Europe LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

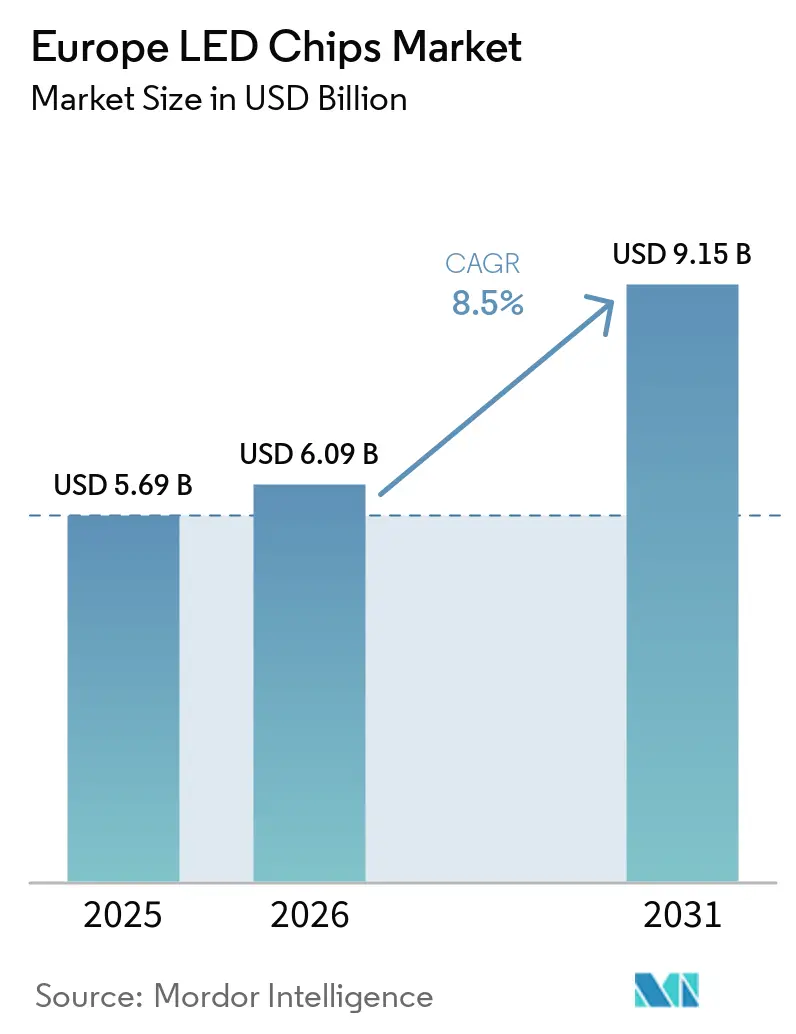

| Base Year Market Size (2025) | USD 5.69 Billion |

| Market Size (2026) | USD 6.09 Billion |

| Market Size (2031) | USD 9.15 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe LED Chips Market Analysis by Mordor Intelligence

The Europe LED chip market size is expected to increase from USD 5.69 billion in 2025 to USD 6.09 billion in 2026 and reach USD 9.15 billion by 2031, growing at a CAGR of 8.5% over 2026-2031. Robust policy support for energy-efficient lighting, a wave of automotive headlamp upgrades, and rapid display technology innovation are steering sustained demand across general lighting, automotive, and premium television backlights. Large European municipalities are limiting electricity outlays by converting high-pressure sodium fixtures to smart LED luminaires, while display OEMs are multiplying LED die counts through mini-LED backlighting to match OLED picture quality. Automakers are accelerating adaptive-beam adoption ahead of the January 2027 ECE regulatory deadline, and local wafer-level packaging projects backed by the EU Chips Act are gradually easing the region’s reliance on Asian contract foundries. Against this backdrop, the Europe LED chip market continues to attract capital into micro-LED pilot lines, UV-C disinfection products, and GaN-on-silicon substrates that promise margin resilience amid raw-material volatility.

Key Report Takeaways

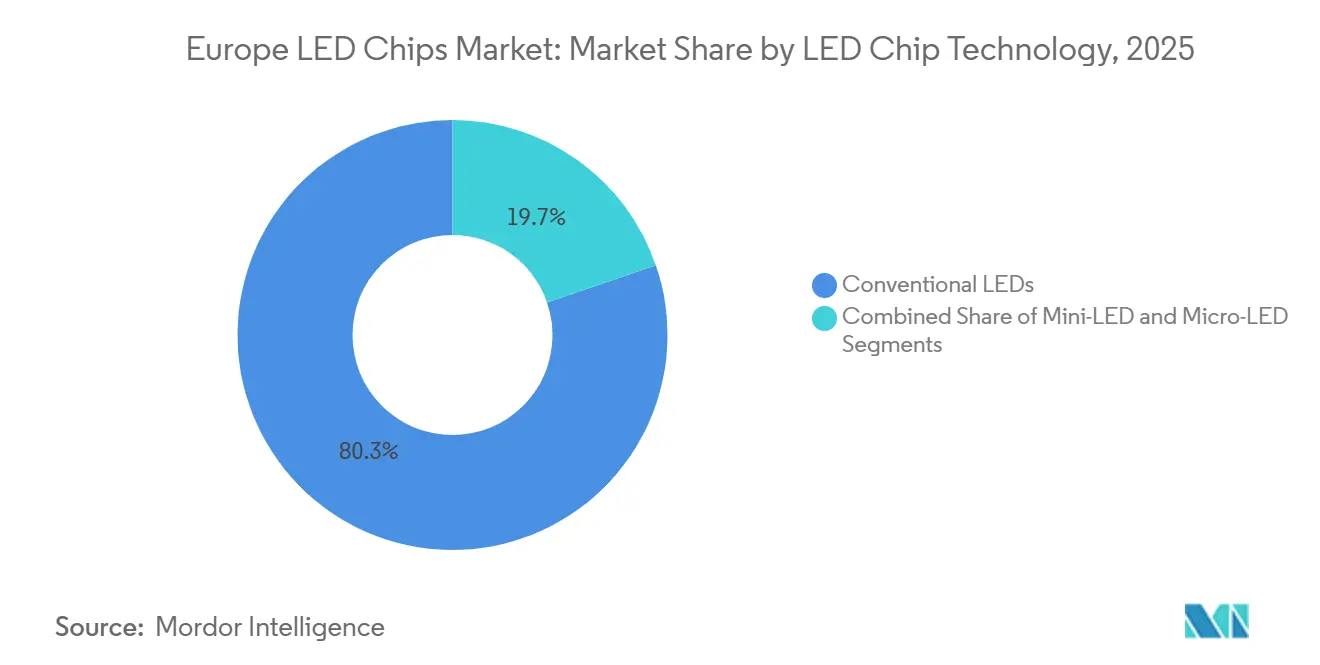

- By LED chip technology, conventional LEDs held roughly 80.26% Europe LED chip market share in 2025, while micro-LED platforms advanced at a 12.34% CAGR through ultra-premium display pilots.

- By semiconductor material, GaN and InGaN compounds accounted for nearly 85.3% of Europe LED chip market size in 2025, whereas AlGaN-based “other materials” grew at a 13.45% CAGR on the back of UV-C disinfection demand.

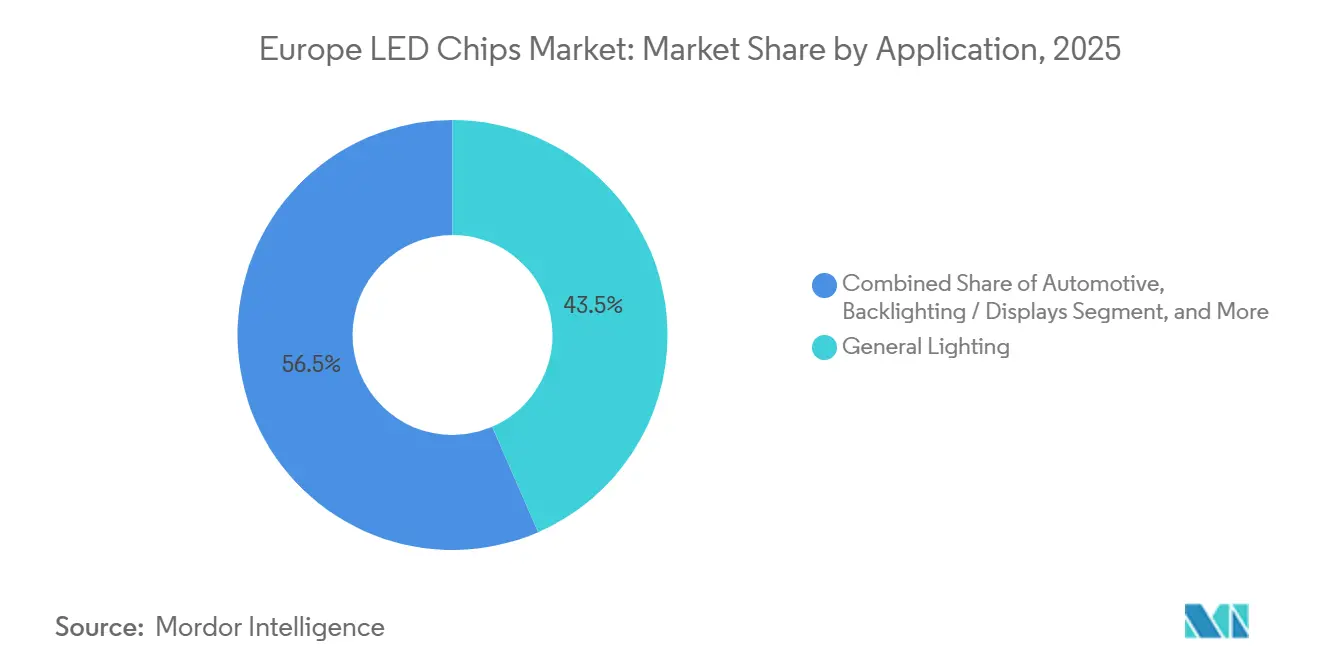

- By application, general lighting commanded a 42.3% share of the Europe LED chip market in 2025, but automotive headlamp content is expanding at a 15.9% CAGR through 2031.

- By geography, Germany led with a 25.47% revenue share in 2025, and France posted the fastest CAGR of 13.2% on the strength of municipal streetlight retrofits.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Adoption of Mini-LED Backlit Displays | +1.8% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Expanding EV Headlamp Integration | +2.1% | Germany, France, Rest of Europe (Italy, Spain) | Medium term (2-4 years) |

| Shift Toward Smart City Streetlighting | +1.5% | France, Germany, Rest of Europe (Bulgaria, Spain) | Long term (≥ 4 years) |

| EU Green Deal Energy-Efficiency Targets | +1.3% | Europe-wide | Long term (≥ 4 years) |

| Increased Local Wafer-Level Packaging Capacity | +0.9% | Germany, Austria | Long term (≥ 4 years) |

| Proliferation of UV-C LED Disinfection Systems | +0.7% | Germany, United Kingdom, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Smart City Streetlighting

Municipalities are retrofitting public lighting to shrink electricity bills by up to 75%. Paris awarded a EUR 700 million (USD 763 million) contract in 2024 to replace 70,000 fixtures with LED luminaires equipped with remote diagnostics. Mulhouse committed EUR 24 million (USD 26.16 million) to modernize 14,000 lamps, targeting completion by summer 2026. France’s Lum'ACTEE+ program earmarked EUR 15 million (USD 16.35 million) for a nationwide upgrade of up to 4 million luminaires by 2028. Smart controls boost per-pole semiconductor content by adding driver ICs and connectivity modules, elevating the overall Europe LED chip market value.

Expanding EV Headlamp Integration

Europe’s vehicle makers are embedding increasingly dense LED matrices to comply with amendments to ECE Regulation 123, which mandate adaptive front lighting on new models after January 2027. ams OSRAM’s EVIYOS HD25 micro-LED array offers 25,600 addressable pixels and is already in volume production for the Audi Q6 e-tron and the NIO ET9. Volkswagen’s 2026 Touareg and Tiguan carry 19,200-pixel IQ. Light headlamps that maintain maximum illumination while avoiding glare for oncoming traffic.[3]Volkswagen AG, “IQ.Light HD Matrix Headlamp Specifications,” volkswagen.com German OEM concentration anchors chip demand locally, and Nichia’s 2024 Aachen innovation center strengthens vendor collaboration with automakers.

EU Green Deal Energy-Efficiency Targets

The Ecodesign for Sustainable Products Regulation 2024/1781 enforces stringent efficacy thresholds that effectively phase out halogen and fluorescent lamps by 2027. The recast 2024 Energy Performance of Buildings Directive stipulates that all new buildings must approach zero-energy standards by 2030, a goal only attainable with LED lighting. These overlapping measures expand retrofit cycles across Europe’s estimated 1.5-2 billion installed light points, anchoring baseline chip demand even as higher-growth niches mature.

Rapid Adoption of Mini-LED Backlit Displays

Premium television and monitor makers are positioning mini-LED as a cost-effective bridge between conventional LCDs and OLED panels, shipping 9.3 million mini-LED TVs in 2025 after 65-inch panel costs fell into the USD 1,100-1,200 band, only 5-10% above OLED alternatives.[1]Omdia Analysts, “Mini-LED TV Shipments Surpass OLED in 2025,” omdia.tech.informa.comSamsung and LG Display unveiled 27- to 32-inch gaming monitors at CES 2026 featuring up to 4,608 local dimming zones and 1,600 nits peak brightness.[2]European Commission, “Ecodesign for Sustainable Products Regulation 2024/1781,” ec.europa.euEach 65-inch mini-LED television consumes 10,000-25,000 discrete dies, compared with roughly 150 for edge-lit LCDs, translating into a step-change in Europe's LED chip market demand. Consumer appetite is concentrated in Germany and the United Kingdom, where higher disposable incomes and greater penetration of gaming hardware foster adoption. Though LG Display projects second-generation OLEDs to hit 1,500 nits in mid-2026, mini-LED retains a cost advantage in screen sizes above 75 inches.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Volatility of Gallium and Indium | −1.2% | Europe-wide | Short term (≤ 2 years) |

| High Capital Cost for Micro-LED Mass Transfer | −0.9% | Germany, France, United Kingdom | Medium term (2-4 years) |

| IP Fragmentation and Royalty Disputes | −0.5% | Europe-wide | Long term (≥ 4 years) |

| Competition From OLED in Premium Displays | −0.6% | Germany, United Kingdom, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost for Micro-LED Mass Transfer

The research company estimated that, in 2025, 86.2% of the materials stemmed from substrates and transfer tools. Springer's 2024 review concluded that yields above 99.9999% are necessary to match OLED panel economics, but current equipment generations rarely meet this benchmark on large substrates. Applied Materials and peers are striving to lift throughput tenfold, yet cost parity with OLED appears unlikely before 2028-2030. European display assemblers, lacking the multibillion-dollar capex muscle of Korean giants, may be forced to focus on niche automotive HUD and wearable panels until the economics improve.

Supply Volatility of Gallium and Indium

China controls as much as 99% of refined gallium and triggered a 365% spike in the European spot price between January 2023 and December 2025 after imposing export licenses.[5]United States Geological Survey, “Gallium and Indium Market Summary 2025,” usgs.gov The European Union relies on imports for roughly 90% of its gallium, leaving local LED assemblers exposed to price shocks. Greece-based Metlen Energy and Metallurgy is investing EUR 295.5 million (USD 322.1 million) in a 50-ton-per-year refinery scheduled for 2027, but output will cover only about one-fifth of Europe’s projected demand. Indium has echoed gallium’s volatility, with prices up 180% during 2023-2025, while germanium, vital to infrared LEDs, jumped 400% on similar controls, further squeezing chip margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Micro-LED Gains Despite Conventional Scale

Conventional LEDs dominated the European LED chip market share at 80.26% in 2025, buoyed by mature supply chains and sub-USD 0.10 pricing for mid-power die suited to general lighting and exterior automotive lamps. Incremental efficiency gains, such as Nichia’s 757 series reaching 220 lumens per watt at 65 milliamps, keep the segment competitive for price-sensitive use cases. Mini-LED occupies the middle ground, enabling thousands of local dimming zones without the mass-transfer hurdles that restrain micro-LED, and is becoming the default upgrade path for premium televisions and in-vehicle infotainment screens.

Micro-LED is advancing at a 12.34% CAGR through pilot deployments in ultra-large televisions, smartwatch faces with sub-10-micrometer pixels, and automotive heads-up displays requiring 10,000-nit brightness. PlayNitride and Plessey are pushing monolithic micro-LED-on-silicon arrays below 5 micrometers, positioning the architecture as a successor to OLED in next-generation AR headsets. Conventional LED revenue will plateau as Ecodesign rules compress retrofit windows, yet its vast installed base secures a lengthy tail. Mini-LED is expected to exceed 15 million television shipments by 2028, maintaining momentum until micro-LED hits mainstream cost thresholds.

By Semiconductor Material: GaN Dominance Confronts UV-C Disruption

GaN and InGaN substrates accounted for roughly 85.3% of Europe's LED chip market in 2025, as they underpin blue and white emitters for lighting, display, and automotive applications. Infineon’s EUR 5 billion Dresden Smart Power Fab integrates a 300-millimeter GaN roadmap, promising 25-35% wafer-cost reductions and on-die driver integration. AlGaInP remains indispensable for red and amber wavelengths used in automotive tail lamps and horticultural lighting, with Broadcom’s latest portfolio reaching up to 480 lumens per watt.

AlGaN compounds are gaining share in UV-C segments that grew 13.45% annually, catalyzed by Ferdinand-Braun-Institut’s 233-nanometer micro-LED breakthrough and ams OSRAM’s 265-nanometer production ramp, delivering 200 milliwatts of output at 10.2% wall-plug efficiency. Crystal IS supplies AlGaN-on-sapphire dies to European water-treatment OEMs, and imec’s 300-millimeter GaN-on-silicon test runs show 15-20% cost savings over sapphire, although thermal constraints currently limit mainstream adoption in headlamps. GaN’s share remains resilient, but UV-C growth offers differentiated margin opportunities for manufacturers with advanced epitaxy expertise.

By Application: Automotive Races Ahead of General Lighting

General lighting retained 42.3% of the European LED chip market in 2025 as residential and commercial retrofits accelerated ahead of the 2027 halogen phase-out, yet commoditization dragged average die prices below USD 0.15. Streetlight conversions, such as Paris’s 70,000-unit program, sustain volume but offer limited margin. Automotive applications are recording a 15.9% CAGR thanks to matrix headlamp platforms like ams OSRAM’s EVIYOS HD25, which multiplies chip counts per vehicle severalfold. Light HD system illustrates how a single model refresh can trigger large incremental die orders.

Mini-LED backlights in premium televisions and monitors are another growth pocket, with each 65-inch panel consuming tens of thousands of chips. Smartphone backlighting is tilting toward OLED, but laptops and tablets still rely on conventional or mini-LED arrays. Industrial niches spanning horticulture, UV curing, and infrared vision offer premium pricing at modest volumes. In revenue terms, automotive and display use cases are set to outpace general lighting’s incremental gains through 2031, even though lighting will remain the single largest application by volume.

Geography Analysis

Germany led the Europe LED chip market with 25.47% revenue share in 2025, underpinned by robust automotive LED demand from Volkswagen Group, BMW, and Mercedes-Benz. Nichia’s Aachen innovation center deepens collaboration with German OEMs, and ams OSRAM’s Austria packaging site supplies wafer-level arrays to German tier-1 suppliers. The country’s dominance draws strength from a dense network of automotive design centers, yet future growth will depend on sustaining EV headlamp innovation and aligning with domestic wafer-level capacity coming online after 2027.

France is the fastest-growing geography at a 13.2% CAGR. The EUR 700 million (USD 763 million) Paris retrofit and the Lum'ACTEE+ program’s EUR 15 million (USD 16.35 million) allocation for up to 4 million luminaires illustrate how centralized subsidy frameworks expedite procurement. Aggressive municipal timelines could narrow France's revenue gap with Germany by the late 2020s. Smart city projects that integrate dimming schedules and remote diagnostics further raise semiconductor content per pole, benefiting upstream LED chip suppliers.

The United Kingdom and the broader Rest of Europe, Italy, Spain, the Nordics, and Eastern Europe offer steady, if more fragmented, opportunities. Post-Brexit border friction prompted some module assemblers to relocate final assembly to mainland sites to maintain frictionless EU access. Cohesion funds support streetlight retrofits in Bulgaria and Spain, while Nordic countries exhibit high per-capita LED adoption due to prolonged winter darkness but contribute modest absolute volume. Overall, Germany’s automotive anchor and France’s infrastructure push define regional growth dynamics through 2031.

Competitive Landscape

The Europe LED chip market shows moderate concentration. Nichia and ams OSRAM collectively hold roughly a 35-40% share, relying on broad YAG phosphor and nitride epitaxy patent portfolios. South Korean vendors Samsung, LG Innotek, and Seoul Semiconductor control 25-30%, leveraging vertical integration spanning wafers to finished modules. Nichia’s recent German court victories against Everlight and Dominant underscore the role of litigation in protecting royalties, while a 2025 cross-license with ams OSRAM resolved overlapping claims, easing supply for automotive OEMs.

Strategically, European suppliers are localizing production. ams OSRAM secured EUR 227 million (USD 247.43 million) under the EU Chips Act for its Premstätten wafer-level packaging line, and Infineon landed EUR 1 billion (USD 1.09 billion) to co-fund its EUR 5 billion (USD 5.45 billion) Dresden Smart Power Fab, which includes a GaN roadmap. These moves aim to reduce Asia-Pacific dependency that exposed weaknesses during the 2020-2022 chip shortages. Niche innovators such as Plessey and Aledia target micro-LED arrays and 3D GaN-on-silicon nanowires, respectively, banking on differentiated IP rather than scale.

Chinese entrants are expanding via acquisition and price competition. UV-C LEDs and micro-LED-on-silicon displays offer white-space opportunities for both incumbents and challengers, and success will hinge on integrating driver ICs, optical filters, and thermal solutions into compact chip-scale packages that meet ISO 26262 and IEC 60601 standards.

Europe LED Chips Industry Leaders

Nichia Corporation

OSRAM Opto Semiconductors GmbH

Samsung Electronics Co., Ltd.

Lumileds Holding B.V.

Cree LED (Penguin Solutions)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ams OSRAM introduced Night Breaker automotive LED lamps for the European aftermarket, widening retrofit options for legacy halogen vehicles.

- February 2026: ams OSRAM divested its non-optical sensor portfolio to Infineon for EUR 570 million (USD 621.3 million) to sharpen focus on optical semiconductors.

- February 2026: Cree Lighting entered a long-term manufacturing pact to safeguard luminaire supply for European commercial clients.

- October 2025: Nichia and ams OSRAM signed a broad cross-license covering nitride LEDs and chip-scale packages, ending longstanding European litigation.

Europe LED Chips Market Report Scope

An LED chip, also known as an LED die, is a semiconductor device consisting of a p-n junction fabricated from compound semiconductor materials such as gallium nitride (GaN), indium gallium nitride (InGaN), or aluminum gallium indium phosphide (AlGaInP), which emits incoherent narrow-spectrum light through the process of electroluminescence when an electric current is applied in the forward direction, and serves as the fundamental light-emitting component that is subsequently packaged with phosphors, electrodes, and encapsulants to form LED lamps, modules, or displays.

The Europe LED Chip Market Report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, AlGaInP, and Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting), and Geography (United Kingdom, Germany, France, and Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| United Kingdom |

| Germany |

| France |

| Rest of Europe |

| By LED Chip Technology | Conventional LEDs |

| Mini-LED | |

| Micro-LED | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| Other Semiconductor Materials | |

| By Application | General Lighting |

| Automotive | |

| Backlighting / Displays | |

| Consumer Electronics | |

| Industrial / Specialty Lighting | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe LED chip market and how fast is it growing?

The Europe LED chip market size is projected to rise from USD 6.09 billion in 2026 to USD 9.15 billion by 2031 at an 8.5% CAGR.

Which LED chip technology segment is expanding the fastest?

Micro-LED platforms are advancing at a 12.34% CAGR as vendors target ultra-premium displays and automotive heads-up units.

Why is automotive demand outpacing general lighting in Europe?

Adaptive driving beam mandates effective January 2027 and rising EV production lift chip counts per vehicle, pushing automotive applications to a 15.9% CAGR.

Which European country offers the strongest growth opportunity for LED chips?

France records the fastest CAGR at 13.2% owing to large-scale municipal streetlight retrofits backed by centralized subsidies.

Page last updated on: