North America LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

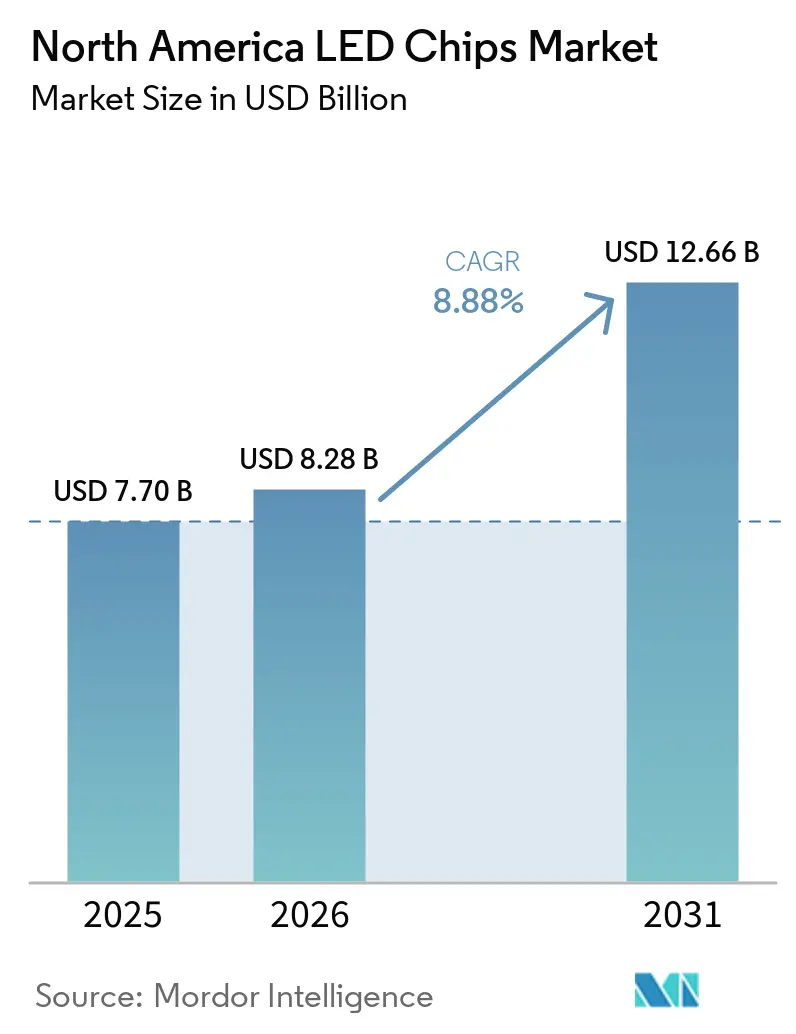

| Base Year Market Size (2025) | USD 7.70 Billion |

| Market Size (2026) | USD 8.28 Billion |

| Market Size (2031) | USD 12.66 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

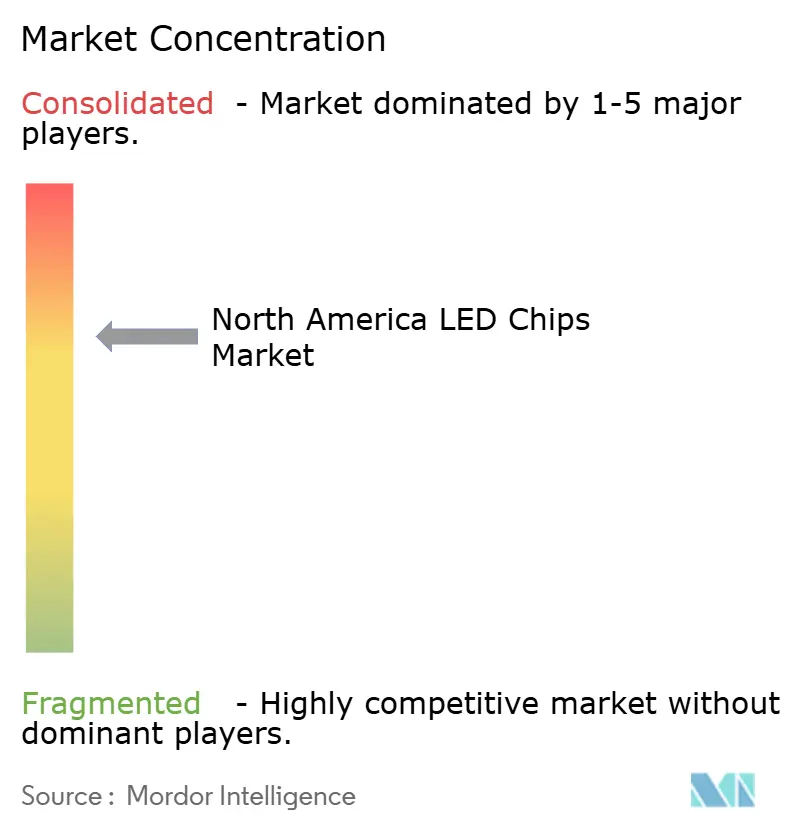

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America LED Chips Market Analysis by Mordor Intelligence

The North America LED chips market size is projected to expand from USD 7.70 billion in 2025 and USD 8.28 billion in 2026 to USD 12.66 billion by 2031, registering a CAGR of 8.88% between 2026 and 2031. The growth path reflects an irreversible shift toward solid-state lighting as end users replace high-intensity discharge and fluorescent sources with LEDs across commercial real estate, automotive headlamps, and premium television backlights. Gallium-nitride devices remain the performance workhorse, but micro-LED lines in the United States and Canada are moving from pilot to low-volume production, signaling a bifurcation between commodity white LEDs and ultra-high-pixel-density dies for displays. Utility rebate values rose in 2026, and federal Section 179D deductions multiplied for projects that met prevailing-wage and apprenticeship requirements, thereby shortening retrofit payback periods in warehouses and big-box retail sites. On the supply side, headlamp makers such as Hella introduced adaptive driving beam modules with more than 100,000 individually addressable pixels, which reduce electric-vehicle range loss by trimming headlamp energy consumption.

Key Report Takeaways

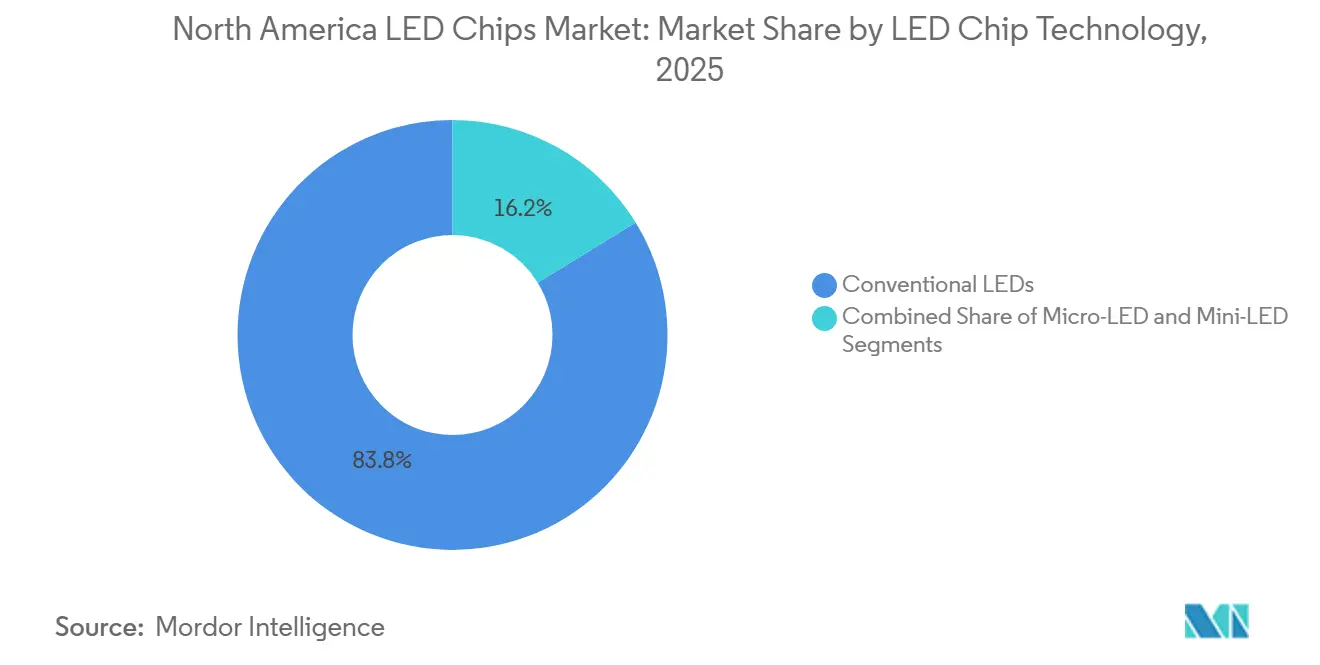

- By LED chip technology, conventional LED chips held 83.77% of the North America LED chips market share in 2025, while micro-LED chips are forecast to advance at an 11.32% CAGR through 2031.

- By semiconductor material, gallium-nitride and indium-gallium-nitride wafers captured 84.31% of the North America LED chips market in 2025, whereas alternative materials centered on red InGaN are projected to grow at a 11.55% CAGR.

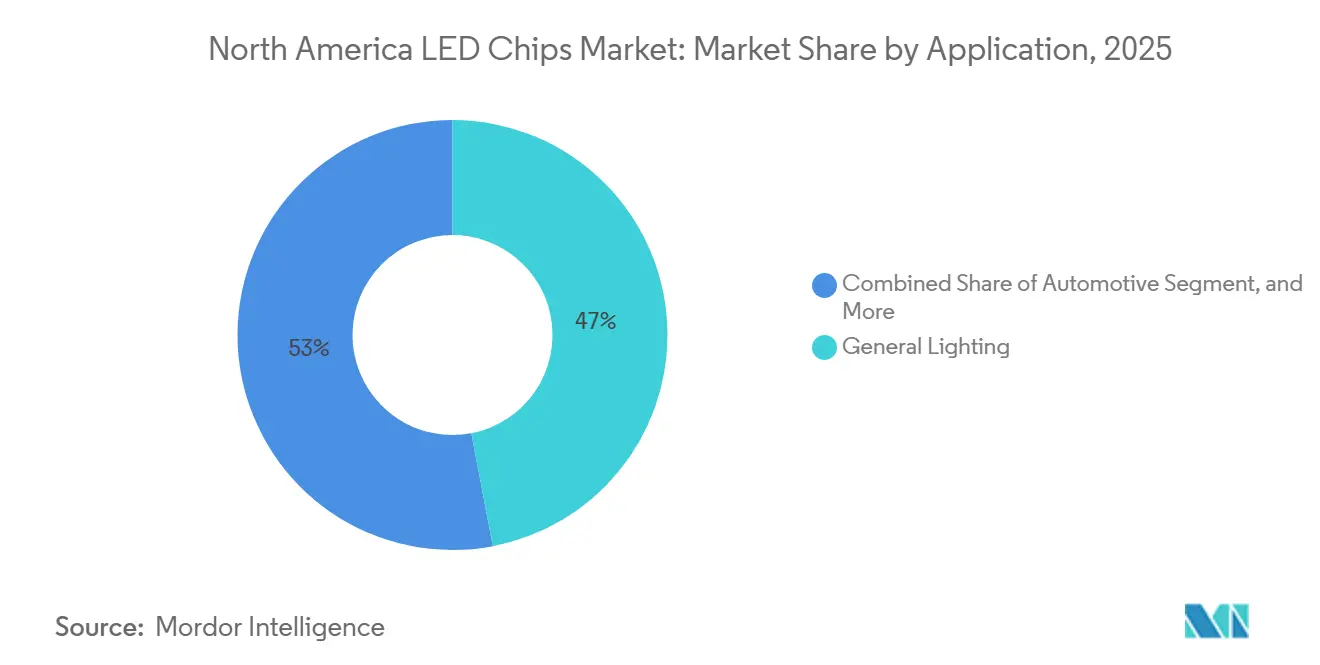

- By application, general lighting led with a 46.99% share of the North America LED chips market in 2025, but automotive lighting is set to record a 12.10% CAGR through 2031.

- By country, the United States accounted for 87.80% of the North America LED chips market revenue in 2025, and Canada is positioned for the fastest expansion at a 10.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing Demand for Energy-Efficient Lighting in Commercial Real Estate | +2.1% | United States and Canada, especially the Greater Toronto Area and the Northeastern U.S. corridors | Medium term (2-4 years) |

| Expansion of Smart City Projects with Intelligent Street Lighting | +1.8% | U.S. municipalities, early adoption in Canadian capitals, and Mexico border cities | Medium term (2-4 years) |

| Automotive OEM Shift Toward Advanced Headlamp Technologies | +2.3% | United States and Mexico manufacturing hubs | Long term (≥ 4 years) |

| Surging Mini-LED Backlight Adoption in High-End TVs and Monitors | +1.6% | United States and Canada premium consumer-electronics retail | Short term (≤ 2 years) |

| Rising Investments in North America Micro-LED Pilot Lines | +0.9% | Oregon, California, Ontario | Long term (≥ 4 years) |

| UVC LED Retrofit Programs for Indoor Air Disinfection | +0.3% | U.S. commercial HVAC market | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Energy-Efficient Lighting in Commercial Real Estate

Utility programs raised average prescriptive lighting incentives by 17% in 2026, with outdoor categories such as parking garages and wall packs exceeding 30% increases. Section 179D deductions now reach up to USD 5.81 per square foot for projects that satisfy prevailing-wage requirements, multiplying the base tax benefit by 5 and boosting retrofit internal rates of return.[1]Internal Revenue Service, “Energy-Efficient Commercial Buildings Deduction,” irs.gov Post-installation monitoring shows that warehouse retrofits can cut lighting energy use by 40-65% and achieve payback in less than 18 months for 24/7 facilities, stimulating recurring demand for replacement chips as first-generation LED luminaires approach end-of-life. The increase in programs that explicitly allow LED-to-LED upgrades keeps the North America LED chips market vibrant even in periods of slower new construction. Manufacturers that supply high-efficacy blue dies and long-lifetime red phosphor blends are best positioned to capture this second retrofit cycle.

Expansion of Smart City Projects with Intelligent Street Lighting

Memphis completed a USD 47 million conversion of 77,000 luminaires to LED fixtures with networked controls, delivering annual energy savings of 37 million kWh and reducing greenhouse-gas emissions by 26,000 metric tons.[2]U.S. Department of Energy, “Memphis LED Streetlighting Project,” energy.gov LEOTEK and 1NCE launched an out-of-the-box cellular-IoT platform that removes roaming complexity for municipalities and accelerates cross-border deployments, with initial rollouts in Boston, Syracuse, and Michigan utility territories. By embedding traffic, air-quality, and public-Wi-Fi sensors into luminaires, cities convert street-lighting grids into revenue-generating data platforms. These feature-rich fixtures require LED chips with strict binning for current uniformity and forward-voltage alignment, which are driving average selling prices higher in the North America LED chips market. Performance-based maintenance agreements that guarantee five-day repair times also favor suppliers with vertically integrated service networks.

Automotive OEM Shift Toward Advanced Headlamp Technologies

Hella’s pixelated micro-LED headlamp module packs more than 100,000 individually addressable emitters and uses graphene heat sinks that dissipate 40% more heat than aluminum, allowing the module to deliver 25 lumens per watt while halving energy draw compared with legacy high-intensity discharge units.[3]Hella GmbH, “Adaptive Driving Beam Module With Graphene Heat Sink,” hella.com For battery-electric vehicles, headlamps can account for up to 15% of night-driving power, and the new module extends real-world range by 5–8 km per charge. Direct-imaging adaptive driving beams showcased at the DVN Munich conference remove projection optics, shrinking package depth so headlights can integrate flush with aerodynamic fascias. Mexico’s module makers, led by SL MEX, added new capacity in San Luis Potosí that can produce 1 million modules a year for regional BMW, General Motors, and Kia plants. These trends raise unit demand for high-brightness chips and sustain the long-term contribution of automotive lighting to the North America LED chips market.

Surging Mini-LED Backlight Adoption in High-End TVs and Monitors

Mini-LED backlit LCD televisions are set to overtake OLED TVs, with shipments surpassing 13.5 million units in 2025 as panel makers push thousands of local-dimming zones and peak brightness beyond 4,000 nits. Samsung expanded its Micro RGB TV lineup to include screen sizes as small as 55 inches, while Hisense introduced a four-subpixel backlight that adds a cyan channel to expand the color gamut. RGB mini-LED architectures increase chip counts because they use discrete red, green, and blue dies rather than a single blue die with quantum-dot conversion. Precise wavelength binning to achieve 100% BT.2020 coverage increases demand for tightly specified bins, thereby bolstering the average selling price per chip in the North America LED chips market. Thermal loads of up to 9,000 nits require consistent junction-temperature control, favoring suppliers that can integrate high-thermal-conductivity substrates at the chip level.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Disruptions for MOCVD Equipment | −1.4% | North America fab expansions | Short term (≤ 2 years) |

| Patent Litigations Increasing Royalty Costs | −1.1% | United States courts, cross-border licensing in Mexico and Canada | Medium term (2-4 years) |

| Thermal Management Challenges in High-Power Chips | −0.7% | Southwestern United States and Mexico automotive markets | Long term (≥ 4 years) |

| Limited Gallium Nitride Wafer Availability | −0.9% | North American fabs dependent on Chinese gallium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions for MOCVD Equipment

AIXTRON and Veeco Instruments supply about two-thirds of global MOCVD reactors, and single-chamber tools cost USD 1.5–3 million. Component shortages for precision mass-flow controllers and vacuum subsystems have stretched deliveries beyond 18 months, delaying planned wafer-capacity additions in Arizona and Ontario. While secondary markets occasionally free up used reactors, retrofitting older tools to run 200 mm GaN processes requires expensive upgrade kits. Infineon demonstrated the first operational 300 mm GaN power wafer line in Europe last year, highlighting the scale economies at stake. North American fabs risk falling behind Asian competitors if equipment delays persist, moderating the expansion rate of the North America LED chips market.

Thermal Management Challenges in High-Power Chips

Pixel-dense automotive headlamps operate in engine compartments that experience ambient temperatures above 80 °C in Southwestern deserts. Junction temperatures can exceed 150 °C without advanced heat sinks, accelerating phosphor degradation and shifting chromaticity outside color-bin tolerances. Suppliers are experimenting with diamond composite substrates and graphene thermal films, but production yields remain below 70%. Reliability concerns thus cap lumen output per package and slow penetration of ultra-compact lamps that depend on power densities above 25 W cm-2.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Conventional LEDs Dominate While Micro-LED Gains Traction

Conventional devices captured 83.77% of the North America LED chip market share in 2025, underscoring white LEDs' cost leadership in general lighting and signage deployments. Micro-LED dies, although a fraction of volume, are advancing at an 11.32% CAGR on the back of smartwatch faces, automotive pillar-to-pillar displays, and augmented-reality headsets. Garmin selected a 1.39-inch micro-LED panel for its flagship multisport watch, set to debut in 2026, citing sunlight readability and 20-day battery life. VueReal’s mass-printing approach positions Ontario as a supply node for these wearables.[4]VueReal Inc., “Scaling MicroSolid Printing,” vuereal.com

Conventional LED makers defend their market share through package innovations, such as high-reflectivity lead frames and hybrid optics, that push efficacy above 220 lm W-1. Yet future premium growth tilts toward micro-LED because direct-emissive pixels eliminate color-shift artifacts and deliver peak brightness exceeding 3,000 nits in head-up displays. As micro-LED transfer yields improve beyond 99.9% in pilot lines, the technology could command 10% of the North America LED chip market by 2031, with mini-LED occupying the middle tier for high-end television backlights.

By Semiconductor Material: GaN Leads, Alternative Alloys Emerge

Gallium-nitride-based wafers accounted for 84.31% of the North America LED chip market in 2025, serving as the foundation for blue dies that power both white-light phosphor systems and the green and cyan channels in emerging RGB backlights. Sharp price swings in gallium have amplified operating-capital requirements, pushing several fabs to lock in multiyear supply contracts denominated in USD rather than renminbi. Red and amber devices traditionally relied on aluminum gallium indium phosphide, yet breakthroughs in red InGaN below 10 µm from Ingantec suggest a path toward monolithic RGB micro-LED wafers that could streamline future display assembly.[5]Ingantec Corporation, “Red InGaN Micro-LED Breakthrough,” ingantec.com

Alternative semiconductor stacks are projected to grow at a 11.55% CAGR as display makers trial quantum-dot-on-chip hybrids and ultraviolet germicidal packages. These specialty dies fetch margins that are two to three times higher than commodity GaN LEDs, improving the blended earnings profile for chip vendors serving the North America LED chips market.

By Application: Automotive Lighting Outpaces Retrofit General Lighting

General lighting held 46.99% of 2025 volume, buoyed by utility programs that now cover up to 90% of fixture and labor costs in Québec and instant point-of-sale discounts in Ontario. Yet saturation in big-box retail and office spaces means year-over-year growth is slowing. Automotive lighting, in contrast, is forecast to compound at 12.10% annually as adaptive driving beams, animated taillights, and dynamic interior ambiance become standard on mid-segment vehicles.

SL MEX’s new plant and Excellence Optoelectronics’ upcoming line in Querétaro enable tier-one suppliers to source modules under the updated United States-Mexico-Canada Agreement rules of origin, which favor regional content. High-power automotive packages increase die size per vehicle, further boosting the automotive contribution to the North America LED chips market.

Geography Analysis

The North America LED chip market relies heavily on U.S. demand centers such as California, Texas, and the Great Lakes corridor, where commercial floor space and automotive plants are concentrated. Federal infrastructure funds that earmark LED roadway lighting generate predictable chip volumes, while Section 179D tax deductions sustain private-sector retrofits. Utility rebates in states like New York and Massachusetts remain among the richest in the region, strengthening project economics even as electricity rates tick up.

Canada’s growth trajectory benefits from an aggressive decarbonization agenda that pushes lighting controls and high-efficacy fixtures. Instant point-of-sale rebates in Ontario and performance-based reimbursements in Québec shorten simple payback periods to less than two years for many indoor projects. The presence of VueReal in Waterloo catalyzes an ecosystem of deposition-tool vendors and automotive display integrators. Provincial incentive stacks further encourage micro-LED pilot lines, which, if successful, will increase Canada’s share of the North America LED chips market.

Mexico acts as the automotive lighting manufacturing hub for the tri-national region. SL MEX and Excellence Optoelectronics are building capacity to produce 1 million modules per year each, supplying adaptive headlamps and LED taillights that will ship to U.S. and Canadian final-assembly plants. New OEM mandates for regional value content under USMCA drive additional chip sourcing from within North America, insulating the North America LED chips market from Asian logistics risks.

Competitive Landscape

The North America LED chips market shows moderate concentration, with five multinationals accounting for a significant share. Lumileds, ams OSRAM, and Cree LED anchor the top tier through vertical integration that spans GaN wafer growth, phosphor formulation, and automotive qualification. Cree Lighting executed a strategic manufacturing agreement in February 2026 to add capacity for harsh-environment luminaires following an extended period of supply-chain disruption.

Everlight’s litigation against Lumileds underscores how intellectual property defense has become a frontline tactic to protect share and monetize R&D investments. Independent suppliers replicate this approach: Seoul Semiconductor maintains higher safety-stock coverage and focuses on ultraviolet dies where competitive density is lower and patent fences stronger.

On the start-up side, VueReal and Stratacache target micro-LED mass-transfer bottlenecks. Their success would diversify a supply chain that today still depends heavily on Asian foundries for display-grade dies. Mid-market players pursue specialization strategies in horticulture, ultraviolet disinfection, and high-density automotive interior lighting. Consolidation pressure remains high as channel partners gravitate toward suppliers that bundle chips, modules, drivers, and cloud controls into turnkey packages, a model that improves service levels and protects gross margin in the North America LED chips market.

North America LED Chips Industry Leaders

Cree LED, Inc.

Lumileds Holding B.V.

Nichia Corporation

OSRAM Opto Semiconductors GmbH

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: LEOTEK and 1NCE partnered to deploy AI-enabled IoT smart-street-lighting systems across 170 countries, beginning with installations in Boston, Syracuse, and Michigan utility territories.

- February 2026: Cree Lighting signed a long-term contract manufacturing agreement with a U.S. industrial-lighting producer to restore on-time deliveries for area, street, and canopy fixtures.

- February 2026: Everlight initiated patent infringement litigation against Lumileds in Delaware federal court, alleging violations of flip-chip electrode patents in Luxeon Go products.

- January 2026: SL MEX inaugurated an MXN 750 million lighting module plant in San Luis Potosí, designed to produce 1 million automotive modules annually for BMW, GM, Kia, and Hyundai.

North America LED Chips Market Report Scope

The North America LED Chips Market Report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, AlGaInP, and Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| United States |

| Canada |

| Mexico |

| By LED Chip Technology | Conventional LEDs |

| Mini-LED | |

| Micro-LED | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| Other Semiconductor Materials | |

| By Application | General Lighting |

| Automotive | |

| Backlighting / Displays | |

| Consumer Electronics | |

| Industrial / Specialty Lighting | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America LED chips market in 2031?

It is forecast to reach USD 12.66 billion by 2031, expanding at an 8.88% CAGR from 2026.

Which application is expected to grow fastest through 2031?

Automotive lighting is set to record the highest growth at a 12.10% CAGR as adaptive headlamps and animated taillights become mainstream.

How dominant is gallium-nitride in current chip production?

GaN and InGaN wafers contributed 84.31% of regional revenue in 2025, making them the backbone of blue and white LEDs.

Why is Canada’s growth rate higher than the United States?

Aggressive provincial rebates covering up to 90% of project costs, along with federal clean-technology manufacturing incentives, accelerate adoption in Canada.

What key factor limits rapid capacity expansion for LED epitaxy in North America?

Extended MOCVD reactor lead times and concentrated equipment supply chain delay wafer-fab buildouts.

How are intellectual-property disputes affecting suppliers?

Patent litigation, such as Everlight’s case against Lumileds, increases royalty costs and can pause design-in activity, thereby raising barriers to entry for smaller entrants.

Page last updated on: