Japan LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

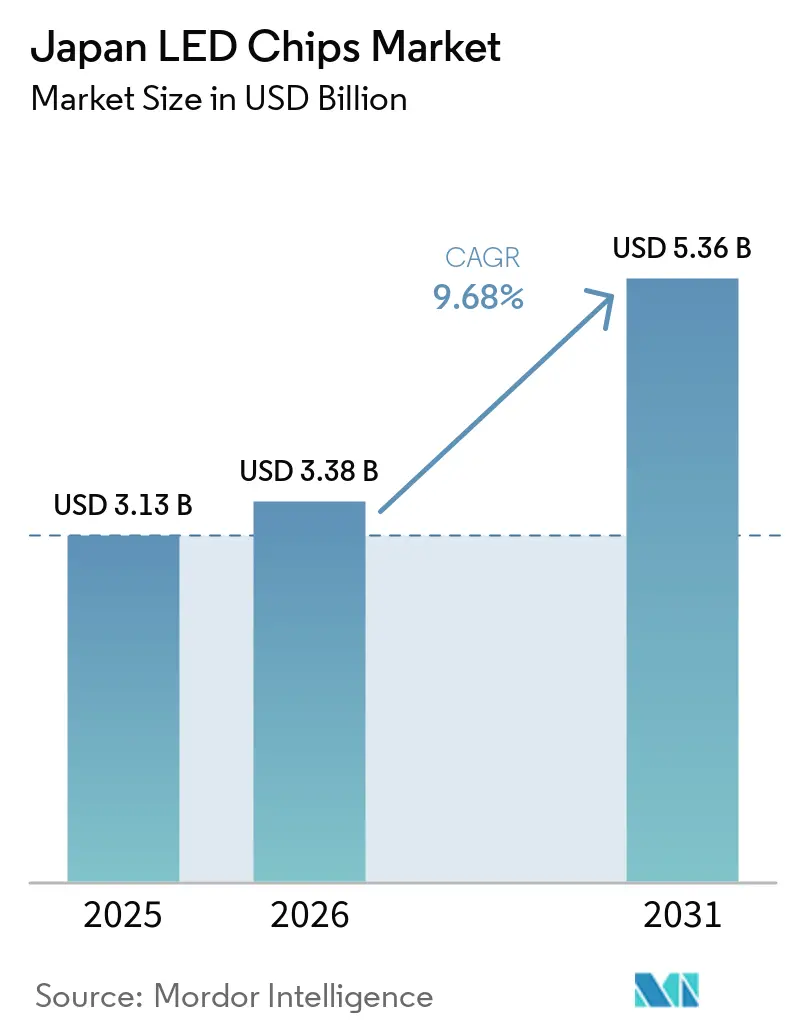

| Base Year Market Size (2025) | USD 3.13 Billion |

| Market Size (2026) | USD 3.38 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 9.68% CAGR |

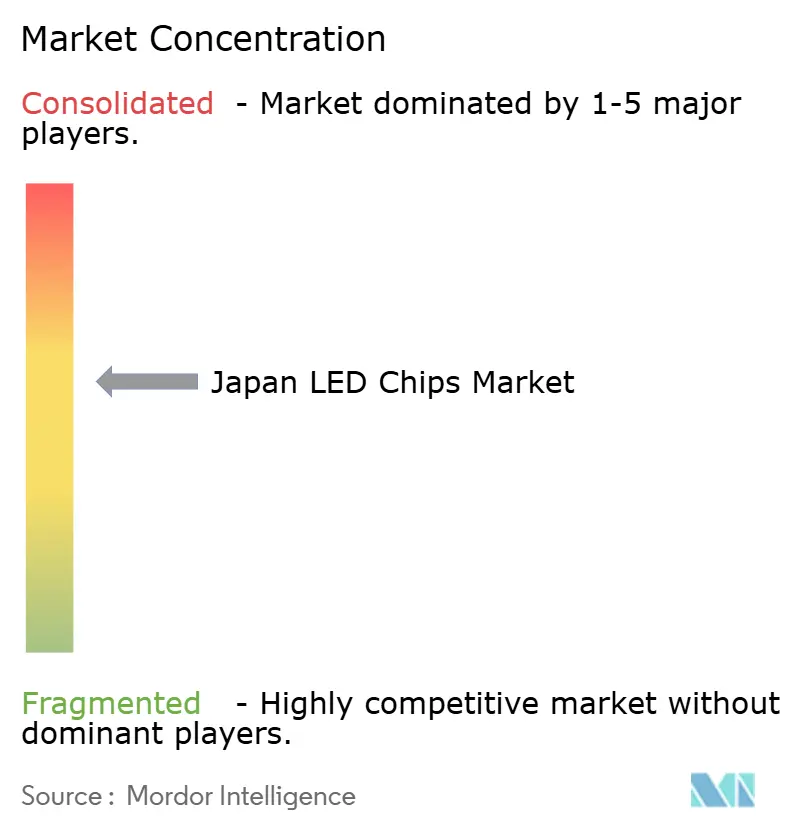

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan LED Chips Market Analysis by Mordor Intelligence

The Japan LED chips market size is expected to increase from USD 3.13 billion in 2025 to USD 3.38 billion in 2026 and reach USD 5.36 billion by 2031, growing at a CAGR of 9.68% over 2026-2031. Momentum stems from government subsidies that lower fab-level risk, automakers’ shift to energy-efficient headlamps, and revised national standards that make light-emitting diodes the default source for roadways and public buildings. Japan’s control of upstream inputs such as photoresists and semiconductor equipment keeps much of the value chain local, shortening lead times for domestic chip producers. Electric-vehicle programs further amplify demand, because adaptive driving beam systems require tens of thousands of addressable chips per vehicle. At the same time, companies hedge against gallium and indium volatility by recycling scrap wafers and qualifying alternative transparent-electrode chemistries.

Key Report Takeaways

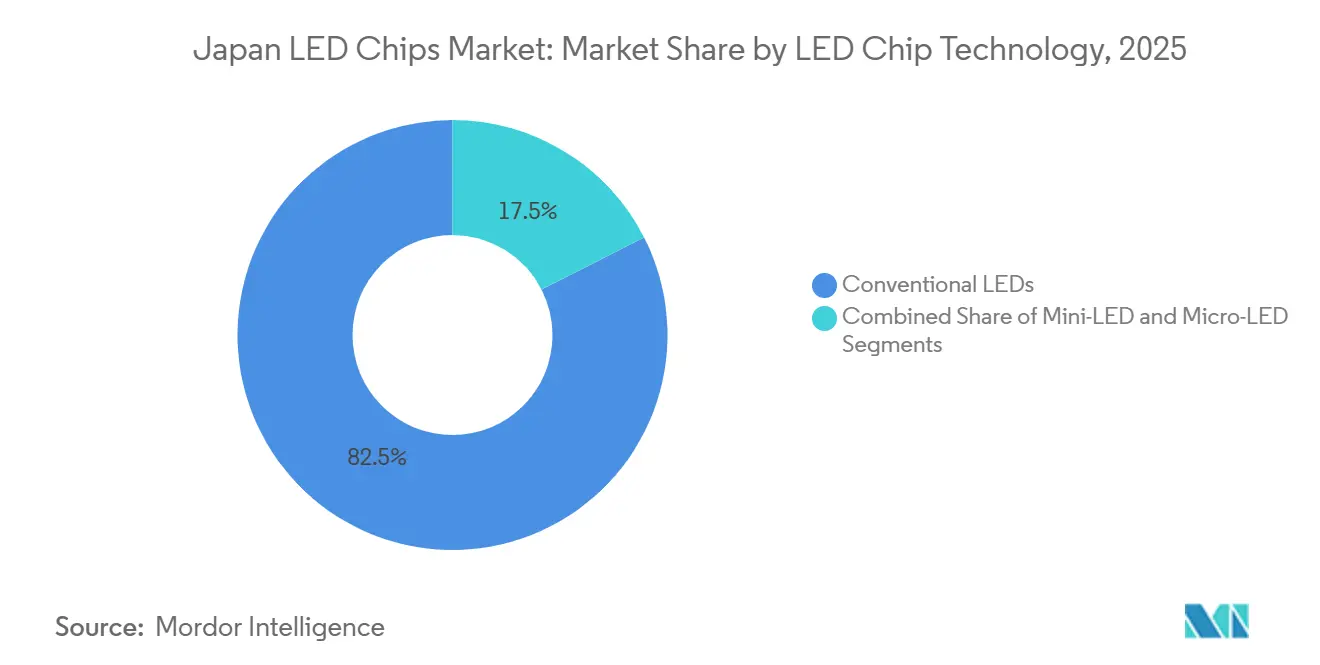

- By LED chip technology, conventional LEDs led with roughly 82.5% of the Japan LED chips market share in 2025, while Micro-LEDs are forecast to grow at nearly 14% CAGR through 2031.

- By semiconductor material, GaN/InGaN devices accounted for about 83% of the Japanese LED chips market size in 2025, and alternatives such as AlGaInP and oxide semiconductors are projected to expand around 13% CAGR.

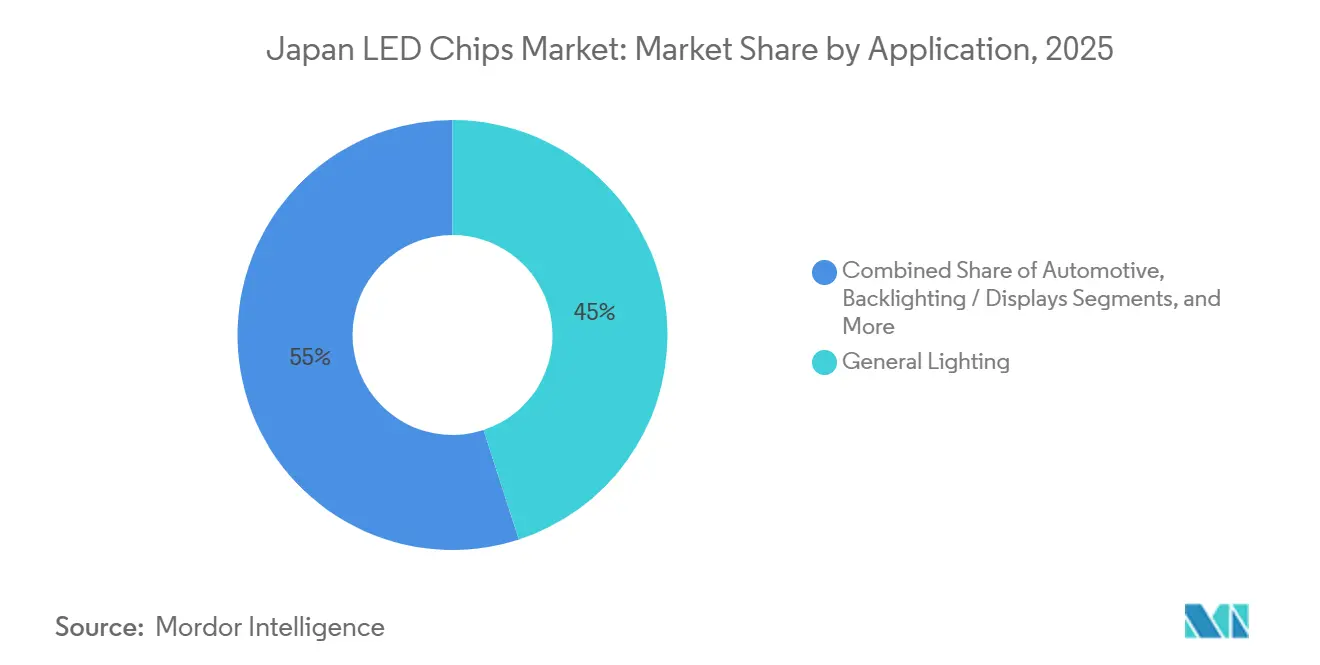

- By application, general lighting captured near 45% revenue share in 2025, but automotive lighting is advancing at almost 15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Adoption of Mini-LED Backlit TVs | +2.1% | Domestic exports to panel hubs in Asia-Pacific | Medium term (2-4 years) |

| Government Incentives for Domestic Semiconductor Production | +1.8% | Kumamoto, Hokkaido, Hamamatsu clusters | Long term (≥ 4 years) |

| Surge in Electric-Vehicle Headlamp Integration | +2.3% | Japan OEM base, global export models | Medium term (2-4 years) |

| Energy-Efficiency Regulations Favoring LED Retrofits | +1.5% | National roads, public buildings, data centers | Short term (≤ 2 years) |

| Increasing Demand for Plant-Factory Horticulture Lighting | +0.9% | Urban vertical farms | Medium term (2-4 years) |

| Growth of Smart Lighting in IoT-Enabled Buildings | +1.1% | Smart-city pilot zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Domestic Semiconductor Production

Japan allocated JPY 1.85 trillion (USD 12.6 billion) in 2023 subsidies for fabs that cover logic, memory, and photonics devices. Support for TSMC’s second Kumamoto plant and Rapidus’s 2-nanometer pilot line finances clean-room infrastructure now shared by compound-semiconductor projects, including LED epitaxy. Workforce training programs in Kyushu and Hokkaido further reinforce the local talent pool, easing recruitment challenges for LED foundries.

Surge in Electric-Vehicle Headlamp Integration

Koito reported that LEDs already represent 82% of its headlamp output and targets 100% by 2030.[2]Nichia Corporation, “Nichia Launches White LED ‘NS2W806H-B2’,” Nichia, nichia.co.jpAdaptive driving beam modules need as many as 16,000 individually addressed emitters, lifting per-vehicle chip counts by two orders of magnitude versus halogen. Nichia and Infineon unveiled a micro-matrix light engine featuring 16,384 emitters that lowers power draw by about 18% compared with preceding solutions, a critical benefit for battery-electric range preservation.

Energy-Efficiency Regulations Favoring LED Retrofits

The Ministry of Land, Infrastructure, Transport and Tourism amended road-lighting standards in October 2025, making LED the mandatory source for all new government-managed luminaires installed after April 2026.[3]Koito Manufacturing, “Integrated Report 2025,” Koito, koito.co.jpTarget penetration is 100% on national roads by 2030. Similar tightening under the Building Energy Efficiency Act accelerates indoor retrofits, while proposed data-center PUE caps below 1.3 push operators toward high-efficacy luminaires that also reduce thermal load.

Rising Adoption of Mini-LED Backlit TVs

Shipments of Mini-LED television panels are on track to top 20 million sets in 2026 as set makers pursue high contrast at a lower cost than OLED. Each 65-inch Mini-LED unit can incorporate 10,000-15,000 mid-power chips, so the trend materially lifts wafer volume for Japanese suppliers. Nichia’s NS2W806H-B2 package, which merges blue and green dies, raises backlight efficacy and widens color gamut without thicker diffuser stacks.[1]Quest Metals, “Indium Prices Surge to Decade Highs,” Quest Metals, questmetals.comExport-oriented demand offsets local TV-assembly decline, though persistent price erosion forces manufacturers to focus on lumen-per-watt leadership and automotive-grade reliability certification.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Disruptions for Gallium and Indium | -1.4% | China-centric raw-material base; single refiner in Japan | Short term (≤ 2 years) |

| High Capital Expenditure for Micro-LED Mass Transfer | -0.8% | Domestic fabs, global equipment supply chain | Medium term (2-4 years) |

| Intensifying Price Pressure from Chinese Suppliers | -1.2% | Export markets for general lighting | Short term (≤ 2 years) |

| Patent Litigation Risks in LED Chip Designs | -0.5% | Cross-border licensing disputes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Micro-LED Mass Transfer

Tool sets that approach 99.99% placement yield remain expensive. Hamamatsu Photonics invested JPY 37 billion (USD 250 million) in 2025 to bring 8-inch wafer processing online, yet the line can still lose profitability if downstream transfer tools underperform.[5]Rare Earth Mining Editor, “Gallium Price 2026: Live Spot, History and MarketSmaller firms often opt to license chip architectures rather than bankroll full Micro-LED back-ends.

Supply Chain Disruptions for Gallium and Indium

China controls nearly all refined gallium and about 70% of indium, and export licensing tightened in 2024. Spot gallium jumped to USD 2,100 per kilogram in March 2026, more than doubling in 14 months.[4]Ministry of Land, Infrastructure, Transport and Tourism, “Revised Road LightingJapanese makers rely on Dowa Holdings for 6N-grade gallium, so any feedstock hiccup or plant outage constrains domestic epitaxy. Indium climbed above USD 550 per kilogram after Beijing cut unwrought shipments 23% year-over-year. Reclamation from obsolete LCD panels helps, but cannot fully offset the shortfall.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Micro-LED Gains Traction Despite Manufacturing Hurdles

Conventional LEDs represented about 82.5% of the Japanese LED chips market share in 2025, anchored by depreciated legacy lines that still deliver competitive lumens-per-dollar for municipal retrofits. Mini-LED bridges performance and cost, giving premium TV brands high local-dimming ratios without OLED expense. The Japan LED chips market size tied to Micro-LED is forecast to expand at a near 14% CAGR because automotive adaptive driving beams and emerging augmented-reality displays require pixel densities that legacy chips cannot achieve.

Nichia’s DominoPLS modules introduced in 2026 cut matrix-lamp cost by integrating micro-arrays onto a common ceramic substrate, simplifying assembly for compact vehicles. Red emitter efficiency below 3 µm remains difficult, but suppliers collaborate with material labs to boost external quantum efficiency beyond 5%, a threshold needed for full-color wearables.

By Semiconductor Material: GaN Dominance Faces Niche Challengers

GaN/InGaN commanded close to 83% of 2025 output thanks to proven growth on sapphire and silicon-carbide templates, which align with existing MOCVD reactors. That leadership secures economies of scale, keeping the core of the Japan LED chips market cost-competitive. Still, demand for deep-UV sterilization, plant-growth spectra, and high-resolution red pixels drives a 13% CAGR for AlGaInP, AlN, and oxide-based alternatives through 2031.

Stanley Electric’s HexaTech unit released 3-inch AlN substrates that boost UVC chip thermal conductivity by roughly 40%, letting water-treatment modules run higher drive currents. Meanwhile, Rohm pairs GaN lighting expertise with power-device lines that enter mass production in 2027, underscoring cross-fertilization of III-nitride knowledge.

By Application: Automotive Segment Accelerates as Lighting Evolves into Sensing

General lighting still delivered about 45% of 2025 revenue, upheld by road-lamp conversions mandated for completion by 2030. Yet automotive products register the fastest climb at nearly 15% CAGR, propelling the overall Japan LED chips market size upward as each adaptive driving beam contains thousands of dies.

Koito’s BladeScan system sweeps 12 high-output LEDs across mirrors to emulate 300 point sources, improving forward visibility without glare. Stanley Electric couples rear lamps with pattern-generating optics that cut driver reaction time by two seconds, hinting that future demand will come from smart modules that both illuminate and communicate.

Geography Analysis

Japan sits inside an Asia-Pacific production web where China hosts about 40% of global Micro-LED capacity and Taiwan another 35%. Domestic fabs, therefore, focus on high-purity epitaxy, reliability testing, and automotive compliance, niches less vulnerable to low-cost rivals. TSMC’s ongoing Kumamoto expansion brings advanced lithography, ultrapure water, and process-equipment vendors into Kyushu, indirectly strengthening the Japan LED chips market by clustering shared suppliers.

Photoresist players such as Tokyo Ohka Kogyo dominate 90% of the global supply, and new lines in Ibaraki safeguard stock for compound-semiconductor lithography. Equipment makers Tokyo Electron, Advantest, and DISCO hold roughly 43% worldwide assembly-and-test share, affording domestic chip houses priority access to next-generation dicing and metrology tools.

Cross-border acquisitions, including Ushio’s purchase of Osram’s specialty-lamp unit, broaden the Japanese footprint in industrial and entertainment lighting ahead of the 2027 World Expo in Osaka. Government roadmap documents target a 40% energy cut in data centers via photonics-electronics convergence, a goal that aligns with compound-semiconductor packaging skills inherent to LED makers.

Competitive Landscape

The Japan LED chips market features medium concentration: the top five suppliers hold roughly 55-60% combined revenue, positioning the field at a 6 on a 10-point concentration scale. Nichia remains the premium benchmark, wielding more than 3,000 active patents that protect flip-chip and phosphor-conversion methods. Even so, 2025 revenue slipped a few points as inventory overhang hit global lighting channels. Toyoda Gosei leverages automotive ties with Toyota to secure early design wins in interior ambient modules such as Dynamic Shadow Illumination that sync to music and proximity sensors.

Stanley Electric broadened its scope by buying Iwasaki Electric for JPY 70.3 billion, fusing outdoor-lighting catalogs with automotive light-source scale. Rohm cross-licenses SiC power-device processes from TSMC, using GaN epitaxy heritage to penetrate inverter modules needed for fast-charging stations. Sharp Display Solutions entered chip-on-board Flip-Chip tiles that cut power up to 60% in conference-room walls, proof that display and lighting lines increasingly overlap.

Chinese challengers differentiate on scale. Sanan’s Lumileds takeover secures richer patent cover, allowing aggressive pricing in mid-power categories. Japanese vendors counter with guaranteed lumen maintenance beyond 10,000 hours at 105 °C and traceable supply chains down to metal-organic precursors, attributes prized by auto and medical customers who cannot afford recalls.

Japan LED Chips Industry Leaders

Nichia Corporation

Toyoda Gosei Co., Ltd.

Stanley Electric Co., Ltd.

Rohm Co., Ltd.

Sharp Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: TSMC will boost its second Kumamoto fab to 3 nm nodes, escalating total spend to JPY 2.6 trillion (USD 16.8 billion) with METI support near JPY 1.23 trillion (USD 7.9 billion).

- February 2026: Rapidus raised JPY 267.6 billion (USD 1.73 billion) to ready a 2 nm pilot line, backed by Toyota, Sony, NTT, and METI’s Information-Technology Promotion Agency.

- January 2026: Stanley Electric agreed to acquire Iwasaki Electric for JPY 70.3 billion (USD 454 million) to expand public-infrastructure lighting and ultraviolet solutions.

Japan LED Chips Market Report Scope

An LED chip, also known as an LED die, is a semiconductor device consisting of a p-n junction fabricated from compound semiconductor materials such as gallium nitride (GaN), indium gallium nitride (InGaN), or aluminum gallium indium phosphide (AlGaInP), which emits incoherent narrow-spectrum light through the process of electroluminescence when an electric current is applied in the forward direction, and serves as the fundamental light-emitting component that is subsequently packaged with phosphors, electrodes, and encapsulants to form LED lamps, modules, or displays.

The Japan LED Chip Market Report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, AlGaInP, and Other Semiconductor Materials), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| By LED Chip Technology | Conventional LEDs |

| Mini-LED | |

| Micro-LED | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| Other Semiconductor Materials | |

| By Application | General Lighting |

| Automotive | |

| Backlighting / Displays | |

| Consumer Electronics | |

| Industrial / Specialty Lighting |

Key Questions Answered in the Report

What is the forecast value of the Japan LED chips market in 2031?

It is projected to reach USD 5.36 billion by 2031.

How fast is the automotive LED segment growing?

Automotive lighting chips are advancing at close to 15% CAGR from 2026 to 2031, the fastest among all applications.

Which semiconductor material leads production in Japan?

GaN/InGaN devices account for nearly 83% of national output as of 2025.

Why are gallium prices a concern for LED makers?

China’s export controls lifted spot gallium to about USD 2,100 per kilogram in March 2026, creating cost and supply risks for Japanese epitaxy fabs.

Page last updated on: