Southeast Asia LED Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.76 Billion |

| Market Size (2026) | USD 2.99 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 10.04% CAGR |

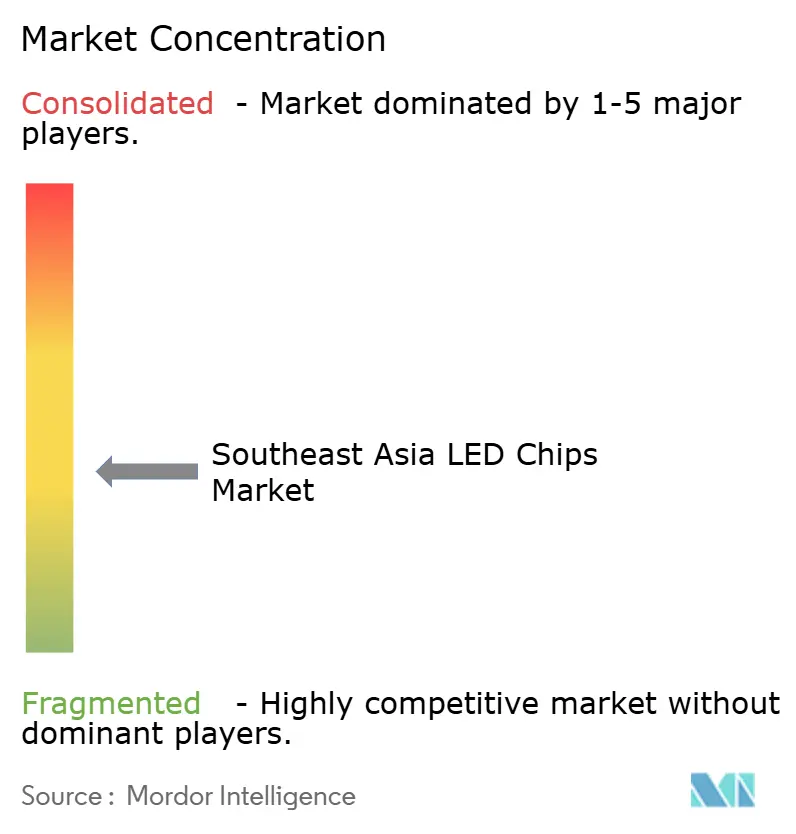

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia LED Chips Market Analysis by Mordor Intelligence

The Southeast Asia LED chips market size was valued at USD 2.76 billion in 2025 and is estimated to grow from USD 2.99 billion in 2026 to reach USD 4.82 billion by 2031, at a CAGR of 10.04% during the forecast period 2026-2031. The Southeast Asia LED chips market is moving into a stronger growth phase as lighting efficiency rules, smart-city spending, and electric vehicle adoption expand demand beyond conventional illumination. Minimum energy performance standards are raising the baseline for chip performance, which is shifting purchasing toward higher-efficacy products and away from low-grade replacements. The move from conventional phosphor-converted designs toward direct-emissive and pixelated formats is also changing where value sits in the supply chain, which is pulling more attention toward upstream design, epitaxy, and packaging capabilities. The region continues to serve as a major production base, but it is also becoming a deeper demand center as urban infrastructure programs, connected lighting systems, and automotive lighting upgrades move from isolated projects into broader deployment. Competition remains moderately fragmented, yet the market is steadily favoring suppliers that can pair scale with strong intellectual property, automotive-grade qualification, and localized manufacturing footprints across Asia.

Key Report Takeaways

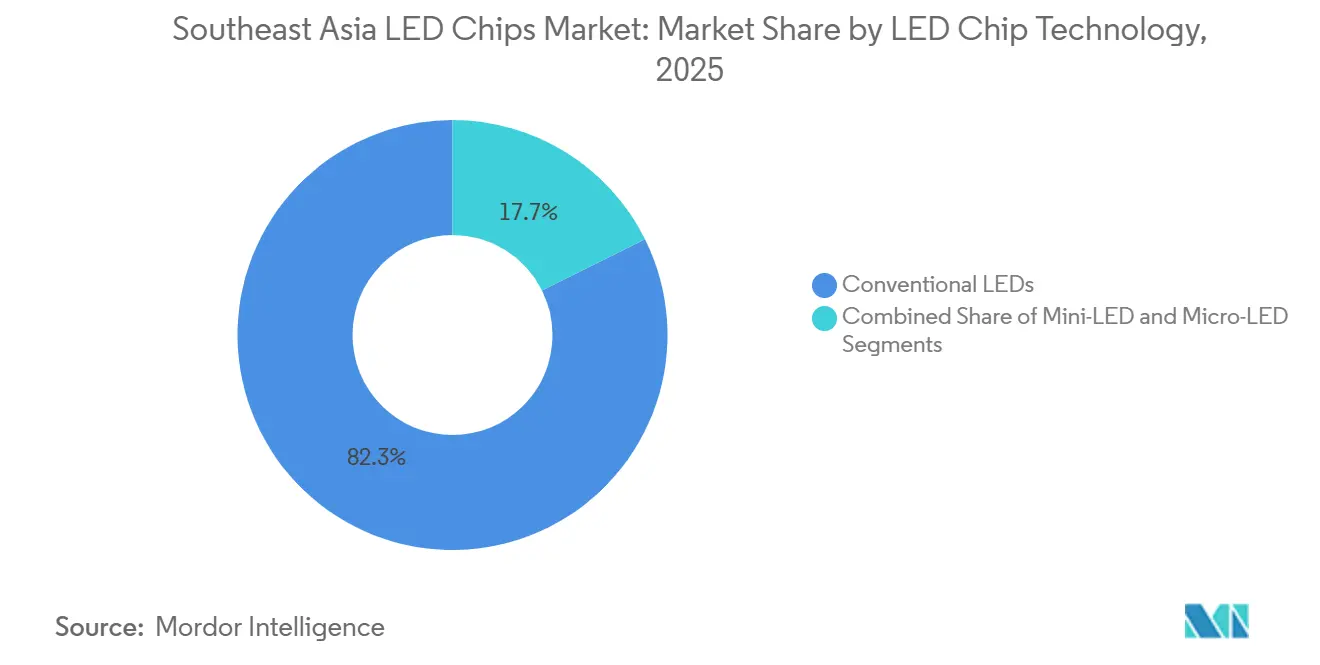

- By LED chip technology, conventional LEDs held 82.34% of the Southeast Asia LED chips market share in 2025, while micro-LED is projected to expand at a 12.04% CAGR through 2031.

- By semiconductor material, GaN and InGaN accounted for 81.78% share of the Southeast Asia LED chips market size in 2025, while other semiconductor materials are expected to grow at an 11.89% CAGR through 2031.

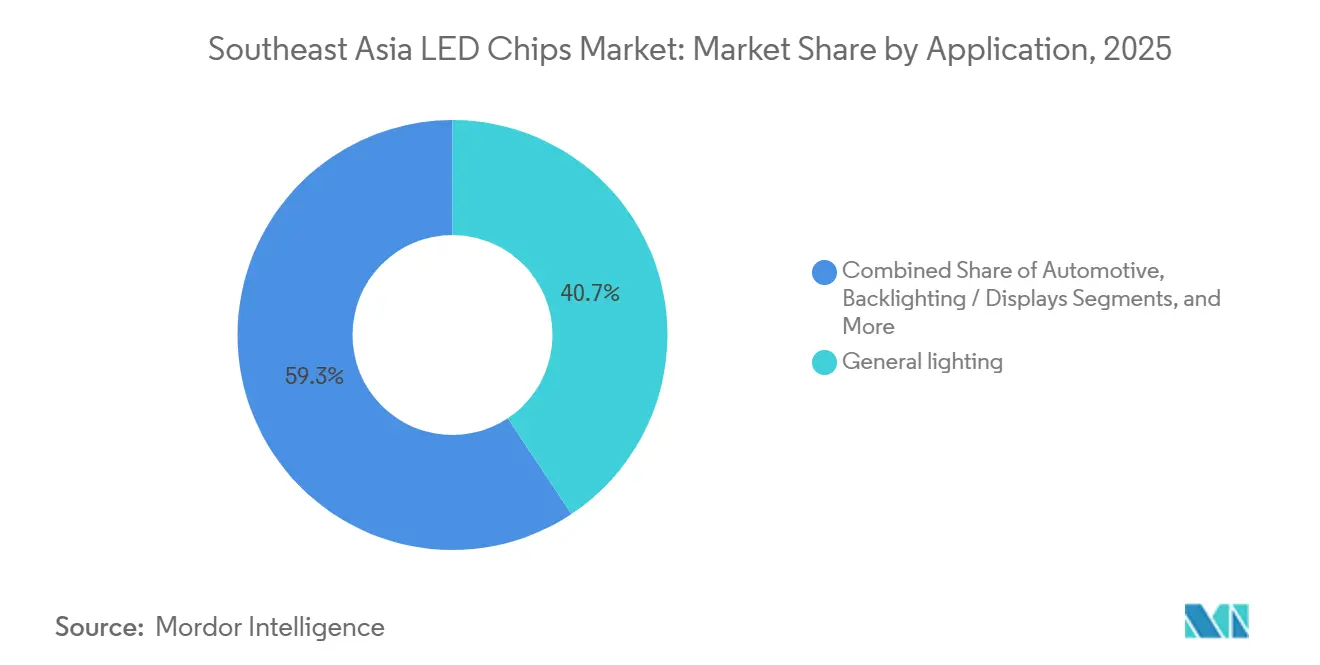

- By application, general lighting captured 40.67% revenue share in 2025, while automotive is projected to advance at a 12.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia LED Chips Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Government Incentives for Energy-Efficient Lighting | +2.5% | ASEAN-wide, concentrated gains in Singapore, Vietnam, Malaysia, and Indonesia | Short term (≤ 2 years) |

| Growth in Automotive LED Headlamp Adoption | +2.2% | China, South Korea, Japan, with spill-over to Thailand and India | Medium term (2-4 years) |

| Rising Penetration of Smart Homes and IoT-Enabled Lighting | +1.8% | Singapore, Malaysia, Thailand, extending to Vietnam and Indonesia | Medium term (2-4 years) |

| Accelerating Urban Infrastructure Projects Across ASEAN Capitals | +1.5% | ASEAN core cities, including Jakarta, Kuala Lumpur, Ho Chi Minh City, and Manila | Medium term (2-4 years) |

| Localization of Mini-LED Backlight Supply Chains | +0.8% | China, Taiwan, South Korea, with downstream spill-over to Malaysia and Vietnam | Short term (≤ 2 years) |

| Emerging Micro-LED Pilot Production in Singapore and Malaysia | +0.5% | Singapore and Malaysia, with early gains in Penang and Jurong Innovation District | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Government Incentives for Energy-Efficient Lighting

Policy-backed efficiency upgrades remain the clearest near-term demand driver for the Southeast Asia LED chips market. Singapore’s Energy Efficiency Grant was extended from April 2026 to March 2027 and then expanded to all sectors through March 2028, with support of up to 70% for SMEs that invest in pre-approved LED lighting equipment.[1]Singapore National Environment Agency and GoBusiness, “Energy Efficiency Grant (EEG),” GoBusiness Singapore, gobusiness.gov.sgThat program matters not only because it lowers purchase cost, but also because it sets a higher technology floor for qualifying lighting systems, which lifts demand for better-performing chips. At the regional level, the ASEAN Center for Energy has been pushing harmonized MEPS for non-directional LED lamps at 80 lumens per watt, which is helping member states move toward a more consistent efficiency baseline.[2]ASEAN Centre for Energy, “Round-Robin Testing for Lighting Appliances in ASEAN, An Assessment of Testing Laboratory Capacity in Supporting the MEPS for Lighting Appliances,” ASEAN Centre for Energy, aseanenergy.orgAs those rules are enforced more consistently, replacement cycles are shifting from simple lamp swaps toward higher-efficacy systems with a better chip mix. That dynamic gives the Southeast Asia LED chips market a more durable volume base because policy demand is less dependent on short consumer cycles than discretionary electronics spending.

Growth in Automotive LED Headlamp Adoption

Automotive is becoming the most specification-driven demand center in the Southeast Asia LED chips market. The segment is already the fastest-growing application in the forecast period, and the reason is not just LED replacement, but the move toward adaptive and pixelated lighting systems that require denser and more precise chip arrays. ams OSRAM’s 2026 product and strategy updates show that automotive lighting platforms are now being treated as a core growth area within its digital photonics transition, especially in pixelated and intelligent lighting architectures. The company’s March 2026 launch of an ultra-efficient micro-LED array built on its EVIYOS platform also shows how automotive-grade chip development is spilling into adjacent high-value uses, which confirms the maturity of this design path. As vehicle makers push more advanced headlamp functions into mainstream platforms, demand is shifting toward chips that support thermal stability, beam precision, and long qualification cycles. That change raises entry barriers and gives the Southeast Asia LED chips market a stronger profit pool in automotive than in standard illumination.

Rising Penetration of Smart Homes and IoT-Enabled Lighting

Connected lighting is adding a different layer of demand to the Southeast Asia LED chips market. In these systems, the chip is not selected only for brightness and cost, but also for tunability, color consistency, current stability, and long operating life under connected use conditions. That makes smart-home lighting less favorable for low-end commodity chips and more favorable for products with better performance control. Mordor Intelligence’s ASEAN smart homes coverage shows that Thailand’s IoT ecosystem is advancing toward USD 2.19 billion by 2030, which supports the broader digital infrastructure that connected lighting devices rely on. As smart switches, app-linked luminaires, and hub-free devices spread through major cities and then secondary urban areas, the baseline chip specification continues to rise. This gives the Southeast Asia LED chips market a steady upgrade path even when unit growth in standard lamps starts to mature.

Accelerating Urban Infrastructure Projects Across ASEAN Capitals

Public infrastructure programs are creating a stable volume base for the Southeast Asia LED chips market. The ASEAN Smart City Action Plan 2026-2035, adopted in September 2025, gives a formal framework for scaling digital and energy-efficient urban systems across 26 pilot cities in the region. That matters because street-lighting upgrades are one of the first categories that city administrations can deploy at scale with clear energy savings and visible public benefit. The OECD also noted in 2025 that 40% of urban infrastructure investment in Southeast Asia is expected to involve energy transition components, which supports the long pipeline for the intelligent lighting system.[3]Organisation for Economic Co-operation and Development, “Financing Sustainable Cities in Southeast Asia,” OECD Publishing, oecd.org As more projects move from pilot stages to funded rollout, procurement shifts from low-cost lamp replacement toward networked luminaires with better optical control and service life. This keeps the Southeast Asia LED chips market exposed to a stream of institutional demand that complements private construction and consumer replacement demand. It also improves visibility for suppliers that can serve municipal projects with reliable scale and compliance documentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for Epitaxial Wafer Fabrication | -1.5% | ASEAN-wide, most acute in Malaysia, Vietnam, and Indonesia where greenfield capacity is planned | Medium term (2-4 years) |

| Price Volatility in Key Raw Materials Such as Gallium and Indium | -1.2% | Global, with highest impact on non-Chinese manufacturers across Taiwan, South Korea, and Southeast Asia | Short term (≤ 2 years) |

| Supply-Demand Imbalance for Trained Optoelectronics Workforce | -0.8% | Malaysia, Singapore, Vietnam, with spill-over to India and Indonesia | Medium term (2-4 years) |

| Environmental Compliance Costs for Wastewater and Chemical Disposal | -0.6% | China, Taiwan, Malaysia, with stricter enforcement in Taiwan and ASEAN export-oriented facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Epitaxial Wafer Fabrication

Capital intensity remains a major barrier to deeper local supply expansion in the Southeast Asia LED chips market. Mordor Intelligence’s coverage of Asia-Pacific LED epitaxy equipment shows that advanced 200 mm batch MOCVD tools still require multi-million-dollar investment per unit when metrology, abatement, and wafer handling are included. That cost burden is difficult for new entrants in ASEAN markets because demand visibility is not yet as deep as it is in Taiwan, South Korea, or China. Even when incentive programs offset part of the upfront cost, fabs still need to absorb long depreciation cycles, service contracts, and consumable expenses. This slows greenfield investment and keeps epitaxial capacity concentrated among well-funded incumbents with established customer relationships. It also means the Southeast Asia LED chips market can grow strongly in assembly, packaging, and downstream design without seeing the same pace of expansion in upstream wafer fabrication. The result is a supply chain that keeps improving, but still depends heavily on a limited group of regional leaders for core chip-making capacity.

Price Volatility in Key Raw Materials Such as Gallium and Indium

Raw material volatility remains a structural constraint for the Southeast Asia LED chips market because gallium and indium sit at the core of high-brightness LED production. These metals are not easily replaced in the main nitride and compound semiconductor pathways used across blue, white, green, and specialty LED devices. When access conditions tighten or export controls reshape trade flows, cost pressure moves quickly into chip manufacturing economics, especially for producers that do not sit inside the most integrated supply networks. That pressure is more serious for suppliers outside China because they face weaker purchasing leverage and less direct access to upstream material pools. San’an Optoelectronics’ 2025 annual report also shows that major producers are already broadening their compound semiconductor focus, which supports the view that material strategy is becoming central to long-term competitiveness rather than a simple procurement function.[4]San’an Optoelectronics Co., Ltd., “2025 Annual Report Summary,” cninfo.com.cn, cninfo.com.cnAs a result, the Southeast Asia LED chips market is likely to reward companies that can pair technology capability with more resilient sourcing models over the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Conventional LED Dominance Masks Structural Technology Migration

Conventional LEDs accounted for 82.34% of revenue in 2025, which kept them firmly at the center of the Southeast Asia LED chips market. That position reflected the strength of commercial and residential lighting demand, where mature phosphor-converted platforms still offer the best mix of cost, reliability, and efficacy for large replacement programs. The segment also benefited from stricter efficiency enforcement across ASEAN, because upgrades often began with established products that already met procurement and compliance requirements. In practical terms, that gave conventional products a strong volume floor even as the technology mix in the Southeast Asia LED chips market continued to shift.

Mini-LED occupies a transitional role that is strategically important for the Southeast Asia LED chips industry. It sits close enough to established GaN supply chains to scale through existing manufacturing know-how, but it also opens access to better-margin uses in display backlighting and premium lighting systems. Micro-LED is the fastest-growing technology sub-segment, with a 12.04% CAGR through 2031, which shows that the Southeast Asia LED chips market is already moving beyond the limits of conventional illumination. The strongest pull is coming from applications that value pixel control, brightness density, and compact optical design, especially in automotive and advanced display use cases. Company roadmaps from ams OSRAM show that micro-LED platforms first developed for intelligent automotive lighting are now being carried into adjacent photonics uses, which supports the wider migration path described in the Southeast Asia LED chips market.

By Semiconductor Material: GaN and InGaN Entrenched but Emerging Materials Offer Margin Upside

GaN and InGaN held 81.78% share in 2025, which made them the clear backbone of the Southeast Asia LED chips market by material. Their dominance rested on long-established yield improvements, broad compatibility with packaging ecosystems, and their central role in blue, white, and green LED production. That installed advantage is difficult to displace because fabs, packaging lines, and downstream customers are already optimized around nitride-based platforms. The result is that the Southeast Asia LED chips industry continues to rely on GaN and InGaN as the main volume engine across both standard and higher-value product categories.

AlGaInP still keeps a defined role in red, amber, and yellow applications where InGaN is less effective, which preserves demand in automotive signal lighting, horticulture, and selected display sub-pixels. At the same time, other semiconductor materials are projected to grow at an 11.89% CAGR through 2031, giving this cluster the strongest expansion path in the material mix. That growth is being supported by UV-C, micro-display, and more specialized photonic uses where performance needs are different from mainstream white lighting. Nichia and ams OSRAM signed a broad patent cross-license agreement in October 2025 covering nitride LED and laser technologies, including matrix headlamp modules, and that move raises the protection around the core GaN stack while indirectly giving more room for differentiated materials in specialized niches. San’an also confirmed ongoing work in gallium oxide and diamond-related semiconductor research, which shows that major suppliers view material diversification as a margin and technology strategy, not just a laboratory exercise.

By Application: General Lighting Still Leads but Automotive Defines the Margin Premium

General lighting retained a 40.67% revenue share in 2025, which kept it as the largest application in the Southeast Asia LED chips market. That leadership came from commercial retrofits, public lighting upgrades, and continued residential penetration across ASEAN. The segment still matters because it provides dependable scale and supports the high-volume demand base that many suppliers need to keep utilization healthy. Even so, the incremental revenue mix in the Southeast Asia LED chips market is gradually spreading into more demanding applications that carry tighter specifications and better pricing.

Backlighting and displays remain important because they require stronger performance in color uniformity, thermal control, and optical precision than standard lighting products. Consumer electronics and industrial lighting also add diversity, especially where UV-based sterilization and wavelength-specific lighting create room for differentiated chip designs. Automotive is projected to grow at a 12.75% CAGR through 2031, which makes it the most important premium application in the Southeast Asia LED chips market. This shift is tied to adaptive headlamps, advanced rear lighting, and the broader electrification cycle, all of which push suppliers toward better chip density, reliability, and optical control. Company positioning across the region already reflects that shift, with automotive lighting becoming a priority growth path for firms that want to move away from margin pressure in commodity illumination.

Geography Analysis

China and South Korea remain the main production and technology centers shaping the Southeast Asia LED chips market. China’s position is built on scale, vertically integrated supply chains, and a domestic demand base that supports both mainstream and advanced LED output. That scale keeps pricing pressure on conventional products while also supporting continued investment in next-generation formats. South Korea, by contrast, keeps more of its strength in premium display and automotive pathways, where tighter engineering standards and product differentiation matter more than pure volume. Together, these two markets account for much of the technological direction the Southeast Asia LED chip market follows across the wider Asia-Pacific market.

Taiwan and Japan continue to hold important positions in higher-value chip segments even as Chinese suppliers compete more aggressively on volume. Taiwan’s suppliers remain active in automotive, advanced display, and smart sensing pathways, helping preserve Taiwan's technology role even when overall scale is lower than China’s. Japan’s Nichia began replacing UV mercury lamps on its own production lines with UV-LED equivalents in January 2026, cutting CO₂ emissions by 35% per light source and demonstrating the commercial maturity of its UV-LED technology. Stanley Electric also announced in March 2026 that its 265 nm deep UV LED had achieved 7.5% wall-plug efficiency, with mass production planned for October 2026, which shows how quickly Japanese specialty LED development is advancing.

Southeast Asia itself is becoming more strategic inside the Southeast Asia LED chips market rather than serving only as a low-cost assembly base. Malaysia and Singapore are attracting more interest for production transfer, engineering support, and pilot-stage capability in newer LED formats. ams OSRAM’s late 2025 and early 2026 disclosures confirmed that it is transferring mature LED product lines to Malaysia while strengthening Asia-based research and development, which adds technical depth to the local ecosystem. This shift suggests that the Southeast Asia LED chips market will become more important not only as a manufacturing location, but also as a regional node for product qualification, supply chain diversification, and application-specific development.

Competitive Landscape

The Southeast Asia LED chips market is moderately fragmented at the chip level, but competitive strength is increasingly concentrated among suppliers that control epitaxy, product design, and key intellectual property. Nichia and ams OSRAM remain especially strong in high-efficacy white LEDs, UV LEDs, and advanced automotive lighting platforms. Their October 2025 patent cross-license agreement covers thousands of innovations in nitride LED and laser technologies, and it extends into LED packages and modules, including matrix headlamp systems. That agreement matters because it reinforces the qualification barriers around premium applications where performance and IP depth shape supplier choice more than price alone. Within the Southeast Asia LED chips market, this keeps top-tier competition focused on defensible niches rather than pure commodity volume.

Chinese producers, led by San’an Optoelectronics, continue to intensify competition in high-volume LED chips while also investing in broader compound semiconductor capabilities. San’an’s 2025 annual report showed continued development across LED, GaN, SiC, and newer material pathways, which supports a strategy that mixes scale with future-facing technology investment. This two-track model is important because it allows large suppliers to protect earnings in mature products while building optionality in more advanced segments. For the Southeast Asia LED chips market, that means competition is tightening from both ends, with commodity pricing pressure at the base and IP-led competition at the top.

Strategic moves across the market show a clear pivot toward higher-value applications. ams OSRAM’s digital photonics strategy targets annual savings of EUR 200 million (USD 220 million) by 2028 and includes the transfer of mature LED lines to Malaysia while redirecting more resources toward AR, AI photonics, and pixelated automotive lighting. Nichia’s internal shift from mercury lamps to UV-LED production-line use also shows how leading companies are validating specialty LED demand with their own operations, not only with external sales claims. The competitive opening in the Southeast Asia LED chips market still exists for companies that can combine ASEAN manufacturing economics with strong process know-how in micro-LED and automotive-grade products. No ASEAN-headquartered supplier has fully locked in that position yet, which is why localization, technology transfer, and engineering partnerships remain central competitive themes.

Southeast Asia LED Chips Industry Leaders

Nichia Corporation

Seoul Semiconductor Co., Ltd.

Osram Opto Semiconductors GmbH

Epistar Corporation

San’an Optoelectronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: D&O Green Technologies Bhd (Dominant Opto Technologies' parent) posted a net loss of MYR 58.62 million (USD 13.32 million) in Q1 FY2026, with revenue declining 6.35% to MYR 225.53 million (USD 51.26 million), as weaker China automotive sales and inventory impairment charges weighed on earnings. Management initiated margin-enhancement programs, including yield improvement, automation, and a 12.5% average selling price adjustment for smart LED products, targeting recovery in the second half of 2026.

- May 2026: FORVIA HELLA launched its high-resolution headlamp system SSL|HD fully localized in China for the first time, integrating it into the Zeekr 8X electric vehicle with entirely domestic supply-chain sourcing, marking a significant step in localizing advanced LED headlamp chip qualification within China's automotive OEM ecosystem.

- May 2026: India's Union Cabinet approved Crystal Matrix Limited's USD 336 million (approximately INR 3,200 crore) mini-LED and micro-LED epiwafer production facility in Dholera, Gujarat, under the India Semiconductor Mission, targeting 6-inch GaN microLED and mini-LED wafer output, positioning India as a future Asia-Pacific competitor in next-generation LED chip supply.

Southeast Asia LED Chips Market Report Scope

The Southeast Asia LED Chips Market Is Segmented By LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN / InGaN, AlGaInP, and Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting / Displays, Consumer Electronics, and Industrial / Specialty Lighting), And Country. The Market Forecasts Are Provided In Terms Of Value (USD Million).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By LED Chip Technology | Conventional LEDs |

| Mini-LED | |

| Micro-LED | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| Other Semiconductor Materials | |

| By Application | General Lighting |

| Automotive | |

| Backlighting / Displays | |

| Consumer Electronics | |

| Industrial / Specialty Lighting | |

| By Country | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the current and forecast value of the Southeast Asia LED chips market?

The Southeast Asia LED chips market was valued at USD 2.76 billion in 2025, stands at USD 2.99 billion in 2026, and is forecast to reach USD 4.82 billion by 2031 at a 10.04% CAGR.

Which LED chip technology segment leads in Southeast Asia?

Conventional LEDs led with 82.34% of revenue in 2025 because commercial and residential lighting still depend heavily on mature phosphor-converted platforms.

Which application is growing the fastest in LED chips across Southeast Asia?

Automotive is the fastest-growing application, with a projected 12.75% CAGR through 2031, supported by adaptive lighting, EV adoption, and rising use of advanced headlamp architectures.

Why are government policies important for LED chip demand in Southeast Asia?

Efficiency mandates, grant programs, and smart-city frameworks are pushing replacement demand toward higher-performance lighting systems, which raises chip content and quality requirements.

What is driving growth in advanced LED formats such as micro-LED?

Micro-LED is projected to grow at a 12.04% CAGR through 2031 as suppliers and OEMs push it into high-value uses such as automotive lighting, advanced displays, and photonics.

Which material platform dominates LED chip production in the region?

GaN and InGaN held 81.78% share in 2025 because they remain the standard platform for blue, white, and green LED production across mainstream and premium applications.

Page last updated on: