-pitting. Cooling jackets webbed into aluminum housings dissipate inverter heat through axle oil, leveraging existing lubrication circuits. Rare-earth-free motors embedded in axles cut magnet material exposure, lowering geopolitical supply risk. Over the decade the automotive axle market will experience further convergence as software-defined powertrains let OEMs tweak torque distribution via over-the-air updates rather than hardware changes.

By Sales Channel: OEM Dominance With Aftermarket Opportunity

OEM channels generated 75.88% of the automotive axle market share in 2024, reflecting axles’ deep integration into under-body modules and just-in-time sequencing at assembly plants. Tier-1s sign lifetime agreements covering ICE and future e-axle generations, bundling software and predictive-maintenance analytics. The aftermarket grows at a 6.87% CAGR due to aging global fleets and rising average vehicle age beyond 12 years. Online platforms ship complete axle assemblies directly to independent garages, shortening downtime for small business fleets.

Remanufactured axles gain traction aligned with circular-economy targets. Warranty programs reach up to 100,000-mile coverage, spurring consumer confidence in non-OEM parts. Sensorized axles feed diagnostic data into cloud dashboards, shifting fleet owners from preventive to predictive maintenance models. As electrified drivelines mature, aftermarket players prepare to service inverter boards, thermal plates, and motor stators in addition to traditional bearings and seals, widening the automotive axle market playing field.

Geography Analysis

Asia-Pacific held 46.14% of the automotive axle market share in 2024, underpinned by China’s 31.4 million vehicle output. Local supply networks spanning forged blanks to precision gears lower logistics costs and speed launches, cementing regional dominance. India’s incentive schemes lure global OEMs to build export hubs, while Southeast Asian nations develop component ecosystems to capture spill-over investment. Regional governments push axle makers to add lightweight materials and high-efficiency hubs to meet emerging fuel rules. Collective engine-downsizing and electric adoption sustain double-digit e-axle volume gains across the automotive axle market.

Middle East & Africa achieves the fastest regional growth at 6.41% CAGR reflecting infrastructure development and increasing vehicle adoption rates. This surge is driven by rising investments in road connectivity, urban expansion, and industrial projects across key countries like Saudi Arabia, UAE, South Africa, and Egypt. Additionally, the growing middle-class population and improving access to financing are making personal and commercial vehicles more attainable, further fueling demand for automotive axles in the region.

North America remains a technology bellwether, contributing steady revenue on the back of full-size pickups and SUVs. Strong consumer preference for high-torque models keeps demand for heavy rear axles robust, though increasing EV adoption brings integrated e-axles into mainstream assembly plants. Europe, on contrary, commands premium market segments and stringent safety rules. Regulation-driven technology such as steer-by-wire and advanced driver-assistance systems increases front-axle content. Lightweight composite axles gain early traction among German luxury OEMs balancing performance and emissions.

Competitive Landscape

Industry concentration tightened after American Axle & Manufacturing’s acquisition of Dowlais, forming a driveline supplier targeting synergies worth millions[3]“Supplier Requirements Manual 2024,” American Axle & Manufacturing Holdings Inc., aam.com. The combined entity scales e-axle production across three continents and invests in additive manufacturing to cut prototype cycles from months to days. Competitors counter through alliances: a notable partnership unveiled a magnet-free e-axle that slashes carbon footprint 40% while preserving output. Top tier-1s pour capital into 800 V inverter integration, heat-spreader casting, and automated stator-winding lines to secure lead positions.

Technology edge defines rivalry. One European supplier embedded phase-change materials in axle housings for peak-load heat absorption, allowing higher continuous torques without radiator enlargement. Another player leveraged binder-jet printed sand cores to cast complex oil-flow channels, trimming pump parasitic losses by 15%. Additive printer farms reportedly break even in under six months, encouraging wider deployment for fixtures and small-batch components. Investment intensity raises barriers for mid-tier firms, driving joint ventures focused on regional niches such as two-wheeler e-axles in India.

White-space markets emerge in light electric freight and off-highway autonomy. Suppliers develop compact beam axles for robotic delivery pods, featuring integrated hub motors and solid-state brakes. Fuel-cell truck programs spur axle designs capable of higher continuous speeds to match motor envelopes. Industry players also explore subscription models bundling hardware, condition monitoring, and predictive maintenance dashboards, pivoting toward service-oriented revenue streams. Market leaders integrate blockchain-based traceability for raw-material provenance, improving ESG scores and audit readiness.

Automotive Axle Industry Leaders

Dana Incorporated

American Axle & Manufacturing

ZF Friedrichshafen AG

Meritor (Cummins)

GKN Automotive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: American Axle & Manufacturing closed a USD 1.44 billion cash-and-stock purchase of Dowlais Group, forming a USD 12 billion driveline supplier with USD 300 million synergy target.

- December 2024: Dana launched the AdvanTEK 40 Pro tandem axle with a 2.05 final ratio for down-sped diesel engines, boosting fleet efficiency.

- October 2024: Bharat Forge acquired AAM India Manufacturing Corporation, adding Pune and Chennai axle operations plus an R&D center.

Global Automotive Axle Market Report Scope

| Drive Axle |

| Dead Axle |

| Lift Axle |

| Front Axle |

| Rear Axle |

| Steering Axle |

| Composite Axle |

| Steel |

| Aluminum |

| Composite Materials |

| Passenger Cars |

| Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Hybrid Electric Vehicle (HEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Axle Type | Drive Axle | |

| Dead Axle | ||

| Lift Axle | ||

| By Position | Front Axle | |

| Rear Axle | ||

| Steering Axle | ||

| Composite Axle | ||

| By Material | Steel | |

| Aluminum | ||

| Composite Materials | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the automotive axle market be by 2030?

It is forecast to reach USD 26.85 billion in 2030, growing at a 4.32% CAGR from 2025.

Which axle type generates the most revenue?

Drive axles lead with 63.58% of 2024 revenue due to their critical role in power transfer across most vehicle formats.

What material trend is reshaping axle design?

Composite materials post a 10.12% CAGR, offering up to 40% weight savings and helping OEMs meet fuel-efficiency targets.

Which region drives future axle demand?

Asia-Pacific commands 46.14% of 2024 value and remains the fastest-growing production hub thanks to China and India.

How is electrification influencing axle specifications?

Integrated e-axles combine motor, inverter, and gearbox, reducing part count and enabling instantaneous torque delivery, which demands stronger gears and advanced cooling.

Page last updated on: