United States High-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

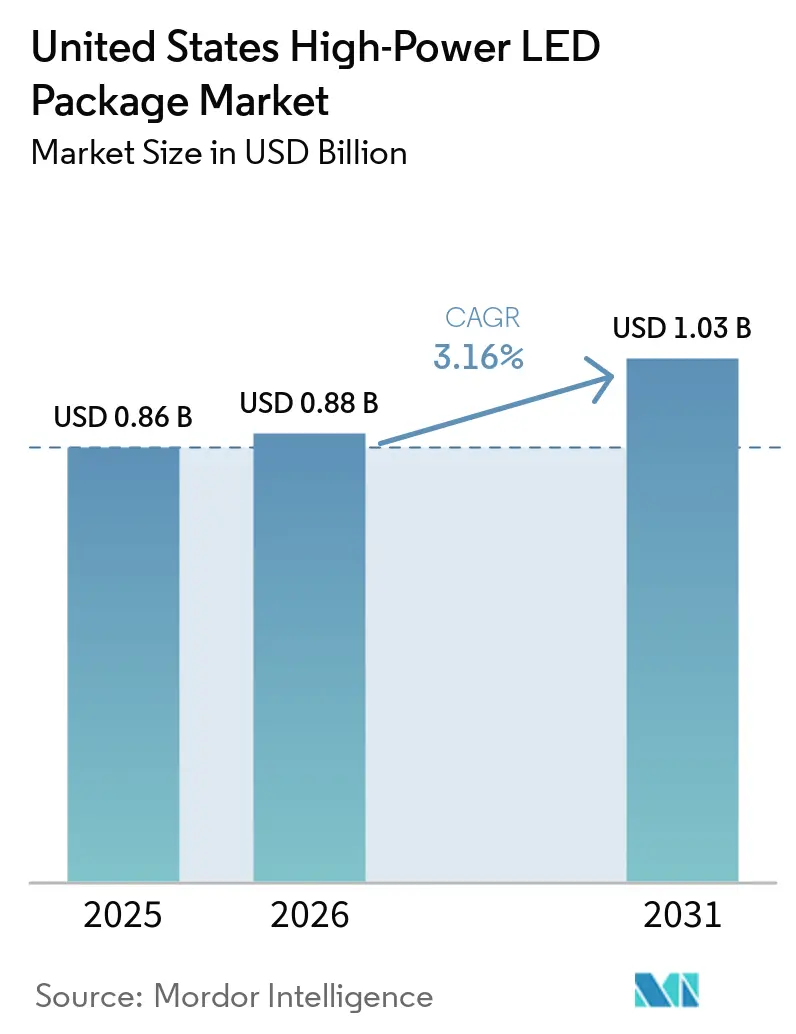

| Base Year Market Size (2025) | USD 0.86 Billion |

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.03 Billion |

| Growth Rate (2026 - 2031) | 3.16% CAGR |

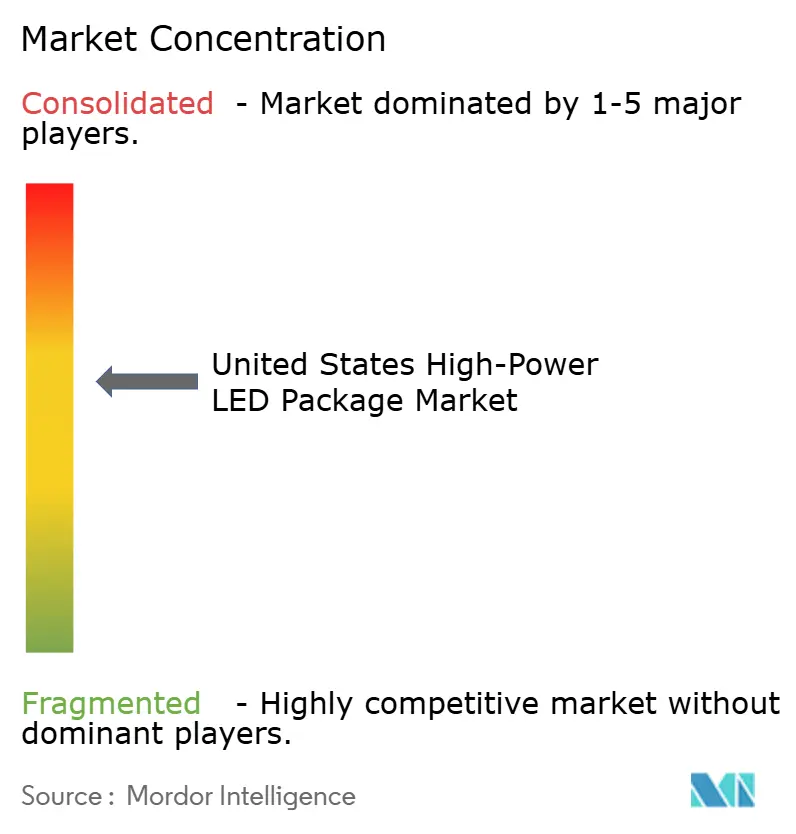

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States High-Power LED Package Market Analysis by Mordor Intelligence

The United States high-power LED package market size is expected to increase from USD 0.86 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.03 billion by 2031, growing at a CAGR of 3.16% over 2026-2031. General-lighting retrofits still anchor unit volumes, yet shipments are tilting toward horticulture grow-lights and automotive adaptive-beam modules as these segments accept premium pricing for flux density and thermal headroom. A first-half 2026 pull-forward occurred when Section 179D deductions were scheduled to lapse, front-loading demand for 3 W-10 W packages in commercial buildings. At the same time, federal and state energy-efficiency codes, combined with fast OLED penetration in televisions, have shifted supplier priorities from legacy LCD backlighting toward applications that value reliability at elevated junction temperatures. Competitive behavior is intensifying: vertical integration into substrates and epitaxy is rising, intellectual-property disputes are escalating, and consolidation, highlighted by San’an Optoelectronics’ pending takeover of Lumileds, signals looming price pressure in premium automotive tiers.

Key Report Takeaways

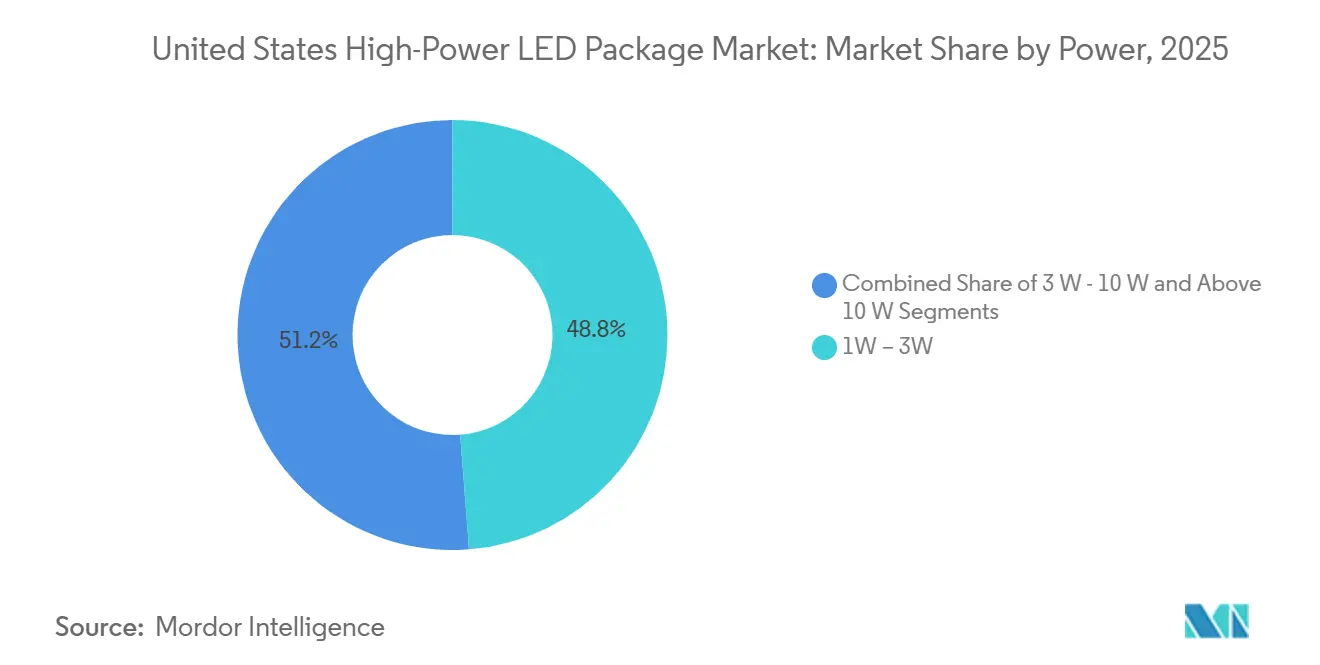

- By power range, the 1 W-3 W tier led with 48.77% of the United States high-power LED package market share in 2025, while packages above 10 W are projected to expand at a 3.58% CAGR through 2031.

- By architecture, single-die formats accounted for 37.62% share of the United States high-power LED package market size in 2025, whereas chip-on-board designs are advancing at a 3.91% CAGR to 2031.

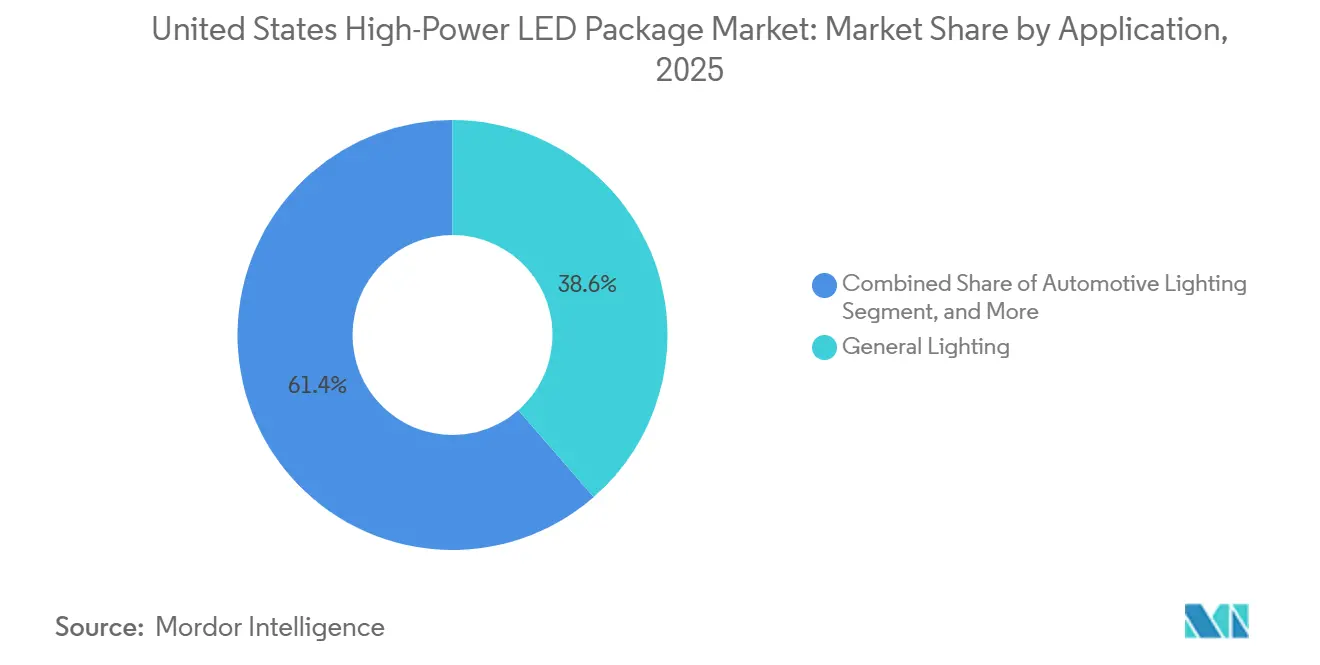

- By application, general lighting held 38.58% of the United States high-power LED package market size in 2025 and automotive lighting is growing at a 3.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States High-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Miniaturized High-Power LED Adoption For Horticulture Lighting | +0.6% | United States, Especially California, Arizona, Texas | Medium Term (2–4 Years) |

| Energy-Efficiency Mandates Driving Retrofit Demand In Commercial Buildings | +0.8% | Nationwide, Strongest In California And New York | Short Term (≤ 2 Years) |

| Declining Cost Of High Thermal Conductivity Substrates | +0.5% | Domestic Assemblers Sourcing AlN And Si₃N₄ | Long Term (≥ 4 Years) |

| Advances In Flip-Chip Architecture Enabling Higher Lumen Density | +0.7% | Automotive And Premium Lighting OEMs | Medium Term (2–4 Years) |

| Automotive Adaptive Headlamp Regulations (FMVSS-108 Updates) | +0.4% | United States | Medium Term (2–4 Years) |

| Integration Of Smart Controls With High-Power LED Modules In Street Lighting | +0.3% | Municipal Deployments | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Surge In Miniaturized High-Power LED Adoption For Horticulture Lighting

In controlled‑environment agriculture, the shift toward compact LED packages with wall‑plug efficiencies above 80% is reshaping vertical farming economics. These advanced packages deliver photosynthetic photon flux densities exceeding 2,000 µmol m⁻² s⁻¹, while second‑generation emitters now achieve an impressive 4.1 µmol J⁻¹. As a result, growers can reduce the number of fixtures required, lower HVAC loads due to improved efficiency, and realize payback periods of less than 18 months, making high‑performance LEDs a cornerstone of sustainable indoor farming.[1]United States Department of Agriculture, “Report on Controlled-Environment Agriculture Investments,” usda.gov

Energy-Efficiency Mandates Driving Retrofit Demand In Commercial Buildings

The Department of Energy has set a minimum standard of 45 lumens per watt for general-service lamps. In California, Title 24's open-ADR rules, combined with widespread utility rebates, have successfully incentivized 78% of the state's population. These measures have led to a significant pivot towards networked luminaires. These advanced luminaires now commonly integrate 3 to 10-watt packages equipped with demand-response capabilities. This shift is enabling quicker recovery of initial costs, even with the impending June 2026 expiration of Section 179D deductions.[2]California Energy Commission, “Title 24, Part 6 Building Energy Efficiency Standards,” energy.ca.gov

Declining Cost Of High Thermal Conductivity Substrates

In 2025, the introduction of combustion-synthesis aluminum nitride powders revolutionized the industry by slashing substrate costs by as much as 50%. This significant reduction in costs enabled the unlocking of impressive thermal pathways, achieving thermal conductivities ranging between 150 to 180 W m⁻¹ K⁻¹. Such advancements are particularly beneficial for packages operating at power levels exceeding 10 W. Meanwhile, in a parallel development, gas-pressure-sintered silicon nitride has seen its thermal conductivities surge past the 90 W m⁻¹ K⁻¹ mark. This leap in performance has paved the way for broader adoption of silicon nitride in automotive modules. These modules are engineered to endure junction temperatures kept below 125 °C, all while maintaining a robust 15-year duty cycle.

Advances In Flip-Chip Architecture Enabling Higher Lumen Density

Eliminating wire bonds in LED packages delivers a substantial performance boost by reducing parasitic resistance, which in turn lowers junction temperatures by about 10 °C. This reduction in thermal stress translates into a 45% cut in power loss, making the architecture far more efficient and reliable under demanding conditions. Modern automotive headlamps have embraced this innovation, incorporating hundreds of individually addressable pixels within a single ceramic package that achieves thermal resistance below 2 K W⁻¹. By meeting the stringent 1‑degree photometric transition requirement set by FMVSS‑108, these designs not only enhance safety but also set a new benchmark for precision and durability in advanced lighting systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal Management Challenges Above 10 W Limiting Reliability | -0.4% | Automotive And Industrial High-Bay Segments | Long Term (≥ 4 Years) |

| Patent Litigation Risk Around CSP And Flip-Chip Packages | -0.3% | U.S. District Courts And ITC | Short Term (≤ 2 Years) |

| Volatility In Gallium Nitride Wafer Pricing | -0.2% | Epitaxy Supply Chains | Medium Term (2–4 Years) |

| Slowdown In LCD Backlight Replacement Cycle Due To OLED Penetration | -0.2% | Consumer Electronics | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Thermal Management Challenges Above 10 W Limiting Reliability

Packages that cross the 10‑watt threshold face significant thermal management challenges, as heat dissipation becomes non-linear without advanced substrates like aluminum nitride (AlN) or silicon nitride (Si₃N₄). When these substrates are absent, the elevated junction temperatures can cause luminous efficacy to decline by roughly 5% for every 10 °C increase, which directly undermines performance in demanding applications. This thermal stress also compromises long-term reliability, with LM‑80 testing often failing to project the desired 50,000‑hour L90 lifetime, making substrate choice a critical determinant of both efficiency and durability.[3]Illuminating Engineering Society, “LM-80 and TM-21 Technical Memorandum,” ies.org

Patent Litigation Risk Around CSP And Flip-Chip Packages

Everlight’s February 2026 lawsuits against Seoul Semiconductor and Lumileds highlight the growing legal risks in the high‑power LED sector. The potential for import‑exclusion orders from the U.S. International Trade Commission (ITC) raises the stakes, as such rulings could force manufacturers to redesign packages and alter supply chains. These outcomes would not only inflate compliance budgets but also create temporary disruptions for OEMs, underscoring how litigation can ripple through both innovation cycles and market stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Above 10 W Packages Win Flux-Hungry Niches

Packages of 1 W-3 W retained 48.77% of the United States high-power LED package market share in 2025, anchored in downlights and troffers that value mature footprints and price competition. Growth, however, is shifting upward: the above 10 W band is on a 3.58% CAGR trajectory to 2031 as vertical farms and matrix headlamps demand superior photon density. The United States high-power LED package market size for the above 10 W class benefits from premium pricing that offsets the 40-60% material uplift tied to aluminum nitride substrates.

Controlled-environment cultivators in California and Arizona tolerate higher capex because a single-percentage-point jump in efficacy can shave USD 8,000-12,000 from annual energy bills. Automotive OEMs echo this dynamic, Tesla’s 2026 matrix system deploys dozens of high-flux dies to paint glare-free beams, a feature impossible with lower-wattage devices. Suppliers that can secure high-conductivity substrates and meet AEC-Q102 grades are therefore outpacing commodity package makers.

By Architecture: Chip-On-Board Captures Thermal And Optical Synergies

Single-die formats owned 37.62% of 2025 revenue, yet chip-on-board is forecast to register the quickest advance at 3.91% through 2031. The architecture trims junction-to-case resistance to below 2 K W⁻¹ and allows flip-chip die attachment, positioning it for high current density designs. Consequently, the United States high-power LED package market size tied to COB modules is growing even as price pressure compresses margins on legacy single-die products.

Automotive pixel arrays exemplify why: one ceramic COB can integrate hundreds of controllable pixels, satisfying FMVSS-108 glare limits while preserving slim headlamp styling. Industrial manufacturers chasing >160 lm W⁻¹ luminaires likewise favor COB because the tight die-to-heatsink coupling extends L90 life beyond 50,000 hours.

By Application: Automotive Lighting Accelerates On Regulatory Tailwinds

General lighting delivered 38.58% of revenue in 2025, but its expansion is slowing as rebate saturation and higher efficacy targets push upgrades into future product cycles. Automotive lighting, by contrast, is advancing at a 3.88% CAGR, lifting its slice of the United States high-power LED package market. Adaptive driving beams, newly legal under updated FMVSS-108, are being rolled out across multiple 2026 model years, locking in demand for AEC-qualified high-flux packages.

Display backlighting softened as OLED television share hit 25% domestically, yet mini-LED dashboards and infotainment screens provide a partial offset. Specialty verticals, UV-C, architectural accents and horticulture, remain comparatively small, though their double-digit volume growth underscores the market’s pivot toward quality-driven niches.

Geography Analysis

California, New York and Texas together generate roughly 40-45% of retrofit activity, propelled by stringent energy codes and robust utility incentives. Title 24’s demand-response stipulation in California and New York’s aggressive watt-per-square-foot caps have essentially retired metal-halide fixtures from warehouses and parking structures. These rules direct buyers toward networked luminaires that house 3 W-10 W packages with open-ADR or 0-10 V dimming interfaces.

Municipal street-lighting conversions illustrate a parallel trend. Memphis achieved a 55% energy cut after installing 77,000 smart fixtures in 2024, while Washington, D.C. contracted a USD 309 million program for 75,000 luminaires in 2025, bundling adaptive dimming and fault diagnostics. More than 400 U.S. cities had adopted networked LED street lights by early 2026, standardizing demand for packages that meet DesignLights Consortium photometric files and 10-year warranty thresholds.

Horticulture deployments cluster in California’s Central Valley, Arizona’s Yuma basin and Texas’s Rio Grande Valley, where drought risk and year-round economics justify premium LED systems. Cannabis facilities in California now specify >3.5 µmol J⁻¹ emitters to push gram-per-watt yield beyond 1.5, absorbing high-flux packages priced at USD 15-20 each. These regional hot-spots collectively strengthen the nationwide shift toward performance-driven, high-power devices.

Competitive Landscape

The United States high-power LED package market is moderately concentrated; the five largest vendors hold an estimated 55-60% revenue share. San’an Optoelectronics’ USD 239 million bid for Lumileds would grant the Chinese giant indirect 74.5% ownership, integrating European and North American supply chains and likely sharpening price rivalry in premium automotive classes.

Vertical integration is a common defense: Nichia opened an Automotive Innovation Center in Germany in 2024 to fast-track pixelated sources, while Cree LED locked a long-term domestic manufacturing deal in 2026 to mitigate tariff exposure. At the same time, Everlight’s February 2026 infringement suits underscore rising patent monetization, which can slice 2-4 percentage points from gross margin when cross-licensing is required.

Disruptors adopt fabless strategies and advanced packaging to sidestep capex. Bridgelux, for example, introduced high-CRI platforms up to 160 lm W⁻¹ in March 2026, leveraging global foundries yet courting U.S. customers that prize Buy America compliance. Success in the United States high-power LED package market therefore hinges on substrate control, litigation resilience and the ability to tailor modules to stricter thermal envelopes.

United States High-Power LED Package Industry Leaders

Nichia Corporation

Cree LED (SGH)

Lumileds Holding B.V.

Osram Opto Semiconductors GmbH

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bridgelux rolled out Thrive, F90 and RGBW high-power families, expanding into IP20-IP68 packages that push 160 lm W⁻¹ while meeting DesignLights Consortium criteria.

- February 2026: Everlight Electronics sued Seoul Semiconductor and Lumileds over flip-chip patents, casting uncertainty over WICOP HF supply.

- February 2026: Cree LED finalized a long-term U.S. manufacturing pact covering area, street and canopy lighting fixtures.

- August 2025: San’an Optoelectronics agreed to acquire Lumileds for USD 239 million, targeting closure in Q1 2026.

United States High-Power LED Package Market Report Scope

The United States High-Power LED Package Market Report is Segmented by Power Range (1 W to 3 W, 3 W to 10 W, Above 10 W), Architecture (Single-die Packages, Multi-die Packages, COB, Others), and Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty). The Market Forecasts are Provided in Terms of Value (USD).

| 1 W - 3 W |

| 3 W - 10 W |

| Above 10 W |

| Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) |

| COB (Chip-on-Board) |

| Others (CSP, Flip-Chip, Hybrid Modules) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| By Power Range | 1 W - 3 W |

| 3 W - 10 W | |

| Above 10 W | |

| By Architecture | Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) | |

| COB (Chip-on-Board) | |

| Others (CSP, Flip-Chip, Hybrid Modules) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Specialty / Niche |

Key Questions Answered in the Report

How fast is demand growing for high-power LED packages above 10 W in the United States?

Packages above 10 W are forecast to expand at a 3.58% CAGR through 2031 as horticulture and automotive headlamps prioritize higher flux density.

Which architecture is advancing quickest in U.S. high-power LED packaging?

Chip-on-board designs are growing at 3.91% CAGR, outpacing single-die formats because they lower thermal resistance and enable flip-chip attachment.

Why are automotive adaptive driving beams boosting LED demand?

Revised FMVSS-108 rules approved adaptive driving beams, prompting OEM rollouts that require hundreds of individually addressable high-power pixels per vehicle headlamp.

What regions lead U.S. commercial retrofit activity?

California, New York and Texas generate roughly 40-45% of commercial LED retrofits owing to stringent energy codes and robust utility incentives.

How does substrate innovation influence LED package reliability?

Cheaper aluminum nitride and silicon nitride substrates now offer ≥150 W m⁻¹ K⁻¹ thermal conductivity, keeping junction temperatures below 125 °C and extending L90 life beyond 50,000 hours.

What is driving litigation risk in the LED package space?

Patent holders are asserting chip-scale and flip-chip intellectual property, with recent suits targeting architectures such as WICOP HF, which may lead to import bans or licensing costs.

Page last updated on: