United States Ketamine Clinics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

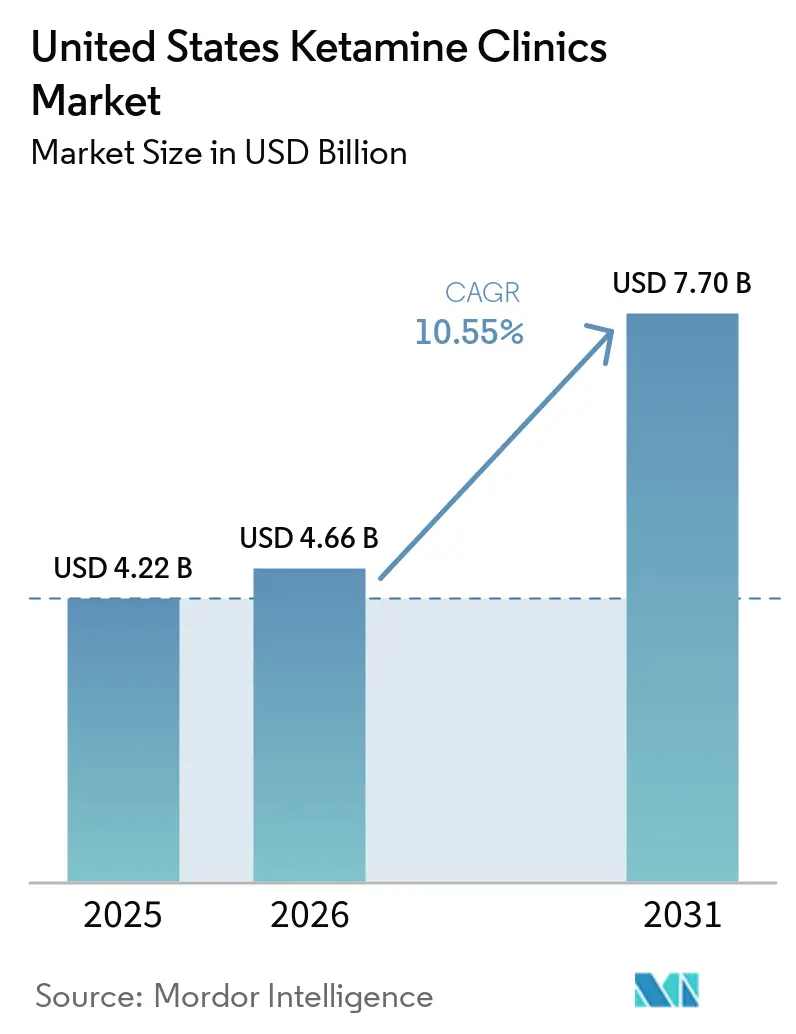

| Base Year Market Size (2025) | USD 4.22 Billion |

| Market Size (2026) | USD 4.66 Billion |

| Market Size (2031) | USD 7.70 Billion |

| Growth Rate (2026 - 2031) | 10.55% CAGR |

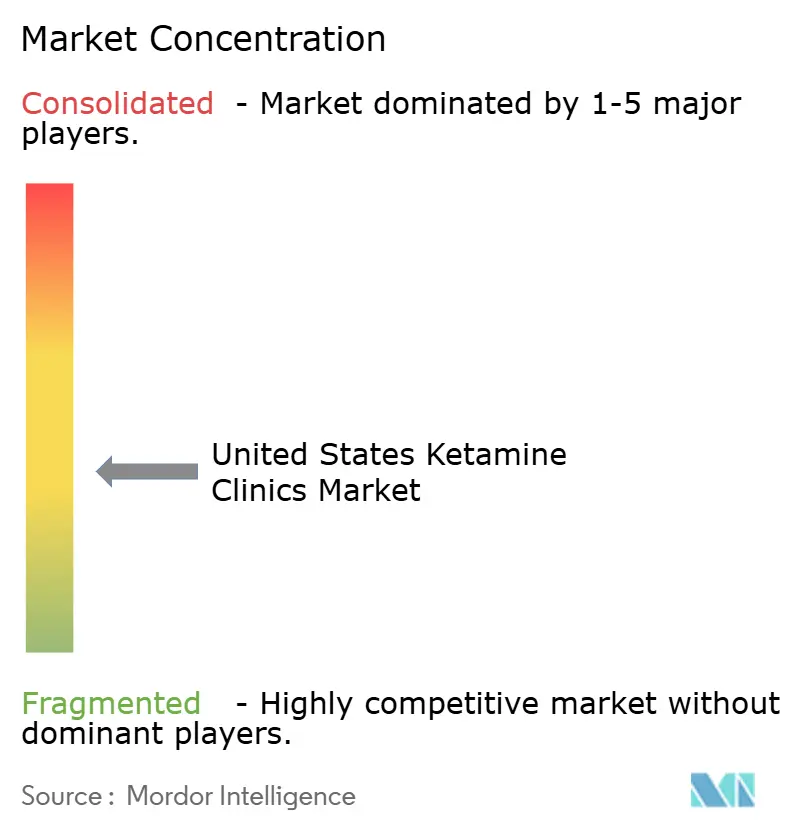

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Ketamine Clinics Market Analysis by Mordor Intelligence

The United States Ketamine Clinics Market size was valued at USD 4.22 billion in 2025 and is estimated to grow from USD 4.66 billion in 2026 to reach USD 7.70 billion by 2031, at a CAGR of 10.55% during the forecast period (2026-2031).

The United States (US) ketamine clinics market is being shaped by the scale of treatment-resistant depression, with 2.8 million adults progressing to TRD within the medicated major depressive disorder population and generating USD 43.8 billion of the USD 92.7 billion annual burden tied to medicated MDD. The January 2025 approval of SPRAVATO as the first monotherapy for adults with TRD removed the prior requirement for concurrent oral antidepressants, which made clinic intake, documentation, and treatment initiation simpler for eligible patients. The US ketamine clinics market is also benefiting from the DEA and HHS decision to keep telemedicine prescribing flexibilities in place through December 31, 2026, which supports national patient acquisition for hybrid care models. At the same time, reimbursement gaps between Spravato-based care and off-label ketamine formats, along with FDA scrutiny of compounded ketamine products, are pushing the market toward operators with stronger compliance systems and more standardized care pathways. The result is a US ketamine clinics market that is widening beyond its original psychiatric base while competition shifts toward scaled platforms that can combine clinical credibility, payer access, and operational discipline.

Key Report Takeaways

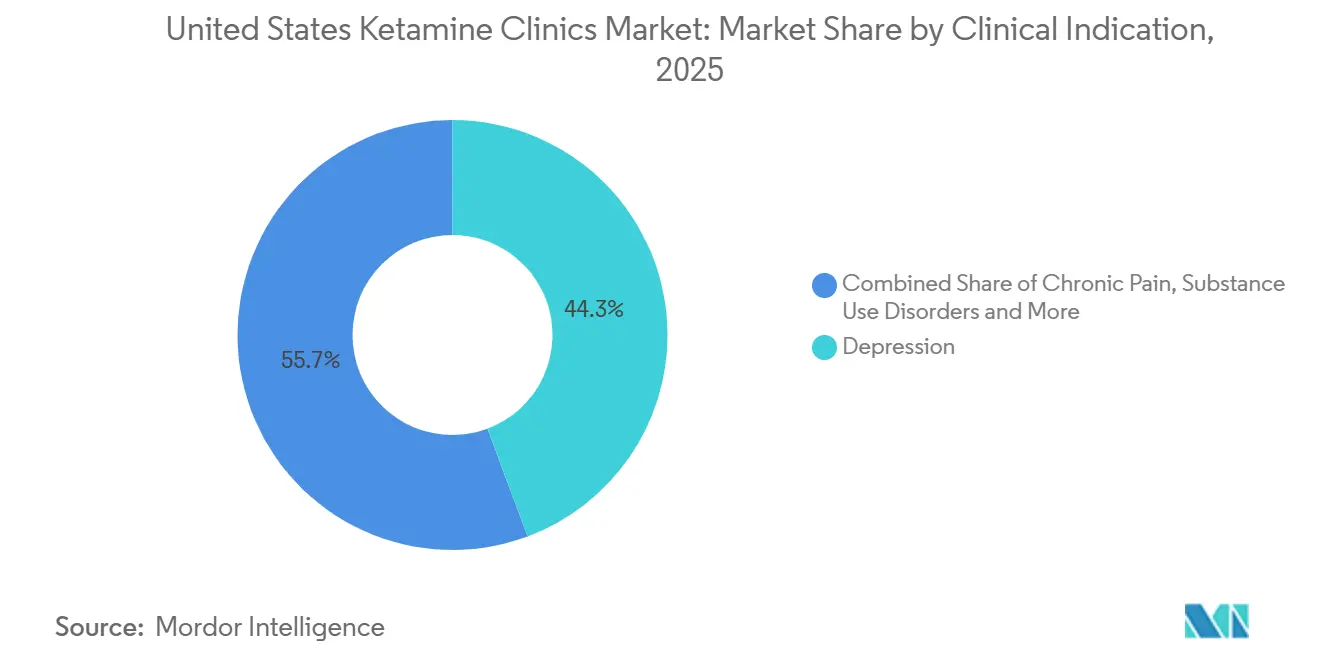

- By clinical indication, depression held 44.31% of the US ketamine clinics market share in 2025, while chronic pain is projected to expand at an 11.38% CAGR through 2031.

- By therapy modality, on-site delivery accounted for 81.24% share of the US ketamine clinics market size in 2025, while online therapy is forecast to record the fastest growth at 14.52% through 2031.

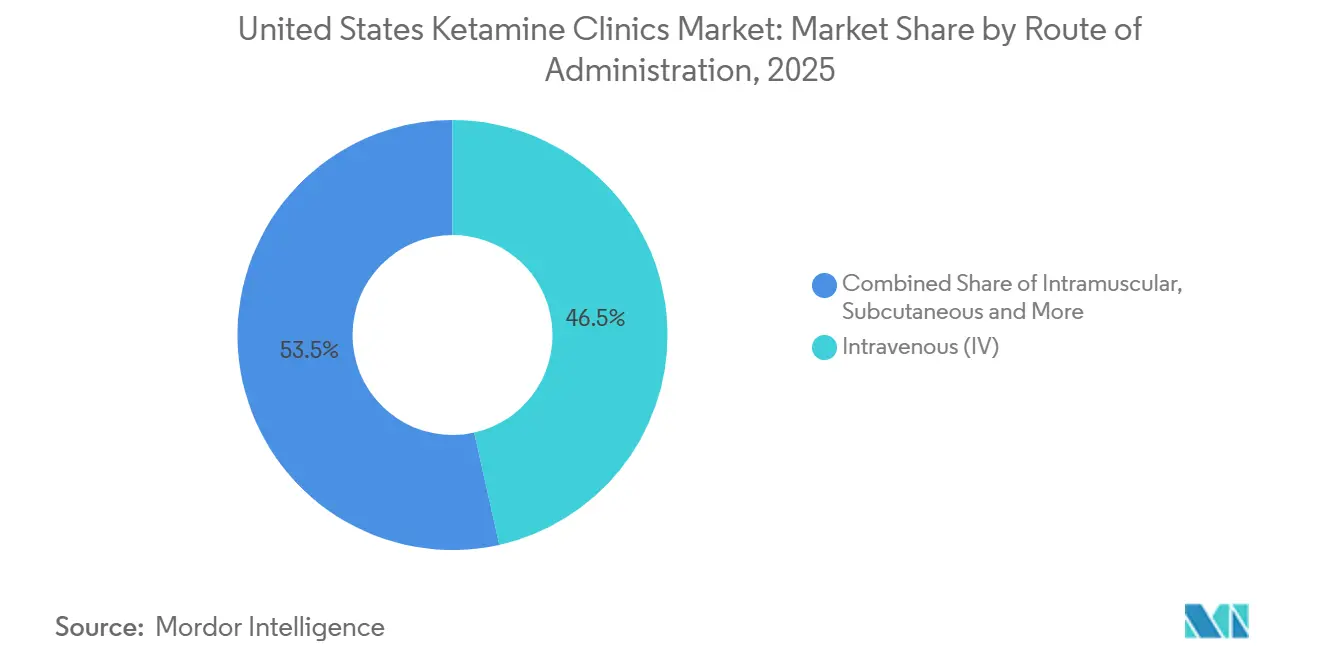

- By route of administration, intravenous infusion led with 46.52% share of the US ketamine clinics market size in 2025, while intranasal esketamine is expected to grow at a 13.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Ketamine Clinics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Treatment-Resistant Depression Burden | +2.1% | National, highest density in urban metros | Long term (≥ 4 years) |

| Rapid-Acting Alternative to Conventional Antidepressants | +1.7% | National | Short term (≤ 2 years) |

| Growing Psychiatrist And Patient Acceptance Of Interventional Psychiatry | +1.0% | National, concentrated at academic medical centers | Medium term (2-4 years) |

| Expansion Of Multi-Site Clinics And Hybrid Care Pathways | +1.4% | National, Sunbelt and suburban expansion corridors | Medium term (2-4 years) |

| SPRAVATO Monotherapy Label Expansion Simplifying Treatment Workflows | +1.2% | National, REMS-certified treatment centers in all 50 states | Short term (≤ 2 years) |

| Telehealth Prescribing Flexibilities Sustaining Hybrid Patient Acquisition | +1.1% | Rural and underserved areas, highest impact in Florida, New York, Tennessee | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Treatment-Resistant Depression Burden

Treatment-resistant depression remains the clearest demand anchor for the US ketamine clinics market because the condition sits inside a large treated depression population and carries high medical and social cost. Among 8.9 million medication-treated adults with MDD in the United States, 2.8 million progress to TRD, and that group accounts for USD 43.8 billion of the USD 92.7 billion yearly burden associated with medicated MDD. The severity gap is also visible in care utilization, since TRD patients recorded average hospitalization costs of USD 6,464 versus USD 1,734 for non-TRD patients and experienced depressive episodes lasting more than 1,000 days versus 452 days. This cost profile gives ketamine clinics a stronger case when they approach referral sources or payers, because the discussion is no longer limited to symptom relief and extends to avoidable hospital use and prolonged disease burden. The CDC also reported that 11.4% of U.S. adults took prescription medication for depression in 2023, with variation by region and disability status, which supports the view that untreated or poorly treated populations remain sizable across the country[1]Nazik Elgaddal, Julie D. Weeks, and Laryssa Mykyta, “Characteristics of Adults Age 18 and Older Who Took Prescription Medication for Depression, United States, 2023,” CDC, cdc.gov. As the US ketamine clinics market expands, these structural demand conditions should keep depression-led referrals elevated even as additional indications gain traction.

Rapid-Acting Alternative to Conventional Antidepressants

The US ketamine clinics market continues to benefit from the practical gap between standard oral antidepressants and the needs of patients in acute distress. Conventional antidepressants show an overall response rate of 37% and often need 4 to 6 weeks before clear clinical improvement becomes visible, which leaves a meaningful treatment window for faster-acting care. In the Phase 3 study behind the January 2025 SPRAVATO monotherapy approval, 22.5% of patients achieved remission at week 4 compared with 7.6% on placebo, and measurable symptom improvement appeared within 24 hours of the first dose. That speed matters clinically because patients with severe symptoms often cannot wait several weeks for an initial response, and it matters operationally because earlier responders can move into maintenance schedules more quickly. A 2024 study published in PMC also found large treatment effects across depression, anxiety, and PTSD at 3 months, with durable though smaller effects at 6 months and meaningful clinical improvement in 50% to 75% of participants. As a result, the US ketamine clinics market is drawing more interest from psychiatrists and primary care physicians who want options that work faster than the conventional medication cycle.

Growing Psychiatrist and Patient Acceptance of Interventional Psychiatry

The US ketamine clinics market is also moving forward because interventional psychiatry is becoming a clearer part of mainstream behavioral health delivery. Ketamine, TMS, and ECT are now discussed more often as structured treatment pathways rather than as isolated last-resort tools, which changes how psychiatrists frame escalation decisions for complex patients. The January 2025 SPRAVATO monotherapy approval reinforced this shift by placing ketamine-based care inside a clearer FDA-recognized pathway for adults with TRD. REMS certification, pharmacy oversight, and formal monitoring protocols are acting as quality filters, so operators that meet those standards are better positioned to build stable referral channels and institutional credibility. The normalization effect is also visible in provider expansion aimed at veteran and military populations, including Avesta’s 2026 move into Norfolk under a VA Community Care model. Within the US ketamine clinics market, broader professional acceptance should continue to favor operators that present ketamine therapy as part of disciplined psychiatric care rather than as a narrow infusion offering.

Expansion of Multi-Site Clinics and Hybrid Care Pathways

The US ketamine clinics market is no longer defined only by single-location clinics serving local self-pay demand. Expansion activity in 2025 and 2026 shows that operators are building wider footprints and using hybrid care models to reach patients who need supervised initiation but want more flexible maintenance options. HOPE Therapeutics opened a Palm Beach clinic in March 2026 that combines ketamine, TMS, and hyperbaric oxygen for depression and PTSD, which reflects a broader move toward multi-service interventional platforms. Radial also expanded to 7 clinics in 6 states in April 2026 with new locations in Brooklyn and Spartanburg, extending insurance-accepting ketamine and Spravato services into additional underserved communities. These moves matter because hybrid pathways let operators match payer preferences for supervised starts with patient demand for easier ongoing access. As more operators adopt that format, the US ketamine clinics market should become less dependent on dense urban cores and more capable of serving suburban, secondary, and veteran-heavy catchment areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Insurance Coverage For Off-Label Ketamine Therapy | -1.6% | National, most acute in states lacking mental health parity enforcement | Long term (≥ 4 years) |

| Protocol Heterogeneity And Limited Long-Term Evidence | -0.8% | National | Medium term (2-4 years) |

| FDA Scrutiny Of Compounded Ketamine Increasing Compliance Burden | -1.0% | National, with elevated impact in telehealth-concentrated states | Short term (≤ 2 years) |

| Prior Authorization And REMS Chair-Time Limiting Spravato Throughput | -0.9% | National, REMS-certified centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Insurance Coverage for Off-Label Ketamine Therapy

Insurance asymmetry remains the most important structural brake on the US ketamine clinics market. The practical divide is clear, Spravato has a formal FDA-approved pathway that fits reimbursement structures more easily, while IV, IM, sublingual, and subcutaneous ketamine for psychiatric use are still much more exposed to self-pay economics. That split creates two parallel business models, one tied to supervised, reimbursable esketamine care and another tied to direct patient payment for off-label treatment. The result is a narrower addressable pool for operators that rely mainly on off-label formats, even when patient demand and physician interest are strong. This also shapes competitive behavior because scale operators can invest more heavily in benefit verification, prior authorization support, and contracts that reduce friction for covered patients. Until reimbursement becomes broader across formats, the US ketamine clinics market will keep growing unevenly across patient income groups, payer types, and clinic models.

Protocol Heterogeneity and Limited Long-Term Evidence

The US ketamine clinics market also faces a credibility constraint because off-label care is still delivered through varying protocols. Dosing levels, session cadence, monitoring practices, and the role of adjunct psychotherapy can differ meaningfully from one operator to another, which makes direct comparison difficult for referring physicians and payers. The 2025 Cochrane review on ketamine and other NMDA receptor antagonists for chronic pain highlighted ongoing evidence gaps and protocol inconsistency, limiting how confidently results can be generalized across patient groups. That matters beyond pain care because the same concerns affect how insurers and medical review teams view psychiatric ketamine services that already sit outside conventional formularies. At the same time, operators that collect prospective outcomes data and publish results are turning a market-wide weakness into a competitive advantage. The FDA’s position that it has not established safe or effective dosing for psychiatric ketamine indications outside SPRAVATO keeps this issue central to the US ketamine clinics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Clinical Indication: Depression Anchors Revenue While Pain Reshapes Mix

Depression accounted for 44.31% of the US ketamine clinics market share in 2025, making it the leading clinical indication and the main revenue base for current operators. The segment is supported by the scale of TRD in the United States, where 2.8 million adults develop treatment-resistant disease within the medicated MDD population. It is also supported by the broader prevalence pool, since NIMH reported that 21 million adults experienced a major depressive episode, which leaves a wide referral base for stepped-up intervention after conventional drug failure[2]National Institute of Mental Health, “Major Depression,” National Institutes of Health, nimh.nih.gov. The January 2025 SPRAVATO monotherapy approval removed a practical barrier that had previously complicated referral decisions for some psychiatrists and patients. Within the US ketamine clinics industry, this keeps depression at the center of physician referral behavior even as clinics broaden their intake across adjacent psychiatric diagnoses.

Chronic pain is projected to record the fastest growth at 11.38% CAGR from 2026 to 2031, which shows that the US ketamine clinics market is expanding beyond its original depression focus. Stanford University began a Phase 4 study in January 2025 to evaluate IV ketamine for chronic pain with comorbid depression under propofol sedation, which should add more methodologically structured evidence by late 2026. A 2025 case series in Frontiers in Pain Research also showed clinically meaningful pain reduction from low-dose ketamine combined with biopsychosocial adjunct therapies, while suggesting a pathway to lower required dosing. Anxiety disorders, PTSD, OCD, and substance use disorders still represent smaller but meaningful pools, and the 2024 PMC study supports the view that multi-indication protocols can capture needs that single-diagnosis reporting misses.

By Therapy Modality: On-Site Dominance Masks Online Acceleration

On-site therapy held 81.24% share of the US ketamine clinics market size in 2025, reflecting the continued importance of supervised administration in psychiatric ketamine care. This dominance is tied to the REMS structure for Spravato, the monitoring requirements around dissociation and sedation, and the clinical preference for physician-observed initiation in more complex cases. The on-site model also supports stronger positioning with referral sources because it looks closer to conventional specialty psychiatry and less like a retail infusion service. Operators within this format are increasingly separating into broader interventional centers that add TMS and related services, and more focused Spravato-led clinics that deepen medication management around a narrower patient pathway.

Online therapy is forecast to expand at a 14.52% CAGR through 2031, making it the fastest-growing modality in the US ketamine clinics market. That growth rests on two linked factors, continued patient demand for lower-friction access and federal policy that still permits remote prescribing pathways through the end of 2026. Even so, fully remote models remain more exposed to scrutiny when they depend on compounded ketamine or less standardized monitoring, which is why hybrid care is becoming the more durable format. In that structure, clinics use supervised treatment to start care and telemedicine to maintain engagement, which reduces travel friction without giving up oversight entirely. The US ketamine clinics industry is therefore likely to keep a large on-site base while allowing online and hybrid models to drive incremental reach and faster growth.

By Route of Administration: IV Anchors, Esketamine Challenges

Intravenous infusion led with 46.52% share in 2025, which kept it as the benchmark route inside the US ketamine clinics market. IV remains attractive because it offers precise titration, a well-established clinical presence in refractory depression and pain care, and a treatment setting where staff can respond quickly to adverse effects. Its position is also helped by long-standing physician familiarity, especially in clinics that built their practices before intranasal esketamine gained wider traction. Intramuscular administration gives some operators a lower-infrastructure alternative, while subcutaneous delivery remains earlier in adoption and is still building clinical visibility relative to IV.

Intranasal esketamine is projected to grow at a 13.28% CAGR from 2026 to 2031, and this part of the US ketamine clinics market size is being supported by both regulatory clarity and reimbursement alignment. The March 2026 prescribing information update confirmed the continued role of REMS and safe-use certification as the framework for SPRAVATO access and monitoring. The monotherapy expansion strengthened that route further because it simplified eligibility documentation while keeping treatment inside a clearly supervised care model. By contrast, sublingual and oral formats face greater pressure from FDA concerns around compounded ketamine use, which narrows the practical room for loosely supervised growth. Within the US ketamine clinics industry, that means future route mix is likely to shift toward intranasal esketamine and supervised IV care rather than toward less regulated take-home formats.

Geography Analysis

California is the largest state contributor to the US ketamine clinics market in 2026, and its lead reflects a combination of large treatment demand, dense urban referral networks, and strong academic psychiatry presence. The state’s position also fits the broader pattern of depression burden and treatment escalation in the United States, where large patient pools support more specialized outpatient mental health services. The Northeast corridor forms the next mature cluster, with New York City, Boston, and the Washington, D.C. area benefiting from high provider concentration, strong specialist referral patterns, and greater familiarity with medically supervised psychiatric care. These geographies are already competitive, so growth there is increasingly tied to operational efficiency, payer relationships, and the ability to offer several interventional therapies under one roof. That leaves the largest near-term upside not in the most mature metros, but in markets where demand exists and structured capacity is still catching up.

The South and Sunbelt are emerging as the fastest-expanding geography in the US ketamine clinics market. Population growth, a larger military and veteran presence in several corridors, and more favorable clinic economics in mid-sized metropolitan areas are helping operators enter places that previously could not support standalone ketamine centers. HOPE Therapeutics opened its Palm Beach clinic in March 2026 with ketamine, TMS, and hyperbaric oxygen services aimed at depression and PTSD, which illustrates this multi-service expansion model[3]NRx Pharmaceuticals, “HOPE Therapeutics, an NRx Subsidiary (Nasdaq: NRXP), Announces Opening of Palm Beach, FL Clinic,” NRx Pharmaceuticals Investor Relations, ir.nrxpharma.com. Avesta’s April 2026 move into Norfolk also shows how veteran-oriented demand is shaping geography, since the clinic entered a military-dense region under a VA Community Care framework.

The Midwest and rural interior remain the clearest white space in the US ketamine clinics market. These areas have thinner specialty mental health infrastructure, which makes travel time and provider scarcity a real barrier for patients who need repeated supervised treatment. Telemedicine flexibility through December 31, 2026 is therefore especially important outside major metropolitan areas because it allows digital intake, remote follow-up, and hybrid care pathways to support access where clinic density is low. The proposed Special Registration framework could become even more important after 2026 because it offers a route to preserve telemedicine-led reach once temporary rules expire. Over time, geographic growth will depend on whether operators can pair telehealth-enabled demand generation with payer support, veteran reimbursement channels, and enough supervised capacity to handle higher-acuity cases.

Competitive Landscape

The US ketamine clinics market remains moderately fragmented, with multi-site operators still holding single-digit revenue shares while a broad field of independent clinics continues to compete at the local level. This structure gives scale players room to grow, but it also means the market has not yet consolidated around a few dominant brands. The main dividing line is no longer simply who offers ketamine treatment, but who can combine insurance access, clinical standardization, and referral-friendly workflows into a more durable operating model. In practice, this gives an advantage to operators that can manage prior authorization, maintain consistent monitoring protocols, and present outcomes in a way that physicians and payers find credible. The US ketamine clinics market is therefore moving away from a purely local infusion model and toward a more systematized outpatient mental health service.

One important competitive move came from Johnson & Johnson, whose January 2025 monotherapy approval for SPRAVATO changed clinic economics by simplifying intake and expanding the number of eligible TRD patients who can enter a reimbursable supervised pathway. Another came from HOPE Therapeutics, which combined clinic expansion with a broader interventional psychiatry format when it opened its Palm Beach site in March 2026. Radial’s April 2026 expansion into Brooklyn and Spartanburg shows a similar attempt to scale through insurance-accepting, multi-state reach rather than through isolated local clinics. Avesta’s Norfolk opening adds a third example, with a strategy built around veteran and military populations under a credentialed care model.

Competitive advantage in the US ketamine clinics market is also becoming more tied to compliance and evidence. FDA scrutiny of compounded ketamine makes it harder for loosely controlled telehealth models to scale without stronger pharmacy oversight and patient monitoring. REMS requirements for SPRAVATO add operating burden, but they also create a recognized quality threshold that can help in payer and referral conversations. This is why white-space opportunities remain strongest in veteran-oriented care, chronic pain protocols, and underserved suburban or secondary markets where standardized operators can still enter ahead of fragmented local competition. Over the next few years, the US ketamine clinics market is likely to reward companies that treat clinical protocol, reimbursement support, and geographic expansion as one coordinated strategy rather than as separate initiatives.

United States Ketamine Clinics Industry Leaders

Mindbloom

Stella Mental Health

Mindful Health Solutions

Better U

Joyous

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Radial expanded its interventional psychiatry network to 7 clinics in 6 states with new openings in Williamsburg (Brooklyn), New York, and Spartanburg, South Carolina, extending insurance-accepting ketamine and Spravato services to two underserved communities. The expansion follows the company's December 2025 USD 50 million Series A and is consistent with a stated strategy to address the nationwide shortage of interventional psychiatric services.

- April 2026: Avesta Ketamine and Wellness opened its fifth clinic in Norfolk, Virginia, its first outside the Washington D.C. metro area, targeting the Hampton Roads military and veteran population. Operating as a VA Community Care provider, Avesta has administered over 20,000 ketamine and Spravato treatments since its founding in 2018.

United States Ketamine Clinics Market Report Scope

As per the scope of the report, ketamine clinics are specialized medical facilities that provide ketamine infusion therapy or administration for various health conditions. These clinics typically focus on the use of ketamine to treat mental health disorders such as depression, anxiety, and PTSD, as well as chronic pain conditions.

The segmentation for the United States Ketamine Clinics Market is categorized by clinical indication, therapy modality, and route of administration. By clinical indication, the market includes depression, anxiety disorders, PTSD, OCD, substance use disorders, chronic pain, and other indications. By therapy modality, it is segmented into on-site therapy, online therapy, and hybrid therapy. By route of administration, the market is divided into intravenous, intramuscular, intranasal esketamine, sublingual/oral, and subcutaneous. For each segment, the market size and forecast are provided in terms of value (USD).

| Depression |

| Anxiety Disorders |

| PTSD |

| OCD |

| Substance Use Disorders |

| Chronic Pain |

| Other Indications |

| On-Site Therapy |

| Online Therapy |

| Hybrid Therapy |

| Intravenous |

| Intramuscular |

| Intranasal Esketamine |

| Sublingual / Oral |

| Subcutaneous |

| By Clinical Indication | Depression |

| Anxiety Disorders | |

| PTSD | |

| OCD | |

| Substance Use Disorders | |

| Chronic Pain | |

| Other Indications | |

| By Therapy Modality | On-Site Therapy |

| Online Therapy | |

| Hybrid Therapy | |

| By Route of Administration | Intravenous |

| Intramuscular | |

| Intranasal Esketamine | |

| Sublingual / Oral | |

| Subcutaneous |

Key Questions Answered in the Report

What is driving growth in U.S. ketamine treatment centers through 2031?

Growth is being supported by a large treatment-resistant depression population, the January 2025 SPRAVATO monotherapy approval, and continued telemedicine flexibility through December 31, 2026.

How large is the U.S. ketamine clinic space expected to become by 2031?

The US ketamine clinics market is forecast to reach USD 7.70 billion by 2031 from USD 4.66 billion in 2026, advancing at a 10.55% CAGR over 2026-2031.

Which patient group currently generates the most revenue for ketamine clinics?

Depression is the largest indication, accounting for 44.31% of revenue in 2025, because referral demand remains anchored in treatment-resistant depression and broader MDD treatment failure.

Which treatment format is expanding the fastest?

Online therapy is projected to grow at a 14.52% CAGR through 2031, although on-site treatment still dominates because supervised care remains central for many protocols and for Spravato administration.

Why is intranasal esketamine gaining momentum against IV infusion?

Intranasal esketamine is expected to grow at 13.28% because it benefits from the SPRAVATO monotherapy label, a structured REMS pathway, and a reimbursement position that is stronger than most off-label ketamine formats.

What is the biggest business challenge for clinic operators today?

Insurance asymmetry remains the main structural constraint because reimbursable Spravato care and largely self-pay off-label ketamine care create very different patient funnels, margins, and scaling paths.

Page last updated on: