Fungal Keratitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

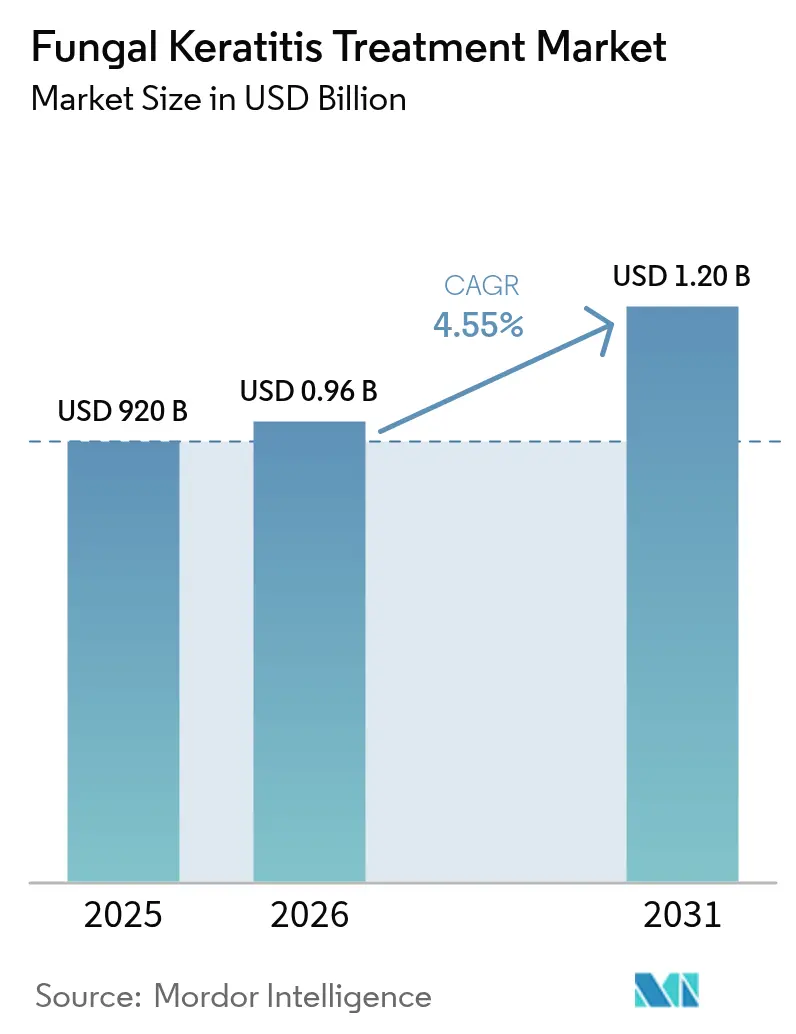

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.2 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fungal Keratitis Treatment Market Analysis by Mordor Intelligence

The Fungal Keratitis Treatment Market size is expected to grow from USD 920 million in 2025 to USD 961.86 million in 2026 and is forecast to reach USD 1.2 billion by 2031 at 4.55% CAGR over 2026-2031.

Steady topline growth masks structural change: resistance to legacy azoles is accelerating, climate change is expanding pathogen ranges, and deep-learning diagnostics have begun trimming the average time from first presentation to targeted therapy. AI classifiers now achieve 94.1% accuracy on slit-lamp images, compressing diagnostic windows that once stretched past five days and improving visual outcomes. Drug-delivery science is moving in parallel, with intrastromal injections and sustained-release implants improving corneal penetration for severe infections. E-commerce channels gain traction as teleophthalmology broadens reach in rural areas, while R&D pipelines pivot toward combination regimens that blunt resistance without amplifying toxicity.

Key Report Takeaways

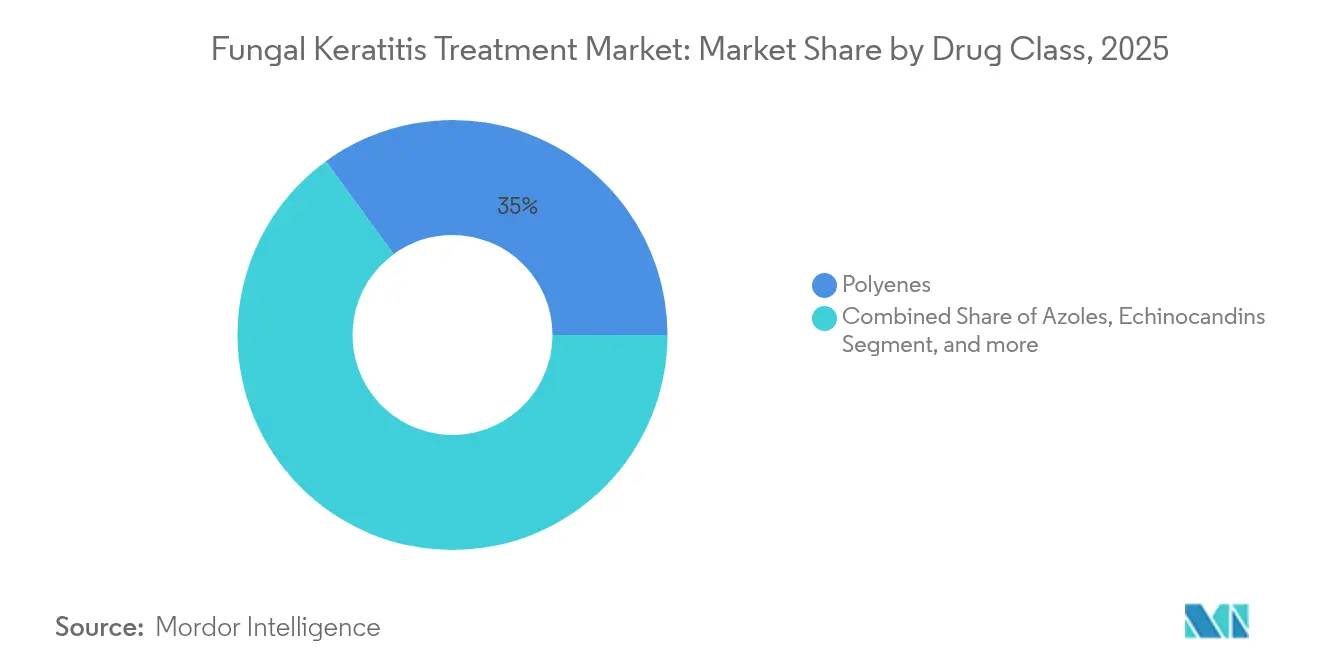

- By drug class, polyenes led with 35.02% of the fungal keratitis treatment market share in 2025; echinocandins are advancing at an 8.06% CAGR through 2031.

- By route of administration, topical therapy accounted for 60.65% of the fungal keratitis treatment market size in 2025; intrastromal injection is projected to rise at a 9.54% CAGR to 2031.

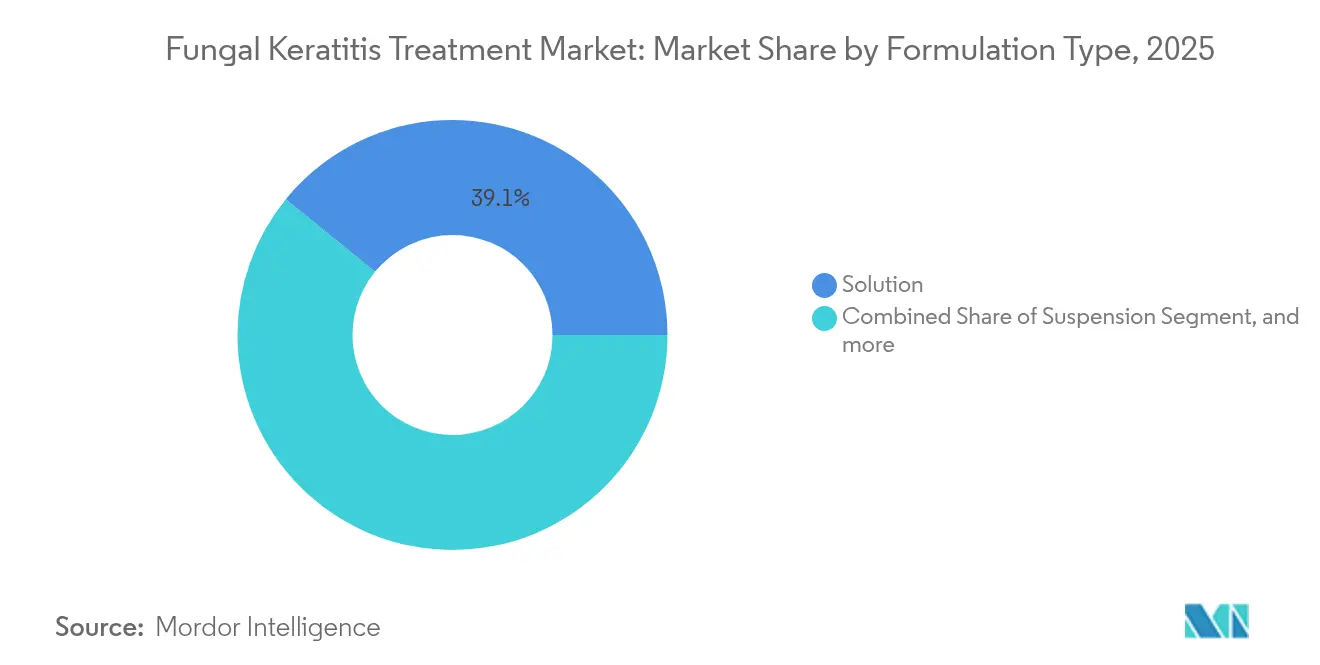

- By formulation type, solutions held 39.12% of revenue in 2025, while ointments and gels represent the fastest growing category at a 6.02% CAGR.

- By distribution channel, hospital pharmacies captured 43.72% of sales in 2025 and online pharmacies are expanding at a 10.05% CAGR.

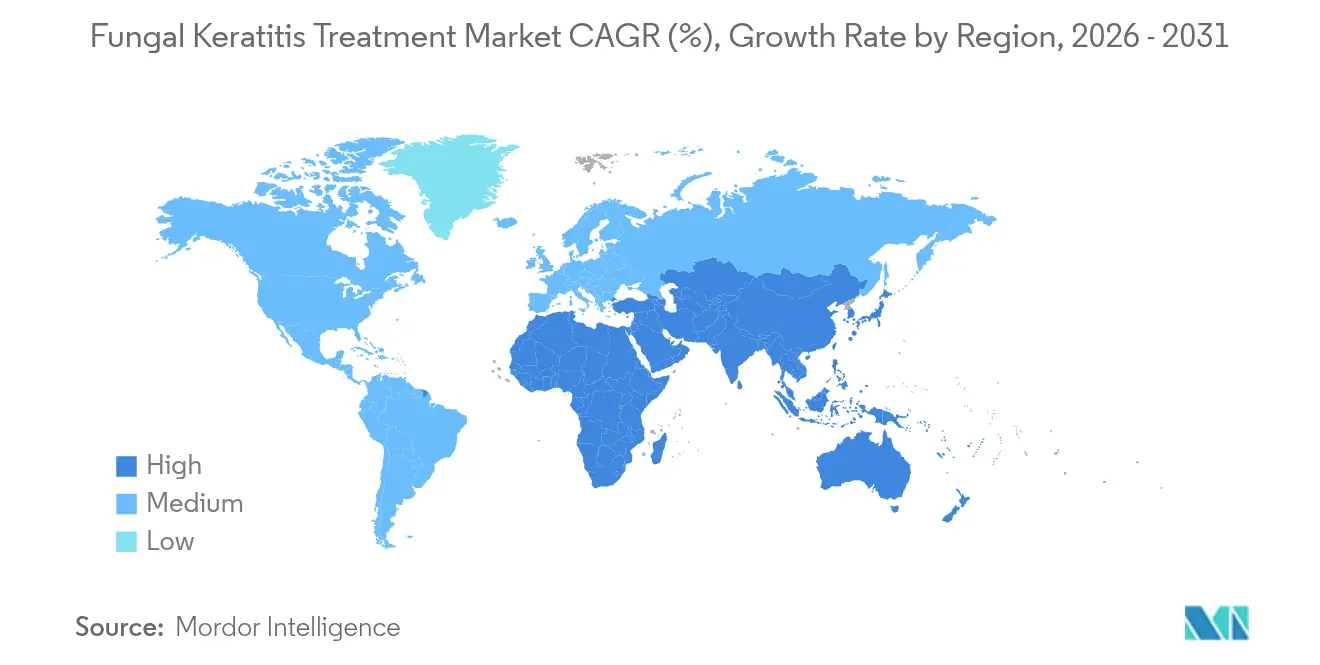

- By geography, North America commanded 36.02% revenue in 2025, whereas Asia-Pacific is the fastest growing region at a 5.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fungal Keratitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of Fungal Keratitis in Tropical & Subtropical Regions | +1.2% | Asia-Pacific, Latin America, Sub-Saharan Africa | Medium term (2-4 years) |

| Increasing R&D Investment in Broad-Spectrum & Targeted Antifungals | +0.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Rising Contact-Lens Use & Trauma-Related Ocular Infections | +0.7% | Global, highest in developed markets | Short term (≤ 2 years) |

| Surge In Lasik & Corneal Transplant Procedures Elevating Post-Op Risk | +0.5% | North America, Europe, select Asia-Pacific cities | Medium term (2-4 years) |

| Climate-Change-Driven Expansion of Fusarium & Aspergillus Habitat | +0.4% | Global, accelerated in temperate regions | Long term (≥ 4 years) |

| AI-Enabled Early-Diagnosis Tools Accelerating Treatment Rates | +0.3% | Developed markets initially, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Fungal Keratitis in Tropical & Subtropical Regions

Tropical and subtropical zones report a rising incidence as urban heat islands, higher humidity, and ongoing agricultural activity expose residents to spore-laden debris. Trauma accounts for up to 60% of rural cases, yet access to protective eyewear remains inconsistent. Hospital records across Myanmar, Ghana, and northeast Brazil confirm diagnostic delays of 5–7 days; early intervention within 48 hours notably reduces perforation risk.[1]J. Smith et al., “Epidemiology of fungal keratitis in developing regions,” Journal of Fungi, mdpi.com Expansion into temperate belts now challenges health systems in southern Europe and parts of the United States as climate change raises fungal thermotolerance.

Increasing R&D Investment in Broad-Spectrum & Targeted Antifungals

Capital is migrating toward novel mechanisms such as dihydroorotate dehydrogenase inhibition; olorofim shows potency against azole-resistant Aspergillus isolates.[2]A. Brown, “Olorofim clinical progress update,” BMC Infectious Diseases, bmcinfectiousdiseases.biomedcentral.com Partnerships between academia and industry accelerate translational timelines: a University of Oklahoma team has isolated persephacin, a plant-derived compound with broad-spectrum activity and reduced toxicity. Venture funds favor combination regimens that cap resistance while controlling dosing frequency through nanocarriers or ocular inserts.

Rising Contact-Lens Use & Trauma-Related Ocular Infections

Global contact-lens penetration has climbed into double-digits, particularly among working-age urban populations. The CDC continues to flag sub-optimal lens hygiene as a principal risk for Fusarium keratitis outbreaks.[3]CDC Staff, “Contact lens related infections,” Centers for Disease Control and Prevention, cdc.gov Biofilm-forming fungi thrive on lens surfaces and within storage cases, complicating standard disinfection. In emerging markets, retail promotions often outpace public health messaging, widening the knowledge gap on lens care best practices.

Surge in LASIK & Corneal Transplant Procedures Elevating Post-Op Risk

Refractive surgery volumes rose 12% in 2024, led by price declines in India and Mexico. Corneal flap creation can act as an entry portal for opportunistic yeasts, while transplant recipients on topical steroids remain immunosuppressed for months. The American Academy of Ophthalmology has documented a growing series of post-pterygium excision yeast keratitis cases.[4]American Academy of Ophthalmology Panel, “Post-surgical keratitis alerts,” AAO News, aao.org Medical tourism adds jurisdictional complexity as follow-up care often occurs in a different regulatory environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent Expiries & Generic Erosion of Key Azoles | -0.9% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| Dose-Limiting Ocular Toxicity & Systemic Side-Effects | -0.6% | Global, regulatory scrutiny highest in US/EU | Medium term (2-4 years) |

| Escalating Antifungal Resistance in Candida Auris & Fusarium | -0.5% | Global, emerging hotspots in Asia-Pacific | Long term (≥ 4 years) |

| Limited Cold-Chain & Diagnostics in Low-Income Regions | -0.4% | Sub-Saharan Africa, rural Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries & Generic Erosion of Key Azoles

Fluconazole’s patent loss and an average USD 14.38 generic price in the United States intensify price compression. Voriconazole, posaconazole, and other second-generation compounds face similar trajectories, pushing innovators to justify premiums via novel carriers or fixed-dose combinations. Market entrants from India and China expand ophthalmic generic capacity, deepening competition and accelerating downward price pressure in Europe and North America.

Escalating Antifungal Resistance in Candida auris & Fusarium

Candida auris outbreaks now require decontamination regimes that include UVC LED technology to eliminate environmental persistence. Reports of pan-resistant isolates force clinicians toward higher-toxicity amphotericin B regimens. Fusarium’s intrinsic azole resistance narrows therapeutic windows further, underscoring the need for class-independent options such as echinocandins and novel agents like rezafungin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Echinocandins Challenge Polyene Dominance

Echinocandins post the strongest outlook at an 8.06% CAGR, even as polyenes retained 35.02% of the fungal keratitis treatment market share in 2025. FDA clearance of rezafungin for systemic candidiasis validates this class despite the absence of ocular-specific labeling. Polyene demand remains anchored by liposomal amphotericin B, which reduces nephrotoxicity and plays a central role in refractory keratitis protocols.

Pipeline activity aligns with resistance realities. Combination regimens linking echinocandins to azoles or allylamines aim to offset single-agent failure rates. The fungal keratitis treatment market size for echinocandins is reflecting their growing adoption for recalcitrant cases. Polyene innovation now focuses on better ocular retention gels to maintain high corneal concentrations without systemic exposure.

By Route of Administration: Intrastromal Delivery Gains Clinical Acceptance

Topical drops accounted for 60.65% of the fungal keratitis treatment market size in 2025, driven by clinician familiarity and patient convenience. Intrastromal injection, however, is gaining traction and it is expected to grow with 9.54% between 2026 and 2031 because it delivers drug directly into the corneal stroma, bypassing epithelial barriers. Clinical studies show faster microbiological clearance when intrastromal voriconazole is used alongside lamellar keratoplasty.

Oral therapy remains a fallback for deep or systemic involvement, yet systemic toxicity curtails widespread use. Sustained-release implants, including micro-reservoir devices, are under investigation to extend dosing intervals to several weeks. Adoption hinges on surgical skill availability and reimbursement models that valorize procedure-based care.

By Formulation Type: Ointments Gain Traction for Sustained Release

Solutions still lead at 39.12% revenue, but ointment and gel formats are expanding because longer corneal residence reduces dosing from hourly to four times daily, growing at a 6.02% CAGR. Butenafine nano-micelles have improved solubility, widening the topical antifungal toolbox. Suspensions wrestle with shelf-life constraints, while ocular inserts target steady 24-hour release.

R&D teams are pairing antifungals with mild steroids in single ointments, addressing infection and inflammation concurrently while avoiding preservative overload. Biodegradable polymers that respond to fungal enzymes are also advancing, promising tailored drug unload in high fungal-burden microenvironments.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies captured 43.72% of sales in 2025 and remain the favored setting for acute care prescriptions that require cold-chain custody. Online pharmacies, however, are growing at a 10.05% CAGR as telemedicine closes geographic gaps. Regulatory bodies now allow e-prescriptions for most topical antifungals, and courier networks with integrated data-logger tracking mitigate temperature-excursion risks.

Platform integration is deepening: image-based AI tools route suspected keratitis cases directly into virtual consults, where ophthalmologists can prescribe and have medication shipped same-day in metro areas. Blockchain pilots for antifungal supply chains aim to combat counterfeits that previously infiltrated informal channels in Southeast Asia. Retail pharmacies face margin squeeze from generic erosion, spurring partnerships with hospital networks for specialty drug referrals.

Geography Analysis

North America contributed 36.02% of 2025 revenue, supported by higher treatment costs, insurance coverage for emerging modalities, and a well-established diagnostics infrastructure. Deep-learning algorithms have been commercialized and embedded in major academic eye centers, slashing time-to-therapy. The region also hosts most late-stage clinical trials, expediting local access to pipeline assets. Temperature anomalies along the U.S. Gulf Coast are already linked to rising Fusarium prevalence, increasing caseloads in states such as Texas and Louisiana.

Asia-Pacific is the fastest growing segment at 5.42% CAGR. Contact-lens adoption is accelerating across China, India, and South Korea, while agricultural exposure remains widespread in rural belts. Studies from northern Thailand found diverse Fusarium strains distinct from Western isolates, underscoring regional pathogen heterogeneity. Government insurance expansions in India and Indonesia now reimburse topical natamycin, widening formal treatment uptake. Public-private diagnostic partnerships seek to strengthen microscopy and culture capacity in district hospitals, which currently lack the ability to speciate pathogens.

Europe shows modest growth amid cost containment pressures. National health services favor generics where possible, trimming revenue per prescription. Yet the region maintains a leadership role in orphan designations and compassionate-use pathways, highlighted by SIFI’s polihexanide ODD in 2024 that promises ten-year market exclusivity upon approval. Southern Europe faces increased fungal keratitis incidence as heatwaves become more frequent, nudging budgets toward prophylactic education and early intervention schemes. Middle East & Africa and South America remain underpenetrated due to limited cold-chain capacity and uneven specialist density, although rising urban incomes are beginning to stimulate demand for premium formulations.

Competitive Landscape

Market structure is moderately fragmented. Large incumbents leverage regulatory expertise, global manufacturing footprints, and legacy azole portfolios. High capital requirements for aseptic ophthalmic lines deter new entrants. Yet mid-sized biotech firms with narrow but deep expertise attract venture funding by focusing on novel delivery or resistance-breaking mechanisms.

Multinationals are pruning portfolios to reshape ownership maps. In 2024, Pfizer divested fosmanogepix to Basilea Pharmaceutica as part of a 24% R&D cost rationalization. This move echoes a broader trend toward externalizing niche anti-infective assets to specialists agile enough to navigate limited-market returns. AI-enabled diagnostic firms are forging data-sharing alliances with drug developers seeking companion diagnostic status for premium pricing.

Strategic moves include licensing local production to circumvent cold-chain gaps in Africa and Latin America, technology transfer agreements for liposomal amphotericin, and equity stakes in start-ups exploring protease-responsive nanoparticles. Bausch + Lomb’s presentation of 39 scientific papers at ARVO 2025 underscores sustained ophthalmology commitment, though antifungal specifics remain thin. Overall, differentiation hinges on combining drug, device, and data into integrated care pathways.

Fungal Keratitis Treatment Industry Leaders

Merck & Co. Inc.

Bausch Health

Gilead Biosciences

Pfizer Inc.

Glenmark Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bausch + Lomb presented 39 scientific studies at the Association for Research in Vision and Ophthalmology Annual Meeting, showcasing advancements in dry eye treatments and ocular surface therapies that may have implications for fungal keratitis management through improved corneal barrier function.

- June 2024: SIFI S.p.A., a prominent Italian ophthalmic specialty pharmaceutical company, achieved a key regulatory milestone as the Committee for Orphan Medicinal Products (COMP) of the European Medicines Agency (EMA) issued a positive opinion for granting Orphan Drug Designation (ODD) to polihexanide for the treatment of fungal keratitis. This designation underscores SIFI's commitment to addressing unmet medical needs in ophthalmology and supports its efforts to develop innovative therapies for rare and vision-threatening ocular infections. The recognition by the EMA provides SIFI with regulatory and commercial incentives in the European Union, including protocol assistance, fee reductions, and ten years of market exclusivity upon approval.

- February 2024: Cipla Limited, a leading global pharmaceutical company, has entered into a strategic partnership with the Council of Scientific and Industrial Research – Central Drug Research Institute (CSIR-CDRI) to co-develop a novel formulation for the treatment of fungal keratitis, a severe and sight-threatening ocular infection.This collaboration combines Cipla’s robust formulation development and commercialization expertise with CSIR-CDRI’s scientific innovation in antifungal research.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fungal keratitis treatment market as all prescription pharmaceutical products, topical, oral, intrastromal or intravenous, specifically indicated to eradicate filamentous or yeast pathogens that invade the corneal stroma and endothelium. Surgical costs are excluded; only branded and generic drug revenues taken at ex-factory prices are modeled, and values are expressed in constant 2025 USD.

Scope exclusion: adjunctive procedures such as corneal cross-linking, therapeutic keratoplasty, and in-office debridement sit outside the revenue pool.

Segmentation Overview

- By Drug Class

- Polyenes

- Azoles

- Echinocandins

- Allylamines

- Novel & Combination Therapies

- By Route of Administration

- Topical

- Oral

- Intra-ocular / Intrastromal Injection

- By Formulation Type

- Solution

- Suspension

- Ointment / Gel

- Tablet / Capsule

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed ophthalmologists, cornea surgeons, regional drug distributors, and pharmacovigilance officers across North America, India, Nigeria, Brazil, and Japan. These discussions verified treatment mix shifts (for example, rising voriconazole salvage use) and refined assumptions on patient leakage from private to public channels before final triangulation.

Desk Research

We began with structured desk work drawing on freely accessible authorities such as the World Health Organization Vision Atlas, the US Centers for Disease Control and Prevention's Emerging Infections Surveillance, India's NPCBVI program statistics, Eurostat hospital discharge records, and peer-reviewed journals indexed on PubMed. Trade data from UN Comtrade helped back-calculate drug movement into high-burden tropical nations. To size corporate exposure, we tapped D&B Hoovers and screened corneal antifungal patent filings through Questel, which signposted pipeline volumes. Company 10-Ks, investor decks, ophthalmology association white papers, and Dow Jones Factiva news flow supplemented incidence and pricing clues. The sources cited here are illustrative; many additional public and proprietary references informed our evidence stack.

Market-Sizing & Forecasting

A top-down incidence-to-treatment flow model converts regional case loads into drug-treated courses, then multiplies by sampled average selling prices; selective bottom-up roll-ups of leading supplier revenues cross-check totals. Key variables include culture-positive keratitis incidence, first-line drug penetration, weighted daily dose, average course length, and generic erosion curves. Forecasts rely on multivariate regression where incidence trends, climate-linked humidity indices, contact lens adoption, and R&D success probabilities jointly project demand. Missing bottom-up data points are interpolated from neighboring markets or corrected through primary validations.

Data Validation & Update Cycle

Outputs pass variance checks against independent epidemiology series and historical sales. Senior reviewers interrogate anomalies, after which results are locked. Reports refresh each year, with mid-cycle updates triggered by material regulatory or clinical events; a rapid pre-publication audit ensures clients receive the most current view.

Why Mordor's Fungal Keratitis Treatment Baseline Commands Reliability

Published estimates seldom agree because study scope, input variables, and refresh cadence differ. We acknowledge this spread upfront, and we show where the gap arises before users build plans.

Key gap drivers here include whether viral and bacterial keratitis therapies are blended, how aggressively pricing inflation is layered, the breadth of pharmacy channels counted, and the frequency with which models are revisited; this is where Mordor analysts apply tighter infection-only boundaries, patient-level price audits, and annual refreshes that some publishers skip.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.92 B | Mordor Intelligence | - |

| USD 1.07 B | Global Consultancy A | Bundles bacterial and viral keratitis drugs and applies list prices without channel discounts |

| USD 0.94 B | Industry Data Firm B | Uses flat 5% ASP uplift, omits developing-world hospital volumes, relies on limited expert outreach |

Taken together, the comparison shows that while other figures swing wider, our disciplined scope definition, live pricing audits, and yearly update cycle give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current size of the fungal keratitis treatment market?

The fungal keratitis treatment market stands at USD 961.86 million in 2026 and is expected to reach USD 1.2 billion by 2031.

Which drug class holds the largest share?

Polyenes lead with 35.02% of the fungal keratitis treatment market share in 2025.

Why are echinocandins growing faster than other classes?

Echinocandins address azole-resistant infections and are projected to record an 8.06% CAGR through 2031.

How is climate change influencing demand?

Rising temperatures expand Fusarium and Aspergillus ranges into temperate regions, increasing caseloads and driving demand for advanced therapies.

Which distribution channel is expanding the quickest?

Online pharmacies are growing at a 10.05% CAGR, supported by telemedicine adoption and improved cold-chain logistics.

What recent regulatory milestone could reshape the market?

SIFI’s polihexanide received EMA Orphan Drug Designation in 2024, granting ten-year market exclusivity upon approval.

Page last updated on: