Ketamine Clinic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

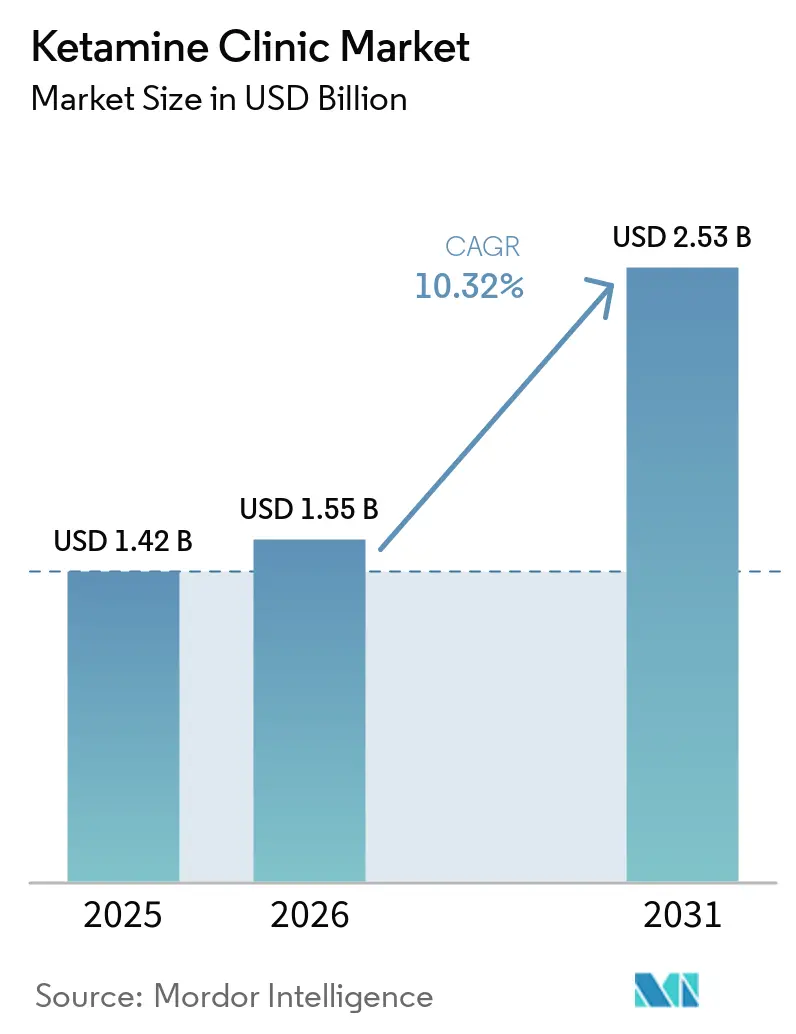

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

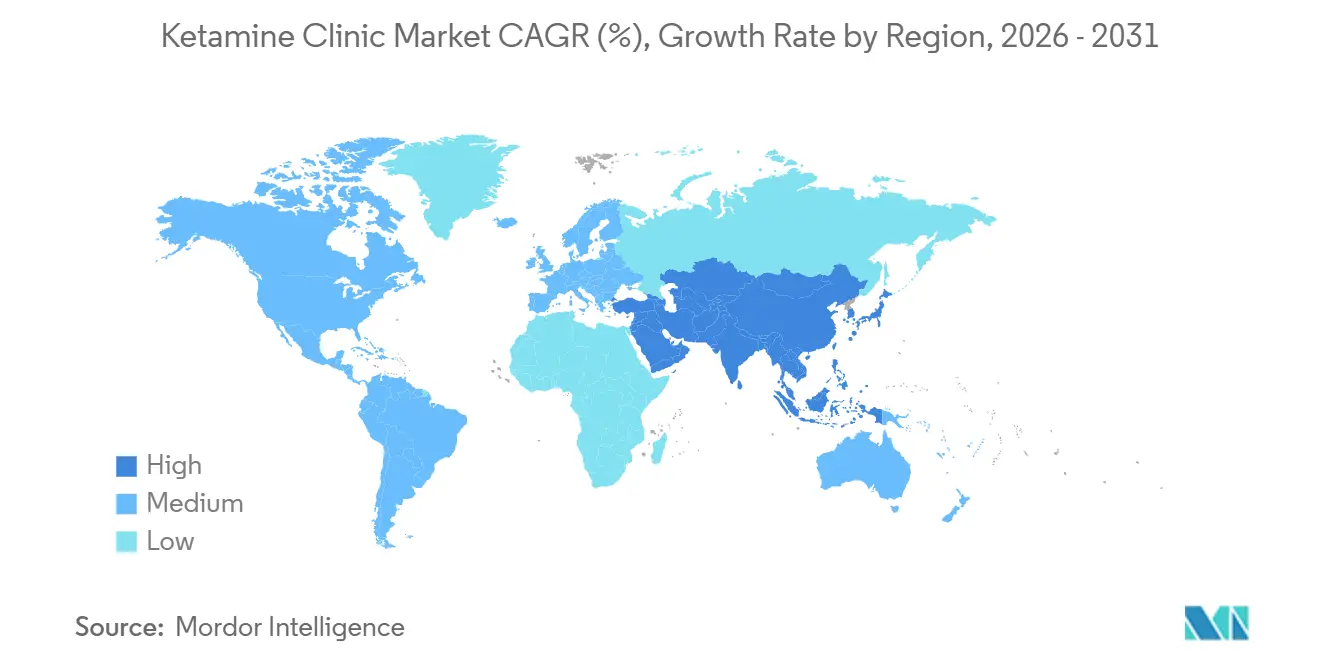

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

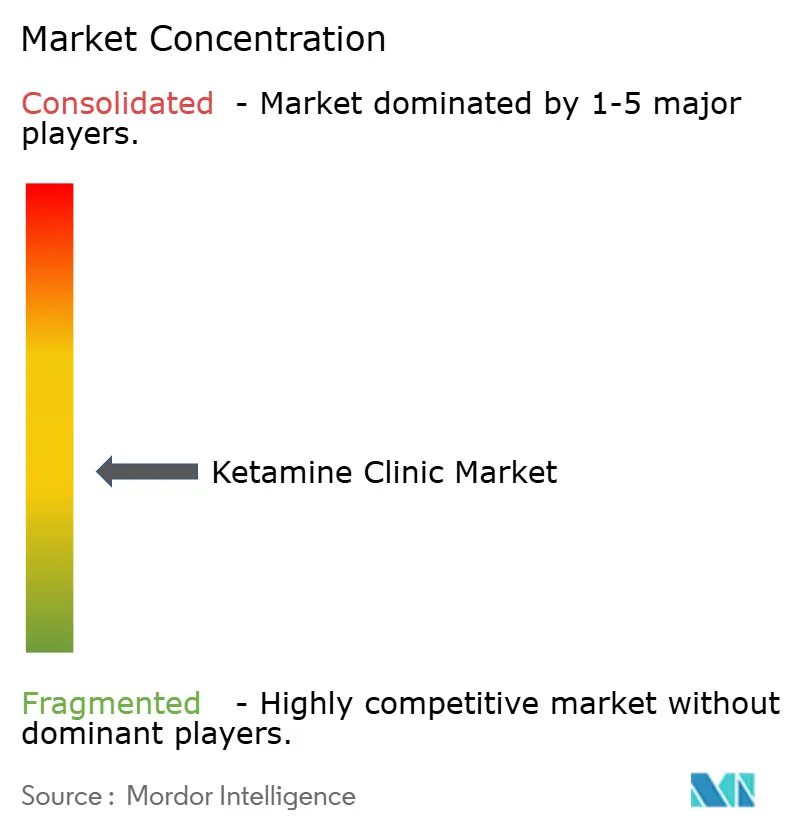

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ketamine Clinic Market Analysis by Mordor Intelligence

The Ketamine Clinic Market size was valued at USD 1.42 billion in 2025 and is estimated to grow from USD 1.55 billion in 2026 to reach USD 2.53 billion by 2031, at a CAGR of 10.32% during the forecast period (2026-2031).

Treatment-resistant depression remains the main structural support for the ketamine clinic market because a large share of adults with major depressive disorder do not achieve remission on oral antidepressants alone, which keeps demand high for faster-acting interventions delivered in supervised care settings. The ketamine clinic market is also being supported by stronger uptake of SPRAVATO, which generated USD 1.7 billion in global sales in 2025 and continued to grow in 2026, giving clinics a larger approved product base around which to build care pathways. The FDA approval of SPRAVATO as monotherapy in January 2025 widened the eligible patient pool because clinics no longer had to rely on mandatory oral antidepressant co-use for every treatment-resistant depression patient. Providers in the ketamine clinic market are responding with more structured intake, closer monitoring, and integrated therapy formats so they can improve retention and defend pricing in a setting where many patients still pay out of pocket. The clearest opportunity in the ketamine clinic market remains with operators that combine compliant administration, stronger documentation, and hybrid delivery models as the treatment base broadens across depression, pain, and related psychiatric indications.

Key Report Takeaways

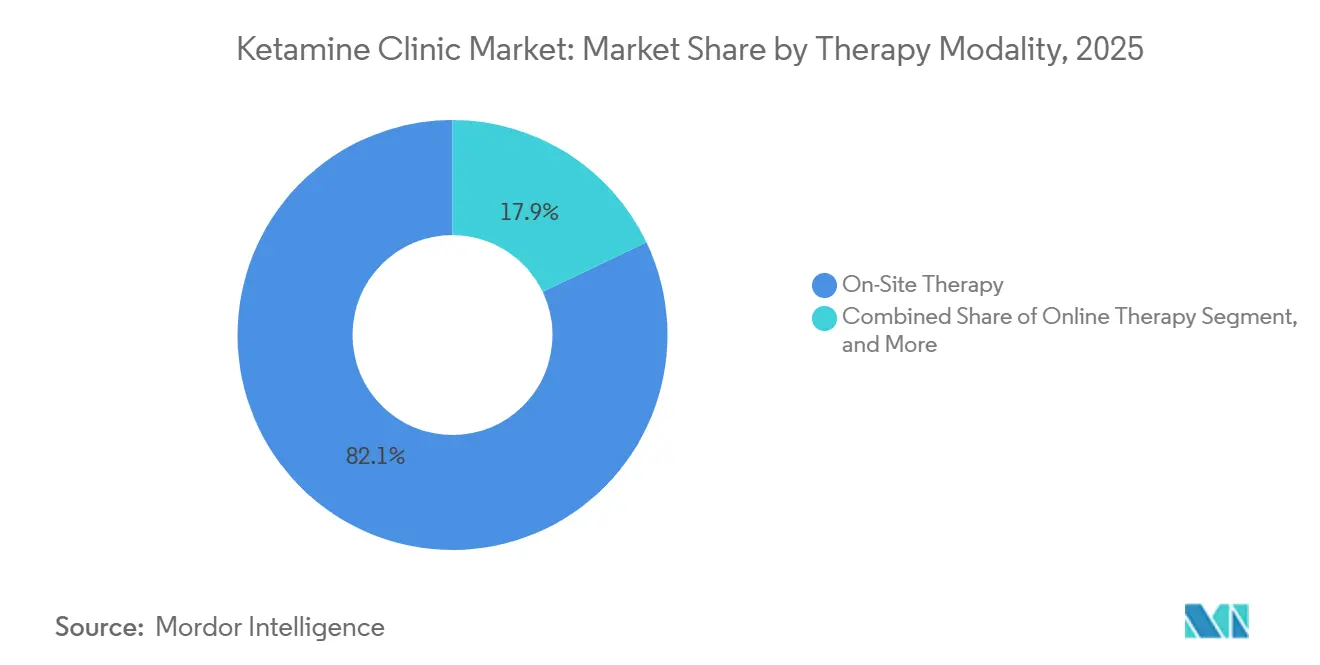

- By therapy modality, on-site therapy held 82.12% share in 2025, while online therapy is forecast to expand at 12.62% CAGR through 2031.

- By clinical indication, depression accounted for 44.17% of the ketamine clinic market size in 2025, while chronic pain is projected to grow at 12.17% CAGR through 2031.

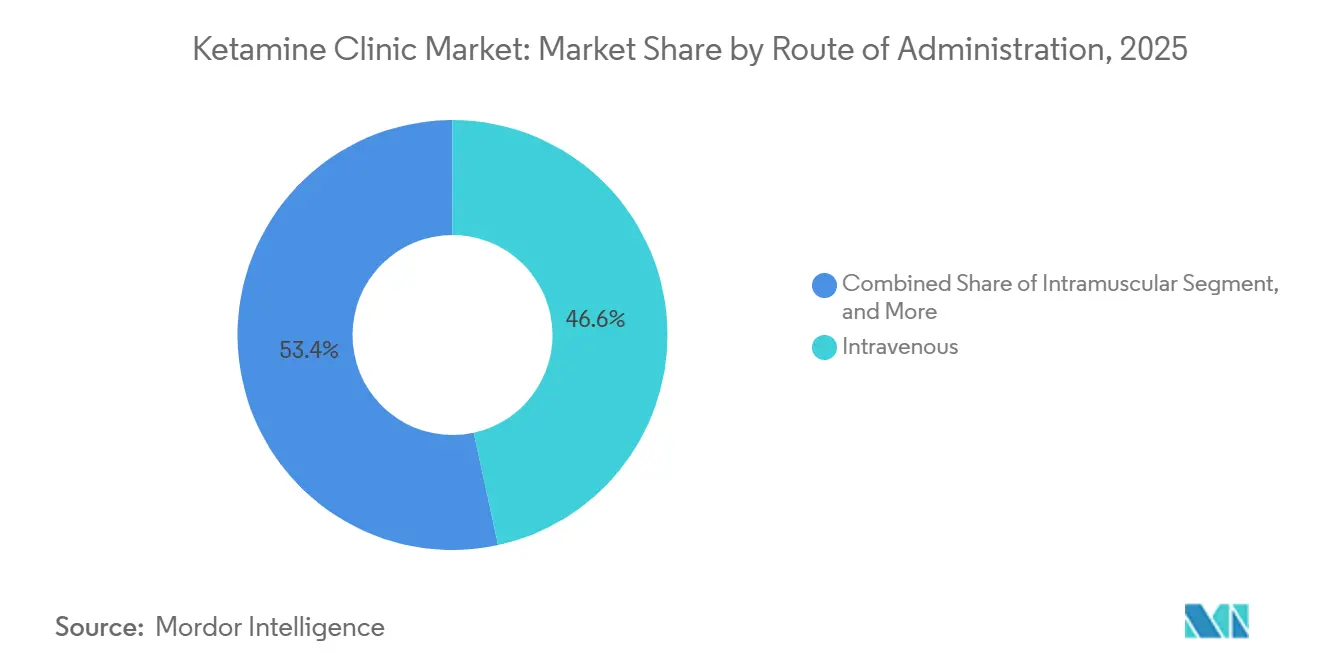

- By route of administration, intravenous delivery held 46.59% share in 2025, while intranasal esketamine is expected to grow at 13.57% CAGR through 2031.

- By care type, medication-only services captured 69.13% share in 2025, while ketamine-assisted psychotherapy is projected to advance at 15.37% CAGR through 2031.

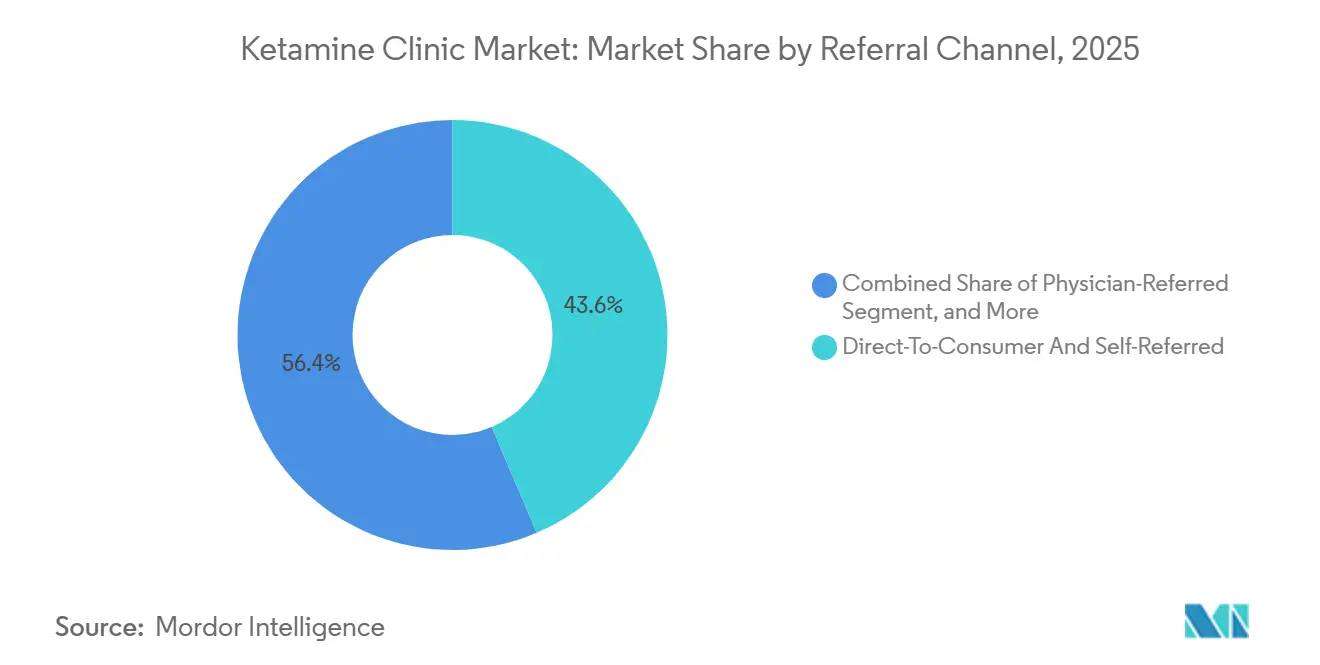

- By referral channel, direct-to-consumer and self-referred patients held 43.62% share in 2025 and are also forecast to expand at 14.07% CAGR through 2031.

- By business model, independently owned private clinics held 36.32% share in 2025, while research and clinical trial centers are projected to grow at 13.72% CAGR through 2031.

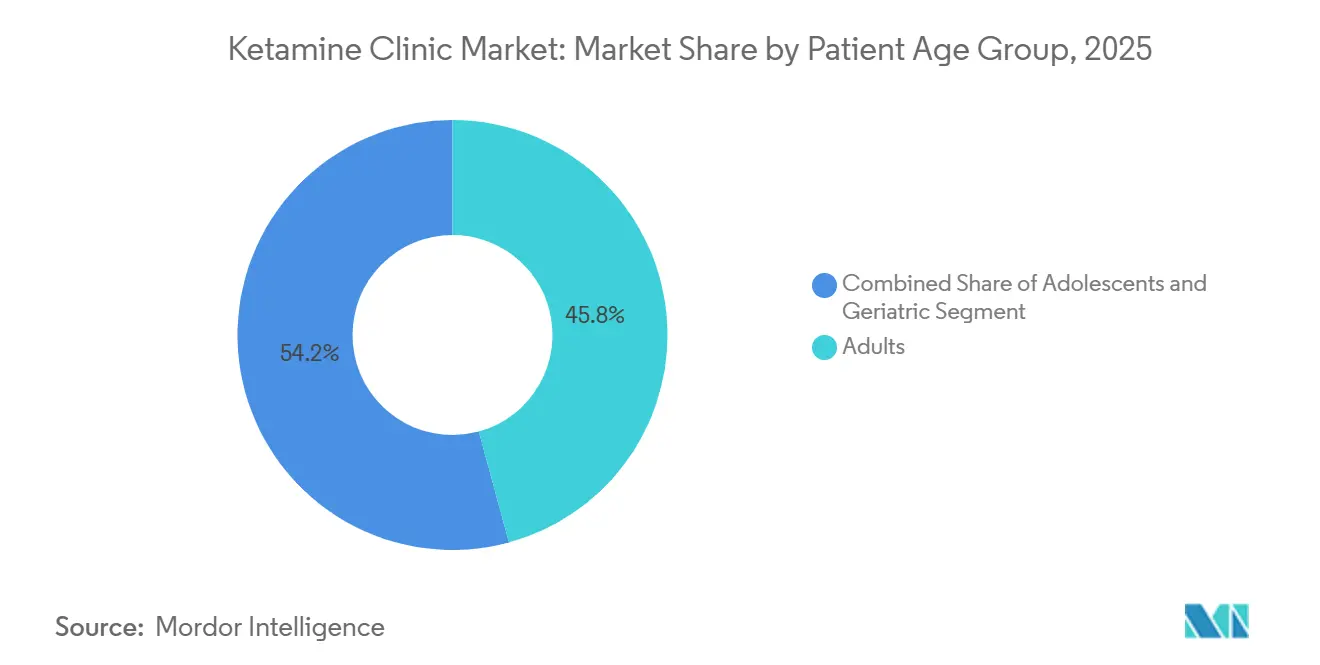

- By patient age group, adults held 45.76% share in 2025, while adolescents are forecast to expand at 12.25% CAGR through 2031.

- By geography, North America held 53.86% of the ketamine clinic market share in 2025, while Asia-Pacific is projected to grow at 11.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ketamine Clinic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Treatment-Resistant Depression Burden | +2.6% | Global, with concentrated impact in North America and Europe | Long term (≥ 4 years) |

| Rapid-Acting Symptom Relief Versus Conventional Antidepressants | +2.0% | North America, Europe, Australia | Medium term (2-4 years) |

| Expansion of Interventional Psychiatry Acceptance | +1.4% | North America, UK, Germany, Australia | Medium term (2-4 years) |

| SPRAVATO Label and Evidence Base Supporting Clinic Adoption | +1.3% | North America, EU, APAC spill-over | Short term (≤ 2 years) |

| Digital Intake, Monitoring, and Hybrid Care Improving Conversion | +0.9% | North America, Australia | Short term (≤ 2 years) |

| Veteran, Pain, and Comorbidity Patient Pools Broadening Demand | +0.8% | North America, spill-over to MEA (military populations) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Treatment-Resistant Depression Burden Expands the Addressable Patient Pool

Treatment-resistant depression supports the ketamine clinic market more directly than the wider antidepressant category because these patients typically reach clinics after repeated medication failure. A 2025 mixed-methods study in The British Journal of Psychiatry covering 2,461 patients with major depressive disorder found that 48% met treatment-resistant depression criteria and 36.9% had tried 4 or more antidepressants, with greater resistance linked to economic inactivity and income loss. A 2025 editorial in Frontiers in Psychiatry also placed treatment-resistant depression prevalence at 30% to 40% among antidepressant-treated patients, which points to a durable ceiling that oral pharmacotherapy alone does not close.[1]Frontiers Editorial Office, “Advancing Education in Interventional Psychiatry, Scoping Review of Simulation Training and the Future of Virtual Reality-Based Learning,” Frontiers in Psychiatry, frontiersin.org This keeps the referral pool unusually qualified because many patients arrive with documented treatment history and a clearer clinical basis for escalation. WHO regional reporting released in September 2025 stated that more than 1 billion people live with mental health conditions globally, which underlines the broad demand base from which ketamine clinics can draw patients across several indications.

Rapid-Acting Symptom Relief Versus Conventional Antidepressants Drives Referral Volume

The ketamine clinic market benefits from the clear contrast between ketamine’s rapid action and the delayed response pattern of standard antidepressants. Johnson & Johnson stated in January 2025 that after a third failed oral antidepressant, 86% of patients do not achieve remission, which gives psychiatrists a strong reason to move suitable patients toward faster-acting options.[2]Johnson & Johnson, “Real World Evidence, Effectiveness and Safety of SPRAVATO Therapy,” J&J Medical Connect, jnjmedicalconnect.com The Phase 4 TRD4005 trial showed improvement within 24 hours of the first dose and a 22.5% remission rate at week 4 compared with 7.6% for placebo across 51 U.S. outpatient centers. This speed matters most in acute suicidal ideation settings because time to effect influences whether the patient stays in a higher-acuity setting or moves into supervised outpatient care. Faster response also helps clinics improve throughput because care cycles can be shortened without removing the need for monitoring during administration.

Expansion of Interventional Psychiatry Acceptance Widens the Prescriber Base

The ketamine clinic market is also gaining from the broader move of interventional psychiatry into routine training and clinical practice. A June 2025 paper in Academic Psychiatry described how one residency program integrated intravenous racemic ketamine into training and linked that decision to evidence showing comparable acute antidepressant effects between ECT and intravenous ketamine. The Interventional Psychiatry Consortium’s 2025 educational series included a dedicated session on ketamine and esketamine with faculty linked to Yale and Stanford, which shows that formal educational attention is widening beyond a small specialist base.[3]Interventional Psychiatry Consortium, “Educational Series Including Ketamine and Esketamine Session,” Interventional Psychiatry Consortium, ipconsortium.org A 2025 scoping review in Frontiers in Psychiatry found broad support for interventional psychiatry training among academic psychiatrists and explicitly pointed to ketamine because peri-procedural monitoring requirements are closer to established interventional treatments than to routine prescribing alone. This is important for clinics because a larger prescriber base means more referrals, more comfort with monitoring requirements, and less hesitation around supervised administration.

SPRAVATO Label and Evidence Base Supporting Clinic Adoption

The January 21, 2025 FDA approval of SPRAVATO as the first monotherapy for adults with treatment-resistant depression removed a major limitation that had tied its use to adjunctive therapy for years. Johnson & Johnson reported USD 468 million in SPRAVATO sales for Q1 2026, up 46.4% year over year, which shows that the approved intranasal pathway is scaling further inside supervised outpatient care. The ketamine clinic market gains from this because approved intranasal treatment lowers setup complexity relative to infusion-heavy models while still supporting in-clinic monitoring. Existing certified administration sites have already absorbed compliance costs, which gives established operators a practical advantage over new entrants trying to build approved care pathways from scratch. Real-world evidence summaries covering more than 6 years of VA experience continued to support the safety and effectiveness profile of SPRAVATO without identifying new safety signals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Insurance Coverage for Off-Label Ketamine Care | -1.7% | National U.S., with partial carve-outs in Canada and EU | Long term (≥ 4 years) |

| Protocol Heterogeneity and Limited Long-Term Outcomes Data | -0.8% | Global | Medium term (2-4 years) |

| FDA and State-Level Scrutiny of Compounded Ketamine and Telehealth Use | -0.7% | U.S. primarily, regulatory influence extends to Canada and Australia | Short term (≤ 2 years) |

| High Total Course Cost and Maintenance Dependence | -0.8% | Global, most acute in uninsured or underinsured North American markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Insurance Coverage for Off-Label Ketamine Constrains Market Expansion

Coverage remains one of the most persistent limits on the ketamine clinic market because reimbursement is much stronger for SPRAVATO than for intravenous or compounded psychiatric ketamine. Harvard Law School’s Petrie-Flom Center noted that Medicare Part B covers SPRAVATO at 80% after the annual deductible, while off-label psychedelic and ketamine pathways remain much harder to reimburse through standard public insurance structures. This creates a split market where REMS-certified and hospital-linked providers are better placed to work within reimbursable channels, while many independent infusion operators continue to rely on self-pay demand. The result is lower treatment continuity for price-sensitive patients who may complete induction but not remain on maintenance schedules. This also limits penetration into lower-income populations even when the clinical need is clear.

Protocol Heterogeneity and Limited Long-Term Outcomes Data Temper Clinical Confidence

The ketamine clinic market still faces hesitation from payers and referring physicians because dosing, monitoring, and follow-up practices vary widely across providers. A 2025 systematic review in Current Treatment Options in Psychiatry covering 8 ketamine-assisted psychotherapy studies and 421 participants found symptom improvement but also highlighted small samples, variable protocols, and short follow-up periods. A 2025 Cochrane review of 67 trials found no clear evidence of benefit for chronic pain and flagged adverse-event concerns such as delusion and delirium with intravenous routes. Cleveland Clinic’s standardized 5-day protocol across 1,034 chronic pain patients showed that clinics can improve confidence when they track completion, repeat use, and follow-up outcomes in a consistent way. Until more of the sector does the same, heterogeneity will continue to slow payer acceptance and broader clinical adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Modality: On-Site Infrastructure Dominates, Digital Delivery Accelerates

On-site therapy held 82.12% of the therapy modality segment in 2025, giving it the largest share of the ketamine clinic market size. REMS requirements keep SPRAVATO administration inside certified settings with direct supervision, which continues to favor facility-based delivery for approved intranasal treatment. Sedation, dissociation, and blood pressure monitoring also make on-site care the safest and most defensible model for higher-acuity psychiatric treatment. Hybrid therapy remains the middle ground because it allows clinics to start induction in person and shift parts of maintenance and follow-up into telehealth workflows. That structure helps operators lower per-patient cost without removing acute-phase oversight.

Online therapy is projected to grow at 12.62% CAGR through 2031, making it the fastest-growing modality in the ketamine clinic market. Growth is being driven by platforms offering oral and sublingual compounded ketamine with digital intake, remote prescribing, and asynchronous monitoring where regulation permits. The ketamine clinic industry is moving toward operators that can manage both compliant in-person administration and digital patient acquisition without weakening clinical screening. That dual positioning helps clinics capture patients earlier, extend engagement after induction, and improve conversion across the care pathway. The larger certified-site footprint in the United States also makes it easier for digital-first platforms to connect remote intake with supervised in-person administration when required.

By Clinical Indication: Depression Anchors Revenue, Chronic Pain Reshapes the Growth Profile

Depression held 44.17% of the clinical indication segment in 2025, making it the largest revenue base in the ketamine clinic market. This leadership reflects the strength of treatment-resistant depression referrals and the clearer reimbursement path available through SPRAVATO for suitable patients. Anxiety disorders, PTSD, OCD, and substance use disorders all add meaningful volume, but they continue to sit more heavily in self-pay channels. That mix keeps depression central because it is the segment most aligned with an approved product, clearer referral patterns, and stronger clinical familiarity. It also means clinics with better psychiatric evaluation and documentation systems are better placed to keep utilization high.

Chronic pain is forecast to expand at 12.17% CAGR through 2031, making it the fastest-growing indication in the ketamine clinic market. Cleveland Clinic reported that 86.1% of patients completed its low-dose infusion protocol and 80% returned for repeat infusions, while 20% to 46% achieved clinically meaningful improvement at 3 and 6 months, which supports stronger retention economics than one-time episodic care. A 2024 Frontiers in Psychiatry meta-analysis across veteran samples found an effect size of 1.8 for ketamine across pain, depression, and PTSD, which supports multi-indication positioning for clinics that already have monitoring capability. Other indications, such as eating disorders and identity-based trauma, remain early-stage niches, but they are beginning to attract more structured protocol development through psychotherapy-linked care. The ketamine clinic market, therefore, remains anchored by depression, while chronic pain is broadening the demand profile and extending maintenance potential.

By Route of Administration: Intravenous Leads, Intranasal Esketamine Disrupts the Protocol Mix

Intravenous administration held 46.59% of the route-of-administration segment in 2025, which made it the leading route in the ketamine clinic market. Intravenous ketamine remains the reference pathway for many treatment-resistant depression and pain protocols because dose titration is precise and onset is fast. Intramuscular and subcutaneous routes hold smaller shares, but they remain clinically relevant where vascular access is difficult or procedural burden must be reduced. This preserves a strong place for infusion-centered care even as product mix changes. It also supports the premium position of hospital-affiliated and specialist clinics that can manage higher monitoring intensity.

Intranasal esketamine is expected to grow at 13.57% CAGR through 2031, making it the fastest-growing route. The January 2025 FDA monotherapy approval widened the patient pool for intranasal use and removed the need for mandatory oral antidepressant co-prescribing in every eligible treatment-resistant depression case. Intranasal treatment also reduces nursing intensity and clinic setup complexity compared with infusion-heavy models, which makes expansion easier for approved outpatient settings. Sublingual and oral routes are growing in telehealth channels, but concerns around compounded formulations and inconsistent dosing continue to limit how far those sub-segments can scale under closer regulatory review. The ketamine clinic market is therefore moving toward a more mixed route profile, with intravenous care retaining its premium role while intranasal therapy expands the reach of supervised outpatient treatment.

By Care Type: Medication-Only Dominates, KAP Commands the Fastest Expansion

Medication-only services held 69.13% of the care-type segment in 2025, which reflects the infusion-center origins of much of the ketamine clinic market. Many providers were built first around medication delivery, observation, and symptom relief rather than around integrated psychotherapy programs. That foundation still supports a large part of current revenue because it is operationally simpler and easier to scale across supervision-based clinic formats. It also fits both approved intranasal administration and established intravenous infusion workflows. As a result, medication-only care remains the largest format even while patient expectations are changing.

Ketamine-assisted psychotherapy is forecast to grow at 15.37% CAGR through 2031, which is the fastest rate across all segmentation types in this study. A 2025 study in The British Journal of Psychiatry found that ketamine infusions combined with psychotherapy and a structured environment sustained depression improvement for at least 8 weeks, compared with the shorter effect window seen with ketamine alone. A 2026 systematic review in Psychopharmacology also reported significant depressive symptom reductions across 11 ketamine-assisted psychotherapy studies. Group-based formats have also shown promise, with a 2025 Frontiers in Psychiatry pilot reporting full retention and meaningful declines in depression and anxiety scores when ketamine-assisted group psychotherapy was combined with cognitive processing therapy. The ketamine clinic industry is moving toward longer engagement cycles and higher-value integrated programs, which gives psychotherapy-linked care a stronger commercial role than medication alone.

By Referral Channel: Self-Referral Signals Strong Consumer Demand With Quality Implications

Direct-to-consumer and self-referred patients held 43.62% of the referral channel segment in 2025, which gave them the largest share in the ketamine clinic market. This shows that many patients do not enter care through traditional psychiatrist or payer pathways and instead search directly for new options after repeated symptom burden. That pattern is consistent with treatment-resistant mental health conditions, where patients often arrive after exhausting several medication lines. It also keeps consumer-facing digital intake and search visibility important for clinic growth. At the same time, self-referral creates more variation in case complexity and diagnostic certainty at the first point of contact.

This channel is also expected to grow at 14.07% CAGR through 2031, which makes it the fastest-growing referral pathway in the ketamine clinic market. Physician-referred patients still tend to bring stronger documentation and higher completion rates, which is why clinics continue to value psychiatrist and health system relationships. Government-linked care pathways may also expand over time as more supervised programs are integrated into institutional settings, especially in veterans and pain populations. The core challenge is that self-referred patients are less likely to arrive with fully verified treatment-resistant depression workups, which complicates standardized outcome reporting across clinics. Operators with tighter pre-intake screening and more consistent eligibility protocols will be better placed to turn this high-volume channel into durable payer and physician trust.

By Business Model: Independent Clinics Hold Largest Share, Research Centres Drive Fastest Growth

Independently owned private clinics held 36.32% of the business model segment in 2025, which made them the largest operator category in the ketamine clinic market. This reflects the entrepreneurial origins of the sector, where many early providers built local cash-pay infusion models before larger systems moved in. Franchise networks, hospital-affiliated centers, and practice-extension models in anesthesiology or psychology also hold meaningful positions. Hospital-linked operators benefit from existing insurance and compliance systems, while procedural practices benefit from staffing familiarity with monitored administration. Even so, independent clinics still retain a large share because they entered early and remain active across many local markets.

Research and clinical trial centers are projected to grow at 13.72% CAGR through 2031, making them the fastest-growing business model. This reflects the overlap between investigational infrastructure and commercial clinic delivery as newer psychiatric and psychedelic-adjacent programs move through late-stage development. The ketamine clinic market is likely to see more providers use trial work to offset operating costs and strengthen protocol discipline as newer products progress through development pathways. That model can be more resilient than pure private-pay structures because it blends patient care with sponsored research activity. It also explains why operators with stronger institutional ties may scale more steadily than clinics that depend only on self-pay volume and repeated maintenance demand.

By Patient Age Group: Adults Lead, Adolescent Demand Reshapes Intake Protocols

Adults held 45.76% of the patient age group segment in 2025, which kept them as the leading age cohort in the ketamine clinic market. This reflects the demographic center of treatment-resistant depression, where working-age patients often present after several unsuccessful antidepressant trials. Geriatric patients form an important secondary group because treatment resistance and chronic pain often overlap in older populations. However, cardiovascular monitoring and comorbidity review can make administration more complex in that age band. Adults therefore remain the largest cohort because need, referral patterns, and clinic suitability align most clearly in this group.

Adolescents are projected to grow at 12.25% CAGR through 2031, making them the fastest-growing age segment. A 2026 report in the Journal of Military, Veteran, and Family Health described significant PTSD score reductions after sublingual ketamine was combined with an intensive outpatient program, which supports the broader point that younger trauma-linked presentations are drawing more attention in supervised care pathways. Clinics serving adolescents must work through parental consent requirements, state prescribing restrictions, and the lack of FDA pediatric labeling for ketamine formulations. That tends to favor hospital-affiliated and franchise operators over smaller stand-alone clinics with fewer legal and administrative resources. The ketamine clinic market is therefore broadening by age, but younger patient growth will require more standardized intake and governance than most providers use today.

Geography Analysis

North America held 53.86% of the ketamine clinic market share in 2025, which made it the largest regional contributor. The region combines the deepest clinic infrastructure, the strongest approved product presence, and the broadest base of psychiatrists and interventional providers. More than 7,000 REMS-certified SPRAVATO administration sites were operating in the United States in 2026, which shows how far supervised delivery capacity has expanded in a short period. Canada is adding private ketamine clinic capacity, but the absence of broad approved esketamine coverage keeps much of care in self-pay channels. U.S. telemedicine rules announced in January 2025 will continue to shape how digital-first providers in the ketamine clinic market expand without creating controlled-substance compliance risk.

Europe is the second-largest regional segment in the ketamine clinic market, with Germany, the UK, and France leading adoption. The region is advancing through a mix of private pay and more formal evaluation pathways tied to national reimbursement systems. Post-marketing experience from academic centers in countries such as Italy and Spain has continued to support the safety and efficacy profile seen in earlier SPRAVATO studies. Wider health technology assessment support would materially lift physician-referred volume, while private clinics continue building demand ahead of fuller coverage decisions.

Asia-Pacific is projected to expand at 11.64% CAGR through 2031, making it the fastest-growing regional component of the ketamine clinic market size forecast. Australia leads regional development, with Avive Health opening a Melbourne clinic in mid-2026 and adding 120 inpatient beds across 2 Victorian hospitals for ketamine and psychedelic-assisted therapies. Japan and South Korea are seeing greater off-label intravenous ketamine use in anesthesiology-adjacent settings, while China’s private hospital sector is building infusion infrastructure for psychiatric and anesthetic applications. India and much of the wider Asia-Pacific periphery remain early stage because regulatory heterogeneity and psychiatrist density still limit near-term penetration. The Middle East and Africa and South America remain smaller parts of the ketamine clinic market, with GCC countries and Brazil appearing most likely to move earlier because private healthcare capacity and higher-income patient pools are more supportive of novel therapy adoption.

Competitive Landscape

The ketamine clinic market shows medium concentration with growing competition across independent clinics, franchise networks, hospital-affiliated providers, and telehealth platforms. No single operator holds a nationally dominant share, which keeps the provider base fragmented across local and regional markets. Competition is mainly local for on-site treatment and broader for digital intake and patient acquisition. This keeps clinical differentiation, protocol quality, and intake conversion central to performance. Johnson & Johnson holds a distinct role in the ketamine clinic market because it supplies the only FDA-approved esketamine product and anchors a large part of the supervised administration framework through SPRAVATO and REMS-linked care pathways.

Leading operators are increasingly using bundled care models that combine ketamine with psychotherapy, TMS, and closer monitoring. HOPE Therapeutics used financing announced in January 2025 and May 2025 to support the acquisition of Dura Medical, Kadima, and NeuroSpa as part of a wider interventional psychiatry buildout. The company also moved to deploy EMOCARE AI monitoring across its network, which shows how digital monitoring is becoming part of clinic differentiation. Johnson & Johnson’s 2025 monotherapy label expansion and continued product growth made intranasal treatment easier to incorporate into outpatient clinic models. Avive Health’s 2026 expansion in Australia also shows that capacity growth is extending beyond stand-alone infusion centers into larger mental health settings.

The ketamine clinic market also shows a widening gap between operators built around disciplined compliance and those that relied too heavily on cash-pay momentum. Providers that produce standardized outcome measures, stronger EHR-linked documentation, and payer-ready records are better placed to access employer and health system channels over time. Smaller technology firms are also helping clinics improve lead qualification and vital-sign monitoring, which narrows the operating gap between larger networks and independent sites. The result is a ketamine clinic market that remains moderately fragmented, but is moving toward clearer differentiation based on compliance, integrated care, and evidence generation.

Ketamine Clinic Industry Leaders

Bloom Mental Health

HealingMaps Ketamine Network

Johnson and Johnson Services, Inc.

Nue Life Health

Revitalist Lifestyle and Wellness Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Avive Health's Melbourne clinic is set to open, adding 120 inpatient beds across two Victorian hospitals and offering ketamine and psychedelic-assisted therapies, supporting approximately 2,000 admissions annually.

- March 2026: The U.S. Department of Veterans Affairs confirmed ketamine and esketamine deployment at 53 VA medical facilities, during a Senate Veterans' Affairs Committee hearing on the bipartisan VHA Novel Therapeutics Preparedness Act of 2026; the Act would also establish a dedicated Office of Novel Therapeutics within the VA.

- May 2025: HOPE Therapeutics signed a USD 7.8 million debt financing term sheet with Universal Capital to fund acquisitions of Dura Medical, Kadima, and NeuroSpa, advancing its national rollup of interventional psychiatry clinics offering IV ketamine, TMS, and AI-based monitoring.

- January 2025: FDA approved SPRAVATO (esketamine) as the first monotherapy for adults with TRD, based on the Phase 4 TRD4005 randomised double-blind trial demonstrating 22.5% remission at week 4 versus 7.6% for placebo; this was FDA's first such approval following Priority Review.

Global Ketamine Clinic Market Report Scope

A ketamine clinic is a specialized medical facility that administers controlled doses of ketamine off-label to treat severe, treatment-resistant mental health conditions, such as depression, anxiety, and PTSD. The ketamine clinic market encompasses the global healthcare businesses and telemedicine providers delivering these services.

The Ketamine Clinic Market is segmented by therapy modality, clinical indication, route of administration, care type, referral channel, business model, patient age group, and geography. By therapy modality, clinics provide on‑site therapy, online therapy, and hybrid therapy options. By clinical indication, ketamine treatments address depression, anxiety disorders, post‑traumatic stress disorder, obsessive‑compulsive disorder, substance use disorders, chronic pain, and other conditions. By route of administration, therapies are delivered via intravenous, intramuscular, intranasal esketamine, sublingual and oral, and subcutaneous methods. By care type, clinics offer medication‑only approaches or ketamine‑assisted psychotherapy. By referral channel, patients access services through direct‑to‑consumer and self‑referral, physician referral, or payer and case‑management referral pathways. By business model, the market includes independently owned private clinics, franchise‑owned clinics, hospital‑affiliated clinics, research and clinical trial centers, and anesthesiology and psychology practice extensions. By patient age group, services are tailored for adolescents, adults, and the geriatric population. Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia‑Pacific), Middle East & Africa (GCC, South Africa, Rest of MEA), and South America (Brazil, Argentina, Rest of South America), reflecting the global expansion of ketamine‑based therapies.

| On-Site Therapy |

| Online Therapy |

| Hybrid Therapy |

| Depression |

| Anxiety Disorders |

| Post-Traumatic Stress Disorder |

| Obsessive-Compulsive Disorder |

| Substance Use Disorders |

| Chronic Pain |

| Other Clinical Indications |

| Intravenous |

| Intramuscular |

| Intranasal Esketamine |

| Sublingual And Oral |

| Subcutaneous |

| Medication-Only |

| Ketamine-Assisted Psychotherapy |

| Direct-To-Consumer And Self-Referred |

| Physician-Referred |

| Payer And Case-Management Referred |

| Independently Owned Private Clinics |

| Franchise-Owned Clinics |

| Hospital-Affiliated Clinics |

| Research And Clinical Trial Centers |

| Anesthesiology And Psychology Practice Extensions |

| Adolescents |

| Adults |

| Geriatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Modality | On-Site Therapy | |

| Online Therapy | ||

| Hybrid Therapy | ||

| By Clinical Indication | Depression | |

| Anxiety Disorders | ||

| Post-Traumatic Stress Disorder | ||

| Obsessive-Compulsive Disorder | ||

| Substance Use Disorders | ||

| Chronic Pain | ||

| Other Clinical Indications | ||

| By Route Of Administration | Intravenous | |

| Intramuscular | ||

| Intranasal Esketamine | ||

| Sublingual And Oral | ||

| Subcutaneous | ||

| By Care Type | Medication-Only | |

| Ketamine-Assisted Psychotherapy | ||

| By Referral Channel | Direct-To-Consumer And Self-Referred | |

| Physician-Referred | ||

| Payer And Case-Management Referred | ||

| By Business Model | Independently Owned Private Clinics | |

| Franchise-Owned Clinics | ||

| Hospital-Affiliated Clinics | ||

| Research And Clinical Trial Centers | ||

| Anesthesiology And Psychology Practice Extensions | ||

| By Patient Age Group | Adolescents | |

| Adults | ||

| Geriatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the ketamine clinic market by 2031?

The ketamine clinic market is forecast to reach USD 2.53 billion by 2031, rising from USD 1.55 billion in 2026 at a 10.32% CAGR.

Which region leads ketamine clinic demand today?

North America leads with 53.86% share in 2025 because it has the strongest clinic infrastructure, approved product presence, and prescriber base.

Which therapy modality is largest, and which one is growing fastest?

On-site therapy was the largest modality at 82.12% share in 2025, while online therapy is projected to grow fastest at 12.62% CAGR through 2031.

Why is demand rising for ketamine-based care?

The main drivers are the high burden of treatment-resistant depression, faster symptom relief than conventional antidepressants, wider interventional psychiatry acceptance, and stronger clinic adoption after the 2025 SPRAVATO monotherapy approval.

Why is ketamine-assisted psychotherapy gaining traction?

Ketamine-assisted psychotherapy is projected to grow at 15.37% CAGR because clinical studies show that combining ketamine with psychotherapy can extend symptom improvement beyond the shorter effect window seen with medication alone.

What are the biggest barriers to wider clinic expansion?

The main barriers are limited insurance coverage for off-label ketamine routes, protocol variation, regulatory scrutiny around telehealth and compounding, and the high cost of full treatment and maintenance.

Page last updated on: