Neurotrophic Keratitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

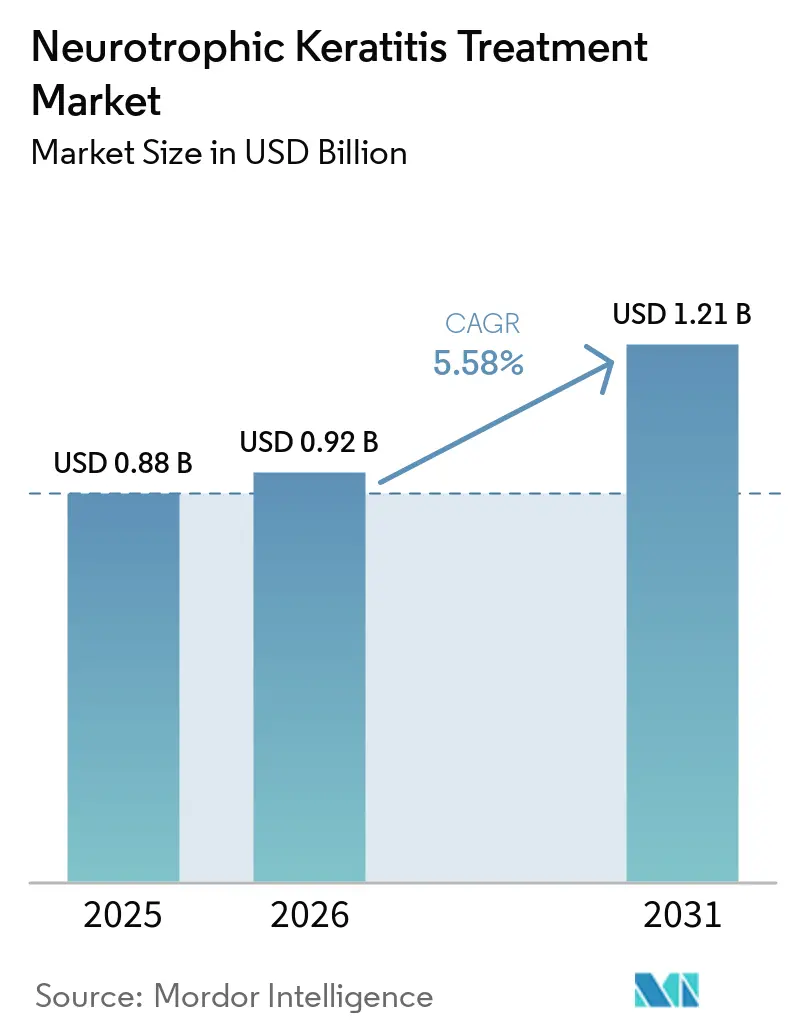

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

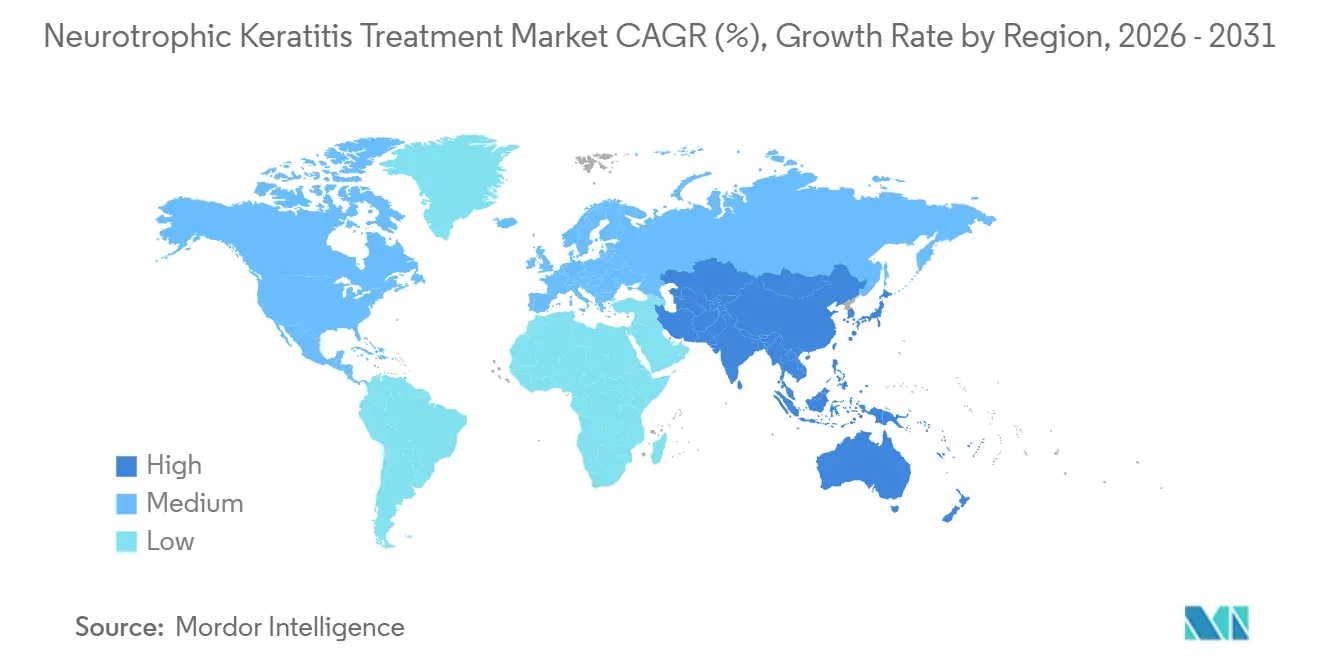

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurotrophic Keratitis Treatment Market Analysis by Mordor Intelligence

The Neurotrophic Keratitis Treatment Market size is projected to expand from USD 0.88 billion in 2025 and USD 0.92 billion in 2026 to USD 1.21 billion by 2031, registering a CAGR of 5.58% between 2026 to 2031.

Accelerated diagnosis, the sunset of cenegermin’s orphan exclusivity in August 2025, and the arrival of lower-frequency gene therapies are reshaping competitive dynamics even as disease prevalence remains stable at 1–5 per 10,000. Artificial tears still dominate prescriptions because most payers require conservative treatment failure before approving recombinant human nerve growth factor (rhNGF), yet hospital formularies are actively preparing for biosimilar entry and streamlined cold-chain logistics. Commercial adoption of portable esthesiometers and in vivo confocal microscopy has more than doubled U.S. claims-based diagnoses since 2020, underscoring that growth is tied to detection rather than incidence. Finally, unmet needs for diabetic and herpes-related corneal neuropathy are intensifying across Asia–Pacific, positioning India and China as pivotal demand centers for next-generation biologics and neurotization procedures.

Key Report Takeaways

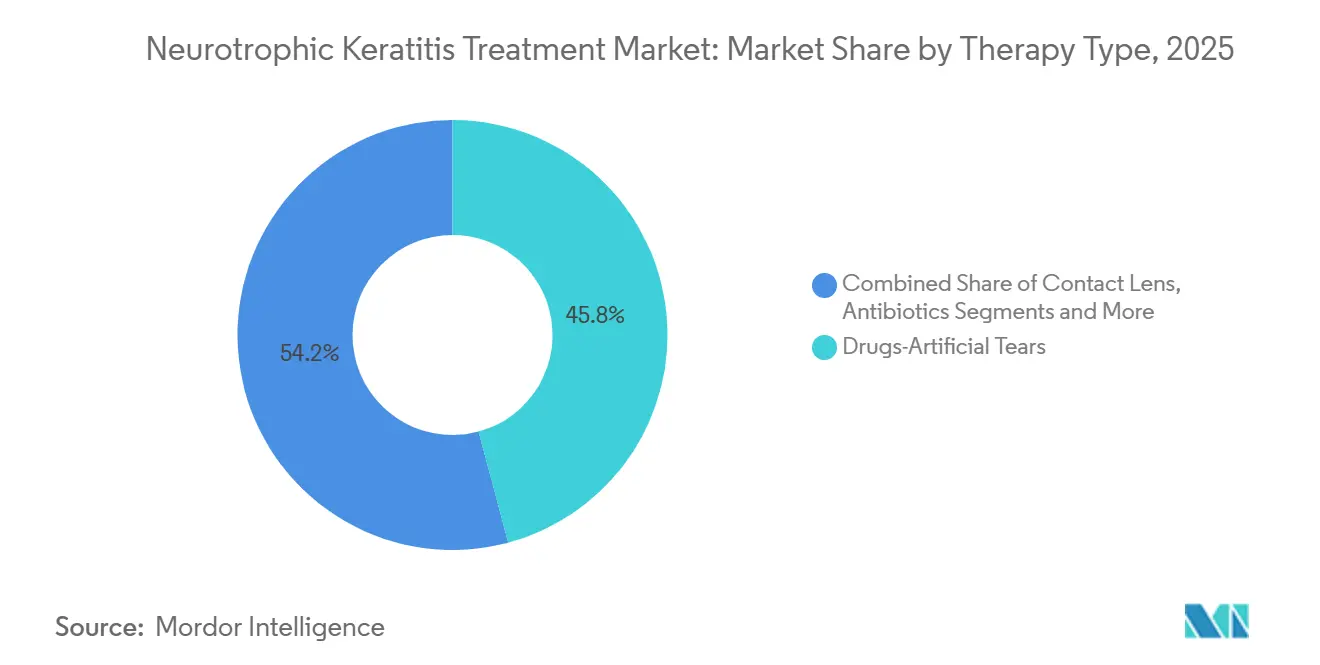

- By therapy type, artificial tears led with 45.82% of the neurotrophic keratitis treatment market share in 2025, while contact lens solutions are forecast to grow at a 5.87% CAGR through 2031.

- By disease stage, stage I disease captured 47.87% share of the neurotrophic keratitis treatment market size in 2025 and is advancing at a 5.92% CAGR through 2031.

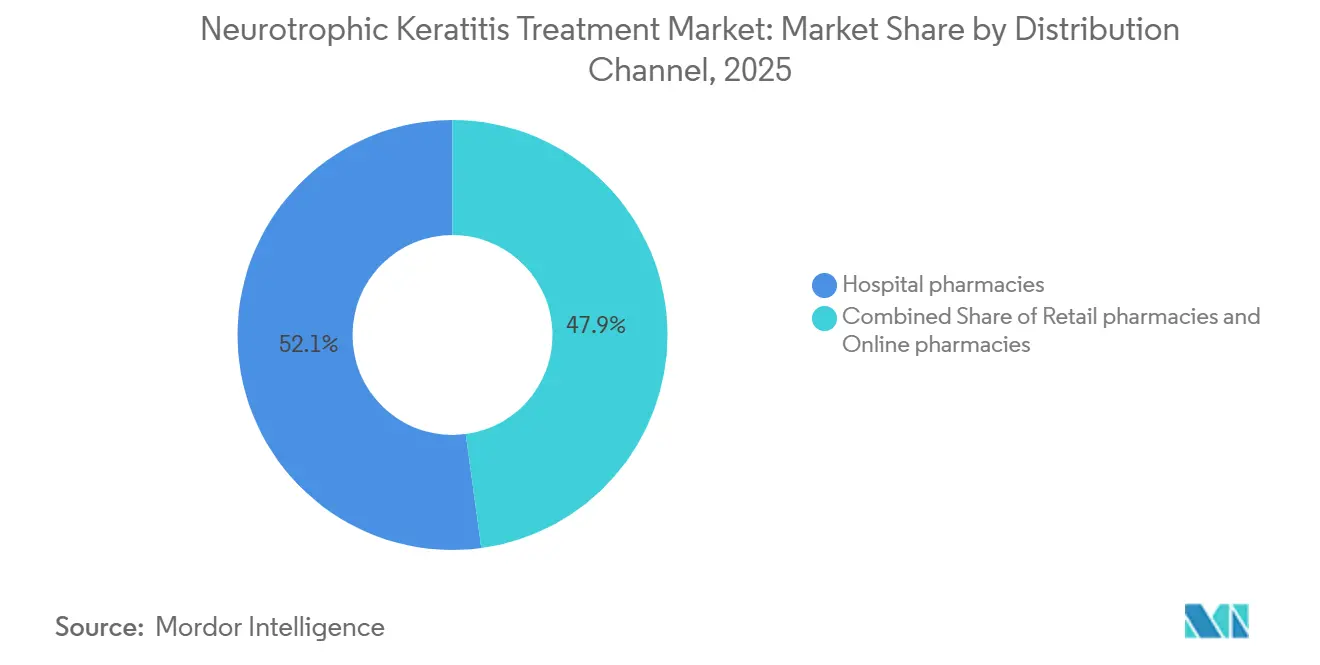

- By distribution channel, hospital pharmacies held 52.13% of 2025 channel revenue, but retail pharmacies are projected to post the fastest growth at 5.67% CAGR owing to step-therapy refill cycles.

- By geography, North America contributed 38.95% revenue in 2025; Asia–Pacific is the fastest-growing region at a 5.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neurotrophic Keratitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding access to cenegermin (rhNGF) | +1.2% | North America and Europe, expanding in China post-Phase IV study | Medium term (2–4 years) |

| Rising HSV/HZO and diabetes prevalence | +1.5% | Global, strongest in Asia–Pacific driven by India | Long term (≥ 4 years) |

| Wider use of esthesiometry and confocal OCT | +1.0% | Tertiary centers in North America and Europe, moving into APAC | Short term (≤ 2 years) |

| Broader coverage for amniotic membrane | +0.8% | North America, Europe, select APAC markets | Medium term (2–4 years) |

| Adoption of minimally invasive neurotization | +0.6% | Specialized centers in North America and Europe | Long term (≥ 4 years) |

| Centralized autologous serum supply chains | +0.5% | North America with pilots in EU and APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Expanding Access to Cenegermin (rhNGF) as First Approved Therapy

Cenegermin’s real-world Phase IV data from China reported 84.6% epithelial closure at week 8, with 90.9% durability at week 56, validating efficacy beyond the pivotal trials. Post-exclusivity biosimilar pursuit is rapid, yet the two-to-eight-degree storage requirement and 15-day discard rule maintain a supply moat for manufacturers with specialty pharmacy infrastructure[1]U.S. Food and Drug Administration, “Cenegermin Prescribing Information,” FDA.GOV. Medicare Part D covers the USD 118,230 eight-week course, but prior authorization imposes 30–60-day delays, nudging hospitals to counsel patients aggressively on adherence. European payers negotiate country-specific rebates, and CADTH has demanded 95% price cuts, signaling cost-effectiveness friction. Gene therapies such as KB801 promise twice-weekly dosing, potentially collapsing both caregiver burden and cold-chain expense.

Rising NK Risk Factors (HSV/HZO, Diabetes)

India hosts 101 million people with diabetes, a figure that could reach 134 million by 2045; diabetic keratopathy affects 47–64% of this population, feeding directly into neurotrophic keratitis prevalence. HSV and HZO continue to underpin neuropathic corneal damage worldwide, and HZO incidence doubles every decade after age 50. Collectively, 31.59% of neurotrophic keratitis patients now carry a diabetes comorbidity, correlating with worse visual outcomes and catalyzing demand for adjuncts like topical insulin, which achieved 81–90% healing in 2024–2025 trials. As LASIK volumes rebound, postoperative hypoesthesia could further enlarge the neurotrophic keratitis treatment market.

Increased Diagnosis Via Esthesiometry and In Vivo Confocal Microscopy

FDA clearance for the portable Brill esthesiometer in 2023 enabled mass screening in dry-eye and glaucoma clinics, driving a 115% jump in U.S. diagnoses from 2020 to 2024. In vivo confocal microscopy measures nerve-fiber length at sub-basal plexus, yet its USD 80,000–150,000 price tag restricts usage to university hospitals. Data from a German referral center showed incidence as high as 13 per 10,000, spotlighting historic underdiagnosis. Earlier detection expands Stage I caseloads but does not guarantee access to regenerative therapy because payers still prioritize conservative management.

Wider Payer Recognition of Amniotic Membrane Devices

Cryopreserved amniotic membranes such as Prokera can be inserted chair-side, reducing surgical backlogs and promoting earlier intervention. U.S. registry data show 29.9% utilization for refractory neurotrophic keratitis, and new policies reimburse use in Stage II disease if conservative modalities fail. The EU MDR 2017/745 tightens post-market vigilance, nudging European tissue banks to consolidate procurement and maintain premium procedure pricing of USD 3,000–8,000. Device makers leverage visual outcome publications to lobby insurers, while ophthalmologists combine membranes with scleral lenses to accelerate epithelial closure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and cost-effectiveness issues | –1.3% | EU cost-sensitive markets and emerging APAC economies | Medium term (2–4 years) |

| Underdiagnosis and late presentation | –0.9% | Markets lacking esthesiometers, especially APAC and MEA | Long term (≥ 4 years) |

| Cold-chain and six-times-daily dosing | –0.7% | Regions without specialty pharmacy networks | Short term (≤ 2 years) |

| Coverage limits on amniotic membrane | –0.6% | U.S. and EU payers enforcing step therapy | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost and Cost-Effectiveness Headwinds for rhNGF Therapy

CADTH calculated an incremental cost-effectiveness ratio above CAD 1 million per QALY and advised reimbursement only after a 95% price cut[2]CADTH, “Cenegermin Reimbursement Review,” CADTH.CA. Germany’s G-BA conferred an “additional benefit” label but is pressing for discounts, while France enforces hospital budget ceilings. Outside wealthy payers, six-times-daily administration imposes hidden expenses because many elderly patients require caregiver assistance. Biosimilars may erode price, yet stringent cold-chain protocols and proprietary fill-finish capabilities remain barriers to commoditization.

Underdiagnosis and Late Presentation Due to Asymptomatic Onset

A multicenter study found 60% of patients presented at Stage II or III, when perforation risk amplifies and costs escalate dramatically. Brill esthesiometer units retail for USD 8,000–12,000, a manageable figure for U.S. practices but prohibitive in many Asian and African clinics. Confocal microscopes cost even more, limiting geographic reach. Consequently, the neurotrophic keratitis treatment market continues to lose value through preventable progression, especially in health systems without reimbursement for preventive testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Artificial Tears Dominate but Regenerative Options Gain Speed

Artificial tears retained 45.82% of neurotrophic keratitis treatment market share in 2025. Their dominance stems from payer-driven step therapy that forces a 90-day trial before higher-cost biologics receive approval, a cycle that perpetuates volume within retail channels. The neurotrophic keratitis treatment market size tied to contact lens solutions is projected to climb at a 5.87% CAGR over 2026–2031 as BostonSight PROSE and EyePrint scleral devices migrate from salvage to first-line protection, establishing a fluid reservoir that shields damaged corneas while awaiting regenerative therapy authorization. Recombinant human nerve growth factor delivered USD 1 billion sales in 2024, yet its six-times-daily regimen and USD 118,230 price tag restrict broad uptake despite proven 84.6% closure rates in Chinese real-world data.

Antibiotics remain ancillary, prescribed prophylactically when defects exceed 2 mm, but they occupy a small revenue slice. Gene therapies are poised to displace chronic eye-drop regimens; Krystal Biotech’s KB801 began dosing in July 2025 and uses a replication-defective HSV-1 vector to provide twice-weekly NGF expression, potentially redefining convenience standards. Should early data replicate cenegermin’s healing outcomes, payer calculus could shift quickly, reducing artificial-tear dependence and altering how the neurotrophic keratitis treatment market evaluates cost-benefit thresholds.

By Disease Stage: Stage I Growth Mirrors Diagnostic Uptake

Stage I accounted for 47.87% of the neurotrophic keratitis treatment market size in 2025 and is growing at 5.92% CAGR, underscoring the impact of widespread esthesiometry screening. Earlier presentation broadens candidacy for autologous serum, bandage lenses, and emerging topical insulin, therapies that deliver lower per-patient spend but prevent costly perforation. Stage II cases drive higher revenue per episode because payers increasingly authorize amniotic membrane once persistent defects emerge.

Stage III forms the smallest pool but the highest cost center; neurotization surgery using AxoGen’s Avance processed nerve grafts achieved about 90% sensory recovery in a 164-eye review[3]AxoGen, “Q3 2024 Earnings Report,” AXOGENINC.COM. These procedures, along with penetrating keratoplasty, consume a disproportionate share of hospital budgets. The neurotrophic keratitis treatment market share tied to Stage III therefore reflects not volume but procedural intensity, reinforcing why insurers face mounting pressure to endorse earlier biologic intervention.

By Distribution Channel: Hospital Dominance Faces Retail Acceleration

Hospital pharmacies supplied 52.13% of 2025 spending thanks to in-house cold storage for cenegermin, on-site amniotic membrane inventory, and integrated contact-lens fitting services. Yet retail pharmacies will post the fastest 5.67% CAGR to 2031 as insurers require three-month artificial-tear trials and as centralized autologous serum providers such as ReGenTree ship directly to local drugstores. The neurotrophic keratitis treatment market size captured by retail outlets could expand further if biosimilar rhNGF achieves ambient stability.

Online channels remain niche because European serialization law and U.S. specialty pharmacy contracts restrict mail-order volume. Nonetheless, vision insurance now reimburses specialty scleral lenses, driving recurring retail transactions for replacement lenses. Cold-chain constraints still steer rhNGF toward hospitals, but any formulation breakthrough would realign share rapidly toward the more convenient retail network.

Geography Analysis

North America commanded 38.95% of 2025 revenue in the neurotrophic keratitis treatment market, with Medicare Part D covering cenegermin despite 30–60-day prior authorization that elongates disease course. Canada’s CADTH approval is conditional on steep discounts, limiting provincial uptake outside Quebec and Ontario. Mexico’s private hospitals carry cenegermin for inbound medical tourists but domestic adoption stays muted due to out-of-pocket burden.

Europe lags North America in revenue yet benefits from an earlier EMA nod and Dompé’s Italian distribution center. Germany’s G-BA labeled cenegermin as conferring “additional benefit” yet is pressing for further rebates, and France imposes tight hospital caps on orphan-drug budgets. EU MDR 2017/745 has slowed U.S. device entry but spurred European tissue banks to scale, partly offsetting supply bottlenecks in amniotic membrane.

Asia-Pacific is forecast to grow fastest at a 5.71% CAGR, propelled by India’s surging diabetes load and China’s positive Phase IV rhNGF data that pave the way for NMPA clearance. Japan and South Korea await regulatory filings yet already perform neurotization with national insurance support, creating pent-up demand once rhNGF or gene therapy clears approval. Middle East and Africa remain constrained by testing gaps and reimbursement limits, whereas Brazil and Argentina show gradual uptake via private insurers.

Competitive Landscape

The neurotrophic keratitis treatment market remains moderately concentrated. Dompé’s Oxervate delivered more than USD 1 billion in global 2024 sales before exclusivity expired. Krystal Biotech’s KB801, dosed first in July 2025 and awarded platform technology designation in October 2025, promises twice-weekly administration that could dismantle rhNGF’s cold-chain moat. Recordati operates a Paris hub handling 27,000 rare-disease orders annually across 60 countries, leveraging specialty pharmacy ties to retain share in hospital channels.

AxoGen reported USD 41.8 million Q3 2024 revenue, up 7% year-over-year, as surgeons increasingly prefer its off-the-shelf Avance graft for corneal neurotization with no donor-site morbidity. BostonSight PROSE and EyePrint devices transition from salvage to prophylaxis, a shift enabled by vision-insurance coverage that bypasses step-therapy clauses. RegeneRx’s RGN-259 achieved 60% complete healing at day 29 versus 12.5% for placebo in Phase III, positioning thymosin β4 as a plausible cenegermin alternative. OKYO Pharma’s February 2026 recruitment of Oxervate’s original developer as chief medical officer signals a pipeline push into corneal neuropathic pain, an adjacent niche. Across tiers, intellectual-property cliffs are intersecting with novel delivery platforms, ensuring that the neurotrophic keratitis treatment market will continue fragmenting while incumbents race to lock in hospital formularies.

Neurotrophic Keratitis Treatment Industry Leaders

Dompé farmaceutici S.p.A.

Bausch + Lomb

Laboratoires Théa

RegeneRx Biopharmaceuticals, Inc.

AxoGen, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ASCRS presented successful management of severe keratoconjunctivitis sicca and neurotrophic keratitis using cryopreserved amniotic membrane with systemic and topical co-therapy.

- October 2025: FDA granted platform technology designation to Krystal Biotech’s HSV-1 vector employed in redosable eye-drop gene therapy KB801 for neurotrophic keratitis.

Global Neurotrophic Keratitis Treatment Market Report Scope

As per the scope of the report, neurotrophic keratitis treatment refers to the medical management aimed at promoting healing and protecting the cornea in cases where there is a loss of corneal sensory innervation. This condition impairs corneal healing due to decreased corneal reflexes and tear production, leading to persistent epithelial defects, ulceration, and potential vision loss.

The segmentation of the neurotrophic keratitis treatment market is categorized by therapy type, disease stage, distribution channel, and geography. By therapy type, the market includes artificial tears, eye drops with recombinant human nerve growth factors, antibiotics, and contact lenses. By disease stage, it is segmented into stage I, stage II, and stage III. By distribution channel, the market is divided into hospital pharmacies, retail pharmacies, and online pharmacies. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Drugs-Artificial Tears |

| Recombinant Human Nerve Growth Factors Eye Drops |

| Antibiotics |

| Contact Lens |

| Stage I |

| Stage II |

| Stage III |

| Hospital pharmacies |

| Retail pharmacies |

| Online pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Drugs-Artificial Tears | |

| Recombinant Human Nerve Growth Factors Eye Drops | ||

| Antibiotics | ||

| Contact Lens | ||

| By Disease Stage | Stage I | |

| Stage II | ||

| Stage III | ||

| By Distribution Channel | Hospital pharmacies | |

| Retail pharmacies | ||

| Online pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the neurotrophic keratitis treatment market today?

The neurotrophic keratitis treatment market size reached USD 0.92 billion in 2026 and is on track to hit USD 1.21 billion by 2031.

What is the expected growth rate to 2031?

The market is projected to register a 5.6% CAGR during 2026-2031, supported by better diagnostics and new regenerative therapeutics.

Which therapy type currently holds the biggest market share?

Artificial tears controlled 45.82% neurotrophic keratitis treatment market share in 2025 because insurers mandate conservative therapy first.

Which segment is growing fastest?

Contact-lens-based solutions are forecast to expand at 5.87% CAGR thanks to wider coverage for scleral devices.

Why is Asia-Pacific witnessing the highest regional CAGR?

Rapid growth in diabetes and herpes zoster ophthalmicus, coupled with broader access to esthesiometry and pending rhNGF approvals, positions Asia-Pacific for a 5.71% CAGR through 2031.

Page last updated on: