Keloid Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

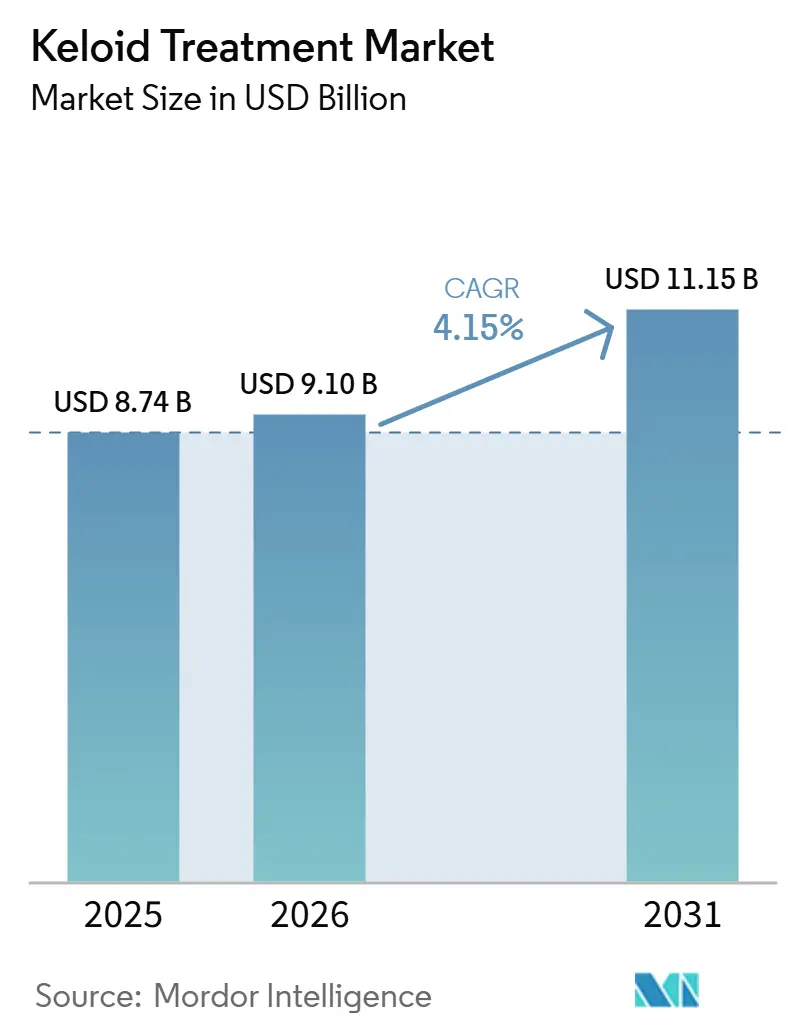

| Market Size (2026) | USD 9.10 Billion |

| Market Size (2031) | USD 11.15 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Keloid Treatment Market Analysis by Mordor Intelligence

The Keloid Treatment Market size is expected to increase from USD 8.74 billion in 2025 to USD 9.10 billion in 2026 and reach USD 11.15 billion by 2031, growing at a CAGR of 4.15% over 2026-2031.

The keloid treatment market is gaining stronger clinical relevance as providers increasingly manage keloids as a chronic fibrotic condition rather than a cosmetic concern. This shift is influencing payer discussions, treatment planning, and follow-up intensity in developed care settings. Globally, around 100 million patients develop new scars each year, and 11 million of these cases progress into keloids, keeping the addressable patient pool broad and clinically significant. Genetic susceptibility continues to shape demand, with keloid incidence reaching 5% to 15% in populations of African ancestry and 4% to 16% in Asian ancestry groups, compared with less than 0.1% in European populations. This trend supports stronger long-term demand across Africa, South and Southeast Asia, and parts of Latin America. The market is also evolving with wider adoption of combination care, rising demand for post-surgical prevention, and a gradual shift in treatment volumes from hospitals to outpatient dermatology channels. A 2025 multi-ancestry genome-wide association study covering 7,837 cases and 1,593,009 controls identified 26 keloid-associated loci, strengthening the biological basis for targeted treatment decisions and potentially expanding the market definition over time.[1]Giulia Kijanka et al., “Keloids Revisited: Current Concepts in Treatment and Differential Diagnosis,” Cancer Letters, sciencedirect.com

Key Report Takeaways

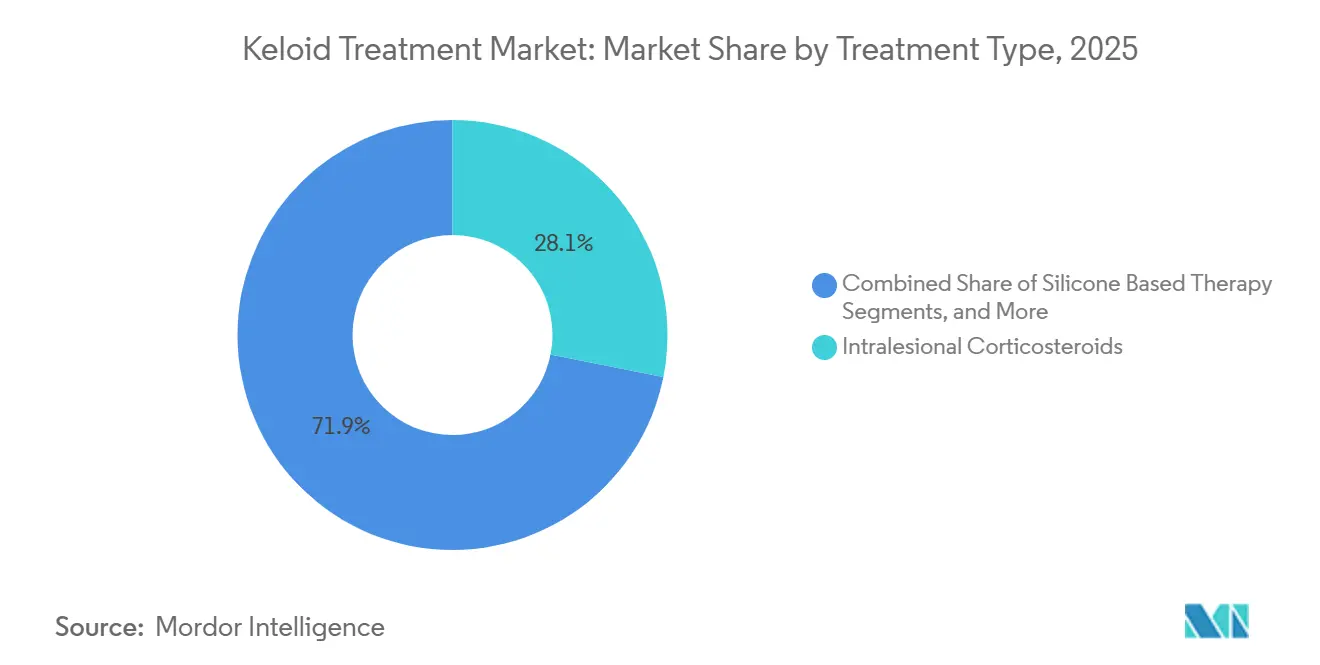

- By treatment type, intralesional corticosteroids held 28.12% of the keloid treatment market share in 2025, while 5-Fluorouracil Based Therapy recorded the highest projected CAGR at 5.53% through 2031.

- By route of administration, injectables accounted for 46.45% of the keloid treatment market size in 2025, while Procedural or Device Based administration is projected to expand at a 6.67% CAGR through 2031.

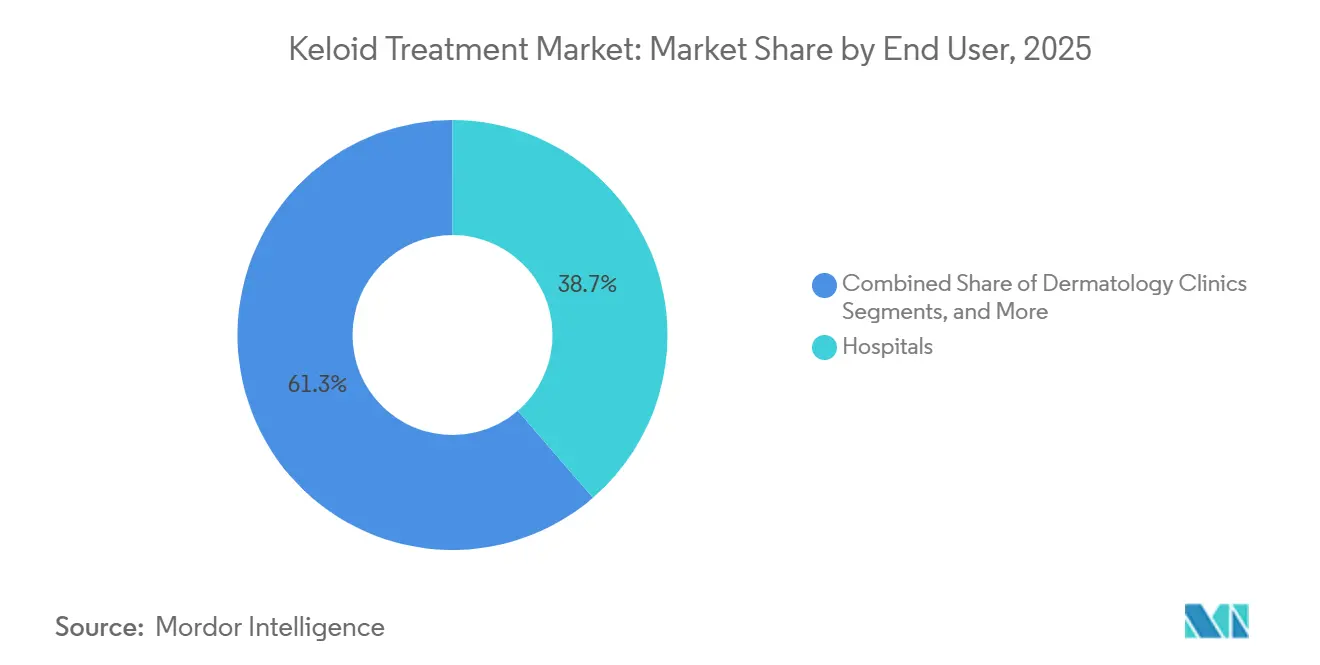

- By end user, hospitals held 38.66% of the keloid treatment market in 2025, while dermatology clinics are forecast to advance at a 7.35% CAGR through 2031.

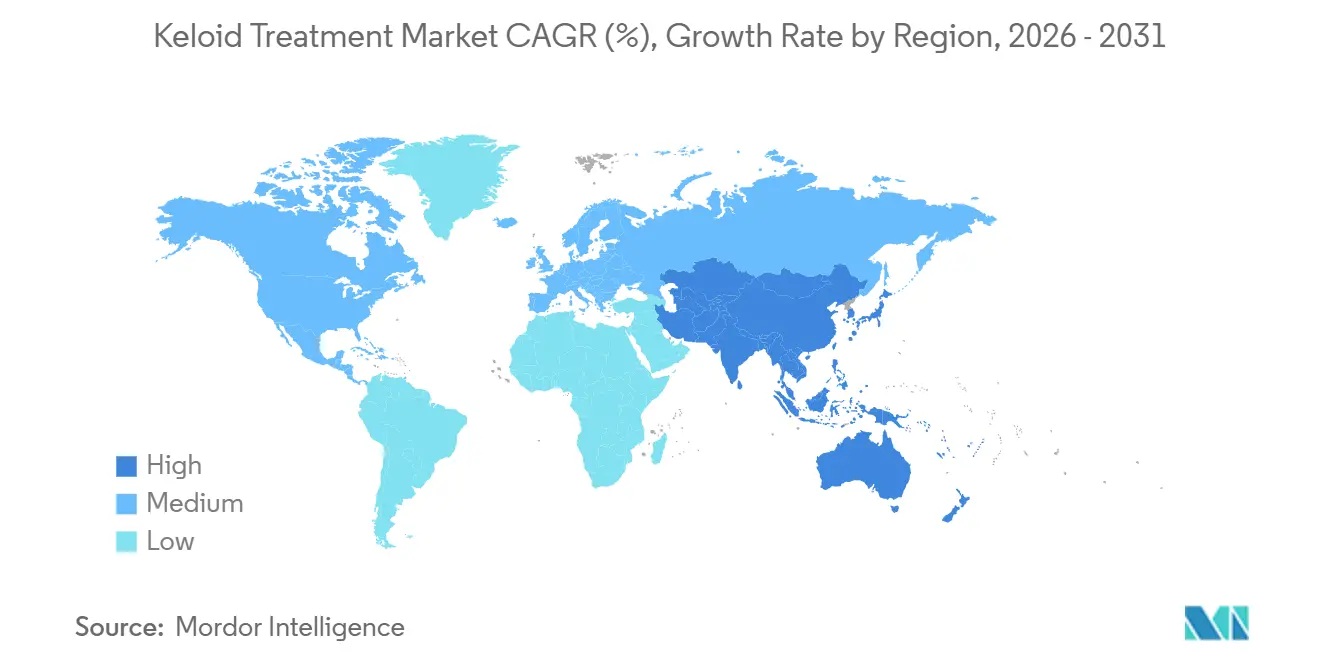

- By geography, North America captured 41.56% of the keloid treatment market share in 2025, while Asia-Pacific is expected to grow at the fastest CAGR of 8.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Keloid Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising preference for multimodal keloid therapy | +1.2% | Global | Medium term (2-4 years) |

| Expanding use of intralesional corticosteroid and 5-FU combination | +0.9% | Global, concentrated in APAC and MEA | Short term (≤ 2 years) |

| Growing adoption of post-excision adjuvant radiotherapy | +0.6% | North America and Europe | Medium term (2-4 years) |

| Better scar-appearance expectations in aesthetic and reconstructive surgery | +0.5% | North America, Europe, and APAC | Long term (≥ 4 years) |

| Increasing availability of laser-assisted delivery and advanced equipment | +0.8% | North America and APAC, especially Japan and South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Preference For Multimodal Keloid Therapy

The keloid treatment market is shifting from single-modality care as recurrence control becomes as critical as short-term lesion reduction. A 2026 systematic review assessing 162 studies found that treatment plans combining intralesional corticosteroids, surgical excision, laser modalities, and radiotherapy delivered stronger and more durable outcomes than single-modality approaches.[2]Masafumi Nakashima et al., “Genomic and Epigenetic Landscapes of Keloid Scarring: Ancestry-Dependent Insights and Therapeutic Implications,” Cosmetics, doi.org This shift increases revenue per treated episode by distributing spending across drugs, procedures, and follow-up visits. A 2025 network meta-analysis reported that Triamcinolone acetonide (TAC) combined with 5-Fluorouracil and pulsed-dye laser achieved a relative risk of 2.98 compared with TAC monotherapy, supporting broader adoption of bundled treatment protocols.[3]Alicia R. Martin et al., “Multi-ancestry Meta-analysis of Keloids Uncovers Novel Susceptibility Loci in Diverse Populations,” Nature Communications, nature.com

Expanding Use Of Intralesional Corticosteroid And 5-FU Combination

The keloid treatment market is benefiting from a clear shift toward corticosteroid and 5-Fluorouracil (5-FU) combinations in settings that support repeat injection protocols. A 2024 systematic review and meta-analysis covering 15 studies found that corticosteroid plus 5-FU delivered stronger patient and observer assessments, greater scar height reduction, and fewer adverse effects, such as hypopigmentation, skin atrophy, and telangiectasia, than corticosteroid-only treatment. This finding supports escalation from low-cost monotherapy to a regimen that improves visible outcomes and tolerability. It also creates a practical market split, with higher-resource clinics adopting combination care and cost-sensitive systems continuing to rely more heavily on steroid-only injections.

Growing Adoption Of Post-Excision Adjuvant Radiotherapy

The keloid treatment market is gaining momentum from the wider use of post-excision adjuvant radiotherapy for large or treatment-resistant lesions. A 2025 retrospective study published in BMC Surgery found that multimodal adjuvant therapy after surgical excision reduced recurrence more effectively than surgery alone. This approach gives clinics a stronger basis for long-term disease control and supports the referral of severe cases to procedural pathways. A March 2025 publication reported zero keloid recurrence across 16 keloids in 12 patients treated with surgical excision plus SRT-100 at Taiwan’s Tri-Service Military Hospital, strengthening the commercial case for superficial radiotherapy systems.

Increasing Availability Of Laser-Assisted Delivery And Advanced Equipment

The keloid treatment market is also receiving support from broader access to laser platforms and related device infrastructure. In December 2025, Sciton received US Food and Drug Administration (FDA) 510(k) clearance for its JOULE 1064nm System for the reduction of red pigmentation in keloid scars, showing that device makers are pursuing specific scar-related indications. In April 2026, Shanghai Apolo Medical Technology received FDA 510(k) clearance for its Picosecond Nd:YAG Laser Systems, signaling that new entrants are targeting regulated scar-treatment applications in the United States. These approvals shorten the path between clinical positioning and commercial adoption while supporting device-linked care as a visible growth engine in the keloid treatment market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High recurrence rates after monotherapy | -1.2% | Global | Short term (≤ 2 years) |

| Adverse events from repeated steroid injections | -0.8% | Global | Short term (≤ 2 years) |

| Limited standardization in protocols and dosing | -0.6% | Global, especially APAC and MEA | Medium term (2-4 years) |

| Access constraints for radiation and device-based care in smaller markets | -0.5% | MEA, South America, and rural APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Recurrence Rates After Monotherapy

High recurrence after single-modality treatment remains a key constraint in the keloid treatment market. A European cohort study (2025) of 206 patients found that patients treated with triamcinolone acetonide (TAC) injections and laser therapy had significantly higher recurrence rates, with TAC reporting χ² = 21.9 and p < 0.001. This limits confidence in low-intensity treatment pathways and increases the likelihood of patients moving through multiple regimens before achieving durable disease control. Repeat visits also reduce care delivery efficiency when they do not result in sustained outcome improvements. In lower-resource settings, where combination care remains less available, this creates a structural ceiling on therapeutic success within the keloid treatment market. Until providers adopt more consistent recurrence-control protocols, the market will continue to record uneven outcomes across regions and provider types.

Access Constraints For Radiation And Device-Based Care In Smaller Markets

The keloid treatment market faces major access constraints in regions with a high epidemiological burden but limited treatment infrastructure. A study from the Regional Hospital Center of Dosso in Niger (2026) reported that local treatment options were largely limited to corticosteroid infiltration and basic excision, while advanced modalities remained largely unavailable. This infrastructure gap limits the conversion of high disease burden into active market revenue. Advanced equipment, trained personnel, and financing channels remain critical to expanding access to higher-value care. Similar constraints affect smaller South American markets and rural parts of Asia, where affordability and practitioner availability continue to limit the penetration of radiation and device-based care. For manufacturers, market expansion will require clinical capacity building, not only product launches and distribution agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Combination Protocols Eroding Corticosteroid Monotherapy Dominance

Intralesional corticosteroids held 28.12% of the keloid treatment market share in 2025, making them the largest treatment segment by revenue. Their position reflected strong clinical familiarity, low acquisition cost, and broad use across hospital and outpatient settings. The segment continues to benefit from established workflows, as clinicians can administer steroid injections without specialized capital equipment. However, the market is shifting away from steroid monotherapy as stronger clinical evidence supports combination regimens for longer-lasting disease control.

A 2025 network meta-analysis showed that combinations involving Triamcinolone acetonide (TAC), 5-Fluorouracil, and laser modalities outperformed monotherapy approaches, supporting protocol migration in high-volume centers. This shift explains why 5-Fluorouracil-based therapy is forecast to expand at the fastest CAGR of 5.53% through 2031 within this segment. Clinicians increasingly use it as the pharmacological backbone of combination regimens rather than only as an alternative injectable. Silicone-based therapy remains important for prevention-oriented use, especially after surgery and in patients for whom repeated injections are less suitable.

By Route of Administration: Device-Based Delivery Gaining Ground On Injectables

Injectable administration accounted for 46.45% of the keloid treatment market size by route of administration in 2025, keeping it the leading delivery channel. This position stemmed from the broad use of intralesional corticosteroids and 5-Fluorouracil in first-line and combination protocols. Injectable therapy aligns well with existing dermatology workflows and does not require the capital investment associated with laser or radiotherapy systems. This advantage keeps injectables central to the market, especially in regions that need familiar and scalable treatment options.

Procedural or device-based administration is projected to grow at a CAGR of 6.67% through 2031, making it the fastest-growing route in the keloid treatment market. Growth reflects demand for laser-assisted delivery, superficial radiotherapy, and cryotherapy systems that improve local tissue targeting while reducing reliance on repeated injections. Device-linked care can also lower dose intensity per session while still supporting visible response. As a result, the market is moving toward a more balanced route mix rather than remaining heavily injectable.

By End User: Dermatology Clinics Outpacing Hospital Growth As Care Migrates Outward

Hospitals held 38.66% of the keloid treatment market in 2025, keeping them the leading end-user category. Their share was supported by complex excision cases, adjuvant radiotherapy delivery, wound management needs, and the ability to coordinate multiple specialists for difficult lesions. Hospitals also remain important because they can manage cases that outpatient clinics are not equipped to handle. Severe lesions, recurrent disease, and post-surgical follow-up continue to create steady hospital-managed demand.

Dermatology clinics are expected to advance at the fastest CAGR of 7.35% through 2031, reflecting the growing role of outpatient care in the keloid treatment market. Providers can deliver intralesional injections, topical follow-up, laser procedures, and cryotherapy without inpatient admission. This improves patient convenience and supports adherence to repeat-session treatment. Shorter visits and lower service intensity also reduce patient drop-off between sessions.

Geography Analysis

North America is expected to account for 41.56% of the keloid treatment market share in 2025, making it the largest regional contributor. The United States is projected to drive this position through its strong dermatology infrastructure, broad procedural availability, and higher per-patient spending on specialist care. The region benefits from an established mix of pharmacological, laser-based, and adjuvant approaches, supporting broader treatment adoption across the care pathway. Canada also supports early commercialization of novel topical options, and BirchBioMed’s expected approval in Canada in February 2026 highlights the region’s role in differentiated product launches.

Asia-Pacific is expected to be the fastest-growing region, with the keloid treatment market size projected to increase at a CAGR of 8.56% through 2031. Elevated genetic susceptibility across several Asian populations, expanding private dermatology networks, and rising focus on scar appearance outcomes after surgery or injury support this growth. South Korea and Japan lead in technology adoption, while China adds scale through its large urban patient pool and expanding dermatology clinic chains. A 2025 multi-ancestry study expected to identify 26 susceptibility loci reinforces the region’s importance for targeted identification and treatment planning.

Europe is expected to hold the third-largest position in 2025, with Germany, the United Kingdom, France, Italy, and Spain contributing most of the regional revenue. The European keloid treatment market reflects a cautious treatment approach, supporting continued use of silicone-led and conservative management pathways. The Middle East and Africa remain underpenetrated despite a high underlying burden, mainly due to limited treatment infrastructure across several countries. South America shows steady growth, with larger countries gradually adopting combination care as dermatology services expand.

Competitive Landscape

The keloid treatment market has a moderately competitive structure, comprising a more recognizable pharmaceutical brand tier and a fragmented device tier. In pharmaceuticals, Alliance Pharma’s Kelo-Cote, Merz Pharma, and Galderma remain prominent through established scar-care and dermatology treatment channels. However, strong reliance on generic corticosteroids and 5-Fluorouracil in many countries limits the control of branded pharmacological players. The device tier remains dispersed, with Sciton, Candela, Cutera, Lumenis, and Sensus Healthcare competing across procedural niches rather than through a single dominant platform.

Several planned and announced developments highlight how companies are strengthening their competitive positioning. Sciton’s December 2025 Food and Drug Administration (FDA) 510(k) clearance for the JOULE 1064nm System would support a more targeted entry into keloid-linked pigmentation management. BirchBioMed’s February 2026 Health Canada approval for FS2 (KynA) would create a differentiated topical offering beyond standard silicone- and steroid-based approaches. Bausch Health and Solta Medical’s April 2025 launch of Fraxel FTX would further strengthen their aesthetic laser portfolio for scar-related treatment settings.

A second competitive shift is emerging from newer anti-fibrotic development programs. Syntara’s topical pan-Lysyl Oxidase inhibitor programs target collagen cross-linking directly, offering a mechanism that differs from established treatments in the keloid treatment market. If this class reaches commercialization, it could create a premium pharmacological layer that existing steroid-led competitors may find difficult to defend. Key white-space opportunities remain in post-surgical prevention, clinic-friendly combination delivery, and improved access models for underserved regions.

Keloid Treatment Industry Leaders

Smith and Nephew plc

Lumenis Be Ltd.

Merz Pharma GmbH and Co. KGaA

Mölnlycke Health Care AB

Cutera, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Shanghai Apolo Medical Technology received FDA 510(k) clearance (K260017) for its Picosecond Nd:YAG Laser Systems (Model: HS-298), enabling US commercialization in the scar and pigmentation treatment segment.

- February 2026: BirchBioMed Inc. received Health Canada approval (NPN 80147114) for FS2 (KynA) 0.5% topical cream as a natural health product for treating scars, including mature keloids, across Canada.

- December 2025: Sciton Inc. received FDA 510(k) clearance (K251077) for its JOULE 1064nm System and Accessories to reduce red pigmentation in keloid scars.

- May 2025: Syntara Limited dosed the first patient in the SATELLITE Phase 1c trial of SNT-6302, a topical pan-LOX inhibitor targeting scar volume reduction in active keloid scars.

Global Keloid Treatment Market Report Scope

As per the scope of the report, a keloid is a type of thick, raised scar that grows beyond the boundaries of an original skin injury. They are typically caused by an overproduction of collagen during the healing process from acne, burns, piercings, or surgery.

The keloid treatment market is segmented by treatment type, route of administration, end user, and geography. By treatment type, the market includes intralesional corticosteroids, 5-fluorouracil-based therapy, silicone-based therapy, cryotherapy, surgical excision with adjuvant therapy, laser therapy, radiation therapy, and other treatment types. By route of administration, the market is segmented into injectable, topical, and procedural or device-based. By end user, the market is segmented into hospitals, dermatology clinics, ambulatory surgical centers, and specialty clinics. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Intralesional Corticosteroids |

| 5-Fluorouracil Based Therapy |

| Silicone Based Therapy |

| Cryotherapy |

| Surgical Excision With Adjuvant Therapy |

| Laser Therapy |

| Radiation Therapy |

| Other Treatment Types |

| Injectable |

| Topical |

| Procedural Or Device Based |

| Hospitals |

| Dermatology Clinics |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Intralesional Corticosteroids | |

| 5-Fluorouracil Based Therapy | ||

| Silicone Based Therapy | ||

| Cryotherapy | ||

| Surgical Excision With Adjuvant Therapy | ||

| Laser Therapy | ||

| Radiation Therapy | ||

| Other Treatment Types | ||

| By Route Of Administration | Injectable | |

| Topical | ||

| Procedural Or Device Based | ||

| By End User | Hospitals | |

| Dermatology Clinics | ||

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of the keloid treatment market?

The keloid treatment market stands at USD 9.10 billion in 2026 and is forecast to reach USD 11.15 billion by 2031 at a CAGR of 4.15%.

Which treatment type leads revenue in keloid care?

Intralesional corticosteroids led treatment revenue with a 28.12% share in 2025, helped by broad clinical familiarity and low barriers to use.

Which therapy is growing fastest for keloid management?

5-Fluorouracil Based Therapy is projected to grow at the fastest CAGR of 5.53% through 2031, supported by wider use in combination regimens.

Why are dermatology clinics gaining share in scar treatment?

Dermatology clinics are projected to expand at 7.35% CAGR because injections, topicals, laser procedures, and cryotherapy can all be delivered efficiently in outpatient settings.

Which region is expanding fastest in this space?

Asia-Pacific is the fastest-growing region, advancing at 8.56% CAGR through 2031 because of higher genetic susceptibility, wider clinic networks, and stronger demand for scar appearance improvement.

What is the main challenge limiting treatment adoption?

High recurrence after monotherapy remains a major barrier, especially in markets where access to combination therapy, radiation, or advanced devices is still limited.

Page last updated on: